Abstract

The study attempts to examine the dubious role of majority shareholders in internal governance in the form of moderating agency problems in Indian manufacturing firms. It uses a set of strongly balanced panel data of 91 manufacturing firms of the BSE 200 index of India from 2011–2018 and adopts panel data regression analysis to establish the relationship among the variables. The study measures ownership concentration through the Herfindahl–Hirschman Index (HHI), vertical agency crisis through assets utilization efficiency (AUE) and general and administrative expenses (G&AE) and horizontal agency crisis through return on equity (ROE). The majority owners are found neither to enhance the operating efficiency nor to minimize excessive discretionary expenses of the management. Besides, a negative impact of ownership concentration on return on equity is evidenced, which indicates increased horizontal agency crisis as a consequence of increased ownership concentration. Given the dominance of majority shareholders in the Indian manufacturing sector, it would be worthwhile for corporate policymakers to know whether these large owners act as an internal disciplinary mechanism to the management or squeeze the minority shareholders’ interest through expropriation. Finally, the study suggests stricter external regulatory and institutional specificities as an alternative mechanism to ensure better corporate governance and protection of minority shareholders’ interest.

Keywords

Introduction

Ownership concentration is not a new phenomenon; rather, it is an endemic feature of most jointly held Indian corporations. Not only Indian but also most Asian firms are either family-controlled or state-controlled, which makes their ownership traditionally concentrated since their establishment (Shakir, 2008). In India, it can be traced back to the days of the British managing agencies (Balasubramanian, 2010). The scene is still prevalent; in fact, ownership concentration in the present day, especially in the hands of a few large promoters, has become a norm rather than an exception in the Indian corporate scene (Pandey & Sahu, 2019a). Additionally, the shift from democratic to plutocratic voting rights—from one vote per shareholder to one vote per share—has really changed the mechanism of corporate governance along with the status and prerogative of large shareholders in public limited companies in many countries (United States, France, Germany, Britain, etc.) including India. Moreover, apart from direct ownership some promoters also acquire more voting rights than their ownership rights through tunneling, cross-holding, and creating pyramiding effects (Chakrabarti, 2005). Notably, while ownership concentration is noticeable in almost all the sectors indiscriminately in other emerging Asian economies, for India the concentration of ownership is much more prominent in the manufacturing sector (Altaf, 2016; Selarka, 2005). Hence, studies on ownership concentration in particular reasonably prefer manufacturing firms as the study sample.

Now, these large/dominant shareholders can exert two types of influences on the corporate governance of Indian manufacturing firms. First, they may safeguard the interest of the shareholders’ fraternity as a whole by promoting the wealth maximization objective through better monitoring the management and limiting its opportunistic behavior. Conversely, these large owners can expropriate the minority shareholders and unjustifiably extract more benefits at their cost. The expropriation can take place in various ways such as diverting firm resources or assets through self-dealing transactions (Johnson et al., 2000), tunneling one firm’s resources and profits to another firm to enjoy more cash flow rights, especially in a situation where a dominant owner has controlling stakes in two different firms with varied cash flow rights (Bertrand et al., 2002), behaving subversively with minority owners and preventing them from exercising their de jure ownership rights (Goswami, 2002), etc.

The nature of agency crises in India is seen to be quite different from that of those in other economies like the United States and the United Kingdom. Where the corporations of these developed countries are facing both kinds of agency issues, that is, conflict of interest between managers and shareholders (type 1 or vertical agency crisis) and that between minority and dominant shareholders (type 2 or horizontal agency crisis), the latter issue is much more prevalent in the Indian corporate sector (Morck & Yeung, 2003; Roe, 2004).

However, the quality of corporate governance in Indian corporation is mainly assessed by its ability to discipline two types of self-servicing attitudes: that of majority owners and that of managers (Varma, 1997). It will be very interesting to test whether the concentrated ownership structure reduces vertical agency conflicts and costs in publicly held Indian manufacturing corporations or it becomes a cause of horizontal agency crises and lowers firm performance. A positive impact on performance with evidence of curtailment in vertical agency costs will definitely endorse their overall internal governance quality. However, the opposite results will indicate the presence of expropriation effects and their inability to serve as an internal governance mechanism.

This article is divided into different sections, with some having sub-sections. The second section includes hypothesis development supported by a brief review of theoretical conception and empirical evidences. The third section presents a detailed description of the data, construction of variables, and the statistical and econometric tests adopted to arrive at the results. The fourth section reports the empirical results and findings. The final two sections conclude the study with some suggestions, policy recommendations, and future research avenues.

