Abstract

This case reveals the story of organizational restructuring at Bharat Petroleum Corporation Limited (BPCL). The story begins in the 1990s when India’s petroleum industry was closed to private enterprise. BPCL’s chairman at that time (Sundararajan) anticipates that India’s government would deregulate the industry. He is concerned that without fundamental changes, BPCL might not survive private competition—and so, he initiates a transformation of the organization’s strategy and structure. The restructuring attempts to dismantle a command-and-control culture, and replace it by one of empowered teams. The change process is undertaken in the spirit of co-creation. The definition of ‘customer’ is altered, causing organizational boundaries to be redrawn. Such an exercise is extraordinary for its time.

The case then presents a picture of BPCL and its challenges in 2015. History seems to repeat itself, as market conditions are nearly identical to those that existed 17 years ago. What should the company do in 2015? This case has a three-fold purpose; viz. (i) to show how the structure of an organization can be aligned with its business strategy; (ii) to illustrate how organizations with a functional structure can reorganize to an ‘M-form’ or SBU structure; and (iii) to help readers consider the latent, long-term effects of restructuring.

Keywords

Introduction

On 1 June 2015, Srinivasan Varadarajan glanced through the day’s newspapers while he was on route to his office in Mumbai. He noticed a news report that competition in the Indian petroleum industry was set to increase (see Suryamurthy, 2015). As chairman and managing director of Bharat Petroleum Corporation Limited (BPCL), Varadarajan was responsible for his company’s strategy and performance. BPCL, a global Fortune 500 company, 1 was primarily engaged in petroleum refining and marketing (R&M) in India. It was one of three such companies that were largely owned by the Indian government. There were also a couple of private firms that owned refineries in India; however, these did not compete in the Indian market because the government controlled the prices of petroleum products. Now, due to speedily unfolding events, the Indian petroleum industry found itself on the cusp of intense competitive rivalry.

It had all begun in October 2014, when prices of crude oil, which had hovered around US$100 for four years, crashed to US$84.40 (USEIA, 2015). Consequently, in the same month, the Indian government deregulated the price of diesel, causing it to fall by about 5 per cent (Ranjan, 2014). In the weeks that followed, prices of international crude continued their decline. By January 2015, crude oil was available for under US$50. By March 2015, diesel in India had become cheaper by an additional 10 per cent. In short, the emerging features of the R&M business context were: (i) input costs were reducing dramatically; (ii) the government had stopped controlling the prices of finished products; and (iii) India’s economy was growing at about 6 per cent. Importantly, these features were likely to sustain over the medium term.

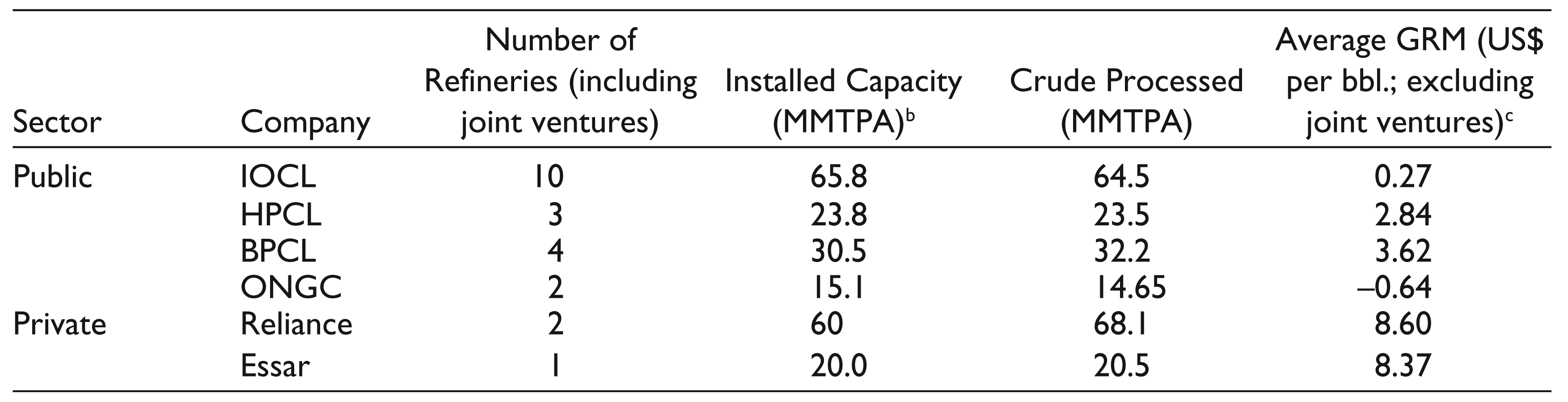

The above conditions augured well for R&M companies with large and efficient operations. In March 2015, only three of India’s 22 refineries were owned by the private sector, but these three refineries processed about 40 per cent of the crude oil refined in India, and did so at almost twice the margins as those of the state-owned refineries (see Exhibit 1). Thus, their scale and efficiencies made private R&M companies highly competitive—and it seemed that India’s petroleum industry would soon be embroiled in battles for customers and their loyalty.

As he considered the turn of events, Varadarajan recalled that in the late 1990s, BPCL had fought a similar war for market leadership. At that time, the company had restructured itself in an unprecedented exercise called Customer Service and Customer Satisfaction (CUSECS). The key questions arising for Varadarajan were: what lessons did CUSECS offer for today’s challenges, and was BPCL’s current structure and strategy strong enough to beat the competition?

The Historical Context of CUSECS

After India gained independence in 1947, its government increasingly regulated the country’s economy and some sectors were closed to private enterprise. By 1977, India’s R&M sector was dominated by three state-owned companies, viz. BPCL, Hindustan Petroleum Corporation Limited (HPCL) and Indian Oil Corporation Limited (IOCL). In December that year, the government implemented a policy known as the administered pricing mechanism (APM). Over the next 25 years, the APM influenced India’s petroleum industry like no other policy. The main characteristics of the APM were:

Prices of most petroleum products were set by the government.

2

Some products (e.g., kerosene) were heavily subsidized as they were used by large (especially poorer) sections of Indian society, whereas prices of other products (e.g., petrol) were set much higher. In effect, this was a practice of cross-subsidization wherein the cost of subsidies was borne by higher priced products. Any deficits due to subsidies were reimbursed to R&M companies through the national budget. Further, the margins of R&M companies were assured as per government norms: These were calculated at 12 per cent of a company’s net worth (share capital plus retained earnings). R&M companies were asked to share infrastructure and products, in a practice that was officially termed ‘hospitality’. Thus, the fuel produced at an IOCL refinery could be stored at an HPCL terminal, and finally be sold at a BPCL retail outlet—or vice versa. For example, in 1990, BPCL produced 7.12 million metric tonnes (MMT) but sold 10.18 MMT of petroleum products (BPCL, 1990, pp. 15, 21).

