Abstract

Abstract

Micro and small enterprises (MSEs) have been found to be engines of growth, drivers of production, income generation, job creation, and tools for poverty reduction. The source of microfinance is important because at the center of every enterprise objective is profitability. MSEs in South-East Nigeria have not played these important roles effectively due to the challenges of access to finance and a host of other factors. The main thrust of this article is to evaluate the effectiveness of informal microfinance sources on the profitability of MSEs in Southeast Nigeria. The study employed a multistage sampling technique in cluster selection from three industrial cities and generated relevant data through questionnaires. A sample of 540 enterprises out of 1994 enterprises was selected across different clusters comprising enterprises under production, trade, and services in the three cities. Employing a regression technique, the study found that informal microfinance sources have impact on the profitability of MSEs. The study further found that enterprises patronized the informal source because of quick responses and personal relationship (social capital). The study recommends that microfinance policy framework and interventions should encourage official microfinance providers to have their location closer to the enterprise clusters with the appropriate regulatory guarantee for operators.

Introduction

Background, Conundrum, and Objective

The role of micro and small enterprises (MSEs) cannot be overemphasized because of their potential in driving economic growth and development. MSEs contribute about 30 percent of global gross domestic product (GDP) and account for about 58 percent of the global working population (Kushnir, Mirmulstein, & Ramalho, 2010). They are numerically leading in the provisions of employment and have become prime sources of new jobs across different developing countries. MSEs currently play the critical role of being a safety net for the bulk of the population in developing economies including Nigeria.

In February 2003, the International Finance Corporation (IFC) and the World Bank engaged Skoup and Company Ltd. in a cluster development program in South-East Nigeria that covered the administrative and infrastructure costs’ survey. The survey results envision an MSEs sector that can deliver maximum benefits of employment generation, wealth creation, poverty reduction, and sustainable economic growth for not only the South-East in particular but for the entire country. This was encouraged by the IFC because of the belief that firms or enterprises that operate in clusters have proven to be able to engineer “rapid economic growth, sustainable leadership in export markets, significant employment generation and preservation of high-value added jobs.” Equally, studies have shown that MSEs operating in clusters provide faster economic development, poverty reduction, and social equity (UNIDO, 2006).

These clusters located in South-East Nigeria and other parts of the country have been part of the driving force of the country toward achieving her dream of becoming industrialized. In an effort to realize this goal, Nigeria’s Vision 20:2020 and the Economic Recovery and Growth Plan (ERGP) of 2017–2020 have highlighted different measures to enhance the ability of MSEs, especially those found in these clusters, to compete effectively through increased productivity, greater technological efficiency, and reduced cost of doing business. In this context, the growth and competitiveness of these MSEs clusters have become the key objectives of the national policy on MSEs.

The Nigerian government, in line with her dream, through the different tiers (federal, state, and local) has shown some level of commitments, budgetary allocations, and policy pronouncements to harness the contribution of MSEs to the economy. Details of such commitments and policies have been documented by Essien, Arene, and Nweze (2013). Even local and international donor agencies have been inundated with requests from nongovernmental agencies and organized private sector associations for grants and other forms of assistance to the sector.

Despite the above interventions, according to Kpakol (2007), the performances of MSEs in Nigeria, particularly in the clusters of the South-East region, have been affected by myriads of problems like poor infrastructure (inadequate power supply, bad roads, and poor transportation system), financial access, poor corporate governance, insecurity, and the hostile legal framework. At the core of these problems has been access to finance, partly for the fact that MSEs in these clusters prefer to operate informally which resulted in formal financial arrangements shying away from extending credit facilities to such operators. Consequently, majority of the operators resort to informal sources like, Isusu (thrift), family and friends, cooperative societies, and trust fund models (TFMs) such as self-help group contribution (SHGC) and nongovernmental organizations (NGOs). Unfortunately, these sources have limitations in ensuring effective contribution of MSEs to economic growth and sustainable development. This has led to the further bolstering of the Nigerian Microfinance Policy in 2018 by the current Central Bank of Nigeria to boost financial inclusion to reduce dependence on informal sources by MSEs operating in different clusters across the country.