Theory, Literature, and Hypotheses

Corporate governance theories claim that in a joint-stock company the ownership structure has many important implications for corporate governance and performance in emerging and emerged economies. The ownership structure is considered as one of the core internal governance mechanisms, and it remains a basis for exercising power and control over the functioning of a corporate entity, especially under an “incomplete agency contract” (Farooque, van Zijl, Dunstan, & Karim, 2007), accompanied by an instable or weak political, legal, and social framework (Roe, 2003; Shleifer & Vishny, 1997). Besides theoretical arguments, the empirical evidences of the impact of ownership structure on corporate governance, agency crises, and performance were prominently available in the context of developed economies like the United States and the United Kingdom (Franks & Mayer, 1997; Hill & Snell, 1989; Leech & Leahy, 1991).

Ownership Concentration and Vertical Agency Crisis: The Efficient Monitoring Hypothesis

The agency contract, that is, the contractual relationship between the principals and agents, is referred to as “incomplete” because of the fact that although typically the agents are supposed to think and act in line with the best interests of the principals, in practice, they take the benefits of freeriding opportunities to realize their private benefits at the expense of the principals (Kirchmaier & Grant, 2005; Shleifer & Vishny, 1997). In this way, the separation of these two entities results in a substantial conflict of interests (Jensen & Meckling, 1976; Shleifer & Vishny, 1997), which is dubbed in the corporate governance literature as type 1 or vertical agency crisis. Therefore, for publicly held companies, especially those with a dispersed ownership structure, the challenge for the shareholders is to safeguard their objective from managerial opportunism (Miguel, Pindado, & Torre, 2004). At this juncture, the controlling owners can play an effective role as proposed by the efficient monitoring hypothesis (Friend & Lang, 1988; Shleifer & Vishny, 1986). As per the proposition of this hypothesis, owners with a “substantial proportion” of shareholding can be more capable of monitoring and controlling the management of affairs of a company and preventing the opportunistic behavior of the management by virtue of their strong voting rights in the company, which ultimately results in decreased vertical agency crisis. Shleifer and Vishny (1997) opine that the institution of corporate governance can largely protect the interest of the shareholders and regulate this agency crisis, resulting in reduced agency costs. Being consistent with the efficient monitoring hypothesis, researchers like Shleifer and Vishny (1986) and Friend and Lang (1988) identify ownership concentration as a source of internal governance mechanism and observe how the market performance of the firms increases with an increase in the proportion of concentrated ownership. Researchers like Huddart (1993), Grossman and Hart (1986) and Denis and McConnell (2003) later on justify this with the fact that large shareholders have more incentives and prerogatives to rigorously monitor management, restrain managerial opportunism, and influence decision-making than the minority ones who own just a little proportion of the firm’s equity. In the last couple of years, the monitoring effect of large shareholders has also been tested and approved by a number of important studies. According to Javid and Iqbal (2008), ownership concentration in the context of Pakistani non-financial companies is an endogenous response of poor investors’ protection mechanism, which seems to have a favorable impact on firm profitability. In the recent past, Gaur, Bathula, and Singh (2015), in a study on the listed firms of the New Zealand Stock Exchange from 2004 to 2007, also approved the role of large owners and showed how the lack of ownership concentration leads to increased agency problems, resulting in the inferior performance of such firms. Al-Saidi and Al-Shammari (2015) endorse the monitoring role of concentrated shareholders for Kuwaiti firms in a more specific way, showing not all concentration by large shareholders but only the government and individual (families) ownership categories are better at monitoring and influencing performance. In another study, Najjar (2016) corroborates the positive impact of concentrated shareholding on the value of Jordanian firms. Most recently, Yasser and Mamun (2017) applying the Hirschman–Herfindahl Index (HHI) to represent ownership concentration approves the monitoring role of controlling owners and their positive contribution towards market-based performance and also the economic profit of firms in Pakistan. Other contemporary studies such as Abbasi, Asadipour, and Pourkiyani (2017) in the context of companies listed in the Tehran Stock Exchange and Mittal and Anjala (2018) in the context of companies listed on the National Stock Exchange of India also provide evidences on the role of large owners in minimizing agency crisis and increasing firm performance.

All these researchers, somehow or the other, approve the favorable impact of ownership concentration on operational efficiency, profitability, and even the market performance of a firm through easing out vertical agency crisis. Based on the above empirical evidences, the study assumes ownership concentration to curtail owners–managers agency crisis in Indian manufacturing firms and subsequently frames the following hypothesis:

Ownership Concentration and Horizontal Agency Crisis: The Expropriation Hypothesis

