Abstract

The study investigates the level of profit efficiency in the Bangladesh banking sector over the years 2004–2011. We employ the Data Envelopment Analysis (DEA) method to assess the level of profit efficiency of Bangladesh commercial banks. The empirical findings indicate that the Bangladesh banking sector has exhibited the highest and lowest level of profit efficiency during the years 2004 and 2009, respectively. We find that there are only eight banks which have been profit-efficient, while another four banks are classified as profit-inefficient. The findings from this study are expected to contribute significantly toward decision-making for regulators, policymakers, bank managers, investors, and also to the existing knowledge on operating performance of the Bangladesh banking sector.

Introduction

The banking sector is the main source of funds for long-term investments and the foundation of economic growth (Schumpeter, 1934). In any country, the efficiency of the banking sector ensures an effective financial system. According to Levine (1998), the efficiency of financial intermediation affects a country’s economic growth and at the same time, bank (financial intermediation) insolvencies could result in systemic crises resulting in negative implications on the economy.

The banking sector in Bangladesh is one of the most important mechanisms of their financial system since the early 1970s. All financial institutions, including commercial banks, are required to fulfill economic objectives set by the government. Basically, there are four types of banks operating in the Bangladesh banking sector, namely, Government-owned Specialized Banks or State-owned Development Financial Institutions (DFIs), Nationalized Commercial Banks or State-owned Commercial Banks (SCBs), Domestic Private Commercial Banks (PCBs), and Foreign Commercial Banks (FCBs).

The efficiency of the banking sector has become an imperative issue in Bangladesh since the formation of the National Commission on Money, Banking and Credit in 1986 (Shameem, 1995). The purpose for the establishment of the commission among others is to find solutions for efficient operations and management of the banking system (Shameem, 1995). Furthermore, in 1991, the World Bank also assisted the Central Bank of Bangladesh (CBB) to strengthen the country’s banking sector regulation and supervision. The efficiency of the banking sector is important to maintain the stability of the banking system.

It could be argued that improvements in profit efficiency could lead to higher bank profitability levels and could ensure the sustainability of the country’s economic growth. Furthermore, profit efficiency is also a firm’s maximization of profit since it takes into account both the cost and revenue effects on the changes in outputs scale and scope. Profit efficiency measures how close a bank is to producing the maximum level of profit, given amount of inputs and outputs and price levels (Akhavein, Berger, & Humphrey, 1997; Akhigbe & McNulty, 2003; Ariff & Can, 2008). Thus, profit efficiency provides a complete description on the economic goal of a bank which requires that banks reduce their costs and increase their revenues. Furthermore, Berger and Mester (2003) and Maudos and Pastor (2003) among others suggest that profit efficiency offers valuable information on the efficiency of bank managements.

The objective of this study is to investigate the level of profit efficiency in the Bangladesh banking sector over the years 2004–2011. To do so, we employ the non-parametric Data Envelopment Analysis (DEA) method. The period covered includes a time of significant reform in the country’s banking sector and also the recent global financial crisis through 2007–2008 (Sufian & Habibullah, 2009). Since the National Commission of Money, Credit, and Banking recommendations for broad structural changes in Bangladesh’s financial intermediation system, the CBB have introduced a series of measures among others to deregulate interest rates, improve transparency, strengthen loan classification standards, improve transparency, and relax control over financial transactions and loan recovery. The measures introduced helped improve the non-performing loan ratios and interest related income; however, the overall profitability level of the Bangladesh banking sector continued to remain unstable.

Given that the issue of increasing the profitability of the Bangladesh banking sector is of utmost importance, the findings from this study are expected to interest various parties such as the Central Bank, policymakers, investors, and bank managers. By analyzing the level of profit efficiency of banks operating in the Bangladesh banking sector, we would be able to identify the actual level of profit efficiency and subsequently the level of profit inefficiency, which is recognized as opportunity loss that leads to unstable profitability in the Bangladesh banking sector.

In the next section, we provide a brief review of relevant studies, followed by a section that outlines the data and methodology. The following section reports the empirical findings. The final section concludes and provides discussions on the policy implications.

Related Literature

The basic concept of efficiency is that it measures how well firms transform their inputs into outputs according to their behavioral objectives (Fare, Grosskopf, Norris, & Zhang, 1994). A firm is said to be efficient if it is able to achieve its goals and inefficient if it fails. In normal circumstances, a firm’s goal is assumed to be cost minimization of production. Thus, any waste of inputs is to be avoided. In the production theory, it is often assumed that firms are behaving efficiently in an economic sense. According to Fare, Grosskopf, and Lovell (1985), firms are able to successfully allocate all resources in an efficient manner relative to the constraints imposed by the structure of the production technology, by the structure of input and output markets, and relative to whatever behavioral goals attributed to the producers.

A wide range of models have been used to investigate a spectrum of efficiency-related issues in a wide range of environments. Koopmans (1951) was the first to provide the definition of technical efficiency where the producer is technically efficient if an increase in any output requires a reduction in at least one output, and if a reduction in any input requires an increase in at least one input or a reduction in at least an output. Meanwhile, Liebenstein (1966) was the first to introduce the concept of X-efficiency. The X-efficiency concept defines cost inefficiencies that are due to wasteful use of inputs, or managerial weakness. The X-efficiency concept seeks to explain why all firms do not succeed in minimizing the cost of production and recognizes that the sources of X-efficiency may also be from outside of the firm. In this regard, Button and Weyman-Jones (1992) suggest that X-inefficiency is due partly to the firm’s own actions as well as from exogenous factors surrounding the environment in which the firm operates.