This study, therefore, is an effort to assess the effect of these informal sources of credit (microfinance) facilities and how it has affected the profitability of MSEs in these clusters. This is important because if these MSEs fail to make profits, the dependence on them for wealth creation, poverty reduction, employment generation, and sustainable economic growth becomes a mirage. Such MSEs clusters in Southeast Nigeria are found within the industrial clusters of Nnewi, Onitsha, Aba, and other emerging locations in the region. Interestingly, these clusters have the advantage of proximity to several raw materials which makes it possible to produce associated semifinished or finished goods in a cheap way. Thus, this study set out to find how effective microfinance from informal sources affects the profitability of operators across MSEs clusters in Southeast Nigeria.

Literature Review

This study hinges on Perroux’s (1950) growth pole hypothesis that referred to a growth pole as “a place of passage of forces, which attracts men and objects to it and also repels them.” It further referred to the growth pole as a center “from where centrifugal and centripetal forces operate.” Boudeville (1964) had polarized a region that is characterized by the dominance of a regional center (growth space) to which all flows such as goods, services, capital, ideas, or political allegiance are predominantly directed. The regional center or growth center links a heterogeneous continuous area into interdependent and interregional units. According to Lasuen (1969), the spatial investment strategy of growth centers purports to advance developmental efficiency and equality goals, and has thus become the predominant investment policy strategy in many countries, especially the developing ones.

Basically, it is held that “growth does not appear everywhere at the same time; it manifests itself in points or ‘poles’ of growth; with variable terminal effects for the economy as a whole” (Perroux, 1950). In a specifically geographic sense, a growth center has been defined as “... a centre of the city with bubbling economic activities having the capacity for self-sustenance” (Merges, Papadaskalopoulos, Christofakis, Arseniado, & Kalliri, 2004). Thus, initially, growth is held to be concentrated at a matrix of favorable points, and subsequently the growth impulses so generated are diffused to the neighboring area referred to as “the growth space.” Hence, according to Merges et al. (2004), “...the longitudinal occurrence of economic growth is a function of distance from the city centre otherwise regarded as the growth poles which in the case of South-East Nigeria are the clusters”. The growth potential of a region is thus held to be closely related to the “intensity of interaction” between the growth center and its surrounding regions. Indeed, it has been argued that “the spatial structure of a region and the size and spacing of its towns may be the crucial factors in explaining regional potential” (Lasuen, 1969), hence the popularity of the concept using industrial or enterprise clusters in developing nations, including Nigeria.

Industrial/enterprise clusters are a typology of a growth pole. In Nigeria, the federal government’s Integrated Rural Development Approach comprises Agricultural Development Projects or the World Bank Projects (WBPs); the Farm Settlement Schemes; the River Basin and Rural Development Approach; and the Local Government Reform of 1976. These were all deliberate interventionist planning policies aimed at developing the rural areas based on the diffusion and growth center models. As a result of the 1976 Local Government Reform, for instance, 301 local government headquarters emerged as new lower-order growth centers that would facilitate a more even and faster grassroots-oriented development. Similarly, the Agricultural Development Programme (ADP) or the WBPs and, lately, the River Basin and Rural Development Authorities’ Projects (RBRDAPs) were designed to serve as growth centers from where ideas, techniques, and innovations in agriculture would diffuse to the wider hinterland.

In line with the study objective, it is imperative to energize industrial clusters as “growth poles” or centers of industrial experiments for interventions. Understanding the existing credit (microfinance) processes to their operators and their limitations would help inform and determine new and more effective strategies to be adopted in making the industrial clusters “growth poles” in name and indeed. Since microfinance to such clusters positively affects the poor, women, and small-scale enterprises (SSEs), such a framework will make the SSEs contribute effectively toward economic growth which will lead to sustainable development. Different studies in Nigeria and across other developing countries have looked into how these clusters or growth poles help in achieving the intended objectives of providing sustainable leadership in export markets, rapid economic growth, as well as significant employment generation, and such studies include, but are not limited to, the following: Mano, Iddrisu, Yoshino, and Sonobe (2011) in their study examined the process through which MSEs in clusters across Sub-Saharan Africa (SSA) including Nigeria can become productive. Their study found performances of these MSEs to be quite low across all countries including those in Nigeria. While the study ascribed the poor performance to factors outside enterprise problems, within enterprise, analyses were rarely scrutinized. In fact, some of the entrepreneurs in some selected clusters were unskilled in the current standard business practices. Based on a randomized experiment in Ghana for example, the study demonstrated that basic-level management training does improve business practices and performance.

