Abstract

In the late 2000s, the Indian market regulator made it mandatory for the listed Indian companies to have a code of conduct for the board members and the top management. However, no significant study has been done to understand the content of the code of conduct documents. This article does an exploratory analysis of the content of the listed Indian firms’ code of conduct document. We hand-collected the corporate code of ethics (CCE) documents of the top 100 listed Indian firms (excluding financial service firms) and analysed the content using a structured instrument and arrived at an index. Our analysis found that ‘conduct on behalf of the firm’ and ‘conduct against the firm’ are the parameters on which the CCE contents focused on. We found significant differences in the content CCE of Indian firms based on the controlling ownership category. However, there were no differences between the CCE content of the firms across industries.

Introduction

Corporate codes of ethics (CCE), also known as the corporate code of conduct, is an old phenomenon and gained importance when the book titled Codes of Ethics by E. Heermance (1924) was published. The researchers used different terms to refer to it; for example, Cressey and Moore (1983) referred to it as ‘code of ethics’, White and Montgomery (1980) as ‘code of conduct’, Benson (1989) as ‘corporate credo’, Schlegelmilch and Houston (1989) as ‘Code of practice’ and Murphy (1995) as ‘corporate ethics statement’.

Similarly, the definitions of the CCE are also multiple, although the underlying idea remained the same. Stevens (1994) defined CCE as ‘written documents through which corporations hope to shape employee behaviour and produce change by making explicit statements about the desired behaviour’. According to Werhane and Freeman (1998), ‘codes of conduct’ are statements of behavioural ideals, exhortations or prohibitions common to culture, religion, traditional professions, fraternal organisations, corporations and trade associations. Codes combine admonitions to avoid specific illegal actions and espouse certain moral principles, especially those that elevate personal behaviour. Kaptein and Schwartz (2008) defined a CCE as ‘a distinct and formal document containing a set of prescriptions developed by and for a company to guide present and future behaviour on multiple issues for at least its managers and employees toward each other, the company, external stakeholders, and/or society in general’.

Till the 1980s, CCE remained mostly a voluntary effort by the firms, with only a few firms adopting it. However, it changed in the late 1980s and early 1990s as the economies worldwide had reduced their control over the economy and the business corporations. Due to the reduced control, new emphasis was placed on self-regulation and social responsibility of business (Jenkins, 2001). Many firms put in efforts to prevent misconduct by their agents in a systematic way to ensure self-regulation, predominantly focusing on creating a code of conduct for top management and employees (Montoya & Richard, 1994).

The perspective of looking at CCE just as a ‘self-regulatory mechanism’ changed in the early 2000s, after a series of corporate scandals in the USA. These scandals demonstrated the need to create internal codes of conduct and apply them to the members of boards and top management to uphold the ethical behaviour and integrity of companies (Aldama, 2003). Sarbanes–Oxley Act, the US response to the corporate scandals, made it mandatory for the public firms to have a code of ethics for their board members and top managers. The market regulators in other countries have also followed suit since then, and recommended public firms to adopt ethical codes for their top management (Rodriguez-Dominguez et al., 2009). Due to the thrust given by the regulators, by mid-2010s, more than 80% of the 200 largest organisations in the world adopted a formal corporate code of conduct (Kaptein, 2017).

In line with the international practice, the Indian market regulator, Securities Exchange Board of India (SEBI), in 2005, made it mandatory for the listed Indian firms to adopt a formal code of conduct for its board members and top management. The regulatory requirements for code of conduct for the listed Indian companies are broad and flexible. Hence, there is a wide variation in the content of the code of conduct or CCE documents of the Indian firms. Some firms, like Infosys Ltd, have CCE documents running into around 50 pages with detailed code. On the other hand, some firms like Hindalco Industries have CCE documents with just four pages. This wide variation in the CCE content of listed Indian firms requires a thorough analysis, identifying the reasons for the variation. However, no significant research has been conducted on the code of conduct of Indian firms. Further, without formal research, the regulators cannot be sure whether the Indian firms took the spirit of the code of conduct requirement into account and developed them in such way that it improves the governance practices of the firm. In this article, we try to plug the research gap in this regard. We conduct an exploratory study on the content of the code of conduct document of Indian listed firms empirically and develop an index for the code of conduct for a set of sample firms and analyse them. The primary objective of this research is to study and map the content of code of conduct document of the top listed Indian firms. We want to explore the focus of the code of conduct document and study the importance given to various conduct related issues in it. Further, we also provide a roadmap to future research to analyse the relationship between the content of CCE and some selective firm parameters.