The above features resulted in some unintended consequences. First, controlled prices led to growth of the oil mafia which adulterated higher priced products like diesel with subsidized fuels such as kerosene. Second, since margins were guaranteed, R&M companies had no need to improve efficiencies. Third, the practice of hospitality limited the competitiveness and growth of R&M companies. Ultimately, the APM began to adversely affect the very consumers whose interests it was designed to protect.

The business context appeared to change in 1991 when the government began a process of liberalization. This phase in India’s economy was marked by the easing of controls and the entry of private companies into formerly restricted sectors. However, in the case of the petroleum industry, the government was concerned that deregulation might make energy products unaffordable to the consumer. To help find answers, in November 1994, the government formed a study group of 75 executives drawn from India’s petroleum companies. The study group was informally termed the Sundararajan committee, after its convener, Uppiliappan Sundararajan (then chairman and managing director of BPCL). In its report, submitted in February 1995, the committee recommended the abolition of the APM and presented a road map for deregulation of India’s petroleum industry.

The Sundararajan Committee Report was widely appreciated, but Sundararajan was a worried man. In the process of leading the study group, he had realized that BPCL was not equipped for a competitive environment. He had also observed that, internationally, ‘wherever deregulation happened, government oil companies suffered in terms of market share […] because they were infrastructure oriented and not tuned to the voice of the customer’. So, to prepare BPCL for a deregulated environment, Sundararajan launched project CUSECS and led a historic transformation of BPCL.

CUSECS and its Results: 1996–2002

Sundararajan began by initiating the process of identifying a suitable consulting firm. In September 1996, BPCL’s board appointed consultant Arthur D. Little (ADL) to support project CUSECS. In the same month, the government’s ‘strategic planning group’ for restructuring the petroleum industry submitted its report. It too recommended that the APM be dismantled, and that it be done in a phased manner from 1998 to 2001.

Sundararajan acted quickly. Within a month, he formed a team of 22 managers, many of whom he handpicked for the project. While constituting the team, Sundararajan had looked for individuals who were unafraid to question the status quo. As Biren Anand observed, ‘many among the twenty-two would say what they wanted to say; not what you wanted to hear’. 3 When they began work in October 1996, neither the team nor the project had a name, but their goal was clear: ‘to prepare BPCL for deregulation’. 4 Over the next 18 months, the team executed their mandate by developing the change plan, redesigning the organization, and managing and implementing the change.

Developing the Change Plan

The CUSECS team began by organizing itself into six smaller teams, each of which focused on one critical area. These focus areas were (i) liquefied petroleum gas (LPG), (ii) lubricants, (iii) marketing (other products), (iv) refining, (v) logistics and (vi) support services and management processes.

Working along with ADL consultants, the CUSECS team compared BPCL’s processes and performance with external practices and benchmarks. Additionally, some teams travelled across the country conducting interviews and focused group discussions with stakeholders including customers, employees, labour unions, suppliers, contractors and government officials.

In December 1996, ADL conducted a workshop for BPCL’s functional directors where the directors shared their vision and aspirations for BPCL. Later that month, a similar workshop was held for the CUSECS team and BPCL’s senior management. The vision articulated at these two workshops served as a beacon to the CUSECS team in their examination of current realities. Sundararajan asked his senior colleagues to informally participate in the current reality assessment—and he led by example. On his official travels, he would ask employees, dealers

5

and customers about their satisfaction with BPCL. Once, Sundararajan was travelling by road from Bangalore to Salem and happened to see a BPCL tank-lorry. He recalled:

I hailed the driver of our tank-lorry. After introducing myself, I asked him what he thought of our service to customers. He appeared a little agitated and said to me ‘You don’t know what is happening. What customer service? Customers are cheated at some pumps. The drivers know everything—you should speak to the drivers.’

