Abstract

This study examines attitudes, actions, and willingness of rural residents to sign up for and pay for health insurance. It explores national health programs, statistical assessments of health insurance in rural populations, and responses to rural communities' attitudes and behaviors towards health insurance. Access to quality healthcare is a basic human right, but rural residents face increasing challenges due to rising healthcare costs. Health insurance can help address these issues. However, awareness, perception, and behavior related to health insurance are still limited among rural residents. Barriers such as high delivery costs and lack of awareness hinder insurance adoption in rural areas. Education on the importance of health insurance and providing financial stability for major illnesses and hospitalization are crucial. This study aims to evaluate rural residents' perceptions, actions, and willingness to sign up for and pay for health insurance, alongside analyzing national health programs and schemes.

Keywords

Introduction

Health Insurance Medical assistance, often referred to as health policy, is a kind of insurance that can be used to pay for an individual’s medical expenditure in case of an illness, accident or emergency. In India, health insurance has lately gained popularity as a way of financing healthcare. Health insurance coverage in India is generally low, and individuals are not benefitting from economic input attributable to failures at several stages. The rural population is equally, if not more, exposed to the same threats as the urban population due to their socioeconomic situation. Health insurance may assist in removing financial constraints and providing better access to high-quality treatment.

Health insurance and technology advancement in technology, for example, e-health and wearables, when utilised by insurance firms, could aid in keeping track of the rising population, number of patients with chronic diseases and number of people receiving geriatric care. The role of the insurer involves keeping an eye on these above-mentioned factors whilst keeping the people healthier and at the same time protected (Silvello & Procaccini, 2019). To ensure that more and more people are covered by and benefit from health insurance, different technological solutions can be utilised.

Wearables and e-health can collect data and assess risk in a shorter span of time as compared to complete medical examinations, which can be time consuming (Litke, 2022). They can help in the early prediction and detection of chronic diseases and the management of the risks associated with these diseases. This can, in turn, help in reducing early deaths.

In places where the distribution of large sets of data is needed among decentralised infrastructures for implementation of healthcare insurance policies, blockchain technology-based applications are gaining momentum as they allow people and medical insurance organisations to come to a mutual conclusion or agreement (Chondrogiannis et al., 2022).

The inclusion of these high-tech devices in the insurance sector helps in risk selection, reduces fraudulent intentions and provides value-added services to the clients. It also allows the medical insurance company to be more proactive in their approach and makes the whole process quicker and more effective. These ensure that the insurance companies take a part in their customers’ health journey than just collecting premiums.

Concept of connected insurance is based around the idea of the adoption of new technology that benefits both the insurers and the insured. It not only makes the health insurance industry more efficient; it also incorporates the latest Internet of Things (IoT) technologies. Connected insurance acts as a medium of connection between all parties (the insurers, clients and other players). It helps in reducing the overall expenditure and personalises the experience of the clients.

The aim of integrating technology with healthcare insurance is to provide convenience and service optimisation to all sectors of society. However, practically, services using technology are still not optimal, especially for people who are economically constrained (Andria et al., 2021). Therefore, technology-intervening solutions must be suggested and adopted to serve the society at large (Pandey & Litoriya, 2020). Health scenario in rural India and coverage of medical insurance on a global level are recognized as strategic priorities to make sure that people do not suffer when in need of quality medical treatments (Hogan et al., 2022). We must shift away from reliance on out-of-pocket payments and towards a medical insurance policy. The following are the reasons: Direct medical expenditures are an impediment to access to quality healthcare. Massive medical expenses can push people into bankruptcy, but people who are medically insured can receive the necessary care without any fear of economic distress, according to Sharma et al. (2022).

