Abstract

M&As are inorganic growth strategies which are not only related to accounting measures of performance of firms but also affect the wealth of shareholders either positively or negatively. According to the hubris hypothesis (Roll, 1986), M&A announcements result in a decrease in the stock price of the acquiring firm, leading to a fall in its value. On the other hand, the synergy hypothesis states that the two firms merge to take advantage of economic gains that result from sharing of resources, resulting in increased returns to the shareholders of both firms. The purpose of this paper is to find out whether there is any difference in the stock price and returns before and after the announcement of M&A. Also, it has been found that Indian stock market is efficient in a semi-strong form in the event of successful merger announcements.

Introduction

Mergers and acquisitions (M&As) are the most common routes taken by corporations for inorganic growth all over the world. In fact, the last two decades have been known as the M&A waves. M&As take place when two or more companies are brought under the same effective control and are managed by the same group. It can be done in two ways: (i) acquisition of one business unit by another or (ii) creation of a new company by complete consolidation of two or more units (Rohra, 2017).

As pointed out by Rohra and Chawla (2015), M&As have always been concerned with bringing benefits including operating efficiency, financial strength and an increase in profitability of the survived firm because of more gains, reduction in expenses, reduction in earnings volatility, achievement of economy of scale and scope and increased market power as well.

Many research studies from the beginning of M&A have focused on approximately every aspect of the firm affected by such events. These issues include firm profitability, efficiency, liquidity and share performance to some extent as well. But most studies—in developing countries like India, have focused on examining the operating performance of the survived firm in the context of profitability, solvency and efficiency, etc. ‘This approach is not accurate in the economic sense because data used is based on historical figures which more likely to ignore the current market value. Other drawback is that changes in results could be due to factors other than M&A solely.’

Since the main goal of a firm is to achieve the objective of shareholder’s wealth maximisation, we must evaluate the performance of the bidding company in the stock market as well. Moreover, the studies which have focused on the impact on firm value are not comprehensive in nature and results are neither consistent nor able to generalise or to accept/reject the hubris (and synergy) hypotheses. Some studies have documented a significant increase in abnormal returns of bidding companies after the event, while others have given results consistent with hubris hypothesis. Therefore there is a need to scrutinise it more.

Besides this, most studies in emerging economies have focused only on the long-term impact on acquiring firms rather than analysing the immediate effect of M&A announcement on shareholders’ wealth. There is a need to examine the short-run effect as well; such an approach helps us to capture the immediate stock market reaction which highlights the true benefits and real economic effect due to the consolidation announcement. This can be done through technical analysis. Technical analysis is based on apparent trends in share prices, and these trends are generated as short-run phenomena not reflecting the long-term fundamentals of the company. So in this paper, through event study, we are measuring only the immediate effect/trend and not the fundamental value.

Further, by making use of panel data analysis, we have investigated the efficiency of the Indian stock market in semi-strong form in case of merger announcements (i.e. publicly available information). In an efficient market, security prices fully reflect all available information. ‘Thus, an information regarding the prospect of the company will affect the stock price to react quickly, which makes it impossible for the investors to earn excess return or abnormal return.’ On the other hand, if the market is not efficient, it will not be able to discount the event/available information; therefore there will be some kink in the price or return trend.

Thus, through this paper, we intend to study the effect of the M&A announcement on acquiring firm value in the short run and examine market efficiency. A sincere attempt has been made to capture the effect of M&A announcement on stock price and returns for the immediate time after the event has occurred. This exercise will provide useful information about the effects of M&A to the management and owners of business firms who are continuously searching for potential partners to implement mergers in the future and to the investors of stock markets as well.

This paper is organised as follows. Section 2 discusses the objectives of the study, Section 3 details the literature review, Section 4 presents the research hypotheses, Section 5 discusses the data and methodology, Section 6 presents the empirical analysis and results, and Section 7 contains conclusions.

Objectives of the Study

The main objectives of this study are to determine the impact of M&A announcements on the stock price and return of acquiring firms in the short run and to examine market efficiency for the Indian stock market in the event of M&A announcement. To put it differently, the objectives are as follows:

To find out whether there is any difference in stock price before and after M&A announcement. To find out whether there is any difference in log return in pre-announcement and post-announcement periods. To analyse if the Indian stock market is efficient in semi-strong form in the event of M&A announcements using abnormal return.