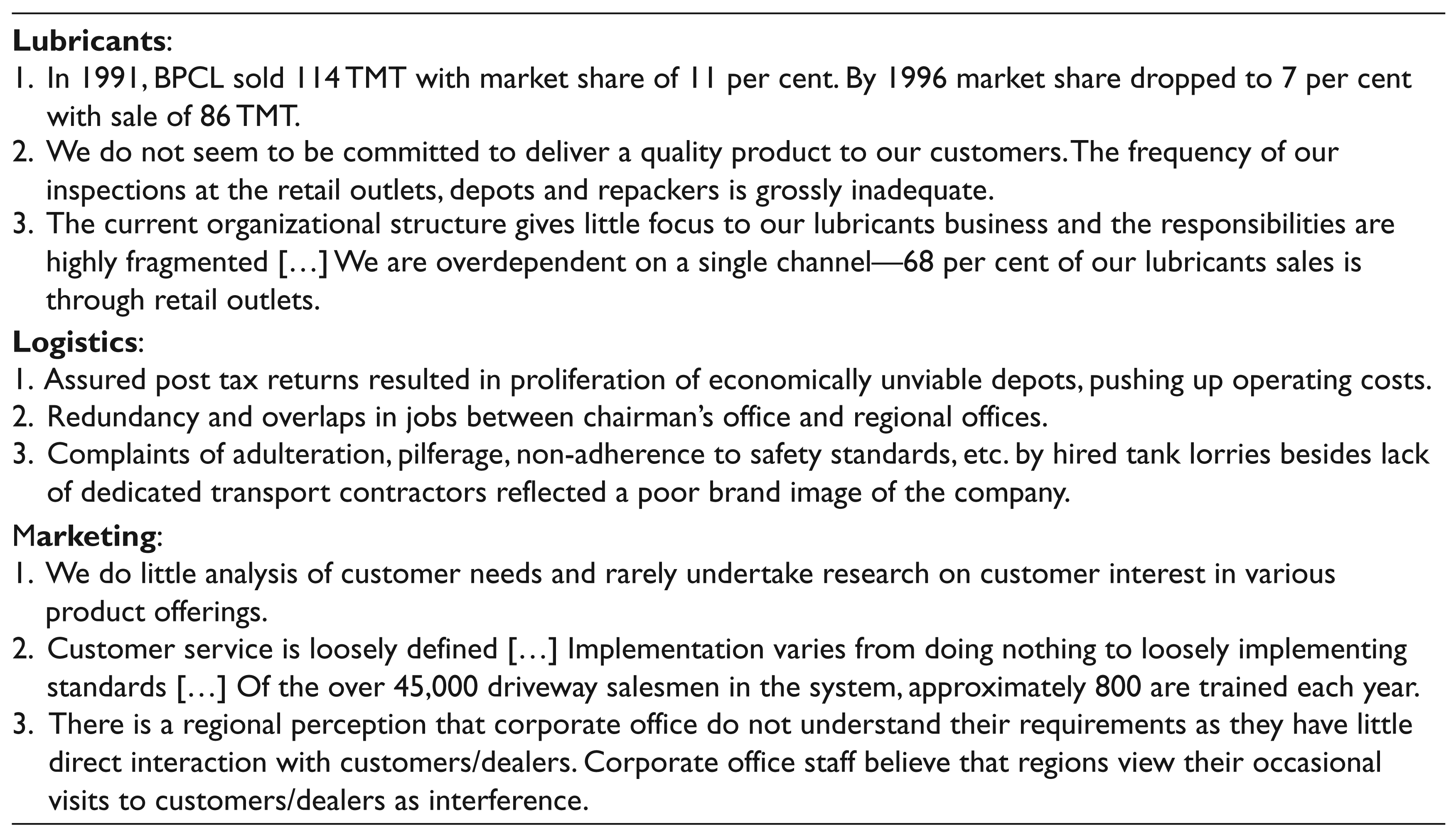

Thus, the current reality assessment had involved a range of people, from various vantage points, within and outside BPCL. The assessment was completed in early January 1997 and was presented to BPCL’s top management team. Several findings were unpleasant (see Exhibit 2), and some among BPCL’s senior leaders were not convinced. The most heated debate was about the question: Who was BPCL’s real customer? This question related to BPCL’s retail channel; and it was significant for two reasons. First, consumer complaints about adulteration and/or over-billing occurred at retail outlets (ROs), 6 most of which were owned and controlled by the company’s dealers. Second, in the previous financial year, BPCL’s ROs had sold 8.7 MMT of products, that is, almost 60 per cent of the company’s annual sales volume. Hence, agreement about the real customer was central to BPCL’s goals and business strategy.

At that time, there was a view that the dealer was the primary customer and that BPCL’s responsibilities ended upon delivery of fuel to ROs. People who held this view were offended by aspects of the current reality presentation—they could not understand how BPCL could be responsible for events occurring outside its organizational boundaries. They rightly observed that even matters as important as dealer-selection were not in BPCL’s control. 7 However, another perspective was that BPCL’s real customer was not the dealer—that the company could not absolve itself from the service accorded to end consumers. There were animated discussions. The group finally agreed that in a deregulated market, the consumer would be ‘king’; and that their shared vision (see Exhibit 3) could not be achieved without the consumer.

Agreement about the ‘real customer’ provided greater impetus to the change process. Three members were added to the CUSECS team and the number of focus areas was increased to 22. Visioning workshops were held at BPCL’s four regional offices; and the shared vision was presented at all divisional offices. Ideas from these presentations served as inputs for the change plan. A group of ‘enablers’ was identified; these were internal subject-matter experts and were quite senior in BPCL’s hierarchy. CUSECS team members shared their data and analyses with enablers, and sought their critical views and expertise. Working in this manner, the CUSECS team identified gaps (between vision and reality) and developed action plans to bridge those gaps. Put together: the current realities, visions and action plans (for the 22 focus areas) formed six volumes and 1600 PowerPoint slides, collectively constituting the CUSECS change plan. The change plan was presented to the board in April 1997, within seven months of having begun project CUSECS.

Immediately thereafter, the change plan was presented to employees, union-representatives, dealers, distributors and contractors. As per Sundararajan’s instructions, the plan was made available on all desktop computers, at each of the company’s offices. Most reactions at BPCL suggested that the transparency was appreciated and the change plan was well received. The plan had been developed at an amazing speed. It reflected an honest picture of reality and of shared aspirations. The plan also listed questions that were yet to be answered; for example:

Should the retail business be a separate strategic business unit? Should we focus on volumes or profits as the key driver of the business? Should we invest in primary transportation facilities, including pipelines?

In essence, through CUSECS’ first phase, BPCL had committed to a strategy of focusing on the consumer. It had articulated its vision and performed a current reality assessment. The company had developed and announced action plans to surmount the gap between reality and aspirations. Now, it was time to align the organization’s structure with its strategy and plans.

