Abstract

This study’s main objective is developing a balanced scorecard (BSC) model as a performance management system for the University of Bisha, Kingdom of Saudi Arabia. The study aims to describe how the University can move from mission to vision using goals and objectives articulated in its strategic plan 2017–2022. The study uses a qualitative research approach. It comprises an extensive review of relevant literature, an in-depth analysis of documentation of the University’s strategic plan 2017–2022, and a comprehensive discussion and face-to-face interview with relevant executives. A BSC framework was developed as a complementary process for the University’s strategic plan 2017–2022. In addition, a strategy map was designed based on the BSC model. The BSC framework and strategy map can be used to assess and monitor the University’s performance towards achieving ‘Educational and Research Excellence’ status by translating its strategic objectives into action plans.

Introduction

The balanced scorecard (BSC) was originally developed by Kaplan and Norton (1992) to complement traditional financial performance measures by including non-financial measures, such as customer satisfaction, internal business process and learning and growth. It has been promoted to overcome the deficiencies of traditional measures and their inability to link long-term strategies with short-term actions (Kaplan & Norton, 1996). The increase in competitiveness in both the private and public sectors, or profit and non-profit organisations, makes it necessary for them to ensure excellent performance. According to Wisniewski and Ólafsson (2004), since performance measurement in profit organisations depends on a set of indicators that measure profitability and competitiveness compared to other organisations, non-profit organisations have come under increasing pressure to modernise and improve their overall performance and service delivery to increase accountability to their stakeholders. Some of the challenges, including the impact of globalisation, electronic commerce, workforce diversification, rapid technological advances, governmental regulations and increasingly competitive environments have complicated strategic management processes within these organisations (Martello et al., 2008). Hence, meeting these challenges requires non-profit organisations to undergo primal changes and continually look for new approaches to create their desired future value. In addition, establishing a strategic plan identifies a non-profit’s objectives for a certain period and how these objectives will be achieved.

Higher education organisations, especially public ones such as public universities, are considered non-profit organisations and must respond adequately to such challenges. In today’s knowledge-based economy and dynamic and competitive environment, it is particularly essential for public universities to articulate their mission, vision and objectives. Public universities are acknowledged as centres of education, knowledge creation and knowledge improvement, which contribute to a nation’s overall growth. The performance evaluation systems could help to address public universities strategic goals (Nazari-Shirkouhi et al., 2020), and to make them more competitive and sustainable over time (Oliveira, 2018). Moreover, addressing strategic plans would definitely pave the way from universities’ present position, based on their mission, to their desired future position, as described by their vision. Hence, adopted as a performance management system, a BSC is a vital management system to ensure the effective and efficient achievement of those objectives (Arjunan et al., 2020). The BSC is supposed to clarify and translate strategic objectives into action plans and link the strategic objectives with measures known as key performance indicators (KPIs). The BSC, through the KPIs, aligns strategic initiatives and action plans with a performance excellence (Nazari-Shirkouhi et al., 2020). This requires considerable time and effort in terms of manager commitment at different levels and, to some extent, a change in staff mindset and thinking (Wisniewski & Ólafsson, 2004). Based on these debates, the main objective of this study is to develop the BSC model as a performance management system for the University of Bisha, Kingdom of Saudi Arabia. The study specifically aims to describe how the University can move from its mission to its vision using goals and objectives articulated in its strategic plan 2017–2022. The findings of the study describe the universities’ objectives translated into initiatives and action plans through the BSC framework and aligned through the strategy map developed based on the BSC model.

Literature Review

Balanced Scorecard Development in Non-profit Organisations

Although the BSC has been widely implemented in numerous for-profit organisations since it was first designed, the model has also been effectively utilised in non-profit organisations (Martello et al., 2008). In addition, the BSC has provided an innovative alternative for non-profit organisations that have not found private sector strategic planning models applicable to their unique planning needs (Ronchetti, 2006). However, Kaplan and Norton (2001a) suggested a number of areas where non-profit organisations might need to modify their approach in adopting the BSC. For example, they have to rearrange the geography of their scorecards, expand the customer concept and redefine the BSC perspectives in consistent with their objectives. Chen et al. (2006) explained the main difference between businesses and non-profit organisations in achieving their missions. That is, non-profit organisations should consider using indicators that fit their special circumstances in their scorecards. For example, non-profit organisations must first ensure they have an appropriate mission and vision to promote their reputation. They must also clearly articulate their mission and vision such that it is achievable through strategic planning (Weinstein & Bukovinsky, 2009; Wu et al., 2011). Moreover, they must ensure that performance measures are not simply focused on costs but also include performance efficiency and effectiveness (Chen et al., 2006; Wisniewski & Ólafsson, 2004).

Although both financial and customer perspectives must be used to enhance the perspectives of internal process and learning and growth, Kaplan and Norton (2001b) suggested that the financial performance is not the main target of most non-profit organisations. The customer perspective through the BSC development in non-profit organisations is the main determinant of the other three perspectives (Chen et al., 2006; Dorweiler & Yakhou, 2005). Dorweiler and Yakhou (2005) described the BSC in non-profit organisations as a ‘top-down’ hierarchy and indicated the structure’s power is integrating the individual efforts among the four perspectives with financial results. However, some empirical studies provided evidence on BSC development in non-profit organisations. For instance, Manville (2007) found that the motivations for adopting the scorecard in the Bournemouth Churches Housing Association in the UK were both internal and external. Farneti and Guthrie (2008) studied Italian and Australian local government organisations and showed that the BSC was used internally as a strategic management device that provides material for external accountability reporting in the Italian case, whereas the BSC was primarily used for internal purposes, with little use for external public reporting, in the Australian case.

Conversely, Greatbanks and Tapp (2007) studied the Customer Service Agency (CSA) section of the Dunedin City Council, and reported that a BSC had a positive effect on achieving a CSA plan and excellence goals regarding delivery of customer service. Similarly, Martello et al. (2008) showed the greatest benefit of BSC implementation at the Rehabilitation Centre is the realisation by Centre personnel that undertaking strategic planning is a significantly more encompassing process than merely looking at long-range planning. Chan (2004) conducted a survey of 451 local government organisations in the United States and 467 municipal governments in Canada. He found that, of the 184 government bodies that responded, only 14 government bodies applied the BSC successfully; the remainder either did not apply the BSC or found it difficult to implement. Moreover, Lawson-Body et al. (2008) also studied the effectiveness of the BSC’s four perspectives on e-government service delivery of 19 country veteran service offices in the United States. They found that three website-supported BSC perspectives (learning and innovation, internal process and veteran value proposition) had a positive impact on e-government service delivery performance, whereas one perspective (financial) had a negative impact because of the digital divide among the various generations of veterans.