Literature Review on Announcement Effect of M&As

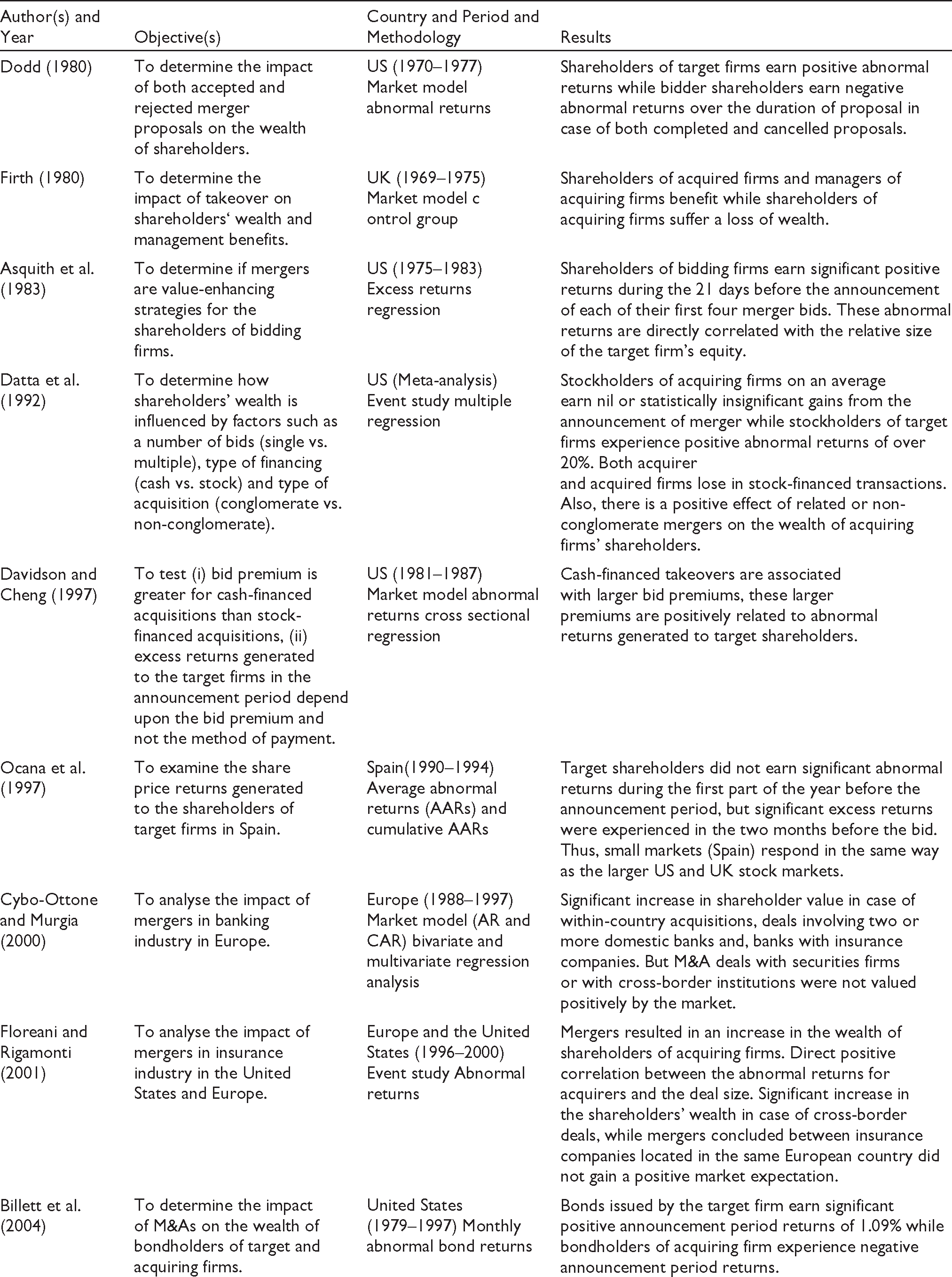

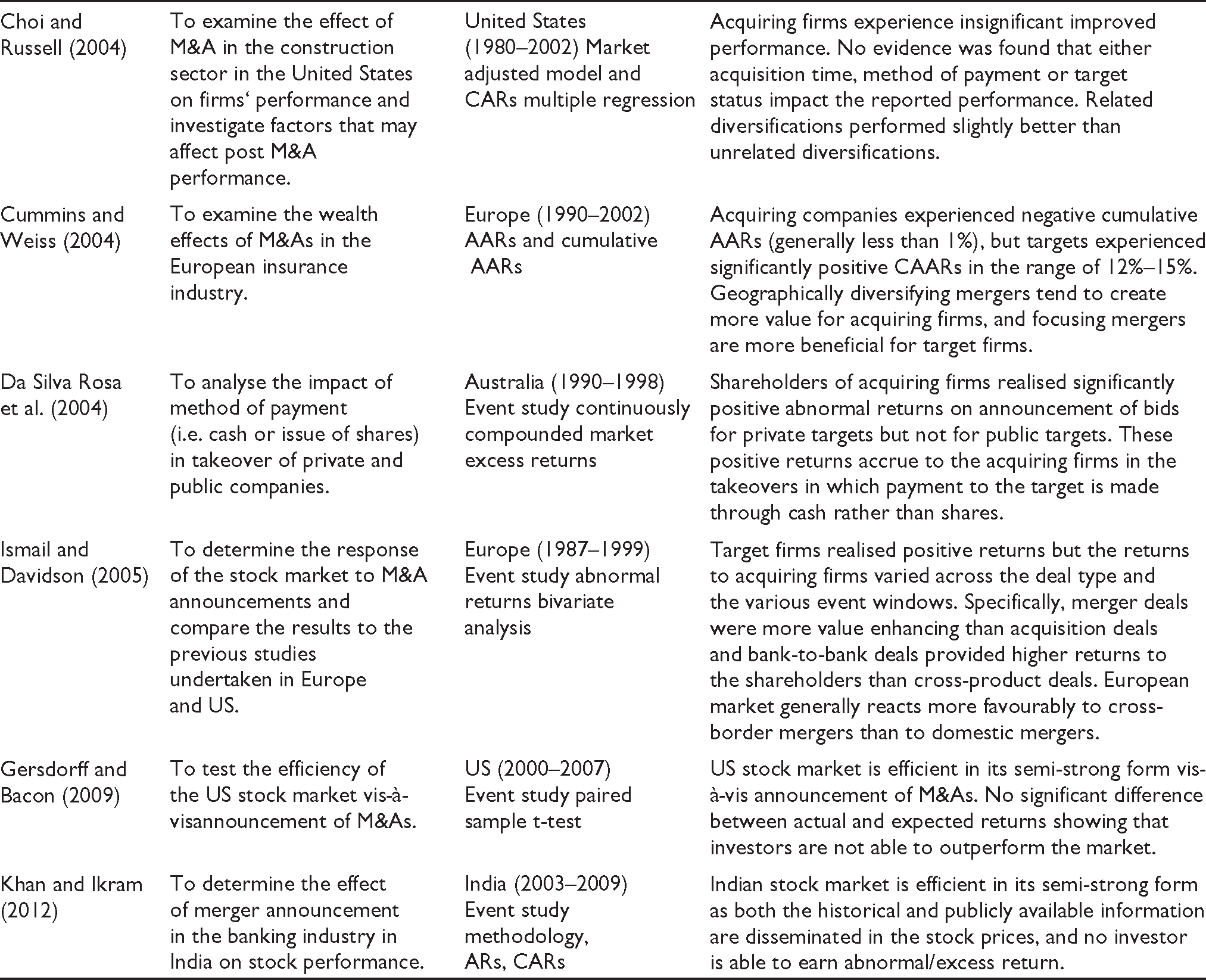

M&As are important strategic decisions that affect the profitability and wealth of shareholders of the company. Researchers, especially in developed economies such as USA and UK, have conducted numerous studies to answer the basic question: Do M&As create any value for the company and its shareholders? Studies focusing on the post-merger performance and value-creation effect of M&As usually follow either of the two general approaches: first is share price analysis—using data regarding share prices to identify gains and losses to shareholders of acquirer and target firms, and second is operating performance analysis—using accounting data to analyse long-run operating and financial performance of acquirers in a merger deal.

The studies falling under these two approaches can be further divided into three categories:

Announcement period studies, Studies focusing on long-term share price performance and Studies focusing on operating performance.

This section discusses some important announcement period studies conducted across the globe to draw a general conclusion on the impact of M&A announcements on corporate performance as well as on shareholders’ wealth.

Announcement Period Studies

Such studies follow event study methodology and consider the short-term returns earned by the shareholders surrounding the announcement period of the event. Whenever there is an announcement regarding the merger of two firms, the market adjusts rapidly to this information and this new information is incorporated into the share prices of firms. The returns generated by shareholders on the days around the announcement that are specifically due to the announcement of the event are called cumulative abnormal returns and have been studied by researchers to determine the gains or losses to the shareholders. A large number of such studies conclude that the target firms earn positive returns while shareholders of acquiring firms experience a loss of wealth. Some important studies are as follows:

Research Hypotheses

H1O: There is no significant difference in stock price before and after the merger announcement.

