Abstract

Debt holders monitoring influence on the business performance has been noted in several research. Another body of research investigates the board of directors and performance linkages. The impact of debtholders on the board composition and firm performance linkage, particularly in State-Owned Enterprises (SOEs), has received little attention in the literature. As a result, this article aims to determine whether the composition of Indian SOE boards has an impact on their performance. It also looks into how leverage influences the association between the composition of Indian SOE boards and their performance. From 2001 to 2019, the panel data regression is performed on 19 Indian SOEs registered on the Bombay Stock Exchange. According to the study, board size, nominee directors improve Indian SOE performance, while independent directors reduce performance. Furthermore, in high-leverage SOEs, board of directors’ supervision is reduced or removed. The findings have implications for policymakers and the government.

Introduction

The extant literature cognized the debtholders’ role in curbing the agency problems between shareholders and management by performing a disciplinary function (Jensen, 1986; Tian & Estrin, 2007). Agency problems arise when managers prioritize their goals over the goals of managers. Debtholders, being conservative, can help reduce these problems by constraining the firm’s risk-taking activities (Levine, 2004; Mintz, 2005) and restricting managers’ self-interest (Grossman & Hart, 1982). According to Jensen (1986), fixed payments connected with debt reduce the company’s free cash flow and inhibit managers’ capacity to misuse corporate resources for personal gain.

Another body of literature explores the linkages between the board of directors and company’s performance (Ameer et al., 2010; Garg, 2007; Guest, 2009; McIntyre et al., 2007). While some authors posit that the board is responsible for overseeing the management of their organization, others have argued that the board may be unfit to perform its monitoring role due to the consolidation of power by the management (Rose, 2005). Furthermore, Chou et al. (2010) argued that if a company has a significant level of financial leverage, the directors’ monitoring can be weakened or even eliminated because debtholders precede shareholders in residual claims and benefit excessively more from the work of the board of directors. The directors of a high-leverage corporation may spend less time overseeing and managing the company due to the reduced incremental value of governance enhancement (Chou et al., 2010). Contrary to this, financial leverage increases the impact of the directors’ actions on the company’s stock value while reducing the risk of financial distress or bankruptcy (Chou et al., 2010). Given the same equity endowment and no threat of bankruptcy, leverage should encourage directors to put in extra hours because the company operates on a larger scale and borrows more aggressively (Chou et al., 2010). Thus, the prior studies present conflicting theoretical arguments regarding the board’s monitoring role and its impact on the performance of companies, especially in high-leverage companies.

Besides the conflicting theoretical arguments, substantial literature has empirically analysed the interface between board composition and the performance of companies (Abang’a et al., 2021; Manna et al., 2016; Puni & Anlesinya, 2020; Vu & Pratoomsuwan, 2019). Additionally, the prior literature has also discussed the monitoring role of debtholders. There is a paucity of studies examining the impact of debtholder monitoring on the linkages between board composition and company performance, particularly in state-owned enterprises (SOEs). The current research aims to close this gap in the Indian context.

Thus, the study has two objectives. First, do the board of directors adequately monitors the managers? In other words, how board composition affects the performance of Indian SOEs? Second, how the presence of debtholders monitoring affects the linkages between Indian SOEs board composition and performance. This study undertakes to achieve this objective by focussing on 19 Indian SOEs for 18 years, that is, 2001–2019. Board composition comprises executive directors, non-executive directors (independent and nominee directors) and board size. The performance parameter of SOEs is return on assets (ROA).

Several reasons motivate studying the SOEs in India. In terms of research, the linkages between board composition and SOE performance have attracted minimal attention (Heo, 2018; Shawtari et al., 2017; Vu & Pratoomsuwan, 2019; Wang et al., 2016). As per several studies, SOEs suffer from a lack of competition and multiple objectives. Additionally, the SOEs suffer political interference from ministries and bureaucrats, who focus on their short-term political goals (Menozzi et al., 2012), which results in lower profitability and slack (Shleifer & Vishny, 1994). This decrease in profits has been mostly plugged in by the government’s subsidies and heavy borrowings that the government guarantees (Srivastava & Kathuria, 2020; Song et al., 2011). Thus, the poor performance of SOEs ultimately converts into a fiscal burden for a nation.

Another motivation lies in the significant role of SOEs in shaping the Indian economy. SOEs generate approximately one-tenth of the world’s gross domestic products. Nevertheless, the recent economic downturn exhibits a fall in the financial performance of Indian SOEs in the future. According to the Public Enterprises Survey, 2019, out of 249 operating SOEs, only 178 enterprises were profitable amounting to ₹174,587 crores during 2018–2019 (Department of Public Enterprises (DPE), 2019). In addition, the market capitalization of 42 listed SOEs has dwindled from 10.69% to 9.08% as of March 31, 2019. Surprisingly, Indian SOEs’ innate ability to raise resources has grown slowly from ₹1.72 trillion to ₹1.98 trillion in the last five years. The total debt of operating SOEs has increased from ₹1,460,351.46 in 2018–2019 to ₹1,684,894.41 in 2017–2018, that is, 15%. Though Indian SOEs have received lots of budgetary support from the government, government funding would squeeze in the coming year. In light of this, it becomes imperative to study the Indian SOEs and draw attention to the measures that enhance their performance.