Another study by Loca and Kola (2013) analyzed the extent to which microfinance services in Albania affected the activities of entrepreneurs, and if there are companies that benefited in their clusters. For the study to achieve its objective, it has to focus on impacts to different aspects of microfinance. Qualitative and quantitative methods were combined to arrive at different indicators that were addressed to beneficiaries. Qualitative data were collected through interviews, focus group discussions (FGDs), and semi-structured interviews to understand the situations that entrepreneurs faced and how they used and perceived microfinance, especially enterprises serviced by microfinance across the country. The results suggested a strong relationship between being microfinance institution (MFI) clients and the variation in enterprise profits over a 1-year period. The study concluded that lending practices from formal sources have positive effect on some entrepreneurial activities.

Furthermore, Kessey (2007) examined microcredit as it affects small and medium enterprises (SMEs) promotion in the Ghanaian informal sector. The study found that entrepreneurs of MSEs whose repayment cycle is on a monthly basis recorded a 2.8 percent default rate as against a default rate of 6.5 percent for entrepreneurs that pay on an annual basis. The study recommended extension of MFIs to enterprises operating in the informal clusters. The study argued that this recommendation will help to improve performances through trainings offered by MFIs as well as to boost their overall performance. This was based on an observation that only informal sources of credits might not be able to move entrepreneurs of MSEs out of poverty in the third world countries where economies have different and ever-changing structures.

In the Nigerian context, not so many works have examined the effect of microfinance of enterprise clusters as a strategy for enterprise performance. However, some related works include the following: Okeke (2008) carried out a comparison of loans granted to MSEs by formal and informal institutions in Nigeria with Ondo State enterprise clusters as case study. Applying descriptive statistics, the study found that on the average, repayment rates were 92.93 percent and 34.06 percent for formal and informal sources respectively. In other words, there was better performance in terms of repayment rate from the formal sources when compared to the informal sources. As a result of the findings, the study recommended provision of basic infrastructural facilities that will reduce the cost of doing business in the country and reduce the ability of these enterprises to pay up when they get credits from informal sources. This was advised because of the fact that MSEs in these clusters opined that paying back the loans from the formal sources was not because of profitability but the fear of default; but they have a way of dealing with informal sources even when the time of payment lapses.

In yet another study, Suberu, Aremu, and Popoola (2011) evaluated the impact of microfinance on clusters of MSEs in Nigeria. Utilizing a simple random technique in MSEs clusters selection across the country, the study found that a significant number of MSEs benefited from credits of MFIs, though a fraction of them were qualified to secure the amount they got. It is interesting to note that MFIs grew in the last decade, but unfortunately, such growth in numbers was not matched with the number of credits given out to MSEs. Most of the MSEs recognized some positive inputs of credits from informal sources toward the promotion of not only market excellence but the overall competitive and comparative advantages. The study recommended further improvements in basic infrastructure to support MSEs growth and development in Nigeria.

Babjide (2011) investigated the impact of microfinancing on MSEs in South West Africa. The study used survey data of 443 MSEs and validated the reliability of the instruments with Cronbach’s alpha. The results suggested that microfinancing enhances the survival of MSEs but the enhancement was not enough for expansion and growth of MSEs operating in the region. The study further found the operational efficiency of many microfinance banks (MFBs) wanting as they grant less of group-based loans and more of individual-based credits.

Osotimehin, Jegede, Akinlabi, and Olajide (2012) carried out a study that examined the existence of prospects and challenges of MSEs operating in different clusters being developed in Lagos State in Nigeria. Applying the use of questionnaire and key informant interviews, the study gathered relevant data which were analyzed. The findings of the study include a remarkable growth of MSEs in Lagos, but this was attributed to the people’s quest to be self-employed and not any government intervention. Enterprises within the clusters studies suffer from lack of access to credit as well as good management which affect their overall performance and profitability. The study recommended capacity building for entrepreneurs in the surveyed clusters.