H11: There is a significant difference in stock price before and after the merger announcement.

H2O: There is no significant difference in log return in pre-announcement period and post-announcement period.

H21: There is a significant difference in log return in pre-announcement period and post-announcement period.

H3O: The Indian stock market is not efficient in semi-strong form in the event of M&A announcements in terms of abnormal return.

H31: The Indian stock market is efficient in semi-strong form in the event of M&A announcements in terms of abnormal return.

Data and Methodology

This section describes the data used for analysis and the various steps forming part of the methodology undertaken for examining the data.

Data

We have used daily adjusted closing stock prices of the sample acquirer companies and BSE Sensex historical prices to calculate the abnormal return around the merger announcement date from the year 2012 to 2014. Stock prices of sample companies and BSE Sensex prices have been obtained from the Yahoo Finance website ( The stock price and index price are available in Yahoo Finance. The index price and stock price of each firm are available for the duration of the event study, which is from −180 to +20 days. The stock is actively traded.

Thus, we have dropped thinly traded stocks from our sample and have included only the stocks with a high volume of trading. Since we intend to check the efficiency of the Indian stock market with respect to M&A announcements, it is better to consider only actively traded stocks listed at BSE Sensex. This is so because BSE Sensex comprises of well established, actively traded and financially sound companies, and hence it can be considered as a representative of the Indian stock market.

Based on the above criteria, Table 1 consists of the companies that have been chosen for analysis.

List of Sample Companies.

Event Study Methodology

To analyse the impact of M&A announcements on the wealth of shareholders of acquiring company, the event study method is being used. This study uses this method because it can directly measure the capital gain earned by shareholders resulting from any event of M&A.

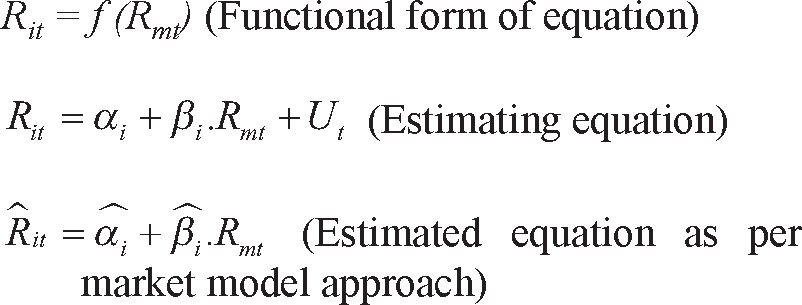

Event study is an empirical research technique that can see the effect of a particular event on a firm’s stock price. Event study uses abnormal returns over the event window to test for market efficiency. An abnormal return, which implies the difference between actual return and expected return will be positive or negative—depends on the information if the market is not efficient. In an efficient market, it is not possible to find abnormal returns because it is impossible for investors to earn excess return. There are many approaches to find an abnormal return. In this paper, we have used the statistical model of the market model. The steps of conducting event study are as follows:

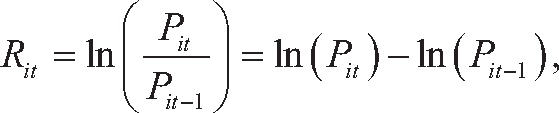

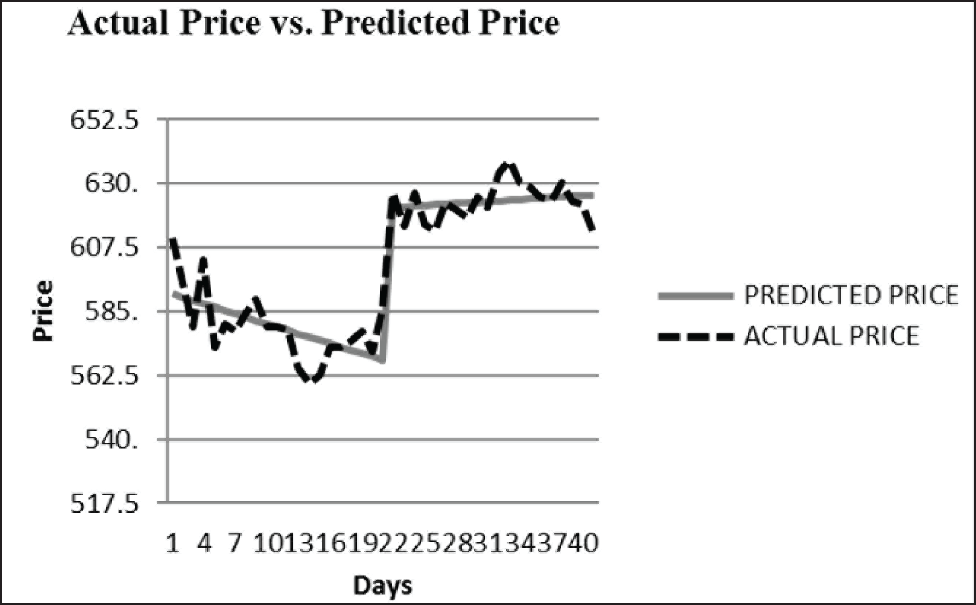

The first step is to define the event and the event window. The event in this research is announcements of successful M&A. Announcements of successful mergers are categorised as positive news which will make the stock prices to increase after the announcement. The event window in our study is 20 days prior and after the announcement day (-20 to +20). The day of the official announcement of acquisition is known as the event day, denoted as 0. Since the market model is used, there is a need to establish estimation window as well. Figure 1 depicts the timeline of event window which uses day −180 to −21 as the estimation window. Gather the daily closing adjusted historical prices of stocks and BSE Sensex from yahoo finance and calculate the daily stock log return (R) and daily market log return (Rm). The returns of each stock along the estimation and event window are calculated using the formula below:

where Rit is the log return of stock i at day t, and Pit and Pit−1 are the closing adjusted price of stock i at day t and the closing adjusted price of stock i at day t − 1, respectively. Then calculate the market return using BSE Sensex daily price. The corresponding market return is also calculated along the estimation and event window using the formula:

where Rmt is the market log return at day t, Pmt and Pmt-1 are the closing price of market index at day t and the closing price of market index at day t - 1, respectively. A regression analysis is conducted using the actual daily log return of each stock (R) as dependent variable and the corresponding daily market log return (Rm) of BSE Sensex as independent variable over the estimation window (180 days prior to the event window) to obtain the intercept—alpha and slope—beta for each stock separately. Table 2 shows alpha and beta that are used for each stock. Alpha and Beta for Each Stock.

where

Then, the abnormal return is calculated as

where

Further, we have used semi-log regression equations to test the effect of time and nature of industry on closing adjusted stock prices and actual returns. We have tried to find out in what time phase these dependent variables are significant. The time phases are, namely, pre- announcement and post-announcement.