Redesigning the Organization

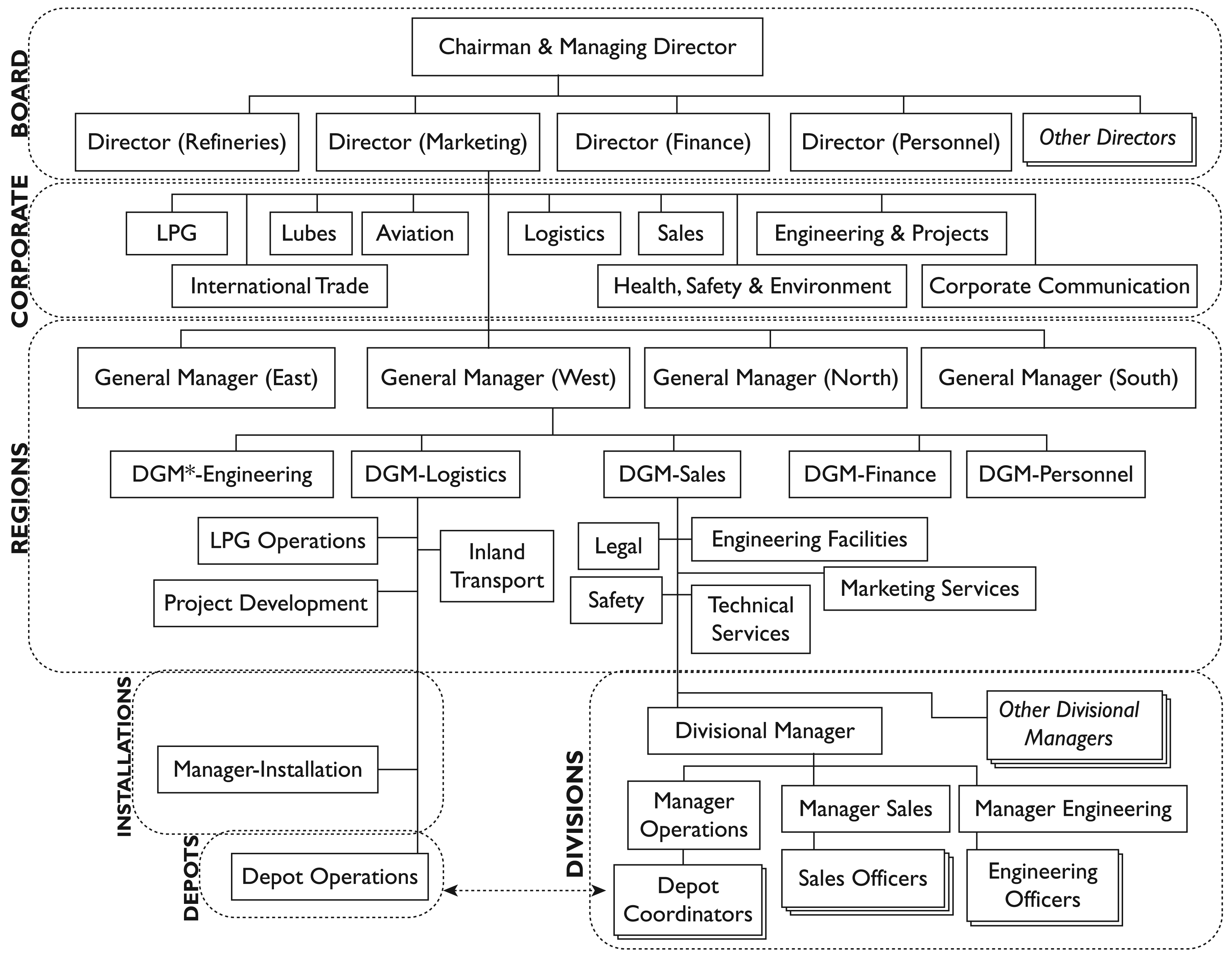

In 1997, BPCL’s organization design was largely based on functions and geography (see Exhibit 4). The company had two profit centres corresponding with its two functions, refining and marketing. Its board was organized by function: two directors headed the line functions (refining, marketing) and another two directors were responsible for support functions (personnel, finance). 8 Since the marketing function was accountable for customer service, it was the primary focus of project CUSECS. A summary of CUSECS findings can be found in a book Management: Text and Cases.

Marketing had a two-tiered structure made up of corporate and regional components. The corporate teams were organized by customer/product groups, but these were exceptions and were far removed from customers. Regions were organized by geography (east, west, north, south) and by the sub-functions of logistics and sales. 9 The regional logistics network was made up of storage and supply locations. In 1997, BPCL had 147 such locations spread throughout the country. Of these, 16 were termed ‘installations’ as they were very large facilities, while the remaining 131 were smaller and were called ‘depots’. The regional sales organization was made up of ‘divisions’ which in turn were responsible for ROs. That year, BPCL had 20 divisions and 4,373 ROs.

Excerpts from the CUSECS teams’ analysis of BPCL’s organization structure (BPCL, 1988, pp. 3–5) read as follows:

Each Division consists of staff from sales and engineering functions for development, up-gradation and maintenance of retail outlets […] there is very little direct coordination at the field level amongst the sales officers and the operations [i.e. logistics] officers […] The functional bias of the existing structure has led to precedence of functional goals over team goals, resulting in role confusion and lack of accountability […]

The demands of our different Customers vary widely, […] e.g. customers who buy Petrol/Diesel from a retail outlet have different needs as compared to those who buy LPG. Likewise, the requirements of industrial customers buying Naphtha, Furnace Oil and Bitumen are quite different from those of another set of customers. In the present scenario, as the entire sales team—from DGM (Sales) down to the sales officer—service all types of customers, they have a diffused focus and often end up unable to concentrate on any […] This has led to a situation where market awareness in the organization is not at the desired level. Even if the field staff identifies areas of improvements in respect of a customer segment/group, it is difficult to pursue it beyond a point—approvals are required from divisional/regional officers where the focus is greatly diffused. This not only results in these initiatives getting lost but also dampens enthusiasm and stifles innovation.

The existing functional structure makes it difficult for senior managers to focus on developing and implementing strategies: […] the formulators of strategy are not in close touch with the ground realities and thus the quality of strategies may be wanting [… or] the implementers do not fully understand the rationale of the strategy and thus are lukewarm in execution. In summary, the current structure was suitable for a relatively stable environment with limited competition. In the unfolding market this structure may not be effective […]

Thus, the main limitations arising from BPCL’s organization design were: (i) a relatively weak understanding of customer segments and their needs; (ii) greater focus on sales volumes than on margins; (iii) inter-functional rivalry; and (iv) a long chain of command-and-control before decisions could be made and implemented. On 26 April 1997, the CUSECS team presented their analysis to BPCL’s board and secured its approval for redesign of the organization.

On 2 and 3 June, ADL facilitated a workshop on ‘organization design’ for BPCL’s senior management and the CUSECS team. An idea that emerged at this workshop was to measure profitability at a level closer to the customer, such as at the level of a logistics depot. This concept was revolutionary for two reasons. First, in those years, BPCL had no sales structures that were equivalent to a depot. The smallest unit of the regional sales organization was the division, which was responsible for over 200 ROs. In comparison, a logistics depot supplied products to about 28 ROs. Second, marketing margins were not measured at the divisional level, nor even at the level of a region. The implications of the idea were clear: new units of organization might have to be created at the frontline. Importantly, authority from corporate, regions and divisions would have to be delegated to these new units if they were to be responsible for margins.

Ideas promoting such radical decentralization went against the organization’s hierarchical, command-and-control culture, and led to much angst at the workshop. Proponents of delegation argued that BPCL would gain competitive advantage when customer-facing employees felt like entrepreneurs. Opponents cautioned that people were not ready for delegation—that it would lead to loss of control and result in corruption. Both camps were convinced that only their view was aligned with BPCL’s shared vision. Sundararajan watched as discussions became chaotic and participants reached an impasse. He then inquired with BPCL’s company secretary, if the laws permitted him to delegate his powers as chairman. Upon receiving confirmation, Sundararajan told the group that he was willing to delegate his own powers. Rajiv Chaturvedi (then General Manager of BPCL’s northern region), recollected, ‘Mr. Sundararajan stunned everyone. It was a wonderful thing he did to break a logjam. If the top man himself is willing to delegate his authority, do the others have an option?’

Over the next few weeks, work on BPCL’s organization design continued. The CUSECS team and ADL consultants explored a range of structural options. Around mid-July 1997, the teams agreed on their recommendations, which were to:

establish new strategic business units (SBUs):

10

retail, industrial, LPG, lubricants and aviation; implement, within each SBU, geographical regions and cross-functional teams; operate logistics as an independent SBU or as a shared-service for SBUs; embed select support functions (finance and human resources) within SBUs; and enable organizational balance and integration of SBUs through lateral councils.

However, even before the recommendations could be properly worded, they ran into opposition from the most unexpected of quarters. It so happened that Sundararajan informally visited the CUSECS team. That evening, the ADL consultants were also present. Sundararajan appreciated all recommendations, except that of an independent logistics function. He reminded the teams that a retail customer’s basic needs (i.e., product availability, quality and quantity) were inseparable from logistics. Accordingly, he suggested that logistics be embedded within the retail SBU. The teams argued that other proposed SBUs also required logistics. However, the fact remained that the bulk of BPCL’s sales accrued through its retail channel. This was perhaps the only occasion when Sundararajan went against his team and asserted his authority. His final question was ‘how would a retail customer’s needs be best served by an independent logistics function?’ As Singh recalled, ‘we did not have an answer to that question’. Sundararajan ordered that logistics be assimilated within the retail SBU. He specified that it be done not just at higher levels, but especially within customer-facing teams. There was to be no further discussion in the matter.

