Abstract

This research evaluates the adoption of digital payment products launched by the National Payments Corporation of India using the Bass diffusion model. The study contributes to Fintech adoption literature and provides empirical and theoretical insights based on historical digital payments data. The findings show that imitation plays a significant role in adoption, with a slow initial adoption followed by acceleration. Among several payment products, UPI (Unified Payments Interface) stands out as the most successfully adopted product. The study highlights the relevance of the Bass diffusion model for estimating adoption rates and offers insights for international regions considering UPI-based payment systems. The results indicate varying adoption rates for different payment products and pronounced impact of imitations, with some experiencing slower adoption post-COVID-19 and others yet to achieve widespread adoption. The results aid business planning in estimating market potential, resource allocation, product development and strategic direction. Regulatory authorities can use this insight to enhance financial inclusion and promote lesser paper cash transactions which lead to socio-economic and business transformation.

Introduction

The rapid advancement and widespread adoption of financial technology, known as Fintech, are fuelling a profound transformation within the financial services industry. Over the past decade, Fintech has experienced remarkable growth, reaching a global market size of $112.5 billion in 2021. It is projected to expand at a compound annual growth rate of 20% in the next decade (Maveric Systems, 2022). Unlike previous technological advancements in finance that originated in major financial hubs, Fintech has gained widespread adoption in developing and underdeveloped countries. Africa and Asia, in particular, have witnessed notable success stories and general acceptance of Fintech applications (Coffie & Hongjiang, 2023). This unprecedented rise of Fintech has captured the attention of researchers, academics, regulators, large technology companies and financial institutions.

According to Rogers (2003), an innovation is defined as a new idea, practice or object that is perceived as such by individuals or other adoption units. The innovation process begins with recognizing a problem or a need. It concludes with the adoption of a commercial product by users (adopters) to address that need. Innovators are the initial adopters in society, while laggards are the final adopters, resulting in socio-economic changes driven by innovation. In the context of innovation in digital payments, the introduction of the Unified Payments Interface (UPI) by the National Payments Corporation of India (NPCI) has revolutionized money transfers and payments. It efficiently caters to the transaction requirements of customers and merchants, thereby reducing transaction costs.

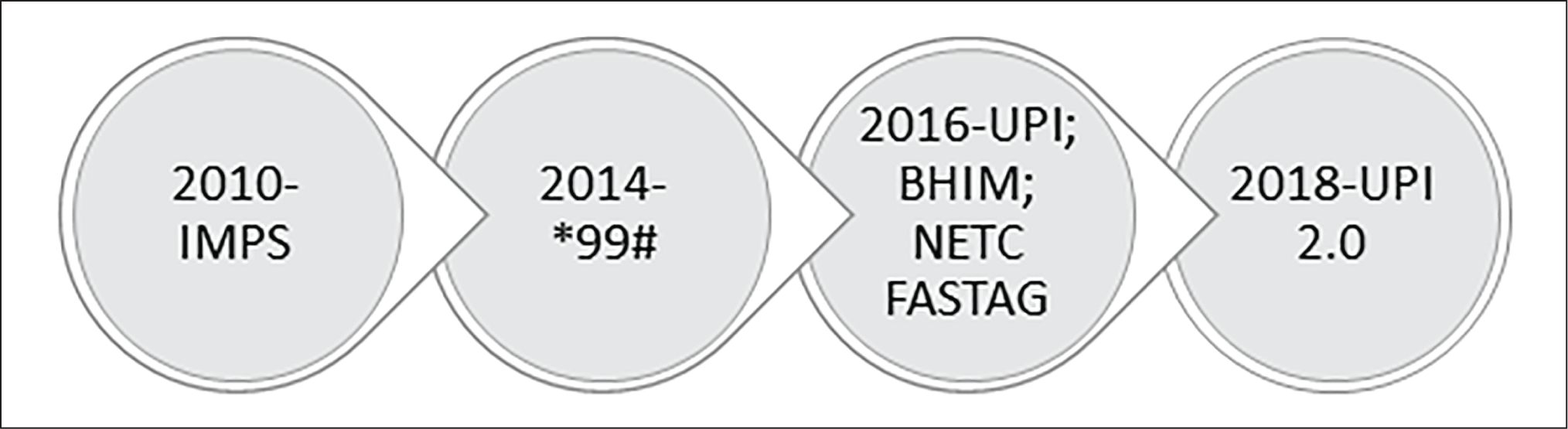

The NPCI developed the UPI, establishing a comprehensive payment and settlement infrastructure in collaboration with the Reserve Bank of India and the Indian Banks Association. NPCI has introduced a range of robust payment systems, including UPI, Immediate Payment Service (IMPS), National Electronic Toll Collection (NETC FASTAG), Unstructured Supplementary Service Data (USSD; *99#), and Bharat Interface for Money (BHIM). Figure 1 demonstrates the distinctive products by NPCI in digital payments (Reserve Bank of India [RBI], 2021). It has effectively harnessed these technologies to facilitate the seamless exchange and integration of digital payment technology on a global level.

IMPS was introduced in India in 2010, marking the country as the fourth nation, following South Korea, the United Kingdom, and South Africa, to establish a fast payment system. Its primary objective is facilitating real-time fund transfers between beneficiaries and remitters, with deferred net settlements between banks. IMPS is a versatile multi-channel system accessible through mobile devices, ATMs, internet banking, bank branches and Business Correspondents. Additionally, it allows payment system providers (PSPs) to participate and facilitate remittances from digital wallets to bank accounts.