Akinbola, Ogunnaike, and Tijani (2013) examined the contribution of microfinancing to entrepreneurial development in Nigeria using multiple regression analysis and data sourced from 10 MFBs in the Ojo Local Government Area (LGA) of Lagos State in Nigeria. The result suggested that MFBs’ impact on entrepreneurial development in Nigeria is still negligible. Data evidence suggests the non-utilization of relevant marketing techniques by MFBs.

Olowe, Moradeyo, and Babalola (2013) in yet another study investigated the effect of microfinance on MSEs growth in Ibadan metropolis using a total of 82 MSEs operators in two different clusters. Applying multiple regression techniques as well as Pearson correlation coefficient, the study found no positive effect of financial services offered by MFBs due to short payback period; and hence this pushes most MSEs toward informal sources. Entrepreneurs complained of the high rate of interest and the insistence on the provision of collateral as possible factors that drove them toward the informal sources. The study recommended that MFBs should reduce the borrowing burden and increase the payback period from 1 year, which entrepreneurs cannot afford.

Findings from the above empirical literature are in line with the direction of the current study and its major objective, thereby providing enough empirical evidence with which to compare the findings of this current study.

Methodology

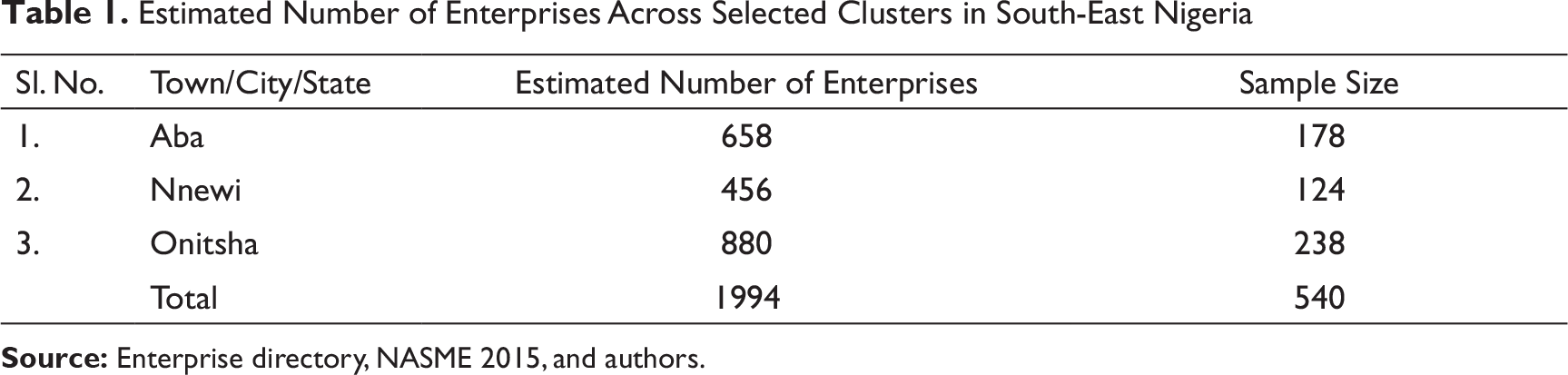

Estimated Number of Enterprises Across Selected Clusters in South-East Nigeria

A three-stage cluster sampling was adopted in this study because of the nature of South-East Nigeria and the number of clusters in existence. A sample of primary unit was selected from the different clusters existing in South-East Nigeria and that gave rise to the selected three cities. The second stage was the selection of sample of secondary units which were chosen from each selected primary unit. This stage resulted in the choice of the following: A.M.E Shoemakers Cluster for production; Omenma Traders Cluster for trade and Global Systems Mobile Network (GSM) and Allied Components Cluster; Aba Central for services, Nnewi Technology Incubation Centre for production, Nnewi Automobile spare parts Cluster for trade, and GSM and Allied Components Cluster in Nnewi; as well as Tinkers Dealers Cluster for production, Building Materials Cluster for trade; and GSM and Allied Components Cluster in Onitsha. Finally, a sample of tertiary unit was selected from each selected secondary unit (nine selected clusters) from the three cities with the help of a sample frame from the Nigerian Association of Small and Medium Enterprises (NASME).