The third reason motivating this study is concerned with the role of the board of directors in enhancing the SOEs’ performance (Mbo & Adjasi, 2017; OECD, 2005; Robinett, 2006). The SOEs’ board performs the monitoring and control role, keeping in mind the public’s interest and also ensures transparency and protection to stakeholders (Peng et al., 2016). Nevertheless, political interference hampers the decision-making power of the board (OECD, 2005). Besides this, the non-existence of potential takeovers and the impossibility of bankruptcy of SOEs reduce the incentives of board members to monitor managers and maximize company value (Menozzi et al., 2012). So, the other two crucial governance mechanisms that help control underperformance are absent. It posits a need to investigate whether any additional monitoring mechanism such as debtholders affects board composition and SOEs performance link.

The forthcoming section presents the literature review and hypothesis development, followed by the study’s research methodology and empirical findings and the conclusion thereof.

Literature Review and Hypothesis Development

In an organization, agency concerns arise from misaligning interests between managers and shareholders (Ibrahim & Abdul-Samad, 2011). The agency problems arising among the various parties are more profound in SOEs (Allini et al., 2016). On the one hand, the lack of incentives from the bureaucrats demotivates the board to motivate the managers to work for higher-level performance (Shawtari et al., 2017). On the other hand, these bureaucrats do not have the adequate business skills and resources to monitor and control the agents of every SOE (Peng et al., 2016). Consequently, information asymmetries aggravate, deviating these SOEs from their goals (Peng et al., 2016). Sometimes, there can also arise principle–principal conflict between majority shareholders (government) and minority shareholders (citizens). The managers in these SOEs are mostly politically linked, and they, along with the government, may serve their political interests, thereby overlooking the interests of minority shareholders (Shawtari et al., 2017). It creates agency problems and diminishes the SOEs’ performance. On the basis of agency theory, robust governance mechanisms balance the interest of shareholders and managers, which consequently ameliorate the company’s performance. The board composition is one of such mechanisms that enhances the companies’ performance by monitoring and controlling the managers (Fama, 1980).

The stewardship theory, on the contrary, claims that managers are custodians of the organization and seek to ensure its success (Abang’a & Wang’ombe, 2020; Donaldson & Davis, 1991). Therefore, SOEs’ managers will always act to enhance the quality of corporate governance (CG) toward the achievements of the stakeholders’ interests (parliamentarians, citizens, and regulatory bodies; Abang’a & Wang’ombe, 2020). They will cease from conflict of interest in the performance of their duties. This approach will significantly enhance fairness, accountability, transparency, and responsibility (Abang’a & Wang’ombe, 2020). Accordingly, stewardship theory does not advocate for a large board size and independent directors. This study builds on the agency theory and stewardship theory to establish the linkages between the composition of the board and the performance of SOEs.

Board Size and Firm Performance

Board size is a crucial determinant of board composition. On the basis of agency theory, an increase in board size affirmatively influences the organization’s performance due to the monitoring and control role. According to this theory, large board size indicates more access to expert ideas and resources from outside the organization (Dalton et al., 1999). In contrast, Hermalin and Weisbach (2003) asserted that a larger board would exacerbate communication and coordination issues, delaying information transfer and slowing decision-making (Aslam & Haron, 2020; Goodstein et al., 1994). There is less expression of notions and thoughts, which will enhance decision-making time (Ahmed et al., 2006; Dalton et al., 1998). The stewardship theory backs up this claim by arguing that managers behave as stewards for the company, and therefore corporations do not need huge board (Donaldson & Davis, 1991).

Previous studies examining the board size–SOE performance link have yielded mixed findings. For example, between 1994 and 2004, Menozzi et al. (2012) found no influence of board size on the performance of 114 Italian public utility SOEs. Owing to a lack of unanimity among a large number of board of directors, Bhat et al. (2018) observed no influence of board size on the performance of nine Pakistani SOEs gauged using Tobin’s Q over the period 2010–2014. Similarly, Abang’a et al. (2021) also analysed 45 SOEs in Kenya for four years, that is, 2015–2018 and found no impact of board size on their performance. In Vietnam, Vu and Pratoomsuwan (2019) found no effect of board size on the SOEs’ performance from 2008 to 2014. Kiranmai and Mishra (2019) observed that board size did not influence the performance of 42 listed Indian SOEs throughout 2012–2017.