Bader, Mohammed, Ariff, and Hassan (2008) point out that there are a fair number of studies which have examined the efficiency of the banking sectors of developing countries. However, previous studies have mainly concentrated on the technical, pure technical, and scale efficiency concept (e.g., Isik & Hassan, 2002; Tahir & Haron, 2008; Yudistira, 2004). On the other hand, studies which investigate the cost, revenue, and profit efficiency are relatively scarce (Adongo, Strok, & Hasheela, 2005; Ariff & Can, 2008; Berger & Mester, 1999; Maudos, Pastor, Francisco, & Javier, 2002).

Berger and Mester (1999) show that separate evaluation of the cost and revenue efficiency may not capture the goal of a bank which is to maximize profit. The profit efficiency concept helps overcome the shortfall since its main goal is to maximize revenues and profit by minimizing cost from various inputs and outputs. Technically, profit efficiency can be divided into two major types, namely, standard profit efficiency and alternative profit efficiency. The study by Maudos et al. (2002) suggests that besides requiring that goods and services be produced at a minimum cost, it also requires that revenues be maximized in order to match the profit maximization objective. In fact, the empirical evidence shows that there are higher levels of revenue and profit inefficiency than cost inefficiency. The wrong choice of outputs or the mispricing of outputs may result in revenue inefficiency.

Adongo et al. (2005) posit that profit efficiency occurs only if the costs rise from producing additional or higher quality services, but the increase in revenues should be higher than the increase in costs. More recently, Ariff and Can (2008) suggest that the standard profit efficiency measure assumes the existence of perfect competition in both input and output factors. Their findings indicate that a bank is a price-taker implying that it has no market power to determine the output prices. On the other hand, the alternative profit efficiency assumes the existence of imperfect competition, where a bank is a price-setter indicating that it has market power in setting the output prices.

The above literature clearly reveals the following research gaps. First, the majority of these studies have concentrated on the banking sectors of the Western and developed countries. Second, studies investigating the efficiency of the banking sector have mainly concentrated on the technical, pure technical, and scale efficiency, while empirical evidence on the profit efficiency is relatively scarce. Third, to the best of our knowledge, empirical evidence on the profit efficiency of the Bangladesh banking sector is completely missing in the literature. In the light of these knowledge gaps, the present article seeks to provide new empirical evidence on the profit efficiency of the Bangladesh banking sector.