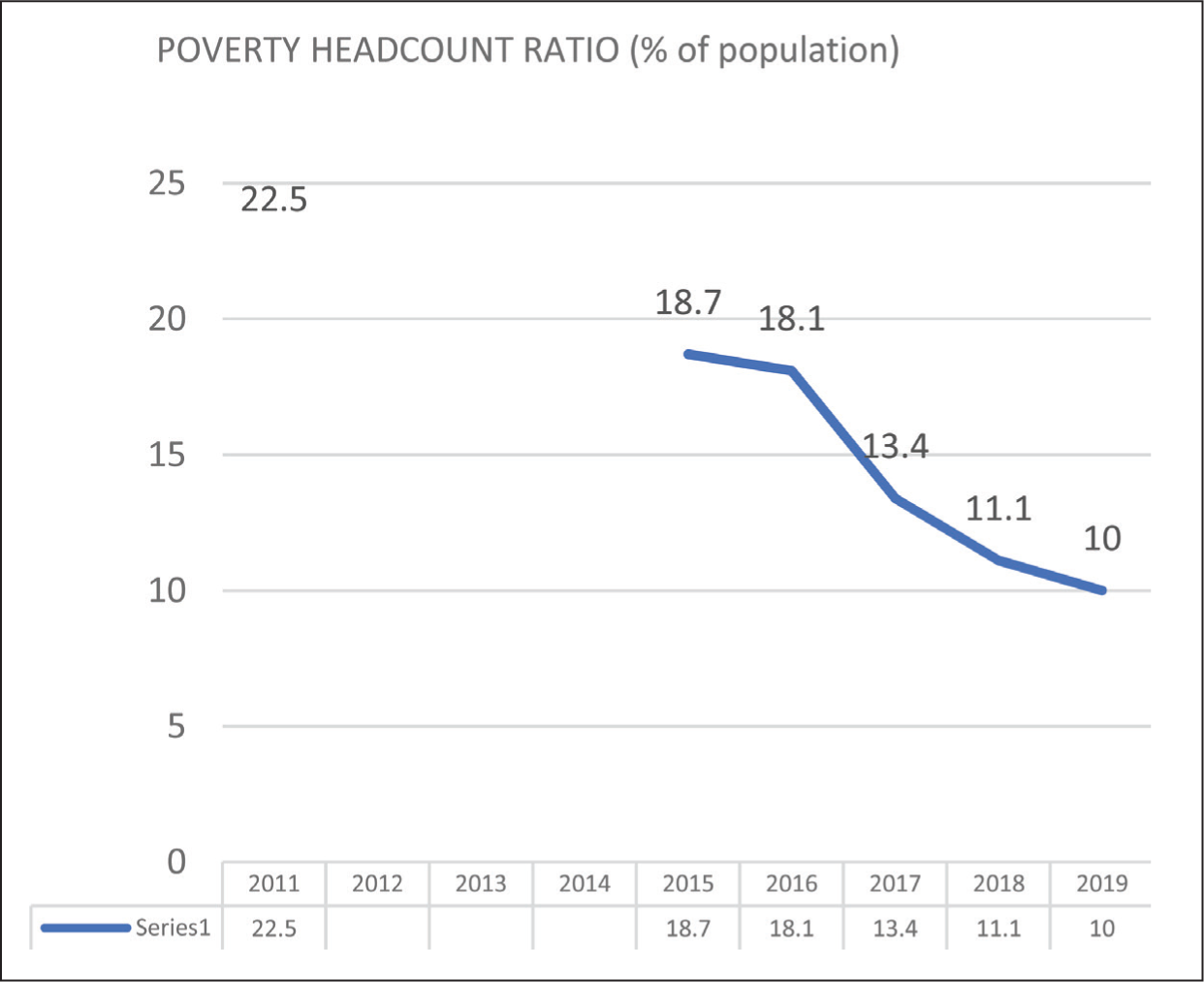

The poverty headcount ratio is defined as the number of persons who live on less than $2.15 per day in 2022 global prices. In 2022, according to the World Bank’s poverty headcount ratio, 10% of the Indian population is impoverished as a result of medical expenses received during hospitalisation (Figure 1). Health insurance alleviates the worry of obtaining funds during illness. Direct out-of-pocket expenses are unjust since they harm the person who needs financial assistance at the time of illness and do not allow people to participate in their own treatment.

Shows Poverty Headcount Ratio at $2.15 a Day (India).

In India, a larger share is spent on account of pharmaceuticals as compared to hospitalisations. Healthcare spending accounts for 1.15% of total GDP, according to the most recent budget. With such low healthcare spending in a densely populated country like India, people are forced to seek out more expensive alternatives. The private sector is unaffordable. With the private sector accounting for 72% of health expenditure and treating 78% of outpatients and 60% of inpatients, India today boasts a privatised health system.

While health insurance has a long history, the increase in coverage dimensions may be explained by the number of government activities and programmes developed to enhance health insurance awareness among the poor.

Recognising the need to provide people with social security, the Central Government launched the Rashtriya Swasthya Bima Yojana in 2008. Rashtriya Swasthya Bima Yojana (RSBY): The Ministry of Labour and Employment created RSBY to offer health coverage for people who fall below the poverty line. The aim of this scheme is safeguard the low-income communities from financial obligations induced by medical emergencies that demand hospitalisation. Eligibility for the scheme would help BPL employees in the unorganised sector and their families (a maximum of five members). The beneficiary is entitled to medical insurance coverage as defined by the government in accordance with population requirements. Funding pattern of the central government provides 75% of the anticipated annual premium. The central government will pay for the smart card.

Delivery of service list of hospitals to choose from is to be provided to the patient while availing this scheme. Based on the qualifying requirements, the insurance provider will empanel the hospitals. The beneficiary is free to choose the hospitals where they will be treated. The hospital might not charge anything for providing health care for up to ₹30,000/. A biometric smart card is given to each recipient family. All RSBY-affiliated hospitals are linked to district-level servers to ensure that information regarding service consumption flows smoothly.

Our research contributes to the corpus of information in India regarding the impact of health coverage on financial risk mitigation in poor families. According to this research, greater health insurance coverage has enhanced the utilisation of health services; nevertheless, the effects on financial risk protection are unclear and tend to be context-dependent, particularly for poor beneficiaries. When people living below the poverty line encounter a medical emergency, they either settle for subpar healthcare or lose loved ones because they lack the financial resources to receive the appropriate treatment at the appropriate time. The Government of India has created many health insurance policies for the poorer parts of society in order to guarantee medical coverage for BPL households.

To gauge the attitudes, behaviours and willingness of rural inhabitants to sign up for and pay for health insurance, several steps can be taken. First, conducting a survey can help better understand the beliefs and practices of rural population around health insurance. This survey can assist in identifying both the characteristics that discourage enrolment and the ones that encourage it, which can help inform strategies to increase participation. Second, it is crucial to participate in dialogue with local authorities and groups in rural regions to inform them of the value of health insurance and the advantages of signing up for a plan. This can increase awareness and understanding of the benefits of health insurance and encourage more people to sign up. Third, increasing the knowledge of health insurance alternatives among rural healthcare practitioners can enable them to better assist their patients in choosing a plan that suits their needs. Finally, it is essential to provide encouragement or subsidies to low-income rural inhabitants to assist them in paying for their health insurance rates. By taking these steps, it is possible to increase their access to healthcare services.

Gaining knowledge about national health initiatives, policies and programmes requires taking multiple steps. One such step is to use government websites, news stories and other pertinent sources to stay informed about modifications and updates to these policies and initiatives. This can help provide a comprehensive understanding of the national health landscape and any changes that may be occurring. Another effective method is to attend healthcare advocacy-related events like conferences and seminars to learn more about national health policies and programmes. These events bring together experts, stakeholders and policymakers to discuss the latest developments and share insights into the current state of healthcare. Additionally, joining organisations that support access to high-quality healthcare can help individuals stay updated about national health policies and initiatives and advocate for such policies. By following these steps, one can stay well-informed about national health initiatives, policies and programmes and contribute to efforts to improve access to high-quality healthcare for all.