Heo (2018), on the contrary, discovered that board size favorably impacts the performance, as measured by ROA, among 320 Korean SOEs. Shawtari et al. (2017) assessed the connections between the characteristics of the board and SOE performance by using a quantile regression technique. In the post-transformation policy period, from 2007 to 2011, they discovered that board size positively influences low-performing SOEs.

As the information asymmetries are severe in SOEs, they require larger boards that supervise and control the managers better. In high-leverage SOEs, debt holders would have more significant incentives to discipline the managers (Tian & Estrin, 2007). Therefore, directors would spend less time monitoring the managers, due to which increasing the board size would not bring any impact on SOEs’ performance. Thus, the hypotheses are developed as follows:

H1a: The board size has a positive impact on the performance of SOEs.

H1b: The board size has a positive impact on the performance of SOEs with low leverage as compared with SOEs with high leverage.

Executive Directors and Firm Performance

Executive directors are another critical component of board composition. They are full-time directors who govern the day-to-day activities of the corporation. Executive directors’ actions are likely to be influenced by the managers in the agency framework, who may put their interests ahead of the interests of shareholders. It depicts that the executive director negatively impacts the company’s performance. Furthermore, insiders create financial and psychological incentives for other board members to be unduly forgiving of executives (Jensen, 1983). As a result, executive directors may be expensive to shareholders. Companies with a more considerable number of executive directors have higher abnormal accruals and pay chief executive officers (CEOs) more for performance out of their control (Muslu, 2010).

In contrast, the stewardship argument asserts that executive directors affirmatively influence business performance as they are more beneficial to the company (Davis et al., 1997; Rashid, 2018; Song et al., 2017). According to Hermalin and Weisbach (1991), the inside directors assisted the CEOs in maximizing the company’s value by providing advice on daily operations. They had access to sensitive company information and a greater understanding of its requirements. It resulted in the corporation making better judgments, which eventually boosted its performance (Fama & Jensen, 1983). Owing to their considerable shareholdings in the company, they had complete control over them. They support the company by providing sufficient financial resources (Srivastava, 2015).

Previous research into the association between executive directors and company performance has mostly found a favorable link (Srivastava, 2015; Yammeesri & Herath, 2010). Puni and Anlesinya (2020) conducted a study that validated these findings. On the other hand, Manna et al. (2016) discovered no such influence of executive directors on the Indian firms’ performance.

Considering the complex nature of SOEs and those mentioned above, conflicting theoretical justifications and empirical evidence, this study expects that executive directors positively affect performance. Furthermore, owing to monitoring by debtholders in high-leverage SOEs, executive directors would not spend much time monitoring the managers, so they may not impact the performance of SOEs.

Thus, the hypotheses are developed as follows:

H2a: The executive directors have a positive impact on the performance of SOEs.

H2b: The executive directors have a positive impact on the performance of SOEs with low leverage compared to SOEs with high leverage.

Independent Directors and Firm Performance

Independent directors are another vital component of board composition. Independent directors have extensive experience and understanding from serving on multiple boards (Yeh et al., 2011). They are extensively involved in ensuring that organizations behave appropriately and that the set objectives are met (Puni & Anlesinya, 2020; Srivastava, 2015). According to authors like Conyon and Peck (1998) and Bouteska (2020), independent directors closely supervise top management because their credibility would deteriorate if they did not perform their job correctly. The agency theory postulates that independent directors can eliminate agency concerns and appropriately supervise the management, who could otherwise easily confiscate the company’s assets (Kao et al., 2019; Shan, 2019).

Independent directors, on the other hand, are said to have a favorable impact on SOE performance, according to the stewardship theory (Kyere & Ausloos, 2021). It could be because of several reasons. First, in exchange for increased salary, independent directors in SOEs give up their independence in overseeing internal directors, allowing for more earnings management and less open expression of unfavorable thoughts to the management (Shi et al., 2018). Second, they lack time and energy to monitor the managers because of sitting on several boards (Kakabadse et al., 2010; Shi et al., 2018). Third, most independent directors are chosen from among previous advisers, former government officials, or substantial shareholders. Many people lack the knowledge and motivation to decide whether management is acting in the best interests of shareholders because they have never worked for the company (Kakabadse et al., 2010; Thompson et al., 2019). Finally, they lack government incentives, causing them to behave passively across the board (Kakabadse et al., 2010). Kakabadse et al. (2010) disclosed dominance by inside directors, information asymmetry, and ineffective recruitment process as the significant reasons impacting the effectiveness of independent directors in Chinese SOEs.