The functional form of semi-log regression equation used (with log price as the dependent variable) is as follows:

where

β0 = Intercept for pre-announcement period β0 + β1 = Intercept for post-announcement period (provided β1 is significant) β2 = Growth rate of price for the pre-announcement period β2 + β3 = Growth rate of price for the post-announcement period (provided β3 is significant) D1 (EVENT DUMMY) = 1, if the announcement period is post announcement, otherwise 0 T = Time period (1 for day −20, 2 for day −19 … 41 for day 20) β4 = Coefficient for industry dummy ID (Industry dummy) = 0, if the industry is manufacturing, otherwise 1

So in this model, the intercepts and slopes vary with the time period—pre and post announcement. β1, that is, differential intercept coefficient gives the difference in intercepts between pre- and post-announcement period, and β3, that is, the differential slope coefficient gives the difference in slopes between the two periods.

Similarly, we have estimated a semi-log regression equation for returns. The functional form of the equation is as follows:

Where,

β0 = Intercept for pre-announcement period β0 + β1 = Intercept for post-announcement period (provided β1 is significant) β2 = Growth rate of stock return for pre-announcement period β2 + β3 = Growth rate of return for post-announcement period (provided β3 is significant) D1 (Event dummy) = 1, If announcement period is post announcement, otherwise 0 T = Time period (1 for day −20, 2 for day −19 ………. 41 for day 20) β4 = Coefficient for industry dummy ID (Industry dummy) = 0, If industry is manufacturing, otherwise 1 β5 = Coefficient for abnormal return in pre-acquisition period β5 + β6 = Coefficient for abnormal return in post-acquisition period (provided β6 is significant).

Thus, using the data for four sample companies, we have formed two regression equations for each company individually—one for price and second for returns as dependent variables. In such regression equations, we have ignored the ID variable as we are concerned with making conclusions regarding individual companies and not for the market as a whole. Also, we have compared the predicted stock price (and predicted return) obtained through regression, with the actual stock price (and actual return) during the event window by drawing line charts for the same. Such an analysis helps us to understand M&A activity undertaken by sample companies in a better way.

However, with such an analysis we cannot make any conclusion about Indian stock market trends and behaviour, that is, is the market efficient, are investors able to exploit market, what is abnormal return and change in abnormal return—all such questions cannot be answered through analysing data for sample companies individually. Therefore, we have pooled the data for sample companies, making it panel data and used a fixed-effects model. Then we have tried to observe the behaviour of the market, is the market able to absorb news, does it lead to further abnormal return or abnormal returns are ironed out etc. … All this will tell us about the nature of the Indian stock market with a sample of the four companies that we have chosen for study.

With respect to the above points, an important feature of our methodology that needs a mention is the use of generic dates. In our study, the main independent variable is time (T) but M&A event for our sample acquiring companies have taken place at different points of time. Hence instead of taking the specific dates on which these events have taken place for individual acquiring companies, we have considered generic dates (i.e. time variable (T) ranging from 1 for day −20, 2 for day −19 … to 41 for day 20 in event window), making it possible for us to pool the data and apply panel regression.

Empirical Analysis and Results

This section details the results of panel regression as well as the conclusions drawn from analysis of each individual sample acquiring company.

Panel Data Analysis

This section contains the results of panel regression using log price (Table 3) and log return (Table 4) as dependent variable one by one.

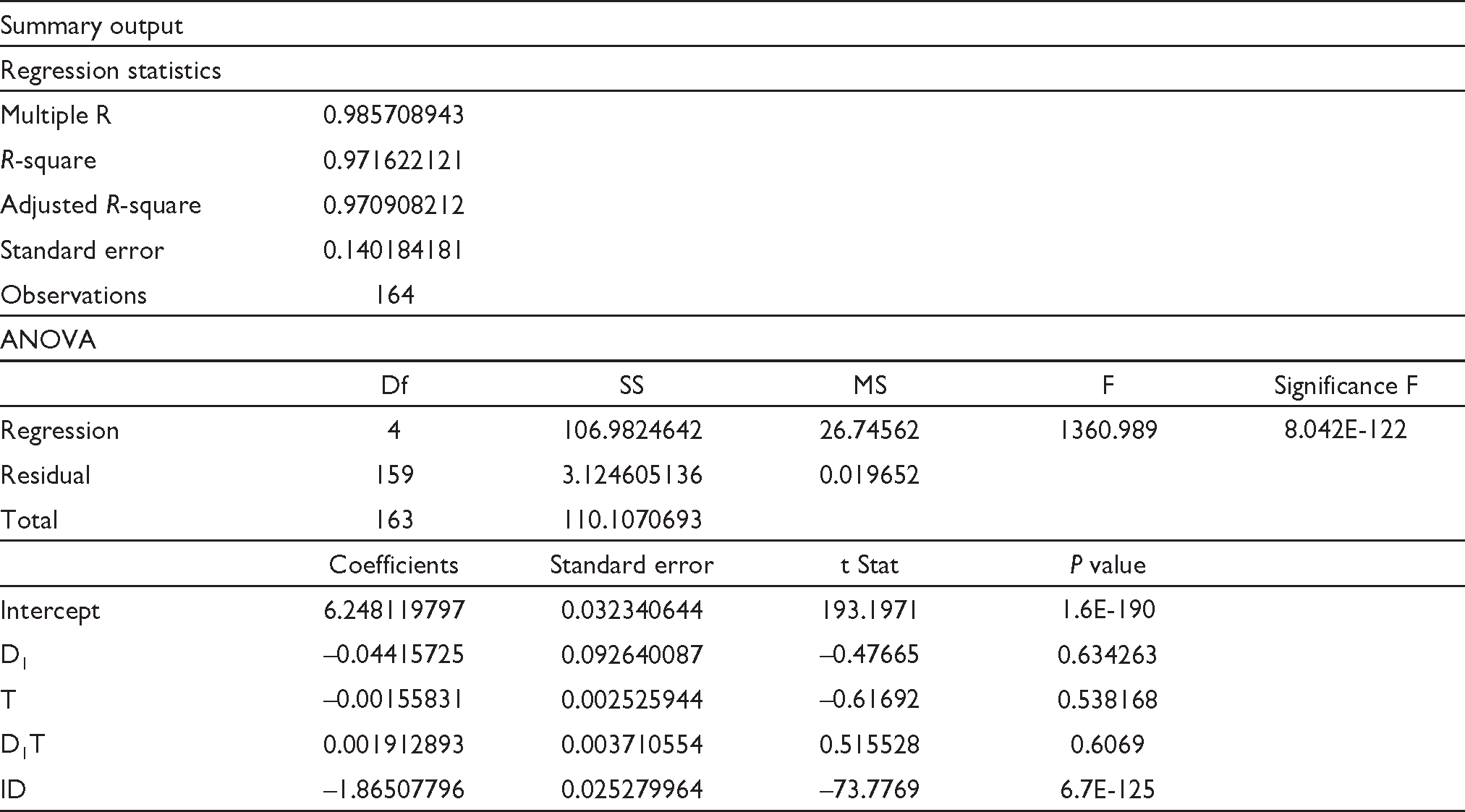

Panel Regression: Log Price.