A statistical analysis of low-income households’ access to health insurance requires a systematic approach. The first step is to examine the statistical analysis in order to comprehend the important conclusions and the methods applied. This can help in understanding the data presented and assessing the validity of the analysis. Next, it is important to note any restrictions or potential biases in the analysis that could affect the interpretation of the results. It is also essential to analyse the results in light of the greater healthcare environment and any pertinent economic or policy considerations. Finally, utilising the data to guide campaigning and policy initiatives focused on boosting low-income families’ access to health insurance can help to address any disparities or challenges identified by the analysis. By following these steps, one can gain valuable insights into low-income families’ access to health insurance and use this information to inform effective policy and advocacy efforts.

Objective

This article aims to achieve three objectives that will enhance our understanding of health insurance access among rural and low-income households.

First, the project seeks to analyse the beliefs and actions of the rural population towards health insurance, specifically their willingness to enrol and pay for coverage. This analysis will provide insights into the factors that influence health insurance enrolment and identify the barriers to access.

Second, the project aims to examine the national health programmes, strategies and plans that are currently in place to give the population access to healthcare and health insurance. This will help identify gaps in the current programmes and suggest areas for improvement.

Thirdly, the project aims to identify the obstacles that hinder low-income households from obtaining medical insurance by conducting a statistical study of the availability of health insurance.

This study will highlight the specific challenges faced by low-income households and suggest interventions to improve access. Overall, these studies will provide a comprehensive understanding of health insurance access among rural and low-income households.

Literature Review

A study by Zuhair et al. (2022) focuses on medical insurance concerns among people in rural areas. Grounded theory was employed to gather and analyse data. Concerns about administration, architecture, financial support for medical services, awareness, orientation and meaningful engagement are a few of the challenges that have been noticed. According to the findings, poor governance was characterised by low perceptions of the quality of medical treatment and administrative challenges. While creating insurance plans, it is crucial to take into account these concerns and consumer preferences in order to raise participation rates for medical insurance. Qin investigated the pattern of risky actions that resulted in the depletion of medical insurance funds. The information was obtained from official websites, and networking site analysis was used to visualise systemic risk actions and discover statistical configurations that result in monetary loss. The soaring reliant framework of pragmatism was state healthcare organisations, which, in accordance with the comparative report’s results, had reduced financial troubles and very little state intervention, whereas the increasing provisional agreement of worrisome adventurism had incredible stress, almost no state intervention and elevated infringement levels (Haque et al. 2023; Qin et al., 2022).

Pillai et al. (2022) conducted a cross-sectional investigation examining patient experience, demand and public opinion of cooperative medical insurance in a chosen region. A total of 295 people from the city of Tumakuru contributed the information that was compiled. It was found that 58.3% of the population knew about the Yeshasvini CHI scheme, 2.7% knew about RSBY, 1.3% knew about Vajpayee Arogyasree and 37.6% knew about other community medical insurance programmes. Among the 113 participants who used the personal setup, 57.5% expressed satisfaction; however, only 47.8% of the 182 participants who used the government setup expressed satisfaction. According to the report’s findings, Tumakuru residents are sufficiently aware of the issue. A 2018 study by Navarrete et al. (2022) examined the effect of healthcare coverage on providing economic protection against hazards. Those with healthcare coverage were shown to have a 15% lower likelihood of having unfulfilled healthcare needs. According to their research, the advantages associated with health coverage depend on how close one is to essential health services.

A total of 210 individuals from three districts of Kerala participated in Joy et al.’s (2021) research on medical insurance literacy and client satisfaction. After the analysis was conducted, it was discovered that the nature of the insurance industry and the policies it offered had a substantial impact on the degree of client satisfaction. The mindset and views regarding the introduction of e-government in the administration of healthcare insurance were examined by Hammouri et al. (2021) and Bhatnagar et al. (2023). This study analyses research on Jordanian residents’ ability to obtain medical insurance coverage. A total of 315 people’s information was analysed, and inferences were derived. The results demonstrated that the government should concentrate on the platform’s applicability to entice people to utilise the digital medical insurance administrative structure and use social networking sites actively to raise knowledge of the platform’s importance. In the context of minor health insurance enterprises in India, Nayak et al. (2021) developed an organisational societal benefit paradigm by integrating concepts related to the social orientation of enterprises and competitive edge. They created this approach using structural equation modelling. A total of 565 individuals’ opinions about several facets of medical insurance were assessed. Results reached indicated that elements such as technological development, creativity and information management techniques greatly impacted the relative advantage of enterprises.

The advantages and uses of blockchain technology in areas like the health insurance business have been investigated by Kurni and Mrunalini et al. (2021) and Upreti et al. (2023). These technology-based health coverage programmes are being created on a daily basis and have the potential to offer transparency and responsibility while protecting customer information. Insurance companies and people covered by insurance will both benefit from these by saving time and money. Garedew et al. (2020) tried to ascertain whether residents of rural communities in select Jimma zone areas would be inclined to cover their medical expenses. The goal of Emmanuel et al.’s (2019) research was to identify the factors that influence decision-making to register in health insurance policies. A total of 464 people were surveyed in 14 distinct Ugandan villages for the dataset. After that, techniques like regression analysis (logistic and zero-inflated negative binomial) were used to identify the variables influencing how many people register in community-based Medicare Advantage plans. According to the findings, socioeconomic position, awareness of medical coverage and occupational status were all powerful determinants of enrolment. According to Dinh-Le et al. (2022), electronic medical records have been implemented in healthcare institutions recently to improve the collection of patient records. This study outlines the challenges of data confidentiality, data saturation and network compatibility while focusing on the incorporation of Electronic Health Records (EHRs) and wearables in various healthcare settings (health insurance firms, enterprises and health institutions). Many healthcare organisations, like Overlap, Royal Philips, Human APU and others, have begun integrating patient records into portals.