UPI is a mobile-based fast payment system that operates 24/7, 365 days a year. It enables instant remittance by utilizing a virtual payment address set by the user, facilitating both person-to-person and merchant transactions. The UPI ecosystem comprises NPCI as the network and settlement provider, issuer and beneficiary banks. PSPs include payer and payee banks and third-party application providers (TPAP) such as Google Pay and WhatsApp. Non-bank PSPs are also part of the UPI system. UPI was launched in September 2016 with an initial transaction limit of ₹0.1 Million, which was later increased to ₹0.2 Million. It has rapidly emerged as the world’s fastest payment system. Further advancements and innovations are being introduced to expand UPI’s reach, including enabling UPI on desktop browsers, feature phones, offline payments and recurring payments. These developments ensure UPI’s continuous evolution and adaptability to meet users’ diverse payment needs.

NETC FASTAG system enables electronic interoperable toll collection. This system utilizes fast-tags issued by banks or highway management companies and affixed to vehicles. These fast-tags are linked to various payment instruments such as bank accounts, UPI and PPI cards, facilitating seamless and convenient toll payments. BHIM is a mobile application that leverages UPI to facilitate quick and easy payment transactions. Users can make payments through the BHIM app using UPI, simplifying the payment process and enhancing financial accessibility. Both NETC and BHIM were also introduced in 2016.

In November 2014, *99# was launched as a USSD-based mobile banking service. It allowed users to access banking services through their mobile devices via a USSD code. This service later expanded into USSD 2.0, providing non-internet-based mobile device users with a dialling option to access UPI functionality. While NPCI has introduced other products in the digital payment landscape, UPI and IMPS products have emerged as front-runners and have had a substantial impact.

