Abstract

Research Question:

What is the role of Proxy Advisory Firms in protecting the interests of the non-promoter shareholders?

Links to theory:

This case study demonstrates how agency cost type 2 may lead to a conflict of interest between the promoters and the financial institutions. It also takes into consideration how the information asymmetry can be alleviated using proxy advisory services.

Phenomenon studied:

The case study explores the role of proxy advisory firms in influencing the votes of non-promoter shareholders at a general body meeting and its impact on the passage of resolution.

Case Context:

The case explores the role of shareholder activism in general and proxy firms in particular to protect the interests of minority shareholders at STFC where financial institutions have substantial stake vis-a-vis the promoters.

Findings:

The case study findings suggest that proxy advisory firms have now earned the confidence of the financial institutions and non-promoter investors. This adds vital fire power to the shareholder activism movement in India. However, the company’s stance that the report was based on quantitative factors and Puneet Bhatia’s contribution has been ignored calls for a more robust method of arriving at recommendations. The role of TPG in directing Puneet not to join should also be commended.

Discussion:

The case study examines in detail the growing influence of proxy advisory firms on voting by financial institutions in annual general body meetings. It raises the issue of whether quantitative metrics such as number of meetings attended can overshadow the qualitative inputs and contributions made by a director. The need for financial institutions to think beyond their interests and consider actively recommendations by proxy advisory firms is also highlighted. Are minority shareholders’ concerns now being better addressed in annual general body meetings is another development the case throws light on. Corporate governance norms in the context of roles and duties of directors is also touched upon.

Gone are the days when shareholders used to disinvest due to issues and when nobody used to ask questions. Stewardship guidelines of SEBI will bring far-reaching changes the way companies are governed. Figurative and ornamental directors are no longer valued

—J. N. Gupta, Founder of proxy advisory firm SES after shareholders blocked re-election of independent director Puneet Bhatia (Unnikrishnan, 2020).

He [Bhatia] has had several informal meetings with the promoters, management of the companies, creating synergy and offering valuable insights. These may be difficult to be captured in the statutorily disseminated data to the Shareholders, which only captures the board and committee meetings.

—Press Release of Shriram Transport Finance Corporation (STFC) after shareholders blocked re-election of independent director Puneet Bhatia (Chaturvedi, 2020).

Shareholder activism has the ability to impact the governance practices favourably for listed companies on the account of power of ownership ensuring wealth maximization for shareholders (Hendrikse & Hendrikse, 2003). However, the failure of the Board of Directors in protecting the interest of the shareholder is evidenced in Anglo Saxon corporate structure where the onus of monitoring implementation of corporate governance falls solely on the financial markets (Chakrabarti, 2005). Indian stock markets are no different. However, shareholder activism in India is evolving and proxy advisors are now playing an important role in protecting the interest of the non-promoters. On 19 August 2020, a big step was taken in this direction when the shareholders of Shriram Transport Finance Company (STFC) stalled the reappointment of Puneet an independent director based on the advice of the proxy advisory firms. Not surprisingly, Puneet was able to garner 100% votes from promoters. But more than four-fifths of the non-promoters (mainly financial institutions) voted against the motion. Effectively the motion ‘to appoint Puneet, who retires by rotation as a director’ fell short by 7% and could not garner the stipulated 50% of votes (Modak, 2020).

On one hand, the voting advisory services were ecstatic as they had issued advisories to the shareholding fraternity of STFC to vote against the motion and hailed it as the victory of shareholder activism in India. On the other hand, the promoters and management of the STFC believed that Puneet had added a lot of value to the company and hence should continue as an independent director. Were the shareholders right in removing Puneet from the board was a pertinent question that remained unanswered.

Theoretical Background

The fundamental problem of markets in Europe and other parts is the existence of a dominant promoter, who has significant voting rights. This leads to agency cost type 2 where the interest of the controlling individual or family and the other shareholders may conflict (Enriques & Volpin, 2007). Shareholder voting right is in theory the most formidable course of action available to non-promoter shareholders (Easterbrook & Fischel, 1983). Given the fact that companies are ‘black boxes’ (Jensen & Meckling, 1976) and there is an agency cost type 2, there exists a need for a system that helps alleviate the information asymmetry that exist between the promoters and non-promoter shareholders. Proxy advisory firms, who advise financial institutions on stance to be taken during the voting on varied resolutions play that role (Sauerwald et al., 2018). However, financial institutions blindly following recommendations of proxy firms fail in their fiduciary duty towards the institutional investors according to McCahery et al. (2016). To quote the paper, ‘SEC Commissioner Daniel M. Gallagher, for example, has indicated that he has grave concerns as to whether investment advisers are indeed truly fulfilling their fiduciary duties when they rely on and follow recommendations from proxy advisory firms’ (McCahery et al., 2016).