Corporate Governance in India

India was under British rule for nearly two centuries, and hence the legal system governing businesses were based on the British system. India’s corporate governance system is no exception and is based on the British common law system (La Porta et al., 1998). Even after independence, when India adopted a new Companies Act 1956, it was modelled on the English Companies Act, 1929, including the many unstructured corporate governance-related provisions (Singh et al., 2011). Indian corporate structure has a single-tier board, and the governance system focuses on the protection of shareholder rights, which are the typical characteristics of the Anglo-American Governance model (Reed, 2002). However, unlike the developed Anglo-American countries, the corporate shareholding in India is not widely dispersed.

The need for stringent formal corporate governance norms was felt after the economic liberalisation in 1991. The formal firm-level governance regulations were put in place in 2000, based on the Birla Committee recommendations. Clause 49, which dictates the corporate governance regulations, was incorporated in the listing agreement that firms sign when they get listed in the Indian stock markets (Chakrabarti et al., 2008). In 2005, SEBI amended Clause 49, based on the Narayana Murthy Committee recommendation. These corporate governance reforms in India focused on board independence, audit committee and disclosures. The modified Clause 49 also made it mandatory for the listed Indian firms to have a code of conduct for the board of directors and senior management and disclose the same on the company website. It also required the board members and senior management personnel to affirm compliance with the code on an annual basis. The regulation defined the senior management personnel as the members of the firm’s management/operating council (i.e., core management team excluding board of directors). The regulation also required the company’s CEO to make a declaration regarding annual compliance in the annual report.

The new Companies Act 2013 gave further imputes to the governance regulations for the public companies. Subsequently, in 2015, SEBI modified the corporate governance norms to be followed by the listed firms by introducing ‘Listing Obligations and Disclosure Requirements (LODR)’. The code of conduct regulations remained the same in LODR, except that it required the document to incorporate the duties of independent directors as laid down in the Companies Act, 2013, as deemed fit. In 2018, SEBI updated governance regulations based on the recommendations of the Uday Kotak Committee. However, the code of conduct regulations for the board of directors and top management remained unchanged.

Literature Survey

Though the CCE is an old phenomenon, significant academic research started only in the 1970s. The initial studies focused on exploring the content of CCE documents using structured instruments, mostly in the US context (Sanderson & Varner, 1984; White & Montgomery, 1980). Cressey and Moore (1983), for example, examined the CCE document contents of 119 US corporations under three categories: (a) policy area—the specific issues addressed in the code, (b) authority—’precepts, trends or principles that make a code’s policies seem ethical, morally necessary or legitimate’ and (c) compliance procedures —those methods ‘specified for monitoring, enforcing, sanctioning or otherwise ensuring compliance with a code’s provisions’. Mathews (1988) grouped the content of CCE of the US firms into 64 categories under 10 major areas: conduct on behalf of and against the organisation, integrity of books and records, basis, reference to specific laws and government agencies, compliance or enforcement practices, penalties for non-compliance and corporate reputation. This instrument was widely adopted by many other studies later.

The 1990s saw the research works focusing on other countries as well. For example, Lebfebvre and Singh (1992), Snell and Herndon (2000) and Brytting (1997) studied the CCE of top Canadian, Hong Kong and Swedish companies, respectively. Most of these initial studies were exploratory, highlighting the firms’ CCE contents in the respective countries. Country-level comparative studies started emerging in the late 1990s. Lefebvre and Singh (1996) compared the content of CCEs of Canadian and American companies, while Farrel and Cobbin (1996) examined and compared codes in Australian and US companies. Wood et al. (2019) found that even in the two historically linked and culturally related countries, namely, the UK and Australia, there were differences in the firms’ CCE content. Overall, the studies on cross-country comparisons of CCE indicated that national differences in ethical beliefs and values were reflected in the content of codes employed by corporations (Arnold et al., 2007).

