Abstract

The case introduces the situation of HSE, a mid-sized German utilities company and leading provider of green energy in the year 2014. The German energy industry used to be very traditional with low levels of innovation. This changed with a major deregulation of the market in 1998, which subsequently led to a severe market shake-up. Established players encountered significant challenges and new players saw chances to enter the market. After the deregulation, HSE successfully transitioned from a regional energy provider operating in a secure and regulated monopoly to a successful nationwide player investing in green energy production. Thus, the company seemed well suited to adapt to the next major disruption in the market: the Energiewende. This term describes Germany’s transition to a sustainable energy system. The German government introduced several regulatory measures to boost green energy; however, details of these regulations changed frequently so that it was difficult for companies to predict future developments and also HSE suffered from these uncertainties. The case describes this situation, the company’s many efforts in sustainability, its situation as a leading provider of green energy and the strategic and operational challenges it faces in terms of regulation, market demand, product differentiation and strategic choice.

Introduction 2

The jury recognizes the exemplary and consistent strategy with goals that were repeatedly outperformed and a clear positioning of the company. (Deutscher Nachhaltigkeitspreis, 2013)

What an achievement! In November 2013, the utility company HSE (HEAG Südhessische Energie) AG received the German Sustainability Award, the country’s most prestigious award of its kind, in the category ‘Germany’s Most Sustainable Corporate Strategy’. A few months later, chief executive officer (CEO) Dr Marie-Luise Wolff-Hertwig still regularly marvelled at the award, which occupied a prime spot in her office. Following the deregulation of the German energy market in the late 1990s, the company developed from a regional municipal utility company in the area of Darmstadt, a mid-sized town south of Frankfurt, to Germany’s second largest provider of clean energy and its largest provider of carbon-neutral natural gas.

However, Dr Wolff-Hertwig realized that this was not the time to rest on their laurels. Despite its past success, the company was facing some tough challenges. Following the initial years of the Energiewende—Germany’s state-mandated transition towards a sustainable economy by means of renewable energy—numerous competitors had entered the market and offered some form of carbon-neutral energy. Despite being one of the first movers, it was difficult for HSE to distinguish its highly sustainable products from less sustainable alternatives. Transparency was low, and the customers were seldom aware of the quality differences in the eco-energy market. Moreover, despite (or may be even due to) being a top priority for the government, regulations in energy policy were unpredictable. In 2013, for example, HSE finished building a new plant with two highly efficient gas turbines. Such turbines were regarded as an environmentally friendly solution to bridge the short-term slacks in renewable energy production when, for example, the sun was not shining or the wind was not blowing. Many actors expected the government to present favourable regulations for such facilities. However, they were never put into practice, so the turbine became a financial burden. It ran only a few hours each year because it operated with higher variable cost compared, for example, to old, highly polluting coal power plants of other companies that had been depreciated years ago.

Moreover, there had been a number of significant internal developments. Not only had the ownership structure changed after E.ON, one of the Germany’s largest energy conglomerates, sold its 40 per cent share to the city of Darmstadt, thus making the company completely owned by local (public) shareholders, but the company board had seen frequent modifications as well. Dr Wolff-Hertwig, who had taken over as a CEO only a few months ago, and her colleagues were searching for a path to steer past the various hurdles into calmer waters.

Deregulation and the Energiewende: The Changing Landscape in the German Energy Sector

Two relatively recent historic developments characterized the German energy market in 2014: the market liberalization in 1998 and the implementation of the Energiewende as an ongoing and politically influenced process towards a sustainable economy.

Turning Point Deregulation: Development of the Energy Sector in Germany

For decades, monopolistic structures characterized the energy sector in Germany, resulting in comfortable situations for the established energy providers. Vertically integrated companies dominated the industry. They owned not only the power plants but also the grids to supply the end consumers (Sachverständigenrat zur Begutachtung der gesamtwirtschaftlichen Entwicklung, 2011). This changed with the liberalization and deregulation of the German energy sector in 1998. From then on, customers were generally free to choose their energy provider. A new law forced a separation of the network business from the production and distribution of energy (the so-called unbundling). Furthermore, the grid owners had to open their power lines for other suppliers so that every energy provider could offer electricity throughout Germany. This completely changed the structure of the energy sector and forced energy companies to entirely re-evaluate their strategies. Beforehand, investments were relatively safe because firms could rely on a steady monopoly rent. The new situation, however, demanded anticipation and creativity to be successful in the market.