It seemed that Sundararajan had bullied his CUSECS team into agreement—and there were different reactions and perspectives to the above episode. Members of the CUSECS team were shocked and felt that their independence had been taken away. They took a brief while to recover and get on with work. Ironically, what helped them in the process was Sundararajan’s reputation. As Singh explained, most BPCL employees trusted their chairman completely, because Sundararajan was known for his selflessness.

11

For its part, ADL found it awkward that they had not anticipated Sundararajan’s views. Excerpts of their notes from a meeting in London read as follows:

ADL [was] cornered by certain parts of the client team. The chairman had very definitive ideas against our proposed solution. ADL proposed Logistics to be a shared service. Chairman decided to embed Logistics in Retail SBU and implement the team-based concepts […] We did not have a solution. Where did we break down [?] [We] did not have insight into political issues.

12

Why was Sundararajan so insistent? Did he also believe that political interests had ‘cornered’ the CUSECS and ADL teams? About 12 years after his retirement from BPCL, Sundararajan was asked these very questions. He offered a simple explanation:

Wherever I had visited, I heard the same story of logistics people blaming sales, and sales people blaming logistics […] the only way to stop the blame-game and get people working together was to put them in one team, with full responsibility for providing best services to customers.

Thus, in July 1997 the early contours of restructuring began to take shape at BPCL. The CUSECS team examined existing organizational units and processes for alignments and impediments. They decided to replace BPCL’s 20 divisions by several territories. Sixty-six territories were to be created within the retail SBU alone. The role of divisional manager (DM) was to be discontinued. Each territory would be managed by cross-functional teams of officers—from sales, engineering, and logistics—that would report to the newly created position of territory manager (TM).

The TM’s role, in comparison with that of the DM, was different in several respects. First, TMs were to focus on products and/or customer segments that were limited to their SBU. Second, they were to have a smaller geographical area of operations and therefore smaller teams. Third, due to the smaller scale of their job, relatively junior officers could be appointed TMs. Hence, TMs could be about five or six years older than those reporting into them, unlike DMs, who were about 15 years older. Fourth, the TM’s job would be wider in scope and complexity. Finally, the authority (including, financial) exercised by DMs, was to be vested in the team comprising the engineering officer, logistics officer, sales officer and TM. 13 These changes held the promise of a culture of empowerment, collaboration and trust at BPCL.

Managing and Implementing the Change

The process for assigning employees to SBUs and to support functions began around 21 July 1997. For several people at BPCL, this process unfolded like an emotional roller-coaster. Those who were disappointed on a given day were to consider themselves lucky a few days later; others who had been open to change turned skeptical or began to resist the restructuring. For example, logistics officers who were anguished that their function was being ‘cannibalized’, now seemed more optimistic. In the new scheme of things, they were being nominated as TMs. 14 On the other hand, DMs who had been ambivalent to CUSECS, now felt adversely affected. There did not seem to be a suitable role for them. Understandably, some of them opposed the idea of SBUs, of territories, and of project CUSECS as a whole—but they had little choice in the matter. Most DMs were appointed to a newly created position of area marketing manager (AMM). This position involved external co-ordination (with state governments and R&M companies), but it did not wield formal authority over territories. According to Sundararajan, AMMs were expected to contribute to the organization in the role of ‘mentor’ to the territories.

Throughout the process of change at BPCL, the government had remained a strong supporter. Sundararajan was trusted by government officials not merely for his advocacy of deregulation, but also because he would brief them about contentious decisions in advance and would show how such decisions were in the interests of consumers. While Sundararajan evoked the government’s confidence and support, the CUSECS and ADL teams helped deal with internal matters of change. By November 1997, the CUSECS team formed virtual SBUs and pilot projects.

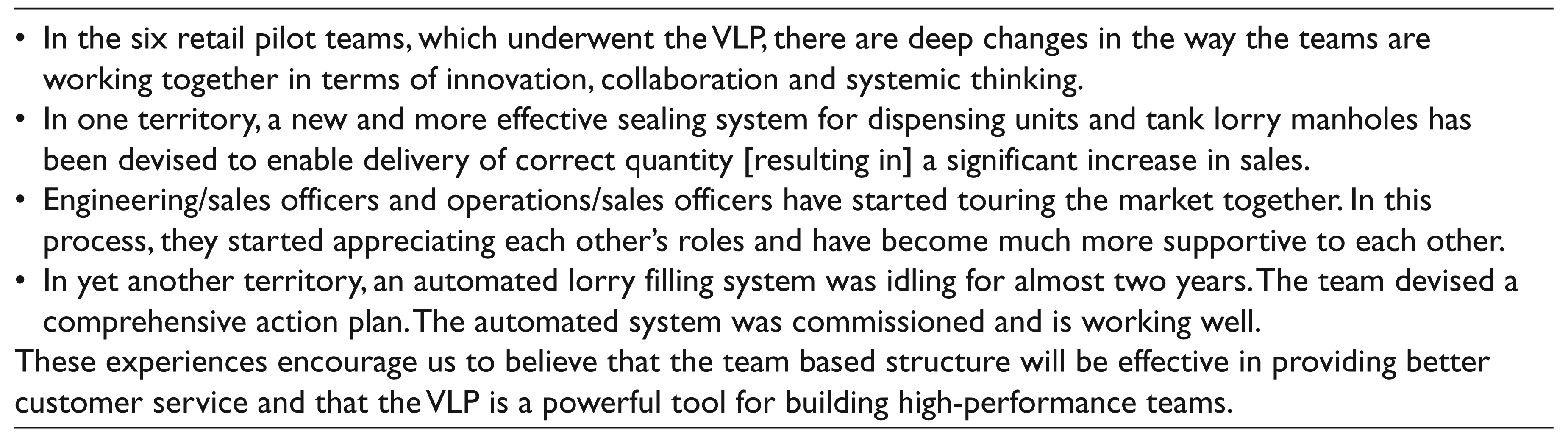

Virtual SBUs were set up at the corporate level and functioned as microcosms of proposed SBUs. Pilot territories were formed in the field, to test how the new team structure might work. Six of these pilots were in the retail SBU. Preparation for pilots and virtual SBUs had begun several months earlier, with a workshop for managers chosen for the new role of ‘internal coach’. 15 The workshop revolved around Peter Senge’s concepts of five disciplines and the learning organization (Senge, 1990). Thereafter, BPCL’s coaches and ADL’s facilitators conducted visionary leadership and planning (VLP) exercises for every virtual SBU and pilot team. VLPs nurtured the principles of empowerment, team-work and enrolment through five key steps, namely (i) articulating the desired vision of the team, (ii) understanding current realities, (iii) identifying gaps between vision and reality, (iv) developing concrete plans to overcome gaps and (v) committing to the plans as a team. Within weeks of the VLPs, dramatic changes started appearing (see Exhibit 5). As Dipti Sanzgiri said, ‘the moment the conversations start, the change has begun’. 16