Few other studies focused on specific industries. For example, Emmelhainz and Adams (1999) examined CCEs in companies in the apparel industry, where sweatshop labour was a concern. Van-Tulder and Kolk (2001) studied the CCEs of multinational companies (MNCs) in the sporting goods industry. Their study found that different sourcing strategies, degrees of multinationalism and national backgrounds affect the CCE contents. Focusing on multinational firms and code of ethics, Helin and Sandstrom (2008) argued that the parent company imposing universal code on the subsidiaries located in other countries would be met with resistance and suggested that uniform implementation process of the code across cultures, rather than the content of CCE, is important.

In the late 1990s, CCE studies began to focus on the influence of the codes on the managers’ behaviour. McCabe et al. (1996) found that while CCEs are associated with reduced unethical behaviour in business organisations, they also reduced self-reporting of unethical behaviour by the employees. Hence, this study suggested that the nature of the code, management’s commitment to its implementation, and the degree to which the code becomes embedded in the organisation’s standard operations are crucial factors to make the code effective in reducing unethical behaviour.

Some studies focused on the process of developing CCE for firms. Raiborn and Payne (1990) argued that corporations need to consider their fiduciary responsibilities while developing the CCE. They suggested that the underlying qualitative characteristics of code should include clarity, comprehensiveness and enforceability, and the CCE should reflect the corporate culture. Schwartz (2005) prepared a normative framework for developing a corporate code of ethics, by identifying six universal moral values which can act as the foundation. It is also essential to focus on what makes the code effective while developing them. Singh et al. (2018) identified the determinants of the effectiveness of CCE by studying the firms from Australia, Canada and Sweden. Their analysis found that four factors related to the corporation’s internal management were positively correlated to executives’ perceptions of the effectiveness of the codes of ethics.

The ethical value system of the firm has close implications for its corporate governance practices and vice versa (Bonn & Fisher, 2005). Hence, the corporate code of ethics is a tool for corporate governance and corporations have instituted CCE stating their publicly mandated commitment to corporate governance (Adelstein & Clegg, 2016). Hence, another stream of studies focused on the link between board and CCE. Rodriguez-Dominguez et al. (2009) studied the influence of independence and the presence of female members on the board in promoting and hindering the creation of a code of ethics. Furlotti and Mazza (2020) confirmed the close association between board governance and CCE as their study found that the board of directors’ independence is positively related to code of ethics policies related to communication with employees.

Till the early 2000s, the studies on CCE focused on the developed countries as the establishment and use of codes of ethics by corporations had become mainstream across there (Erwin, 2011). In the 2010s, the researchers started focusing on the CCE of the firms from emerging markets as well. For example, Saygili and Öztürkoğlu (2017) and Roberts-Lombard et al. (2019) studied the CCE of Turkish and South African firms, respectively.

Although India is an important emerging market, only a few studies have analysed the CCE of firms in the Indian context. Elankumaran (2006) studied the CCE of top Indian corporations, at that time, adopting and disclosing the CCE was not mandatory in India, hence only 32 corporations agreed to share their CCE. This study indicated that most Indian codes, except that of Tata group companies, are nowhere close to ‘an ideal code’. Lefebvre (2011) compared the cross-cultural aspects of business ethics in India and the USA by studying the CCE contents of the top 50 companies in both countries, using the instrument developed by O’Dwyer and Madden (2006). The hierarchical and collectivist nature of the Indian culture versus the all-encompassing and individualistic nature of the US culture was reflected in their findings.

Except for the two studies mentioned above, there seem to be no studies worth referring to in the Indian context. Given the limited literature available in the field of code of ethics in the Indian context, in this article, we conduct an exploratory study of the content of the code ethics documents of listed Indian firms.

Methodology

We considered the top 100 listed Indian firms (excluding financial services firms) based on market capitalisation as of 31st March 2018 as our sample. We excluded financial services firms, as their CCE documents are influenced by the requirements of the Reserve Bank of India, the Central Bank, along with that of SEBI. We hand-collected the CCE documents, known as ‘code of conduct’ document in the Indian regulatory context, from the sample firms’ websites on 31st March 2018.