Following the deregulation, competition increased and energy prices dropped dramatically in 1998, only to recover soon after. Nevertheless, in 2011, the price of electricity was only 5 per cent higher than in 1998—a relatively low increase when compared to the general inflation. The German electricity grid was considered to be the most reliable in Europe. On average, consumers experienced power failures for only 16 minutes in an entire year (Bundesnetzagentur, 2013).

The Energiewende: Clean Energy for an Entire Country?

Almost simultaneously with the deregulation, another major change in the German energy sector was initiated: the Energiewende (energy transition). This now famous word describes the quest for an economy based on renewable instead of fossil and nuclear fuel energy. The aim was to produce 35 per cent of all energy sustainably until 2020 and 80 per cent until 2050 (Bundesministerium für Wirtschaft und Technologie, 2010). However, the road that led to the Energiewende was not always straight. Different governments changed regulations several times, and amendments were not always congruent. One example was the different dates for the nuclear phase out. Initially announced by the coalition of the Social Democratic Party and the Greens in 2001, nuclear power plants were supposed to shut down in roughly 20 years (Frankfurter Allgemeine Zeitung, 2015). At the end of 2010, the Conservative–Liberal coalition then decided to postpone the nuclear phase out significantly (TAZ, 2010). However, the nuclear catastrophe in Fukushima (Japan) 3 in March 2011 led to another sudden change in energy policy: following a security check of all German nuclear power plants and a temporary shutdown of the seven oldest facilities, a definite exit until 2022 was decided (Sachverständigenrat zur Begutachtung der gesamtwirtschaftlichen Entwicklung, 2011). Similar to the nuclear phase out, the regulations promoting renewable energy also saw several changes in 2004, 2009, 2012 and 2014 mainly in terms of reduced rates for the fixed compensation for green energy fed to the grid, which were first introduced in 2000 to improve predictability for investors (Bundesverband für Energie- und Wasserwirtschaft e.V., 2014).

One reason for the ongoing changes was the success of the so-called Renewable Energy Sources Act (Maubach, 2013) in boosting renewable energy in Germany. From 2000 to 2014, the quota of renewable energy of total energy consumption increased from 6.2 to 26.2 per cent (AG Energiebilanz e.V., n.d.). This led to an increase in total energy prices because the fixed compensation for renewable energy was financed by allocating the costs to the customers. 4 Consequently, less than a third of the price for electric energy in 2013 was determined by the market. Almost half of the price was state-induced costs and the rest grid fees (Bundesministerium für Wirtschaft und Energie, n.d.b). Interestingly, while the total energy cost rose to 29 Cent/kWh on average for private households in 2013, the part of the price that was determined on the spot market actually declined significantly due to the extensive supply of renewables, which can be explained by the merit-order effect (Sensfuß, Ragwitz & Genoese, 2008). The merit order ranks sources of energy according to their short-term marginal costs of production. The sources with the least marginal cost are the first to satisfy demand. Marginal costs of renewable energy sources are near zero because once they are built, they do not need fuel to run. The sources with the highest marginal cost (usually gas turbines) are therefore crowded out. This led to a problem for the Energiewende and for the goal of decreasing greenhouse gas emissions. Due to the highly fluctuating character of wind and solar energy, the industry had to hold sufficient capacity from non-renewable sources in order to constantly satisfy demand. Gas turbines were regarded as an attractive solution because they are flexible and also emit much less CO2compared to coal power plants; so many actors expected the government to support energy from gas turbines. However, no such regulation activity occurred, therefore preventing gas turbines from running profitably due to their relatively high variable cost and despite the fact that they required only comparably low initial investments (the problem was increased by falling prices for CO2 certificates, which made power from climate-damaging coal energy comparably even less expensive) (Krizikalla, Achner & Brühl, 2013).

The Current Market Situation

Small Companies, Mid-sized Players and Big Tankers: The Competitive Situation 5

In total, the gross electric energy production of Germany reached 633.2 TWh 6 in 2013 (Statistisches Bundesamt, 2015). Households and small businesses (consuming less than 10 MWh per year) accounted for 24.8 per cent of total energy consumption, medium-sized consumers (10 MWh to 2 GWh) for 26.9 per cent and large industrial consumers (> 2 GWh) for 48.3 per cent. Generally, one has to distinguish between producers and distributors of electric energy. Often, companies were active in both areas. In 2013, about 300 companies were active in producing electricity, and roughly 1,100 distributors sold it to the consumers. Furthermore, quite a few large industrial energy consumers at least partly engaged in producing electricity in their own facilities, and a significant number of households installed decentralized renewable energy sources, especially rooftop photovoltaic solar panels, in order to produce electricity.