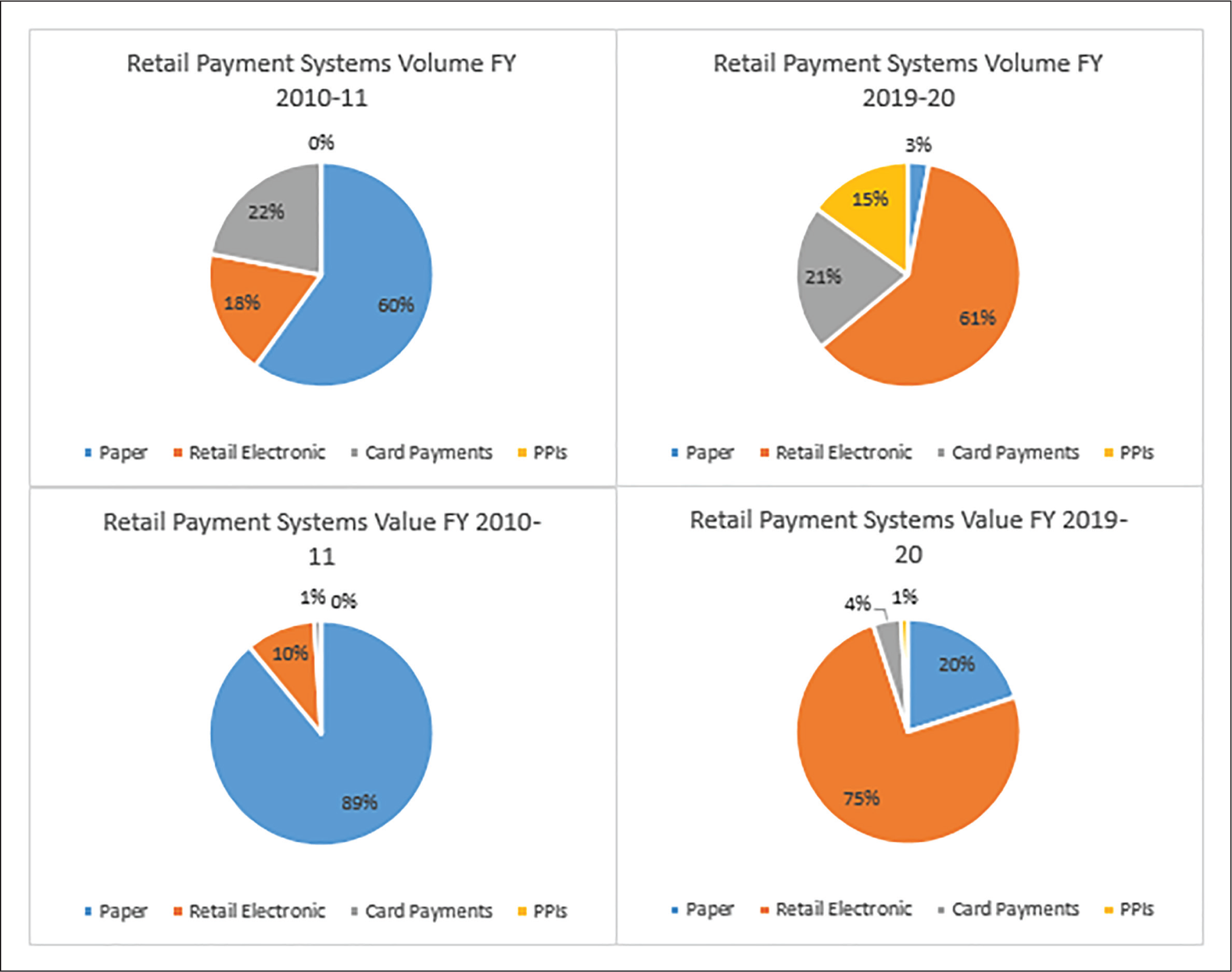

Payment systems are vital in ensuring the reliability, stability, efficiency and accessibility of financial transactions within any country. Throughout history, these systems have progressed from barter systems to the introduction of currency to digital payment systems. This evolution has significantly enhanced the ease of exchanging goods and services. Digital payment systems, in particular, have distorted the way transactions occur by eliminating the reliance on physical currency. Furthermore, the COVID-19 pandemic has significantly fuelled digitalization globally. As physical distancing measures and lockdown restrictions were implemented to curb the spread of the virus, there was a surge in the adoption and usage of digital payment methods. Consumers, merchants and businesses increasingly turned to contactless payments, mobile wallets and online transactions to minimize physical contact and ensure a safer payment experience. This shift has increased transactional efficiency and convenience for customers, as they can now make payments conveniently from the comfort of their homes without needing physical money. These factors have led to the market’s swift adoption of digital payment systems. They have emerged as viable alternatives to traditional forms of payment such as paper, cash, cards and retail electronic-based transactions in India. This trend is evident in Figure 2, which showcases the share of payment systems (RBI, 2021).

These digital initiatives have made banking services more accessible to the general population in India. Over the past decade, the proliferation of digital payments has propelled India to become a global leader in the digital payments landscape, surpassing China in 2017 (CNBC, 2023). The international expansion of UPI-based digital settlements into regions such as Europe, the United States, the Middle East and other parts of Asia and Africa is a testament to this innovative product’s success.

This study focuses on a timely and crucial subject by examining the innovative adoption of digital payments in the banking and monetary transaction payment landscape. The findings related to the diffusion patterns of different payment technologies hold substantial significance for socioeconomic and business realms. By understanding how these technologies are being adopted, the study can shed light on the barriers and gaps that hinder their widespread use. This knowledge is invaluable for policymakers and financial institutions as they can devise targeted strategies to ensure underserved populations can access these innovations.

The remaining sections of the research paper are structured as follows: The next section introduces the research context, theoretical application, data sources, and relevant previous studies. The Methodology section outlines the application and estimation of the Bass diffusion model, which serves as the analytical framework for this study. The Empirical Results section presents numerous compelling findings from the analysis. The Discussion section delves into the significance of these findings and the Implication section summarizes the key application for the current business environment, both in practical and theoretical terms. Finally, this paper summarizes the essential findings and their implications in the Conclusion section. Furthermore, it explores potential future research directions.

Background

Existing literature on the subject has explored various aspects of digital payments and lending, such as their impact on income inequality, financial inclusion and household consumption. However, much of the available research relies on theoretical models, surveys or calculated Fintech indices (Chen et al., 2023; Fahad & Shahid, 2022; Jiao et al., 2021; Palm, 2022; Savitha et al., 2022; Yang & Zhang, 2022). Further, a recent study by Ehret and Olaniyan (2023) analysed the role of mobile payment in addressing the institutional voids in Nigeria.

The payment landscape has continuously evolved since ATMs, online banking and mobile banking emerged. However, introducing digital payments based on the UPI has brought a radical transformation. Despite the transformative impact of Fintech on the financial industry, limited research has focused on investigating the diffusion and adoption of innovation within this ecosystem (Fahad & Shahid, 2022). The relative novelty of the Fintech industry presents challenges in accessing historical data, making it difficult to model the diffusion of innovation accurately. This article aims to bridge this research gap by examining the adoption and diffusion of new-age digital payment instruments in India, utilizing the strategies formulated by Frank Bass in his innovation diffusion theory (Bass, 1969). Additionally, the study identifies indicators associated with adoption rates. It predicts the future utilization of various Fintech payment systems by analysing historical digital payment transaction data and modelling the diffusion properties.

Understanding the rate and pace at which technological innovations diffuse in the digital payment landscape holds tremendous significance for Fintech companies, traditional banks, other financial institutions and regulatory institutions. The diffusion of Fintech innovation has direct and indirect effects, contributing to enhanced overall efficiency in the financial sector and promoting financial inclusion. At the same time, specific existing business models have become obsolete in the payment landscape.

The Bass diffusion model (Bass, 1969) has been widely utilized across various domains to study the adoption and dissemination of innovations. It considers factors such as the innovation’s inherent attractiveness, the influence of early adopters and the cumulative effect of word-of-mouth communication. Over the past five decades, the Bass diffusion model has been extensively applied to analyse adoption rates in numerous industries, providing valuable insights for managers and accurately predicting the rates at which technological innovations are adopted. By fitting the historical payment data to the Bass diffusion model, researchers can estimate the adoption rate and forecast future usage of UPI and BHIM.

By studying the adoption rate and diffusion patterns of UPI and BHIM, researchers can gain insights into the success and impact of these innovations. This information is valuable for business planning, policymaking and understanding the dynamics of the digital payment ecosystem. It allows varied stakeholders, including financial institutions, policymakers and Fintech companies, to make informed decisions and develop strategies based on these payment systems’ adoption trends and potential growth. Hence to analyse the diffusion of innovation, historical payment data has been obtained from the NPCI, the overarching organization responsible for managing various payment systems in India.

