Abstract

On one monthly time-series data set of Vietnam economy over 02/2008–09/2018, the Time-Varying-Coefficient VAR model records that the trade-off between inflation and output growth is mitigated by the foreign capital inflows. The inflation is mostly determined by credit supply growth, while output growth is largely driven by foreign direct investment (FDI) capital inflows. A monthly increase of FDI by USD 1 billion can raise 1.77% of monthly output growth rate. The result also holds on accounting for exchange rate fluctuation.

Keywords

Introduction

Within the recent financial globalization phenomenon over last decades, the soundness of macroeconomic fundamental is more and more important. Rey (2015) stresses that the policy trilemma on international finance, including free cross-border capital flows, exchange rate management and independent monetary policy, becomes a dilemma between exchange rate regime and domestic financial condition. Recently, Obstfeld et al. (2017) show that the exchange rate is one channel for one open economy to absorb the shocks from world economy into domestic economic growth and inflation.

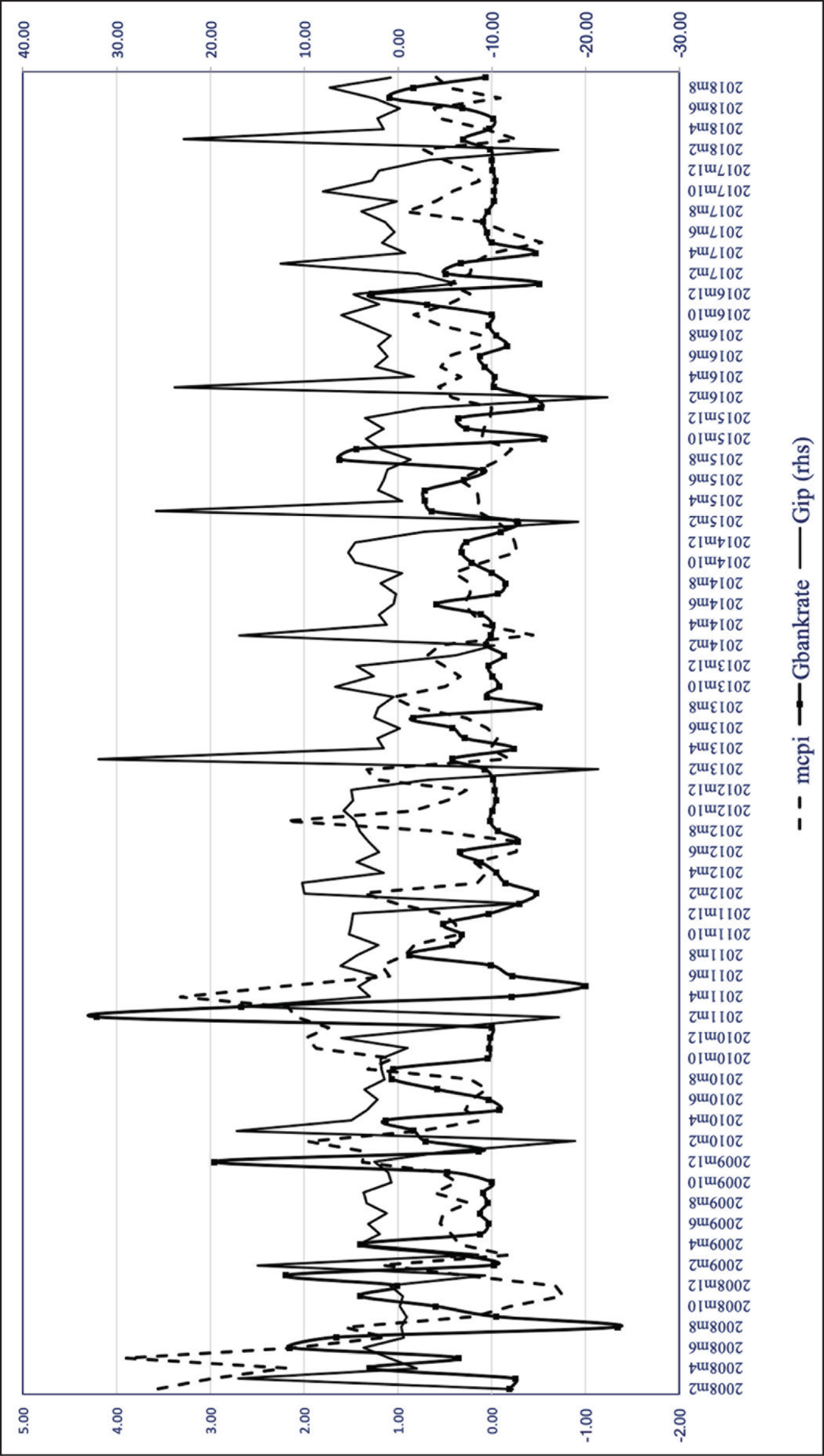

Figure 1 shows the case of Vietnam which is a small open economy with profound financial integration. Over 02/2008–09/2018, the output growth has a quite stable mean and variance while the inflation rate has a lower mean and less variance since 01/2013. This stylized fact imposes an open question on the existence of output-inflation trade-off, which is a cornerstone of macroeconomic fundamental. Our article aims to fill in the gap.