The average private household could choose amongst 72 different electricity providers and industrial clients amongst almost 90 that were active in their region. Those distributing companies that were selling more energy than they produced either directly bought energy from producers in Germany and abroad or from the spot market usually through the European Energy Exchange (EEX) in Leipzig, Germany. Despite the increasing competition following the deregulation some 15 years ago, the large players still heavily influenced the market although their market share was quickly decreasing. The ‘big four’—RWE, E.ON, Vattenfall and EnBW—supplied 43.5 per cent of the total energy used by households and small businesses, 29.5 per cent used by medium-sized consumers, and 55.4 per cent used by large industrial consumers. However, deregulation and the Energiewende meant tough times for these big tankers and all of them had to rethink their business models more or less drastically (following Fukushima, RWE and E.ON, for example, announced that they would cut 13,000 and 11,000 jobs, respectively; cf. Hoffmann, 2013). Further, not only was the market for electricity deregulated and increasingly fragmented but also the gas energy market counted 850 distributors, making it the most fragmented in Europe. The market share of the five largest distributors totalled 44.3 per cent, with E.ON being the biggest fish (2013 total revenues € 122 billion, electricity sales 704 TWh, gas sales 1,091 TWh) (E.ON, 2014).

Apart from the big four, there were a couple of mid-sized players, as well as an abundance of smaller municipal energy suppliers (roughly 800), smaller private energy suppliers (roughly 100) and distributors that specialized in green energy (roughly 150). In 2009, eight of the mid-sized municipal energy suppliers formed a loose alliance (‘8KU’

7

) aiming at improving their market position and increasing their market share, especially for renewable energy:

8

Enercity (revenues € 2.45 billion in 2013, electricity sales 16.4 TWh, gas sales 21.7 TWh) HSE (€ 1.91 billion, electricity 6.1 TWh, gas 8.9 TWh) Mainova (€ 2.21 billion, electricity 11.0 TWh, gas 15.2 TWh) MVV Energie (€ 4.0 billion, electricity 25.8 TWh, gas 25.1 TWh) N-ERGIE (€ 2.24 billion, electricity 13.7 TWh, gas 9.5 TWh) RheinEnergie AG (€ 2.55 billion, electricity 14.6 TWh, gas 8.1 TWh) Stadtwerke Leipzig (€ 3.38 billion, electricity 55.1 TWh, gas 5.6 TWh) Stadtwerke München (€ 6.3 billion, electricity 17.6 TWh, gas 99.1 TWh)

However, a part of the mentioned revenues also came from operating local grids and from a full portfolio of products, such as, water, telecommunications or public transport, stemming from their historical roots as regional full-service suppliers.

Still a Niche? Green Energy in Germany

Before the Fukushima catastrophe, green energy was merely a niche in the German energy sector. After the incident, however, the number of companies offering some sort of green energy increased dramatically. In 2013, 24.1 per cent of all electricity produced in Germany came from renewable energy sources. Over the years, the green energy sector became a major economic power in Germany. A closer look at the numbers revealed some drastic changes: While the conventional energy sector shrank from almost 570,000 employees in 1991 to merely 220,000 in 2013, the entire renewable energy sector grew from virtually nothing to more than 370,000 employees in 2013 (Bundesministerium für Wirtschaft und Energie, n.d.a).

In the beginning, a few eco-pioneers, such as, the Elektrizitätswerke Schönau, Lichtblick, Greenpeace Energy and Naturstrom AG, all founded already in the mid- to late 1990s, shaped the market. In 2013, already 832 of all 1,100 energy distributors (including the big four) offered green energy (Heide, 2013). Interestingly, the big players did not dominate this market. In 2012, the largest supplier (in terms customers numbers) was Lichtblick (485,000 customers), followed by the HSE subsidiary ENTEGA (376,000) and Naturstrom (240,000). All of these companies, however, had either lost customers in the previous years or at least were not able to increase their customer base any longer. This was attributed not only to the increasing competition but also to the ambiguous transparency of the market. In terms of price, customers could easily compare different offers using several independent online comparison sites. But also, the quality of green energy differed significantly and information on quality was much less transparent. Ambitious providers of green energy, for example, often did not buy electricity at the EEX, but rather did so directly from the source so that the origin of the energy was traceable. Furthermore, they also actively advanced the development of renewable energy by investing in wind farms, biogas facilities, solar parks and so on, while others simply bought certified electricity without further investing into new renewable energy sources (Stiftung Warentest, 2012). Theoretically, there were numerous labels identifying different qualities of green energy. However, the end consumer was seldom able to distinguish between stronger (e.g., the OK-power label and the Grüner Strom label) and weaker labels (e.g., the European Renewable Energy Certificate System (RECS) certificate). Apart from the source of the energy, customers often looked for further quality indicators. Many, for example, valued a 12-month price guarantee, an easy and a fast change of service provider, and a short minimum contract term and cancellation period.