The existence of large owners under a concentrated shareholding pattern may call upon a new challenge for the minority owners. According to World Bank (1999), a closely held firm with few circumscribed controlling owners faces a situation of undue dominance over and expropriation of minority shareholders by such controlling shareholders. It brings in a challenge for the minority shareholders to prevent and control such extracting behavior of the large shareholders. Some empirical studies endorse a competing hypothesis called expropriation hypothesis and provide evidences of exploiting or expropriating behavior of large shareholders and their action against the value maximization objective of the firm as a whole, which leads to the generation of a horizontal or type II agency crisis (Burkart & Panunzi, 2006; Fama & Jensen, 1983; Shleifer & Vishny, 1997). In a typical form of expropriation, there is a possibility that they redistribute the wealth of the firm in both efficient and inefficient ways from other minority shareholders without taking the interest of such shareholders into consideration (Miguel et al., 2004). Therefore, in this sense, the controlling owners become costly for the minority owners and can unfavorably affect the performance of a corporation. Fama and Jensen (1983) also elucidate as to how concentrated shareholding could raise firms’ cost of capital due to decreased market liquidity and ultimately result in decreased firm value. Kuznetsov and Muravyev (2001), in the context of Russian non-financial private enterprises, show how the benefits of ownership concentration in the form of improved efficiency and productivity do not accrue to minority shareholders due to expropriation by large shareholders. Similarly, Earle, Kucsera, and Telegdy (2005), by using panel data for firms listed on the Budapest Stock Exchange, show that the marginal costs of concentration outweigh the benefits when the increased concentration involves “too many cooks.” Moreover, studies like Demsetz and Villalonga (2001) and Alipour (2013) suggest diffused ownership to be more advantageous for a firm. Demsetz and Villalonga (2001) illuminate that although diffused ownership may intensify owners–managers agency problems, it can yield compensating advantages that generally offset such problems. Goswami (2002), in the context of India, also evidences subversive behavior of large owners towards minority owner. The large owners are also found to be preventing the minority owners from exercising their de jure ownership rights. Similarly, Shakir (2008) studies 81 Malaysian property firms during the period 1999–2005, confirms the negative impact of block ownership on firms’ market performance, and suggests dispersed ownership structure. The study also infers that the market fears large shareholders as they may impose their wills in order to improve their own positions at the expense of other shareholders. Kumar and Singh (2012) and Hamid, Ting, and Kweh (2016) also evidence the expropriation of minority shareholders typically through tunneling and propping activities in the context of Indian and Malaysian firms respectively. In this regard, Kumar and Singh (2012) in the context of India recommend ensuring a conducive environment and tight regulations for the protection of minority shareholder rights. Hamid et al. (2016) suggest that an independent audit committee can help reduce this expropriation in a company. Most recently, Altaf and Shah (2018), in the context of Indian manufacturing firms, confirmed that after a certain threshold of ownership concentration the large shareholders expropriate the minority shareholders, which results in increased agency costs between majority and minority owners and leads to reduced firm performance. According to the study, after a high level of ownership concentration, the agency crisis shifts from an owners–managers conflict (vertical agency crisis) to a majority owners–minority owners conflict (horizontal agency crisis). The study also highlights the need for an alternative mechanism of good governance like investor protection in India. Thus, taking the above-discussed theoretical understanding and empirical literature into consideration, this study assumes ownership concentration to generate and propel horizontal agency crisis in Indian manufacturing firms and subsequently frames the following hypothesis:

The extensive corporate governance literature fosters inconclusive findings and equivocal evidences regarding the relationship between ownership concentration, agency problem, and performance of firms in different emerging and emerged markets’ perspectives. Another noteworthy point is that ownership concentration is mostly measured by the three or five largest block-holders. However, in India, the largest five block-holders may constitute a shareholder having a very insignificant stake in a firm, say less than 5 per cent. Thus, to be more practical, following Selarka (2005), this study sets a threshold of 5 per cent for considering an ownership as concentrated. Besides, by introducing the HHI, the study also captures the differential impact exerted by two large shareholders on different proportions of ownership in a firm (Curry & George, 1983).

Data, Methodology, and Model Specifications

Data

The study uses a set of strongly balanced panel data of 91 manufacturing firms listed in the BSE 200 index of Bombay Stock Exchange of India for the period from 2011 to 2018. The data are collected from financial databases, namely, Prowess and Capitaline Plus developed by Centre for Monitoring Indian Economy Pvt. Ltd and Capital Market Publishers Pvt. Ltd, respectively. Further, the study also uses annual reports of the sample firms for different financial years. The study sets a range of

Construction of Variables

Ownership concentration is considered as the independent variable of the study. The study introduces assets utilization efficiency (AUE), general and administrative expenses (G&AE), and return on equity (ROE) as the three dependent variables. Among these three, the study uses AUE and G&AE of the firms to represent the vertical agency problem whereas ROE is used to proxy the horizontal agency problem. Besides, to control the moderating effect of other possible determinants, the study introduces different firm-specific variables like age, liquidity, size, and leverage as the control variables. Following is a brief description on the construction of the variables and their relevance to the study.

