Abstract

In this study, we examined (1) the effect of changes in outstanding student debt on trajectories of subjective financial well-being (SFWB) over time and (2) how these trajectories vary according to family socioeconomic and emerging adult financial factors. We used three waves of longitudinal data from the Arizona Pathways to Life Success for University Students (APLUS) study and used growth curve models to analyze the data. Net of family socioeconomic and emerging adult financial factors, student debt was significantly and negatively associated with SFWB across the emerging adult period. Trajectories of SFWB varied slightly in relation to changes in student debt. Between-person differences in debt mattered more for trajectories of SFWB relative to within-person changes in debt over time. Family socioeconomic factors had a strong influence on SFWB trajectories. Findings illustrate how student debt may suppress postsecondary education’s impact as an inequality reducing mechanism. They also suggest the need for both individual- and policy-level intervention.

Keywords

The events that unfold as emerging adults complete postsecondary education and transition to independence are part of the foundation on which later social inequalities are built. During this life stage, individuals assume increasing economic responsibility and rely less on institutional and family supports because of need, preference, or social pressures. Emerging adults’ well-being is determined, in part, by the degree to which there is a match between the resources that they have access to and the challenges to which they are exposed (Wood et al., 2018). Financial debt plays a large role in this process. Debt may be a resource that smooths consumption, facilitates investment in human capital, and increases well-being (Modigliani, 1966; Rothstein & Rouse, 2011). Debt may also exert economic pressure that increases financial instability and stress and diminishes well-being (Drentea, 2000; Elliott & Nam, 2013). Further, the effects of debt may be offset or exacerbated by other aspects of individuals’ background and concurrent life circumstances.

The goals of this study are to examine the relationship between changes in levels of outstanding student debt and trajectories of subjective financial well-being (SFWB) of emerging adults over time and to examine variation in these trajectories according to family-of-origin socioeconomic and emerging adult financial factors. SFWB is important because an individual’s perception of their financial condition is likely to influence their decision-making around financial and other life-course milestones and their overall sense of well-being (Netemeyer, Warmath, Fernandes, & Lynch, 2018). Student loans are often the first and most significant financial responsibility that emerging adults assume. Understanding changes in the impact of student debt over time is important because this impact varies relative to how much student debt one holds, whether one is in the borrowing or repayment period, and other financial commitments in one’s life. Findings inform the timing and targeting of public policies and practice interventions that address burdens associated with holding and repaying student debt.

Student Debt in the United States

In the United States, holding student debt is a pervasive feature of emerging adults’ financial lives. In the past three decades, there has been a significant increase in the overall number of student debtors, total outstanding student loans, and average size of these loans. Four in ten individuals under the age of 30 have outstanding student loan debt (Baum, Ma, Pender, & Welch, 2016). Total borrowing for postsecondary education rose from US$46.5 billion in 1997 to US$106.5 billion in 2017, and the median debt of recent graduates more than doubled from US$12,434 in 1993 to US$26,885 in 2012 (Fry, 2014). Default rates suggest that emerging adults struggle to manage their outstanding student debt. In 2018, more than 10% of borrowers were more than 90 days delinquent or in default (Federal Reserve Bank of New York, 2018). Comparable international data from household economic surveys suggest that median student debt amounts in the United States (US$20,000) are almost double that of Canada, the UK, and Australia (US$9,448, US$10,846, and US$10,217, respectively (Luxembourg Wealth Study, 2019). 1

Student Debt and Trajectories of SFWB

Subjective well-being captures individuals’ cognitive and affective evaluations of their own life (Deiner, Lucas, & Oishi, 2002) and is important because it provides a universal measure of the quality of human experience (Layard, 2011). Subjective well-being is conceptualized as an amalgam of constructs spanning life domains (e.g., relationships, career, and health; van Praag, Frijters, & Ferrer-i-Carbonell, 2003). In this study, we focus on the financial domain. SFWB consists of an individual’s perceptions and evaluations of their own financial condition (Sorgente & Lanz, 2017). SFWB is important to human development because of its positive association with overall subjective well-being and with mental and physical health (Shim, Xiao, Barber, & Lyons, 2009; Tay, Batz, Parrigon, & Kuykendall, 2017).

Subjective well-being may be unstable during certain developmental periods, and instability may depend on personal and contextual circumstances (Headey & Muffels, 2017; Lucas & Donnellan, 2007). Brüggen, Hogreve, Holmlund, Kabadayi, and Löfgren (2017) explain that SFWB is inherently dynamic because of its relationship to changing financial resources and needs over the life course. Plagnol (2011) found that declines in debt between one’s mid-30s and mid-70s were associated with increased financial satisfaction over time. 2 However, how trajectories of SFWB unfold during emerging adulthood, and specifically in relation to changes in student debt, are not well understood.

There is limited research on the relationship between student debt and SFWB. In a review of related literature, Nissen, Hayward, and McManus (2019) found that most studies identified deleterious effects of student debt on economic, physical, and mental well-being. Walsemann, Gee, and Gentile (2015) found that student loans were significantly associated with poorer psychological functioning among college students. Outstanding student debt was also associated with weaker financial health and lower net worth (Elliott & Nam, 2013; Fry, 2014), lower retirement savings (Elliott, Grinstein-Weiss, & Nam, 2013), and lower likelihood of purchasing a home (Gicheva & Thompson, 2015).

The impact of student debt on emerging adult well-being may not be negative across the entire developmental period or for all borrowers (Dwyer, Hodson, & McCloud, 2013). Student debt may be perceived as a resource because it provides access to the social and economic premium associated with degree attainment in the United States (Carneiro, Heckman, & Vytlacil, 2010) and therefore may positively impact SFWB in the long run. However, whether this positive impact is present during the emerging adult period—while individuals are still holding or repaying their student debt—is unclear.