Next to the business-to-consumer (B2C) segment, the business-to-business (B2B) area also proved to be of growing importance for providers of green energy. A significant number of companies not only looked for clean energy but also for other ways to improve their own carbon footprint, however, usually without much internal knowledge on how to do so. Apart from sustainability reasons, economic reasons also drove companies because a reduced carbon footprint usually came with a significantly reduced energy bill or other benefits, such as, an improved image or compliance with customer standards and demands.

HSE: The Sustainable Energy Company

Company with Tradition: Historic Roots and Recent Developments

HSE can trace its roots back through more than 150 years of history (see HEAG, 2012). At the end of 2012, HSE employed about 2,600 people (HSE, 2013b). Already in 1999, the HEAG Versorgungs-AG established the ‘NATURpur Energie AG’ and the ‘ENTEGA Vertriebsgesellschaft’ (Entega). This step was regarded as a first major change in the HSE business philosophy towards sustainability. The NATURpur Energie AG acted as a producer of green energy, and ENTEGA became the distributing branch of the company. Since 2008, long before Fukushima, ENTEGA exclusively provided green energy to its customers (HSE, 2013b). Consequently, HSE also announced its goal to invest € 1 billion in renewable energy until 2015, as described by the former CEO Albert Filbert: ‘We invest on a large scale in renewable energy and efficient cogeneration of heat and power’ (HSE, 2011, p. 13).

Also in 2008, the ‘NATURpur Institut für Klima- und Umweltschutz GmbH’ was founded with the mission of supporting research and development for clean energy. The NATURpur Energie AG and the ‘HSE Regenerativ GmbH’ (added in 2009) now bundled the competencies for planning, building and operating renewable energy power plants. Markus Horn, managing director of HSE Regenerativ, explained the benefits: ‘Previously, we bought turnkey wind farms. Nowadays, we have the knowhow in house to develop and implement the farms from scratch together with our partners generating a higher share of added value in the company’ (HSE, 2013b, pp. 31–32). Also since 2009, HSE has held a minority stake in the ‘Forest Carbon Group’ (49.85 per cent in 2013). This subsidiary invested in reforestation projects and used the generated emission certificates to set off CO2 emissions, for example, of industrial clients. In 2011, HSE acquired BLUENORM, a company that specialized in consulting services for energy efficiency and complemented the portfolio of the existing subsidiary ‘ENTEGA Energieeffizienz’.

Some Recent Internal Changes: Ownership and Board Structure

Since the foundation in its modern form in 2003, a majority share of HSE belonged to the city of Darmstadt (together with the municipal savings bank). In 2003, they owned 52.9 per cent of the company through its ‘HEAG Holding AG’. Other shareholders were the ‘Ruhrgas Energie Beteiligungs-AG’ (21.3 per cent), the energy giant E.ON (18.7 per cent) and regional counties, municipalities and other shareholders (7.1 per cent) (HSE, 2004). In 2005, E.ON acquired the shares of Ruhrgas, thus increasing its stake to 40 per cent. Only seven years later, E.ON decided to sell its shares. On 21 June 2012, the HEAG Holding AG acquired the shares for € 280 million, mainly financed through credit (Stadt Darmstadt, 2013). Thus, HSE was now again completely owned by the city of Darmstadt and other regional municipalities.

In addition to the ownership, the board was also subject to some major shake-ups in the recent past. In 2011 and 2012, the chief technology officer (CTO) Dr Ulrich Wawrzik and CEO Albert Filbert resigned (HSE, 2012a). Christine Scheel, a former member of the German Bundestag for the Green Party joined the board. She left after a few months due to differences on the strategic course of HSE. In the same year, another board member (Holger Mayer) also left the company. They were replaced by two interim board members. In 2013, the appointments of Dr Marie-Luise Wolff-Hertwig as CEO and Dr Kristian Kassebohm as CFO led to a permanent solution (HSE, 2013b). Andreas Niedermaier, who has held his post on the board since 2010, completed the three-person board.