Ownership Concentration: Herfindahl–Hirschman Index

The study, following Cubbin and Leech (1983), Demsetz and Lehn (1985), Bruton, Filatotchev, Chahine, and Wright (2010), and Brendea (2014), uses the HHI to measure ownership concentration. The HHI as a variable is constructed by summing up the squares of the fractions of equity held by each shareholder with at least 5 per cent ownership stake. The study considers a shareholder with at least 5 per cent of ownership as large. Now, simply summing up all the fractions of ownership by each shareholder with at least 5 per cent of the shares implies a shareholder with 5 per cent of shareholding and a shareholder with 50 per cent as equally powerful in terms of the influence they exert in the management of affairs of a firm. Application of the HHI permits us to capture this difference. For example, for five shareholders with 20 per cent of shareholdings each, the HHI will be 0.2, whereas for two shareholders with 50 per cent of shareholdings each, the HHI will be 0.5. A higher HHI index indicates higher ownership concentration and vice versa.

Assets Utilization Efficiency

Assets utilization efficiency has been used as a popular representative of agency problem in a number of studies like Li and Cui (2003), Matusin, Andryan, and Pamela (2014). It is measured by asset turnover ratio (ATR), which is the ratio of annual sales to average total assets of firms and represents how efficiently the management of a firm is utilizing its assets to generate sales (Ang, Cole, & Lin, 2000). It reflects the existence of agency problem between owners and managers and the monitoring efficiency of large owners towards easing out such problems.

General and Administrative Expenses

It is the percentage of general and administrative expenses (including selling and distribution expenses) on total sales revenue of firms. General and administrative expenses are non-productive in nature. These expenses also tend to capture managers’ discretion in spending the firm’s resources on excessive perquisites. Managers are supposed to use these expenses to conceal their expenditure on perquisites (Singh & Davidson, 2003), and therefore higher spending on these expenses reflects higher agency conflict and weaker monitoring of managerial opportunism by large owners. Following Singh and Davidson (2003) and Nazir and Saita (2013), the study uses this ratio to measure vertical agency costs.

Return on Equity

Following Krishnan and Moyer (1997), Perrini, Rossi, and Rovetta (2008), Bokhari and Khan (2013) and Goyal (2013), the study uses ROE to represent horizontal agency crisis. It signifies how efficient a firm is in generating returns on the investment it received from its equity shareholders. It is a ratio between the net income and shareholders’ equity of a firm. An increase in ROE signifies decrease in horizontal agency crisis and vice versa.

Age

The age of firms, both theoretically and empirically, is known to have a very strong connection with their functioning, efficiency, and level of profitability. The age of firms is correlated with operational efficiency and performance of firms in a number of empirical studies like Hannan and Freeman (1984), Katz (1982), Loderer and Waelchli (2010), Pandey and Sahu (2017), etc.

Liquidity

The theory of corporate finance advocates important implications of firms’ liquidity on operating efficiency and profitability. The relationship is also sufficiently endorsed by a number of empirical investigations like Saleem and Rehman (2011), Niresh (2012), Lartey et al. (2013), etc. This study uses current ratio as a measure of liquidity.

Size

The size of firms is an important moderating variable, which is supposed to confound the relationship between firm performance and any other variables. The firm size is used as a control variable in many important corporate governance studies like Farooque et al. (2007), Zeitun (2009), Santos, Moreira, and Vieira (2014), and Maqbool and Zameer (2018).

Leverage

Firm financial leverage is also proved to be an important determinant of a firm’s profitability and agency costs (Grossman & Hart, 1982; Jensen, 1986; Pandey & Sahu, 2019b; Stulz, 1990). Almost all studies that linked corporate governance parameters with corporate performance have considered firms’ financial leverage (mostly in the form of debt:equity ratio) as control variable.

Methodology and Model Specifications

The study first introduces the panel data model to establish the relationship between ownership concentration and agency crisis in Indian manufacturing firms. The panel data analysis mainly includes the selection of the best fit regression model among ordinary least square model (OLS), fixed effect model (FEM), and random effect model (REM). In panel data analysis, the model largely influences conclusions on the individual coefficients. In a panel dataset with the number of cross-section units larger than that of time-series units, as in the present case, the estimates obtained by the FEM and REM differ significantly. In fact, all these three regression models have different underlying assumptions.

The OLS model assumes the intercept as well as the slope coefficients to be same for all the manufacturing firms taken in the sample. The FEM allows the intercepts to vary across the firms to incorporate special characteristics of the cross-sectional units. Finally, the REM assumes the intercept of a particular firm to be a random drawing from a large population, which varies non-systematically with a constant mean value (Mishra & Kumar, 2011). As not all these three conditions can prevail simultaneously, the study needs to select an appropriate model for regression. For this purpose, the study introduces restricted F-test, Breusch and Pagan’s Lagrange multiplier test, and Hausman test. Besides, the study introduces diagnostic tests such as tests of multicollinearity and heteroskedasticity to ensure robustness of results. The study uses variance inflation factor (VIF) as a test of multicollinearity. The Breusch–Pagan/Cook–Weisberg test and information matrix test are applied to check the existence of heteroskedasticity problem in the models.

