Abstract

Corporate social responsibility (CSR) is a buzzword worldwide. In today’s globalized world, one of the great challenges faced by firms is integration of CSR in business. Stakeholders require a lot more from companies than merely pursuing growth and profitability. They demand information about economic, social and environmental performances of the companies. Previous studies in developed countries have confirmed that a true and sincere corporate communication leads to the building of stakeholders’ trust. There is, however, a dearth of such studies in developing countries such as India. This study is an attempt to bridge the gap by conducting an exploratory study on how the top management of a company reports CSR. Using the technique of content analysis, this article assessed the extent and nature of CSR reporting by Indian companies. We used multiple regression analysis to evaluate how well a set of predictors explain the social disclosure practices of Indian firms. The results indicated that there is no significant relationship between a firm’s profitability and its corporate social disclosure (CSD). However, a firm’s ownership (private sector or public sector) has influence on CSD practices. The findings also suggest that firm size has a positive association with CSD under the community development theme. This implies that large companies with public visibility favour community development. Finally, the study ends with a conclusion that has strong managerial implications: sincere and honest social reporting can harness a better relationship with all stakeholders.

Introduction

Corporate Social Responsibility and Stakeholders

Organizations that consider the self-regulation process of corporate social responsibility (CSR) have to address the question ‘to whom are we responsible?’ The common answer to this question is ‘to stakeholders’, which indicates that identification of stakeholders is vital, in order to manage CSR (Mattingly, 2004; Steurer, 2006). Management of CSR has become stakeholder management, to a certain extent (Donaldson & Preston, 1995). The stakeholder problem is not easily solved, as it includes modelling and normative issues. The modelling issues refer to questions such as ‘who are our stakeholders?’ and ‘to what extent is it possible to draw a line between stakeholders and non-stakeholders?’ However, normative issues refer to queries such as ‘which stakeholders do we take into account?’ and ‘which stakeholders are we willing to listen to?’

Freeman in his book, Strategic Management: A Stakeholder Approach, put forward the theories of stakeholder management. He explained the relationship of a firm with its environment, and its behaviour within that environment. His work suggested that besides stockholders, other internal and external factors also affect firm behaviour. Adam Smith’s (1937) identification of external interests to the firm may be viewed as an early recognition of stakeholders, he indicated consumers as a vital external stakeholder who are affected by and had interest in the firm. Barnard (1938) opined that employees are important to a firm’s success, so their concerns should be addressed carefully. Some CSR advocates such as Abrams (1951) and Eells (1960) argued that corporates are accountable to many different sectors of society. Abrams (1951) identified four important corporate stakeholders-customers, employees, stockholders and, public (including government).

A significant weakness in the current academic understanding of CSR lies in the traditional concept of discrete and dyadic relationships between an organization and its stakeholders (Freeman, 1984). This perspective does not capture the true interactions in the network of firm–stakeholder relationships (Frooman, 1999; Mattingly, 2004; Rowley & Berman, 2000). This indicates that stakeholders individually contend for managerial action and resources. Stakeholders often interact, cooperate and form alliances with other stakeholders (Frooman, 1999). An stakeholders’ group may seek to persuade other stake-holders to oppose or support a firm; for example, a protest group seeking to persuade consumers to boycott a particular organization’s product or services. Hence, in the informative era, firms are forced to strike a balance with all stakeholders to conduct business in a sustained manner over a period of time (Singh & Verma, 2014).

CSR Disclosure in India

While discussing to Corporate Social Disclosure (CSD), we begin with the question ‘Why organizations should disclose their social practices to stakeholders?’ The answer is: stakeholders have more knowledge and awareness about the role and responsibilities of a corporation than ever before in this era of information technology (IT). They want transparency and accountability from companies. Some incidents in the recent past, such as Satyam Computers Services scandal, have shaped increasing stakeholders’ demand for responsible business behaviour and transparent CSR reporting. A number of theories ranging from the agency theory to stakeholder theory are being used for CSR reporting in Asia (Raman, 2006). Japan has made positive strides in corporate social reporting, but countries such as India, China and Bangladesh have a very limited number of companies which report their social initiatives and that too in industries like oil, chemicals and steel (KPMG, 2005). Content and extent of corporate social disclosure (CSD) in India is underemphasized. Regulatory developments over the last 2 years, however, have set the momentum for a higher to Corporate Social Disclosure (CSD) rate in India (KPMG, 2013). The release of national voluntary guidelines on social, environmental and economic responsibilities of business (NVG-SEE) by the Ministry of Corporate Affairs in 2011 helped to gain the attention of a larger industry audience towards adopting CR practices and transparent disclosure. The guidelines were progressively adopted by the Securities and Exchange Board of India (SEBI) in 2012 to mandate the compulsory disclosure of adoption of NVG-SEE for the financial year ending on or after 31 December 2012. The Department of Public Enterprise (DPE) issued guidelines on CSR and sustainability for Central Public Sector Enterprises (CPSE), which address the requirements of corporate social reporting to assess the overall performance of these enterprises. The other vital development that will affect CSR reporting is the new Companies Act, 2013. The landmark act includes CSR as a mandatory agenda at board-level meetings and requires companies to report their CSR policies and governance along with the CSR budget.

Literature Review and Framework Development

‘The notion of companies looking beyond profits to their role in society is generally termed as CSR’ (Sharma & Kiran, 2012). The European Commission defined CSR in 2006 as ‘a concept whereby companies integrate social and environmental concern in their business operations and their interaction with the stakeholders on voluntary basis.’ However, definition or measurement of CSD is not standardized yet. Gray, Owen, and Maunders (1987) defined CSD as ‘the process of communicating the social and environmental effects of organizations’ economic actions to particular interest groups within society and to society at large’. In its early years, the National Association of Accountants (NAA) Committee on Accounting for Corporate Social Performance identified four major areas of corporate social performance and disclosure: community development, human resources, product and service development, physical resources and environmental contribution. Elkington (1997) emphasized the importance of the triple-bottom-line approach that combines economic, social and environmental reports. The triple-bottom-line approach of CSR action and reporting is demanded by governments, financial investors and local communities (Bebbington et al., 1999; Gray, 2002; Gray, Kouhy, & Lavers, 1995; Mathews, 1997).

CSR goes beyond occasional community service. It is a corporate philosophy that drives strategic decision-making, stakeholder management, hiring practices and ultimately brand development. CSR is a powerful means of gaining sustainable competitive advantage and instilling long-lasting values among shareholders and stakeholders. CSR and reporting thereof offers a point of vantage not only to government and investors, but also to society. Thus, organizations must build on their corporate values to create an organizational culture that is flexible to change and able to sustain CSR strategy in the long run (Maon, Lindgreen, & Swaen, 2009). Basalamah and Jermias (2005), in their study, investigated the practice and motivation for social and environmental reporting and auditing in two Indonesian companies. They found that CSD and auditing are undertaken by management for strategic reasons, rather than on the basis of sense of responsibility. Companies believe that by reporting and auditing their social and environmental program and activities, they would be able to gain trust of various stakeholders. Chapel and Jeremy (2005) investigated the CSD pattern of 50 companies, through analysis of website reporting in seven Asian countries: Indonesia, Malaysia, India, the Philippines, South Korea, Singapore and Thailand. They concluded that CSD varied across the seven countries. Moreover, it was noted that the CSDs of MNCs were higher than that of the companies operating in their home country. The reason for this is that the management of MNCs believed that honest CSR and reporting thereof provided them with the green signal to operate. Zakimi and Hamid (2004), in their study, found that product-related disclosure is higher in the banking and finance sector companies of Malaysia.