Balanced Scorecard Development in Public Universities

As non-profit organisations, public universities have to establish effective measurement systems to ensure their goals achievement. The rapid increase in competition and information technology usage has caused intense competition among public universities, which in turn have tried to improve the resource quality of teaching and research. In essence, public universities need to increase the number of students and specialisations to ensure they remain competitive in their teaching and educational programs (Hsieh et al., 2006; Umashankar & Dutta, 2007). Therefore, they should establish a set of performance evaluation techniques to pursue their educational objectives and develop strategic plans to ensure their competitive advantages within the global environment (Chen et al., 2006). Beard (2009) claimed that identifying and using key performance measures that are consistent with the institution’s mission and core values offer opportunities to create value in higher education. The focus should be on academic measures, such as student numbers, student pass percentages and dispersion of scores, class rank, percentile scores, graduation rates, percentage of graduates employed upon graduation, faculty teaching loads and faculty research/publications, rather than financial measures and the business demands of external accountability and comparability (Umashankar & Dutta, 2007).

Previous studies on BSC implementation in public universities provides insights supporting its successful application. In the earlier stages of BSC development in public universities, Self (2003) indicated that adopting a BSC in the University of Virginia Library began with identifying the scorecard metrics, which must be specific and measurable. The metrics depend on the library’s values, such as customer service, securing funding, controlling costs, digital materials and supporting and developing staff. In addition, Kettunen (2005) also proved that applying a BSC for the Centre of Mechanical Engineering in Southwest Finland can serve as a basis for a campus-wide management information system. Karathanos and Karathanos (2005) described how the Baldrige Education Criteria for Performance Excellence have adapted the BSC and discussed significant differences as well as similarities between BSCs for businesses and education. They found the Rosier School of Education at the University of Southern California adopted a BSC to assess its academic program and strategic planning. McDevitt et al. (2008) stated the BSC provides University administrators with a measurement system that is not only linked to mission and strategy, but also a learning model that supports continuous improvement and environmental responsiveness. The learning environment, which includes facilities, accommodations, physical environment, policies and procedures, may affect whether students are attracted to University (Umashankar & Dutta, 2007). Since universities depend on committed staff to sustain their competitive advantages and achieve superior performance (Bashir & Gani, 2020), Dorweiler and Yakhou (2005) affirm that the BSC provides a framework for staff contributions to the academic institution’s objectives and also as a rewards instrument.

Drtina et al. (2007) identified the following 10 core values cited by faculty and administration: student-centred culture, small classes, globalisation emphasis, excellent teaching, use of technology, experiential learning, career management emphasis, faculty involvement, leadership and ethics and academic reputation. The survey results of 171 participants revealed that the Rollins College (GSB) touted its excellent teachers, and its academic reputation score increased. While teaching was the second-highest value, technology and a student-centred culture scored lowest. They commented that the BSC offered a mechanism for correcting University misalignments, achieved by selecting measures that encouraged employees to act in a way consistent with market expectations. Additionally, Kettunen (2006b) revealed the BSC approach helped the Centre for Mechanical Engineering partners accomplish its strategic themes and objectives for communicating its strategy. Kettunen (2006a) also found that the BSC approach helped managers and employees of higher education institutions in Finland to better understand strategic plans and describe the regional development network strategy. McDevitt et al. (2008) suggested the BSC model requires formulating objectives, metrics, targets, process developments and strategic plans; the latter becomes clearer as the BSC improves over time. They studied the experience of business school faculty with several strategic models before selecting the BSC approach. They found the BSC put the academic unit in a strong position for requesting University funds for strategic initiatives and allocating resources to the major programs that met its desired goals and objectives. They commented that the business school faculty’s BSC model was successful in attaining greater involvement, clarifying the school’s goals and objectives, and establishing guidelines for the administrative units. Similarly, Umashankar and Dutta (2007) asserted that successful application of the BSC in Indian universities will achieve excellence in their chosen fields and serve as a driving force, moving them towards their goals. Drtina et al. (2007) indicated that before a business school implements a BSC, it must define its strategy using a strategic planning process. Alani et al. (2018) revealed that the KPIs through the BSC’s four perspectives act as a strategic tool to evaluate the performance of Sohar University in Oman. In their study, the KPIs allowed all staff members to understand the direction of the BSC in performing their tasks and duties through an effective communication channels throughout the University. Kettunen (2005) concluded that the scorecards of Turku Polytechnic in Finland were based on an agreement between each department and the senior management teams. The BSC was useful to staff because it improved their understanding of the strategy and objectives. In addition, SWOT (strengths, weaknesses, opportunities and threats) analysis has been affirmed by some researchers (Al Frijat, 2018; Lassoued, 2018) as an important step when identifying KPIs to ensure the BSC model is actionable in a way that is consistent with the organisational strategic goals and objectives. Valdez et al. (2017) found that BSC development helped Autonomous University of Coahuila ensure that its strategy is clear enough to be operational by converting its vision into a structured and operative strategy through which the different department and unit duties could be assigned in balanced importance of strategy achievement. Additionally, in the study of Alani et al. (2018), the BSC framework was adopted and adapted through translating Sohar University’s vison, mission and strategy into a set of objectives and measures. They found an association between the BSC four perspectives and the University performance. Arjunan et al. (2020) also adapted the BSC model for Malaysian public universities and found that the proposed model helped to translate the strategy of security practices into a system of performance indicators.

However, successful BSC implementation among higher education institutions such as public universities may face some challenges. For example, Umashankar and Dutta (2007) pointed out that higher education institutions in India are confronted with many barriers, including obstacles originating from the members themselves that hinder them from moving towards their goals. The reasons for resistance include change, fear of accountability and failure and lack of commitment. Additionally, McDevitt et al. (2008) presented several important challenges that face BSC adoption by other academic units, including maintaining a variety of programs, obtaining consensus within and among groups, establishing efficient communication tools across working groups and developing performance measures for long-term objectives.

Balanced Scorecard’s Four Perspectives in Public Universities

The four perspectives of the BSC in public universities have been indicated by the literature in a different arrangement than those of other organisations. They can be restructured to be suitable for the circumstances of public universities, and then to be aligned with the achievement of their strategic goals. For example, Kettunen (2006b) indicated the customer perspective should be at the top of the strategy map, followed by the financial and internal process perspectives, and finally, the learning and growth perspective. In addition, Martello et al. (2008) found that the consumer perspective and financial perspective are placed together at the top of the strategy map of the Rehabilitation Centre. However, the BSC construction in public universities requires cause-and-effect linkages between its four perspectives and objectives within the strategy map that clearly communicate how the objectives can be achieved (Chen et al., 2006; Jusoh & Parnell, 2008; Kettunen, 2005, 2006a, 2006b).