Several studies have looked into independent directors and SOEs’ performance linkage. They have, however, produced inconsistent and even contradicting results. From 1994 to 2004, Menozzi et al. (2012) discovered that independent directors do not influence the performance of 114 Italian public utility SOEs. Similarly, Wang et al. (2016) found no influence of independent directors in improving the performance of Chinese SOEs from 2009 to 2013. In addition, both these studies revealed that the presence of politically connected directors adversely influence the performance of SOEs. Similar results were obtained by Kiranmai and Mishra (2019) on the performance of 42 listed SOEs throughout 2012–2017. Considering 320 Korean SOEs, Heo (2018) also found the insignificant effect of independent directors. Abang’a et al. (2021) looked at 45 SOEs in Kenya for four years, from 2015 to 2018, and concluded that independent non-executive directors had no impact on performance. Vu and Pratoomsuwan (2019) discovered that independent directors had a beneficial effect on SOEs’ performance in Vietnam from 2008 to 2014. Independent directors had a favorable influence on the performance of nine Pakistani SOEs measured by Tobin’s Q(Q) from 2010 to 2014, according to Bhat et al. (2018), because they lower agency expenses and safeguard shareholders’ interests. Liu et al. (2015) studied board independence and company performance linkage in Chinese listed companies, as assessed by return on equity (ROE) and ROA. They discover a favorable relationship, particularly for government organizations.

Similarly, Kao et al. (2019) found that board independence favorably impacts the performance gauged via ROA and ROE for a sample of Taiwanese publicly traded companies. According to Fauver et al. (2017), independent directors’ reforms resulted in an upsurge in firm value, which was quantified by Q for 41 countries. In contrast to these studies, Shawtari et al. (2017) used a quantile regression technique to analyse an association between board characteristics and the SOEs’ actual performance. Independent directors adversely impacted the SOEs with high performance after the transformation policy period, that is, 2007–2011.

In light of contradictory theoretical considerations and practical evidence mentioned above, this study expects that independent directors in SOEs would improve SOE performance. Furthermore, in high-leverage companies, independent directors would spend less time monitoring the managers, so they may not impact the performance of SOEs. Thus, it is hypothesized that

H3a: The independent directors have a negative impact on the performance of SOEs.

H3b: The independent directors negatively impact the performance of SOEs with low leverage compared to SOEs with high leverage.

Nominee Directors and Firm Performance

Nominee directors are appointed either by the government, lender, or employees. According to agency theory, nominee directors favorably influence the company’s performance. The information hypothesis and monitoring hypothesis have supported it. The information hypothesis highlights that appointment of nominee directors on the board provides easy access to the information to the nominating institute, which is not possible otherwise. It enables the company to get easy access to the finance at cheap rates, which reduces agency problems and ultimately upgrades its performance.

Similarly, according to the monitoring hypothesis, nominee directors are also outsiders and have professional expertise. They facilitate the boards’ adequate functioning and ensure that the organizational policies and plans have been appropriately implemented (Ghosh, 2018). It leads to improved manager supervision and fewer agency issues, enhancing firm performance. Nachane et al. (2005) reported that nominee directors could quickly strengthen the flow of information between the appointer and a company. They also shared that the easy sharing of information by the executive directors develops a relationship among them. It enables SOEs to approach the government to raise finance in a financial crisis.

In contrast, some authors proclaim that a close relationship between these directors and the company may lead to an information-based monopoly (Rajan, 1992). Agarwal and Kaul (1972) opined that nominee directors do not have shares in the company and are responsible to the government; protecting the public interest or controlling mismanagement in the company is not possible. Empirically, Kiranmai and Mishra (2019) did not observe any influence of nominee directors on the performance of 42 listed Indian SOEs throughout 2012–2017.

Given the complex agency problems in the SOEs, the role of nominee directors seems to be more critical. The proper flow of information and easy availability of finance would affirmatively affect the SOEs’ performance. Moreover, the relationship maintained by nominee directors with the government and the company enables them to take care of the interest of all stakeholders. If SOEs have high leverage, conflicts between lenders and equity holders will arise because nominee directors appointed by the lenders prefer less risky strategies, which may not impact SOEs’ performance. Thus, it is hypothesized that

H4a: The nominee directors positively impact the performance of SOEs.

H4b: The nominee directors positively impact the performance of SOEs with low leverage compared to SOEs with high leverage.

Research Method

Sample, Period, and Data Sources

The sample for the study is chosen from 61 SOEs registered on BSE, which constitutes 7.18% of the total market capitalization as of February 29, 2020. Out of the 61 SOEs, the study considers only 24 SOEs among the top 500 companies by market capitalization. These include 10 Maharatnas and 14 Navratnas. These Maharatnas and Navratnas enjoy excellent corporate governance grading, and their board has received more powers from the government than Miniratnas (Public Enterprise Survey, 2019). From the initial dataset of 24 SOEs, five SOEs not listed on BSE during the entire period (Garg, 2007) get eliminated, leaving the final sample to 19. It considers the time frame from April 2001 to March 2019, that is, 18 years. The sample begins in 2001 as clause 49 of the listing agreement became operational in 2001 and ended in 2019 as it is the latest year for which data are available. The sample starts in 2001 because clause 49 of the listing agreement became operational in that year, and it concludes in 2019 as the data are available till that year. The study combines the data from the Bloomberg database and the company’s annual reports. The final sample consists of a panel of 342 observations, that is, 19 companies for 18 years.