Monthly transaction volumes for UPI from July 2016 to October 2022, IMPS from September 2013 to October 2022, and BHIM, NETC FASTAG and *99# from December 2016 to October 2022 have been collected from the NPCI website. They are utilized to model the adoption rate using the Bass diffusion model. This modelling approach helps analyse and understand the rate at which users adopt these payment systems.

Methodology

Bass (1926–2006) was the author of the classical Bass diffusion model after he proposed this in 1969. The model has found its versatile application in various environments. It captures the behavioural aspects such as early and late adopters consistent with adoption, implementation and innovation diffusion. It provides managerial insights as it offers new products’ rate of technological innovation adoption over thousands of industrial applications for the past 50 years. The Bass diffusion model successfully forecasts technological innovations such as Microsoft Windows operating system, Satellite Radio, DirecTV and XM-Sirius (Cosguner & Seetharaman, 2022; Pinto et al., 2022). The significant appealing aspect of the success of the Bass diffusion model is its simplicity and parsimony.

The latest research by Takahashi et al. (2024) deploys the classical Bass diffusion model to analyse and compare the innovation diffusion through search trend and patent. Kumar et al. (2024) investigated the application of the Bass diffusion model within the realm of mobile technology. These recent research highlights the relevance of Bass’s model, despite its age. It retains its status as a foundational theory offering crucial insights into the adoption of innovations. Its significance persists across diverse domains such as technology adoption, healthcare innovations and social media trends. Nevertheless, it is imperative to acknowledge the limitations of Bass’s model when confronted with evolving market dynamics and the digital transformation. Using only two parameters—innovation coefficient and imitation coefficient—it fits a wide range of adoption patterns and influences the market adoption of new product innovation. Using the parameters from Bass diffusion model, the volume of digital payments systems can be predicted. Although forecasting is its primary use, it aids another managerial aspect, such as strategy formulation, by analysing the adoption rate for different digital payment systems. Furthermore, the development stage at which different payment systems at present and future would provide essential insights to policymakers as it determines significant socio-economic change and makes few other products and services obsolete.

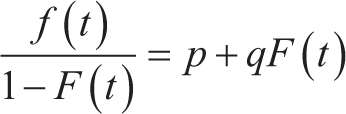

As stated by Bass in 1969, the likelihood of a consumer adopting the new development at time t, within a market size of M consumers, can be quantified using the following equation:

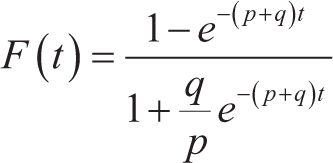

Where p represents the coefficients of innovation and q represents the coefficient of imitations. F(t) is the cumulative distribution function; f(t) is the probability density function characterizing the consumer’s time to adopt a new product through a random variable t, solving the differential equation mentioned above by assuming F(0) = 0 lead to the following equation.

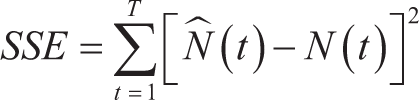

Discrete time intervals such as quarterly, monthly or yearly data are available for digital payment systems. The discrete time version of the Bass diffusion model is estimated using the nonlinear least square method, first proposed by Srinivasan and Mason (1986) by minimizing the following criterion.

Where T stands for the total number of periods, N (t) captures the observed sales at period t, and