STFC: The Business Model That Works

STFC, founded in the late 1970s, was a part of Shriram group and operated as a deposit-taking, asset-financing non-banking financial company (NBFC). The company predominantly financed commercial vehicles (CV)—both pre-owned and new for small transport companies who usually owned one or two trucks. Over the years STFC had also expanded to financing vehicles primarily related to agriculture. With more than 40 years of presence, the company was a dominant player in the industry, with around 15% share in India’s CV financing market and around two-fifth of the NBFC CV financing space as on 31 March 2020 (Karvy Online, 2019). It had an asset under management of over ₹11,000,000 million. Management had indicated that they planned to augment distribution network to increase their reach in existing businesses in both towns and villages (Karvy Online, 2019).

There were three factors that led to the company’s emergence as a bellwether in the CV segment evidenced in strong financial performance (See Exhibit 1). Firstly, the company operated majorly in a segment which catered to the second-hand truck financing market which was hugely untapped market and had the potential to grow exponentially. Secondly, the market was dominated by private finance players who charged exorbitant rates. STFC saw this as an opportunity and constantly endeavoured to corporatize the highly unorganized market. Its loan appraisal method, special bond with clients, rural penetration and robust financial assessment proficiencies helped the company create a niche for itself. Majority of the business processes were in-house and therefore helped in improving efficiency level and thereby resulted in costs savings. Hence, its cost to income ratio was among the lowest in the industry at around 25% in FY2020. It had also strategically positioned itself in a high-yield pre-owned CV financing business (5-year Average Yield on advances 15.45%; HDFC Securities Online, 2017).

Thirdly the company had a strong management team under the professional leadership of Umesh Revankar, an old timer in the Shriram Group who was ably supported and guided by the septuagenarian R. Thyagarajan the brain behind the group. Moreover, R Thyagarajan was a man of discipline and frugal habits. The chairman of the ₹760,000 million worth Shriram Group did not use a mobile and drove a hatchback (a Hyundai Santro). The group also had a tradition of having strong independent board of directors who contributed to the overall strategy of the company (Choudhary, 2014).

The Precursor to the 19 August Meeting

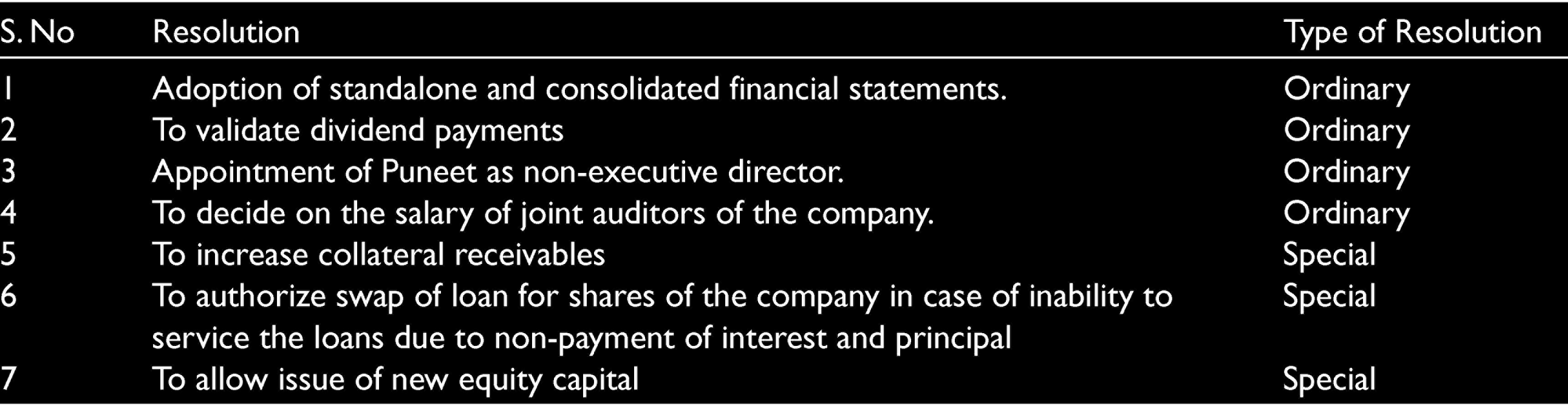

STFC was supposed to have a general body meeting on 19 August 2020. There were seven resolutions that were slated for voting. The details of the same have been captured in Table 1.