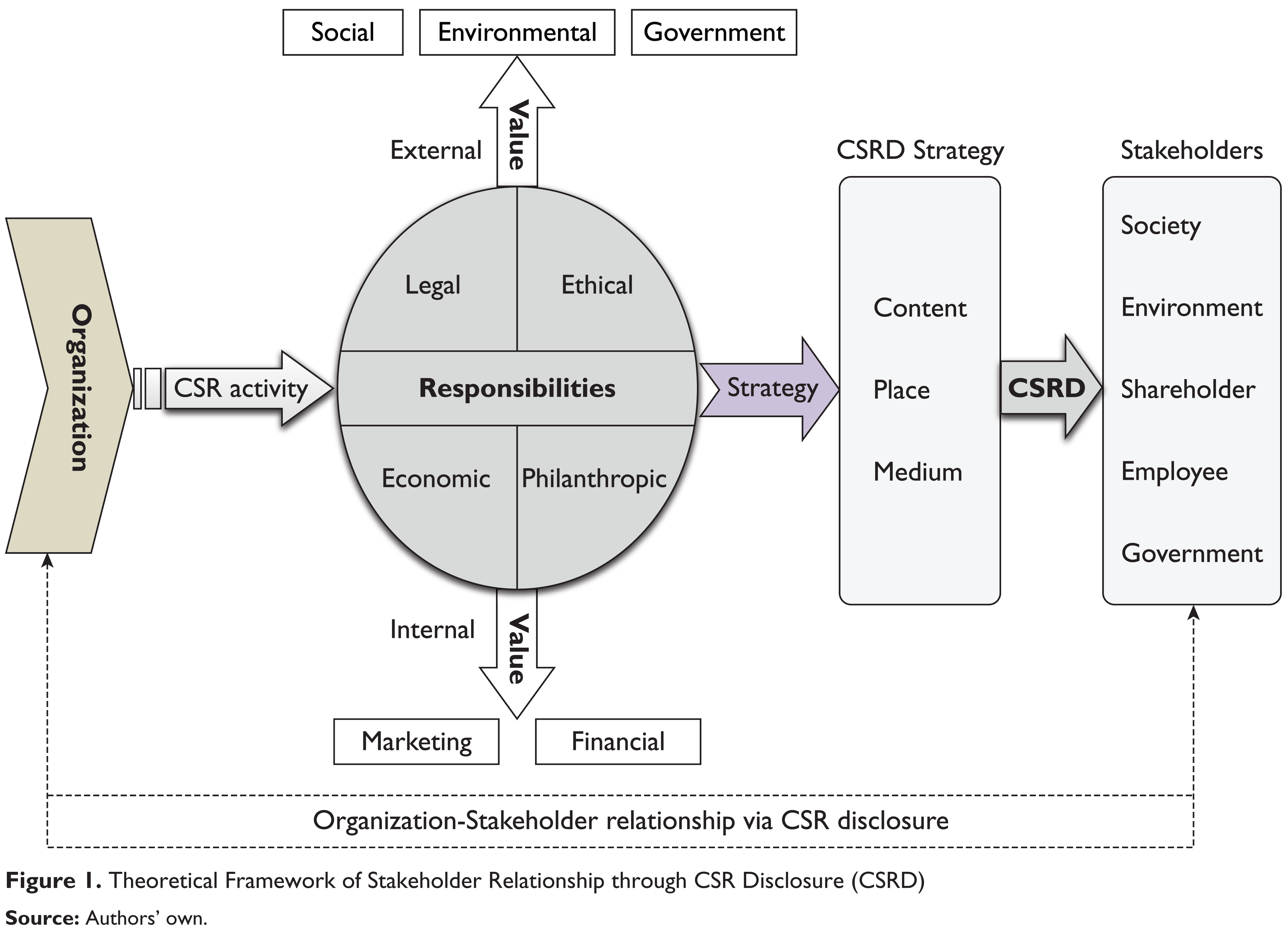

Branco and Rodrigues (2006) conducted a study on CSD in the annual reports and websites of 15 banks. They found that banks with high visibility among customers exhibited higher concerns to improve corporate image through social disclosures. They used a legitimate theory to explain the social disclosure of Portuguese banks. Piacentini, MacFadyen, and Eadie (2000) conducted a study on motivation and extent of CSD of food and confectionery retailers in Scotland. They used audit reports of food retailers followed by an in-depth interview with key decision-makers. Findings of the study showed that only certain proactive companies recognized the benefits of being viewed as a socially responsible company. Singh and Ahuja (1983) conducted a study on CSD among public sector companies in India. They found that CSD practices varied between companies. It was also revealed that the age of a company does not have a significant influence on CSD items such as net sales, but the size of a company, in terms of total assets, does have a positive impact on social disclosure. Thus, we propose a theoretical framework (Figure 1) of organization-stakeholder relationship through CSR disclosure.

The theoretical framework of this study consists of theories and literature on CSR and stakeholder relations. The theoretical literature typically distinguishes the different approaches to answer the questions: what are organizations responsible for and what are they motivated by? The classical view says: ‘The social responsibility of business is to increase the profits’ (Friedman, 1970). Under this notion, social responsibility is considered to be primarily a responsibility of the government. However, according to stakeholders’ perspective, companies are not only accountable to the owners, but also to the stakeholders (Freeman, 1984).