According to a study by Patil et al. (2022), insurance firms can adapt to rapidly evolving client requirements, competitors’ movements and compliance standards with the use of strategic flexibility. This study concentrates on how having health coverage among rural dwellers might reduce their economic strain during difficult times. In order to achieve optimum coverage, this study also discusses the current situation of healthcare insurance in India, technological advancements in this field, government-sponsored programmes, as well as the difficulties encountered. The goal of Spender et al. (2022) was to integrate wearables and the IoT into health care and life insurance sector. The variety of these items presents both opportunities and difficulties for the medical field. The possibilities and depth of information that wearable devices may supply in the medical insurance sector are the subject of this research. The fate of insurance is also explored, along with risks, problems and upcoming technological advancements. Ramesh (2022) examined the health coverage for the underprivileged in India and talked about the numerous health insurance programmes that have been launched for those who are struggling financially. Seno’s (2022) article outlines the critical steps that can significantly increase the acceptance and usefulness of such health insurance programmes for efficiently managing people’s health.

Research Methodology

A closed-ended questionnaire was used to collect data on the characteristics of the study population and their perspective on medical insurance.

The purpose of this survey is to learn what people think about health insurance in rural regions.

The survey was completed using paper and pen. The participants were asked to check the boxes next to the numbers and ranges that applied to them.

There were 20 questions on the survey form.