Family Background and Concurrent Factors

The impact of student debt on SFWB is likely shaped, in part, by other aspects of emerging adults’ lives, including, but not limited to, family of origin and personal financial resources. Studies show that emerging adults from socioeconomically disadvantaged backgrounds are more likely than their more advantaged counterparts to take on student debt and accrue excessively high levels of debt (Fry, 2014; Houle, 2014), to report feeling burdened by their student debt (Robb, 2017), and to experience its detrimental impact on psychological functioning (Walsemann, Gee, & Gentile, 2015). Further, declining household wealth across the income distribution as a result of the Great Recession of 2008 has made it increasingly difficult for many emerging adults to rely on family financial support (Fry, 2014). Regarding personal financial resources in emerging adulthood, evidence suggests that low- and moderate-income earners with student debt are more likely to experience financial hardship than their counterparts without student debt (Despard et al., 2016). And, emerging adults who receive financial support from family and have lower debt-to-income ratios have an easier time repaying, and thus coping with, their outstanding debt (Baum & Schwartz, 2006; Schoeni & Ross, 2005). Overall, taking on student debt is likely to generate or at least exacerbate inequalities between those with and without personal and family resources. To our knowledge, this study is one of the only to examine disparities in the impact of student debt on emerging adult SFWB in relation to family socioeconomic and emerging adult financial factors.

Other noneconomic individual-level factors—including race and mental health—may also shape the relationship between debt and SFWB. Black young adults are more likely than Whites to hold debt and have higher debt (Houle & Addo, 2018), to worry about the affordability of student loan repayments (Ratcliffe & McKernan, 2013), and to default on their student loans after college (Huelsman, 2015). Further, as mentioned, previous research shows a clear negative association between student debt and mental health (Sweet, Nandi, Adam, & McDade, 2013; Walsemann et al., 2015). While we include these factors in our analysis, our central focus is on how family socioeconomic and emerging adult financial factors shape the relationship between student debt and SFWB.

Study Purpose and Research Questions

Prior evidence suggests that student debt has negative impacts on well-being, that this impact may be more acute for borrowers from socioeconomically disadvantaged backgrounds, and that the relationship between student debt and well-being is likely to change over time and across people in relation to personal and contextual factors. However, little is known about how changes in student debt across the emerging adult years relate to changes in SFWB or how this relationship varies according to background socioeconomic and concurrent financial circumstances. Our study aims to address these limitations by asking: What is the effect of changes in outstanding student debt on trajectories of SFWB over time? How do these trajectories vary according to family socioeconomic and emerging adult financial factors?

We hypothesize that there is a negative impact of student debt on the SFWB of young adults and that the magnitude of this impact increases just prior to or during repayment. Further, we hypothesize that the impact of student debt on SFWB depends on the size of the debt and other financial and nonfinancial dimensions of emerging adults’ lives.

Most studies on the relationship between debt- and SFWB-related constructs use cross-sectional data, focus only on students while in college (Archuleta, Dale, & Spann, 2013; Solis & Ferguson, 2017), or include samples that span a wide age range (Robb, 2017). In this article, we examine the effect of changes in outstanding student debt on trajectories of SFWB over time. Examining trajectories—rather than point-in-time estimates—from entry to college through the early career period allows us to describe within-individual change in the relationship between debt and SFWB over time. Further, we examine how these trajectories vary according to family socioeconomic, emerging adult financial, and personal factors that the literature identifies as having an influence on student debt accumulation and impacts. Examining interindividual differences in these trajectories illuminates how the impact of debt may be shaped both by intergenerational and concurrent socioeconomic and financial inequities. Together, findings on changes within emerging adults over time, and across subgroups of emerging adults, can help inform the timing and targeting of policy, programmatic and practice interventions that ease the burden of, and help emerging adults cope with, outstanding student debt.

Method

Data

We used data from the APLUS study, a longitudinal survey of emerging adults who attended a large public university in the southwest United States. 3 We used data from three waves: when students were aged 18–21, 21–24, and 23–26. We limited our sample to respondents who had supplied complete data pertaining to student debt and SFWB (n = 903) and restructured the data into a person-wave format 4 (2,709 person-waves). 5 At Wave 1, all respondents were full-time, first-year students. At Wave 2, the majority of respondents were still enrolled in an undergraduate degree program (n = 881). At Wave 3, the majority had graduated from their undergraduate program (n = 812) and were working full-time (n = 479), part-time (n = 208), or were self-employed (n = 21) and/or in graduate school (n = 147). 6

We replaced missing values on covariates with the sample mean (for continuous variables) or zero (the reference category for categorical variables). We conducted bivariate tests to assess differences in the characteristics of our analytic sample and respondents excluded due to missing data. We found no significant differences in baseline SFWB or student debt and only slight differences at other time points. 7

Measures

SFWB

We measured SFWB using three statements with responses ranging on a scale from 1 = strongly disagree to 5 = strongly agree. The items were “I am satisfied with my current financial status,” “I have difficulty paying for things,” and “I am constantly worried about money.” In empirical analyses, we used the summary score of the 3 items and reversed negatively worded items so that a higher summary score represented more positive SFWB. Previous research reported acceptable reliability with a coefficient α of .84 (Serido, Shim, & Tang, 2013).

Student debt

We used measures of outstanding undergraduate student debt at Waves 1 and 2, and a combination of outstanding undergraduate and graduate student debt at Wave 3. To remove outliers, we applied a 99th percentile top code to the reported debt amount and adjusted values for inflation across years (represented in 2016 dollars). In our empirical models, we used the natural log of debt that truncates values from a positively skewed distribution, pulling them closer to the mean and creating a normal distribution (Friedline, Masa, & Chowa, 2015). We added a value of one to the raw debt amount as it is not possible to take the log of zero. 8

Family socioeconomic factors

Three variables were used to operationalize family socioeconomic factors: parental income, parental education, and childhood financial situation. Parental income was measured categorically: less than US$50,000 [referent], US$50,000–$99,000, US$100,000–$200,000, and over US$200,000. Parental education included high school or less [referent], some college, and bachelor’s degree or more. The measure of childhood financial situation was derived from three questions that asked about participants’ perception of their financial situation in childhood. 9 Negatively worded items were reversed so that a higher score represented more positive perception of financial situation in childhood. In empirical analyses, we divided respondents into three quantiles to create low, medium, and high childhood financial situation.