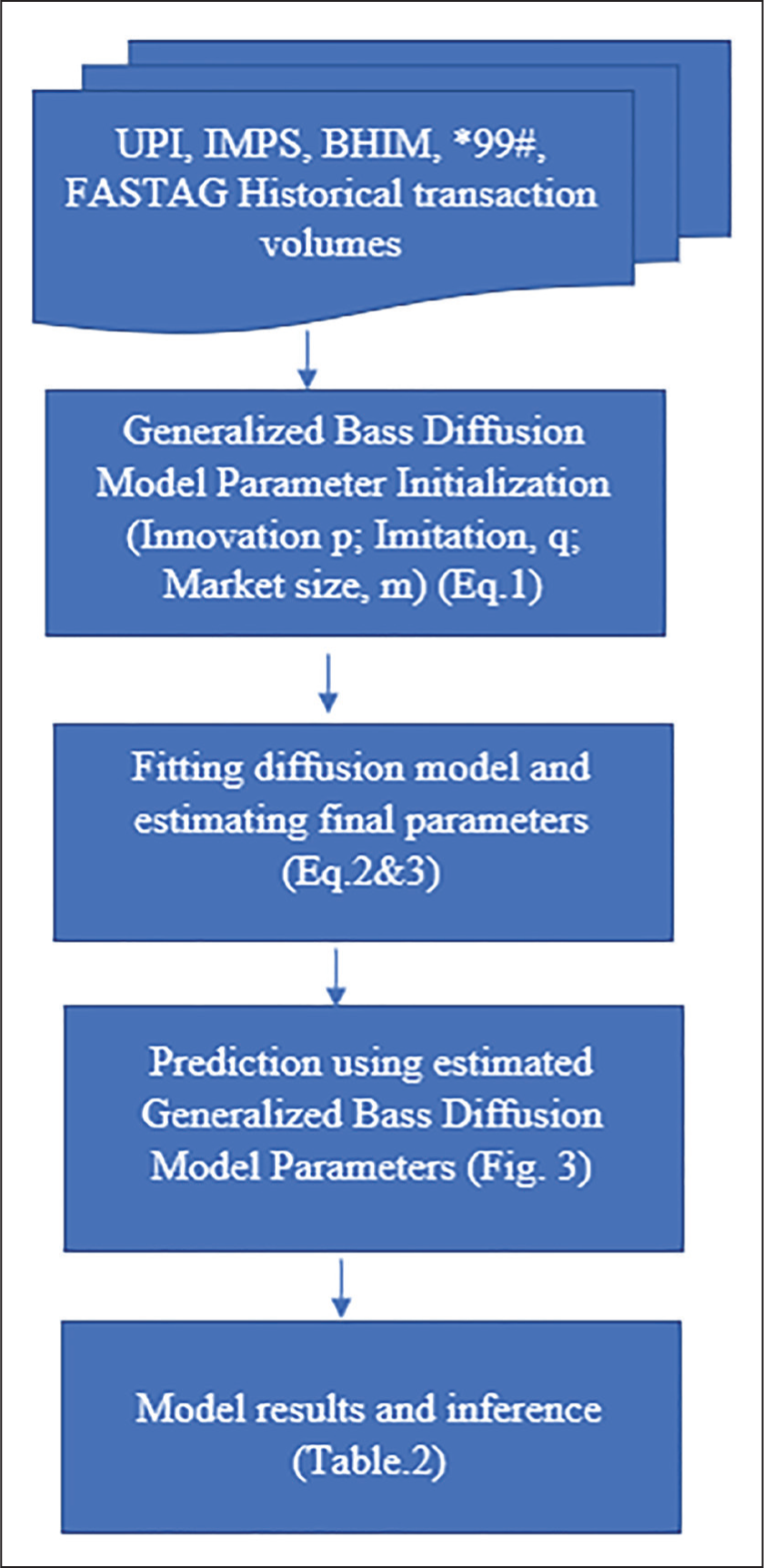

Minimizing the criterion function, as mentioned for sum of squared error (SSE), yields the estimates of p, q and M for new product innovation. The above equation provides the forecasts for any period t, whether in-sample or out-of-sample. The conceptual flow of the model has been presented in Figure 3. There will be no historical data during the introduction of digital payments in other economies. During those scenarios, these coefficients for comparable products can be used as analogues to predict the rate of diffusion initially, then use Bayesian updating for these parameters after the observation of data and eventually rely on historical data once there is substantial new product historical data. Since India is the forefront runner in the digital payment landscape, actual data is made available by NPCI. The same is used to predict the adoption rate for payment systems such as UPI, BHIM, IMPS, *99# and NETC FASTAG.

Generalized Bass Diffusion Model.