We employ a Time-Varying-Coefficients Vector Autoregression (TVC-VAR) model to analyse the output-inflation trade-off. First, the model accounts for the interaction of three variables: output growth, inflation rate and depreciation rate of domestic currency. This structure captures the role of exchange rate as a key variable of macroeconomic fundamental. As Figure 1 shows, the depreciation rate of domestic currency (Vietnam Dong, VND) follows closely the fluctuation of inflation rate. Second, the model also includes the foreign capital as an exogenous variable. This set-up stresses the role of foreign capital inflows as a channel for world economy to exert an one-way impact on a small open economy such as Vietnam and Singapore.

The model is based on a time-series data of 128 observations covering 02/2008–09/2018 for Vietnam economy. In particular, Vietnam is a small open economy with an in-dept integration into the world economy. Its sum of export and import of goods and service accounts for nearly 200% of gross domestic product, as recorded by the General Statistics Office of Vietnam. Moreover, this developing economy has maintained a high economic growth rate and stable inflation rate for recent years. Therefore, the timeseries analysis on the Vietnam economy can shed a new light on the trade-off between output growth and inflation rate.

We show that the output-inflation trade-off is mitigated by the foreign capital inflows. In particular, on baseline model with three endogenous variables including the output growth, inflation and credit growth rate, a higher credit growth rate raises both the output growth and inflation rate. On adding the foreign direct investment (FDI) capital inflows into the baseline model, the credit growth rate has an insignificant impact on the output growth rate but still raises the inflation rate. And more FDI inflows push up the output growth rate. The result also holds for extended model which adds the exchange rate as an endogenous variable into the baseline model. Therefore, the output growth is largely driven by the foreign capital inflows while the inflation rate is mostly determined by the credit growth rate.

The article belongs to the literature on the output-inflation trade-off, which is motivated by one seminal paper by Lucas (1973). The author shows the existence of output-inflation trade-off on an international evidence. Ball et al. (1988) study the trade-off by a panel data sample. They find that the trade-off is affected by the average rate of inflation. On a cross-section data of 91 economies, Badinger (2009) confirms that globalization, measured by higher trade and financial openness, is associated with larger output-inflation trade-off. Recently, Justiniano et al. (2013) prove that there is no trade-off between inflation and output stabilization, in an estimated Dynamic Stochastic General Equilibrium (DSGE) model of United States economy, which accounts for worker’s market power. On the case of India economy, Behera and Mishra (2017) argue that there is a structural break in the relationship between inflation and economic growth. If the inflation exceeds 4%, it will negatively affect the economic growth.

Our article differs these aforementioned papers by two key features. First, we analyse the trade-off on one small open economy with controlled floating exchange rate regime. The context stresses the interaction of exchange rate fluctuation with both output growth and inflation rate. Second, we account for foreign capital inflows as an important driver of the trade-off. And this feature is crucial for the case of developing economies which attract the foreign capital flows to compensate the domestic investment.

Our article is closely related to the literature on the international capital flows. Borensztein et al. (1998) show that the foreign direct investment (FDI) capital inflows have a positive effect on the economic growth by the transfer of technology. Moreover, the domestic productivity improves only when the host country has a minimum threshold stock of human capital. Prasad et al. (2007) find that the FDI capital inflows can raise the domestic economic growth if the host economy has a high enough level of financial development. Recently, Gnangnon (2020) records that a greater trade openness exerts a positive and significant impact on the diversification of external financial flows for development, especially in the least developed countries.

Our article complements these papers by employing a monthly sample to show that the foreign capital inflows can raise the economic growth. Thus, the result provides short-run evidence as complementary to the long-run results recorded on the aforementioned papers. Moreover, the foreign capital can even play more important role than the domestic monetary supply on driving the economic growth. Thus, the foreign capital inflows can crowd out the domestic capital investment on determining the economic growth.

Next, the second section presents empirical model and characterizes the data sample. The third section presents the evidence on output-inflation trade-off under impact of foreign capital inflows. And the fourth section concludes the article.

Framework

Empirical Model

We build up a baseline model to analyse the trade-off between the output growth and inflation rate. There are three endogenous variables including output, inflation and monetary supply. On theory (Krugman et al. (2018)), a higher money supply can raise both the output growth and inflation rate. Thus, there is a trade-off between output growth and inflation: a higher output growth is associated with a higher inflation rate. Moreover, the model has an exogenous variable including the foreign capital inflows. This variable captures the context of a small open economy. In particular, since the small open economy takes the world capital market as given, the foreign capital exerts an one-way impact on the domestic economy. Thus, the FDI capital inflows are considered as an exogenous variable on the model.