Emerging adult financial factors

We included measures of respondents’ income and financial independence from parents at each wave. In Waves 1 and 2, the survey asked about monthly income earned as a student. In Wave 3, the survey asked about annual employment income. We first regrouped the student income categories into low (<US$500) and high (>US$500), and the employment income into low (<US$25,000) and high (>US$25,000). We then created a time-invariant variable by regrouping into the following categories: always low, always high, and varies across waves. In the survey, financial independence was measured using the item: “I am financially independent from my parents (i.e., parents do not claim you on their tax return).” We created a time-invariant variable for financial independence by regrouping into the following categories: financially dependent at all waves, financially independent at all waves, and varies across waves. 10

Personal factors

We included measures of gender, race/ethnicity, and depressed mood. Gender was comprised of male [referent] and female. Because of documented large racial inequities in student debt loads and impacts, especially for Black students (Houle & Addo, 2018), we included an indicator of race/ethnicity as White [referent], Black, and other. Four items measuring depressed mood were included in the survey and measured at each wave. 11 We used the average of each person’s score on the 4 items at each wave.

Empirical Strategy

A series of growth curve models (GCM; Singer & Willett, 2003) were estimated to understand emerging adults’ initial SFWB at Wave 1 (intercepts) and changes in their SFWB over time (slopes) as a function of outstanding student debt, and personal, family socioeconomic, and emerging adult financial factors. The composite growth model took the following equation:

13

Groups of covariates were added sequentially in order to reveal changes in the coefficient for debt. 13 To better understand the role of debt, we parsed student debt into its between and within effects, creating a “hybrid model” (Allison, 2009). The between-person coefficient represented the effect of overall mean debt for each participant, while the within-person coefficient represented the effect of the deviation from each person’s mean debt. StataIC (Version 15) was used for all analyses.

Results

Descriptive Results

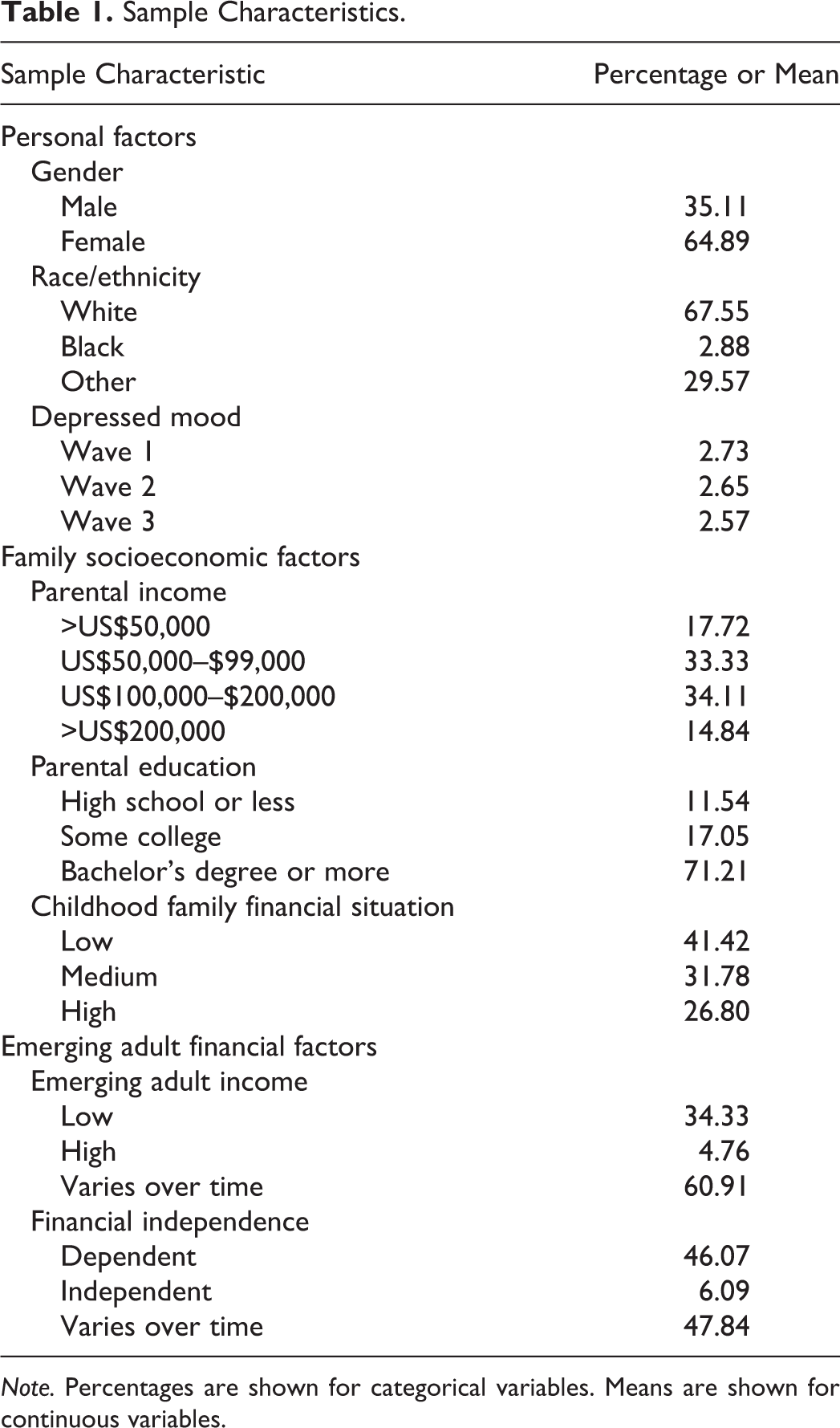

Table 1 provides sample characteristics. Respondents were majority female (64.89%) and White (67.55%). Mean depressed mood scores declined slightly across waves from 2.73 to 2.57. Most participants’ parents were in the middle of the income distribution (a combined 67.44% were in the middle two categories) and had a bachelor’s degree or more (71.21%), yet the largest share of respondents identified their families as falling in the low financial situation category (41.42% were low, 31.78% were medium, and 26.80 were high). Finally, most respondents’ incomes were either consistently low (34.33%) or varied across time (60.91%), and most were either financially independent at all waves (46.07%) or at least one wave (47.84%).

Sample Characteristics.

Note. Percentages are shown for categorical variables. Means are shown for continuous variables.