We used a structured instrument to analyse the content of the CCE documents of Indian firms. Cressey and Moore (1983), one of the oldest studies on CCE, developed a structured questionnaire for examining the content of the CCE documents of the sample firms. The questionnaire focused on the criteria like policy area, authority and compliance procedures. Based on the Cressey and Moore instrument, Mathews (1987) examined the content of the CCE document along three broad categories: (a) the behaviour and actions which are discussed in the code, (b) the enforcement procedures, and (c) the penalties associated with illegal behaviours. The contents of the codes are also analysed along 64 additional groupings. Lefebvre and Singh (1992) used the 64 groupings and classified them in 10 categories and prepared an instrument/questionnaire to query the content of CCE documents in their study. We use same instrument that Lefebvre and Singh (1992) used but modified it to suit the Indian legal and regulatory system. As indicated earlier. this instrument was widely used in multiple studies on CCE content. To explore the content, the instrument groups the potential content of CCE documents into 10 categories. Then it queries the presence/ discussion about various items/issues in each category. There are 65 specific queries in total, across the 10 categories. The 10 categories and the number of queries in each category are as given below.

Conduct on behalf of the firm 14 queries

Conduct Against the firm 8 queries

Laws cited 9 queries.

Government Agencies referred to 3 queries.

Compliance/reinforcement procedures -

Internal -Oversight 7 queries

Compliance/reinforcement procedures -

Internal –personal integrity 7 queries

Compliance/reinforcement procedures -

External 4 queries

Penalties for illegal behaviour –Internal 5 queries

Penalties for illegal behaviour –External 2 queries

6 queries

For content analysis using the instrument, the given firm’s CCE document were checked for the presence of these 65 items/issues, based on the respective query. Depending on the presence and the importance given, the scores were assigned for each of the issue/item. The instrument identifies four levels of scoring for each of the items, as explained below.

Not discussed: the issue is not addressed by the CCE of the organization– 0 points given

Discussed: the CCE discusses the issue in one or two short sentences–1 point given

Discussed in detail: the issue is reviewed in more than two sentences, and up to one full paragraph or two short paragraphs–2 points given

Emphasised; the CCE addresses the item in two or more full paragraphs–3 points

We, the authors, independently read through each sample firm’s CCE document and checked for each of the 65 items in the sample firms’ CCE documents and assigned scores for each of the 10 categories individually. We have also calculated the total scores. Ideally, the scores given by both the authors for each item for every firm should be the same, given the standard criteria. Hence, the scores given by both the authors were compared, and in case of any discrepancy, the content of that CCE is taken for analysis once again, and the discrepancy is resolved. For each of the 100 firms, the points were totalled for each of the 10 categories and overall total, that is, CCE Index. Higher the CCE index of the firm, the better the content of the code of conduct document.

Analysis and Discussion

Among the sample firms, based on our instrument, Infosys Ltd gets the maximum total score of 126. While the minimum total-score is 13, the mean is 58.66 for the sample firms. Among the 10 categories in the CCE instrument, ‘conduct on behalf of the firm’ category gets the maximum focus in the CCE documents. It examines the activities that reflect the top management’s behaviour in the marketplace in the name of the company. This category has the maximum number of queries (14) among all categories as well. The sample companies got an average score of 20.6 out of a maximum possible 42. This trend is in line with other global studies. Across the studies, conduct on behalf of the firm is the category that gets the maximum attention (Wood et al., 2019). Given the increased awareness among the corporate stakeholders about their rights and the tightening laws to protect their interests, the companies want to ensure the top management’s appropriate behaviour on its behalf.

The second most important item among the 10 categories is ‘Conduct against the firm’, which examines the activities that the employees engage in and occur in the marketplace against the company’s best interests. It is important as the company wants to protect itself from the unethical behaviour of employees. The sample companies got an average score of 11.44 out of a maximum possible 24.

Among the 10 categories, the sample companies’ CCE focussed least on the item ‘External penalties’ with an average score of 0.61 (maximum six). The descriptive statistics of the parameters are given in Table 1.

Descriptive Statistics.

Next, we analyse all 10 individual categories individually to understand the content of the CCE.