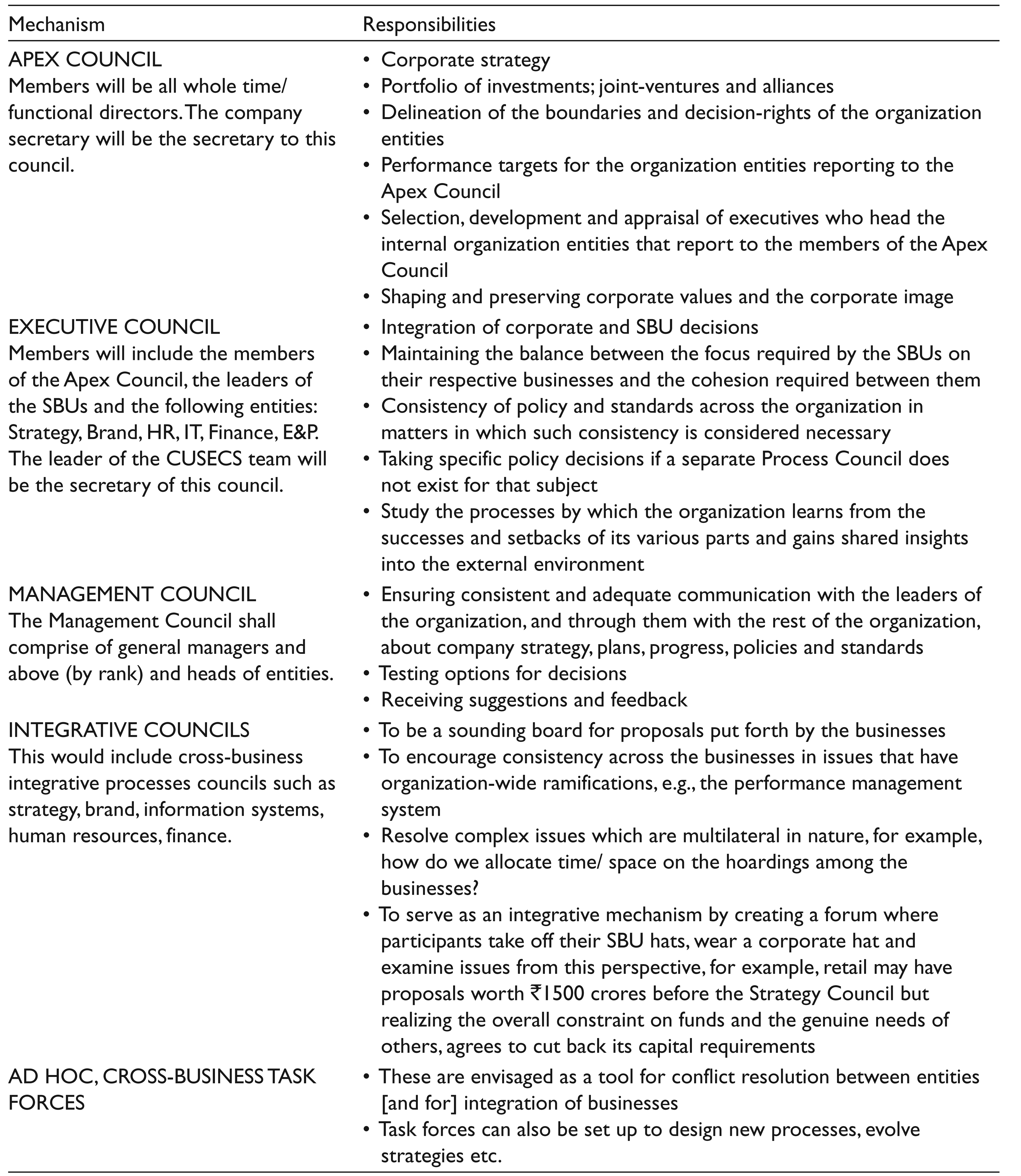

Although the results of pilot projects exceeded expectations, there was a concern that individual SBUs might function without regard to the rest of the organization. Therefore, BPCL decided to set up several lateral linking structures (see Exhibit 6). BPCL’s board approved the company’s new organization design in April 1998. BPCL’s employees moved into their new roles in May 1998. And, although project CUSECS came to a close, it was hoped that the culture of a learning organization—of readiness for change—would be sustained.

The immense energy generated by project CUSECS continued to be felt within BPCL in the years that followed. Several initiatives that had been identified in the change plan came to fruition. These were firsts of their kind, and so they enhanced BPCL’s status as a pioneer in India’s R&M sector. The initiatives included:

PetroCard and SmartFleet: loyalty programmes with prepaid cards (implemented in 1999 and 2001, respectively). Pure-for-Sure: third-party certification which guaranteed the quality and quantity of fuel sold at ROs (launched in August 2001). SAP’s enterprise-wide resource-planning solution: deployed by BPCL at over 300 locations in India (implementation completed in February 2002).

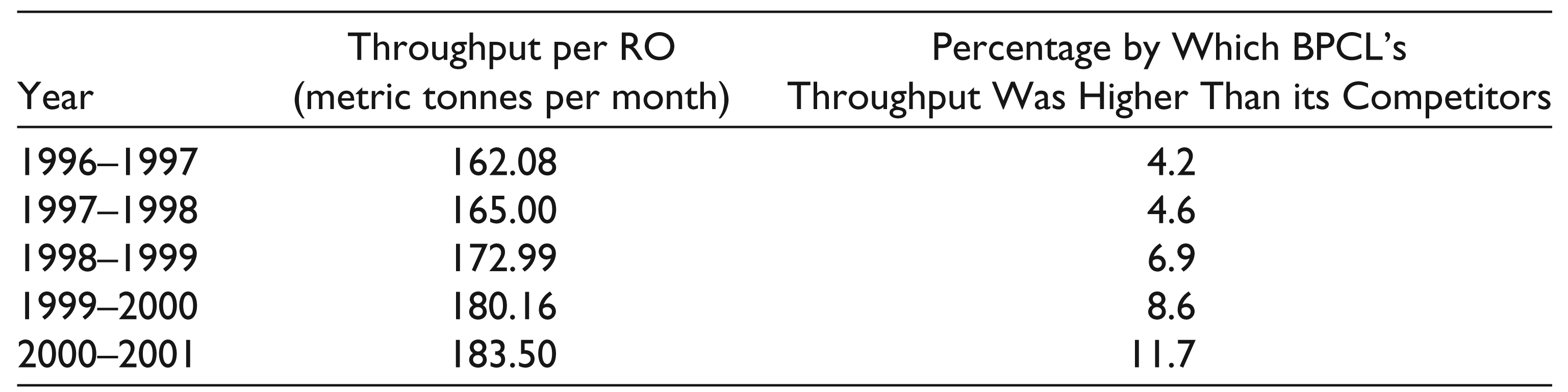

Perhaps the most remarkable results occurred in BPCL’s retail SBU, where average sales (throughput) per RO, per month, increased 11 per cent (from 165 tonnes in 1998 to 183 tonnes in 2001). In effect, BPCL’s throughput figures in 2001 were nearly 12 per cent higher than those of its competitors (see Exhibit 7). By 30 June 2002, when Sundararajan retired, it seemed that BPCL had successfully transitioned to a new strategy, structure and culture.