Data and Methodology

Data Collection

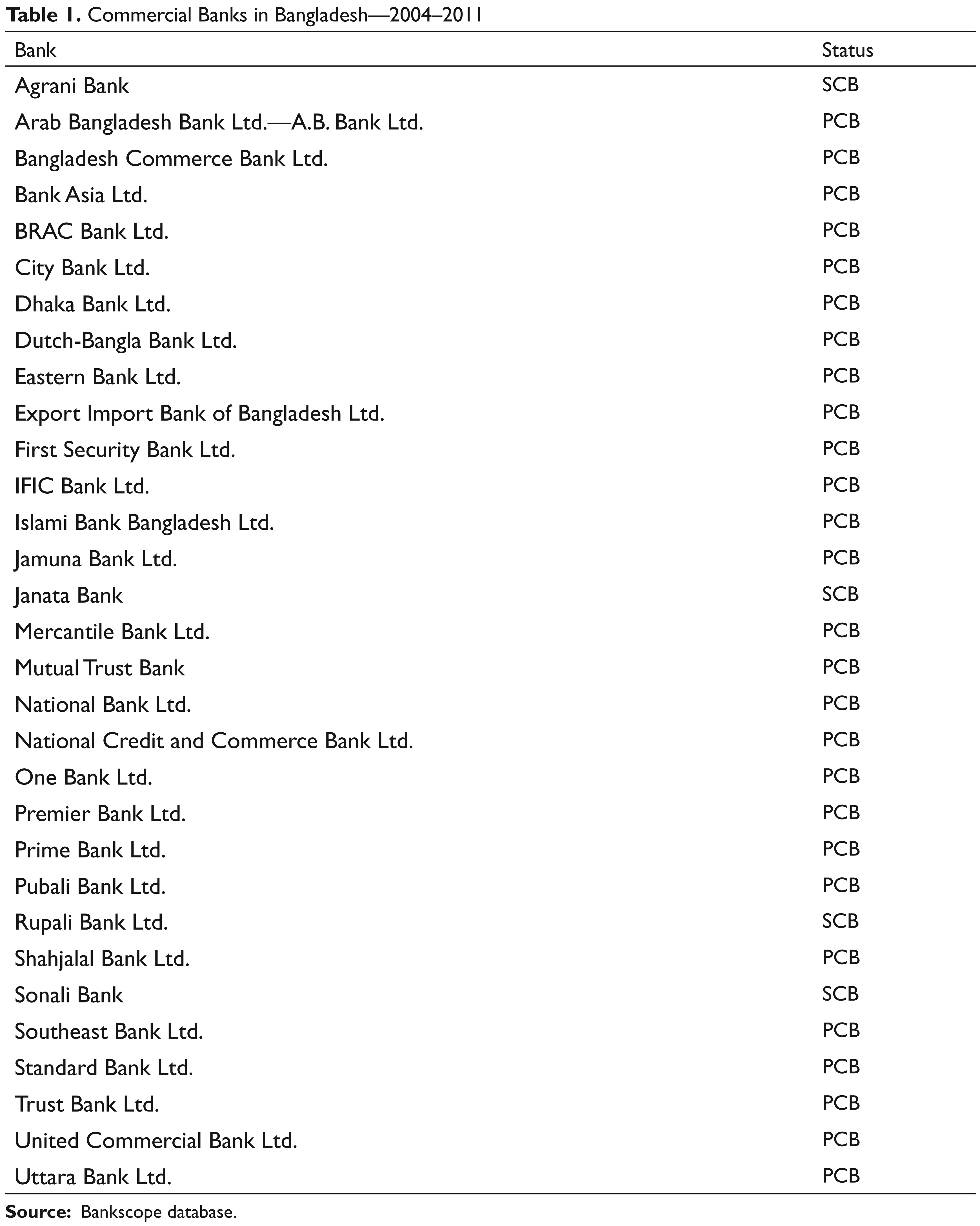

The present study gathers data on all commercial banks operating in the Bangladesh banking sector from 2004 to 2011. The source of financial data is the Bureau van Dijk’s BankScope database which provides banks’ balance sheet and income statement information. The actual number of banks in Bangladesh varies according to year. For the purpose of the present study, we include 31 commercial banks of which complete data are available from 2004 to 2011. The complete list of banks included in the study is given in Table 1. In order to maintain homogeneity, only SCBs and PCBs are included in the analysis. FCBs and specialized development banks (SDBs) are excluded from the sample. 1

Commercial Banks in Bangladesh—2004–2011

Data Envelopment Analysis (DEA)

There are two different frontier analysis methods normally employed to measure bank efficiency, namely, the non-parametric and parametric methods (Berger & Humphrey, 1997). The most commonly employed non-parametric methods are the DEA and Free Disposal Hull (FDH), while the parametric methods are Stochastic Frontier Approach (SFA), Thick Frontier Approach (TFA), and Distribution Free Approach (DFA). According to Murillo-Zamorano (2004), the choice of estimation approach has attracted debate since no method is strictly preferable over the other.

The study employs the non-parametric DEA method, also known as the mathematical programming approach to compute the efficiency of individual banks operating in the Bangladesh banking sector. The method constructs the frontier of the observed input–output ratios by linear programming techniques. The linear substitution is possible between observed input combinations on an isoquant (the same quantity of output is produced while changing the quantities of two or more inputs) that is assumed by the DEA method.

There are six reasons why this study adopts the DEA method (see Sufian, 2004, 2007). First, each decision-making unit (DMU) is assigned a single efficiency score that allows ranking among the DMUs in the sample. Second, the DEA method highlights the areas of improvement for each single DMU such as excessively used input, or under produced output. Third, there is a possibility of making inferences on the DMU’s general profile. The DEA method allows for the comparison between the production performance of each DMU to a set of efficient DMUs (called reference set). Thus, owners of DMUs may be interested to know which DMU frequently appears in this set. A DMU that appears more than others in this set is called the global leader. Apparently, the DMU owner may obtain a huge benefit from this information, especially in positioning its entity in the market. Fourth, several studies suggest that the DEA method does not require a preconceived structure or specific functional form to be imposed on the data in identifying and determining the efficient frontier, error, and inefficiency structures of the DMUs (e.g., Bauer, Berger, Ferrier, & Humphrey, 1998; Evanoff & Israelvich, 1991; Grifell-Tatje & Lovell, 1997). Fifth, the DEA method does not need standardization, therefore, allowing researchers to choose any kind of input and output of managerial interest (arbitrary), regardless of the different measurement units (Ariff & Can, 2008; Avkiran, 1999; Berger & Humphrey, 1997). Finally, the DEA method works fine with small sample sizes.

Based on the idea of Farrell (1957) who originally developed the non-parametric efficiency method, Charnes, Cooper, and Rhodes (1978) introduce the term DEA to measure the efficiency of each DMU, obtained as a maximum of the ratio of weighted outputs to weighted inputs (hereafter referred to as the CCR model). The more the output produced from given inputs, the more efficient is the production. The CCR model presupposes that there is no significant relationship between the scale of operations and efficiency by assuming constant return to scale (CRS) and it delivers the overall technical efficiency (OTE). The CRS assumption is only justifiable when all DMUs are operating at an optimal scale. However, firms or DMUs in practice may face either economies or diseconomies of scale. Thus, if one makes the CRS assumption when not all DMUs are operating at the optimal scale, the computed measures of OTE will be contaminated with scale inefficiency (SIE).

To obtain robust results, the present study estimates efficiency under the assumption of variable returns to scale (VRS). The VRS model was first proposed by Banker, Charnes, and Cooper (1984) and extends the CCR model. The BCC model which derives efficiency estimates under the VRS assumption relaxes the CRS assumption. The VRS assumption provides the measurement of pure technical efficiency (PTE). The PTE measures the efficiency of DMUs without being contaminated by scale. Therefore, efficiency results derived from the VRS assumption provide more reliable information on the efficiency of the DMUs (Coelli, Prasada-Rao, & Battese, 1998; Sufian, 2004). The OTE scores obtained from the CRS DEA can be divided into two components, one due to SIE, the other from pure technical inefficiency (PTIE). If there is a difference between the two OTE scores of a DMU (CRS OTE and VRS OTE), then it indicates that the DMU has SIE and the SIE could be measured from the difference between the PTE and OTE score (Coelli et al., 1998).