Business Areas, Products, Markets

The structure and strategy of HSE as a sustainability company rested on three pillars: delivering sustainable energy (avoid CO2), energy efficiency (reduce CO2) and carbon offsetting (compensate CO2). Through vertical integration, the company was active in all major steps of the value chain. The company was separated into six business units covering the entire scope of an energy and infrastructure company. The non-profit ‘HSE Stiftung’ (HSE foundation) and the ‘NATURpur Institut’, which engaged in research and development in the area of climate and environmental protection, complemented the picture.

Electricity production. Since its strategic change towards sustainability, HSE increasingly invested in renewable energy. In 2009, the company announced a € 1 billion investment programme aimed at producing 100 per cent of its renewable energy sales to private households in own renewable energy facilities until 2015 (HEAG, 2010). Until 2012, € 843 million were already invested in renewable energy facilities (see Appendix 1). In total, this was enough to supply 245,000 households with renewable energy (HSE, 2013b). Additionally, the company owned conventional power plants in order to balance short-term fluctuations: a gas turbine plant in Darmstadt (100 MW, operating since 2013) and a 9 per cent stake in a gas turbine plant in Irsching near Munich (total 876 MW, HSE stake 79 MW, operating since 2010). These two, however, could not be operated profitably in 2013.

Distribution. One of the most important subsidiaries of HSE was ENTEGA, its distribution branch for private and business customers. In 2013, Germany’s second largest provider of sustainable energy served 376,000 households with clean electricity. However, the customer base had already been shrinking for the second year in a row. On the other hand, the number of commercial customers had increased. Despite slightly reduced total electricity sales, the sales of renewable energy thus increased to 37 per cent of all electricity sold (Appendix 2) (HSE, 2013a). ENTEGA was also active on the gas market. With 110,000 customers, ENTEGA was the largest provider of carbon-neutral gas in Germany (HSE, 2012c). The company’s total share of sales for carbon-neutral gas was 30 per cent. Carbon neutrality was achieved through reforestation projects of the Forest Carbon Group, which also offered its services to other clients to compensate their CO2 emissions. Further products offered by subsidiaries were, for example, energy efficiency services, drinking water and thermal heat.

Construction and operation. This business area included the planning, construction and operation of infrastructure and grids, environmentally friendly energy facilities, air conditioning and refrigeration technique and the construction or modification of buildings and facilities in order to achieve energy efficiency.

Telecommunication. HSE offered broadband internet access and individual communication services in the Darmstadt area. Furthermore, it offered metering, claims management and associated information technology (IT) services.

Waste management. Also in the region of Darmstadt, HSE offered wastewater treatment and waste management to the municipalities. Waste was turned to energy in a waste-to-energy plant operated (but not owned) by HSE.

Grids. A subsidiary of HSE planned, built and operated the electricity grid, the gas distribution system and the water network in and around Darmstadt.

Sustainability at HSE

The 2013 German Sustainability Award was only the most recent in a series of praises for HSE. Already in 2012, for example, ENTEGA was nominated as one of Germany’s Most Sustainable Brands, and in 2011, it received a nomination for Germany’s most recycling paper friendly company (Deutscher Nachhaltigkeitspreis, n.d.). Over the years, sustainability had indeed become part of the genes of the company. In 2007, the company offered its first product for pure renewable energy, and one year later, it completely banned nuclear energy from its mix, announced its ambitious investment programme into renewables and offered solely green energy to new private household customers (HSE, 2013b). In 2009, the first carbon-neutral gas tariff compensated CO2 with certificates from the Forest Carbon Group. Apart from clean energy, HSE—through its subsidiary ENTEGA—also offered energy-efficiency services and solutions for CO2compensation. However, with such an ambitious programme, some setbacks were inevitable. In 2013, for example, the company felt that it was necessary to reintroduce a conventional gas tariff offered next to its eco-gas tariffs to cater to its economic reality.

Nevertheless, the company saw itself as a pioneer and invested in research and development as well as in public awareness building. The ‘NATURpur Institut’ cooperated closely with universities on research on smart grids, e-mobility or energy storage (HSE, n.d.). Furthermore, the institute organized, for example, the so-called Future Energy Dialogue, connecting experts from politics, business and society.Since 2009, ENTEGA was the main sponsor of the soccer club ‘1. FSV Mainz 05’. Not only the company name was present on the jerseys but the company also supplied the club with clean energy and consulted with it to become the first carbon-neutral club in the Bundesliga, Germany’s famous soccer league. HSE also used this channel for numerous activities in order to familiarize the fans with climate change issues. In a similar way, local sports clubs were sponsored by installing solar panels or other features. To sensitize the population, ENTEGA also used its initiative ‘Denkanstöße’ (roughly translated: ‘food for thought’). On one occasion, for example, citizens of Berlin built hundreds of snowmen for what was titled a ‘snowmen rally’. These snowmen ‘demonstrated’ against climate change and environmental pollution, holding signs, such as, ‘Help!’, ‘Some like it cold’ or ‘Save the snowmen’ (Utopia, 2010). Other creative campaigns followed.