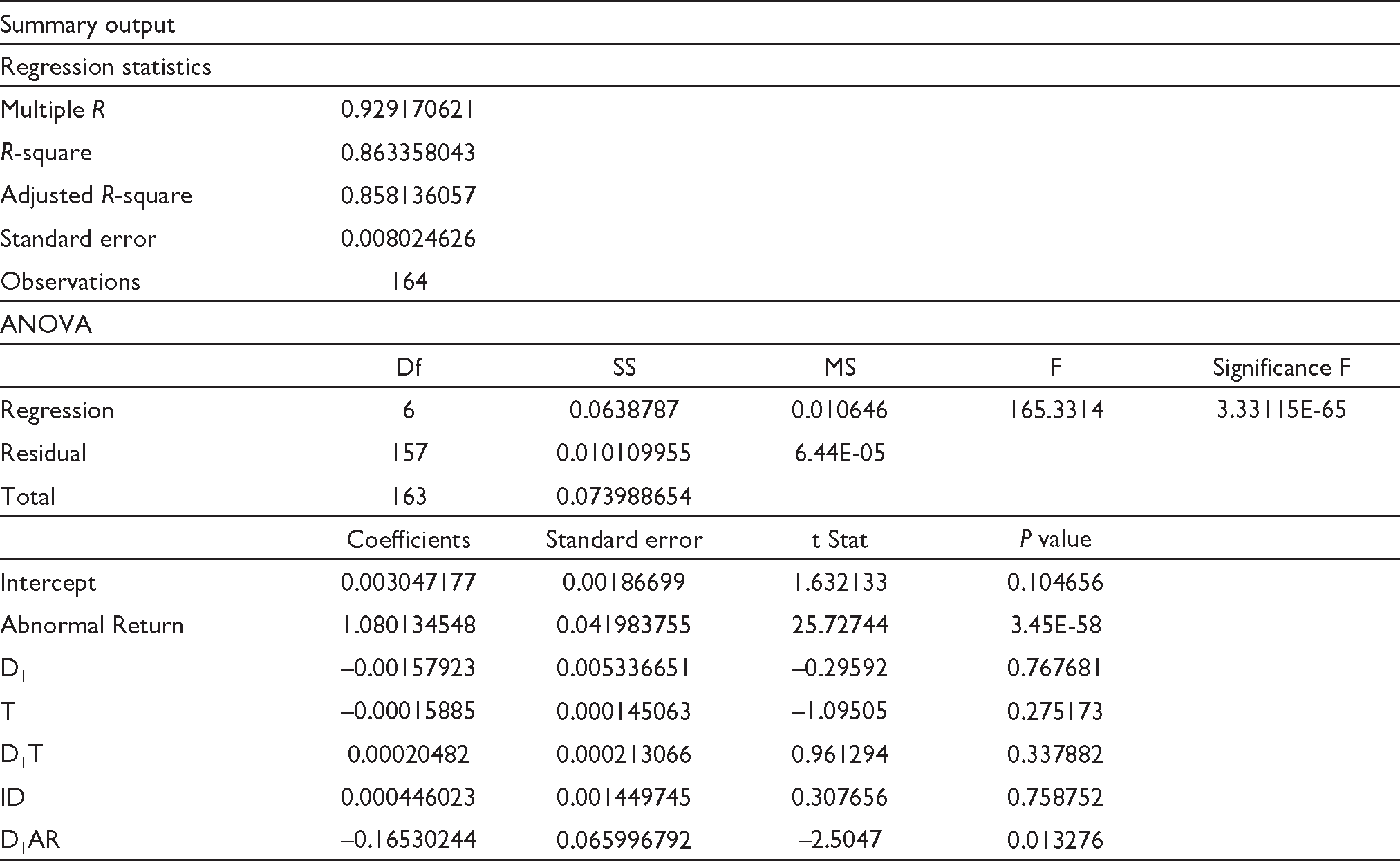

Panel Regression: Log Return.

The analysis shows us that the coefficient of ID is negative and statistically significant at the 5% level, this means that the share prices of the service industry are lower than those of the manufacturing industry. But, as such the M&A event does not have any significant impact on share price because post-acquisition, the share price falls, but the fall is not statistically significant at a 5% level, and also it is very marginal (4.41 of a per cent).

Taking a look at the coefficient for time, we can notice that the growth rate of share price for the pre-acquisition period is −0.15 of a per cent, but this fall in share price in the pre-acquisition period is not statistically significant. However, after the event, there is a slight revival in share prices; in actual terms as compared with the pre-acquisition period, the revival after the event is 0.34 of a per cent, but again this increase is not statistically significant at 5% level.

Thus, we can conclude that the Indian stock market is efficient in semi-strong form because from the sample under study, the analysis shows that the trend of stock prices is actually falling in the pre-acquisition period, but the combined effect is that post-event, the growth rate of prices starts rising; as a result net effect is 0.34 of a per cent increase in growth rate. But because this change in share prices is very low in magnitude and is not significant in terms of P value, we can only conclude that the market is efficient and it is discounting the event; the information of event is being absorbed completely in the market. Moreover, because the growth rate of prices has reversed from being negative in the pre-acquisition period to positive in the post-acquisition period, it can be said that the M&A event has been treated as good news by the investors.

The analysis shows that coefficients for all variables except abnormal return are not statistically significant at a 5% level. Starting with the intercept, we can notice that the log return was positive in pre-acquisition period, but it has become negative after the event. However, this change is not statistically significant at the 5% level.

Taking a look at the coefficient for time, we can notice that the growth rate of returns for the pre- acquisition period is −0.015 of a per cent, but this falling trend in returns in the pre-acquisition period is extremely small and not statistically significant. Therefore, it can be said that the return series is levelled. However, after the event, there is a slight revival in returns; in actual terms as compared with the pre-acquisition period, the rise after the event is 0.035 of a per cent, but again this rise is minuscule and not statistically significant at 5% level. So, return after event as such is not increasing.