Methodology

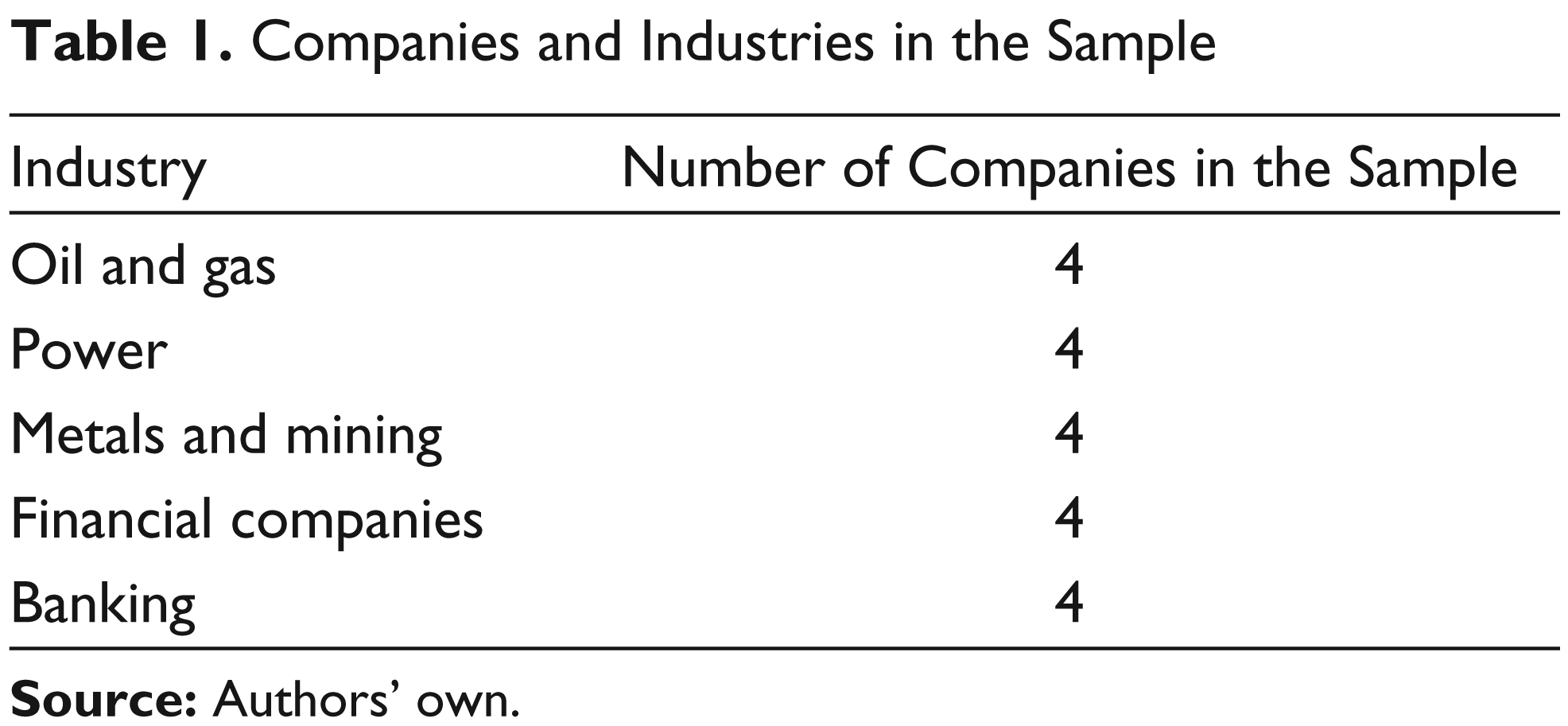

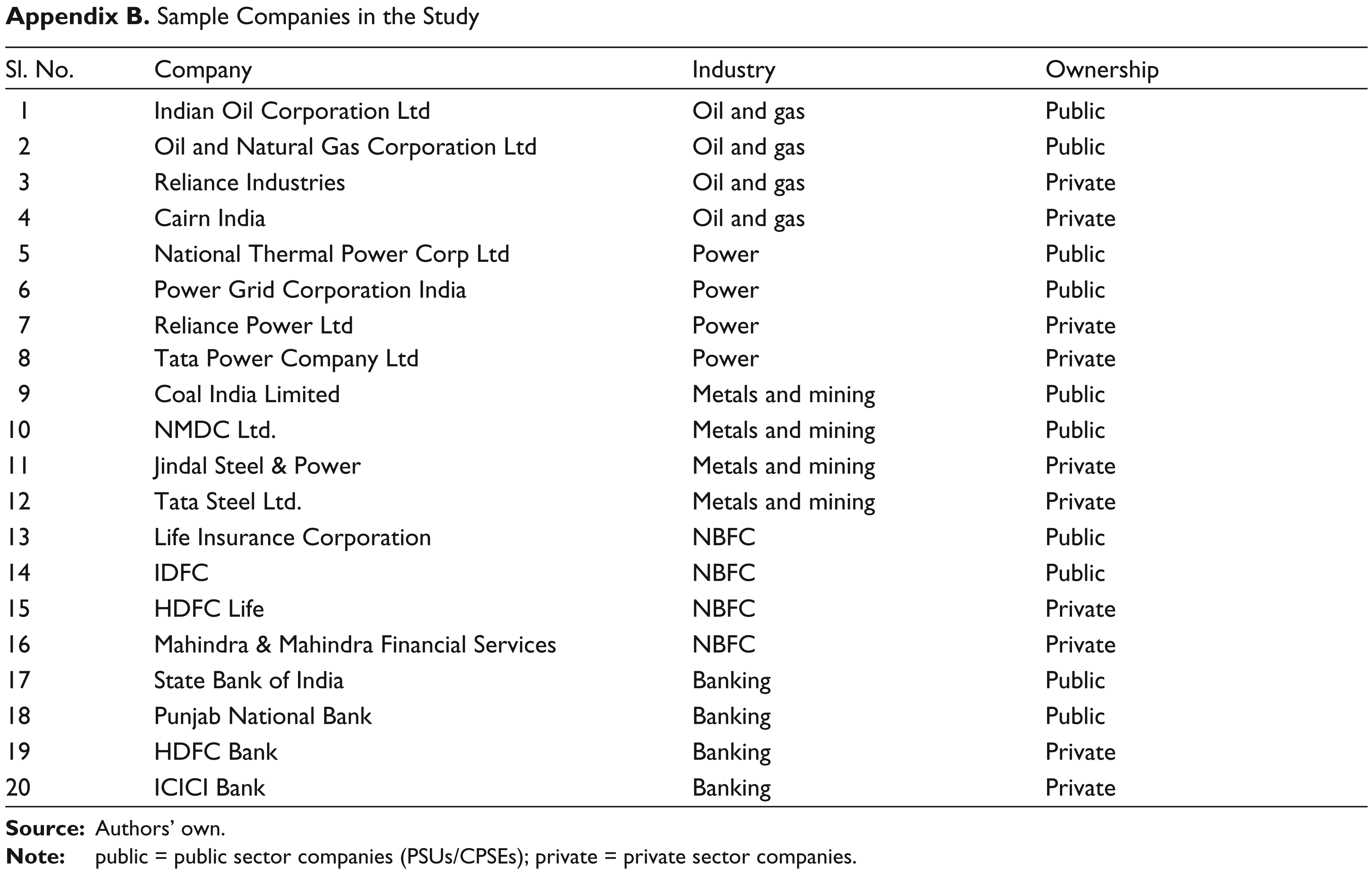

To figure out the extent of socially responsible practices of Indian organizations, the contents disclosed in the annual reports of the top 20 Indian firms were analyzed using the technique of content analysis. The reports were from the year 2010 to 2014 and selected from the list of Bombay Stock Exchange (BSE-500). The criteria of selecting companies and the industries were in accordance with the objectives of this study. The main objective of the current study was to analyze the nature and extent of social disclosures in Indian firms across industries. The study also intended to examine the influence of profitability and firm size on CSD practice while controlling the effect of firm ownership, that is, public or private sector companies, and industry affiliation. Hence, for the purpose of this study, only those industries in which both public and private sector companies existed were selected, as there are industries with no public sector companies such as automobile, retail, pharmaceuticals and textiles. Furthermore, companies chosen were those that were listed in the BSE-500. In this way, we identified 20 companies from five different industries, namely oil and gas, power, metals and mining, non-banking financial companies (NBFCs) and banking (see Table 1). The top four companies (two public and two private) were handpicked from each of these five industries.

Companies and Industries in the Sample

Annual reports are the most widely used documents in the analysis of corporate social activities among other documents, such as brochures, press releases and the likes, used to disclose corporate social practices to the public. According to Gray et al. (1995), annual reports are vital documents of corporate communication and instruments for maintaining the relationship with various stakeholders. In order to quantify CSD, the annual reports were subjected to the content analysis technique. This is an accepted research technique in social and environmental reporting (Abbott & Monsen, 1979; Ernst & Ernst, 1978; Guthrie & Mathews, 1985; Guthrie & Parker, 1990; Krippendorff, 1980; Zeghal & Ahmed, 1990).

Annual reports of the companies were downloaded from their websites and their Corporate social responsibility disclosures (CSD) in each section were assessed. The content of a company’s annual report is divided into five broad sections: chairman’s message, letter to stakeholders, management discussion and analysis, directors’ reports and others. This study used the number of sentences as the unit of measurement of corporate social responsibility disclosure (CSD) since sentences provide complete, meaningful (Unerman, 2000) and reliable data for further analysis (Hackston & Milne, 1996; Milne & Adler, 1999). Different units of measurement, such as the number of words (Zeghal & Ahmed, 1990), number of lines (Raman, 2006) and number of pages (Gray et al., 1995), have been used in prior studies. The correct choice for the unit of measurement has been debated in literature (Gray et al., 1995; Milne & Adler, 1999; Raman, 2006; Unerman, 2000). Pages, for instance, are criticized for variations in font size, graphics and margins (Milne & Adler, 1999). Number of words are criticized due to concise or verbose styles of writing and number of lines also criticized for font size (Hackston & Milne, 1996). So, in this study, the number of sentences was considered as a favourable and accurate unit of measurement (Hackston & Milne, 1996; Ingram & Frazier, 1980; Milne & Adler, 1999; Unerman, 2000). The annual reports of Indian companies use both Hindi and English. However, in order to avoid linguistic issues, we adhered to the English language while analyzing the contents of the reports.