Customer perspective. Chen et al. (2006) described this perspective as representing a strategy focused on value creation and differentiation as perceived by the customer. This perspective helps organisations link their internal business processes with customer desires to improve financial outcomes, using different performance measures such as customer satisfaction, customer response time, market share and on-time delivery (Jusoh & Parnell, 2008). However, BSC development targets in public universities are students as the main ‘customers’ and academic interpretations of the other three perspectives (Dorweiler & Yakhou, 2005). Thus, the customer perspective should tend to the immediate needs and desires of students, parents, faculty and staff, alumni, the corporate sector and society at large (Umashankar & Dutta, 2007). According to Kettunen (2006a), there are three objectives in the customer perspective that can be achieved through the innovation, service and learning processes described in the internal process perspective: organisational competitive advantage, regional development and student satisfaction. However, lecturers, administration, staff and students are all internal customers, whereas the government, society and parents are external customers (Chen et al., 2006). Moreover, Dorweiler and Yakhou (2005) indicated the customer perspective comprises the following themes: students, employers, alumni, parents, teaching innovations, public image, faculty reputation, service quality and continuous improvement.

Internal process perspective. This perspective refers to the critical internal processes that drive customer and shareholder satisfaction (Papenhausen & Einstein, 2006). According to Jusoh et al. (2008), this perspective focuses on the internal processes the organisation must do well to add value to customers and generate financial returns for shareholders. This perspective’s KPIs may include production efficiency, quality, defect rates and cycle time. In universities, however, this perspective focuses on introducing and achieving a degree of excellence in their academic programs and research system (Umashankar & Dutta, 2007). Kettunen (2006a) described the internal process perspective as including sequential processes focused on research and development, online services and education, which form the causal chain of value creation. Moreover, the internal process perspective comprises the following measures (Dorweiler & Yakhou, 2005): teaching and curriculum excellence, service quality and efficiency and strategic issues.

Learning and growth perspective. This perspective aims to identify the skills and processes that drive the universities performance to continuously improve their internal processes (Papenhausen & Einstein, 2006). Jusoh et al. (2008) suggested this perspective focuses on employee abilities, systems and procedures and the capabilities used to achieve performance in internal processes that satisfies customer desires and ultimately produces financial outcomes. Moreover, the learning and growth of the teaching and learning activities, research and community services are the core functions of higher education institutions, and thus have considerable internal processes related to these functions (Reda, 2017). This is accomplished by measuring staff training, development, satisfaction, retention and productivity. Thus, a complete database and network facilities could provide the latest information and encourage staff learning and innovation (Chen et al., 2006). Kettunen (2006a) described this perspective as including three objectives—research and development capabilities, customer knowledge and the educational institution’s pedagogical skills—while Dorweiler and Yakhou (2005) indicated it includes the following measures: teaching and learning excellence, faculty development, technology leadership, teaching and learning innovation, program innovations and improvements, pedagogy enhancements, distance learning, value-added learning, lifelong learning, quality of facilities, reward systems and mission-driven processes.

Financial perspective. The financial perspective includes strategic measures of growth, profitability and risk from the shareholders’ perspective (Chen et al., 2006), such as operating income, return-on-investment, economic value-added, sales growth, cost control and cash flow (Jusoh et al., 2008). Unlike business organisations, where profit-driven financial measures have traditionally been used as KPIs (Dorweiler & Yakhou, 2005), the financial perspective in non-profit organisations might include maximising funding from outside sources or maintaining fiscal stability, instead of profit (Martello et al., 2008). For example, Kettunen (2006a) mentioned that the financial perspective includes the objectives of external funding and funding from central government. Consequently, educational organisations emphasise academic measures rather than financial performance (Umashankar & Dutta, 2007). They do not pay enough attention to the financial perspective, but emphasise the role of customers and employees (Kettunen, 2005). Nonetheless, good financial condition can provide a University with easy access to the latest facilities and excellent resources. Excellence in the financial position is expected to ensure the adequacy of University’s resources, the effectiveness of using the funds and continuing the education processes (Gamal & Soemantri, 2017). Dorweiler and Yakhou (2005) indicated the financial perspective comprises the following measures: fund raising, revenue from operations, human capital investment and financial management.

Research Methodology

Case Study

In the Kingdom of Saudi Arabia, universities play a vital role in generating the essential human capital needed to convert Saudi Arabia into a developed country by achieving Kingdom’s mission 2030; hence, they must move in tandem with global challenges, competitiveness and technological developments. In addition, establishing policies and governance frameworks for pursuing academic achievement will enable universities to educate a new generation of graduates who can actively engage in the global world.

University of Bisha, as a new university established in 2014, was selected as a case study to achieve the study objective of developing a BSC in Saudi universities. The University’s role is partly to develop academic programs both at a semi-professional and professional level consistent with Kingdom’s vision 2030. Since its establishment in 2013, the University has introduced many professional programs as part of its endeavour to provide quality accredited programs and ensure continuous improvement in both teaching and learning processes and research. The University’s goal is to ensure its ‘Academic and Research Excellence’ status is consistent with its vision and mission. A performance management system such as the BSC is a compulsory and complementary system as the University of Bisha pursues institutional accreditation for its current and newly established programs. The BSC model is expected to help the University of Bisha tie its strategies to excellent performance to create stakeholder value. The University of Bisha was adopted for a case study to develop a BSC model as a performance management system that will provide an inclusive overview of the achievement of the University’s strategic objectives articulated in its strategic plan 2017–2022. A primary question was drawn to explore the BSC development as a performance management system to translate the University’s strategic plan 2017–2022 into action plans. Subsequent scorecard questions were formulated to explore the suitability and applicability levels within the BSC framework and strategy map.

Data Collection

Qualitative data were gathered using subsequent processes to answer the primary study question and scorecard questions. The primary study question was ‘how to develop the BSC model as a performance management system for the University’s strategic plan 2017–2022?’ The scorecard questions were related to the applicability level of the proposed initiatives (action plans) and KPIs with its aligned percentages. However, the data collection began with analysing the University’s strategic plan 2017–2022, followed by a structured interview and in-depth discussion with relevant executives and officers in the Deanship of Development and Quality–University of Bisha. Of the Deanship of Development and Quality staff and officers, 8 members were interviewed together two times during February 2019. This was followed by many meetings, workshops and presentations on the progress of developing the initiatives (action plans) and KPIs during this study over a 2-month period during May to July 2019, which were accordingly amended and finalised. The proposed initiatives (action plans) together with relevant KPIs were approved, and finally assigned to allow the development of the BSC’s framework and strategy map.