The coefficient for IDis positive and extremely small (0.044 of a per cent), favouring the service industry but again it is not statistically significant.

But very surprisingly before the event, abnormal return is positive and statistically significant at 5% level, and after the event also it is still significant but it has fallen significantly by 16.53%. Thus, before event, AR was strong and significant but after the event, AR has fallen significantly. This means that there was the anticipation of the event in the market prior to the event, and after the event, there has been complete absorption of news in the market due to which AR has fallen after the event. In other words, prior to the event, investors in the market were exploiting information which was only anticipated and was not being absorbed in market and by using such information, they were able to earn extra-normal returns and hence outperform the market in the pre-acquisition period.

Individual Company Analysis

This section describes the results obtained from the analysis of stock price and return data of each sample acquiring company individually.

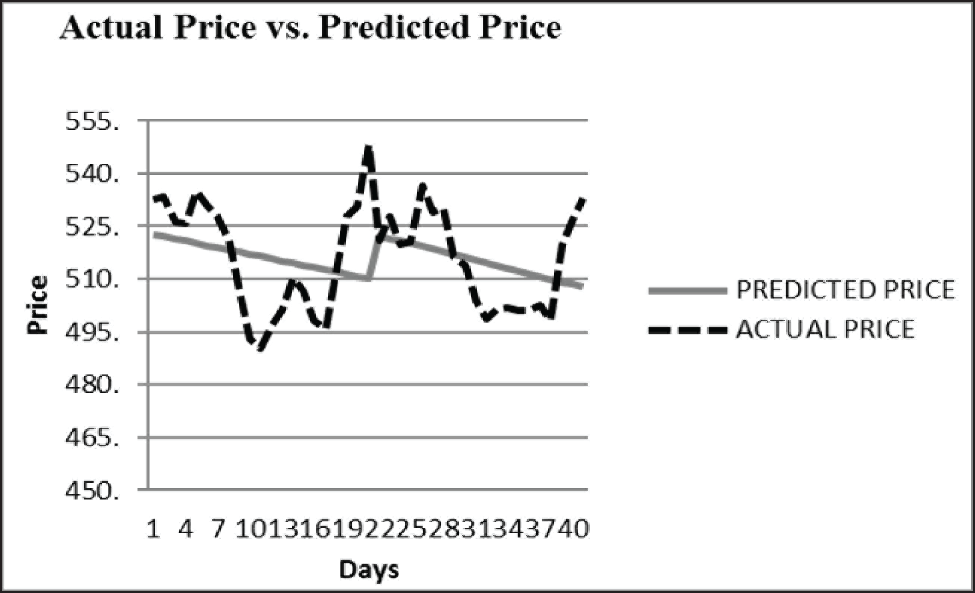

Sun Pharmaceuticals

The stock price of Sun Pharmaceuticals shows a clear trend as per Figure 1. Prior to the announcement of acquisition by the company, the stock prices have been showing a falling trend. On the announcement day, there has been a strong revival in stock prices. Thereafter, the stock price has been increasing but at decreasing rate.

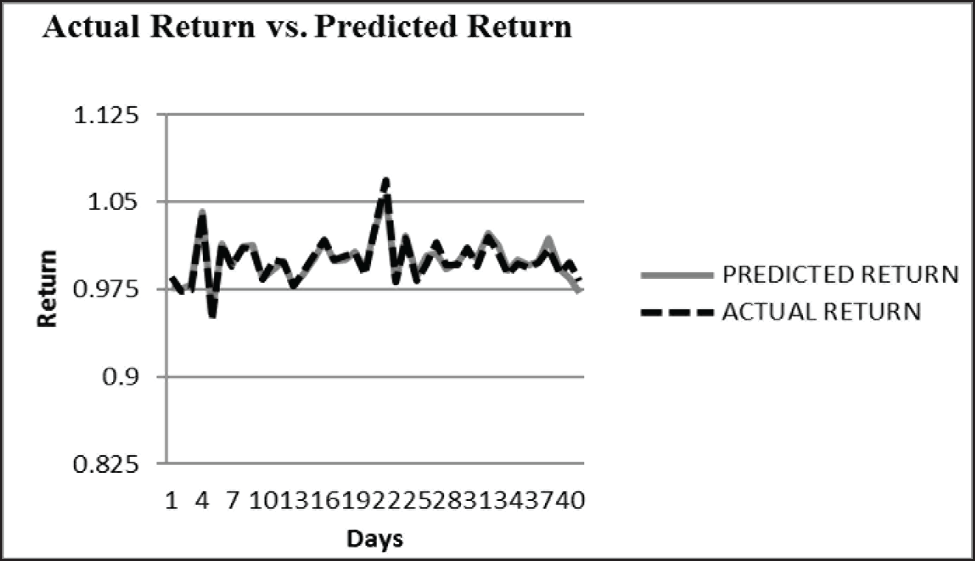

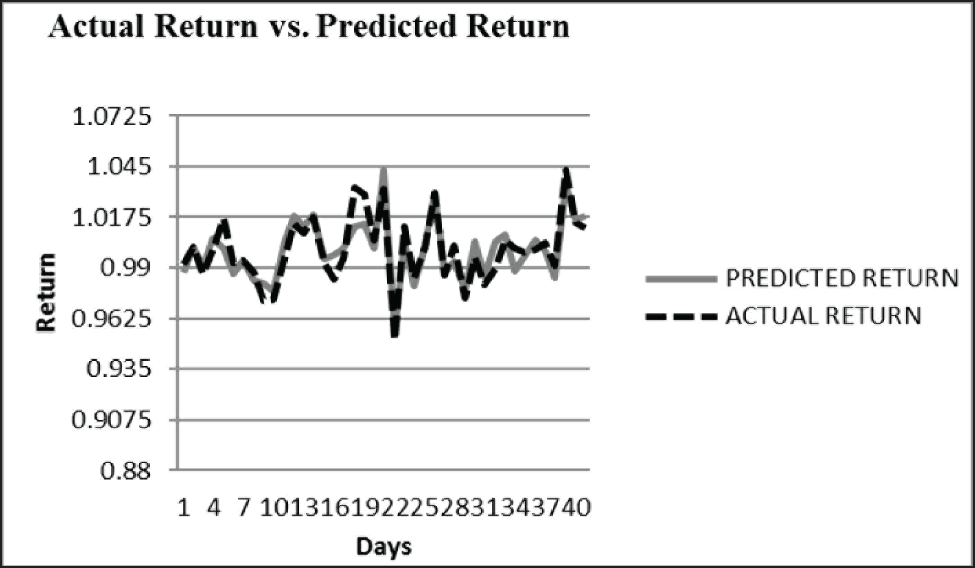

The return generated by Sun Pharmaceuticals shows a mixed trend in Figure 2. Prior to the announcement of the acquisition by the company, the return has been showing a mixed pattern. On the announcement day, there has been an increase in return. Thereafter, again the return is not showing any consistent pattern.