Analysis of CCE Content

Conduct on behalf of the firm: Among the 14 items for this parameter, three items, namely ‘relations with employees, ‘accepting bribes’ and ‘conflict of interest for top management’ had an average score of ‘2’ (out of 3). The other items, like relations with home government, relations with customers, relations with business partners, relations with investors, civic and community affairs, and environmental affairs, had an average score between 1.4 and1.6. On the other hand, ‘product safety’, ‘product quality’, relations with a foreign government and ‘payments to government officials’ are the items with an average score of less than one. This indicates that the companies are not yet concerned much about product-related issues in the Indian context though they care about relations with the customers.

Conduct against the company: Among the nine items for this parameter, only one item, ‘Insider Trading’ had an average score of two. It is because ‘Insider Trading’ regulations of SEBI require the listed firms to have a detailed policy to prevent unlawful insider trading by the company’s top management. Six other items, namely ‘divulging trading information’, personal character matters, divulging trade secrets/proprietary info, integrity of books and records, legal responsibility and ethical responsibility of top management, had an average score between one and two. The last item ‘other conduct against the firm’ had an average score of 0.75.

Laws cited: The CCE of Indian listed firms seldom quote the Indian laws in their contents as none of them has an average of more than ‘one’. The Competition act, Securities act and Labour act are those laws that had an average score between 0.9 and 1.0. The other items, namely, Environment acts, Food and drug-related acts, Consumer protection act, Corruption laws, Marketing and advertisement laws, and Other general laws, had an average score of less than 0.85. The past studies indicate that discussion on laws in the CCE is important as the top management needs to be aware of the laws that concern them. Any lapse in this regard might cause severe damage to the reputation of the firm. And that is one of the main reasons why this category has got nine queries, second highest among all categories. However, Indian firms are not yet focusing on this category.

Government agencies: For this parameter, the instrument looked in for three items: ‘competition commission’, National Company Law Tribunal’ and ‘other agencies’. However, very few companies discussed the government agencies in their CCE. The average score was less than 0.5 (out of 3). This could be because the government agencies are just evolving in the Indian context in the last decade, replacing the older ones, and firms are yet to understand them fully.

Compliance/reinforcement procedures—Internal oversight: This is about the internal oversight for ensuring compliance with the rules and policies of the organisation as well as the general laws. Out of the seven possible internal oversight procedures, there is only one, ‘Internal Audit’, (average score of 0.74) that finds significant reference in the CCE of Indian firms. All other internal oversight procedures, namely, supervisor surveillance, internal watchdog committee, read and understand affidavit, routine financial, budgetary review, legal department review and other oversight procedures, did not find any significant reference with an average score of less than 0.5 (out of 3). This could probably be because only the ‘Internal Audit’ has legal standing in the Indian context, and the rest of the oversight mechanisms depends on firm-level policies.

Compliance/reinforcement procedures—Internal oversight—Personal integrity: There were seven items related to internal oversight procedures based on personal integrity. They have relatively better references in the CCE of Indian firms than the oversight procedures in the previous category. Supervisor (average score 0.63), compliance affidavits (0.66), employee integrity (1.42), and senior management role models (0.98) were the important items covered in the CCE. The other items, namely, internal watchdog committee, corporation’s legal counsel and others (within the firm), had less than 0.5 as their average score. This suggests that companies trust personal integrity rather than procedure-based oversight to ensure that employees comply with ethical policies.

Compliance/reinforcement procedures—External: There were four possible external compliance procedures that this instrument looked for in the CCE: Independent Auditors, Law Enforcements, Codes mentioning enforcement or compliance procedure, and other external compliances. Among them, ‘codes mentioning enforcement or compliance procedure’ had the highest average (0.77) followed by Law Enforcements (0.66). The other two items had less than 0.5 average scores. Overall, the external compliance procedures are not given importance in the CCE than the internal oversight procedures. It indicates that the companies generally do not prefer external courses of action for non-compliance, as it may force the company to reveal more about internal issues to the external stakeholders.

Penalties for illegal behaviour—Internal: There were five items in this category, of which only one item, that is, the threat of demotion, was prominently found in the CCE with an average score of 1.67. The other four items, namely, reprimand, fine, dismissal/firing and other internal penalties, have seldom been discussed with an average score of less than 0.7. We believe that this reflects the rigid and complex labour laws in India, which makes it difficult for the firms to mention the potential action against employees, which include the top management personnel.

Penalties for illegal behaviour—External: Both the items in this parameter, namely,; egal prosecution and other external penalties, had a score of less than 0.5, in average, indicating that they did not find any significant reference in the CCE.