Despite the frivolity, HSE was serious about sustainability. HSE implemented an environmental policy that sought to significantly reduce environmental impact as well as a strict code of conduct and a supplier management, which included social and ecological criteria (HSE, 2013a). A CO2 cap for company cars was set, waste and recycling quotas were monitored, all printed articles were carbon-neutral and used recycled paper, and so on. The company implemented quality, environmental and energy management systems, such as, ISO 9001, ISO 14001, EMAS and ISO 50001. Apart from the mostly ecological aspects, social sustainability was high on the agenda as well. The company positioned itself as an attractive employer, for example, with extensive corporate health management, lifelong learning programmes and an open dialogue between management and the workforce (HSE, 2012b).

Furthermore, HSE aimed at an intensive exchange with its stakeholders. This was done through the aforementioned communication channels as well as, for example, through a customer and a stakeholder advisory board. The company actively signalled its sustainability focus as a signee of the United Nations (UN) Global Compact, the Clean Development Project (CDP) Initiative for mid-sized companies, the German Corporate Governance Code and the German Sustainability Code. It regularly published a comprehensive and externally assured sustainability report according to the guidelines by the Global Reporting Initiative, which was fed with data from its company-wide sustainability management, including 60 ‘sustainability ambassadors’ that were appointed throughout the company.

The Financial Situation: Bright Past and Bumpy Future?