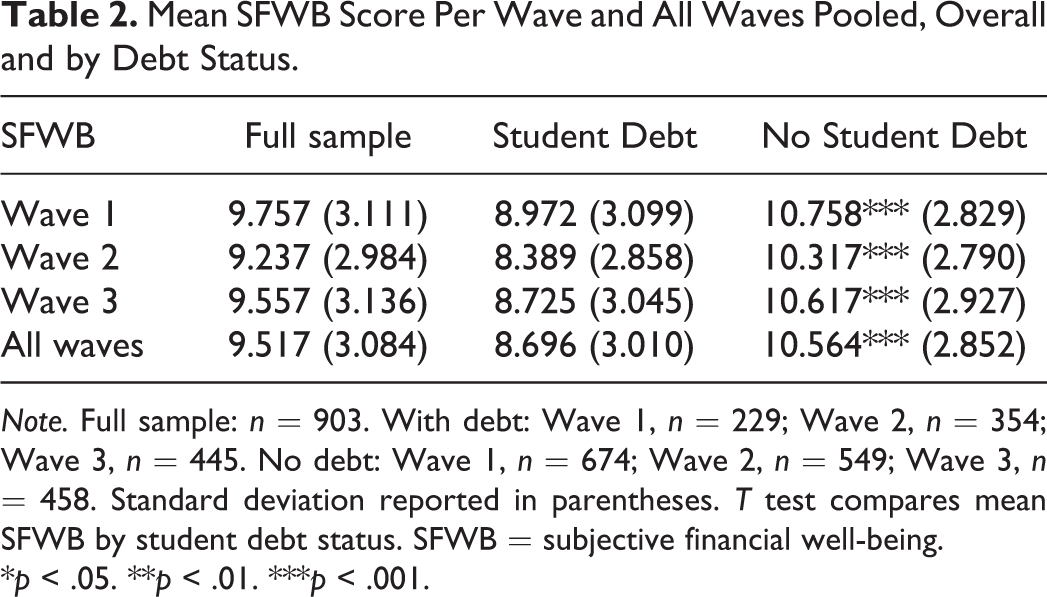

Mean SFWB was higher overall and at each wave for nondebt holders as compared to debt holders (p < .001; see Table 2). Mean outstanding student debt nearly quintupled from US$7,268 in Wave 1 to US$34,128 in Wave 3 (see Table 3).

Mean SFWB Score Per Wave and All Waves Pooled, Overall and by Debt Status.

Note. Full sample: n = 903. With debt: Wave 1, n = 229; Wave 2, n = 354; Wave 3, n = 445. No debt: Wave 1, n = 674; Wave 2, n = 549; Wave 3, n = 458. Standard deviation reported in parentheses. T test compares mean SFWB by student debt status. SFWB = subjective financial well-being.

*p < .05. **p < .01. ***p < .001.

Mean Student Debt Levels Per Wave and All Waves Pooled.

Note. Standard deviations reported in parentheses. Includes only student debtors at each wave. “All waves” include all individuals who had student debt at least one wave. Student debt displayed in 2016 dollars.

