Abstract

The usage of banking functions through Internet is comfortable and time saving process, since the usage rates of different banking functions through Internet banking mechanism are very low. The present study aims to evaluate the variations between physical banking and internet banking and explores the problems faced by banking customers in using internet banking amid the COVID-19 pandemic. The primary data for the present study were collected from banking customers, who were identified on a random basis from three different areas of the Union Territory of Jammu and Kashmir. The total sample size was 1,200, comprising a breakup of 400 for each of the sampling areas of central Kashmir, south Kashmir and north Kashmir. Internet banking adoption is changing the physical usage of non-financial products and financial products worldwide. Today, a click of the mouse and mobile banking offer a lot of transactions regarding electronic non-financial products and electronic financial products. Still, the adoption rates of these products are very low. The present study has examined the situation of electronic banking adoption amid the COVID-19 pandemic, and hence, it is found that maximum number of customers are non-users of electronic non-financial products and electronic financial products. Amid the pandemic, the reason for non-usage of technology banking by a majority of customers was lack of awareness, technological barriers and security concerns. They also used physical banking activities and did not follow social distancing as suggested by the Government of India during March 2020. Therefore, it is the basic responsibility of the banking industry to motivate their customers and address their concerns regarding the usage of electronic non-financial products and electronic financial products, as the maximum number of banking customers are non-users of electronic non-financial products and electronic financial products. If the banking industry will address the concerns of banking customers regarding the usage of technology banking, then only a country like India with a huge population can have technological banking and environment-friendly banking and can face situations like the COVID-19 pandemic in future.

Keywords

Introduction

Physical Banking

Physical banking is basically brick-and-mortar banking. In physical banking, customers visit the bank branch for different banking functions and speak with the staff of the bank (Khalfan & Alshawaf, 2004). Hence, physical banking can be explained as banking in which banking customers visit bank branches for day-to-day banking activities. According to the 2016 Global Consumer Banking survey, among the surveyed 55,000 banking customers in 32 countries, 60% said they would want to do physical banking or speak with a real person in order to do banking related to financial transactions or non-financial transactions.

Electronic Banking

Electronic banking, also known as internet banking, is an electronic system that enables customers of a bank or financial institution to conduct a wide range of financial and non-financial transactions through the financial institution’s website or through the mobile banking application of a particular bank (Sheikh & Rajmohan, 2017).

Electronic Financial Products

The different financial products that support electronic banking platforms are called electronic financial products (Sheikh & Rajmohan, 2017). Previously, banking customers were using financial products offline, but due to the revolution of information and technology, all financial products are supported by electronic mechanisms (Gupta, 2008). The list of important electronic financial products that can be handled with e-banking by banking customers is as follows:

Electronic fund transfer (NEFT, RTGS and IMPS) Using a debit card for online transactions Managing credit cards Investments in derivatives Paying insurance premiums Mutual fund investments Loan EMI payments Investments in futures and options Internet banking account Online share trading

Electronic Non-financial Products

The different non-financial products that support electronic banking platforms are called electronic non-financial products. According to Sheikh and Rajmohan (2017) and Jammu and Kashmir Bank, HDFC Bank, ICICI Bank, AXIS Bank, etc, the list of important non-financial products that can be handled with e-banking by banking customers is as follows:

Electricity bill payment Payment for train tickets Mobile recharge DTH recharge Payment for bus tickets Landline bill payment Payment for buying products through Payment of income taxes and other taxes Payment for flight tickets Charity donations

Review of Literature

Margaret and Thompson (2000) report that the intention to adopt electronic financial products and electronic non-financial products can be predicted by attitudinal and perceived behavioural control factors but not by subjective norms. Kettinger and Lee (2005) examined that the attitudinal elements that are critical and need to be improved; alignment with the respondent's characteristics, background, requirements, and potential risks (Sheikh & Rajmohan, 2017). The discoveries of this investigation revealed that apparent attitude has a negative relationship with reception aims, and this relationship is not huge. One possible reason is that since electronic financial products and electronic non-financial products are relatively new, most internet users have yet to try them. Information technology usage and adoption is not easy; if wrongly operated, it can prove to be very dangerous for individuals, customers and organisations (Sheikh & Rajmohan, 2017). The results of this study have also shown that there are other factors besides attitudinal ones that can help us better understand the adoption intentions of digital banking (Sheikh & Rajmohan, 2017).