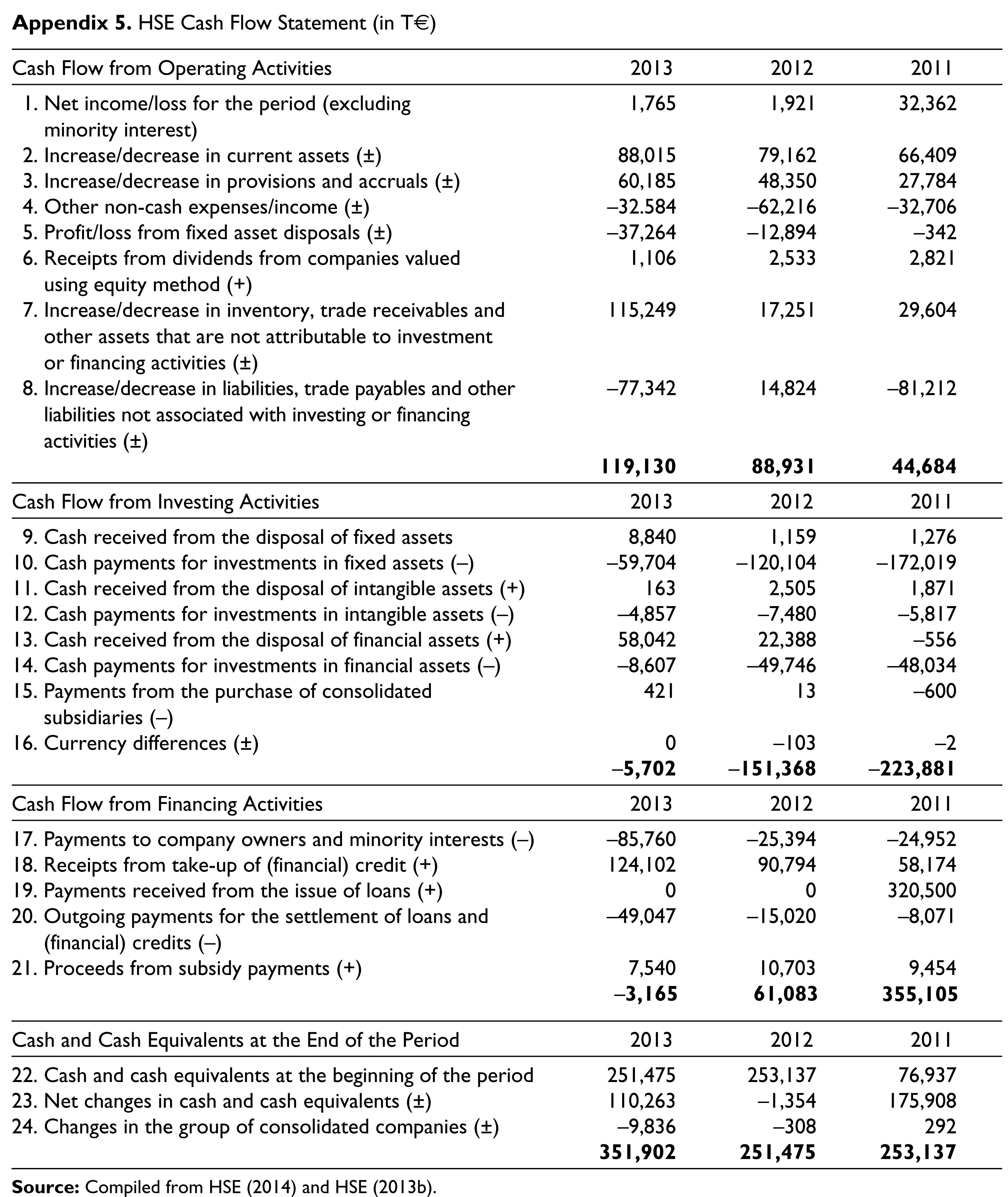

The year 2012 was an intense year for HSE. Revenues shrank slightly from € 2.3 billion in 2011 to € 1.97 billion, and profit fell dramatically from € 32.36 million (EBITDA € 141.5 million) to only € 1.92 million (EBITDA € 134 million) (Appendices 3, 4 and 5) (financials in this paragraph retrieved from HSE, 2013d; HSE, 2013b). This slump was mainly due to a few specific events. For example, the tax burden in 2011 was € 8 million less because of unique single events, and the company had to make extraordinary depreciations in 2012 of € 10 million and € 8 million for the gas turbines in Darmstadt and Irsching, respectively (the initial total investments amounted to € 55 million for the Darmstadt power plant and € 400 million for the entire Irsching plant, of which HSE owned 9 per cent). Finally, the company had to make a provision of € 8 million for pending water cartel proceedings. Despite the unsatisfactory results, the company was able to pay its shareholders a special dividend of € 85.54 million by cutting back on retained earnings and by distributing earnings from a capital decrease at its grid subsidiary. This dividend was highly appreciated by the public shareholders because the city of Darmstadt mostly debt-financed the buying of the E.ON shares, and the city was highly indebted. Dr Wolff-Hertwig, however, made clear that this was considered a one-time event: ‘The special dividend is an exception and we will return to a level of dividends that is usual for HSE’ (HSE, 2013d).

In 2013, revenues (€ 1.91 billion) and profit (€ 1.77 million) stayed on the 2012 level and no dividend was paid (HSE, 2014). The investment in the gas turbine in Darmstadt had again to be depreciated by € 27 million. During the last year, the company introduced a package of more than 300 measures with the aim to achieve cost savings and growth. First results manifested in an increased cash flow from operating activities of € 119.1 million (up from € 88.9 million in 2012 and € 44.7 million in 2011). Since 2008, € 843 million had already been invested in renewable energies so that the company almost reached its 2015 target of € 1 billion. Thus, HSE had an investment quota in renewables of 8.55 per cent of total revenues. One major investment that was supposed to bear fruit quickly was, for example, the 24.9 per cent stake in the offshore wind farm Global Tech I. ‘With our share alone, we expect to be able to supply 115,000 households with green energy starting in spring 2014,’ Dr Wolff-Hertwig explained (HSE, 2013d).

Rethinking the Challenges Ahead

Dr Wolff-Hertwig looked through her window down on the brand new gas turbine power plant. For a technophile, this was actually a nice view. From a business perspective, however, it made for a rather troublesome issue. Anticipated regulations favouring gas turbines had not been implemented thus far, and it was doubtful whether politics would change that soon so that this efficient technology could currently not be operated profitably. This let Dr Wolff-Hertwig once again to think about the general path of HSE. How could HSE continue to successfully follow the sustainability path?