Variable Measurement

Dependent variable: In line with Liu et al. (2015), Heo (2018), and Kao et al. (2019), firm performance is gauged via ROA. The values are collected from the Prowess database.

Independent variable: According to the guidelines issued by the Department of Public Enterprises in 2001, the board composition variables comprise functional directors (similar to executive directors), nominee directors, and independent directors. Board size depicts the aggregate of directors on the board. Executive directors are calculated as the percentage of executive directors (PED). They are full-time employees who assist with the daily operations of the organization. Independent directors are gauged as the percentage of independent directors (PID), and nominee directors are computed as the percentage of nominee directors (PND). In SOEs, the government appoints the nominee directors.

Control variables: Following previous studies such as Shawtari et al. (2017), Heo (2018), Vu and Pratoomsuwan (2019), and Kiranmai and Mishra (2019), some control variables have been incorporated to account for the various factors that might affect the performance of SOEs. The first firm size is gauged via the natural logarithm of market capitalization. The second control variable, firm age, is calculated by subtracting the current year’s log from the year of incorporation. The asset turnover ratio, the third control variable, is calculated by multiplying net sales by total assets. The fourth control variable, sales growth, is computed as the ratio of current year sales minus prior period sales over the last year’s sales.

Model Specification and Estimation

Panel data regression is used to examine the association between board composition and SOEs performance. When dealing with both the cross-sectional as well as time-series data, panel data are only used. Panel data comprise three models: pooled ordinary least square (OLS), fixed effect, and random effect. The Hausman test can be used to determine whether the model is fixed effect or random effect (Baltagi, 2008; Greene, 2003), with the fixed-effect model being preferred. Furthermore, the two problems that may affect the results of an OLS regression are heteroskedasticity and serial correlation (Gujarati, 2003). If these problems persist in the data, then the standard errors linked with the regression coefficients will not be accurate (Gujarati, 2003). The white heteroskedasticity test (Dehaene et al., 2001) and the Breusch-Godfrey Serial Correlation LM test are used in this research. The null hypothesis is rejected by the white heteroskedasticity test (2 = 44; p = 0.000). The null hypothesis is also rejected by the Breusch-Godfrey Serial Correlation LM test (2 = 2; p = 0.000). It highlights the variables’ heteroskedasticity and serial correlation issues. The study used a fixed-effect model for the whole period using a generalized least square (Hausman, 1978). The model of the study is

where

Furthermore, this study applies to moderate variable leverage. Similar to the prior studies, leverage is gauged as the total debt scaled by the total assets (Abor & Biekpe, 2005; Amin et al., 2019; Ghosh, 2007; Shawtari et al., 2017; Wen et al., 2002). The SOEs with high leverage are separated from those with low leverage by taking the median of the values. All the values less than the median are termed low leverage, and vice versa. Then a separate panel data regression is run on both the samples to know how leverage affects the association between board composition and the SOEs performance. Out of the total sample of 19 SOEs, 9 SOEs have high leverage and 10 have low leverage.

Results and Discussion

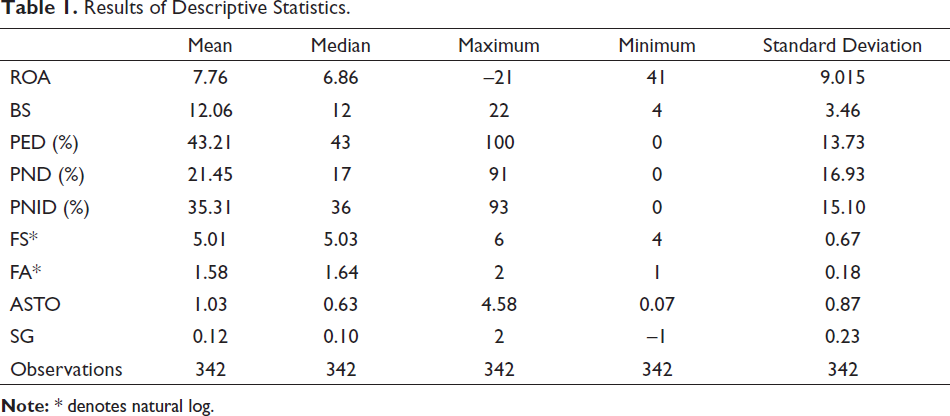

Table 1 illustrates the results of the descriptive statistics for the variables used in the study. The mean (median) of ROA is 7.76 (6.86). The average board size of all the companies is 12.06. The average PED is 43.21, with the minimum and maximum value of 0 and 100, respectively. In comparison to this, the average PND is 21.45. The smallest and highest PND is 0 and 91, respectively. The average PID is 35.31. The lowest and highest PID is 0 and 93, respectively. It means that the boards of Indian SOEs have the majority of executive directors followed by independent directors and then-nominee directors. Furthermore, some firms have all executive/independent/nominated directors, while others do not.