Two additional influencing factors (subjective norms and perceived behavioural control) proposed by Ajzen (2002) in the theory of planned behaviour were included in this study. Although subjective norms were not found to significantly influence adoption intentions, perceived behavioural control dimensions were nonetheless found to have significant influences. Sheikh and Rajmohan (2017) explored that, in particular, self-efficiency towards using electronic financial products and electronic non-financial products and the facilitating condition of perceived government support for internet commerce were both found to significantly affect intentions to adopt electronic financial products and electronic non-financial products; however, Mohamed (2012) reported that e-banking services are being used with increasing frequency in most countries. Khalfan and Alshawaf (2004) found that electronic banking enhances the development of the banking system and is considered a strategic weapon for banks. Although it provides various benefits for both banks and customers, a low level of customers’ adoption of electronic banking services is noted in Jordan. Also, electronic banking services cannot achieve the expected benefits if they are not used by banking customers (Poon, 2007). A research model was developed by integrating TAM with TBP and incorporating five cultural dimensions and perceived risk to provide a comprehensive study of the results, which reported that perceived usefulness and ease of use had quite a positive and significant impact on the customers’ attitude towards electronic banking services (Khalfan & Alshawaf, 2004).

Banks are supposed to continue providing electronic banking services. They could achieve this by increasing the customers’ awareness of the usefulness of using electronic banking services through advertising and long-term customer services. This study used a cross-sectional design by Kotler and Keller (2011). One possible direction for future studies is to conduct a longitudinal study to see whether the variables and their relationships are consistent with time. Second, this study used Hofstede’s national cultural framework (Sakkthivel, 2006). However, Lichtenstein and Williamson (2006) report key findings from an interpretive study of Australian banking, which provide an understanding of how and why specific factors affect the consumers’ decision of whether or not to use internet banking mechanisms for financial transactions (Khadem & Mousavi, 2013). A practical explanation links it to the adoption of digital banking. This study also provides a set of recommendations for Australian banks. Additionally, the findings suggest that attitudes depend on the adoption of internet banking services, while there is a range of other influential factors that may be modulated by banks (Pearson et al., 2010). This study also highlights increasing risk acceptance by consumers with regard to internet-based services and the growing importance of offering deep levels of consumer support for such services (Parasuraman et al., 2002). Gender differences are also highlighted. Finally, this study suggests that banks will be better able to manage consumer experiences while moving to electronic financial products and electronic non-financial products if they understand that such experiences involve a process of adjustment and learning over time, and not merely the adoption of a new technology (Sheikh & Rajmohan, 2017). Also, Jayashree in 2013 studied that online banking (digital banking) has emerged as one of the most profitable e-commerce applications over the past decade (Sakkthivel, 2006).

However, other studies have examined the condition where information and technology had been already adopted for banking services, and there is limited empirical work which simultaneously captures the success factors (positive factors) and resistance factors and explores and integrates the various advantages of online banking to form a positive factor named perceived benefit. Results from perceived risk focused on the usage and adoption of technology from a banking point of view through the TAM (Technology Acceptance Model). The results of this study indicated that the intention to use online banking is adversely affected mainly by security/privacy risks, as well as financial risks, and is positively influenced by perceived usefulness and attitude. Thompson et al. in 2011 explored a research framework based on the theory of planned behaviour (Ajzen, 1985), and the diffusion of innovation theory was used to identify the attitudinal, social and perceived behavioural control factors that would influence the adoption of digital banking (Sheikh & Rajmohan, 2017). The results revealed that attitudinal and perceived behavioural control factors, rather than social influence, play a significant role in influencing the intention to adopt digital banking (Laio, 2002). In particular, perceptions of relative advantage, compatibility, trainability and risk towards using the internet were found to influence intentions to adopt electronic financial products (Poon, 2007). In addition, confidence in using such services as well as perceptions of government support for electronic commerce were also found to influence intentions (Mohammad, 2010).

Agarwal (2000) proposed a new framework for analyzing consumer behavior related to the usage of Internet banking services while as Akinci (2004) conducted a study on customer satisfaction in the hospitality industry by usage of internet banking services however De Ruyter et al. (2001) explored the relationship between service quality and customer loyalty through e services Also, Hofstede’s (2007) cultural dimensions theory has been widely used in cross-cultural research Pearson (2010) conducted a study on the effects of advertising through electronic mechanism on consumer behavior while as Zeithaml et al. (2002) developed the SERVQUAL model to measure service quality.