Our model investigates the role of FDI capital inflows on determining the trade-off between output growth and inflation rate. First, recent evidence records the crucial role of FDI on the economic growth. Prasad et al. (2007) shows that the foreign capital has a positive impact on the economic growth when the home country has a high financial development level. On the context of Vietnam economy, the FDI even builds up an economic sector which account for 20% of GDP, 71% of exports and 60% of imports in 2018, as recorded by the General Statistics Office (GSO) of Vietnam. Second, within the controlled floating exchange rate regime, an economy can only take care of exchange rate management and independent monetary policy, due to the existence of policy trilemma. The foreign currency induced by the foreign capital inflows needed to be absorbed by the monetary policy by central banks. The foreign exchange market intervention, in turn, opens a channel for the foreign capital to affect the inflation rate. In brief, the foreign capital inflows are potential to affect the relationship between output growth and inflation.

Next, we build up an extended model by adding the depreciation rate of domestic currency on the baseline model. In particular, the trade-off between the output growth and inflation rate can be affected by exchange rate fluctuation. The exchange rate depreciation can raise the output growth through the stimulation of exports. Moreover, it also affects the inflation by the impact on the price of import goods, as well-known exchange rate passthrough literature. Therefore, a full model with output growth, inflation and exchange rate can shed an additional light on the output-inflation trade-off under impact of foreign capital inflows.

We employ a Time-Varying-Coefficient Vector Autoregression (TVC-VAR) model to investigate the trade-off between output growth and inflation rate in Vietnam. On Figure 1, there exists a changing regime of economic fundamentals (economic growth, inflation and VND depreciation rate) over time. In details, both mean and variance of these macroeconomic variables reduces substantially after 01/2013, and also decrease again after 12/2015 when the central bank adopts the controlled floating exchange rate regime. In Cogley and Sargent (2001), the TVC-VAR is also employed to analyse the changes on pattern of macroeconomic variable in case of United States. In brief, the TVC-VAR is adequate to capture the observed pattern of macroeconomic variables in Vietnam.

The TVC-VAR model can be expressed as:

yt = (mcpit, Gipt, Gbankratet, Gcreditt) is a 4x1 vector of endogenous data, including the inflation rate (mcpit), output growth rate (Gipt), VND depreciation rate (Gbankratet) and credit supply growth rate (Gcreditt). A1,t is a matrix of dimension 4x4, C is a 4x1 vector of exogenous regressor which are the foreign capital inflows (Fdit). And єt = (є1jt, є2,t, є3,t, є4,t) is a vector of residuals following a multivariate normal distribution.

The VAR coefficients are assumed to follow the autoregressive process:

The covariance matrix Ω is assumed to be a random variable endogenously determined by the model.

The parameters of interest to be estimated include the VAR coefficients β = {β1,…, βT}, the covariance matrix Ω for the shocks on the dynamic process, and the residual covariance matrix Σ. The estimation is based on the Bayesian Estimation, Analysis and Regression toolbox (BEAR), developed by Dieppe et al. (2016).

Data Description

The dataset is one monthly time series sample with 128 observations for Vietnam, from 02/2008 to 09/2018. The inflation rate, denoted by (mcpi) on percentage, is the monthly growth rate of consumer price index. The output growth rate, denoted by (Gip) on percentage, is the monthly growth rate of real industrial output. These variables are from Vietnam’s GSO. The daily exchange rate is measured as the number of domestic currency units (VND) per one unit of US dollar (USD). The exchange rate is close rate in the Vietnam interbank market. Then, we take the VND depreciation rate, denoted by (Gbankrate) on percentage, as the change of exchange rate between two consecutive months. These two variables are explored from Reuters database.

The credit supply is the difference between the credit from banking system to domestic firm and the deposit from households to banks. Then, we take the growth rate of credit supply between two consecutive months. This data is from State Bank of Vietnam. Finally, the foreign capital inflows are measured by the monthly disbursed foreign direct investment, which is from the Vietnam’s GSO.