General information: This parameter focuses on the company’s general expectations from the CCE, focusing on items like ‘need for corporate reputation’, introductory remarks from the Chairman/CEO, code specific to a country, vision and mission, equal opportunity, and others. Five items out of the six had an average score from 1.0 to 1.45, indicating equal importance. The sixth item, ‘code specific to which country (home country/world/general others)’ had an average of 0.83. It is because not all the companies in our sample have operations outside India, and hence, they did not specifically mention which country these codes focus on.

Content of CCE and Firm Ownership

Next, we analyse whether the ownership of the firm has any influence on the content of the CCE. Most of the Indian listed non-financial firms have a controlling shareholder, designated as ‘Promoters’. Indian Companies Act, 2013 defines ‘promoters’ as the persons whose name appears on the face of the prospectus, who controls the affairs of the company or according to whose directions the members of the board of directors are accustomed to work. Further, most of the Indian firms also belong to family-owned business groups. These two phenomena in the firm ownership structure have an impact on the governance practices of the firms. Varma (1997) pointed out that the governance issues differ across listed Indian firms based on the firm’s dominant (controlling) shareholder. Similarly, Bertrand, Mehta and Mullainathan (2002) pointed out the complicated ownership structures of group-affiliated firms facilitate tunnelling, thereby making the corporate governance problems severe, compared to the standalone firms. To understand this, we studied whether the type of controlling-owner group influence the CCE score for various items differ across firms. Bang et al. (2017) classified the controlling owners of the listed Indian firms into six categories. However, we considered only four categories of controlling-ownerships, namely, family business groups (FBG), standalone family firms (SFF), state-owned enterprises (SOE), and MNCs. We ignore the categories non-FBG and standalone non-family firms as there are only two and one in numbers for the respective categories in our sample.

Given that this is a pioneering study in this field in the Indian context, we are unsure about the determinants of CCE contents. Hence, we could not run sophisticated econometric tools like regression analysis. We chose a simple single-factor ANOVA test to understand the significance of the difference between the scores of firms across different controlling-owner categories.

Table 2 indicates that the subsidiaries of MNCs had better scores in most of the parameters and the overall score. It is because the MNCs are mostly from developed Western nations and have well-developed standards for CCE. Their global subsidiaries simply adopt them with minor modifications to suit the local legal requirements. The Indian subsidiaries of the MNC are also adopting the same approach. We checked the CCE of the MNC parents of the Indian subsidiaries in our sample and found that CCE documents of Indian subsidiaries have borrowed around 70%–80% of the content, mainly ‘Conduct on behalf of the firm’ and ‘Conduct against the firm’ from their MNC parent CCE.

Content of CCE and Firm Ownership Single-factor ANOVA Test.

Another interesting observation was that the SOEs scored the highest average for all the internal parameters, namely, internal oversight, internal personal integrity and internal penalties. However, the differences were not statistically significant. This, we believe, reflects the bureaucratic culture with lots of internal controls that prevails in the SOEs (Kanungo et al., 2001) with stringent disclosure norms (Asthana & Dutt, 2013).

The firms belonging to FBG scored better than in SFF in overall score (p value in t-test is significant) and in many other parameters, mainly ‘conduct on behalf of firm’. The difference could be because the business groups firms learn from the experience of sister group firms and improve upon their code of conduct. Some business groups have a standard code of conduct for all group companies. For example, India’s largest business group, Tata Group, in 1998, come out with the ‘Tata Code of Conduct’ and all the Tata group companies subscribed to it (Maheshwari & Ganesh 2006). We found that the legal CCE document of the listed Tata firms borrows liberally from the Tata Code of Conduct.

While the above analysis provides primary evidence to support the argument that the CCE document differs based on the controlling ownership and group affiliation of listed Indian firms, it needs to be studied further in detail.

Content of CCE and Industry

Next, we analysed the differences across the firms across the industry. Beasley et al. (2000) has pointed out that corporate governance problems differ across the firms based on their industry. Further, the capital, regulatory and competitive requirements also vary across the industries. To understand the industry level differences, we classified the firms in our sample based on NIC’s two-digit Industry classification. The firms in the sample fall into nine categories of industries, and one firm is classified as diversified. Of the nine industries, ‘Manufacturing’ alone accounts for 67 firms, distantly followed by ‘Communication’ with 11 firms (Table 3).