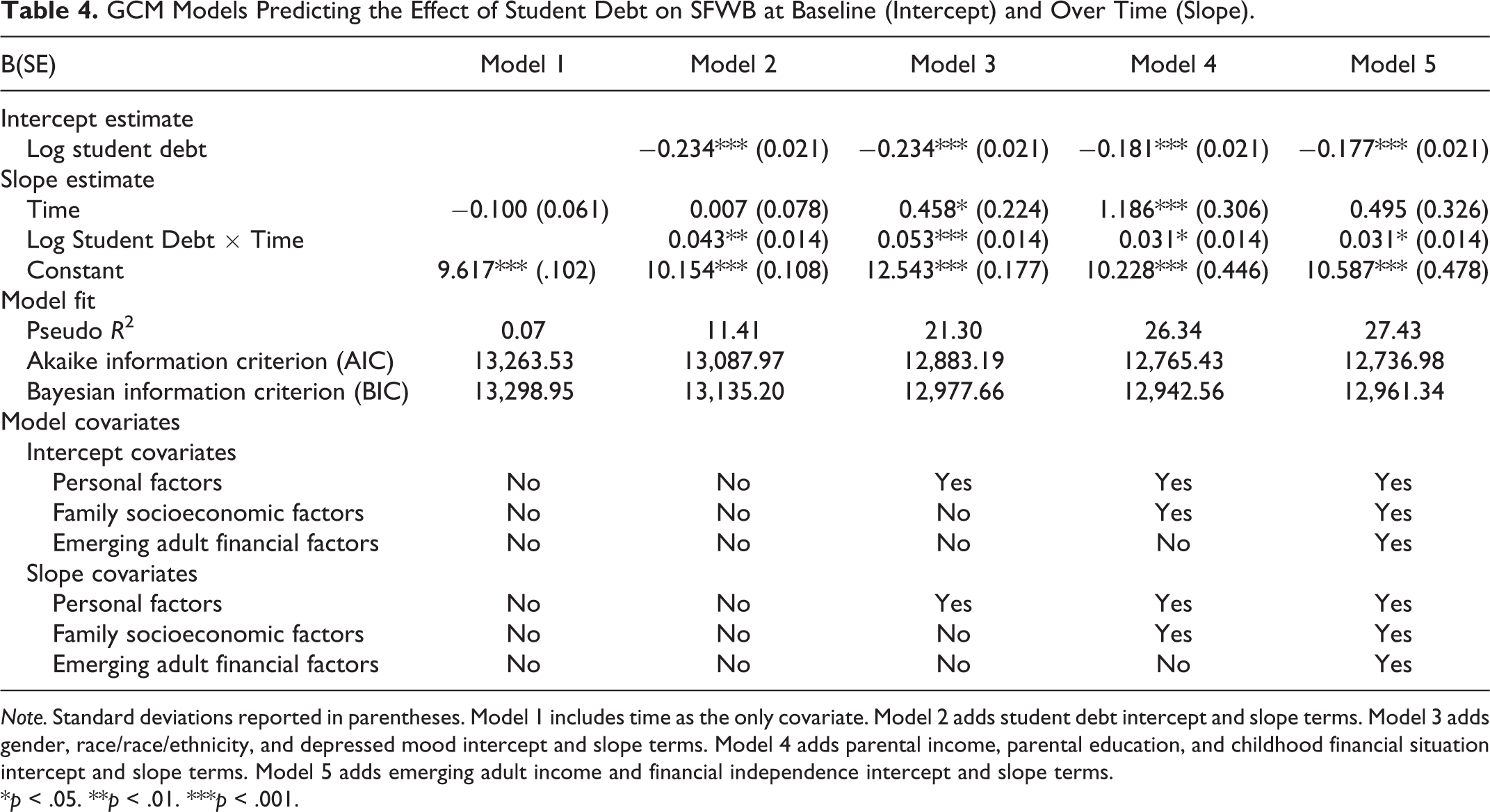

GCM Results

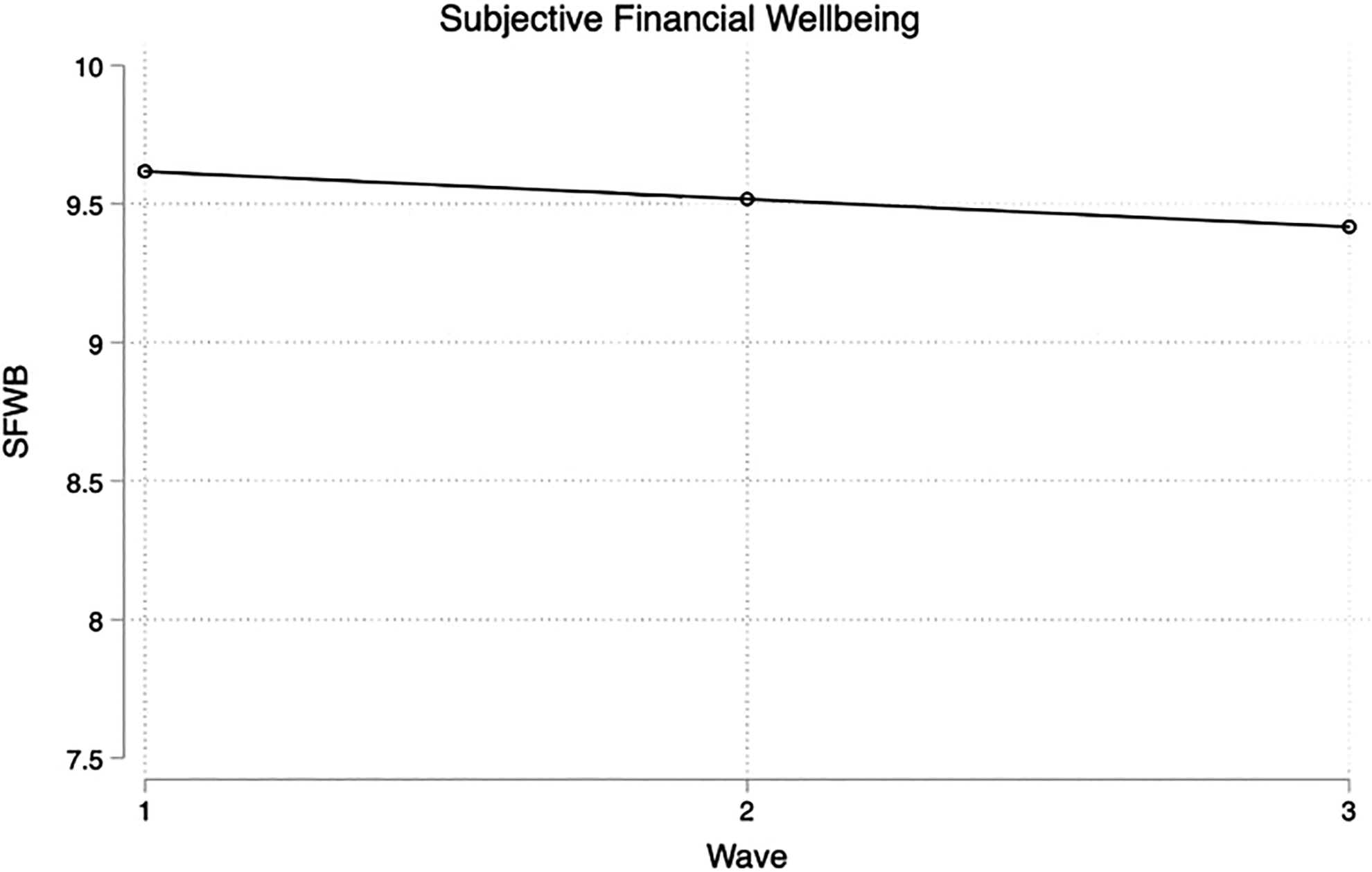

The mean uncontrolled SFWB trajectory over time was modestly negative (b = −.100, p > .05; see Model 1 of Table 4 and Figure 1).

GCM Models Predicting the Effect of Student Debt on SFWB at Baseline (Intercept) and Over Time (Slope).

Note. Standard deviations reported in parentheses. Model 1 includes time as the only covariate. Model 2 adds student debt intercept and slope terms. Model 3 adds gender, race/race/ethnicity, and depressed mood intercept and slope terms. Model 4 adds parental income, parental education, and childhood financial situation intercept and slope terms. Model 5 adds emerging adult income and financial independence intercept and slope terms.

*p < .05. **p < .01. ***p < .001.

Mean uncontrolled subjective financial well-being trajectory across waves. Based on estimates from Table 4, Model 1.