From Regulation to Deregulation and Back: 2002–2015

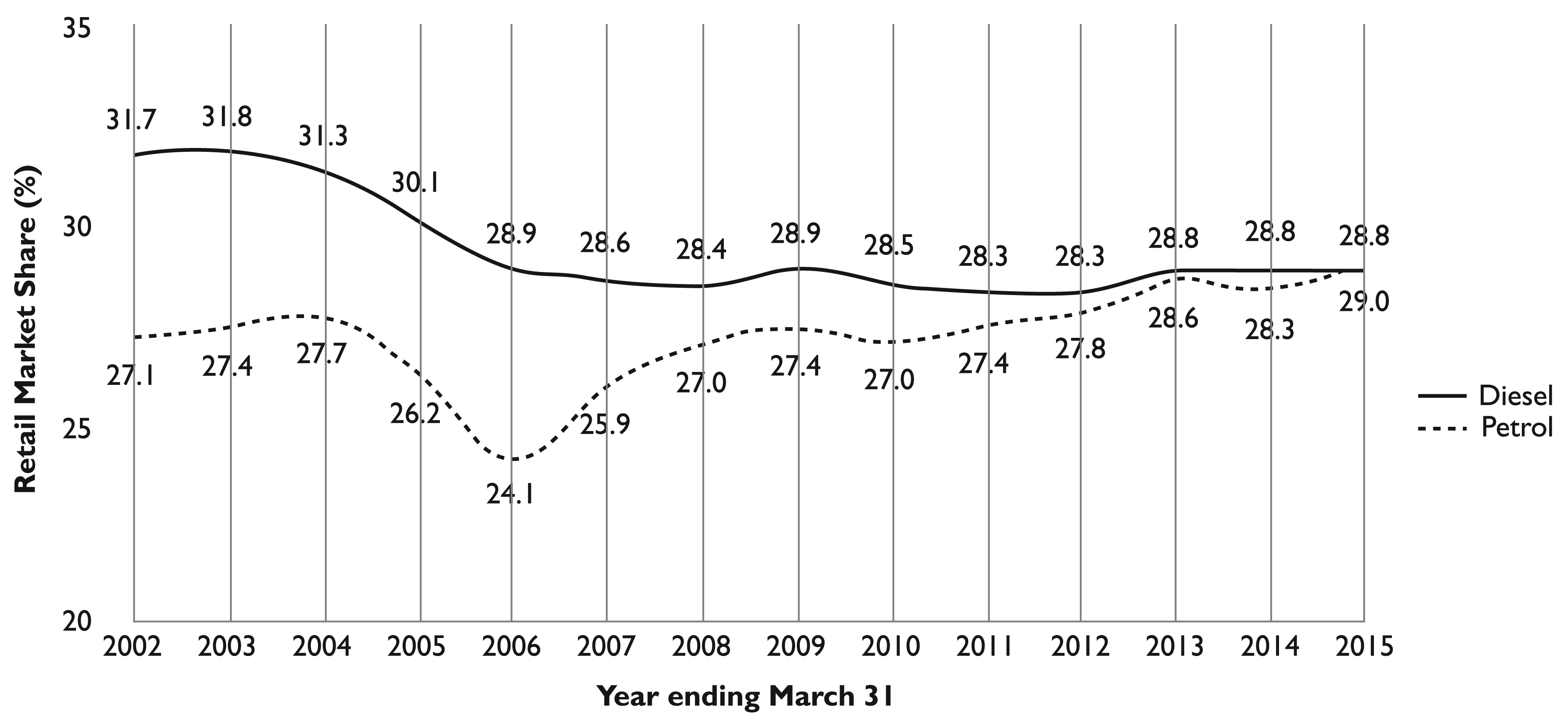

In the years since 2002, India’s petroleum industry experienced much volatility in crude prices, statutory environment and in the reactions of R&M companies. For example: the government dismantled the APM in 2002 and permitted private players to engage in retail sales of petrol, diesel and aviation fuel. In 2003, international crude prices increased by about four US dollars to reach an average price of US$26.65 per bbl. The government was alarmed. In September that year, it reintroduced price-controls and cross-subsidization (Srinivasan, 2003). By the end of 2004, three private-sector companies (Essar, Reliance and Shell) set up ROs in India. In the first quarter of 2005, these private companies held almost 10 per cent share of the country’s diesel market (Essar Oil Ltd, 2005, p. 13). The biggest drop in BPCL’s market shares occurred in the year 2006 (see Exhibit 8). Crude prices breached 50 US dollars per barrel (bbl.) in 2006, and the government extended subsidies to petrol and diesel. Private companies could not match subsidized prices and suspended domestic retail sales. Crude prices sustained their upward spiral and were about US$100 per bbl. from 2011 to 2014. During this time, the government continued to control prices, and private ROs had effectively shut down.

Despite above dynamics and uncertainties, India’s growing economy led to increased demand and consumption of petroleum products. India’s R&M sector began to be characterized by the following:

Increasing dependence on international crude: 75 per cent of the crude processed in India, in 2012, was imported—this figure, by 2035, was likely to be 92 per cent (Ahn & Graczyk, 2012, p. 62). Surplus refining capacity: the difference between India’s production and consumption of petroleum products, in 2014, was a surplus of almost 62 MMT (Petroleum Planning & Analysis Cell, 2015a, p. 21). Transportation led consumption: 50 per cent of the petroleum products consumed in India, in 2012, were in the transportation sector (Ahn & Graczyk, 2012, p. 61).

In many respects, BPCL was a stronger organization in 2015 than in the days of CUSECS. From one refinery with an annual capacity of 6.9 MMT in 1998, the company now had four refineries with a combined refining capacity of 30.5 MMT per annum.