For our analysis, we considered only the industries with a minimum of five firms in our sample. Hence, we considered the firms from only four industries for our analysis: manufacturing, information, construction and electricity (Table 4).

Sample Firm Industries.

Content of CCE and Industry.

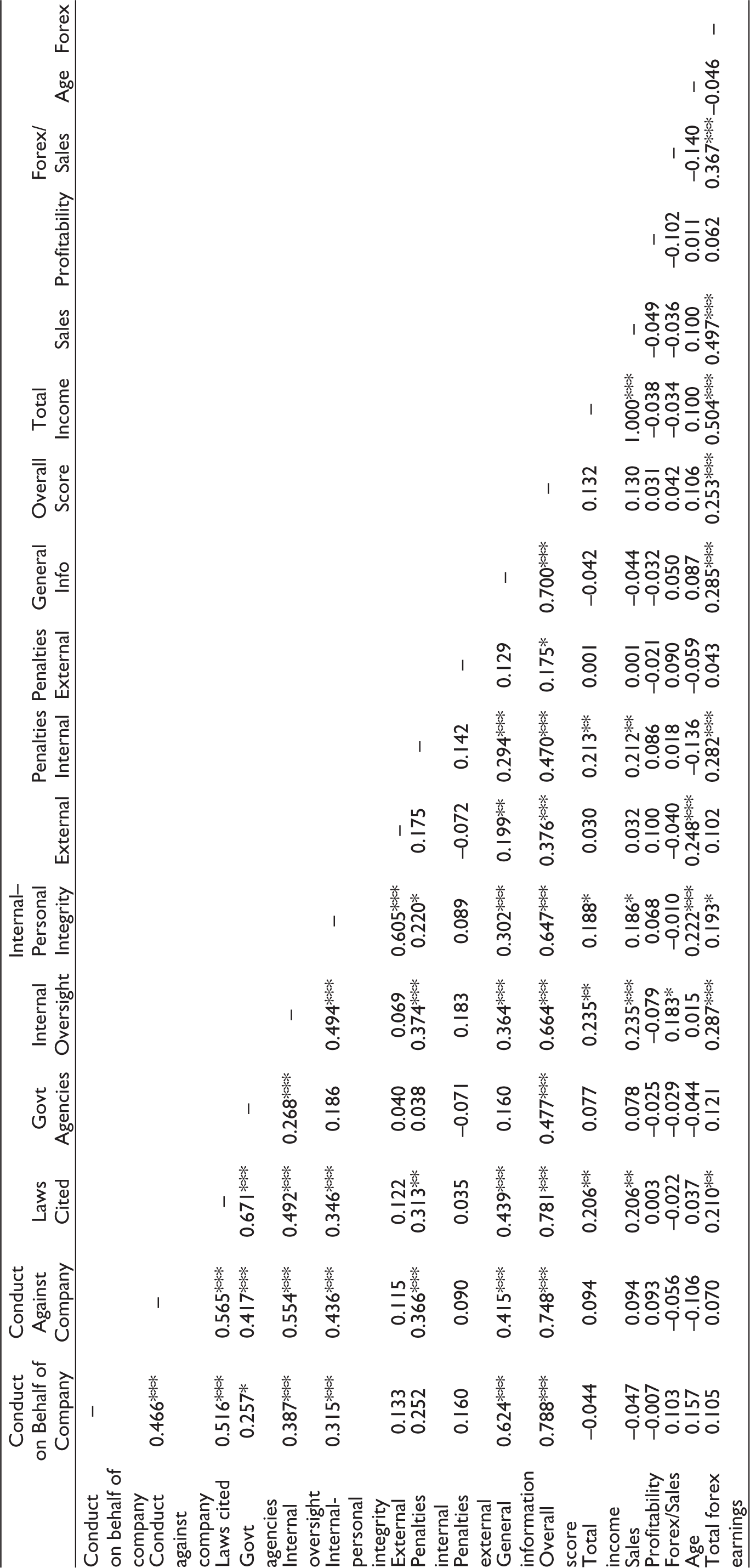

Correlation Matrix (Pearson’s r).