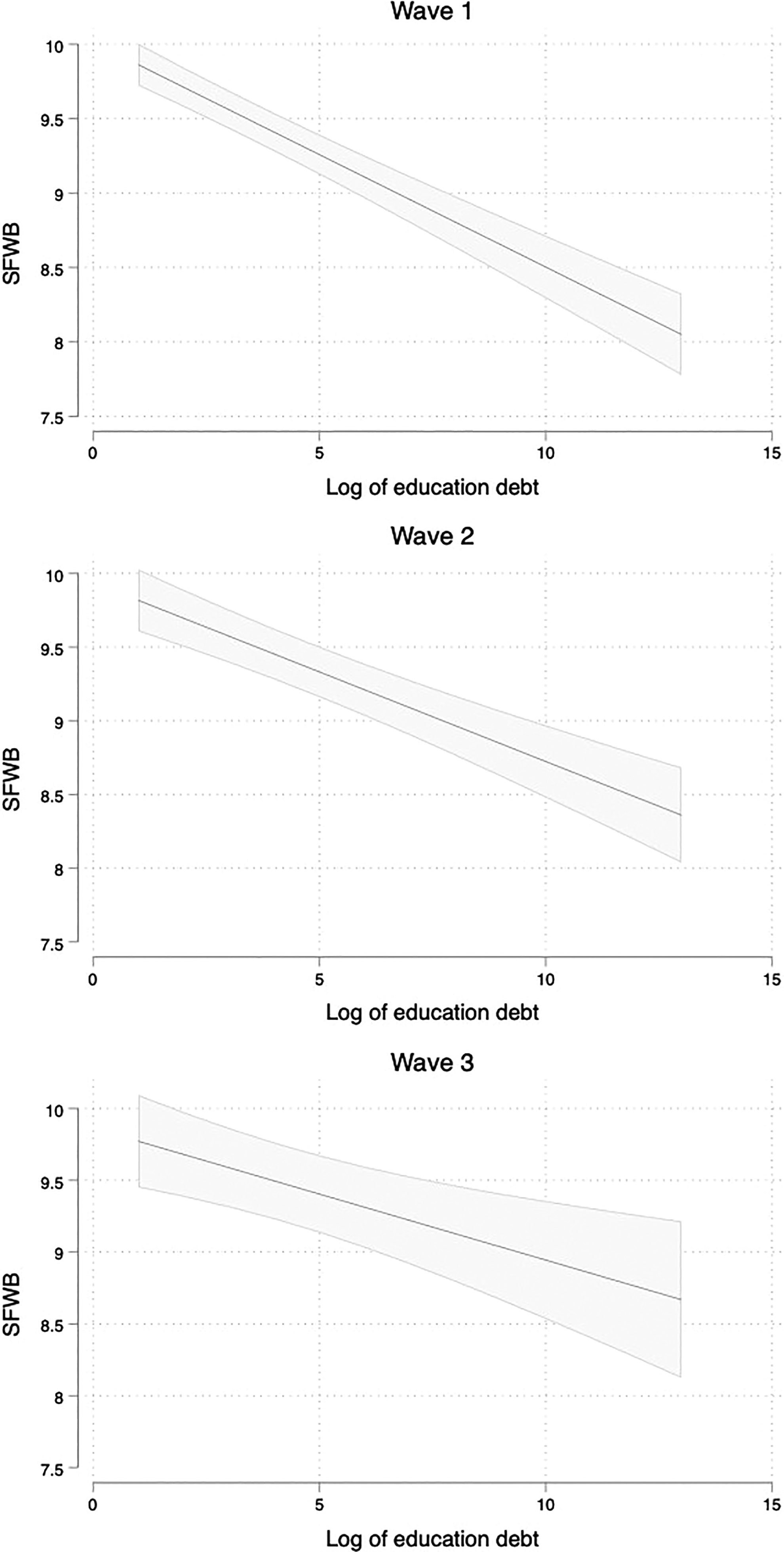

Moving to adjusted models, a significant negative association between initial level of debt and initial SFWB was observed in Model 2 of the GCMs (b = −.234, p < .001; see Table 4), along with a positive association between changes in debt and changes in SFWB over time (b = .043, p < .01). Higher levels of debt were consistently associated with lower SFWB, regardless of change in debt from the previous period of observation (see Figure 2).

Predicted subjective financial well-being scores based on debt, controlling for other covariates, for each wave. Based on estimates from Table 4, Model 5. Shaded portions indicate 95% confidence intervals.

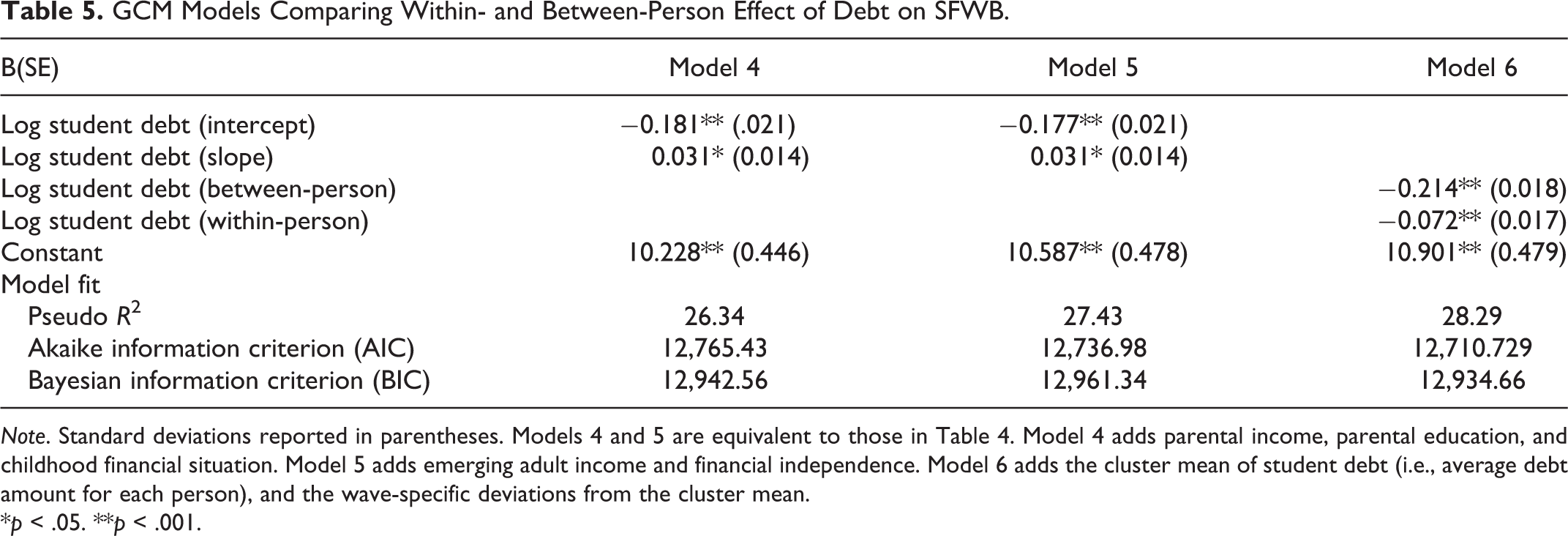

The addition of personal factors improved model fit but did little to alter the relationship between changes in debt and changes in SFWB (see minimal changes in coefficients between Models 2 3). A large reduction in the intercept coefficient for student debt was observed when family socioeconomic factors were added (Model 4). The slope coefficient for debt was only slightly statistically significant, indicating that family socioeconomic factors may account for much of the relationship between changing debt and changing SFWB. Model fit also improved considerably with the addition of these variables. Little change was observed when emerging adult financial factors were added (Model 5). In our hybrid model (see Table 5), we found that the between-person differences in average debt did more to explain SFWB trajectories than did the change in debt within-person over time.