It is noteworthy that, with a three-stage sampling, covering a large city may be impossible. Therefore, such a city can be further divided to administrative units. The number of enterprises located within the city can be determined by selecting a sample of administrative units before choosing a sample location within the selected administrative units. This can be followed by interviewing/administering a sample of firms/enterprises at the selected location. Details of the estimated number of enterprises across the nine clusters in the three cities are presented in Table 1 below.

Models Specification for Microfinance Source on Profitability and Method of Data Analyses

The argument, as presented in the theoretical framework, informs the current study’s focus on impact of informal funding sources on empowerment or outcome variable which is profitability. The study in line with this estimated the following basic regression:

where outcome is the measure of profitability

α is the regression constant;

In the above model, D denotes the cluster-specific dummy variables (locations of the cluster, e.g., Aba, Nnewi, and Onitsha).

However, there are other controls or enterprise-level characteristics that determine how enterprises perform which include: financial supports source of microfinance (sc) which is the focus of this study; age of enterprise (age); educational level of the enterprise head (edu); total number of employees (empl); enterprise sector of activity (a dummy for the three sectors under consideration: production, trade, services) (sec); capital stock per employee (capem); ownership structure (owns); cluster location (cluloc); and the background (apprentice activity of the entrepreneur) (soc).

The above factors have theoretical and empirical evidence on their relationships with enterprise performance (as shown under the a priori expectation). Enterprise performance is measured with the profit of the enterprises. Given that the profit shows to what extent the enterprise is actually growing, high output might not necessarily mean growth of the enterprise if the enterprise equally records high expenses in terms of production and indirect costs. In order to decipher (Equation [2]) into an expression appropriate for econometric analysis, the study adopted an explicit functional form model with second-order transcendental logarithmic (translog) giving rise to the following equations classified into a model thus:

where LnSC stands for log of source of microfinance (here we focus on informal sources);

LnAGE stands for log of age of enterprise;

LnEDU stands for log of educational level of the enterprise head;

LnEMPL stands for log of total number of employees;

LnSEC stands for log of sector with three sectors (production, trade, and services with production serving as the control group);

LnCAPEM stands for log of capital stock per employee;

LnOWNS stands for log of ownership structure;

Microfinancing Source and Profitability

LnSOC stands for log of social capital component (membership of different cluster groups that embark on cash contributions hence somewhat give financial assistance); hit is the usual disturbance which has a zero mean and variance; and

The results therefore could also be understood as the profitability determinants of enterprise clusters once all the enumerated factors have been accounted for, while variances in profitability was the outcome of unseen features such as market structure, skills, managerial ability, as well as technology of the enterprises.