Results of Descriptive Statistics.

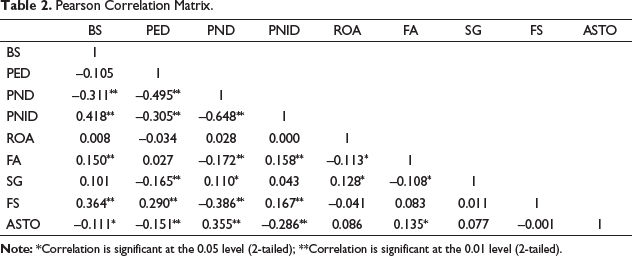

Table 2 reports the results of the Pearson correlation matrix. It infers that the correlation coefficients range from –0.648 (between nominee directors and independent directors) to 0.418 (between board size and independent directors) between all the variables. To further detect multicollinearity among the variables, the variance inflation factor (VIF) test is used, as presented in Table 3. It depicts that the VIF value is above 10 in the case of executive directors, nominee directors, and independent directors, that is, 13.09, 20.29, and 16.96, respectively. There is a multicollinearity problem between these two variables, that could be avoided if we use them interchangeably in the model (Mishra & Kapil, 2017; Shrivastav & Kalsie, 2015).

Pearson Correlation Matrix.

Results of VIF.

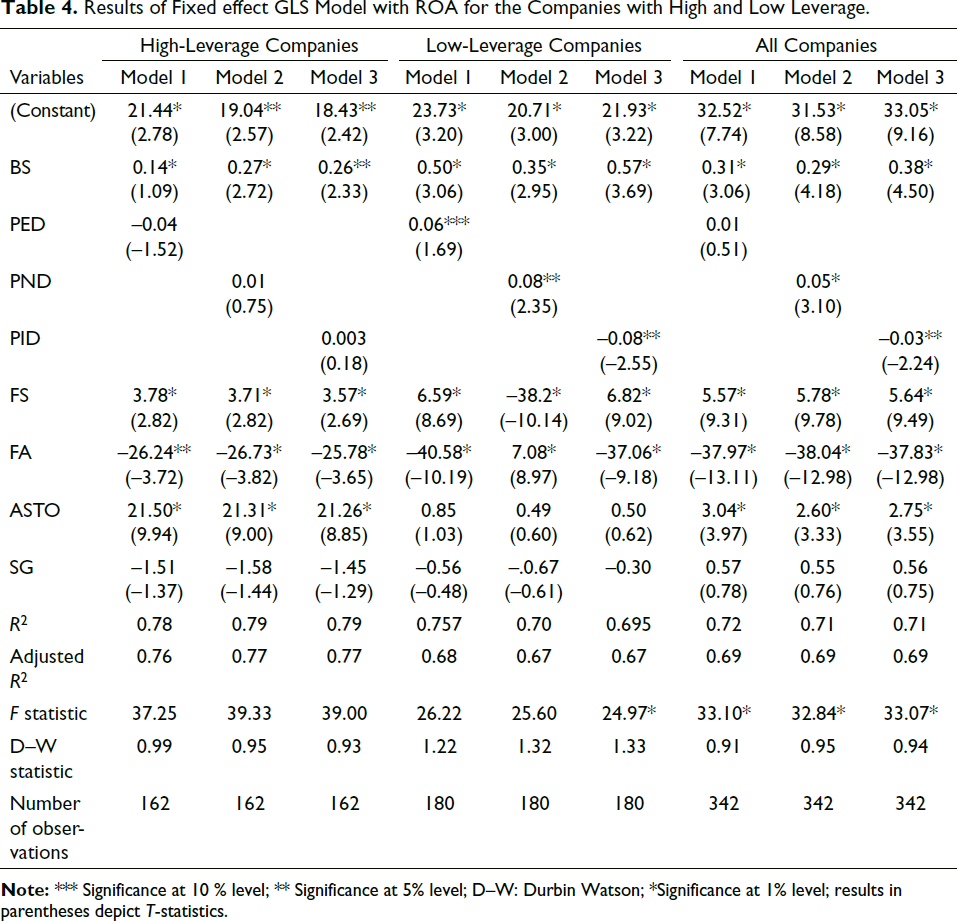

The sample is segregated into two parts: SOEs having high leverage and SOEs having low leverage. Table 4 presents the results of the fixed effect generalized least square (GLS) model for high-leverage companies, low-leverage companies, and the entire sample. Models 1–3 report the panel regression results, including board composition variables one at a time for all 19 companies.