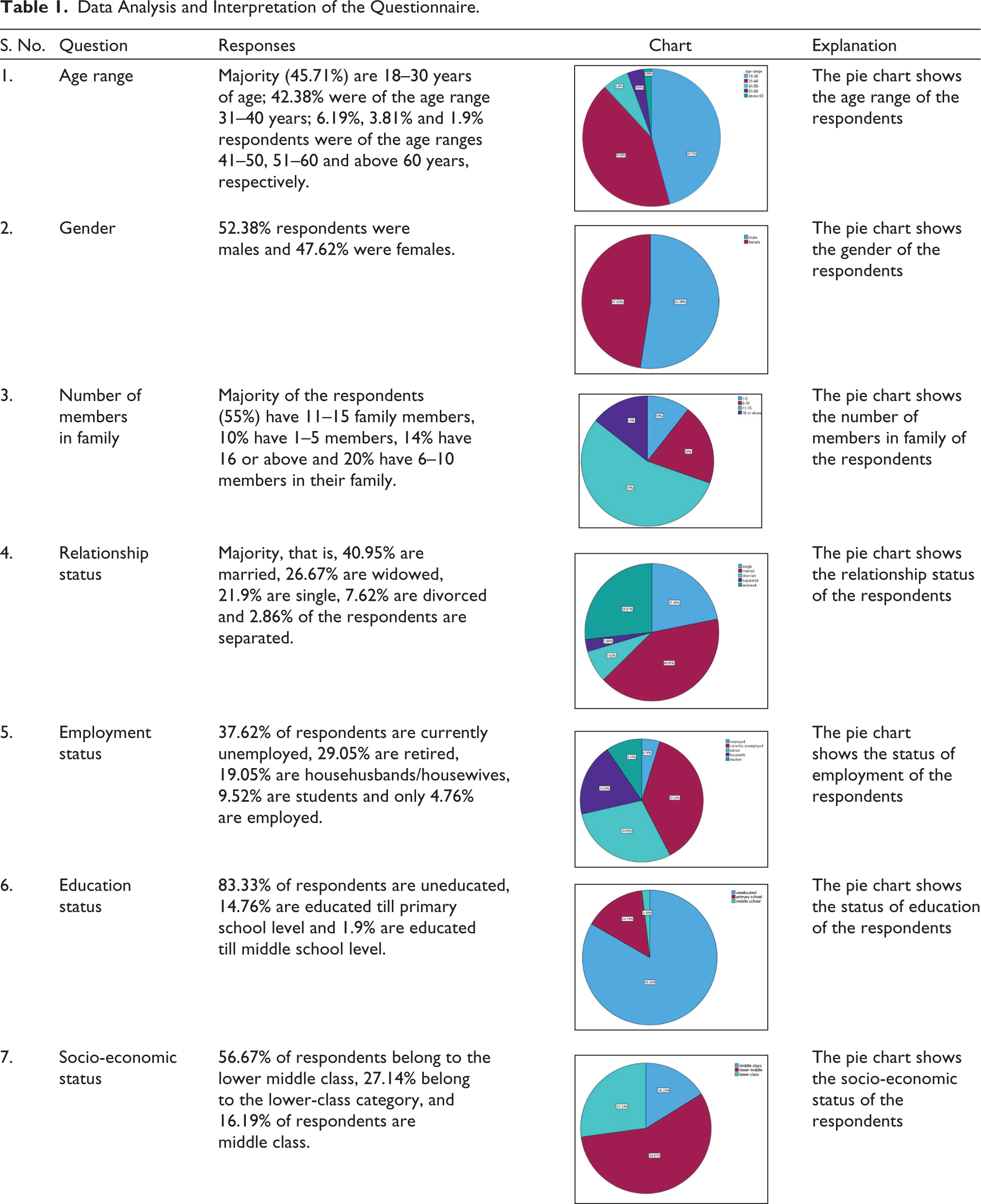

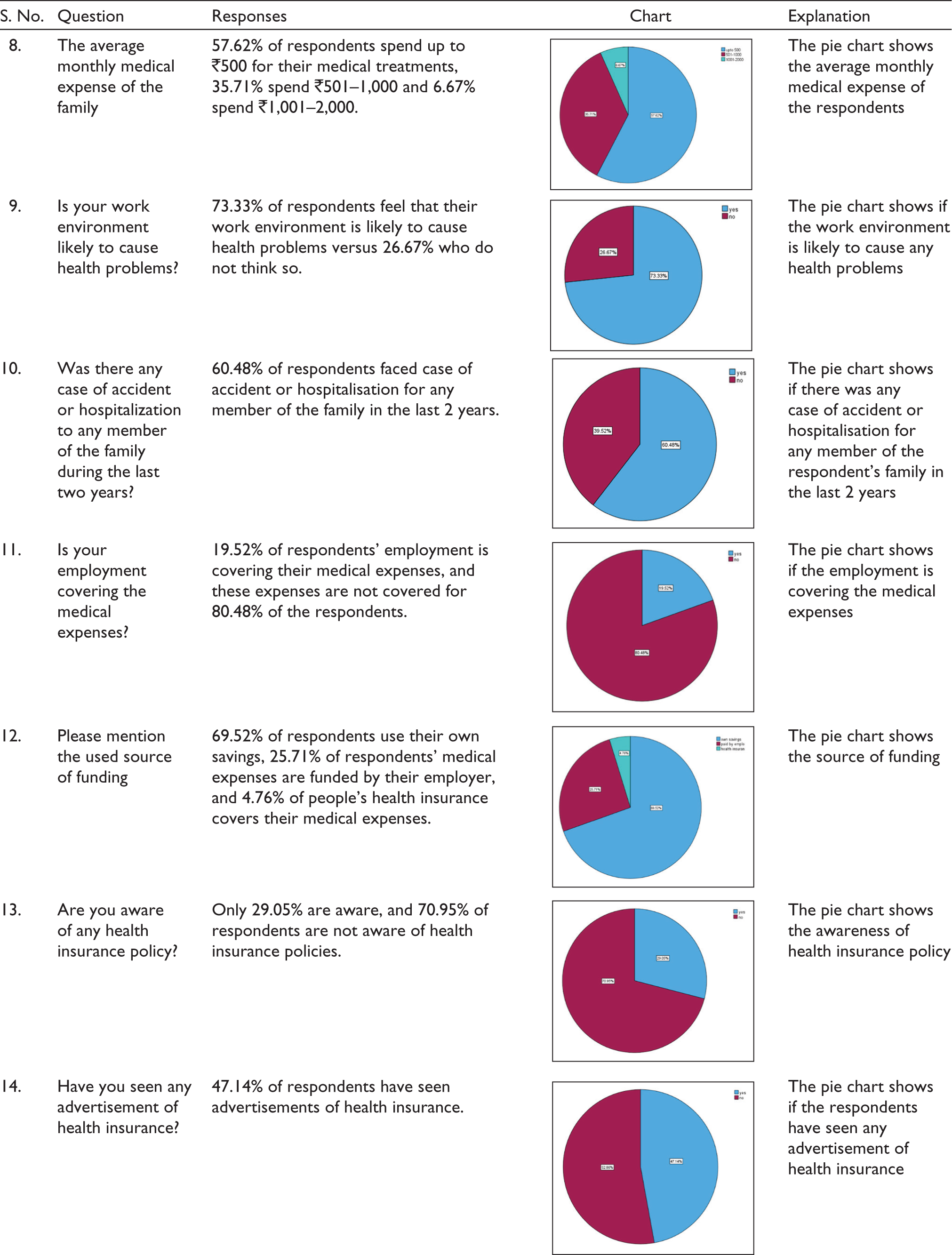

The questions were posed to people of various ages (starting from the age of 18 years), as shown in Table 1.

Data Analysis and Interpretation of the Questionnaire.

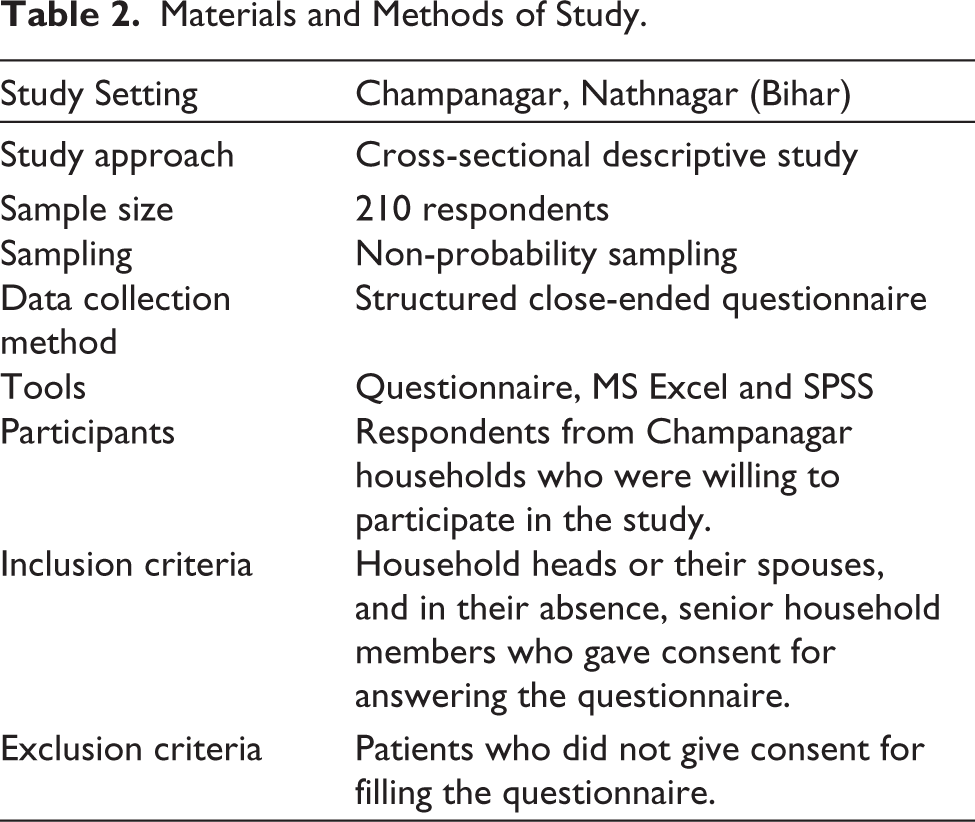

A list of all the villages was generated in ascending order by population, and villages were picked by probability proportionate to size, with 210 respondents chosen using a simple random selection procedure, as shown in Table 2.

Materials and Methods of Study.

1. Data collection

All participating houses were provided with prior, informed written permission in the local language. The consent was read and communicated to those who were uneducated in their native language, and their thumb impression was taken in the presence of a witness. Data was collected by visiting selected homes and conducting face-to-face interviews using a closed-ended structured questionnaire with questions about socio-demographic information and health insurance awareness.