Findings and Discussion

Steps to Articulate the University’s Strategic Plan 2017–2022

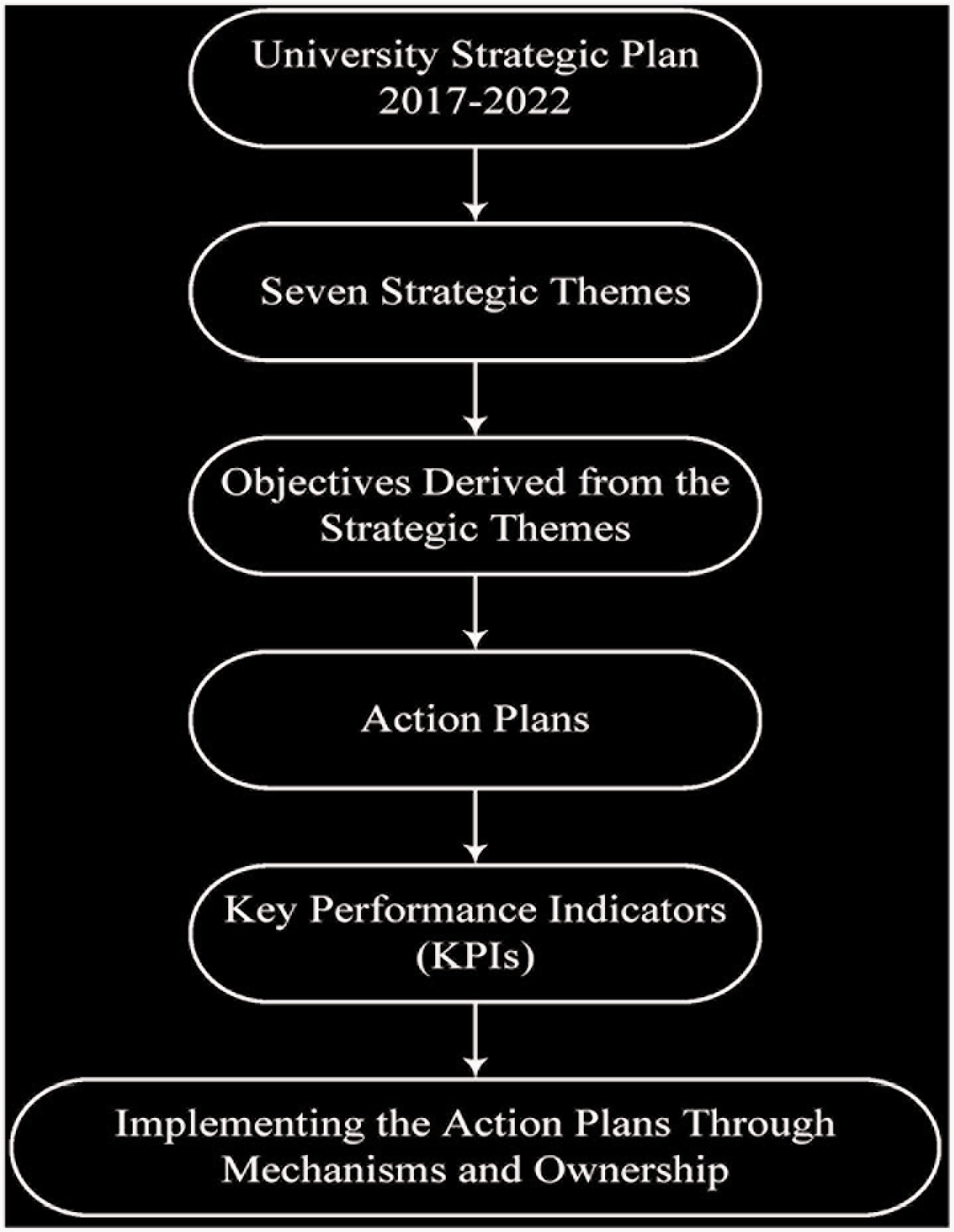

The University’s strategic plan 2017–2022 was reviewed and analysed, and the key steps shown in Figure 1 were developed to illustrate the University’s movement from its current position, described by its mission, to the targeted position, described by its vision. The University strategy was considered the foundation for the following steps; strategic themes, objectives, initiatives (action plans) and KPIs were then developed using the BSC model.

Through the key process steps developed, the University addresses the consequential dependency of the strategic planning horizon by conducting the short-term planning at regular intervals to ensure that the long-term planning is met. In essence, in the 5-year strategic planning 2017–2022, the University should start to lay down the achievement of its vision and mission based on the seven strategic themes, which derive the strategic objectives. Responsibilities for each strategic objective under each of the strategic theme are identified and pursued through the actions plans, and reported through the KPIs cards developed. Consequently, the critical issues related to implementation mechanisms must be well positioned to denote the importance and urgency of the mechanisms as well as to ensure that the mechanisms are applicable.

The Strategic Objectives and Initiatives of the University’s Strategic Plan 2017–2022