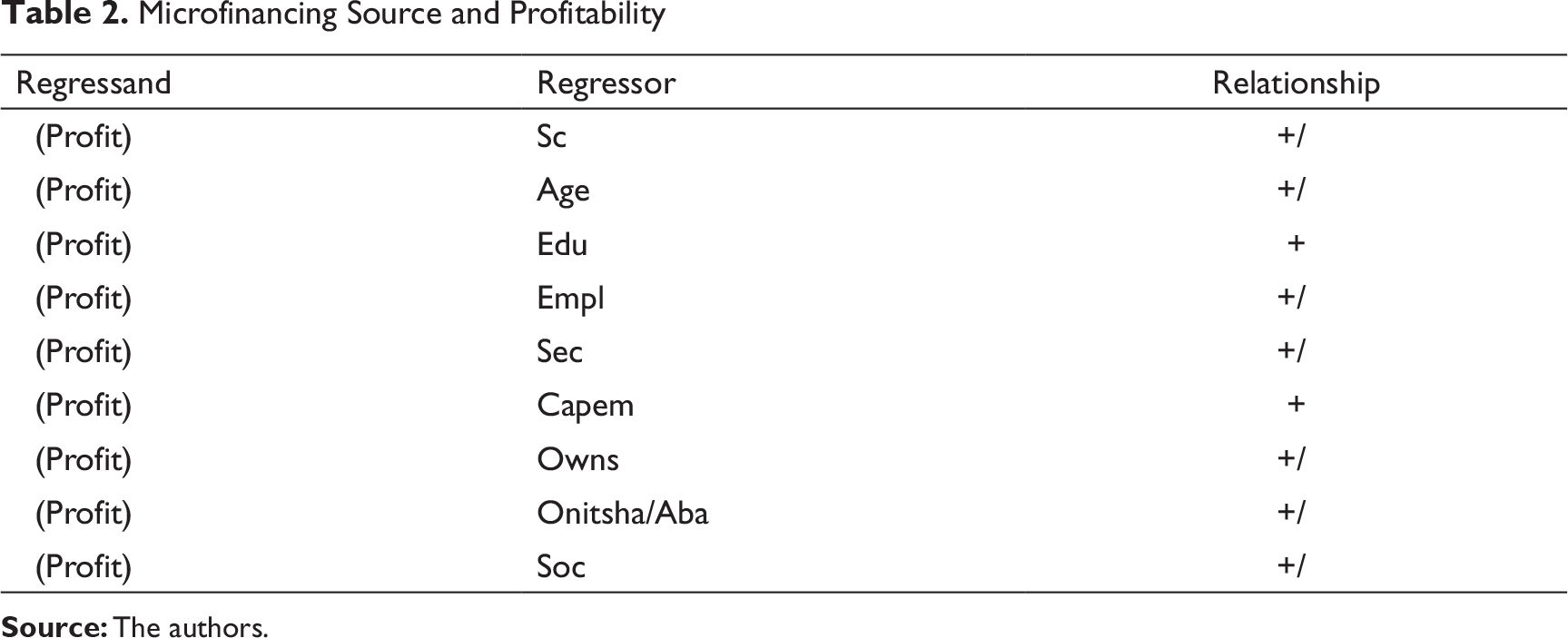

A Priori Expectations

A priori expectation will help to show whether the sign of economic or development theory, that is, if the sign and size of the parameters or development relationships follow the expectation of the theory. The a priori expectations in tandem with capital flight theory are presented in Table 2 below.

Note that: a “+” indicates that the regressand and the regressor increase (or decrease) together in the same direction. Thus, they possess a direct relationship. Contrarywise, a “−” implies an opposite relationship between the regressand and regressor. Thus, an increase (or decrease) in the regressor leads to a decrease (or increase) in the regressand.

Study Results, Findings, and Discussions

Effects of Informal Microfinance Sources on the Profitability of Enterprise Clusters in South-East Nigeria