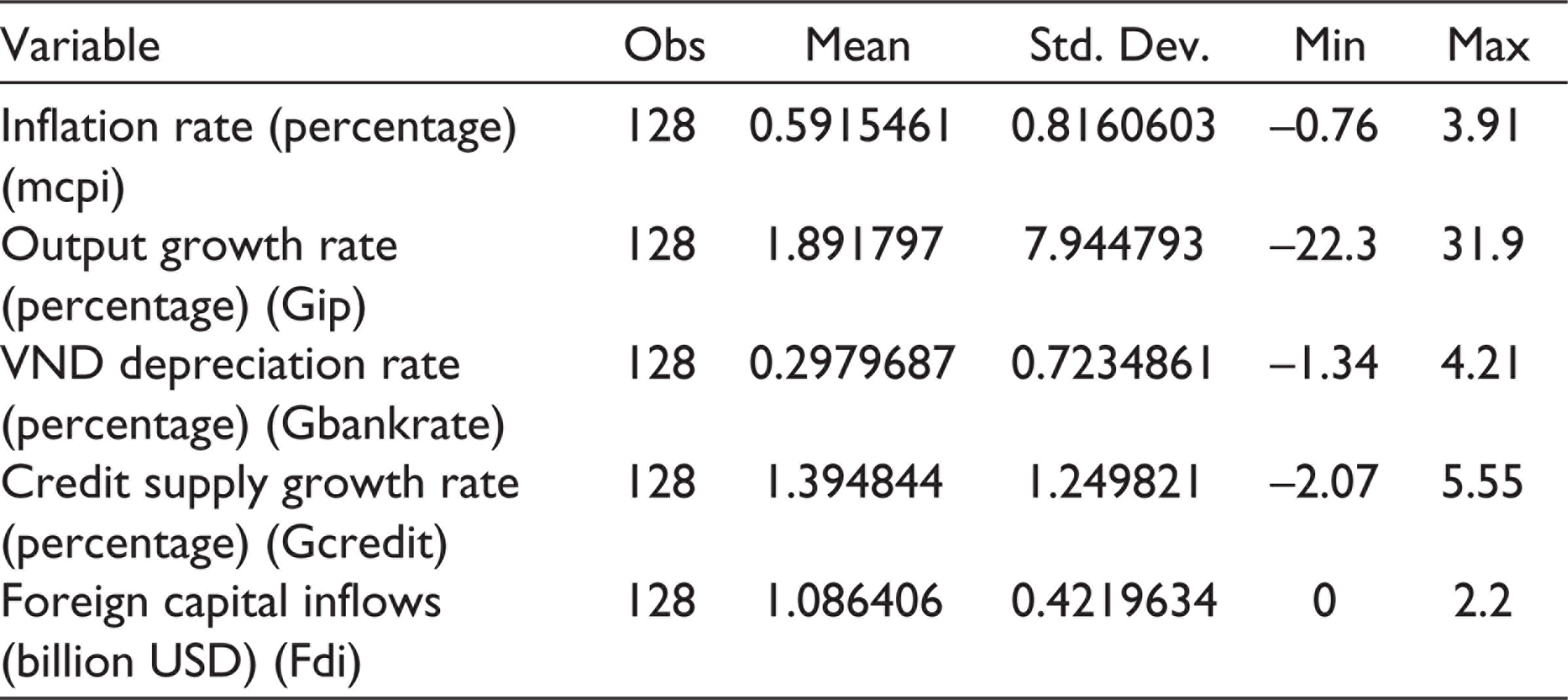

Table 1 reports the descriptive statistics on the sample. The inflation rate has a mean of 0.6% with a standard deviation of 0.82%. The output growth rate has a higher mean, 1.89%, and a higher standard deviation, 7.94%. The VND depreciation rate has a mean at 0.29%, and a standard deviation at 0.72%. Compared with this variable, the credit supply growth rate has both a higher mean at 1.39% and a larger deviation at 1.24%, while the foreign capital inflows has a higher mean at 1.08% but a lower deviation at 0.42%. In brief, the data set offers rich variation for exploring the relationship between the output growth and the inflation rate.

Descriptive Statistics.