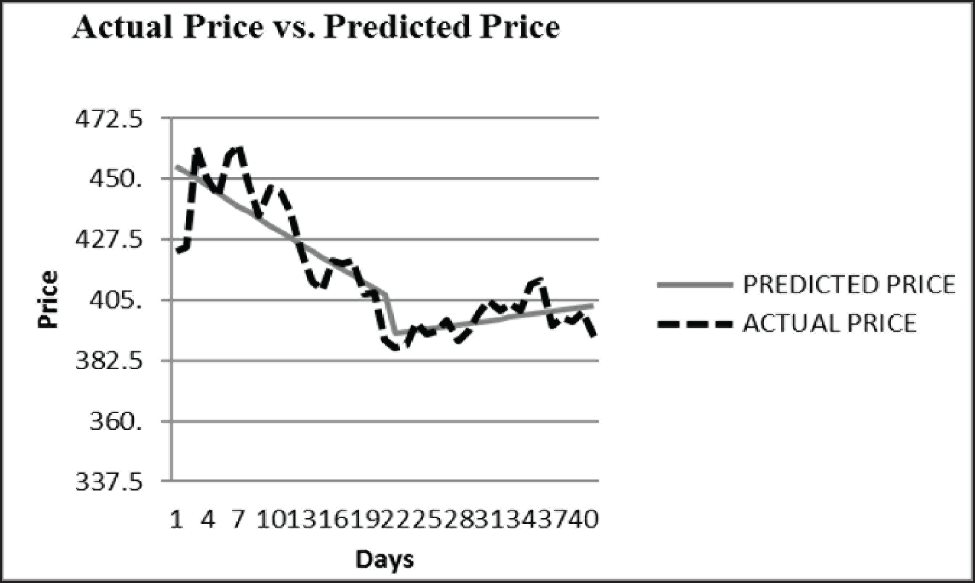

Asian Paints

The stock price of Asian Paints shows a clear trend as per Figure 3. Prior to the announcement of acquisition by the company, the stock price has been showing a falling trend. On the announcement day, there has been a strong revival in stock price. However, after the announcement again stock price has been falling.

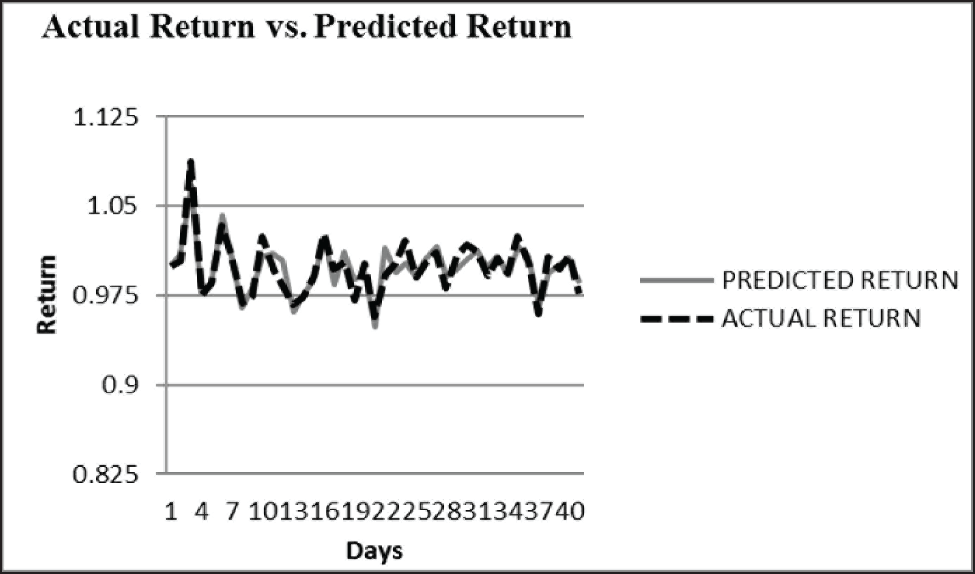

The return generated by Asian Paints shows a mixed trend in Figure 4. Prior to the announcement of acquisition by company, the return has been showing a mixed pattern. On the announcement day, there has been an increase in return. Immediately after the announcement, the return has decreased sharply. Thereafter, again the return is not showing any consistent pattern.

Jindal Steel

The stock price of Jindal Steel shows a clear trend as per Figure 5. Prior to the announcement of acquisition by the company, the stock price has been showing a falling trend. On the announcement day, there has been a decrease in stock price, which is continuing on the day next to the announcement day. Thereafter, again stock price has been increasing.

The return generated by Jindal Steel shows a mixed trend in Figure 6. Prior to the announcement of the acquisition by the company, the return has been showing no consistent pattern. On the announcement day, there has been a decrease in return. Thereafter, again the return is showing a mixed pattern.

Thomas Cook India

The stock price of Thomas Cook shows a clear trend as per Figure 7. Prior to the announcement of acquisition by the company, the stock price has been showing an increasing trend. On the announcement day, there has been a strong fall in stock price. Thereafter, again stock price has started increasing but at a minuscule rate.

The return generated by Thomas Cook shows a mixed trend in Figure 8. Prior to the announcement of acquisition by the company, the return has been showing no consistent pattern. On the announcement day, there has been a decrease in return. Thereafter, again the return is showing a mixed pattern.