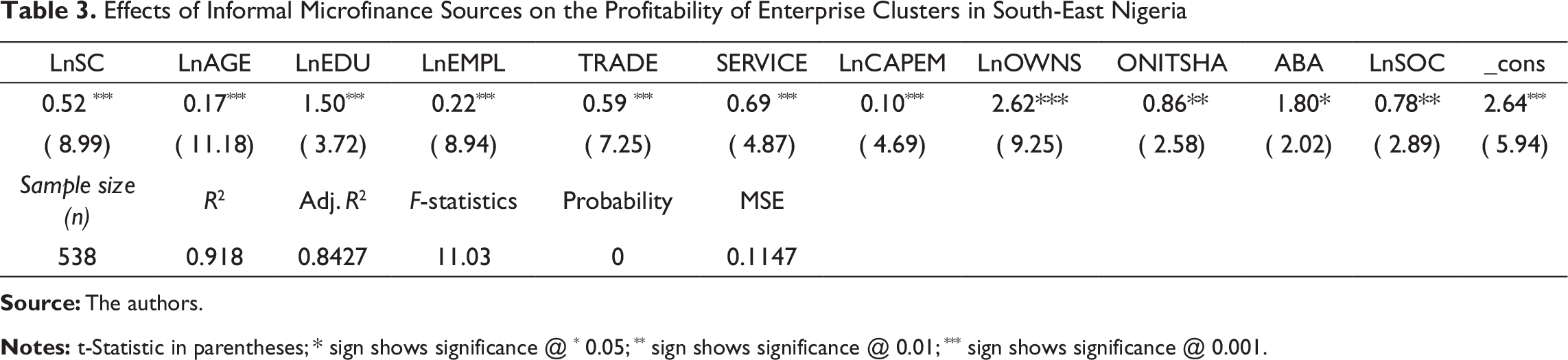

The Ordinary Least Square (OLS) estimation result above implies that the general model is statistically significant while the F-statistics (11.03) used to examine the significance of the model is greater than F-table value (4.08) and hence, the study concludes a significant relationship between the dependent variable (profitability) and the independent variables. Furthermore, the F-value probability of 0.000 which is less than 0.05 shows that the model is significant at the standard 5 percent significant level.

The R2 signifies the percentage of variations in the dependent variable accounted for by the variations in the independent variables. Thus, the higher the adjusted R2, the more the model is able to explain the changes in the dependent variable due to changes in the independent variables. In the regression result, the adjusted R2 is 0.8427 which infers 84.27 percent explanation of the disparity in the dependent variable by the independent variables. This indicates a perfect fit of regression line. The t-statistics which appeared in parenthesis were used to determine the level of significance for each variable coefficient(s) with variables significant at different critical levels such as 0.01 (***) or 1 percent, 0.05 (**) or 5 percent, and 0.10 (*) or 10 percent, and insignificant when there is no star sign.

A look at the individual coefficients revealed that the significant determinants of profitability include age of the enterprise manager, level of education, number of employees, ownership, ratio of capital to employees, as well as the indicator for social capital proxied by membership of different cluster groups. Here, age of the enterprise manager has a positive effect on profitability, which suggests that for informal microfinance sources, higher age is an added advantage. This is well understood from the culture of the South-Easterners in Nigeria because of the high regards they have for gray hair. This implies that the older one becomes, the less fraudulent such a person tends to be ceteris paribus.

Production is the control group for sector-specific effect and the results suggest that trade and services fared better than actual production in determining the enterprise profit. Similarly, Nnewi is the control for cluster city effect, with the results suggesting a significant though negative cluster effect for Onitsha and Aba, implying that the Nnewi cluster in overall fared better in determining the profitability of enterprises within the cluster than Onitsha and Aba when the source of microfinance is informal. This suggests that generally there may be better collaboration among enterprises in different groups in the clusters in Nnewi than in Onitsha and Aba. Interviews and Focused Group Discussions (FGDs) confirmed such where cluster participants in Nnewi revealed a culture of apprenticeship that allows younger entrepreneurs to enjoy credit facilities from their mentors without time limits. This was not that strong in Aba and Onitsha where there seems to be mutual suspicion between the mentors and their mentees. In general, results suggest that enterprises within clusters in Nnewi are likely to make more profits than enterprises within clusters in Onitsha, while enterprises within clusters in Ontisha are more likely to make more profit than their counterparts in Aba when they use an informal source of microfinance.

Labor equally shows significant positive effect on the profit of enterprises within the clusters that receive credit from informal sources. The capital to labor ratio is also a significant determinant of the profit of enterprises that receive credit from informal sources. The fact is that the relationship the enterprise has with the borrower (social capital) does significantly affect the profit of the enterprise when the source of microfinance is informal. The informal results corroborate with the cluster advantage of the entrepreneur. The advantage of each enterprise being in a cluster and becoming members of different capital associations does significantly improve profits of that enterprise.

It is noteworthy that the study objective is to ascertain the impact of informal financial credit on the profitability of enterprises that receive it. The variable used to proxy this is the sum total of credits received from financial institutions that year regressed on the rate of return or the profit for that year. The t-value for the informal credit sources is 8.99 and is greater than 1.96, while the p-values are 0.009 which is less than 0.05. Hence, we reject the null hypothesis, which implies that an informal source of microfinance significantly affects the profitability of the enterprises that receive them. Also, there are positive coefficients for informal credits and the return on investments of enterprises that receive them within the clusters. In fact, from the coefficient we can infer that, as credit increases by N1, the return on capital for enterprises that receive them increases significantly by N0.529 or 53k.