Evidence

Output-inflation Trade-off

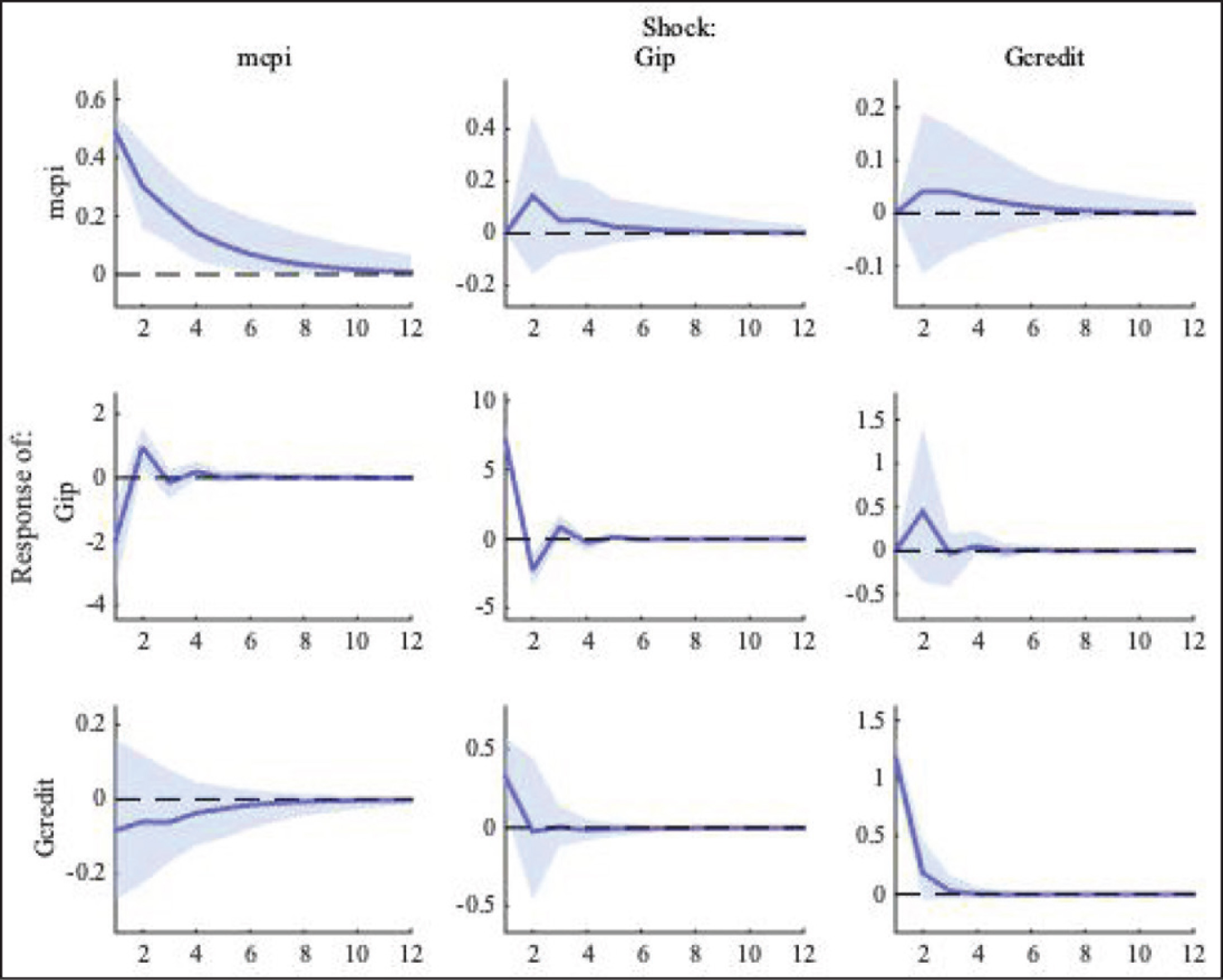

Figure 2 presents the evidence on the trade-off between the output growth and inflation rate on the baseline model. On the first row, a shock of an increase of 1% on the credit supply growth rate raises the monthly inflation rate by a maximum of 0.028% at the 2nd month, then the effect decreases gradually and dies out at the 8th month. On the second row, the shock also raises the output growth rate by a maximum of 0.4% at the 2nd month, then the effect dies out immediately at the third month. Therefore, a credit growth policy which accelerates the output growth also induces a higher inflation rate. This evidence illustrates the trade-off between the output growth and inflation rate.