The study frames the following regression models to represent the relationship among the variables:

where AUEit, G&AEit, and ROEit denote the asset utilization efficiency, general and administrative expenses, and return on equity of ith firm at time period t. α depicts the constant term. γ1 to γ5 denote the coefficients of the independent and firm-specific control variables. εit represents the error term.

Data Analysis and Results

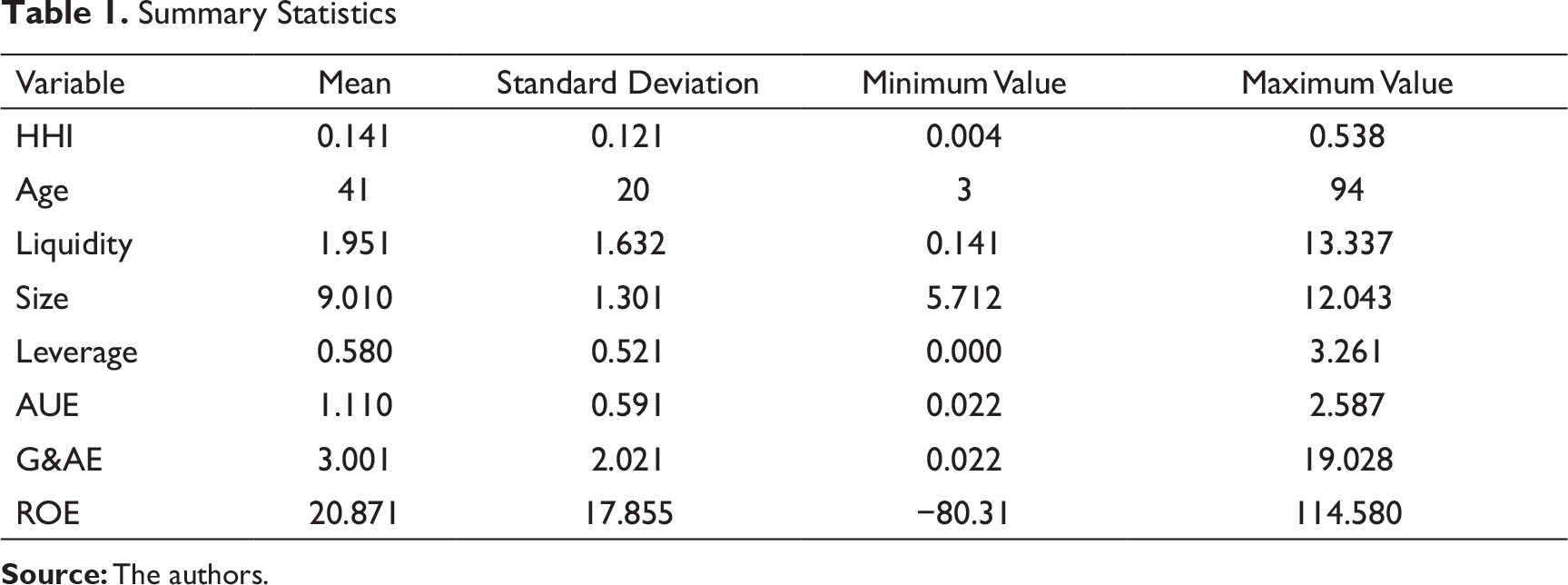

Descriptive Statistics

Summary Statistics

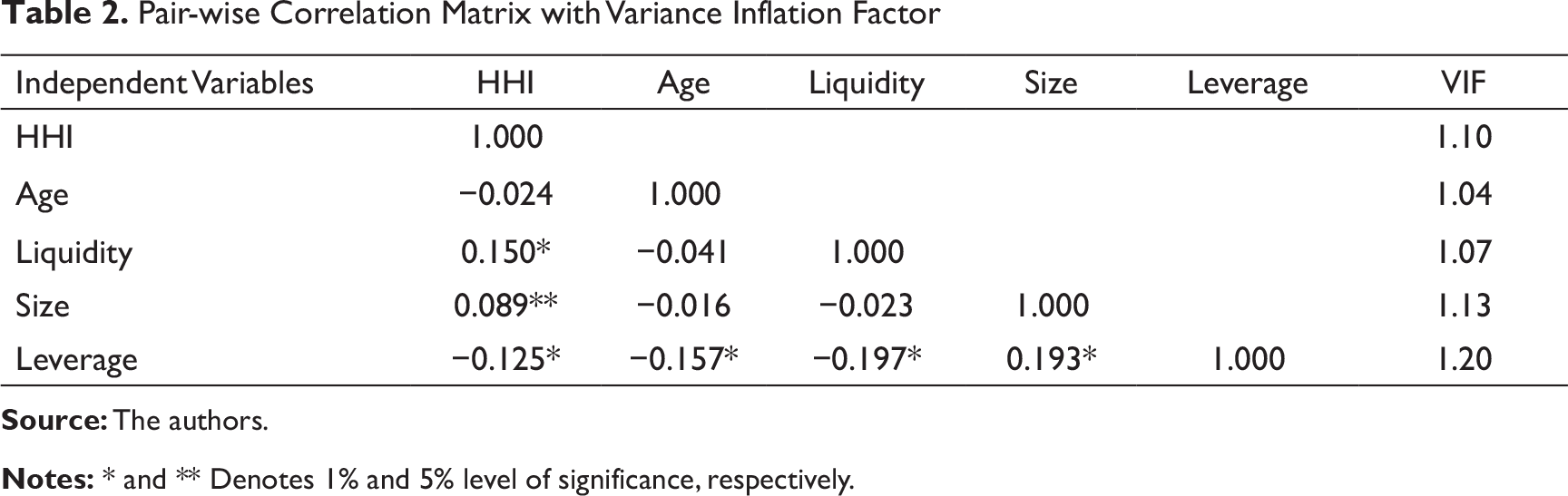

Pair-wise Correlation Matrix with Variance Inflation Factor

Diagnostic Tests

The presence of the multicollinearity property among the variables can produce erroneous results and lead to spurious inferences. The study introduces pair-wise correlation matrix and VIF (Table 2) to check the presence of multicollinearity. The pair-wise correlations and maximum value of VIF both suggests that the explanatory variables used in this study are free form multicollinearity. The correlations are found to be very low and even insignificant for some pairs of variables, and the maximum VIF value is 1.20. Although there is no formally prescribed criterion for determining the bottom line of the tolerance value of VIF, according to Gujarati (2004), explanatory variables can be regarded as highly collinear if the VIF value exceeds 10.

Besides, the classical regression model assumes that the modeling errors or error terms are uncorrelated and uniform and the variance of such error terms is constant, which fits under a condition of homoskedasticity. Now, when the error terms do not have constant variance they are said to be heteroskedastic, and the existence of this problem is a major concern in the application of regression analysis as it can invalidate statistical tests of significance. Therefore, regarding the heteroskedasticity, the study introduces two tests, namely, the Breusch–Pagan/Cook–Weisberg test (Hettest) for heteroskedasticity and the Information Matrix test (Imtest) for heteroskedasticity (White, 1980). The results of the Hettest, as depicted in Table 3, confirms that our first and third regression models are suffering from heteroskedasticity. Again, the Imtest also confirms the existence of heteroskedasticity in all three models. Hence, to control the adverse effects of the heteroskedasticity problem, the study applies robust standard errors (White, 1980) while computing the individual coefficients through the regression models to make the results best linear unbiased estimator.