Empirical Results

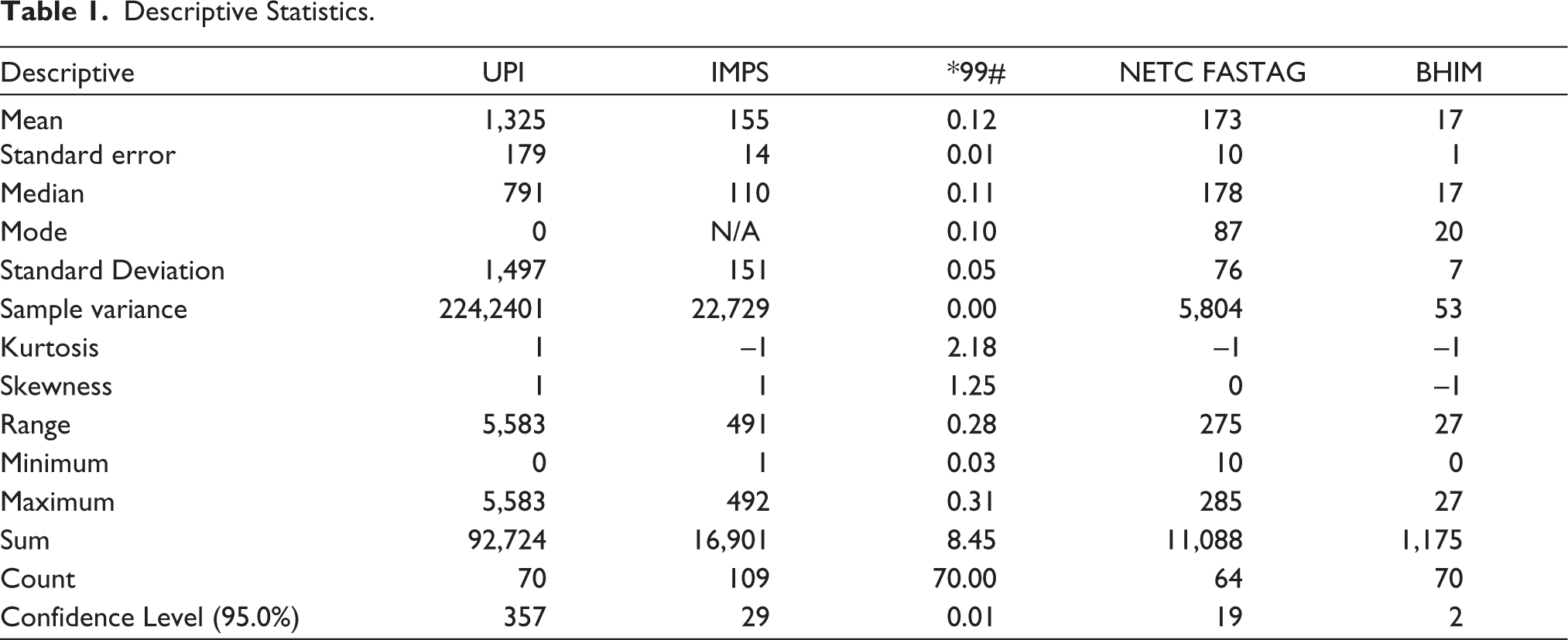

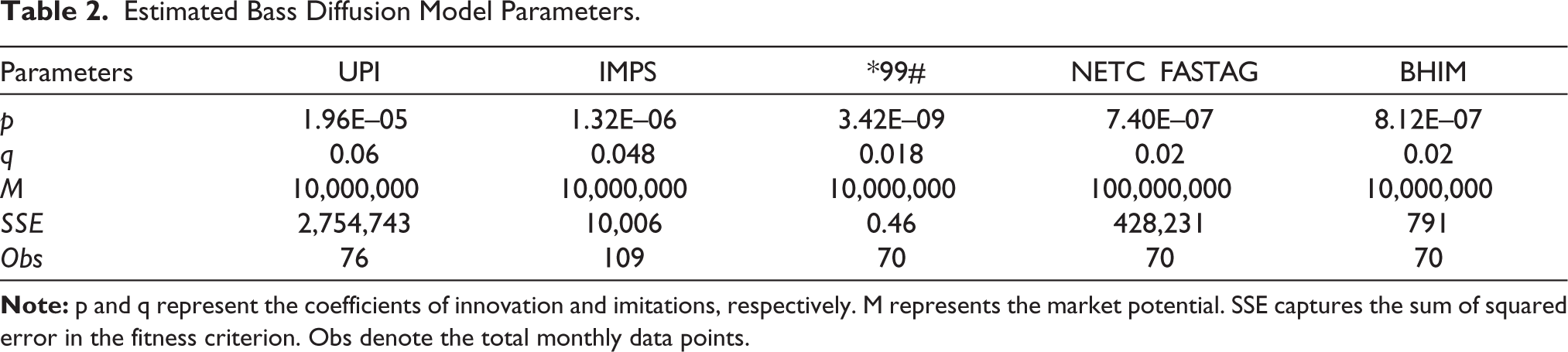

Descriptive statistics for different digital payment systems such as UPI, IMPS, *99#, NETC FASTAG and BHIM have been presented in Table 1. The monthly average number of transactions for UPI has been higher than IMPS, even though IMPS was introduced much earlier and had multi-medium accessibility. The monthly adoption parameters of payment systems such as UPI, IMPS, *99#, BHIM and NETC FASTAG are obtained using the Bass diffusion model. The results of the fitness criterion (sum of squares due to error) and the Bass diffusion model parameters are given in Table 2.

Descriptive Statistics.

Estimated Bass Diffusion Model Parameters.