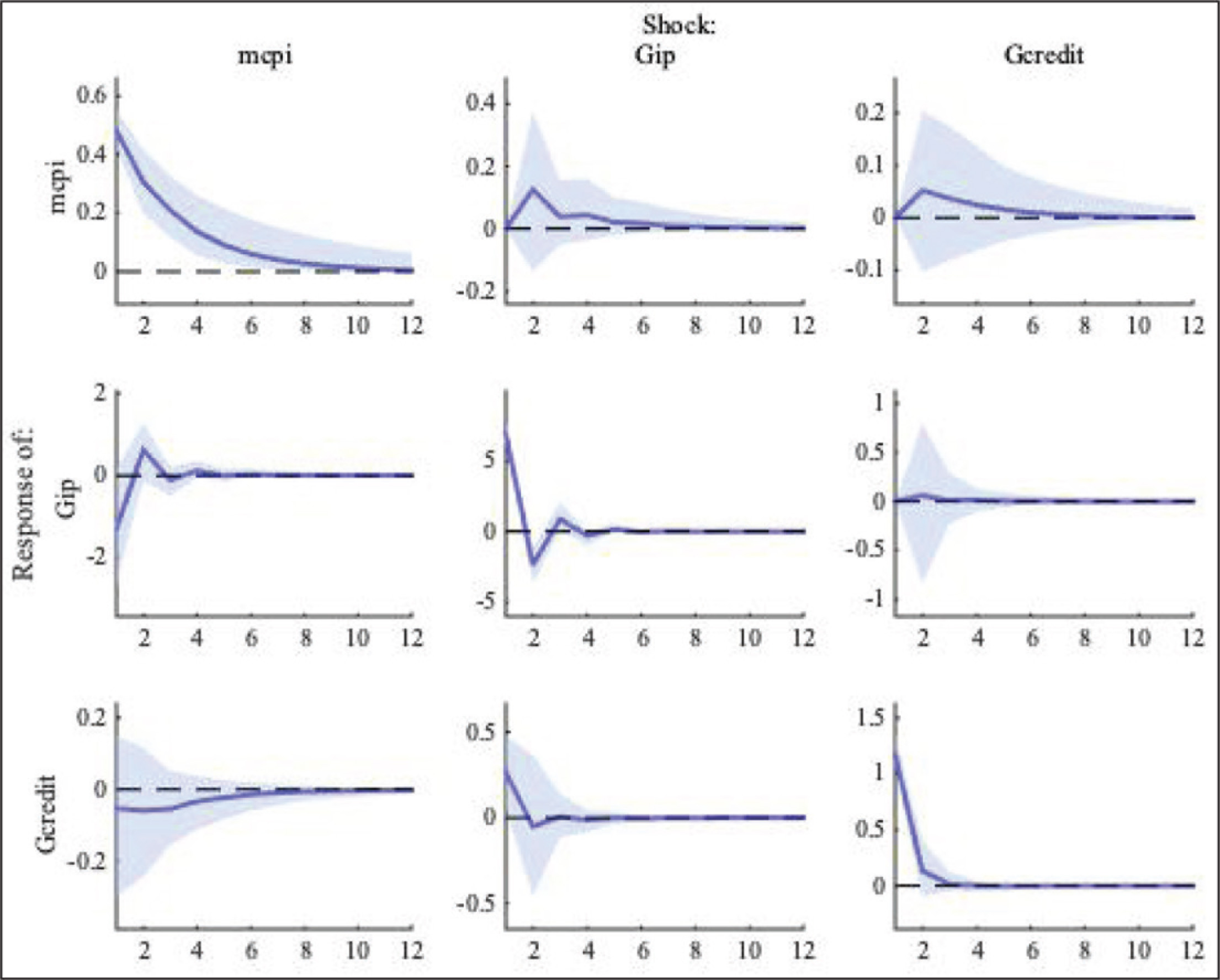

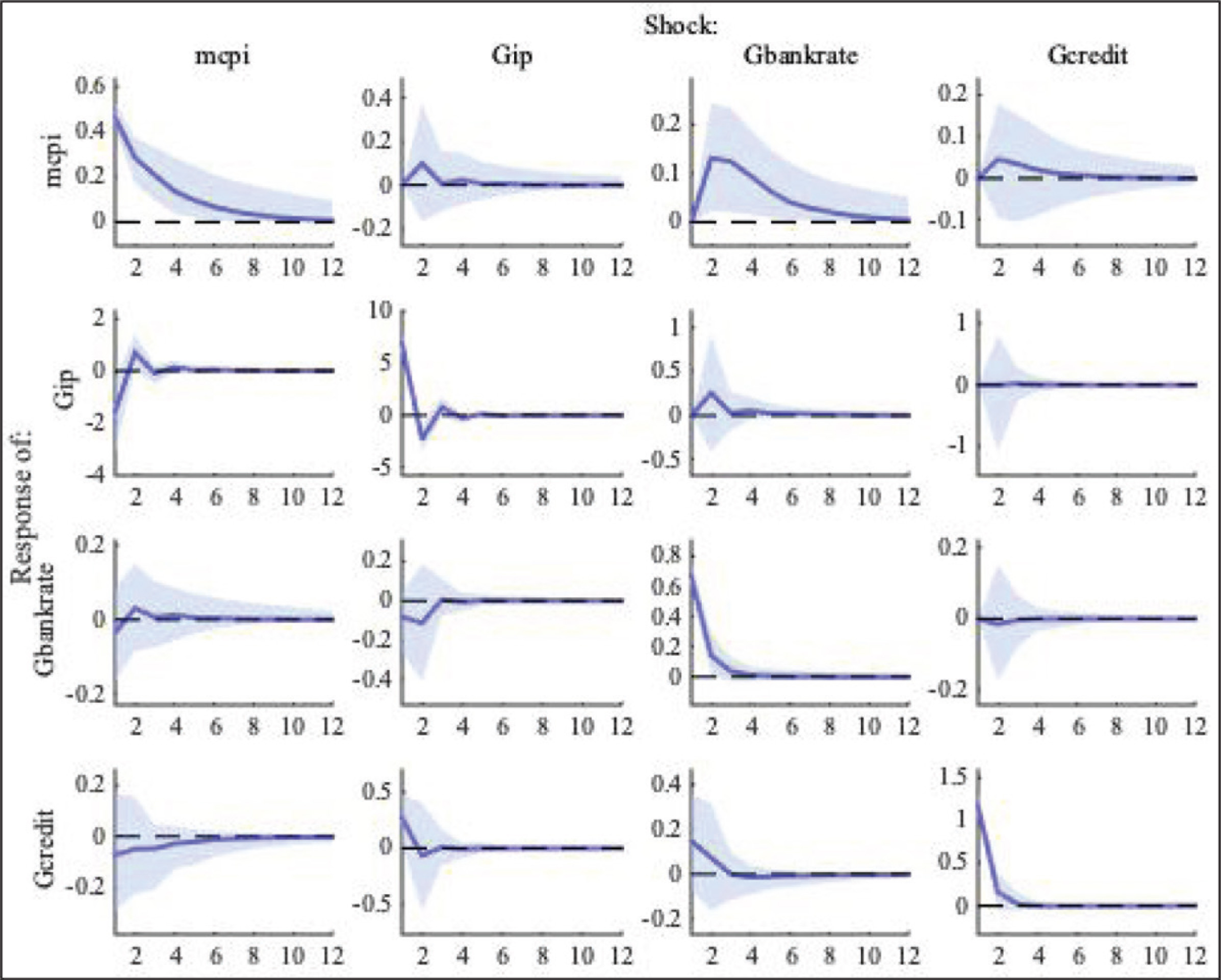

Figure 3 shows the output-inflation trade-off on accounting for the foreign capital inflows. On the first row, a higher credit supply growth still levels up the inflation rate, a standard result recorded on Figure 2. In particular, a shock of an increase of 1% on the credit supply growth rate raises the monthly inflation rate by a maximum of 0.045% at the 2nd month, then the effect decreases and dies out at the 8th month. On the second row, the credit growth rate exerts a negligible impact (approximately 0%) on the output growth rate. Thus, the addition of foreign capital inflows mitigates the influence of credit supply on the output growth rate. Furthermore, the foreign capital inflows have a significantly positive impact on the output growth rate (not shown in Figure): an additional USD 1 billion of FDI raises the output growth rate by 1.85%. In brief, the inflation rate is mostly affected by the credit growth rate while the output growth rate is largely driven by the foreign capital inflows.

Extended Model with Foreign Exchange Rate

Figure 4 illustrates the regression result of output-inflation trade-off on the extenbded model with foreign exchange rate. On the first row, a shock of an increase of 1% on the credit supply growth rate raises the monthly inflation rate by a maximum of 0.033% at the 2nd month, then the effect decreases and dies out at the 6th month. On the second row, however, the shock exerts a, insignificant impact on the output growth rate. These results are consistent with the recorded result on Figure 3 for the baseline model. In brief, on the extended model with the exchange rate, the foreign capital inflows still reduce the magnitude of trade-off between the inflation and output growth rate.