GCM Models Comparing Within- and Between-Person Effect of Debt on SFWB.

Note. Standard deviations reported in parentheses. Models 4 and 5 are equivalent to those in Table 4. Model 4 adds parental income, parental education, and childhood financial situation. Model 5 adds emerging adult income and financial independence. Model 6 adds the cluster mean of student debt (i.e., average debt amount for each person), and the wave-specific deviations from the cluster mean.

*p < .05. **p < .001.

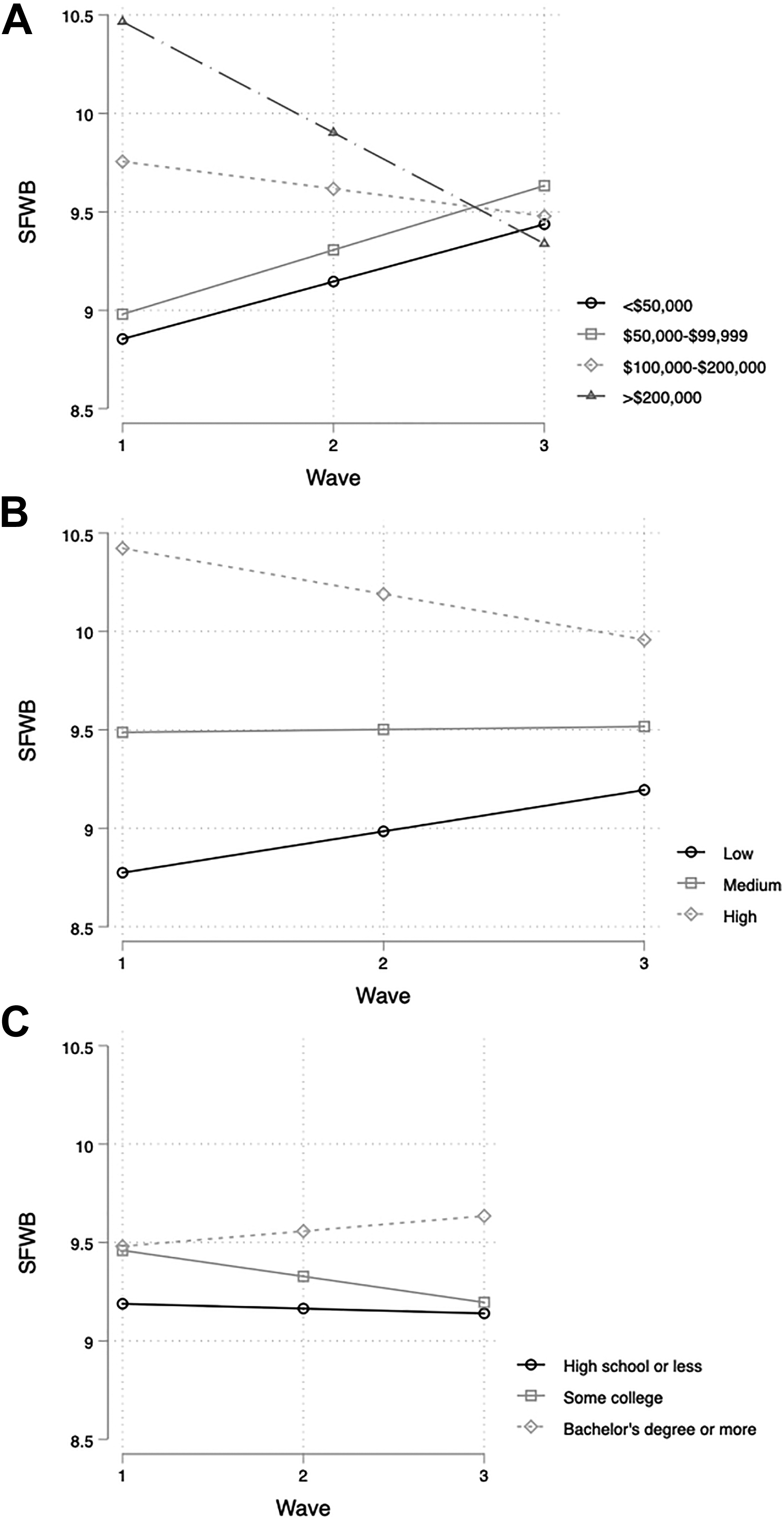

Figure 3 shows disaggregated family socioeconomic factors. Emerging adults from families with higher parental income had higher initial SFWB but experienced a steady decrease in SFWB across waves (see Figure 3A). In contrast, those with lower parental income experienced a steady increase in SFWB across waves. Figure 3B reflects similar findings with regard to differences across levels of childhood family financial situation. Figure 3C shows that emerging adults with higher educated parents experienced a slight increase in SFWB across waves, and those of less educated parents experienced either a slight decline (some college) or no change (high school or less). However, the coefficients for parental education were not significant.

Predicted mean subjective financial well-being trajectories over time by family socioeconomic factors. Based on estimates from Table 4, Model 4. (A) Parental income. (B) Childhood financial situation. (C) Parental education.

Discussion

By examining the relationship between changing debt and changing SFWB, our study provides new insights into financial instability in emerging adulthood. The main finding of this study is that student debt had a consistent negative impact on SFWB, regardless of timing. Specifically, student debt was significantly and negatively associated with emerging adults’ SFWB at first year of college, toward the end of college, and in the early years afterward. This finding is consistent with the broader literature on the impacts of debt, generally, and student debt specifically, on mental health and financial satisfaction (Archuleta et al., 2013; Walsemann et al., 2015).