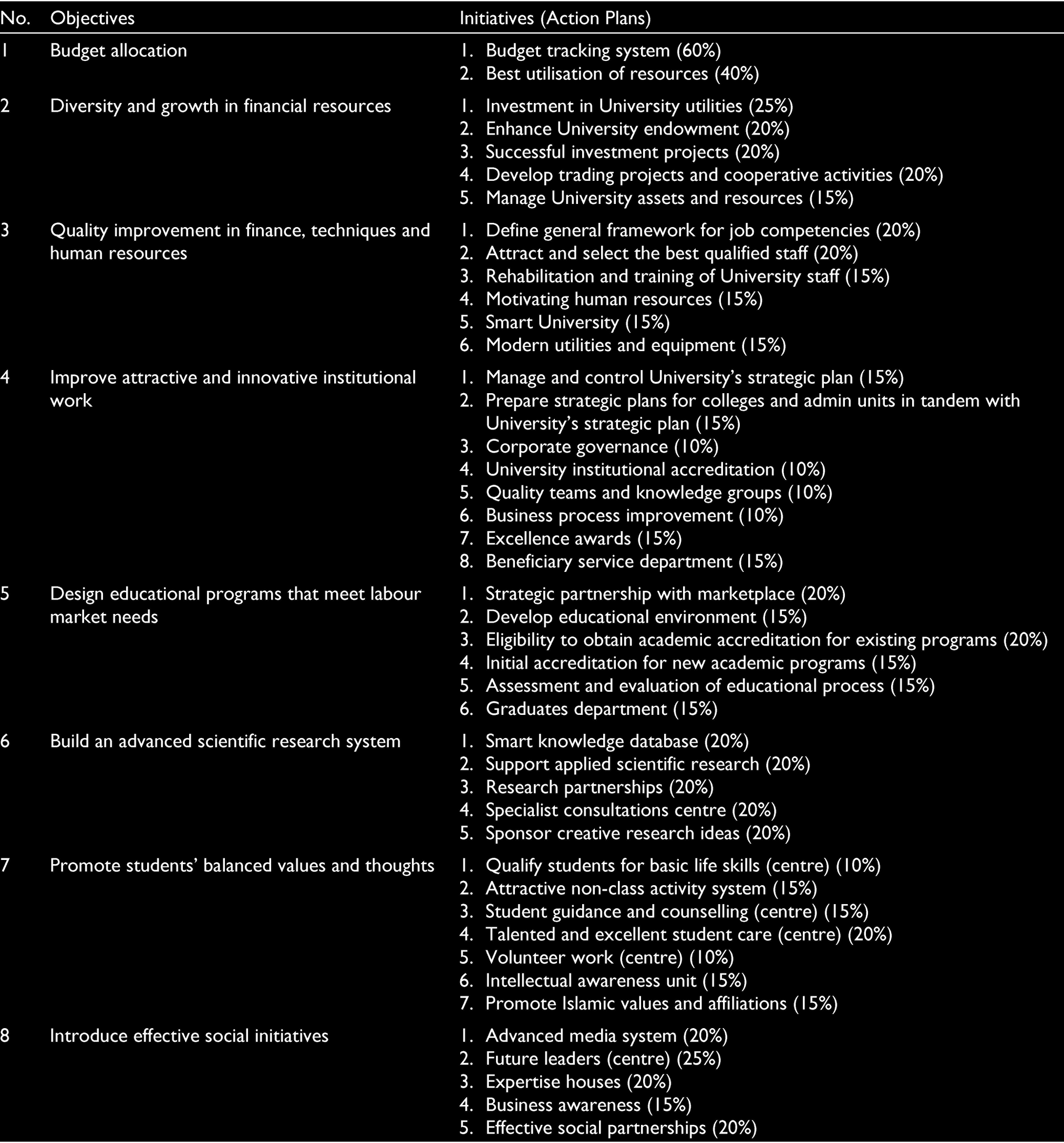

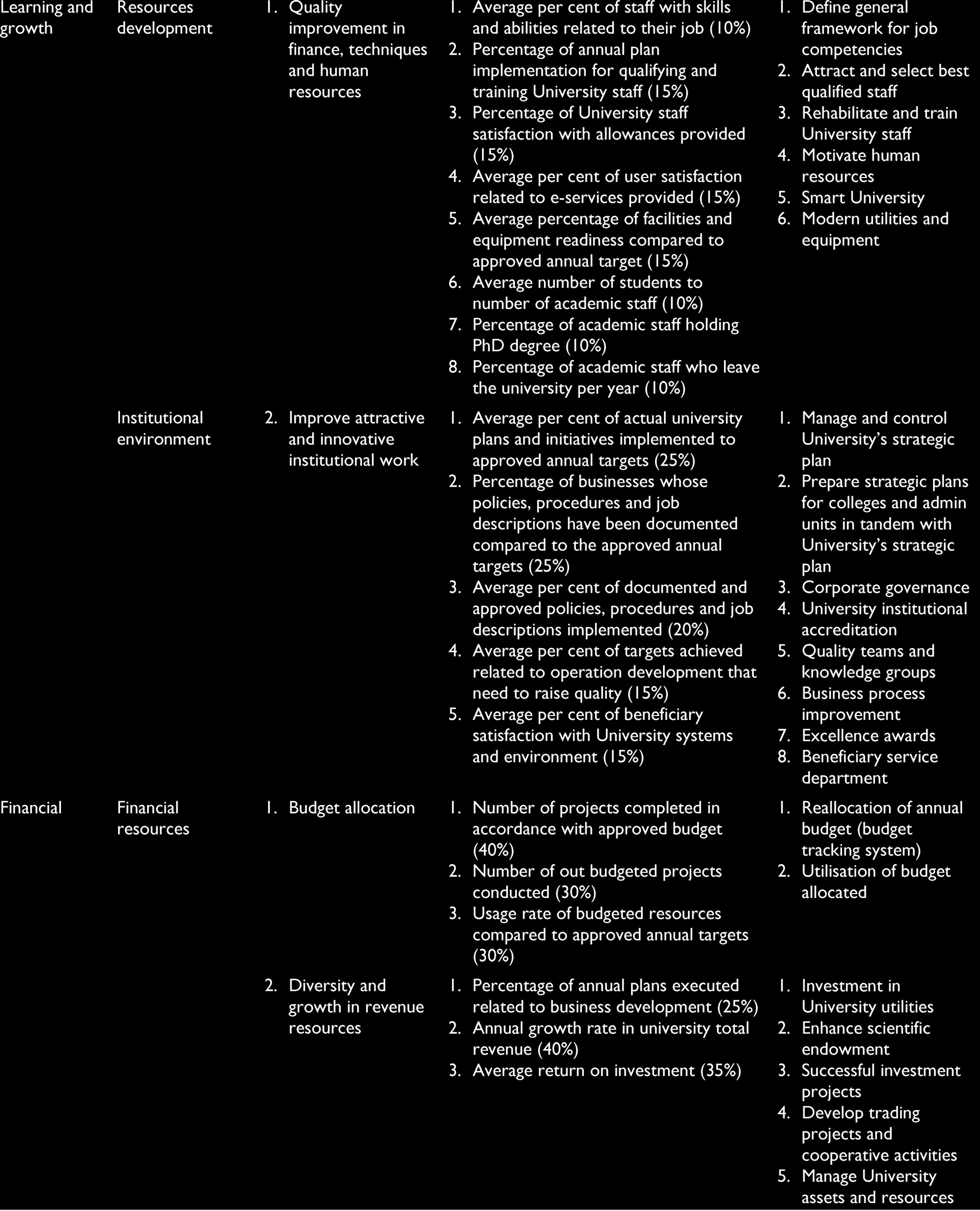

The University’s strategic plan 2017–2022 is considered a movement towards ‘An Innovative and Creative Society’ by placing more focus on ‘Excellence and Sustainability in teaching and research’, as stated by the Dean of Quality and Development. After a long discussion with the Deanship of Quality and Development team, eight strategic objectives were articulated to ensure the University’s sustainability by report card for the 51 KPIs and 45 initiatives (action plans) in tandem with the eight standards of the Institutional Accreditation Authority in Saudi Arabia. The eight objectives consist of the following: (1) Budget Allocation, (2) Diversity and Growth in Financial Resources, (3) Quality Improvement in Finance, Technical and Human Resources, (4) Improve Attractive and Innovative Institutional Work, (5) Design Educational Programs that meet Labour Market Needs, (6) Build an Advanced Scientific Research System, (7) Promote Students’ Balanced Values and Thoughts and (8) Introduce Effective Social Initiatives. Unlike previous studies (Chen et al., 2006; Gamal & Soemantri, 2017; Kettunen, 2005; Martello et al., 2008; Umashankar & Dutta, 2007; Wu et al., 2011), each action plan was assigned a proportion based on the relevant strategic objectives as discussed with interviewees and approved in the final meeting with Quality and Development Deanship officers. This allows assigning an importance level for each plan’s implementation and control the achievement level in the yearly report. Table 1 provides the initiatives for the strategic objectives.