The analysis sheds a new light on the macroeconomic fundamental at financial integration. In Vietnam, from 2008 to 2018, the average of disturbed FDI is USD 1.09 billion per month. By the empirical evidence, an additional USD 1 billion of FDI raises the output growth rate by 1.767%. Thus, when there is a sudden stop of FDI for one month (USD 1 billion of FDI does not flow into the Vietnam economy), the output growth rate of that month reduces immediately by 1.767%. Therefore, for a stable macroeconomic fundamental, an economy needs to insure against the risk of sudden stops of FDI capital inflows.

Case Study: 1997 Asian Financial Crisis

The financial crisis in East Asia follows the collapse of the Thai baht in July 1997. Corsetti et al, (1999) show that the crisis reflects the structural and policy distortions in the countries of the region. As recorded by World Development Indicators (WDI) database, the output growth rate of 1998 also dropped from that of 1997 by –1.3% in China, –11.3% in Republic of Korea, –10.5% in Singapore, –4.8% in Thailand and –2.3% in Vietnam. And the inflation rate also fell by –3.5% in China, –2.3% in Singapore while raised by 3.0% in Republic of Korea, 2.3% in Thailand and 4.0% in Vietnam. In brief, the different experiences across countries in the crisis provide useful case study for the trade-off between the output growth and inflation rate.