List of Resolutions: STFC’s Annual General Meeting (AGM)

The third resolution pertained to the re-appointment of Puneet as a non-executive independent member of the board of directors of the company. Puneet, was in charge for the operations of TPG Capital Asia in India. He had been a director for around one and a half decade and was due to step down as his term was over. STFC recommended continuance of his term. More than half of the votes were required in favour of the motion for passage of the ordinary resolution (Chaturvedi, 2020).

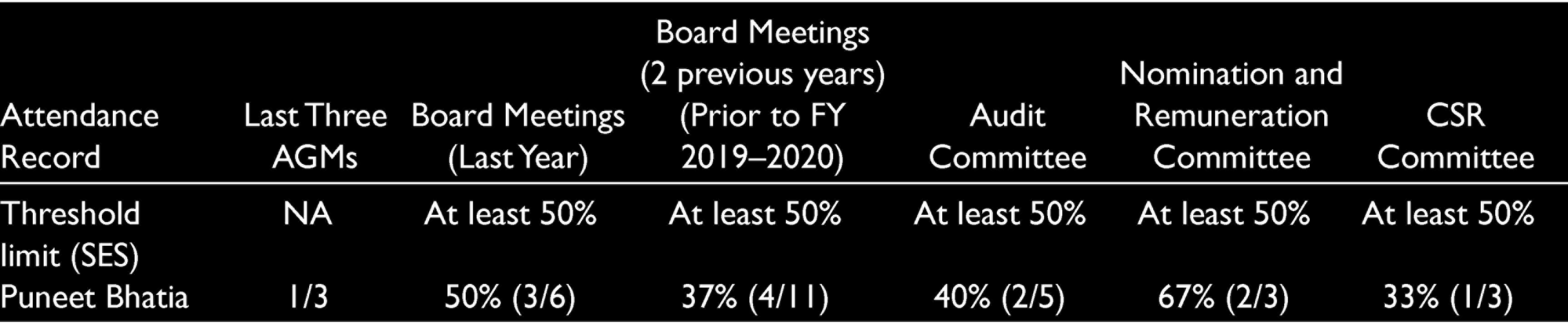

Performance of Puneet Bhatia Measured in Terms of Time Commitment

Table 2 and Table 3 capture information pertaining to the performance of Puneet in terms of his attending the meetings. Table 2 measures his performance with respect to his time commitment. Table 3 measures his performance in terms of him attending the meetings.

Performance of Puneet Bhatia Measured in Terms of Attendance

As can be seen in Table 2 performance of Puneet in terms of time commitment was satisfactory as he was not overburdened with director role keeping the statutory limit as a benchmark.

As can be seen in Table 3 performance of Puneet in terms of attendance was not satisfactory on three counts. He had not attended the stipulated number of meetings of audit committees, nomination and remuneration committees, and the board meetings in the previous two years. This cast an aspersion on his commitment levels.

Puneet and His Long Association with STFC

Puneet was spearheading the operation of TPG. His portfolio included pharmaceutical, retail and financial companies. He was also a director in his portfolio companies. Before his stint with TPG Puneet managed the Private Equity arm of GE Capital. He had also worked with ICICI Ltd as a senior analyst (Stakeholders Empowerment Services Proxy Report, 2020).

His association with Shriram Transport Corporation dated back to 2005 when TPG was looking for investment opportunities in the financial services sector in India. TPG had entered India in 2004 with an investment in the pharmaceutical sector. Leveraging on the Indian growth story the financial sector was showing exponential growth at the time so TPG started scouting for investment in the then sunrise industry. STFC was one of the first companies to attract the private equity firm’s attention. Puneet knew that it was an investment that could change TPG’s fortunes in India. However, it was not easy for Puneet to convince R. Thyagarajan—the man behind STFC to permit TPG to buy stake in the company. It took a long time for Thyagrajan to see the merit of allowing a private equity firm to buy stakes of his company (Choudhary, 2014).