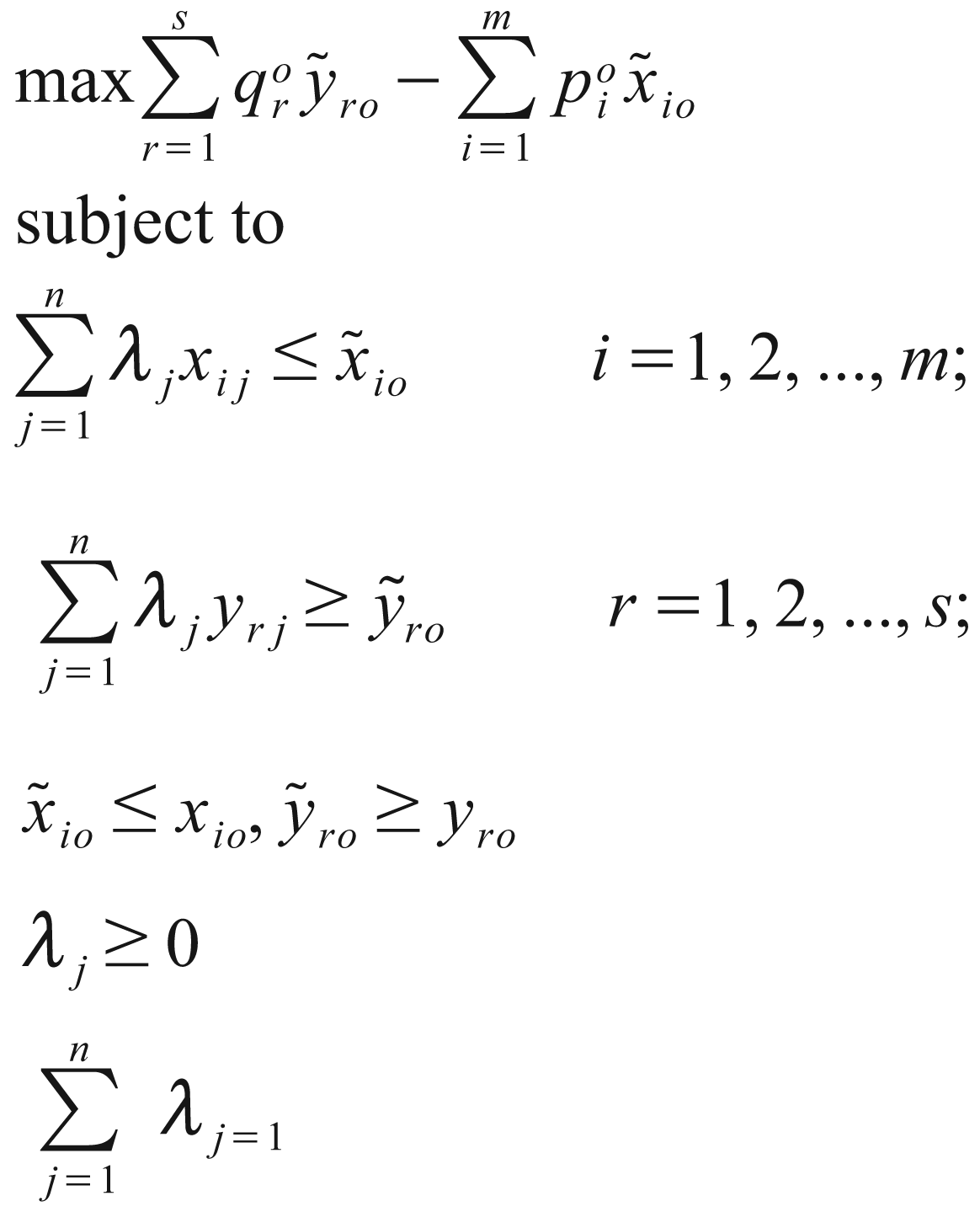

For the purpose of this study, we adopt the DEA Excel Solver developed by Zhu (2009) under the VRS model to solve the profit efficiency problem. The profit efficiency model is given in Equation (1). As can be seen, the profit efficiency scores are bounded within the 0 and 1 range. 2

Profit efficiency (VRS Frontier)

where s is output observation; m is input observation; r is sth output; i is mth input;

Inputs, Outputs, Approaches, and the Choice of Variables

The definition and measurement of bank’s inputs and outputs in the banking function remains arguable among researchers (Sufian, 2007). To determine what constitutes inputs and outputs of banks, one should first decide on the nature of banking technology. According to Das and Ghosh (2006), the selection of variables in efficiency studies significantly affects the obtained results. The problem is further compounded by the fact that variables’ selection is often constrained by the paucity of data. Most of the financial services are jointly produced and the price of costs and outputs are typically assigned to a bundle of financial services.

In essence, there are three main approaches that are widely used in the banking theory literature, namely, production, intermediation, and value added approaches (Frexias & Rochet, 1997; Sealey & Lindley, 1977). The first two approaches apply the traditional microeconomic theory of the firm to banking and differ only in the specification of banking activities. The third approach goes a step further and incorporates some specific activities of banking into the classical theory and therefore modifies it.

The first approach is the production approach which assumes that financial institutions serve as producers of services for account holders, that is, they perform transactions on deposit accounts and process documents such as loans. Previous studies which adopt the production approach are Ferrier and Lovell (1990), Fried, Lovell, and Eeckaut (1993), and DeYoung (1997). The second approach, the value added approach, identifies balance sheet categories (assets or liabilities) as outputs which contribute to the value addition of a bank, for example, business associated with the consumption of real resources (Berger, Hanweck, & Humphrey, 1987). Under this approach, deposits and loans are viewed as outputs, because they are responsible for the significant proportion of value added.