The Strategic Objectives and Initiatives.

The aligned percentages for each initiative can be used to direct their projects. Initiatives and procedures together form the mechanisms that will ensure the strategic objectives and overall vision are achieved. While developing the 45 initiatives, 194 value-creating procedures with aligned percentages were identified. For each initiative’s procedures, another 12 executive KPIs were assigned to assess the procedure implementation. These include: the weighted ratio, expected results, execution responsibility, starting and ending date, execution requirements, expected costs, execution ratio and execution quality ratio, performance level and the initiative’s participation ratio for each procedure.

The BSC framework and strategy map development are for the strategic objectives and initiatives articulated by the KPIs, which generally concisely describe the University’s strategy. According to Kettunen (2006b), the strategic objectives and initiatives formed should be coherent and consistent in how to move the organisation towards its vision. Therefore, the 45 strategic initiatives (action plans) stated above aim to control complexity and focus on the critical issues related to all procedures suggested under each strategic objective. They expedite proper positioning that denotes the importance and urgency of implementation.

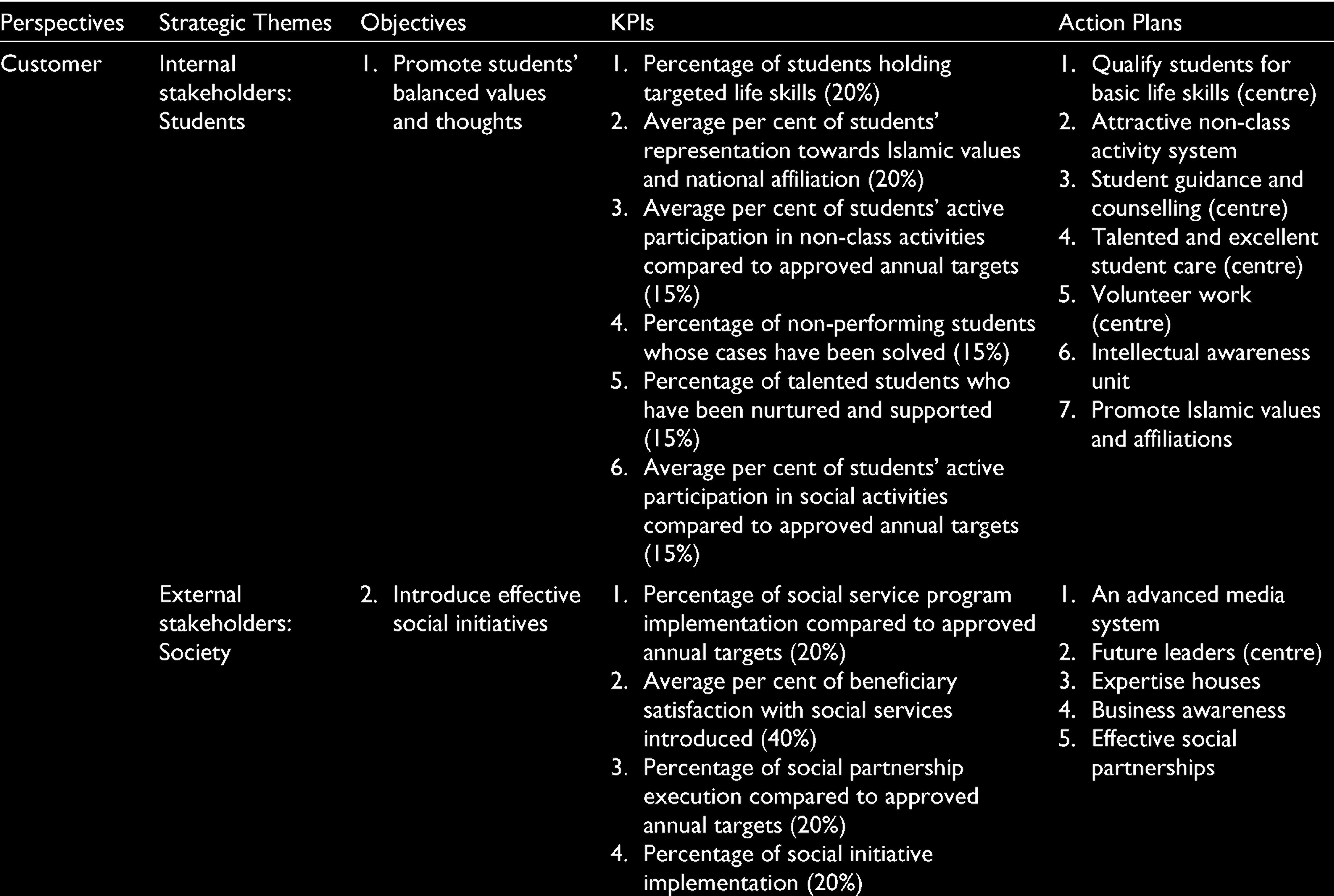

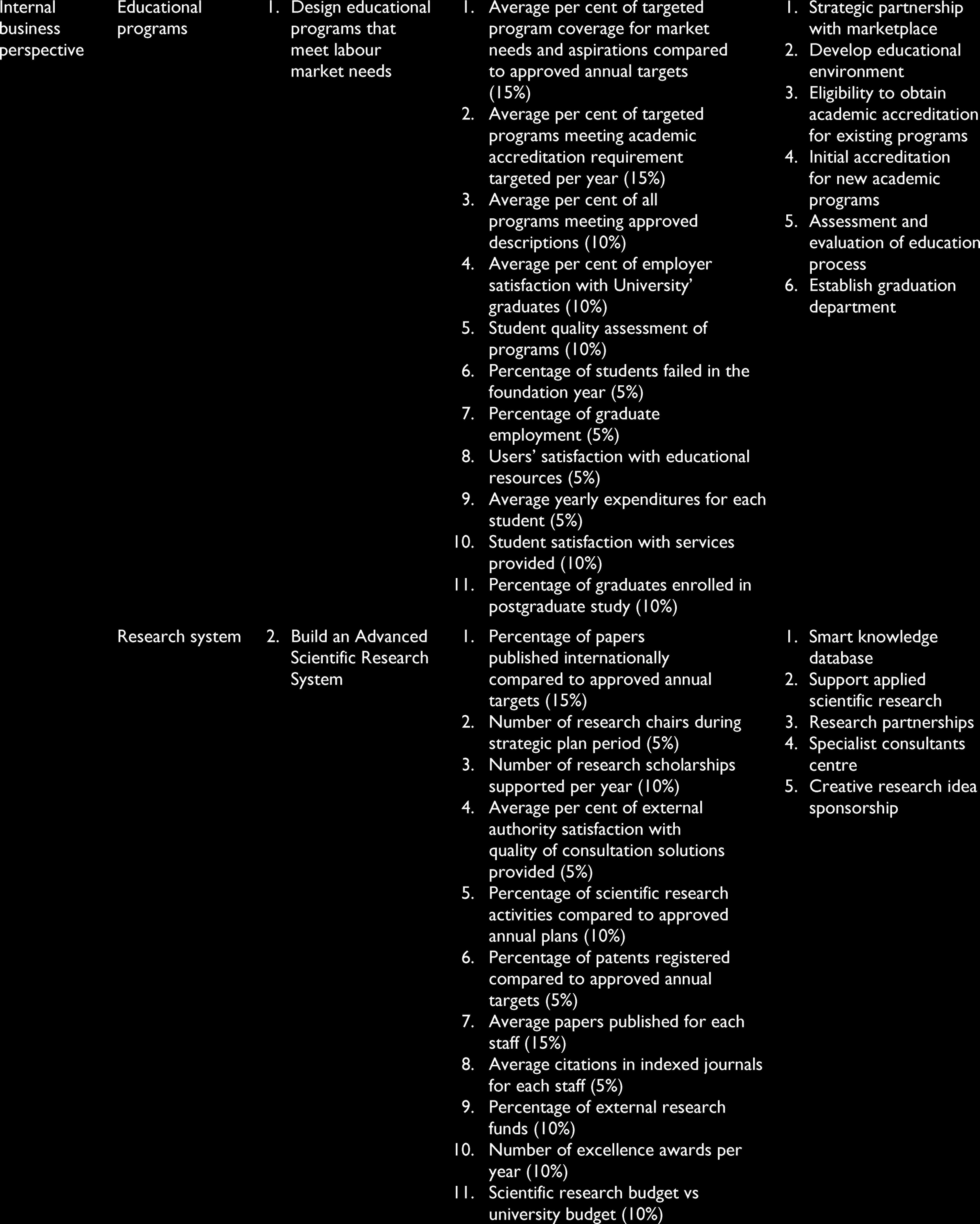

Balanced Scorecard Framework