However, Thyagarajan finally acquiesced. This was TPG’s foray in NBFC sector in India. Private Equity firms generally do not pursue reluctant companies. However, Puneet was impressed with the business model of STFC and believed it made sense to invest in the company. Thyagarajan let each of his companies run independently with a professional management. This was the beginning of a strong symbiotic relationship between Puneet Bhatia and Shriram Group. Puneet-led TPG Group soon increased its exposure to Shriram Group companies through its investment in Shriram Group companies which included Shriram City Union Finance, Shriram Capital and Shriram Properties. By 2014, TPG had a portfolio of $1 billion in India out of which 55% was invested in Shriram Group. This told a lot of the relationship R. Thyagarajan shared with Puneet. It was a relationship built on trust and mutual admiration (Choudhary, 2014). According to Puneet,

We don’t feel like we are dealing with one promoter or one family. The way this group is structured, it is not a typical conglomerate. All the four companies that we’ve invested in have their own distinct management teams. Each firm has a different rhythm. Investing is like a marriage; there are so many ups and downs and we can’t anticipate everything. They (Thyagarajan and Shriram Group’s board of directors) are very enlightened and treat us as partners. We would rather invest in them than seek out new businesses (Choudhary, 2014).

Shareholder Activism in India fuelled by Proxy Advisory Firms

Shareholder activism entails the attempts of the investors to cause a required change in the functioning of the business entity or to pressurize the board in managing the corporation to safeguard their rights. The success of shareholder activism to a great extent is hinged on the support provided by the company. Proxy advisors primarily served the needs of high-net-worth investors (HNI) and institutional investors by offering them with unbiased and objective analysis and views, to facilitate informed and rational decision making on both routine and non-routine matters that impacted the future profitability of the company these investors had invested in. The financial institutions hence relied on these proxy firms in the process of decision making. Their capability and experience to handle varied sectors of the economy made them apt to offer advice on how to vote at general body meetings.

The first step in India in terms of promoting shareholder activism was taken by Securities Exchange Board of India (SEBI) in 2010 when it required mutual funds listed in India to divulge their voting policies from the subsequent year. Mutual Funds in India before 2011 were concerned primarily with takeovers and major reorganization exercises of the companies they invested in (Subramanian, 2015). These domestic institutional investors did not vote on routine matters as they were not able to track changes in all the companies, they had invested in. However, the promulgation of Securities and Exchange Board of India (Research Analysts) Regulations 2014 gave teeth to the shareholder activism movement in India. This has led to emergence of proxy advisory firms. Domestic proxy advisory firms such as Institutional Investor Advisory Services (IiAS), InGovern and Stakeholder Empowerment Services (SES) emerged to get proactively involved in protecting the interests of non-promoter shareholders. With mutual fund investment becoming a popular investment vehicle the need for such proxy advisory firms had increased. Mutual Fund companies invested in a large number of companies, and it was not possible for them to follow the corporate governance practices of each of the company. Globally they relied on proxy reports for voting. In India too, the trend had been changing. In 2012–2013, financial institutions refrained from voting on more than half of the total proposals. This had decreased substantially, with around 10% of institutional voters abstaining from voting in 2017 (Mint, 2018). There had been tangible impact of the same too. An early case of effectiveness of shareholder activism in India was Indian Hotels which categorized Shapoor Mistry as an independent director in its annual report of 2012 had to show him as a non-independent director in the subsequent year due to pressure from proxy firms (Subramanian, 2015). The rejection of an increase in remuneration of certain key executives of Tata Motors by its shareholders in July 2014 was another illustration of how proxy investors were making their advice matter. Furthermore, shareholders at Raymond Ltd prevented the transfer of ownership of corporate head office at lower than fair value to the founders of Raymond Ltd (Shah Vasan, 2017).

Role of Proxy Firms in Blocking Puneet’s Re-Appointment as Non-Executive Independent Director

Table 4 captures the trend in shareholding pattern of the company in the period 2017 to 2020. The shareholders have been primarily divided into three groups: promoters and public; institutions and public; and others.

Shareholding Pattern

As can be observed from the table the share of public and others had decreased from more than 20% to less than 10% in the period June 2017 to June 2020. On the other hand, the share of institutional investors had increased to more than 65% in the period June 2017 to June 2020. This brought about a material change in the shareholding pattern. It meant that institutional investors had the power to get their resolutions passed at the general body meeting. The interest exhibited by financial institutions could be attributed to the performance of the company (See Exhibit 1) under able guidance of an independent management team. On the other hand, promoters share also increased but only marginally by 0.17% as they bought shares from the secondary market.

Table 5 shows how the proportion of institutional investors as a percentage of free float increased to almost 90% from a little more than 87% in 2019. Exhibit 2 shows the major shareholders.