The most important process of the content analysis technique involves identification of themes or categories into which contents can be classified. Content categories were identified based on the scrutiny of literature (Batra, 1996; Branco & Rodrigues, 2006; Imam, 2000; Murthy, 2008; Raman, 2006) and recommendations of the NAA Committee. Following are the four major themes:

Community development activities Human resources activities Product and service activities Environmental activities

Results and Discussion

Descriptive Statistics

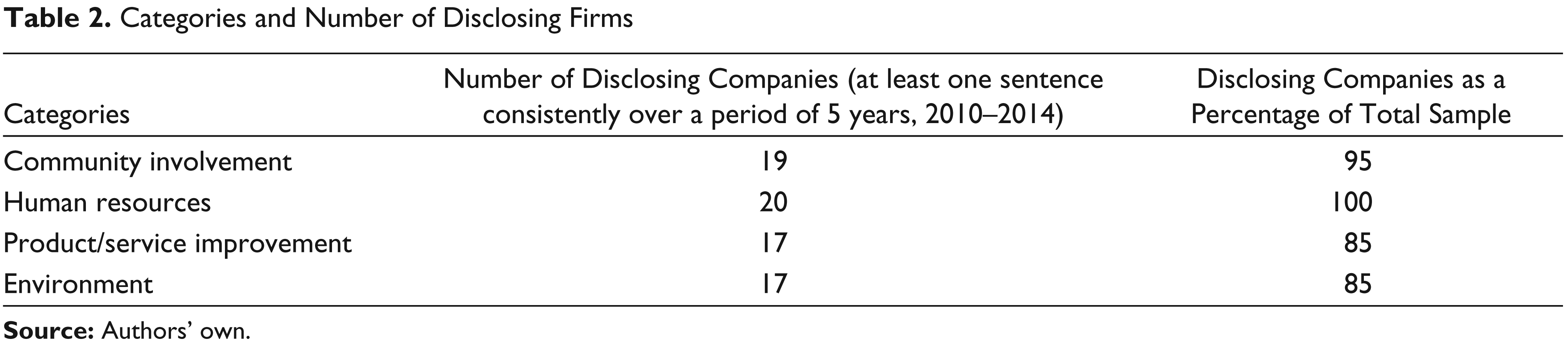

An analysis of the contents revealed that Indian companies have initiated significant disclosure of their social responsibilities in their annual reports. The companies even had a separate section for CSR reporting. As shown in Table 2, the sample companies disclosed more than 60 per cent in each of the four categories. All the companies (100%) disclosed their human resource activities followed by community development (95%), product/service improvement (85%) and environment (85%). The findings of this study are consistent with those of United Nations Development Programme (2002), which indicates that community relations and human resource development are perceived as very important aspects of CSR in Indian organizations. The results are in contrast to Raman’s (2006) findings, which point out that less percentage of companies disclose community development activities in their annual reports.

Categories and Number of Disclosing Firms

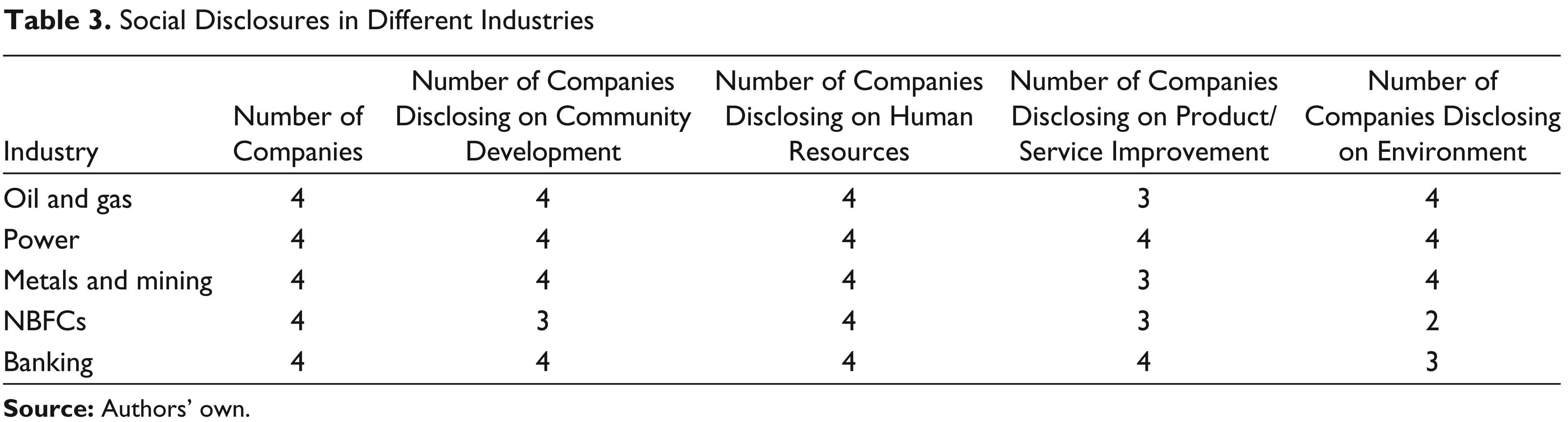

Table 3 presents social disclosures by companies in different industries and under different CSD themes. It shows that human resource development is the most popular theme (100% participation by the sample firms) followed by community development, product or service improvement and environment. The power sector is the only industry wherein all the companies disclosed reports with regard to each of the four themes.