>2. Statistical analysis

Data that was collected was analysed using SPSS software. Descriptive statistics were calculated. The collection and evaluation of information in order to identify patterns and trends is known as statistical analysis. It is part of data analytics. Statistical analysis may be used for a variety of purposes, including obtaining research interpretations, statistical modelling and creating surveys and studies.

3. Criteria for inclusion

Household heads or their spouse, and in their absence, another senior household member aged 18–45 eager to engage in our study. The working family head was given preference.

4. Criteria for exclusion

Household members who refused to participate in the study. People who were very unwell at the time of the survey.

5. Ethical consideration

Participants gave their consent prior to data collection. Ethical concerns are primarily concerned with preventing damage to youngsters and adolescents as a consequence of their involvement in your organization’s decision-making processes. Voluntary engagement, informed permission, anonymity, secrecy, potential for damage and outcomes communication are among these principles.

Result Analysis

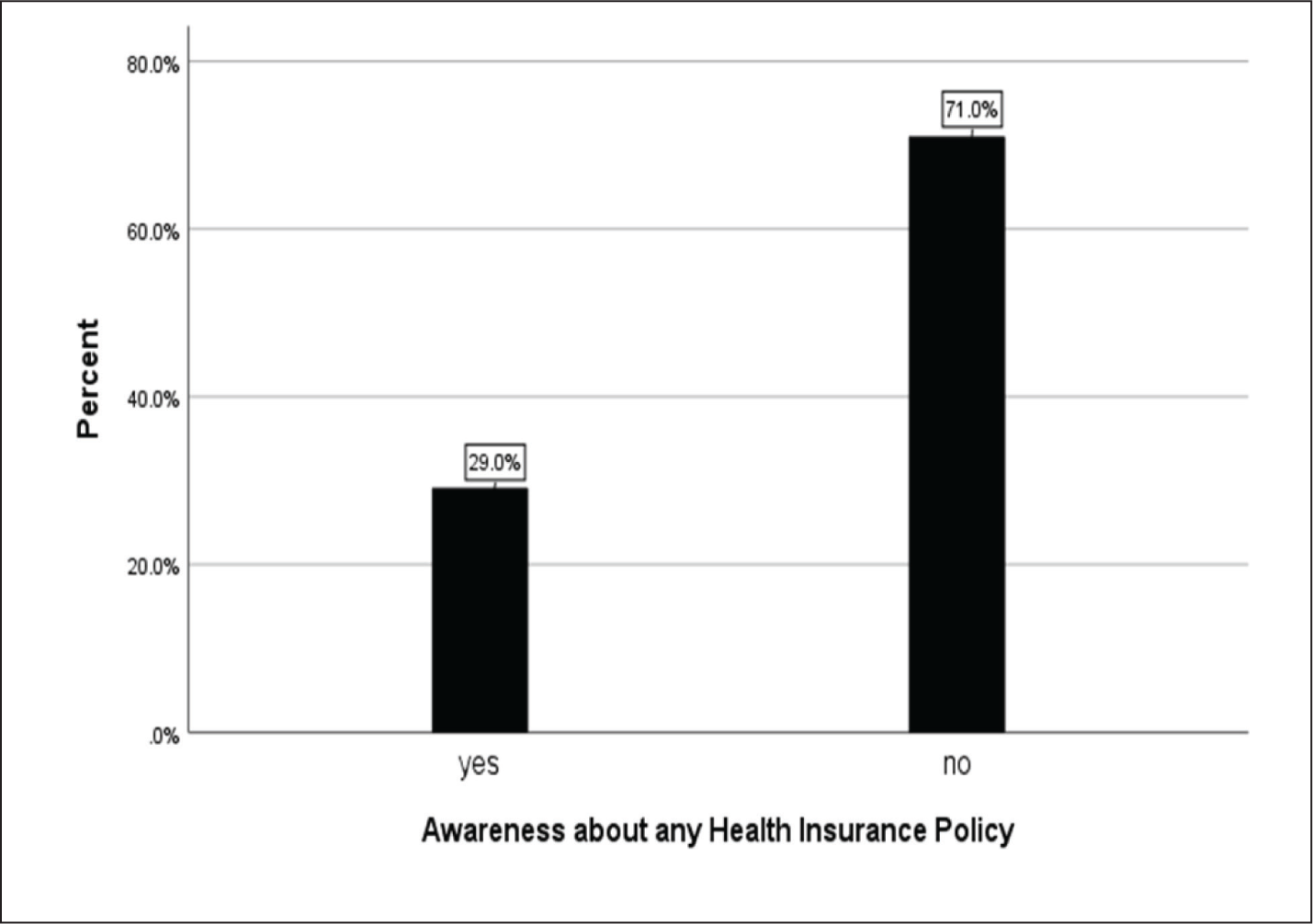

Of the 210 respondents, only 29.05% were well aware of health insurance policies, whereas 70.95% did not know about them, as shown in Figure 2.

Shows the Comparison of People Who Are and Who Are Not Aware of Health Insurance Policies.