The means of various parameter scores of CCE are different across the four sectors. Particularly the mean of Section D (Electricity and Gas) and Section F (Construction) sector firms had a high overall score compared to the other two. It could probably be because these two sectors are highly regulated in the Indian context, and hence the firms put up more content in the CCE to avoid serious problems. However, the single factor ANOVA test suggested no significant difference between the mean of parameters across the four industries. Still, this issue requires further analysis as the sample size in Section D (Electricity and Gas) and Section F are very low. Hence, the above results do not provide conclusive evidence to conclude that the content of CCE document differs across the industries for listed Indian firms. However, it needs to be studied further in detail.

Content of CCE and Firm Parameters

The past research works (Subramanian & Reddy, 2012) on corporate governance have indicated that firm-level parameters such as firm size, age and forex revenue have a significant influence on the firm’s corporate governance practices. Next, we analysed the CCE scores based on the age of the sample firms. We chose the simple correlation analysis to understand the relationship as the causality if not known. The analysis indicated a very low correlation (0.106) between age and the overall CCE score.

We also tested the relationship between the overall CCE score of the sample firms and the firm level parameters: firm sales, total revenue, foreign exchange revenue through correlation analysis. However, the correlation coefficients were low and insignificant. Given the exploratory nature of our study, we did a simple correlation analysis for testing the relationship. It is insufficient to provide conclusive evidence that the CCE document differs based on firm-level parameters in Indian listed firms.

Conclusion

Vedic based Indian ethos and value systems are unique and have a history of more than 2000 years with a strong foundation (Chakraboty, 1995). The firms from such a country tend primarily to draw on indigenous cultural values and practices to develop corporate strategies and management practices (Viswesvaran & Deshpande, 1996). Despite that, the academic literature on business ethics is limited in the Indian context. One such topic with limited academic research is the corporate code of ethics, known as the code of conduct in the Indian context.

CCE was a voluntary and self-regulatory measure to enforce expected ethical behaviour among the top management. However, in the early 2000s, the regulators across economies have made it mandatory for the listed companies to have a formal corporate code of ethics and linked it to impose better governance practices. SEBI made it mandatory for the Indian listed firms to adopt a code of conduct for the board of directors and top management in 2005. As a pioneering study, in this article, we conducted an exploratory analysis of the CCE content of top listed Indian companies. We used a structured instrument that classified the CCE content into 10 parameters. Our analysis found that ‘conduct on behalf of the firm’ and ‘conduct against the firm’ were the parameters on which the CCE contents focused on. We found significant differences in the content CCE of Indian firms based on the controlling ownership category. We also found that the listed Indian subsidiaries of MNCs cover much more than the rest in their CCE content. However, there were no differences between the CCE content of the firms across industries. Similarly, the CCE content did not correlate with firm age, Sales, and profitability.

This article has conducted only an exploratory analysis, mapping a broad picture of the content of CCE and hence all the limitations of the exploratory studies are applicable to this study as well. However, by doing a simple analysis of the relationship between CCE contents and ownership, industry and firm parameters, the article opens up multiple new research avenues.

The future research could focus on the relationship between CCE and corporate culture. Given the well-established unique Indian culture, research can focus on how far it is reflected in the CCE documents of the Indian firms compared to other countries with the British legal system background. The research works can also study the firm level and business group level culture and its relationship to the content of CCE document within India. Another stream of research can focus on the relationship between firm-level corporate governance and CCE document. CCE document is an important corporate governance mechanism and hence it is expected to be influenced by board composition and structure. So, the research works can explore the relationship between board characterises of the firm and their CCE content. One can also study to what extent the content of CCE influences the behaviour of the top management by analysing the relationship between CCE content of the firms and legal cases against them by various stakeholders.

From the regulatory perspective also, the article opens up new avenues for fine-tuning the corporate governance regulations. A detailed research on industry level differences in the content of CCE documents of the firms would provide light on differential regulatory requirements to govern the CCE content. The study provides managerial implications as well. Given that the listed family-owned firms are increasingly hiring professional managers at top management level, they need to have a well-defined CCE document to reduce promoter-manager (Principal-Agent) conflicts. Hence a detailed study comparing family-owned firms with professional managers and the owner-manager firms would provide more insights into it.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.