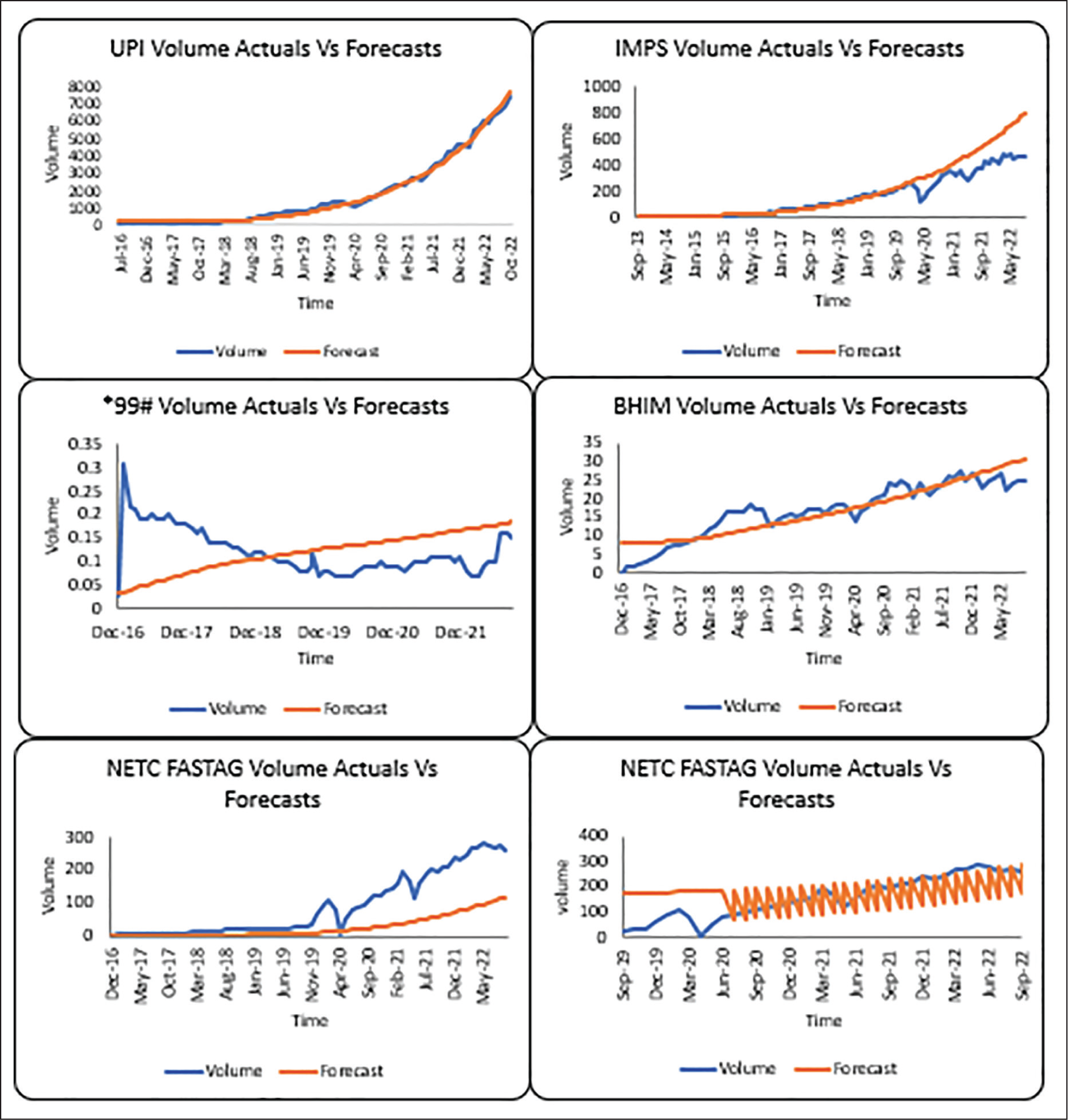

The monthly transaction volume for the various digital payment systems and predicted volume using the Bass diffusion model have been presented in Figure 3. UPI’s transaction volume has witnessed steady growth over the historical period; the Bass model fits well in predicting the UPI transaction volume throughout the sample period. The adoption rates estimated by parameters of innovation and imitation were able to predict the adoption without any structural changes in the pre-COVID-19 and post-COVID-19 scenarios. IMPS, although it was introduced in 2010, much earlier than UPI, has witnessed a sharp decline during the first wave of COVID-19 in 2020. The adoption rates estimated by parameters of innovation and imitation were able to predict the adoption in the pre-COVID-19 scenario better than in the post-COVID-19 scenario. After a sharp decline, the number of transactions through IMPS in the post-COVID-19 scenario failed to regain momentum. There could be various reasons, such as a change in behavioural preference, which needs further investigation. *99#, a payment product that facilitates transactions using a calling option, has yet to witness successful adoption patterns compared to UPI and IMPS. The adoption rates estimated by innovation and imitation parameters could not predict an increase in adoption. BHIM is an app that facilitates payments based on UPI; even though it has witnessed stable growth since its introduction in 2016, demonetization has fuelled its growth since 2016, whereas in the recent period, it has been witnessing a drop-in transaction volume. The adoption rates estimated by parameters of innovation and imitation were able to provide a reasonable prediction.

Digital Payment Products: Prediction vs. Actual Comparison.

However, the competition from other private players such as GPay, PhonePay, and Paytm needs to be investigated further. NETC FASTAG has witnessed massive growth since 2019, except for a drop due to the COVID-19 lockdown. The adoption rates estimated by innovation and imitation parameters were not found to be a suitable prediction model for NETC FASTAG. The actual growth outnumbered the predicted volume due to structural changes in 2019 as the government mandated using NETC FASTAG. So the consumers adopted by force rather than by choice at this point. Hence, using the parameters calibrated post the structural changes after 2020 have been able to fit the transaction volume.

Discussion

The study focuses on an important and current topic, investigating innovation within the banking and monetary transaction system. The research findings related to the diffusion patterns of different payment technologies hold substantial implications. The results from applying the Bass diffusion model offer valuable insights into consumer adoption of digital payments. One noteworthy observation is that the imitation coefficient for these digital products exceeds the innovation coefficient by significant margins. For instance, the imitation coefficient for UPI is 3,071 times higher than the innovation coefficient. Similarly, IMPS, NETC FASTAG and BHIM ratios are 36,020, 26,447, and 24,128, respectively. The ratio for *99# is particularly striking, indicating an imitation coefficient that surpasses the innovation coefficient by a staggering 5,350,883 times. These ratios highlight the strong influence of imitation in driving the adoption of these digital payment technologies.

A larger ratio between the coefficient of imitation and the coefficient of innovation indicates a greater emphasis on imitation than innovation in driving the adoption of products or technologies. The results about the innovation and imitation parameters bear a solid resemblance to Ashokan et al. (2018) adoption parameter findings from his examination of smartphone technology. While it is important to note that this is not a direct comparison due to the differing nature of the products, this represents the most analogous product studied in the literature. The results for UPI suggest that while innovation still plays a role, individuals and organizations have a stronger inclination to adopt or imitate existing products. However, the results for BHIM, NETC FASTAG, IMPS and *99# indicate an even more significant impact of imitation. In the case of *99#, the dominance of imitation in the adoption process is particularly pronounced, overshadowing the role of innovation. Indeed, a higher coefficient of the model suggests that social norms, conformity, or risk aversion significantly influence product adoption.