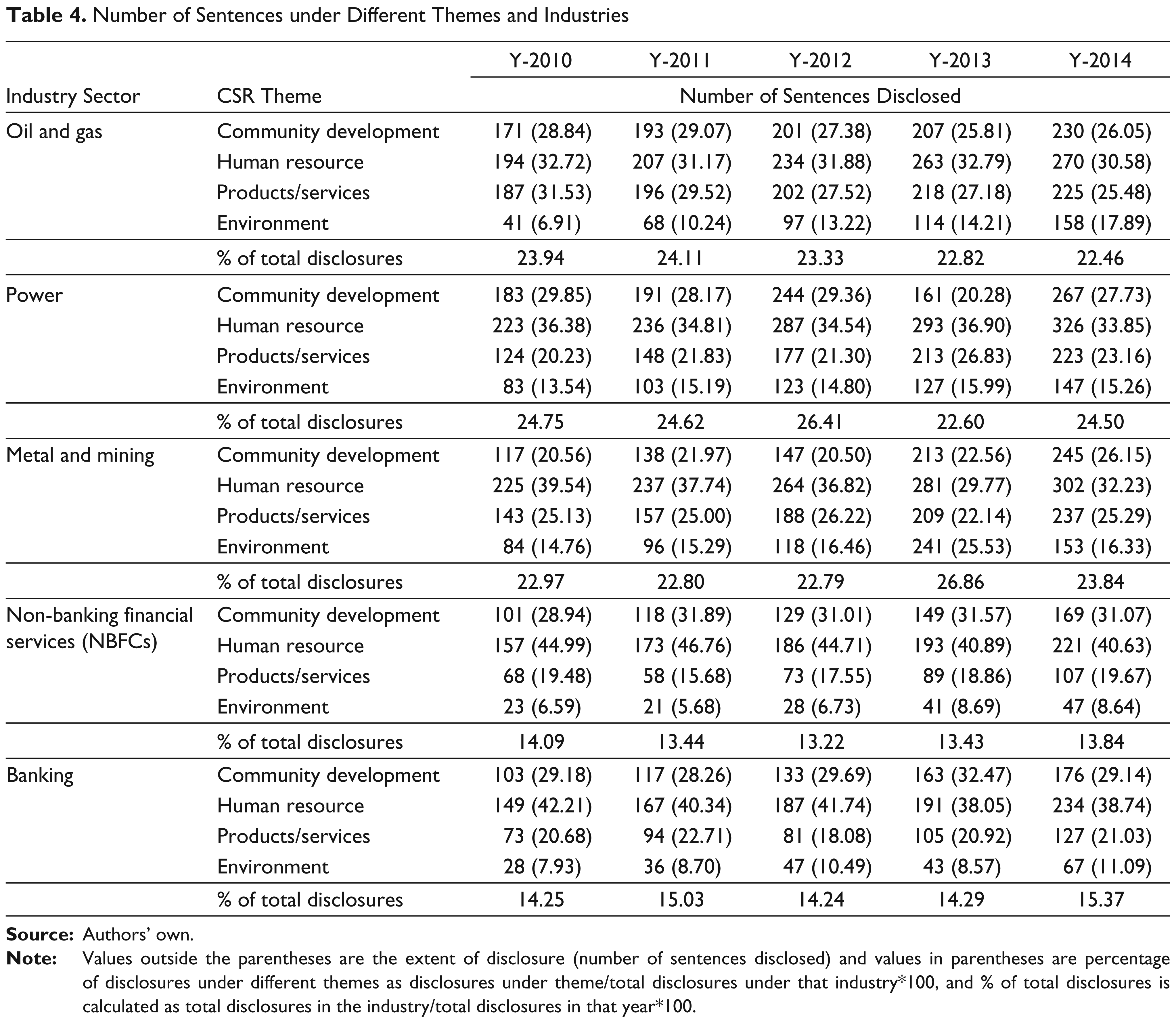

As shown in Table 4, oil and gas companies favoured the human resource development theme among others during 2010–2014: 194 sentences (32.72% in 2010), 207 sentences (31.17% in 2011), 234 sentences (31.88% in 2012), 263 sentences (32.79% in 2013) and 270 sentences (30.58% in 2014) were disclosed. Environmental disclosure was the least favoured theme by the industry: 41 sentences (6.91% in 2010), 68 sentences (10.24% in 2011), 97 sentences (13.22% in 2012), 114 sentences (14.21% in 2013) and 158 sentences (17.89% in 2014) were disclosed.

A similar pattern of disclosures was exhibited by the four other industries. For example, banking companies have disclosed their maximum under the human resource development theme: 149 sentences (42.21% in 2010), 167 sentences (40.34% in 2011), 187 sentences (41.74% in 2012), 191 sentences (38.05% in 2013) and 234 sentences (38.74% in 2014). It can be seen from Table 4 that the manufacturing and processing sector companies (oil and gas, power, and metals and mining) disclosed relatively more on the environment theme than service sector companies (NBFCs and banking). The reason for such a predicament is that manufacturing companies’ operations have a higher effect on ecological footprint than service sector companies.

Social Disclosures in Different Industries

Number of Sentences under Different Themes and Industries

The amount and quality of disclosures under the environmental theme was alarming. Voluntary disclosures under this theme are not emphasized by most of the companies. From Table 3, not even all the firms in the NBFC (two companies) and banking (three companies) sectors have disclosed reports on the environmental theme. In the environmental category, Indian companies have to raise the bar of CSD to meet the demands of some deeply associated stakeholders like the government, environmental activists and local communities.

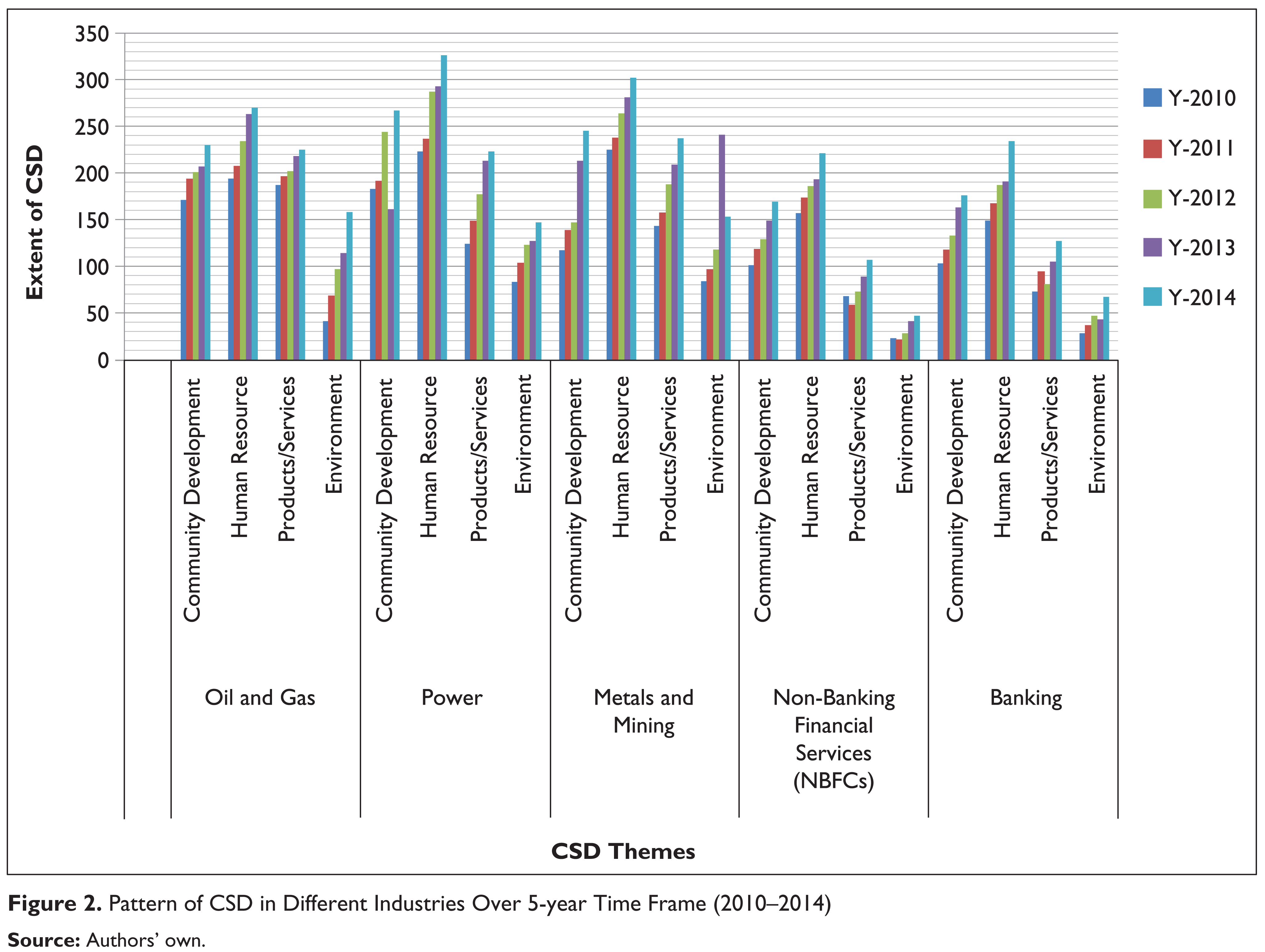

Figure 2 presents a holistic view of CSD as practised by Indian firms with respect to industry affiliations during 2010–2014. There was an increase in the extent of disclosures by oil and gas companies under all the CSD themes. Power sector companies reflected a similar pattern of disclosures under all the themes except community development wherein the amount of disclosure declined in 2013. Inconsistency in disclosure amount was observed in the metals and mining sector with respect to the environmental theme, and in the NBFC and banking sectors with regard to both product/service and environment themes.