Panel Data Analysis

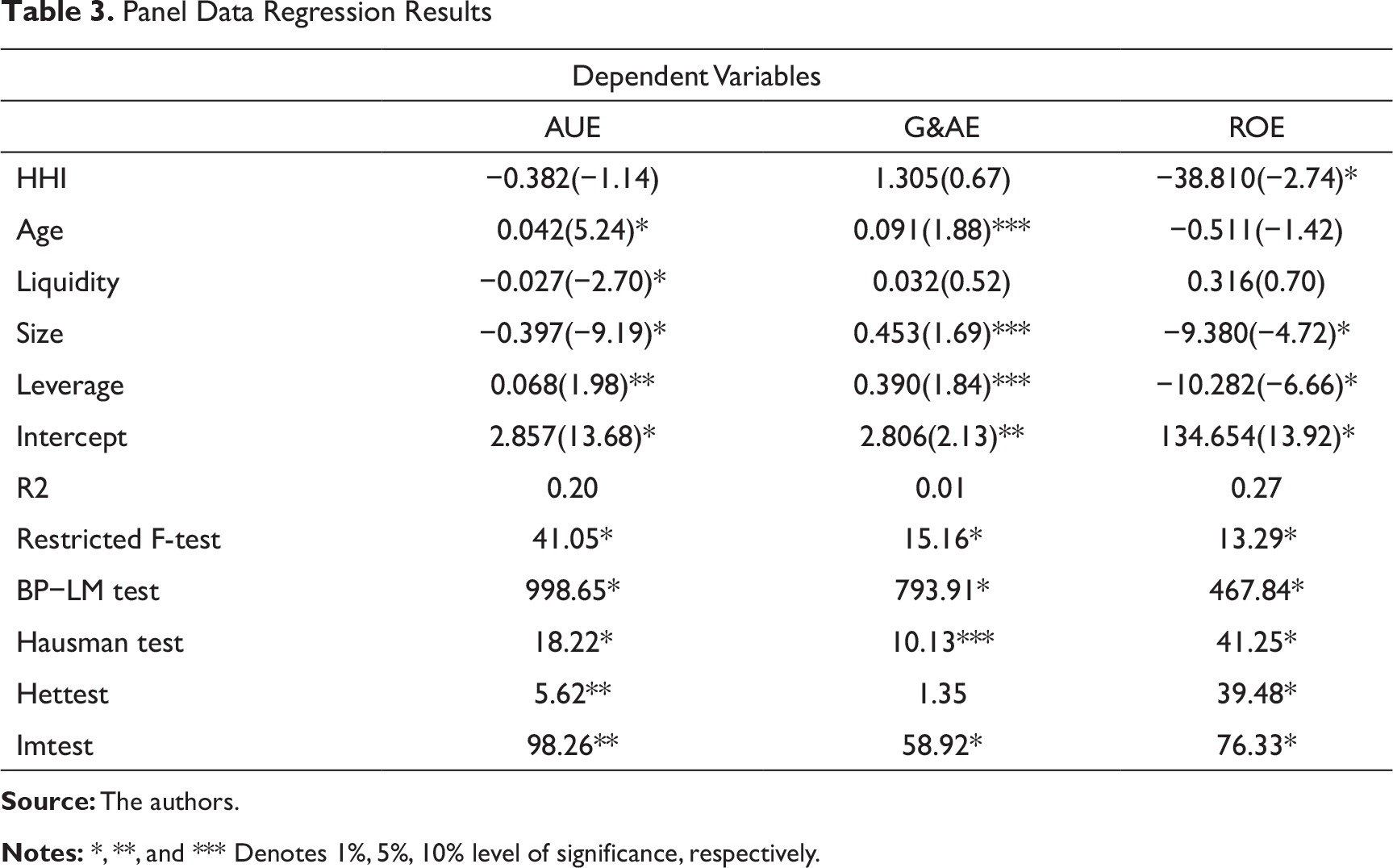

Panel Data Regression Results

Figures in brackets are t-values.

Restricted F-test is the test for selection between OLS and FEM.

where LM test is the Breusch and Pagan’s (1980) Lagrange multiplier test which provides selection between OLS and REM. Hausman test is the Hausman (1978) specification test for selection between FEM and REM. Hettest is the Breusch–Pagan/Cook–Weisberg test for heteroskedasticity. Imtest is the information matrix test for heteroskedasticity (White, 1980).

Similarly, for the second model, which tests the relationship between G&AE and the HHI, the test statistics of restricted F-test (15.16*), BP–LM test (793.91*), and Hausman test (10.13***) are again found to be significant, and therefore we find FEM as the best fit regression model to establish the relationship between the concerned variables. Lastly, for the third regression model, which examines the relationship between ROE and the HHI, we again find all three tests statistics to be significant at 1 per cent level of significance, and once again we find FEM as the best fit model.

From the results of the panel data regression analysis, the study can infer that ownership concentration measured by the HHI does not affect the assets utilization efficiency of the sample firms. The regression coefficient of the HHI in our first regression model is found to be statistically insignificant (-0.382). This signifies that the large block-holders in Indian manufacturing corporations are not pursuing the role of an efficient monitor of the management and thereby do not discipline the managers to act for the efficient utilization of firms’ resources. The study also does not evidence any significant effect of ownership concentration on the general and administration expenses of the sample firms as it finds a statistically insignificant regression coefficient for HHI (1.305). Therefore, the large owners in the Indian manufacturing firms are found neither to enhance the operating efficiency nor to minimize the excessive discretionary expenses of the management. The study introduces these two variables to represent vertical agency crisis, that is, the conflict of interest between managers and shareholders. From the findings of the study, it is clear that ownership concentration does not affect the vertical agency problem in Indian manufacturing corporations. Therefore, these findings are found to be inconsistent with our first hypothesis, which assumes ownership concentration to minimize owners–managers conflicts of interest in Indian manufacturing firms.

The third regression model confirms that there is a statistically significant and negative relationship between the HHI and ROE. The coefficient for the HHI in the regression model is found to be -38.810 with 1 per cent level of significance. Therefore, the study gets clear evidence of the adverse impact of large owners on the profitability of Indian manufacturing firms. The result points towards the expropriation of minority shareholders by the large ones and the consequent rise in horizontal agency crises, that is, the conflicts of interest between large and minority owners with increased ownership concentration. Therefore, our findings in this regard remain consistent with the second hypothesis, which assumes ownership concentration to bring about majority–minority owners’ conflicts of interest and result in decreased firm performance. The findings of the present study are in line with the previous Indian evidences like Kumar and Singh (2012), Hamid et al. (2016), Altaf and Shah (2018), etc. and confirm the presence of the expropriation effect in Indian manufacturing firms resulting in increased horizontal agency crises. However, we cannot completely deny the role of such large owners on disciplining the management. Perhaps, it would be much more logical to infer that the role of such large shareholders is not strong enough to ensure safeguarding shareholders from managerial opportunistic behavior. In a nutshell, the expropriation effect seems to overweigh the monitoring effect, resulting in decreased profitability.