While our growth curve modeling revealed a modest positive association between changes in student debt and changes in SFWB, it seems family socioeconomic factors play an important role. Changes in how families of origin shape later life SFWB is a key finding of this study. Specifically, disparities in SFWB according to parental income and childhood financial situation that exist during the first year of college trend toward convergence over time. This supports previous work that found a strong parental influence on emerging adults’ financial behaviors and attitudes at entry into college but that weakens over time as factors beyond the family take on more importance (Serido et al., 2015). For SFWB, it is plausible that, for emerging adults from more disadvantaged families, increased physical and temporal distance from family socioeconomic factors and building one’s own personal financial resources might increase one’s sense of financial well-being. The opposite mechanism may function for those from more advantaged families: socioeconomic status and personal resources are likely to decline as they distance themselves from their parents. Importantly, selection effects may explain this finding, as students from socioeconomically disadvantaged households who enroll and persist in college, compared to those who do not pursue higher education, may have unmeasured characteristics that contribute to higher SFWB (Walsemann et al., 2015).

The Great Recession was a unique macroeconomic phenomenon that likely impacted participants in powerful ways. Participants were first surveyed in 2008, just prior to the Great Recession, and then again in 2010 and 2013. The economic downturn limited future career options and earning potential of emerging adults (Bell, Blanchflower, & Blanchflower, 2010), increased deliberation about whether a college degree was “worth it” (Peralta, 2012), and heightened worry about the impacts of student debt for other aspects of emerging adults’ financial lives (Stone, Van Horn, & Zukin, 2012). Together, these factors likely had a unique and substantial effect within this study on individuals’ objective financial circumstances and may contribute to the downward trajectory of SFWB observed in some participants.

The persistent negative effect of student debt on emerging’ adults SFWB implies that significant changes are needed at multiple levels. At the policy level, reforms that address the rising cost of tuition, expand access to low-interest subsidized loans, increase availability of nonrepayable grants, and tighten regulation around loans limits are vital for structural change. At the individual level, increasing awareness of and access to alternative repayment plans (such as income-driven repayment) may help reduce stress for some borrowers. Further, policy makers, high school staff, and parents can help build knowledge and decision-making capacity among adolescents and emerging adults in the years before and during postsecondary education.

Our study raises key areas for future research. Prolonging the time frame of the current study would allow us to determine the extended trajectories of student debt and SFWB and might add variation in the impact of debt. This is important because default rates continue to grow a decade into repayment, indicating the borrowers continue to struggle with their debt long after leaving college (Brown, Haughwout, Lee, Scally, & Van Der Klaauw, 2015). Also, SFWB is important on its own and because of its relationship to other subjective and objective outcomes, both in emerging adulthood and throughout the life course. Further exploration of the underlying mechanisms linking debt and SFWB, and of the impact of SFWB on other aspects of emerging adult development, including career choice, home ownership, and family formation, is needed.

A limitation of our study is that the average decline in SFWB may indicate a period artifact rather than a reliable developmental pattern. Also, because study participants attended the same university, and were majority female and White, our findings should not be generalized to a wider population. Given evidence of racial disparities in both the use and impacts of student loans (Houle & Addo, 2018), additional research on this dimension is needed. Additionally, despite small rates of missingness, our imputation method may have resulted in slightly biased parameter estimates. Further, our measure of parental income was indirectly reported by participants rather than by parents, which entails some measurement error.

Overall, student debt is associated with lower SFWB across emerging adulthood in this sample. Practitioners working with emerging adults in the areas of financial and mental health and postsecondary education counseling must be aware of the impact of student debt on SFWB, that this impact may change over time and in relation to contextual factors in individuals’ lives, and of the potential spillover effects onto other life domains. Further, there is a pressing need for the detrimental impacts of student debt on well-being to be addressed at various levels of state and federal higher education policymaking.

Supplemental Material

Supplemental Material, Cherney.etal.2019.EmergingAdulthood.Appendix.Final - Subjective Financial Well-Being During Emerging Adulthood: The Role of Student Debt

Supplemental Material, Cherney.etal.2019.EmergingAdulthood.Appendix.Final for Subjective Financial Well-Being During Emerging Adulthood: The Role of Student Debt by Katrina Cherney, David Rothwell, Joyce Serido and Soyeon Shim in Emerging Adulthood

Footnotes

Authors’ Note

This research uses data from the Arizona Pathways to Life Success for University Students Project, directed by Joyce Serido at the University of Minnesota-Twin Cities and designed and founded by Soyeon Shim at the University of Wisconsin–Madison and Joyce Serido. Information on how to obtain access to the APLUS data files is available on the APLUS website (![]() ).

).

Acknowledgments

We thank Drs. Richard A. Settersten, Geneviève Gariépy, and Jill Hanley who provided insight and expertise that greatly improved this article.

Author Contributions

Katrina Cherney contributed to conception and design, analysis, and interpretation; drafted the article; critically revised the article; gave final approval; and agreed to be accountable for all aspects of work ensuring integrity and accuracy. David Rothwell contributed to conception and design, analysis, and interpretation; critically revised the article; gave final approval; and agreed to be accountable for all aspects of work ensuring integrity and accuracy. Joyce Serido and Soyeon Shim contributed to acquisition, critically revised the article, gave final approval, and agreed to be accountable for all aspects of work ensuring integrity and accuracy.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Funding support for the study was provided to Katrina Cherney and David Rothwell through the Arizona Pathways to Life Success for University Students Project research award from The University of Wisconsin–Madison. Katrina Cherney also received funding support from the Fonds de recherche du Québec. Data collection was funded by the National Endowment for Financial Education, Great Lakes Higher Education Corporation & Affiliates, and Citi Foundation.

Open Practices

The raw data contained in this article are not openly available due to privacy restrictions set forth by the institutional ethics board but can be obtained from the primary investigators of the APLUS study following completion of a privacy and fair use agreement. The analysis code used in this study is not openly available but is available upon request to the corresponding author. No aspects of the study were preregistered.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.