The BSC framework was developed to translate the University’s vision as articulated in its strategic plan 2017–2022 into action plans, referred to above as ‘initiatives’. All the strategic themes, objectives, initiatives and KPIs are assigned in the BSC framework illustrated in Table 2. Unlike previous studies (Chen et al., 2006; Gamal & Soemantri, 2017; Kettunen, 2006b; Martello et al., 2008; Umashankar & Dutta, 2007), the aligned percentages for each KPI under each action plan have been established to indicate the importance of their execution and assessment. The aligned percentage for each KPIs indicates the measurement level towards achieving the strategic objective. Like the action plans, aligned percentages were assigned based on the relevant strategic objectives as discussed with interviewees and approved in the final meeting with Quality and Development Deanship officers.

Balanced Scorecard Framework.

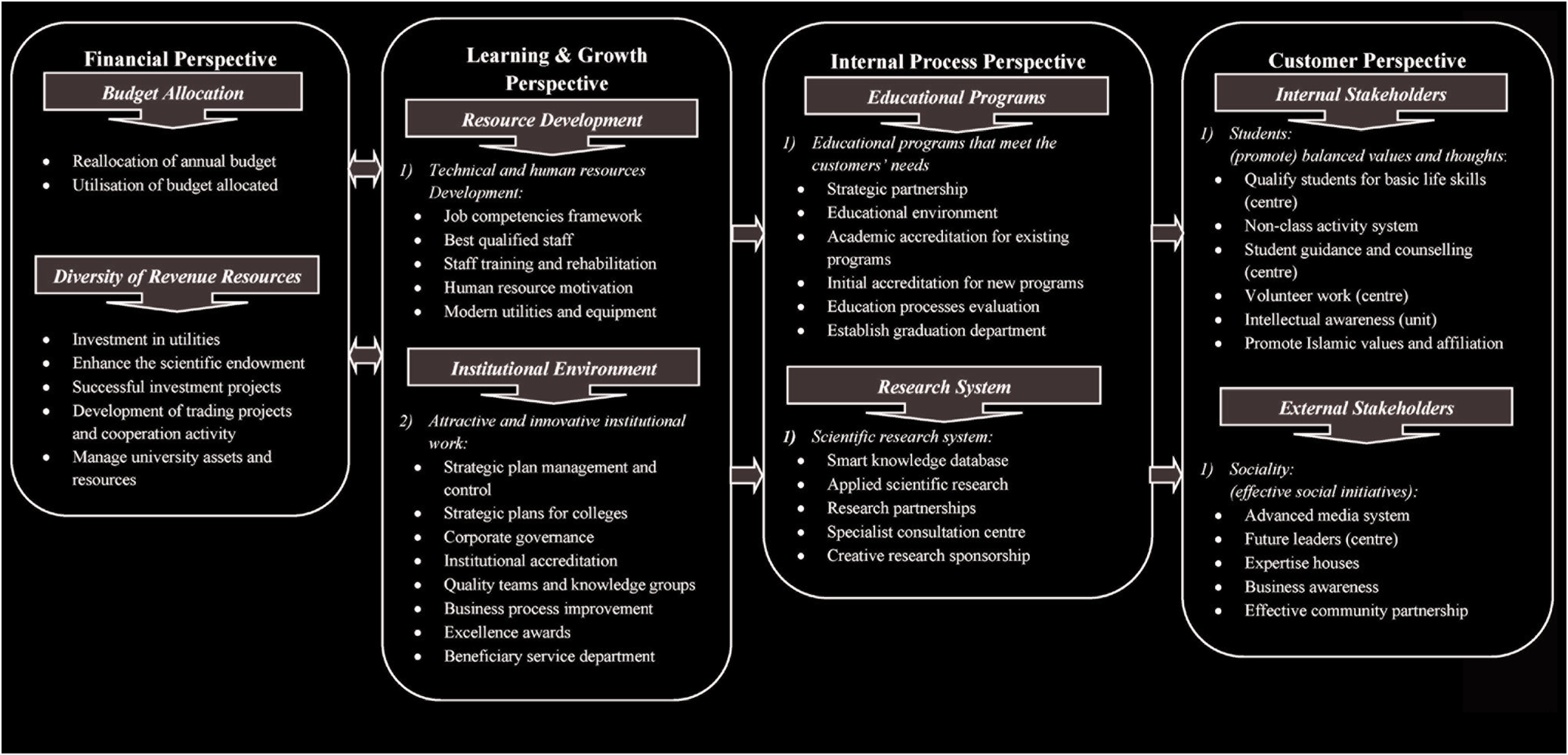

Strategy Map Based on the Balanced Scorecard Model

A strategy map is a graphical representation of an organisation’s strategy and includes the objectives of the BSC perspectives and their causal relationships (Kaplan & Norton, 2001b, 2005). Following Drtina et al. (2007), a strategy map was developed to formulate the long-term idealistic strategy targets to achieve the full vision of ‘Towards a Creative and Knowledge-based Community’. The strategy map’s role is to facilitate communicating the University’s strategic plans and provide a vision of how these plans are linked to the overall objectives. Figure 2 uses the four major perspectives of the BSC model to depict the University of Bisha’s strategy map. It primarily illustrates the cause-and-effect linkages between the eight strategic objectives and initiatives within the BSC’s four perspectives based on the four generations of the model