Yes, it seems as though there was an ever-growing number of people interested in green electricity and carbon-neutral gas. Despite various hurdles, Germany’s population was generally still in favour of the Energiewende, and sustainability was an ever-growing issue. However, this favourable environment brought an increasing number of competitors to the field. Dr Christian Jungbluth, Managing Director of ‘ENTEGA Energieeffizienz’, was convinced of the quality of HSE:

We decided years ago that we did not want to pursue a fig leaf policy, but instead go for a sustainable energy supply. This is our unique selling proposition amongst all the green alibi offers that are on the market nowadays and that are not so green any more upon closer inspection. (HSE, 2013b, p. 45)

However, a lack of transparency with regard to the environmental quality of the products still made it difficult for true pioneers, such as, HSE, to distinguish themselves from less ambitious market players or even greenwashing companies. On the brighter side, it seemed as if consumer knowledge about green energy was increasing along with a generally growing interest in the topic. For already quite some time, the board had thought about how to add value for household and industry customers. HSE’s three pillars, ‘avoid CO2’, ‘reduce CO2’ and ‘compensate CO2’, definitely made sense from a sustainability perspective, but how could the company leverage the potential of its portfolio of sustainability products and services in the B2C as well as in the very important B2B market? It proved to be difficult, for example, to develop energy-efficiency services into a veritable market. ‘Nobody has found the key for successful business models in the area of energy efficiency. One does not learn this overnight,’ explained Dr Wolff-Hertwig (Köpke, 2013). Finally, the recently increased share of the city of Darmstadt illustrated once more that HSE was not only a national player but also a company with very strong regional roots, a fact that was also evident from its history and from some of its business areas. How could this be kept in balance, and how could the company strengthen its regional focus without losing sight of the bigger picture?

Despite the current challenges, Dr Wolff-Hertwig was optimistic for the future of HSE as a leading sustainable energy company. ‘The entire workforce will adapt to these challenges and we will have to find a market-based solution. HSE has always proved that it has the strength for strategic realignments’ (HSE, 2013c).

Footnotes

Appendix

HSE Cash Flow Statement (in T€)

| Cash Flow from Operating Activities | 2013 | 2012 | 2011 |

| 1. Net income/loss for the period (excluding minority interest) | 1,765 | 1,921 | 32,362 |

| 2. Increase/decrease in current assets (±) | 88,015 | 79,162 | 66,409 |

| 3. Increase/decrease in provisions and accruals (±) | 60,185 | 48,350 | 27,784 |

| 4. Other non-cash expenses/income (±) | –32.584 | –62,216 | –32,706 |

| 5. Profit/loss from fixed asset disposals (±) | –37,264 | –12,894 | –342 |

| 6. Receipts from dividends from companies valued using equity method (+) | 1,106 | 2,533 | 2,821 |

| 7. Increase/decrease in inventory, trade receivables and other assets that are not attributable to investment or financing activities (±) | 115,249 | 17,251 | 29,604 |

| 8. Increase/decrease in liabilities, trade payables and other liabilities not associated with investing or financing activities (±) | –77,342 | 14,824 | –81,212 |

|

|

|

|

|

| Cash Flow from Investing Activities | 2013 | 2012 | 2011 |

| 9. Cash received from the disposal of fixed assets | 8,840 | 1,159 | 1,276 |

| 10. Cash payments for investments in fixed assets (–) | –59,704 | –120,104 | –172,019 |

| 11. Cash received from the disposal of intangible assets (+) | 163 | 2,505 | 1,871 |

| 12. Cash payments for investments in intangible assets (–) | –4,857 | –7,480 | –5,817 |

| 13. Cash received from the disposal of financial assets (+) | 58,042 | 22,388 | –556 |

| 14. Cash payments for investments in financial assets (–) | –8,607 | –49,746 | –48,034 |

| 15. Payments from the purchase of consolidated subsidiaries (–) | 421 | 13 | –600 |

| 16. Currency differences (±) | 0 | –103 | –2 |

| – |

– |

– |

|

| Cash Flow from Financing Activities | 2013 | 2012 | 2011 |

| 17. Payments to company owners and minority interests (–) | –85,760 | –25,394 | –24,952 |

| 18. Receipts from take-up of (financial) credit (+) | 124,102 | 90,794 | 58,174 |

| 19. Payments received from the issue of loans (+) | 0 | 0 | 320,500 |

| 20. Outgoing payments for the settlement of loans and (financial) credits (–) | –49,047 | –15,020 | –8,071 |

| 21. Proceeds from subsidy payments (+) | 7,540 | 10,703 | 9,454 |

| – |

|

|

|

| Cash and Cash Equivalents at the End of the Period | 2013 | 2012 | 2011 |

| 22. Cash and cash equivalents at the beginning of the period | 251,475 | 253,137 | 76,937 |

| 23. Net changes in cash and cash equivalents (±) | 110,263 | –1,354 | 175,908 |

| 24. Changes in the group of consolidated companies (±) | –9,836 | –308 | 292 |

|

|

|

|

Acknowledgements

The authors thank the HSE AG, Darmstadt, Germany, for the ongoing support.