While the impact of the diffusion parameters is significant, it is essential to recognize that various factors influence successful product adoption. Social, technological, demographical, behavioural, economical and political aspects all play a role in shaping diffusion dynamics (Dash et al., 2023; Lohana & Roy, 2023; Singh et al., 2020). In the context of the study period, there were several consequential events in India across these domains that likely influenced the patterns of adoption. One notable event was the implementation of demonetization on 8 November 2016, which involved the withdrawal of legal tender status for specific currency notes and aimed to promote a cashless economy. This event led to increased utilization of digital financial services, as evidenced by the rise in transaction volumes for existing products such as UPI and IMPS. However, it is essential to note that the impact of products introduced after demonetization could not be measured within the study period, and their influence on adoption patterns may extend beyond the scope of this study. This analysis allows for a more nuanced understanding of the diffusion dynamics and the broader context that shapes product adoption.

Implication

This research has significant business and policy implications, as the model demarcates the adoption life cycle of digital payment technologies from early adopters to the majority and laggards. It provides regulators, such as the RBI and the Government of India’s Ministry of Electronics and Information Technology, with predictive insights into adoption rates and patterns. The Government of India has implemented various measures to discourage large-scale cash payments. The Income Tax Act includes provisions to promote digital payments and prevent cash transactions. Additionally, several sectors and government agencies have made it mandatory to accept digital payments. For example, toll collection on highways, government welfare schemes, utility bill payments and specific merchant categories are required to offer digital payment options. Understanding these patterns is crucial for timing the introduction of regulations that can facilitate a smooth transition to digital payments, address cybersecurity risks, ensure the interoperability of payment systems and promote financial inclusion. For example, the fast acceptance from early adopters might necessitate early regulatory interventions to prevent fraud and protect consumers’ data privacy. Conversely, as the majority begin to adopt digital payments, regulations might focus on enhancing digital literacy to prevent the digital divide and ensure that payment systems are robust and scalable.

Financial institutions and Fintech companies, on the other hand, can use the model’s insights to customize their marketing campaigns, create consumer education programmes specifically targeted at them and create products tailored to the different demands of early adopters compared to the majority who embrace later. This model enables businesses to strategize their market entry and product offerings more effectively by providing a structured framework to forecast the adoption rates of digital payments. Additionally, the model’s predictive capability can guide infrastructure investments, ensuring that the necessary digital and financial infrastructure is scaled appropriately to handle the growth in digital transactions.

When studying the adoption and diffusion of digital technologies, researchers and practitioners have access to various theories that can comprehensively understand this complex process. This research results provide insights into approaches including innovation diffusion theory, technology adoption theory (Rogers, 2003), digital transformation theory (Hess et al., 2016) and institutional theory (DiMaggio & Powell, 1983) and its application to digital payments. Innovation diffusion theory helps explain how innovations spread among individuals and groups. Technology adoption theory sheds light on the factors that facilitate or hinder the acceptance and diffusion of innovations. Digital transformation theory provides insights into how organizations can leverage digital technologies to transform their operations, strategies and customer interactions. Institutional theory emphasizes the role of institutions in addressing institutional voids.

Integrating these theories can offer a deeper understanding of the interplay between institutional factors, organizational responses, individual acceptance and overall consumer behavioural patterns. Recognizing that adopting innovations is influenced by complex and multifaceted factors is crucial, as discussed in this research. Moreover, these factors interact and can vary across countries, regions and user segments. Future research could explore these aspects to provide valuable insights for organizations, governments and industry stakeholders. This knowledge can be used to promote widespread adoption and acceptance of digital payments, fostering economic growth, efficiency and transparency in financial transactions.

Conclusion

This study uses the Bass diffusion model to examine the adoption of innovative digital payment products in India. The research finds that the coefficient of imitation is higher than that of innovation, indicating a slow initial adoption followed by acceleration across digital payment products. UPI is the most successfully adopted product with a higher imitation coefficient than other digital payment products. The Bass diffusion model also accurately predicts the adoption of UPI and IMPS payment systems in pre-COVID-19 scenarios. However, in the post-COVID-19 period, the actual adoption of IMPS is lower than forecasted, indicating slower recovery. BHIM shows steady adoption, while *99# has limited growth. NETC FASTAG demonstrates remarkable growth, with a temporary decline during COVID-19 lockdowns. These findings offered multifaceted insights into innovation diffusion theories and their application in the digital payment landscape. These insights help understand the dynamics of digital payment adoption patterns across different products and offer predictions and estimations of market potential. These findings underscore the continued relevance and utility of the Bass diffusion model for estimating adoption rates, analysing market potential, informing business planning, shaping economic policymaking and providing managerial insights for financial institutions. Additionally, these results offer valuable insights to international regions considering the introduction of UPI-based payment systems, enabling them to assess the potential demand and adoption rate in their respective markets. Future research on digital payment innovation adoption can focus on understanding adoption factors within the realm of the diffusion model, analysing user experience and security features, studying transactional analysis to prevent fraudulent transactions, exploring behavioural economics, conducting cross- cultural studies, examining emerging technologies and evaluating policy implications.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.