The causal relationships between strategic themes as performance drivers of strategic objectives are drawn starting with the financial perspective to the customer perspective. The financial perspective includes budgeting and the diversity and growth in revenue resources that must be aligned with the learning and growth and internal process perspectives to achieve customer satisfaction (customer perspective). However, the learning and growth perspective includes resource development and institutional environment themes to improve the quality of finance, techniques and human resources. These objectives could support satisfying customers’ needs and desires through the University’s activities in the internal process perspective. Designing educational programs that meet the labour market and an advanced scientific research system could strengthen the target concerns of the University’s relationship with its external stakeholders.

The customer perspective comprises both ‘Internal Stakeholders’ and ‘External Stakeholders’. Internal stakeholders include one major category, ‘students’, with one major objective. This objective is concerned with students’ balanced values and thoughts and aims to develop qualified, skilled and talented students aligned with balanced Islamic values and affiliations. Moreover, external stakeholders include one major category, ‘society’, which includes one objective concerned with introducing effective social initiatives that aim to strengthen the University’s relationship with its external stakeholders.

The strategy map shows that the University typically should emphasise its stakeholders’ needs and desires. Satisfaction of both internal and external stakeholders results from the classes and non-class activities, as well as value-creating projects under the internal process perspective. Specifically, both are satisfied by strategic themes of ‘educational programs’ and ‘research system’ processes. Hence, the internal process perspective describes the joint projects and initiatives planned to support the ‘educational programs’ and ‘advanced research system’ targets, based on the performance drivers of integrity, quality and ethical culture pursued in the learning and growth perspective. The performance drivers in the University learning and growth perspective describe how to improve finances, techniques, human resources and attractive and innovative institutional work to excel in internal processes, while the financial perspective objectives in the budgeting and income diversity and growth processes are aligned with the objectives of the internal process and learning and growth perspectives. In other words, financial support of the learning and growth perspective would definitely propel internal processes towards achieving customer satisfaction.

Conclusion and Implications

This study’s goal was to develop a BSC model as a performance management system for the University of Bisha, Kingdom of Saudi Arabia. The BSC development was a complementary process to the suggested framework for the University’s strategic plan 2017–2022, which was based on the eight strategic objectives identified through the seven strategic themes. The findings document the University’s strategic plan 2017–2020 in a manner that reflects long-term strategic plans revisited to ensure the University’s sustainability. The findings also aligned the strategic plans with the University’s mission and vision to construct the BSC approach. The strategic plans identify the directions that lead to customer satisfaction based on the strategic goals. Hence, the findings show the initiatives and KPIs that would help the University implement its strategy. The BSC framework was developed using a customer-based strategy since customer satisfaction is at the top of the University’s strategy. The fundamental finding is the translation of the University’s strategic goals into action plans. Based on the objectives under each strategic theme, those objectives were classified into the BSC’s four perspectives to develop the framework. The choice of strategic themes and objectives for the BSC’s four perspectives was based on what is necessary to clarify the strategy identified through the documentation analysis and interviews. The customer perspective includes two objectives for achieving customer satisfaction. The internal process perspective includes two objectives that propel value-creating projects towards achieving ‘Academic and Research Excellence’. The learning and growth perspective includes two objectives to support finance, techniques, human resources and attractive institutional work objectives to excel in the internal process perspective. Finally, the financial perspective includes two objectives aligned with the objectives of the learning and growth and internal process perspectives. Strategic initiatives were assigned, and the KPIs under each initiative were normalised with all objectives under each perspective.

A total of 44 initiatives and 51 KPIs are included in the BSC’s four perspectives; these indicators were tied to faculty performance evaluation. The KPIs are followed by specific action plans (initiatives), as structured value-creating projects were positioned to achieve strategic objectives under each of the strategic themes. The findings also include the University of Bisha’s strategy map, which presents the University strategy’s main characteristics in a manner that ensures the action plans are linked with the overall objectives under each theme. Hence, it provides a visual linkage between the strategic objectives and action plans to help the University staff and employees work in a more coordinated and collaborative manner towards achieving the overall objectives. The visual linkage provided in the strategy map allows the University’s progress towards a better future described by its vision to be measured and evaluated.

According to the study’s findings, some major practical implications can be identified. First, the BSC framework can be used to assess and monitor the Saudi universities’ overall performance towards achieving its ‘Academic and Research Excellence’ status locally and internationally. The framework developed translates the innovative themes, identified with aligned strategic objectives, into aligned action plans through the KPIs developed and geared to the individual action plans. Thus, relevant management units in Saudi universities could consider the framework developed in this study as a reference to assess their activities regarding each aligned KPI for enhancing or reforming their performance. Second, the strategy map developed based on the BSC model describes the cause-and-effect linkages of the objectives under strategic themes with action plans. The map focus reflects the direction of operational excellence in the internal processes towards stakeholder value and ‘Academic and Research Excellence’ status. The map also shows the importance of learning and growth combined with global development in educational programs to excel in internal processes and aligns these objectives with the financial objectives. Therefore, using the strategy map as a best way to capture the Saudi Universities’ strategic objectives and assess the priorities of importance for each value-creating project discovers the facets needed to be tracked and improved. Finally, through the BSC model developed in this study, it could be useful for Saudi universities to assess their academic and research status from viewpoints of internal and external customers, internal processes, learning and growth and finance perspectives in order to further enhance their performance actively.

Like other studies, this study includes some limitations. The University perceptions of BSC implementation and its expected outcomes is the main limitation. A questionnaire survey should be conducted to support the research findings with some significant results. In addition, the specific KPIs of the financial perspective related to the budgeting process are not considered in detail, especially in the BSC framework. Hence, future research should investigate BSC implementation as an integral model, taking into consideration all the detailed KPIs and action plans of the financial perspective. In other words, in addition to the interview conducted with the Deanship of Quality and Development members, other data collection sources from the relative departments should be considered to highlight the overall opinion of University staff and key personnel regarding the BSC model and how it works.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.