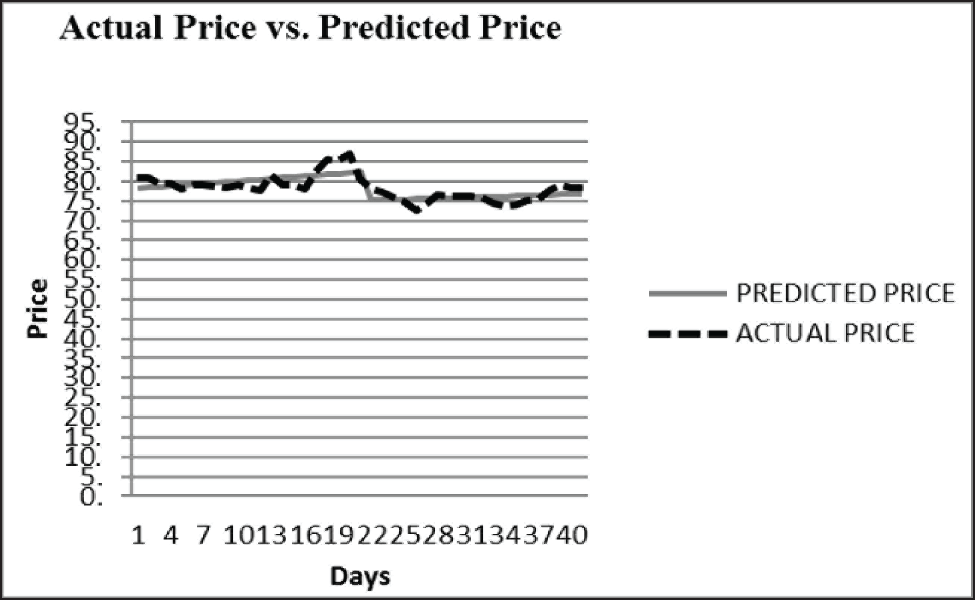

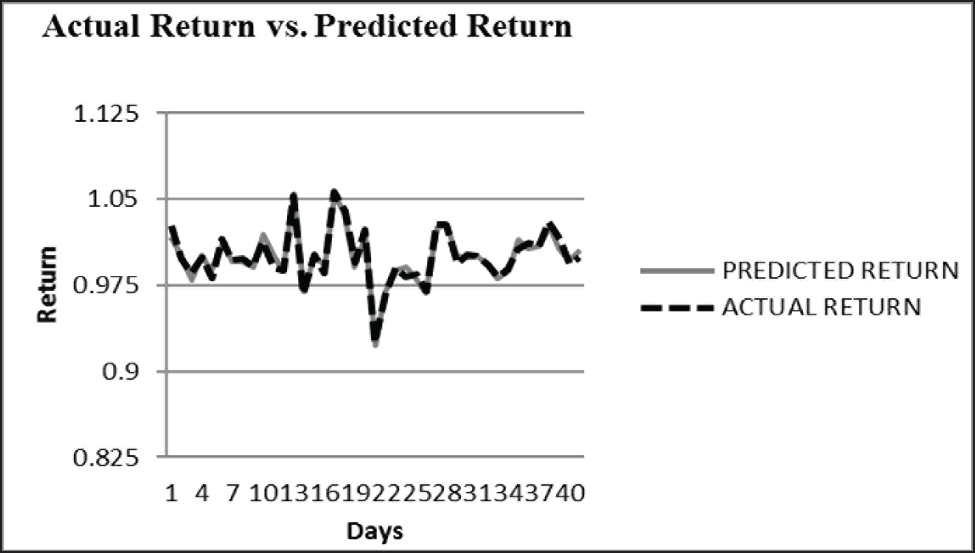

As seen for all four sample acquiring companies, the predicted values of stock price (and return) come closer to the actual values, the points on the dotted line fall closer around the black line. Because the actual stock price (and actual return) is very close to the predicted stock price (and predicted return) in the case of our four sample companies, we can say that share price and return generated by these four sample companies have not changed significantly after their respective M&A event. Moreover, the investors of none of these four companies have been able to outperform the market by investing in their respective companies.

Conclusion

The main goal of a firm is to maximise the wealth of its shareholders. In this light, an important issue in the area of corporate restructuring is to determine the effect of M&A on the wealth of shareholders of the company.

In past many researchers have tried to address this issue by using event study methodology and have documented that the shareholders of acquiring firm suffer due to the announcement of M&A by their company. However, a large number of such studies have been carried out only in developed countries so the results cannot be inferred directly without being investigated in developing economies.

This study has taken a sample of four acquiring companies listed on BSE, which made acquisition announcement during the period 2012–2014. We have chosen stocks listed on BSE Sensex because through this study we intend to test the market efficiency of Indian stock market in event of an M&A announcement. Such an objective can be well accomplished through the study of companies listed on BSE Sensex because Sensex comprises actively traded and financially sound companies, and hence it can be taken as a representative of the Indian stock market.

To capture short-run/immediate effect of M&A announcement on the stock price and shareholders return, this study has used the market model to calculate abnormal returns and involves the estimation of semi-log regression equations to test the effect of time and nature of industry on closing adjusted stock price and actual returns. We have tried to find out in what time phase these dependent variables are significant. The two time phases being pre-announcement and post-announcement periods.

The analysis shows that the trend of stock prices and log returns is actually falling in the pre-acquisition period, but the combined effect is that post-event, the growth rates of prices and returns start rising. But because these changes in share prices and returns are very low in magnitude and are not significant in terms of P value, we can conclude that the Indian stock market is efficient in semi-strong form in the case of M&A announcements. This implies that the news/information resulting from the event of the announcement of merger is fully discounted by the market. Thus, we fail to reject our null hypotheses 1 and 2, and hence we can conclude that there is no significant difference in stock price (and log return) in pre-announcement and post-announcement periods. Accordingly, we fail to make any generalised conclusion about operation of hubris and synergy hypotheses in the market for corporate control in India.

Also, we have seen that before event, AR was strong and significant but after the event, AR has fallen significantly. This means that there was anticipation of the event in the market prior to the event, and after the event, there has been complete absorption of news in the market due to which AR has fallen after the event. In other words, prior to the event, investors in market were exploiting information which was only anticipated and was not being absorbed in market and by using such information, they were able to earn extra-normal returns and hence outperform the market in the pre-acquisition period. Thus, we can reject null hypothesis 3 and conclude that the Indian stock market is efficient in semi-strong form in event of M&A announcement in terms of abnormal return.

However, we have considered only four cases of M&As and have studied the stock prices and log returns of acquiring firms (biding firms) only and not of target (acquired firms) due to data unavailability. There is a need to study a larger sample and explore in the future, the results for the acquired firm where M&A are not for 100% ownership.

Also, since M&A events for our four sample acquiring companies have taken place at different points of time, so instead of taking the specific dates on which these events have taken place, we have considered generic dates. Thus, although we have not taken actual dates, we have used generic dates for our independent variable time, making it possible for us to pool the data and apply panel regression.

Thus, a plethora of literature is available on M&As, studying the impact of such activities on the wealth of shareholders of acquiring companies. But what makes our study different from all such studies is the use of panel data analysis and log returns. While earlier studies have analysed stock prices and cumulative abnormal returns to make a conclusion about M&A events, our study is different in the sense that we are using stock prices, log returns and abnormal returns to conclude about the market efficiency of the Indian stock market through the use of panel regression.

The management of firms can use this information regarding the impact of an M&A announcement while deciding about/carrying out these corporate restructuring activities. Since takeovers do not necessarily increase the shareholders’ wealth, therefore the decision needs much scrutinisation before entering in any M&A, because the main aim of a firm is to increase shareholders’ wealth. On the other hand, investors and other stakeholders, particularly in India, may get an idea of the impact of an M&A announcement on their wealth and can act accordingly.