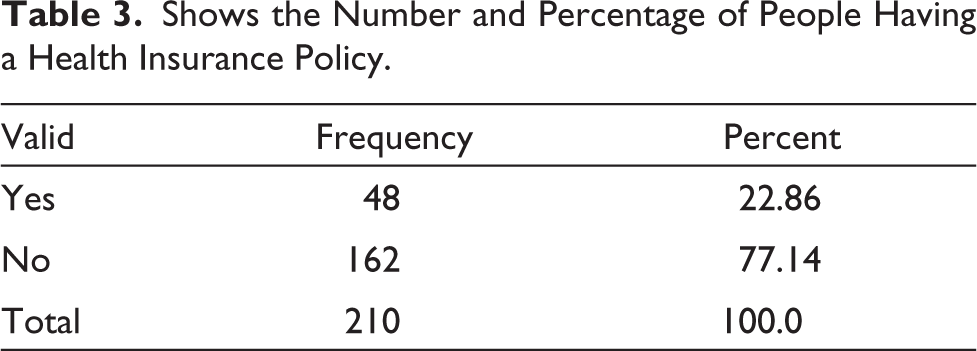

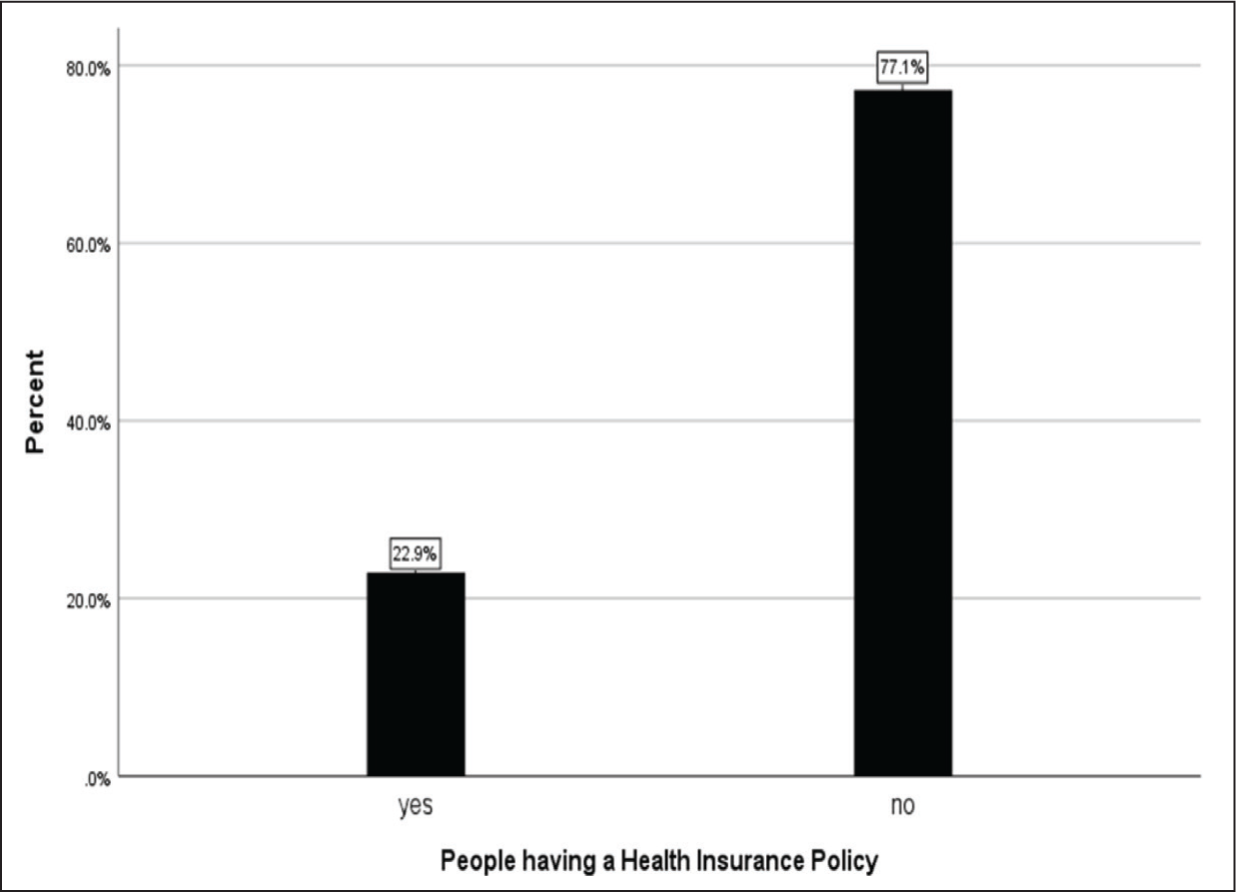

Out of the total respondents who were aware of health insurance, 22.86% of respondents had health insurance and 77.14% did not have any health insurance, as shown in Table 3 and Figure 3.

Shows the Number and Percentage of People Having a Health Insurance Policy.

Shows the Percentage of People Who Have a Health Insurance Policy.

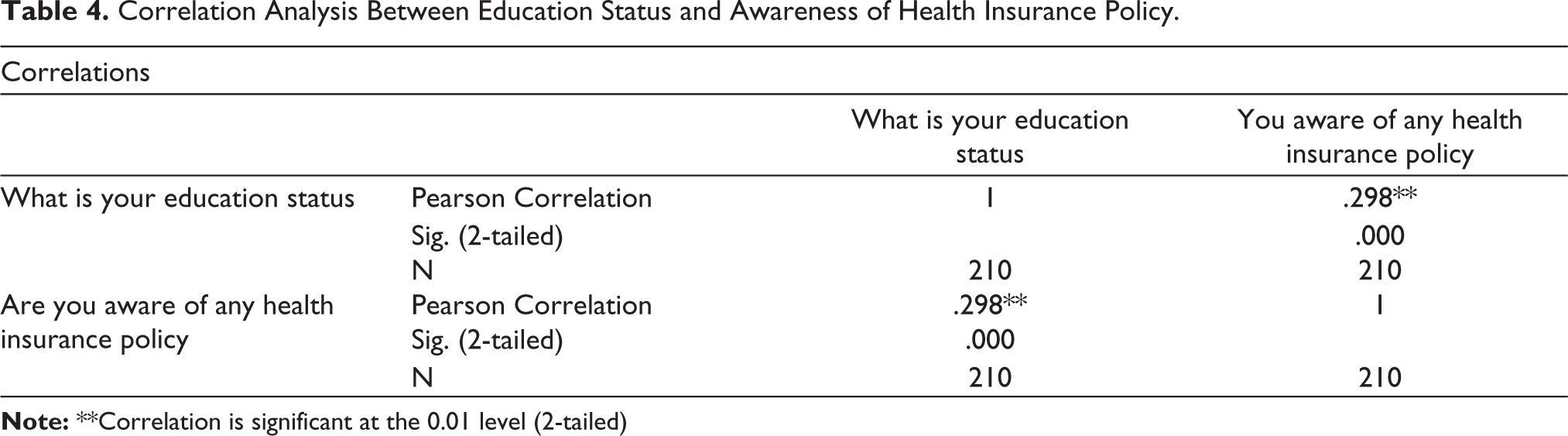

We used correlation analysis, which is a statistical method used to find out the relationship between two different attributes. In Table 4, we have analysed the correlation between education status and awareness of health insurance policies. The Pearson correlation value of 0.298 suggests that there is a positive relationship between these two attributes, and it is safe to say that these are highly correlated. Thus, as the education level increases, awareness among people also increases.