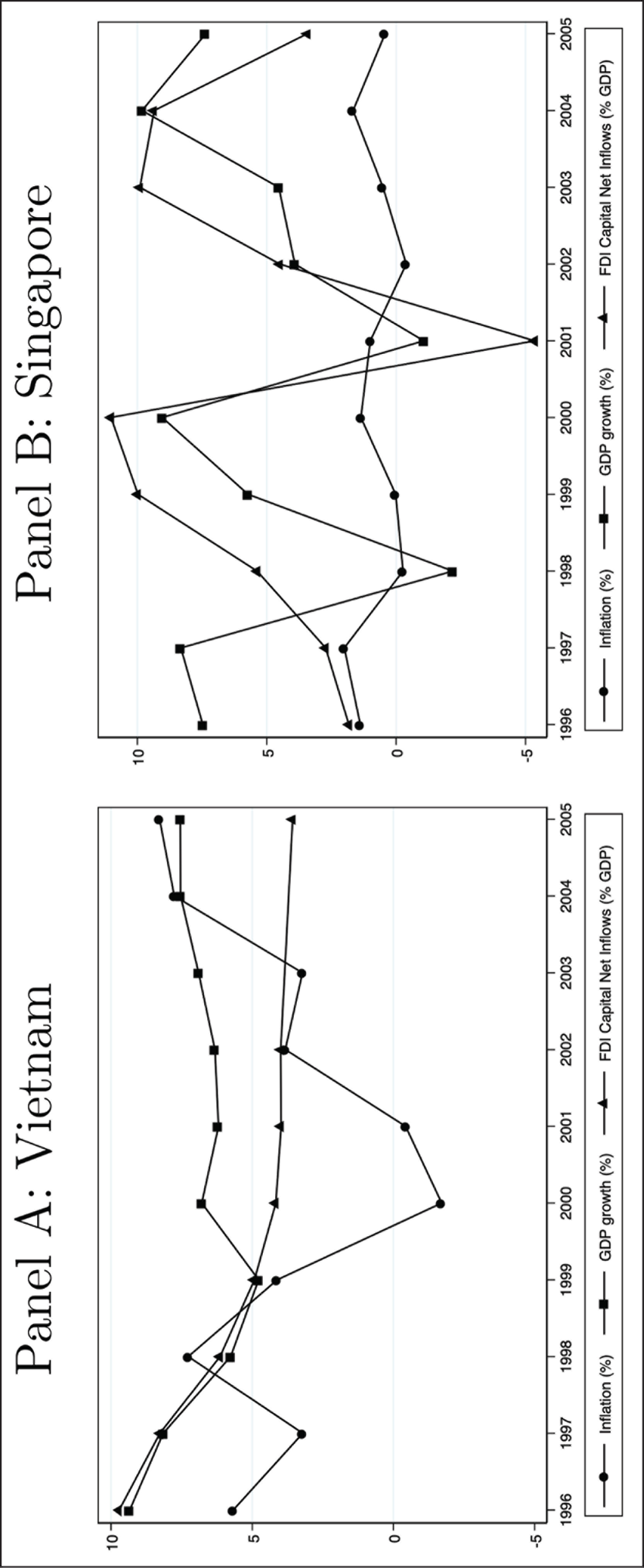

Panel A of Figure 5 illustrates the dynamic of growth and inflation in the Vietnam economy during the 1997 Asian financial crisis. There exists a trade-off between the output growth and inflation rate, which is more clearly observed for the 2000–2005 period. In 1998, a lower output growth rate goes along with a higher inflation rate. Thus, the trade-off seems to break on the time of financial crisis. Our empirical evidence suggests that the decrease of output growth rate is largely driven by the reduction of foreign capital. In fact, the decrease of output growth is closely accompanied by the reduction of FDI net capital inflows from 1996 to 1999. The output growth rate goes down from 8.15% in 1997 to 4.7% in 1999 while the FDI per GDP ratio reduces from 8.27% in 1997 to 4.9% in 1999, as recorded by WDI database. At the same time, the money supply in Vietnam also increases from 12.54% in 1997 to reach a peak at 50.49% in 1999, as recorded by International Financial Statistics (IFS) database. Thus, the effect of money supply on the output growth seems to be modest during the crisis. In brief, the foreign capital inflows can crowd out the domestic money supply on determining the economic growth.

Panel B in Figure 5 shows the case of Singapore. There exists a trade-off between output growth and inflation rate in Singapore during 1996–2005, excepting in 2002. In particular, the output growth rate is closely accompanied by the net FDI capital inflows. For instance, the output growth rate raises from –2.19% in 1998 to 9.0% in 2000, while the FDI net inflows per GDP surges from 5.3% in 1998 to 11.9% in 2000. At the same time, the growth rate of domestic money supply also raise from –13.33% in 1998 to 28.57% in 1999, before falling to –13.67% in 2000, as recorded by the IFS database. Therefore, in comparison with the money supply, the foreign capital inflows have a stronger impact on the output growth in Singapore during the 1997 financial crisis.

Conclusion

We show that the trade-off between inflation and output growth is affected by the foreign capital inflows. The inflation rate is mostly determined by the growth of credit supply, while output growth is largely driven by the foreign direct investment capital inflows. The evidence is based on a TVC-VAR model, which captures the switching regime of economic fundamental in Vietnam over time.

The result provides important policy implication. Since the foreign capital inflows can affect the domestic output-inflation trade-off, it raises an additional constraint for domestic monetary policy. Thus, the monetary policy needs to be equipped with a public policy to relax that constraint. For example, reducing the dependence of domestic output growth on the foreign capital inflows can be an important policy to improve the effectiveness of monetary policy.

For future research avenue, the model can be extended to investigate the impact of world shocks, such as change of world interest rate or oil price’s shock on a small open economy like Vietnam.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.