17

BPCL’s dependence on ‘hospitality’ arrangements with other R&M companies had significantly reduced. In 2015, the company produced almost 84 per cent of its sales volumes. BPCL had also added 546 km to its product pipelines and more than doubled their capacity (see Exhibit 9). Its retail distribution network had grown to 13 installations, 114 depots and 12,809 ROs. However, in recent years, the following practices at BPCL had reflected a degree of concern:

Of the various lateral linking mechanisms created during CUSECS, only the apex met regularly. Few councils met occasionally, whereas other councils had become inoperative. During VLPs, some employees indicated that collaboration within the organization, especially between SBUs, was a matter of concern. Few employees said, ‘we are not proactive in infrastructure building’ (BPCL, 2012).

The Current Situation

As indicated by the press report of 1 June 2015, market conditions for BPCL had turned full circle with the renewed threat of private competition. Whereas CUSECS had redefined the ‘customer’ and helped BPCL become more customer-centric, times had changed. Varadarajan observed three key differences:

‘The group which went through CUSECS, and the group which is experiencing BPCL now, is completely different.’ The competitive edge that BPCL enjoyed due to initiatives such as PetroCard and SmartFleet was largely neutralized, as competitors had replicated those initiatives. The year 2015 presented the challenge of the ‘millennial’ customers, that is, customers for whom the brand differentiator would be neither price nor product, but customer experience.

Varadarajan sought to rejuvenate the organization with higher levels of collaboration and strategic thinking. Soon after being appointed chairman and managing director of BPCL, he had held a series of conversations with BPCL employees in a process called ‘let’s talk’.

18

At one of those meetings, Varadarajan had asked employees:

Twenty years hence, you won’t have any fuel to deliver. [Imagine] there is no oil, technology has taken over, there’s distributed energy everywhere, people run their cars on batteries—so, you won’t have to dispense energy, what will you do?

Varadarajan’s questions raised enthusiasm within BPCL. Employees responded with various ideas, including: (i) enhance customer service to the level of enterprise-wide loyalty, that is, a state where customers are loyal not only to a given product/SBU, but to the BPCL brand and to all its offerings; (ii) expand current businesses beyond India; and (iii) enter into non-fuel businesses in India.

Questions

What circumstances led to the restructuring of BPCL in 1996?

What were BPCL’s major structural features before project CUSECS?

What changes did project CUSECS make to BPCL’s design and structure?

To what extent can project CUSECS be considered a success?

Did the restructuring result in any unintended consequence(s)?

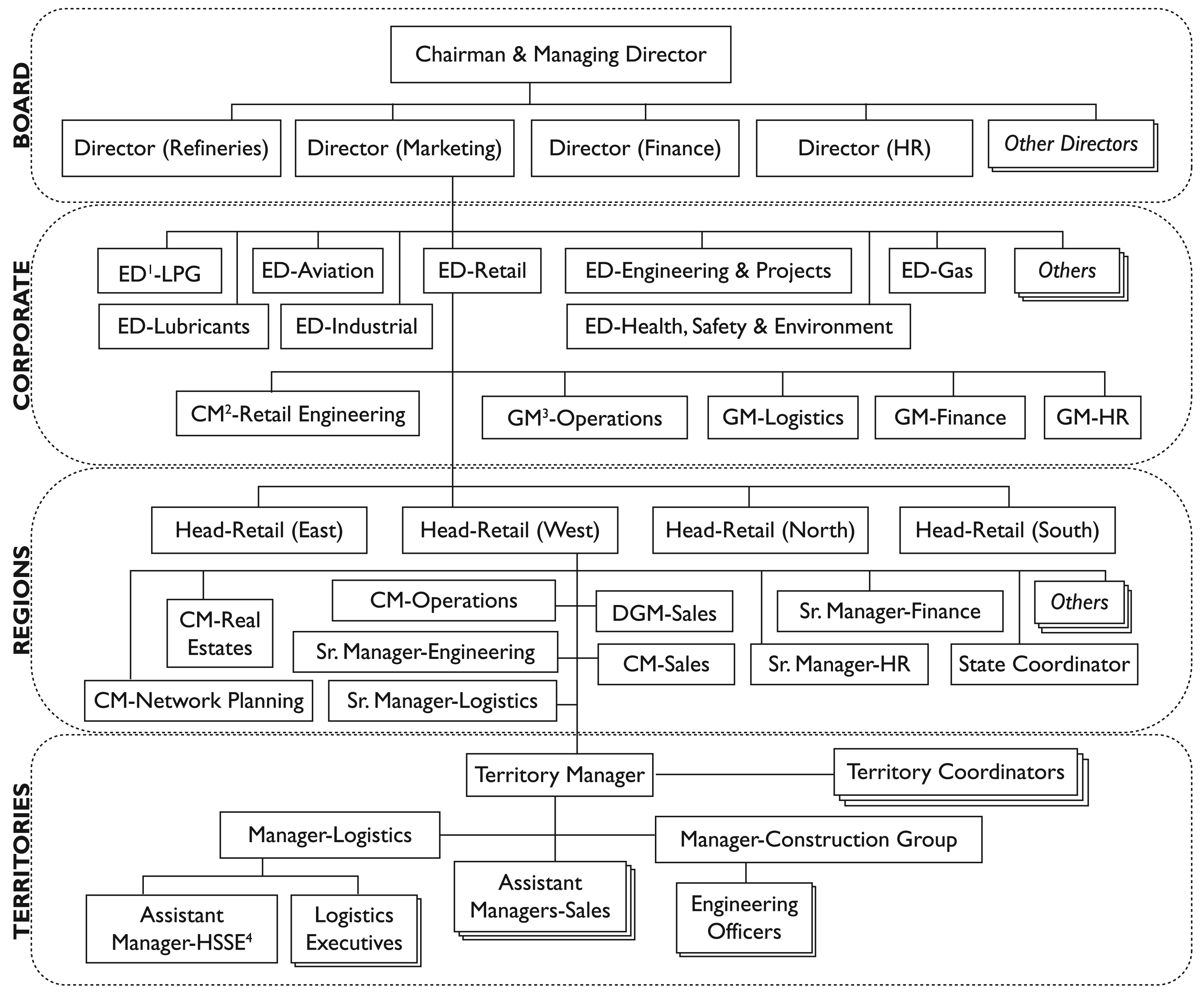

How might BPCL address the competitive challenges of 2015—and, is its current structure (see Exhibit 10) strong enough to beat competition?

Performance of Public and Private Sector Refineries in Indiaa

bMillion Metric Tonnes Per Annum.

cGross Refining Margin.

Excerpts from Current Reality Assessments at BPCL

BPCL’s Shared Visiona

Preliminary Results of VLPs and Pilot Projects

Lateral Linking Mechanisms

Increase in Throughput (Average Sales) per Retail Outlet

Comparative Product Pipeline Networka