The entire sample in Table 4 shows that the estimated coefficients of “board size” are positive and significant (Model 1-β=0.31; p <.01; Model 2-β=0.29; p <.01; Model 3-β=0.38; p <.01), confirming that board size increases the performance of SOEs. The positive impact of board size is consistent with Heo (2018) and inconsistent with Kiranmai and Mishra (2019) and Menozzi et al. (2012), thus confirming H1a. In case of high-leverage SOEs, board size has no influence on their performance (Model 1-β =0.14; Model 2-β =0.27; p <.01; Model 3-β =0.26; p <.05). In contrast to it, low-leverage SOEs depict positive impact of board size on their performance (Model 1-β =0.50; p <.01; Model 2-β =0.35; p <.01; Model 3-β =0.57; p <.01), thus confirming our H1b. One explanation for this finding is that an increase in the SOEs board size enables better monitoring and controlling of the managers, supporting agency theory. In the presence of debtholders, the directors would spend less time monitoring the managers. Increasing the number of directors would not impact SOEs’ performance.

As depicted in Model 1 of Table 4, the estimated coefficients of “executive directors” show a positive but insignificant impact on the performance of Indian SOEs for the entire sample (β =0.01). The results provide no support for H2a. In high-leverage SOEs, executive directors remain statistically insignificant though negative (β = –0.04). In low-leverage SOEs, the executive directors positively and significantly impact SOEs’ performance (β =0.06; p <.10). These results support H2b and are inconsistent with Srivastava (2015), who indicates that the government’s lack of adequate incentives and monitoring skills demotivates executive directors to work for higher performance. In SOEs with high leverage, the presence of debtholders will also demotivate the directors to monitor the managers, thus bringing an insignificant impact on the performance. Otherwise, less leverage would push directors to put work harder. As it borrows more aggressively, the company works on a wider scale (Chou et al., 2010), ultimately driving its performance.

Regarding “independent directors”, as depicted in Model 3 of Table 4, the estimated coefficients exhibit an adverse influence on the Indian SOEs performance (β = –0.03; p <.05), stating that independent directors impair the Indian SOEs performance, accepting H4a. The results are consistent with Shawtari et al. (2017) and in contrast with Vu and Pratoomsuwan (2019) and Bhat et al. (2018). In SOEs with high leverage, the coefficients show the affirmative and statistically insignificant effect on the Indian SOEs’ performance (β =0.003). In SOEs with low leverage, the coefficients display an inverse and significant influence on the Indian SOEs’ performance (β = –0.08; p <.05), confirming H4b. The adverse influence of independent directors on the SOEs’ performance can be the dominance of inside directors, excessive political interference, and ineffectiveness in their recruitment process (Kakabadse et al., 2010; Thompson et al., 2019), thereby confirming stewardship theory. As soon as SOEs increase their leverage, debtholders would affect the fair and independent decision making of the independent directors, thereby bringing no influence on the performance.

Concerning “nominee directors,” as shown in Model 2 of Table 4, the estimated coefficients show an affirmative influence (β = 0.05; p <.01), stating that nominee directors improve the performance of Indian SOEs, supporting H4a and agency theory. The results are inconsistent with Kiranmai and Mishra (2019). In SOEs with high leverage, the coefficients show an affirmative and statistically insignificant effect on the performance of Indian SOEs (β = 0.01). In SOEs with low leverage, the coefficients show an affirmative and statistically significant influence on the performance of Indian SOEs (β =0.08; p <.05), which confirms H4b. This finding demonstrates that the relationship of nominee directors with the government and the company enables the proper flow of information. It would help the SOEs to get finance from the government quickly. If SOEs have high leverage, there will arise conflicts between lenders and equity holders because nominee directors appointed by the lenders prefer less risky strategies, which may not impact the performance of SOEs.

Results of Fixed effect GLS Model with ROA for the Companies with High and Low Leverage.