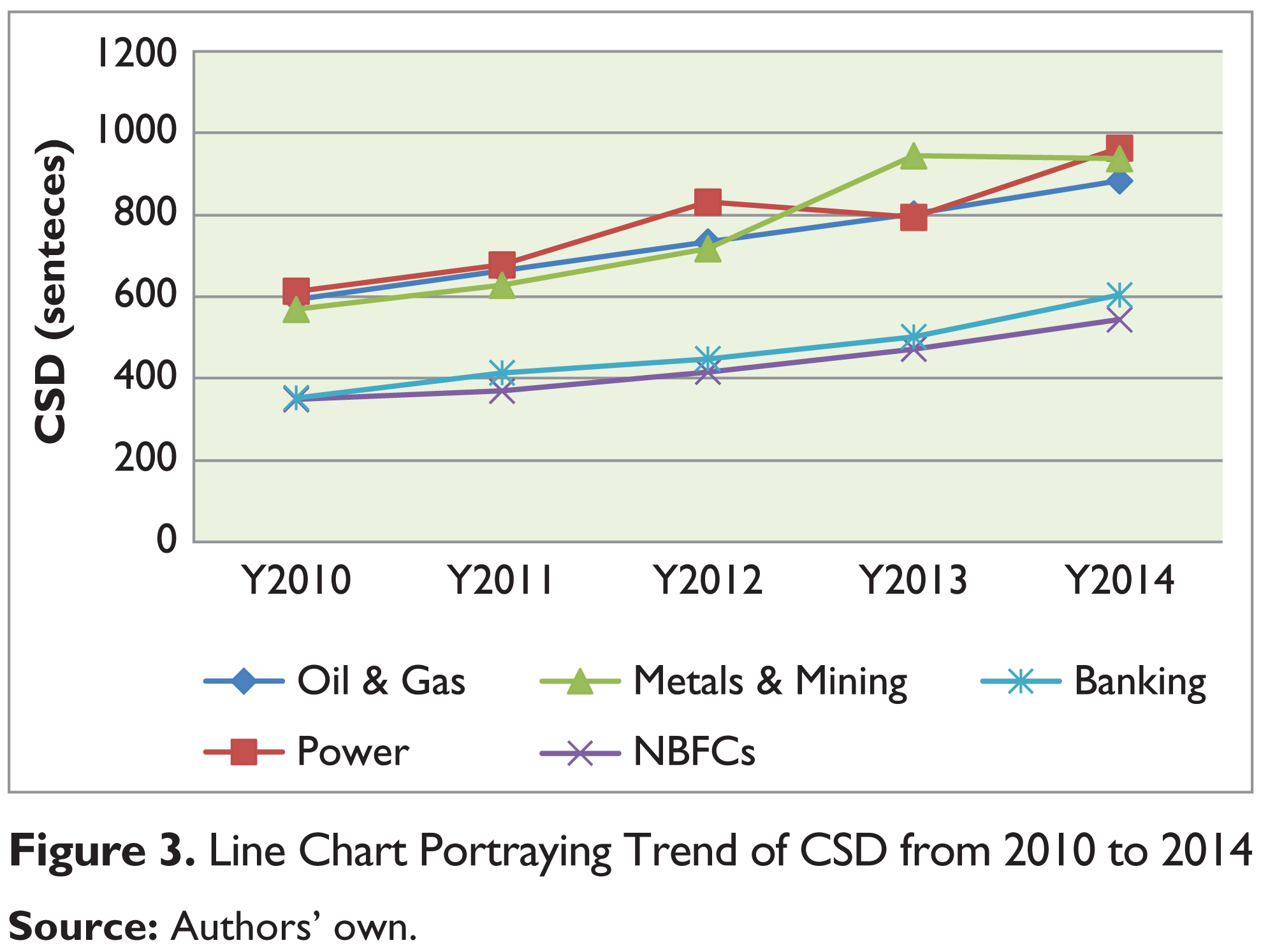

In the period 2010–2014, all the annual reports of the sample companies reflected some amount of social disclosures. Figure 3 portrays the overall trend of disclosing CSR information. In general, the manufacturing and processing industry (power and metals and mining) provided a higher amount of disclosures but also displayed a fluctuating trend. Oil and gas sector companies, however, showed consistent growth trends. The other two industries, that is, NBFCs and banking, exhibited almost similar trends (in nature as well as in the extent of disclosures).

Correlation Results

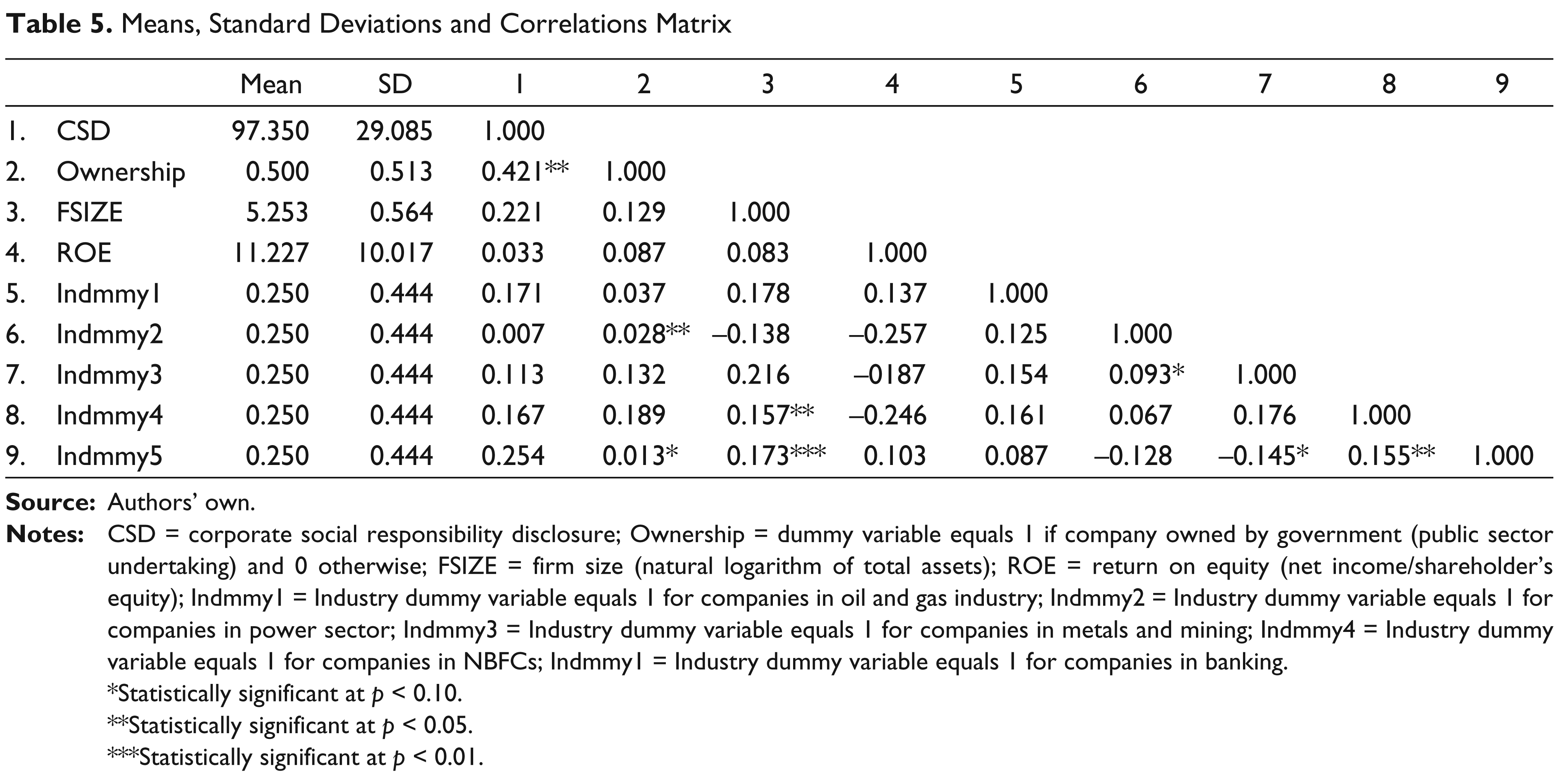

Table 5 presents the mean and standard deviation (SD) of variables along with their inter-correlations. The dependent variable, that is, CSD, had a mean value of 97.350 and an SD of 29.085. The magnitude of SD indicated that there is a high variance of CSD among the sample companies. The size of the firms was measured keeping in mind the natural logarithm of their total assets. The mean and SD were 5.253 and 0.564, respectively, which shows that there is less variance in the size of the firms. However, there was a high variance in return on equity (ROE) among companies (mean = 11.227; SD = 10.017). Correlation matrix (see Table 5) showed that CSD is positively correlated with ownership (ρ = 0.421; p < 0.05), and no significant correlations were found between CSD, firm size (FSIZE) and ROE. This indicated that ownership (public or private sector companies) has effect on CSD. It was observed that public sector companies are more engaged in CSR activities than the private sector companies, as the former’s disclosure practices are as per the demands of the local communities and the general public as a whole.