Conclusions and Policy Recommendations

Most Asian firms are either inherently family-controlled or state-controlled, which makes their ownership traditionally concentrated since their establishment (Shakir, 2008). Moreover, unlike other emerging Asian economies, concentration of ownership is much more prominent in manufacturing sectors in the case of India (Altaf, 2016; Selarka, 2005). Indian corporate laws vest tremendous power in such controlling family owners/promoters and thereby make them sufficiently capable of exercising their unjust “whims and fancies” in the board, which many times becomes a cause of oppression of the minority ones. Now, amid great controversy over the impact of such concentrated ownership structures on the quality of corporate governance in Asian firms, it is very interesting to test the actual role that majority owners pursue in a jointly held manufacturing corporation in India. We have tested this on a sample of 91 Indian manufacturing firms for the period from 2011 to 2018. Using panel data regression analysis, we do not find any evidence of a significant association between ownership concentration and owners–managers conflicts of interest, that is, vertical agency problem, in the sample firms. Nonetheless, the study finds evidence of significant negative impacts of ownership concentration on the profitability of the Indian manufacturing firms, which indicates towards increasing horizontal agency problem within the firms.

Inquiring into the root causes behind such expropriation in Indian firms, we reach at some specific reasons as to why it is quite easy to abuse minority shareholders in India. First, the status of minority shareholders is largely different in India in comparison to the developed economies like the United States and the United Kingdom. For instance, in the United States, all major corporate decisions are initiated by the board itself, and the majority shareholders hardly influence any such corporate decisions of the board. The shareholders may change the course of the corporation only by replacing the board. Conversely, in India, while taking corporate decisions, a board follows the fundamental principle that the “opinion of majority shall always prevail.” Second, both the versions of the Indian Companies Act, that is, that of 1956 and 2013, have prescribed more or less similar criteria for minority shareholders to apply to the National Company Law Tribunal (NCLT), or previously, the Company Law Board (CLB), in case they feel oppressed. As per the provisions of the Companies Act, a member/shareholder having less that 10 per cent of ownership in company-issued share capital cannot alone seek redressal from the tribunal in case he/she feels oppressed. In such a case, a minimum of 100 members or one-tenth of the total members, whichever is lower, is required to apply to the tribunal. More often than not, it becomes a cumbersome work for minority shareholders in India, especially those with less financial awareness and knowledge of legislation, to comply with the above stipulated criteria. Third, the tribunal also shows reluctance to quickly interfere in internal corporate affairs, with the caution that there may be unscrupulous shareholders who may take undue advantage of the provisions through acting on the pretext of investors’ rights. Apart from these, there are a number of instances when courts in India act under the principle of non-interference and refuse to interfere in the management of a company. Finally, high costs, tedious and vexing legal procedures, less hope and instances of success, and the lack of education and legal awareness have also discouraged lay investors of India from initiating action against giant shareholders who are economically and politically powerful. Hence, the provisions on minority interest protection in India seem quite inaccessible and unrealistic for the lay investors, and it becomes quite easy for the majority shareholders to reap the benefits of the legal flows or regulatory loopholes.

Finally, the study, based on its findings, doubts the role of majority shareholders as an internal governance mechanism in the Indian manufacturing firms and accordingly suggests stricter external regulatory and institutional specificities as an alternative mechanism that could ensure better corporate governance and protection of minority shareholders’ interests, as previously suggested by Kumar and Singh (2012), Hamid et al. (2016), and Altaf and Shah (2018). Besides, the study also recommends possible amendments in the corporate laws towards improving the legal status and redressal-seeking power of the small investors in India. To conclude, we must admit that the findings and thereby drawn inferences of this study are valid for Indian manufacturing firms. Hence, further studies on other sectors, markets, or for different periods may reveal varied results. Moreover, the study strongly recommends sector-specific inquiries and even cross-country investigations as future research avenues.

Limitations of the Study and Future Research Directions

The scope of this empirical investigation is limited to the Indian capital market and the concurrent regulatory environment. The status of large shareholders or promoters and their role in the internal governance of firms differs from market to market, and therefore, the present evidence on the ownership–performance relationship cannot be generalized for all countries. Therefore, we must sensibly admit that the findings and thereby drawn inferences of this study are valid for Indian manufacturing firms and for the considered period only. Hence, further studies on different sectors, markets, or for different periods may produce varied results. Moreover, regarding further research directions, the researchers strongly recommend sector-specific inquiries and even cross-country investigations on this topic. Further, future researches may also consider and address the issues of endogeneity and non-linearity in the relationship between the variables to capture the dynamism of the relationship.

Footnotes

Declaration of Conflicting Interests

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.