The third approach, the intermediation approach, is the preferred approach among researchers employing the DEA method to examine the efficiency of banking sectors in developing countries (e.g., Bader et al., 2008; Sufian, Kamarudin, & Noor, 2012; Sufian, Muhamad, Ariffin, Yahya, & Kamarudin, 2012). The intermediation approach views banks as financial intermediaries. Under the intermediation approach, the primary role of banks is to obtain funds from savers and convert them into loans for profit (Chu & Lim, 1998). Banks are regarded to purchase labor, materials, and deposits to produce outputs such as loans and investments. The inputs considered among others include interest expense, non-interest expense, deposits, purchased capital, staff numbers (full-time equivalent), physical capital (fixed assets and equipment), demographics, and competition. The potential outputs are measured as the dollar value of the bank’s earning assets where the costs include both the interest and operating expenses (Berger et al., 1987). Previous banking efficiency studies which adopt the same approach include Charnes, Cooper, Huang, and Sun (1990), Bhattacharyya, Lovell, and Sahay (1997), Sathye (2001), and Sufian (2009).

The study attempts to evaluate the efficiency of the banking sector as a whole. It adopts the intermediation approach for the following reasons. The intermediation approach is the most preferred approach among researchers investigating the efficiency of banking sectors in developing countries (e.g., Bader et al., 2008; Hassan, 2005; Isik & Hassan, 2002). As Sealey and Lindley (1977) suggest, financial institutions normally employ labor, physical capital, and deposits as inputs to produce earning assets; the intermediation approach is preferable in this study since it normally includes a large proportion of any bank’s total costs (Avkiran, 1999; Berger & Humphrey, 1991; Elyasiani & Mehdian, 1990).

As Jaffry, Ghulam, Pascoe, and Cox (2007) point out, banks play an important economic role in providing financial intermediation by converting deposits into productive investments in developing countries. The banking sectors of developing countries perform a critical role in the intermediation process by influencing the level of money stock in the economy with their ability to create deposits (Askari, 1991; Bhatt, 1989; Mauri, 1983). Therefore, it is reasonable to assume that the efficiency of banks in terms of their intermediation functions is crucial as an effective channel for business funding.

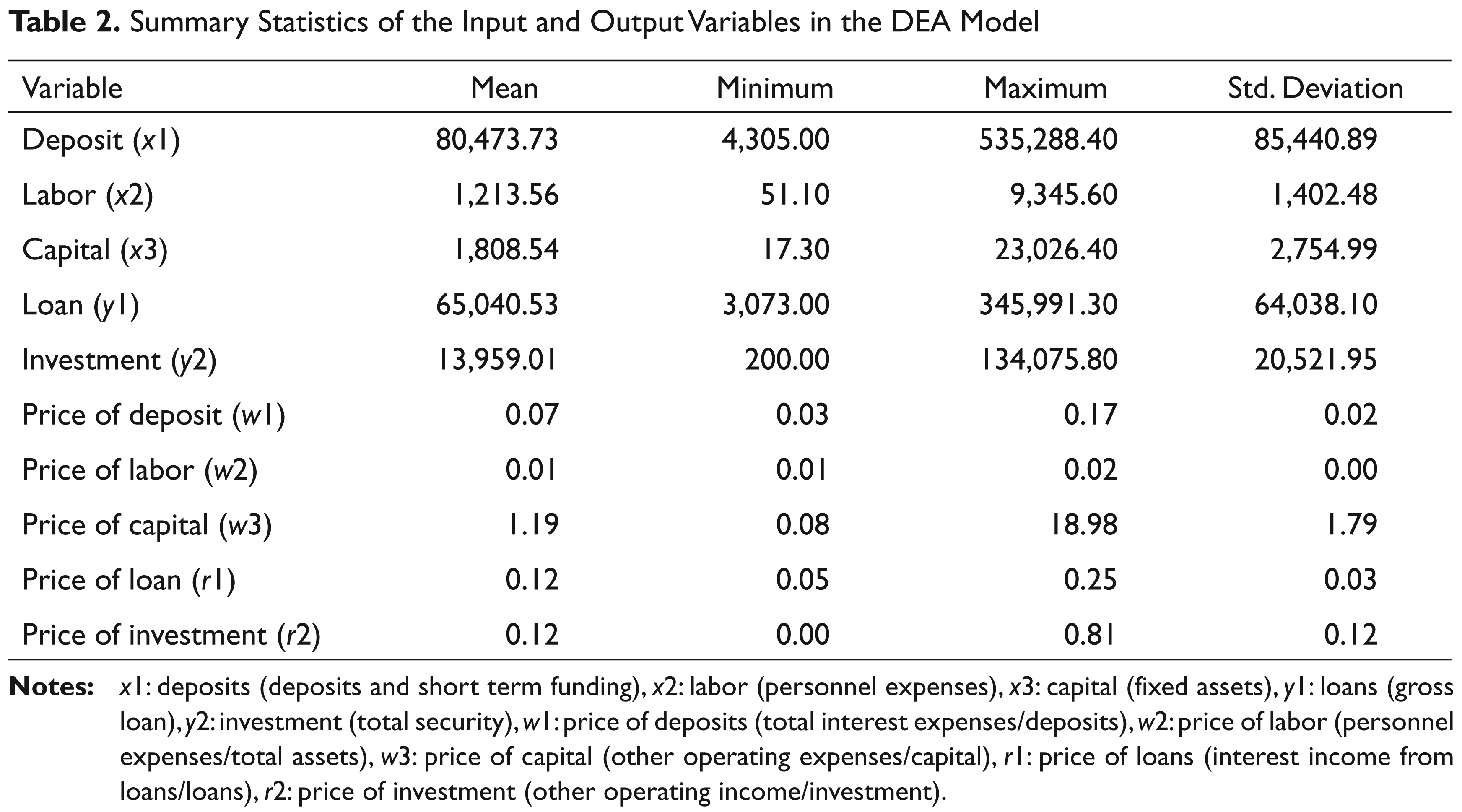

For the purpose of this study, three inputs, three input prices, two outputs, and two output prices variables are chosen. The selection of the input and output variables is based on Ariff and Can (2008) and other major studies on the efficiency of the banking sectors in developing countries (e.g., Bader et al., 2008; Hassan, 2005; Isik & Hassan, 2002; Sufian & Habibulah, 2009; Sufian, Kamarudin, et al., 2012; Sufian, Muhamad, et al., 2012). The three input vector variables consist of x1: deposits, x2: labor and x3: capital. The input prices consist of w1: price of deposit, w2: price of labor and w3: price of capital. The two output vector variables are y1: loans and y2: investments. Meanwhile, the two output prices consist of r1: price of loans and r2: price of investments. The summary of data used to construct the efficiency frontiers is presented in Table 2. 3