Low or no significant correlation was found between independent variables (see Table 5). In general, none of the correlation coefficients was high, that is, more than 0.50. Hence, there was no concern for the existence of multi-collinearity. Furthermore, a collinearity diagnostics test was performed (i.e., VIF test) and results indicated that no such problem existed (see Table 6). Variance inflation factors (VIFs) were also found to be within the acceptable limit (less than 3 according to Branco & Rodrigues, 2006), thereby confirming the absence of significant multicollinearity.

Means, Standard Deviations and Correlations Matrix

*Statistically significant at p < 0.10.

**Statistically significant at p < 0.05.

***Statistically significant at p < 0.01.

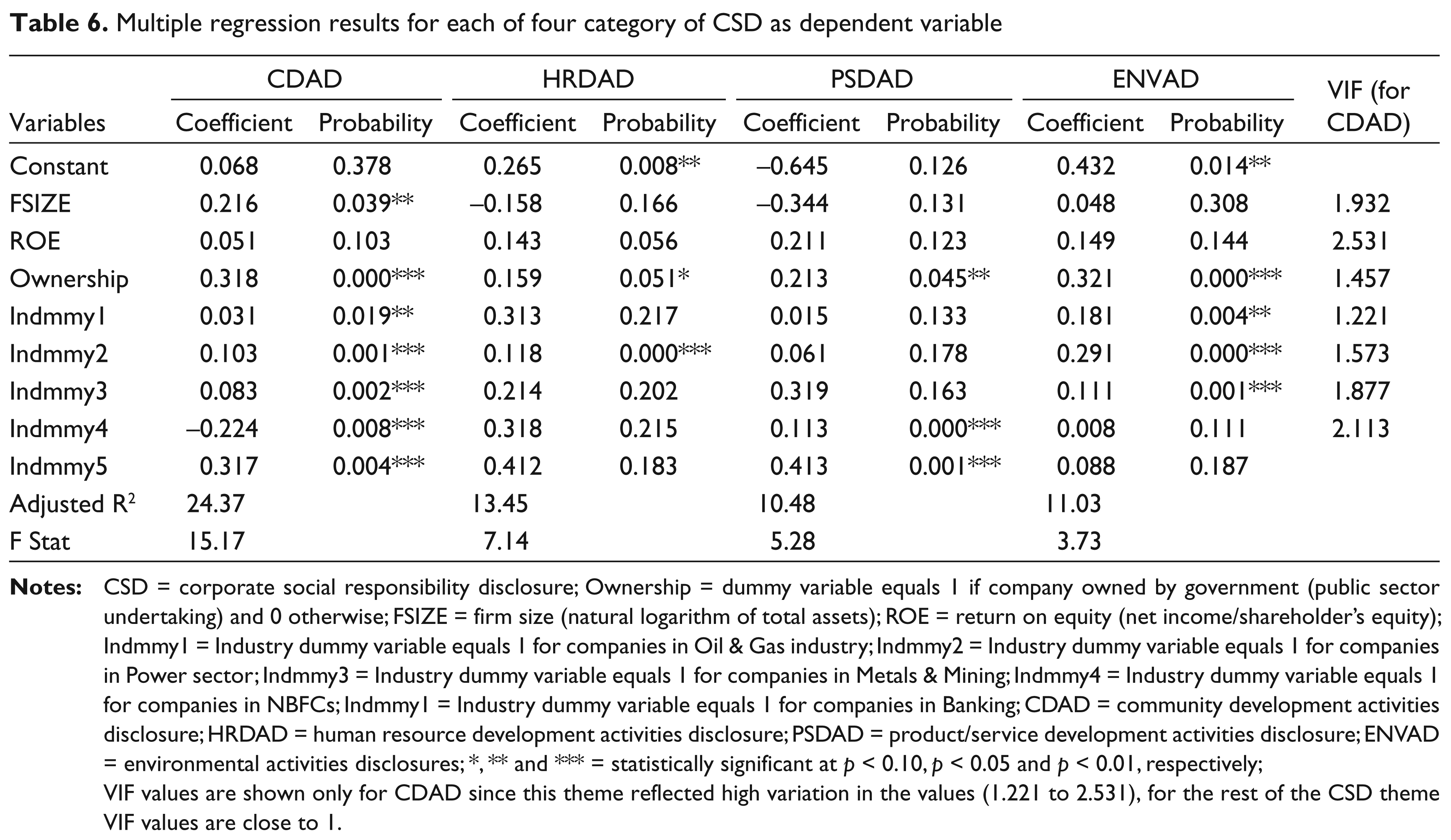

Multiple regression results for each of four category of CSD as dependent variable

VIF values are shown only for CDAD since this theme reflected high variation in the values (1.221 to 2.531), for the rest of the CSD theme VIF values are close to 1.

Multiple Regression Results

We used multiple regression analysis to evaluate how well predictor variables (i.e., firm size and profitability) explain CSD practices of Indian companies. The dependent variable of the study was CSD, a measure of the extent of CSR information disclosed in annual reports. The study used two explanatory variables (independent variables) and two control variables.

The first independent variable was firm size. Few studies used some proxies to measure firm size, namely total assets (Teoh & Thong, 1984), net sales (Belkaoui & Karpik, 1989) or revenues (Roberts, 1992), whereas others used multiple measures such as sales, total assets and market capitalization (Hackston & Milne, 1996). This study employed total assets as the proxy to measure firm size.

As for corporate economic performance or profitability, the second independent variable, prior studies used proxies such as return on assets (ROA) and return on equity (ROE) (Haniffa & Cooke, 2005) or a combination of ROA and ROE (Shen & Chang, 2009). Cowen, Ferreri, and Parker (1987, p. 113) concluded that researchers ‘cite profitability as a factor that allows, or perhaps impels, management to undertake and to reveal to shareholders more extensive social responsibility programs.’ Thus, this study considered ROE as a proxy to measure corporate profitability. The study included effects of control variables (ownership and industry affiliation) that were found, in prior research, to be related to CSD (Anas, Rashid, & Annuar, 2015; Muttakin & Subramanian, 2015). Ownership, in the present study, indicated whether the company is owned by the government (i.e., public sector undertakings or PSUs) or private individuals (i.e., private companies). PSUs are expected to disclose more about their social responsibilities (Muttakin & Subramanian, 2015). Industry affiliation was another control variable in this study. Industries such as oil and gas, power and metals and mining have greater obligations towards the local communities and the general public due to the nature of their operations. On the other hand, service industries such as banking, consultancy or finance have comparatively lesser obligations (Hackston & Milne, 1996; Ratanajongkol, Davey, & Low, 2006).

Thus, the following model was designed to analyze the relationship between study variables:

where CSD is the extent of corporate social disclosure by the company; SIZE is the natural logarithm of total assets of the company; ROE is the net income/shareholder’s equity; OWNERSHIP is the dummy variable for ownership classification, that is, government-owned or private-owned companies; INDUSTRY is the dummy variable of industry classification; 1 refers to oil and gas, 2 refers to power, 3 refers to metals and mining, 4 refers to non-banking financial service companies (NBFCs), and 5 refers to banking; βi is the coefficient (i = 1, …, 8); and ε is the error term.

The above model was used for each theme (community development, human resource, product and/or service and environment). The measurement of independent variables (profitability and size) was based on prior studies (Amran & Devi, 2008; Haniffa & Cooke, 2005; Muttakin & Subramanian, 2015).

Table 6 reports the results of regression analysis using CSD as a dependent variable. Results showed that ownership has a significantly positive impact on all to Corporate Social Disclosure (CSD) themes: community development (CDAD) (β = 0.318, p < 0.01), human resource development (HRDAD) (β = 0.159, p < 0.10), product/service development (PSDAD) (β = 0.213, p < 0.05) and environment (ENVAD) (β = 0.321, p < 0.01). This indicated that public sector companies operate in the interest of its various stakeholders and feel liable towards them. Conversely, private companies operated in the interest of its shareholders only and focused on the mechanism of maximizing shareholders’ wealth. These companies considered CSR an added cost or burden on the company. Thus, the public sector companies are more engaged in CSR activities and reporting thereof than the private ones.