Correlation Analysis Between Education Status and Awareness of Health Insurance Policy.

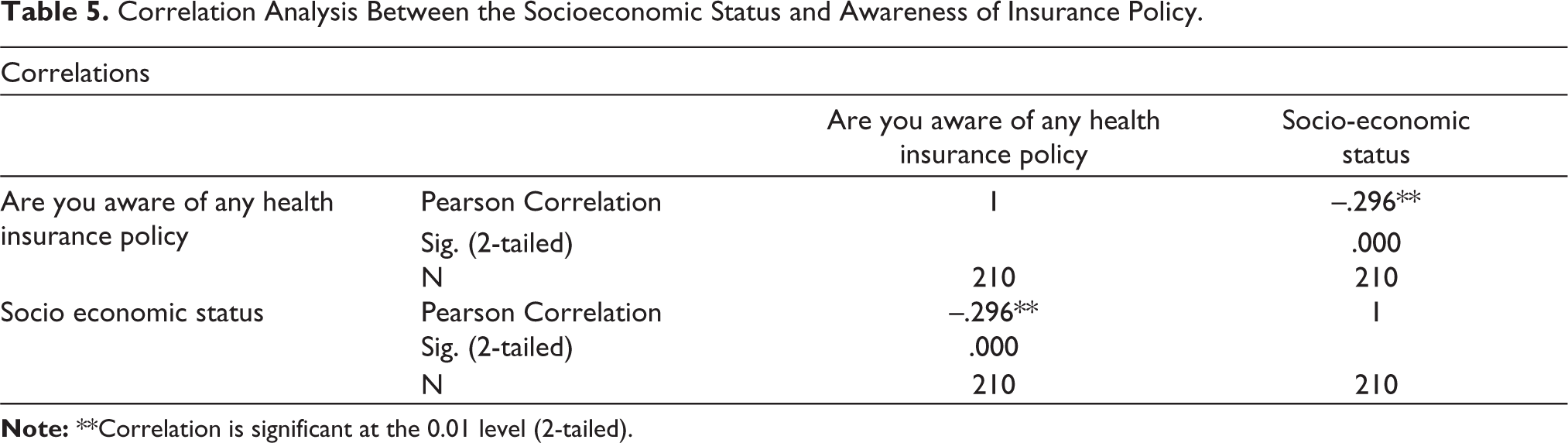

Now, it is based on the Pearson correlation value (–0.296), as seen in Table 5, the attributes— socioeconomic status and awareness of health insurance policies—were found to be inversely correlated. As socioeconomic status changes from lower to upper middle class, the awareness of policies increases.

Correlation Analysis Between the Socioeconomic Status and Awareness of Insurance Policy.

Discussion

The goal of this study is to determine the level of awareness regarding medical insurance among people and the factors that influence awareness. The proportion of health insurance awareness among 210 rural respondents was 29.05%. When compared to other studies, this study found a lower prevalence of awareness, implying that the government must make greater efforts to fulfil its responsibilities of raising public awareness of medical insurance and making the process of sanctioning policies in critical times easier and faster.

Individuals’ degrees of awareness are impacted by a range of factors, including their education and social background. Effective education and communication initiatives will improve people’s understanding of insurance. The majority of respondents stated that creating a health insurance policy involved multiple steps and they had a hazy understanding of the different rewards and hazards included in a policy. Insurance companies must first analyse the behaviour of individuals before establishing a scheme that must be accessible, inexpensive and acceptable to everybody. The study also indicated that awareness levels were significantly influenced by a lack of confidence in insurance firms and their policies. This implies that insurance providers must try to increase trust with prospective clients by being open and honest about their plans and perks and by offering top-notch customer service.

Lastly, this study emphasizes the significance of focused outreach and communication initiatives. To reach people in remote locations who might not have access to the internet or conventional media outlets, medical insurance firms and governments need to establish specialised communication strategies. Initiatives like mobile clinics, community outreach programmes and awareness campaigns in regional languages might fall into this category. Overall, this study emphasises the significance of spreading knowledge about medical insurance and the necessity for legislators and insurance providers to collaborate in order to develop open, transparent and affordable policies that meet the needs of all people, regardless of their social or economic background.

Conclusion

In rural regions, where there is minimal awareness of insurance, the report emphasises the need for immediate action to boost health insurance coverage. People’s socioeconomic status and level of education were revealed to be important determinants of health insurance awareness. Hence, in order to inform the public about the value of medical insurance, particularly in emergency situations where unexpectedly significant medical costs may arise, strong public awareness campaigns are required.

A comprehensive strategy that takes into account issues with knowledge, accessibility and price is required to boost insurance penetration in rural regions. With AI, ML and data analytics technologies examining consumer behaviour and preferences to increase access to insurance products for individuals of all income levels, technology may play a critical role in this endeavour. The adoption of insurance platforms that provide affordable insurance policies has been prompted by the rise in smartphone use in the rural market in recent years. With the help of these tools, which provide smooth API access and end-to-end digital operations, the user experience has been optimised and the insurance sales process has been made easier. Also, this has sped up the dissemination of instant policies, making it simpler and quicker to sanction regulations in urgent situations.

In conclusion, the study highlights the necessity of a coordinated effort to encourage health insurance coverage in rural regions, utilising a mix of successful public awareness campaigns and cutting-edge technological solutions. Policymakers and insurance providers may collaborate to ensure that individuals in rural regions have access to the medical insurance they require to safeguard themselves and their families from unforeseen medical bills by addressing issues with awareness, accessibility and affordability.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.