Cooper, Seiford, and Tone (2002) point out that there is a rule required to be complied with in order to select the number of inputs and outputs. A rough rule of thumb which could provide guidance can be given as

where n is a number of DMUs; m is a number of inputs; and s is a number of outputs.

Empirical Results

Profit Efficiency of the Bangladesh Banking Sector: Evidence from Specific Years

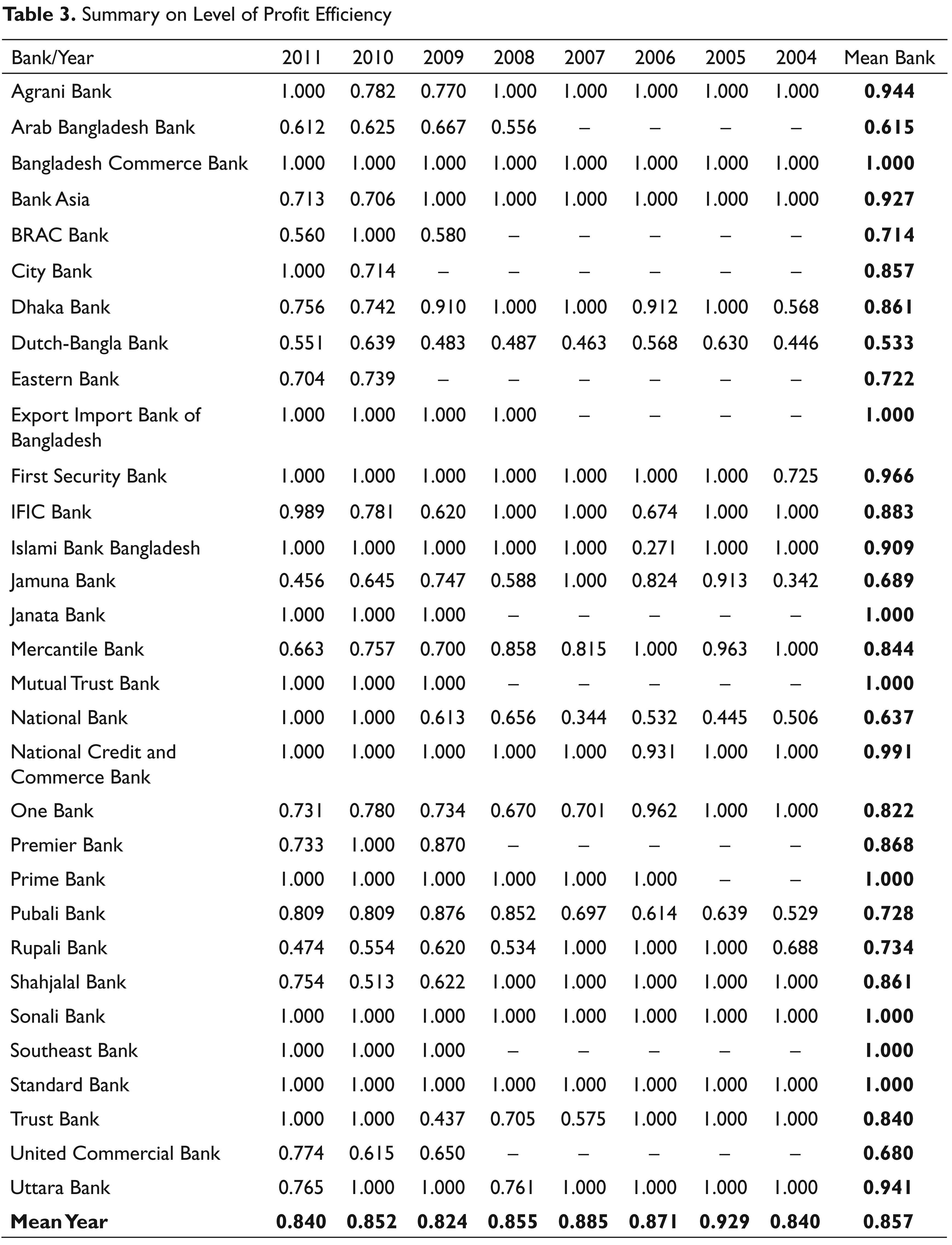

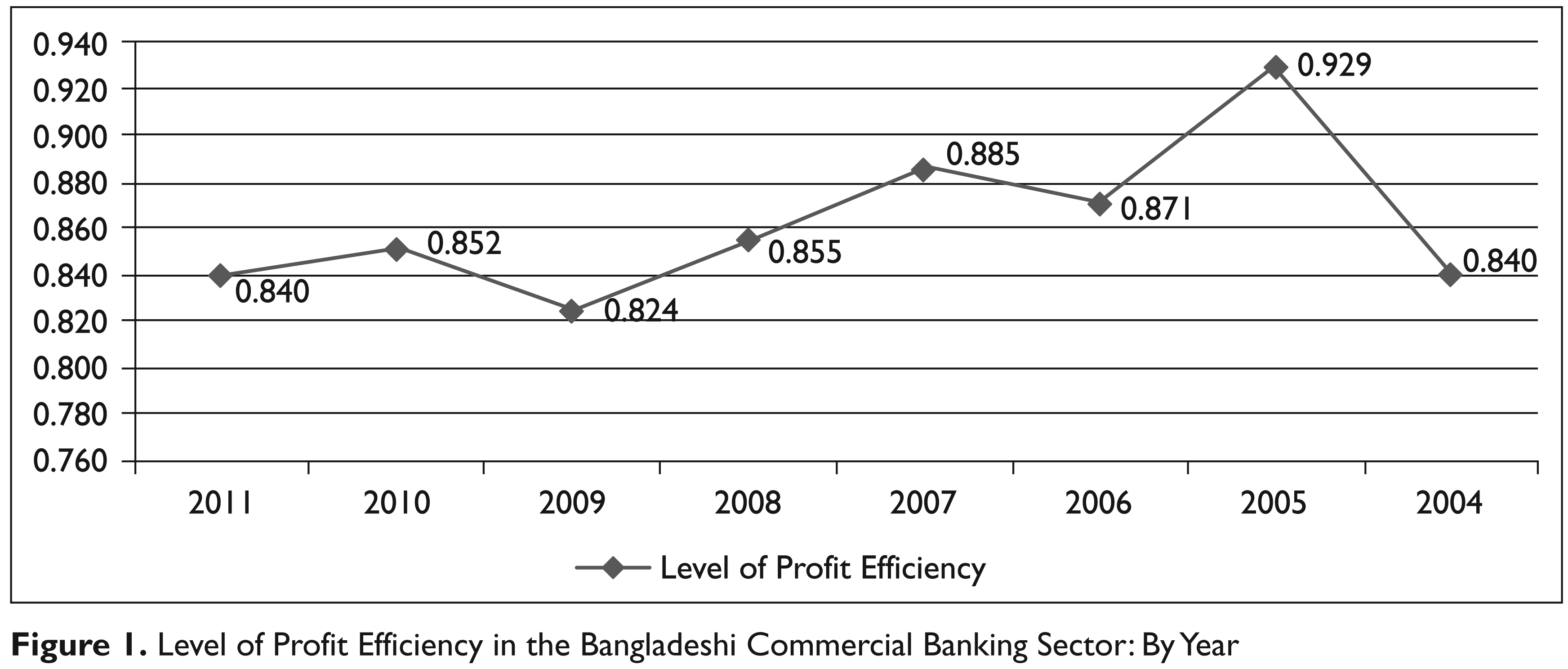

Table 3 shows the mean level of profit efficiency for the Bangladesh banking sector for specific years from 2004 to 2011. The results seem to suggest that during the year 2004, the profit efficiency has been the highest at 92.9 percent and the lowest during the year 2009 at 82.4 percent (see Figure 1). In other words, the Bangladesh banking sector is said to have slacked if they fail to fully minimize costs and maximize revenues resulting in the existence of profit inefficiency. The empirical findings seem to indicate that the highest (lowest) level of profit efficiency (inefficiency) was attained during the year 2004 (84.0 percent [7.1 percent]), while the lowest (highest) level of profit efficiency (inefficiency) was recorded during the year 2009 (82.4 percent [17.6 percent]). In essence, the empirical findings from this study indicate that on average Bangladesh banks have earned 92.9 percent during the year 2004, but only 82.4 percent during the year 2009 and lost the opportunity to make 7.1 percent and 17.6 percent more profit from the same level of inputs during the years 2004–2009.