Firm size does not necessarily influence all CSD themes. While there were links between CDAD and size (β = 0.216, p < 0.05), there was no statistically significant impact on other themes. This suggested that the large companies with public visibility appear to favour community development. The results also showed no significant impact of profitability on CSD. This indicated that financial visibility does not translate to more (or less) social information. Finally, industry affiliation was seen to have a fluctuating effect on the level of CSD. Manufacturing industries provide the following disclosures on the environmental theme oil and gas (β = 0.181, p < 0.01), power (β = 0.291, p < 0.01) and metals and mining (β = 0.111, p < 0.01). But industries such as NBFCs and banking did not. Only the power sector companies showed an interest in human resource disclosure (β = 0.118, p < 0.01). The community development theme was, however, favoured by all the industries except NBFCs, which provided less disclosures on the community development theme: oil and gas (β = 0.031, p < 0.05), power (β = 0.103, p < 0.01), metals and mining (β = 0.083, p < 0.01), NBFCs (β = –0.224, p < 0.01) and banking (β = 0.317, p < 0.01).

Our findings related to the nexus of profitability and the extent of CSD are consistent with prior studies (e.g., Anas et al., 2015; Belkaoui & Karpik, 1989; Hackston & Milne, 1996; Roberts, 1992). The findings with regard to the link between firm size and CSD partially support the findings of Cowen et al. (1987), Patten (1991), Hackston and Milne (1996) and Muttakin and Subramaniam (2015), as these studies had reported that firm size does impact CSD practices. Cowen et al. (1987) posited that larger firms have diverse stakeholders, having more effect on local communities, society and environment and feel a higher sense of responsibilities. However, our study revealed that larger Indian companies are inclined to disclose on community development theme only.

The results of our analysis with regard to the first control variable, that is, firms’ ownership, are in line with the findings of Muttakin and Subramaniam (2015). The findings with respect to the effect of industry affiliation, the second control variable, on CSD are consistent with the findings of Patten (1991), Roberts (1992), Hackston and Milne (1996), Mahadeo, Oogarah-Hanuman, and Soobaroyen (2011) and Anas et al. (2015).

The amount and quality of CSD in the developed countries is far better than the developing countries (Bhatia & Tuli, 2014; Wanderley, Lucian, Farache, & de Sousa Filho, 2008). In the race that features two of the fastest emerging economies, India is leading in CSD and China is lagging behind (Baskin, 2006; Bhatia & Tuli, 2014). Bhatia and Tuli (2014) found a significant difference in the extent of CSD between India and China; the total mean disclosure score of India was 81.34 per cent, whereas China registered a meagre 31.25 per cent. Alon, Latteman, Fetscherin, Li, & Schneider (2010) concluded that Indian firms disclose better than Chinese firms. Preuss and Barkemeyer (2011) revealed that India records higher environmental disclosures in comparison to China, as per the Global Reporting Initiative (GRI). However, the scenario is not as favourable as it seems because only few large Indian firms disclose on environment (Kansal & Singh, 2012). Human resource, by far, is the most reported CSD category followed by community development and product/service contribution in India and other developing nations (Bhatia & Tuli, 2014; Mahadeo et al., 2011; Murthy, 2008). The environmental disclosure practices are at a nascent and alarming state in other developing countries such as Indonesia, Bangladesh, China, Malaysia, Brazil, Mauritius and South Africa (Anas et al., 2015; Belal, 2001; Chapel & Jeremy, 2005; De Villiers & Van Staden, 2006; Huang & Wang, 2010; Mahadeo et al., 2011; Wanderley et al., 2008). In recent years, however, there has been an emphasis to promote sustainability disclosures in Asian markets such as India, Indonesia, Malaysia and Taiwan by governments and regulators (Anas et al., 2015; Singh & Verma, 2014).

Conclusion

This study highlighted the CSD practices of 20 top Indian companies listed in the BSE. The findings of the study indicated that firms in India disclose many aspects of the social responsibilities in their annual reports. CSD, however, varied between different firms and industries. As mentioned in the ‘Results and Discussion’ section, all the firms disclose their social responsibilities significantly on community development, human resources and product/service improvement, but the scores are not good on the environment front. The important thing is that the relative disclosures of the companies on each theme have improved over the years. The results obtained from multiple regression analysis reveal no significant association between firm’s profitability and social disclosure practices, that is, highly profitable firms may not be necessarily highly motivated to disclose their social responsibilities in their annual reports. Larger firms are willing to disclose more on community development activities in their annual reports.

In the present study, annual reports from five different industries were analyzed. Dissimilarity is found with respect to CSD theme on one hand and dimensions and/or discourses expressed in terms of stakeholders’ priorities, perspectives, contextual information and organization’s ambition level on the other hand. In the global economy, increasing expectations of transparency and accountability towards all stakeholders has become an important part of management discussions. Organizational decisions about adopting CSR and CSR reporting to meet stakeholders’ needs and expectations are complex but deemed necessary. These expectations have evolved through a range of global and regional standards, codes and guidelines (Golob & Bartlett, 2007). In today’s society, the future of any company depends critically on how the company is viewed by its key stakeholders such as shareholders, creditors, customers and members of the community in which the company operates (Cornelissen, 2004, p. 9). Thus, companies need to build and harness a healthy relationship with stakeholders. Reporting is one of the vital activities used by companies in a strategic and instrumental manner to foster stakeholders’ trust in order to survive and prosper. According to Birth, Illia, Laurati, and Zamparini (2008), companies can improve their CSR performance and CSR communication through three possible ways. First, careful selection of type of CSR activities to be engaged in. Second, focused disclosure towards some key publics, such as customer, shareholders, lenders and government, which may cause major margin of improvement in strengthening the trust. Finally, companies may benefit from adopting international reporting standards.

Limitations and Future Research Directions

Findings of the study should be interpreted while acknowledging some limitations. First, contents disclosed in only annuals reports have been analyzed but other sources like websites, newspapers or magazines have not been considered in this study. Hence, further research can be conducted to analyze the information disclosed in such mass communication media. Second, the study could not fully consider the quality of social disclosures because only a few Indian companies provide quantitative or monetary to Corporate Social Disclosure (CSD) (Kansal & Singh, 2012). Third, we assessed the influence of only two factors (firm size and profitability) on CSD practices. Further research may consider the effect of ‘CSR award’. Prior studies suggest that the most important factor that influences the quality of CSD is the award received for good CSR practices (Anas et al., 2015; Boesso & Kumar, 2007). Fourth, there might have been a possibility of errors being introduced while analyzing the content of the annual reports, although utmost care was taken to minimize them.

Footnotes

Appendix

Sample Companies in the Study

| Sl. No. | Company | Industry | Ownership |

| 1 | Indian Oil Corporation Ltd | Oil and gas | Public |

| 2 | Oil and Natural Gas Corporation Ltd | Oil and gas | Public |

| 3 | Reliance Industries | Oil and gas | Private |

| 4 | Cairn India | Oil and gas | Private |

| 5 | National Thermal Power Corp Ltd | Power | Public |

| 6 | Power Grid Corporation India | Power | Public |

| 7 | Reliance Power Ltd | Power | Private |

| 8 | Tata Power Company Ltd | Power | Private |

| 9 | Coal India Limited | Metals and mining | Public |

| 10 | NMDC Ltd. | Metals and mining | Public |

| 11 | Jindal Steel & Power | Metals and mining | Private |

| 12 | Tata Steel Ltd. | Metals and mining | Private |

| 13 | Life Insurance Corporation | NBFC | Public |

| 14 | IDFC | NBFC | Public |

| 15 | HDFC Life | NBFC | Private |

| 16 | Mahindra & Mahindra Financial Services | NBFC | Private |

| 17 | State Bank of India | Banking | Public |

| 18 | Punjab National Bank | Banking | Public |

| 19 | HDFC Bank | Banking | Private |

| 20 | ICICI Bank | Banking | Private |