The Proportion of Institutional Investors as a Percentage of Free Float

With the institutional investors having an important say in the voting process the role of proxy firms’ advice also became critical in the case of STFC. The proxy firms played an important role in the process of protecting the interest of the institutional investors as they relied on the advice of firms such as SES Advisory Services and IiAS (See Exhibit 3 and Exhibit 4 for the profiles of the firms). The proxy firms in their advisory reports provided their stance with detailed reasoning on each of the resolutions that was to be passed. It acted as a guiding light for the institutional investors.

In the case of re-appointment of Puneet as an independent non-executive director both SES (Exhibit 5) and IiAS had raised concerns. As seen in Table 2 he had low attendance in the board and governing committee meetings. Proxy Advisory Firms mandate at least 50% attendance. Puneet failed to meet the cut. However, STFC believed that even though Puneet was not regular at the meetings he was providing the requisite advisory support needed for the firm’s growth. They attributed the reservations to the fact that the proxy firms had resorted to a very stringent quantitative metrics that ignored qualitative factors such as the quality of advice given by these firms.

19 August General Body Meeting and Its Fallout

On 19 August 2020 in the general body meeting of STFC the shareholders voted against the motion of reappointing Puneet. Motion for his re-appointment failed to muster the requisite simple majority by almost 7%. The proposed resolution got 100% of the promoter’s vote. However, over 83% of the institutional investors voted against the motion based on proxy advisory firm reports. With approximately 64% of the votes controlled by these financial institutions (Refer Table 4 and Table 5), the promoters could not get the resolution passed.

The proxy advisory firms such as SES and IiAS which had advised the institutional investors to vote against the motion were happy and believed it was a victory for shareholder activism in India.

According to Amit Tandon, an expert and renowned shareholder activist in India,

A director is no more an ornament for the company or a badge for an individual. Investors expect directors to be more engaged with companies whose boards they serve on. In the absence of any parameter on this, board attendance is seen as a surrogate measure of board-level participation (Modak, 2020).

However, STFC did not concur with the view of the proxy advisory firms. Proxy voting companies are often decried by affected organizations for adhering to objective yardsticks such as turnout in the meetings. The company in a press release termed the decision of the shareholders to stall the passage of the re-appointment of Puneet Bhatia solely on his not attending meetings as ‘unfortunate’ (Unnikrishnan, 2020).

However, this was not the end of the story. STFC refused to relent and within ten days of the meeting decided to re-appoint Puneet as a nominee of the promoter. The company felt that he had contributed enough and hence deserved to be a director. However, the proxy advisory firms such as IiAS and SES questioned the decision. Amit Tandon, CEO, IiAS, believed that the committees which appointed him were answerable to the shareholders who had stalled the reappointment in the first place and had hence failed to protect the interest of the shareholders (Chaturvedi, 2020).

TPG finally intervened and directed Puneet not to join. He was asked to respect the decision of the shareholders (Modak, 2020).

Conclusion

Shareholder activism has gained traction and proxy advisory firms are now being taken seriously. The same is evidenced in STFC shareholders saga. The success of proxy advisory in protecting non-promoters’ interests is contingent on how seriously the financial institutions take the advice of the shareholders and the total percentage of voting rights they have. In the case of STFC the financial institutions due to the professional attitude of the company had found the company investment worthy. Ironically, this was what built the symbiotic relationship between Puneet and STFC in the first place. The role of TPG to direct Puneet to accept the decision is also commendable. The incident would definitely go a long way in creating a conducive environment for developing an effective corporate governance ecosystem in India which is traditionally dominated by closely held promoter led management system.

As far as the proxy firms are concerned, they now wield a lot of control on the voting pattern of financial institutions. However, the metrics that the firms use as rightly pointed out by the company is highly quantitative. This may impact their ability to take the right decision. Over time it is pertinent to evolve a more robust methodology of recommendation and also take into consideration the views of the company through direct interactions with key personnel in the company. Moreover, financial institutions which hold stake in companies on behalf of their investors also has a fiduciary duty to exercise discretion in accepting the advice given by the proxy advisory firms.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Appendix

SES Views on Reappointment of Puneet Bhatia

| Mr Puneet Bhatia retires by rotation at the ensuing AGM. No concern has been identified regarding his profile and time commitments. However, he has attended less than 50% Board Meetings held in FY 2017–2018 and 2018–2019. Further, in FY 2019–2020 also he attended only 50% of the Board Meetings. He also attended only 40% Audit Committee Meetings. Based on the above, SES is raising a concern in the appointment of Mr Puneet Bhatia due to low attendance. |