Looking at study objective that seeks to ascertain the effect of informal microfinance sources on the profitability of enterprises in South-East Nigeria, the study can comfortably conclude that there is a significant differential impact of the informal microfinance sources on the profitability of enterprise clusters in South-East Nigeria. The total annual average credit from informal sources equally, significantly, and positively affects the profitability of its recipients as expected a priori.

Though enterprises that receive credit from informal sources complain about the inability to raise huge funds, such firms have the advantage of being able to borrow as many times as possible with fewer protocols as requested by the formal credit providers. The sum total by the end of the year might, therefore, be enough to impact on the profitability of the enterprises as is the case in this study. Also, the other determinants that significantly affect the profits or the return on investment are capital, labor (number of employees), age, and cluster advantage (social capital), as well as level of education of the enterprise head, sector, and city of operation.

This finding is consistent with the result of the study by Loca and Kola (2013), which used qualitative and quantitative tools to show a positive relationship between entrepreneurial activities and lending practices in snowballing employee salaries, general employment level, and job creation, as well as the profit margin of enterprises in Albania. These are in line with the results of the current study showing that formal and informal credit are substantial determinants of profitability for enterprises in South-East Nigeria. Several other studies show similar findings. An example is Wanambisi and Bwisa (2013) who used descriptive statistics and logistic regression to demonstrate that the amount of loans is significantly and positively related with performance of MSEs in Kitale Municipality.

Policy Implications of Findings and Conclusions

The study found that informal microfinance sources significantly and positively affected the profitability of its recipients across enterprise clusters in South East of Nigeria. This is expected a priori as credit taken is usually intended to expand the business and, so, should ordinarily reflect on the profit of the enterprise. Another determinant crucial for policy is the high impact of social capital including cluster advantage. There is a need for policy direction to tap from such social capital including cluster advantage.

Another policy question from the finding is why has Nnewi performed better than Onitsha and Aba? Are there inherent qualities and strategies that need to be harnessed in order for Aba and Onistha to measure up with Nnewi? A clear answer to this would be to leverage on social capital in Onitsha and Aba the way Nnewi entrepreneurs have done since the same apprenticeship practice are com mon across all cities in South East, Nigeria. Harnessing such culture and values of trust would equally improve profitability for Onitsha and Aba entrepreneurs.

The study also found that the amount or volume of credit needed, relationship with the service provider, problematic extent of protocols, interest rate, length of repayment period, the cluster advantage, (social capital component) and the categories of the sectors are all determinants for choosing a particular source. It is equally important to note that any positive improvement on the part of policymakers on any of these variables sways an enterprise from informal sources to formal sources and vice versa. Also, the extent to which the length of the repayment period is offered is equally a positive and significant variable. Hence, it increases the odds in favor of choosing the informal source over the formal source, given that it is a challenge for both the formal and informal institutions. However, it apparently affects the formal institutions more than the informal institutions. The trade and service categories of the sectors of activity are positive and significant relative to the production sector. Hence, they equally increase the odds in favor of choosing from the informal sector.

Findings from the study suggest that informal credit sources support MSEs much more than the formal sources. This is equally confirmed by the FGDS that were held in these clusters as the informal sectors could give credit faster and frequently more than the formal sectors. This submission is, however, paradoxical to one of the principal challenges faced by enterprises that benefit from them as they stated that the inability to give out large loans is problematic. Nevertheless, this could be explained by the fact that, though the informal credit providers may not be able to provide huge sums, they are more likely to give out as many credits as possible. The credits may make a significant impact in the long term.

The study recommends that MFBs should relocate to enterprise clusters to be able to tap from cluster advantage and should be supported with necessary policies and enabling environment that will enable them do so by their regulatory authorities. This is consistent with the objectives of the rural banking scheme of the 1970s that is no longer in operation. The scheme provided that a minimum of 45 percent of total deposit liabilities of bank branches located in local areas be given to the location as credit facilities. Credits can therefore be given on the basis of social capital and group dynamics to the informal sectors that act as the backup for securities. Once the fear for physical and tangible security is not there, it would encourage enterprises to borrow and create more confidence in formal financial credit providers.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.