Robustness Check

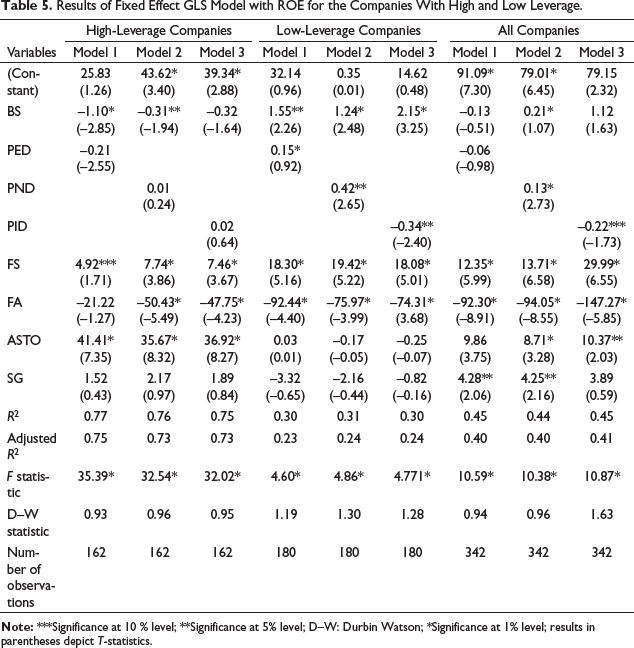

The present study performs a robustness analysis of the findings to ensure they were correct. First, in line with previous research, such as Liu et al. (2015) and Kao et al. (2019), this study re-examined the above-mentioned linkage utilizing accounting-based firm performance and ROE. The study uses the prowess database to select ROE values. Table 5 reports the results with ROE. The findings are similar to the main results in Table 4, except for board size, which is significant with ROE in the case of high-leverage companies. Moreover, the regression results with ROE have less R2 than the results with ROA in the entire sample, high- and low-leverage companies.

Results of Fixed Effect GLS Model with ROE for the Companies With High and Low Leverage.

Conclusion

This study analyses how the board composition affects the performance of 19 Indian SOEs over 18 years (2001–2019). The study also investigates whether the presence of debtholders, another monitoring tool, impacts the relationship between board composition and Indian SOEs’ performance. Board composition embraces board size, executive directors, and non-executive directors (independent and nominee directors). The findings show that Indian SOEs have big boards with a maximum number of executive and independent directors, using ROA as a performance indicator and fixed-effect regression. The study contemplates that board size and nominee directors ameliorate the performance of Indian SOEs, whereas independent directors dwindle the performance of Indian SOEs. The results are consistent with Heo (2018) and Shawtari et al. (2017). Heo (2018) found a positive influence of board size on the performance of Korean SOEs, and Shawtari et al. (2017) found an inverse effect of independent directors on the SOEs with high performance and a positive effect of board size on the SOEs with low performance. The results are inconsistent with Kiranmai and Mishra (2019), as they found a negative effect of board size and nominee directors on the performance of Indian SOEs. Furthermore, because debtholders prioritize shareholders in residual claims and earn disproportionately more from the directors’ actions in excessive leverage in SOEs, board of directors’ supervision is minimal or non-existent. As the marginal value of governance enhancement in a high-leverage firm is reduced, directors may spend less time monitoring and managing the company (Chou et al., 2010), with no effect on SOEs’ performance.

The current research has theoretical implications. It questions the validity of agency and stewardship theory in SOEs regarding a variety of corporate governance variables. First, the findings highlight the significance of further research into the moderating effect of leverage on SOE board composition. When debtholders are less effective in monitoring SOEs board composition variables (e.g., executive directors) are necessary. Second, the findings highlight the various roles inside directors, outside directors, and debtholders play in SOEs. Owing to a lack of incentives and political influence, the executive and independent directors seemed unsuccessful in reducing agency conflicts between shareholders and management in SOEs.

On the other hand, nominated directors seem to boost the performance of SOEs. As a result, agency and stewardship theories seem to provide only a partial understanding of board composition and SOE performance. The board composition of SOEs needs to be re-examined in light of various ideas.

This study has practical implications for the government and policymakers also. First, SOEs’ internal resources are just 35% (Department of Public Enterprises (DPE), 2019), and their dependence on the debt has increased in the last year. So, the SOEs will have to reduce their reliance on debt for the internal governance mechanisms to be more effective. Second, the study throws light on the fact that the decisions taken by the board of Maharatnas and Navratnas are influenced by the politicians, which adversely impacts their monitoring role. This study highlights the importance of clearly demarcating the roles of government and top management to avoid “excessive interference” by the former. It will help SOEs to become globally competitive. There is a need for an industry expert-led board to take all strategic decisions to increase the speed and efficacy of decision-making to “transform SOEs from being ministry-driven to board-driven.” Third, the regulations restrict SOEs to having only two nominee directors. The study results depicting that nominee directors positively impact the performance of SOEs do not support this regulation. Therefore, the government and regulators can find motivation for reform in the appointment of nominee directors. Last, regulations encourage the appointment of independent directors on the board of SOEs. The findings depicting that independent directors adversely affect SOEs’ performance draws immediate attention in this area. The study suggests that the government should bring more clarity to the definition of independent directors in the SOEs. The government should provide executive directors with more incentives to collaborate with independent directors and enhance SOE performance.

The study has a few limitations also. It has ignored the endogeneity amid board composition and the performance of SOEs. Second, it has not considered other elements of the board of directors, which influence the performance like tenure, skills, qualifications, and remuneration package.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.