Summary Statistics of the Input and Output Variables in the DEA Model

Summary on Level of Profit Efficiency

Profit Efficiency of Bangladesh Banking Sector: Evidence from Specific Banks

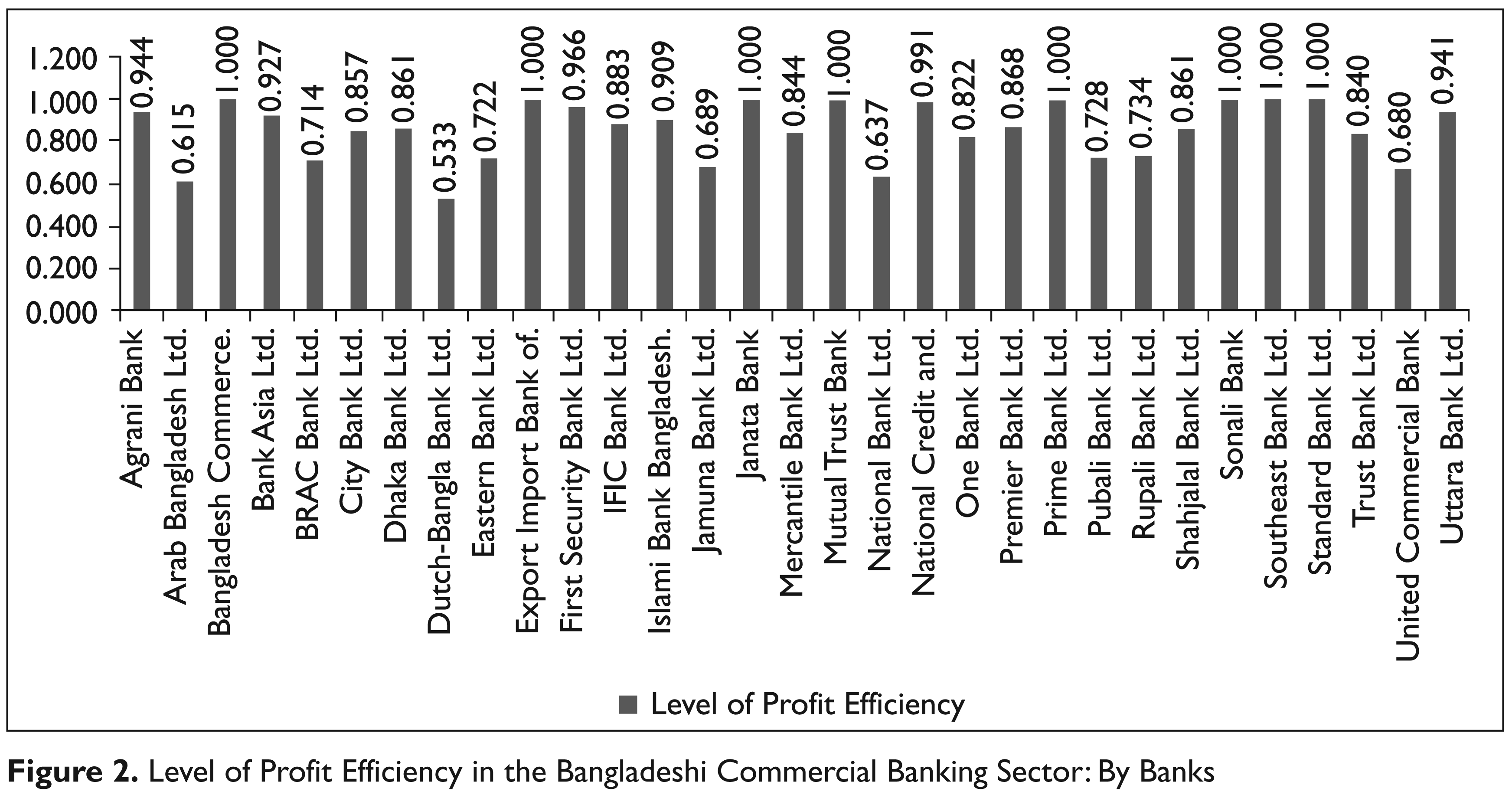

The mean profit efficiency level for specific banks during the years 2004–2011 is given in Table 3. The empirical findings seem to suggest that eight banks, namely, Bangladesh Commerce Bank, Export Import Bank of Bangladesh, Janata Bank, Mutual Trust Bank, Prime Bank, Sonali Bank, Southeast Bank, and Standard Bank, have exhibited the maximum profit efficiency level. This indicates that these banks have not slacked in their intermediation function and have been successful in fully maximizing revenues while minimizing costs subsequently leading to the perfect profit efficiency.

From Figure 2, it can be observed that United Commercial Bank 68 percent (32 percent), National Bank 63.7 percent (36.3 percent), Arab Bangladesh Bank 61.5 percent (38.5 percent), and Dutch-Bangla Bank 53.3 percent (46.7 percent) have exhibited the lowest (highest) profit efficiency (profit inefficiency). The results indicate that these four banks have earned the lowest of what was available and therefore greater loss of opportunity to make higher profits despite utilizing the same level of inputs compared to their peers.

Level of Profit Efficiency in the Bangladeshi Commercial Banking Sector: By Year

Level of Profit Efficiency in the Bangladeshi Commercial Banking Sector: By Banks

Conclusions

To date, studies on bank efficiency are numerous. However, most of these studies have concentrated on the banking sectors of Western and developed countries. On the other hand, empirical evidence on the developing countries is relatively scarce and the majority of these studies focus on technical, pure technical, and scale efficiency. The present study attempts to fill in this demanding gap and provides new empirical evidence on the efficiency of the Bangladesh banking sector during the years 2004–2011. We employ the non-parametric DEA method to measure the level of profit efficiency of individual banks operating in the Bangladesh banking sector.

The empirical findings from this study indicate that the Bangladesh banking sector has exhibited the highest profit efficiency level during the year 2004, while profit efficiency seems to be at the lowest level during the year 2009. We find that Bangladesh Commerce Bank, Export Import Bank of Bangladesh, Janata Bank, Mutual Trust Bank, Prime Bank, Sonali Bank, Southeast Bank, and Standard Bank have exhibited a perfect or 100 percent profit efficiency level. On the other hand, United Commercial Bank, National Bank, Arab Bangladesh Bank, and Dutch-Bangla Bank have been the least profit efficient during the period under study.

The empirical findings from this study clearly call for regulators and decision-makers to review the profit efficiency of banks operating in the Bangladesh banking sector. This consideration is vital because profit efficiency is the most important concept which could lead to higher or lower profitability of the banking sector. To improve the performance of banks, regulators may need to study, employ and exercise information technologies, skills, and risk management techniques applied by well-recognized efficient banks.

Bank managers need to be cognizant of profitability and efficiency levels. This means banks operating in the Bangladesh banking sector need to consider all potential technologies that could improve their profit efficiency levels since the main motive of banks is to maximize shareholders’ value or wealth through profit maximization.

Furthermore, the results from this study have implications for investors whose key motive is to reap higher profit from their investments. Investors may consider planning and strategizing their investment portfolios based on efficiency-based performance.

Finally, the findings of this study are expected to contribute significantly to existing knowledge on the operating performance of the Bangladesh banking sector. The study provides insights and raises implications with regard to the need for optimal utilization of capacities, improvement in managerial expertise, efficient allocation of scarce resources, and productive scaling of commercial bank operations in the Bangladesh banking sector. Such directions may also facilitate sustainable competitiveness of the Bangladesh banking sector operations.