Joshua (2015) introduced a novel approach to market segmentation for electronic services while as Kannabiran and Narayan (2009) investigated the impact of social media on brand perception. Keller (2010) discussed the role of branding in consumer decision-making through online services while as, Kennickell and Kwast (1997) examined electronic banking usage patterns in different geographies. Liao and Cheung (2002) proposed a model for predicting customer churn. Madu and Madu (2002) analyzed factors influencing customer satisfaction in the electronic service industry while as Oliver (1980) introduced the concept of satisfaction as a key determinant of customer loyalty in electronic banking.

Methodology and Objectives

Statement of Problem

The growth of internet banking has been observed both in practice and in literature in recent times. While every banking institution operating in India is offering internet banking features to its customers, the exact choice of the customers towards its adoption still remains uncharted, both in practice and in literature, in the Indian context. Further, various financial institutions and non-financial institutions in India have started offering online services with good success in their respective e-service initiatives. While many of the online initiatives of financial institutions and non-financial institutions have succeeded, not all the categories of customers served by those institutions have reaped the benefits offered online. One distinctive factor that differentiates such customers is none other than the digital divide factor leading to the adoption and usage of the internet as a whole. However, the clarity of the other factors leading to the adoption of such e-services offered by those financial institutions and non-financial institutions still remains unclear. While technology acceptance models act as the basic framework to estimate the factors that can contribute towards the adoption of technology, the intricate limitations of each of those models expose the unsuitability of those models from a banking technology perspective. However, the Unified Theory of Acceptance and Use of Technology (UTAUT) explains and succeeds in its adoptability of measuring factors contributing to technology-based banking and online financial transactions by customers, and hence, the following objectives were framed to carry out this work:

Objectives

To find out the variations between physical banking and internet banking usage amid the COVID-19 pandemic

To find out variations in the behaviour and intentions of customers leading to internet banking usage in different areas of living

To find out the variations between education and usage of internet banking by banking customers.

Hypotheses

Sampling Area

The primary data for the present study were collected from banking customers, and these customers were identified on a random basis from three different areas of the Union Territory of Jammu and Kashmir: central Kashmir, south Kashmir and north Kashmir.

Sampling Technique

The sampling procedure adopted for the present study was a stratified random sampling method.

Sample Size

The primary data for the present study were collected from banking customers, and these customers were identified on a random basis from three different areas of the Union Territory of Jammu and Kashmir. The total sample size of 1,200 comprised of 400 for each of the sampling areas of central Kashmir, south Kashmir and north Kashmir.

Sampling Details

The nature of the topic and the objectives warrant banking customers as the sample for this study. Also, it is possible to interpret the adoption of internet banking as an innovation which is still under diffusion among the banking customers in India. Under these circumstances, the guidelines suggested by Rogers in 1983 on the diffusion of innovation theory were used as the basis to locate the sampling areas for the present study. On the basis of social articulation levels, three segments that were identified as relevant sampling areas for this study were located on a random basis. They are metropolitan cities, other cities and sub-urban places. Accordingly, the highest levels of social articulation were noted in Smart City Srinagar. Hence, Srinagar from central Kashmir as one of the sampling places was finalised on a random basis. The next highest levels of social articulation are noted in tier 2 cities. Out of these cities, Anantnag from South Kashmir as one of the sampling places was finalised on a random basis. The threshold levels of social articulation that can sustain the diffusion of innovations like internet banking could be located among various suburban places. Out of these places, Kupwara from North Kashmir as one of the sampling places was finalised on a random basis. The process of locating banking customers in the identified sampling areas was done by first identifying the banking institutions that deal with banking customers who constitute the relevant sample for the present study. In this regard, four banking institutions that are commonly operating in all three identified sample areas were finalised. These four banking institutions also have significant levels of customers with internet banking adoptions. Also, 4 out of all of these banking institutions are listed in the top 10 banking enterprises operating in India.

The primary data for the present study was collected between June 2020 and August 2020. The data collected were coded and transferred into the Statistical Package for Social Science (SPSS) for the purpose of analysis.

Data Analysis and Discussion

Relationship Between Intensity Levels Of Internet Banking And ATM Usage Amid COVID-19 Pandemic

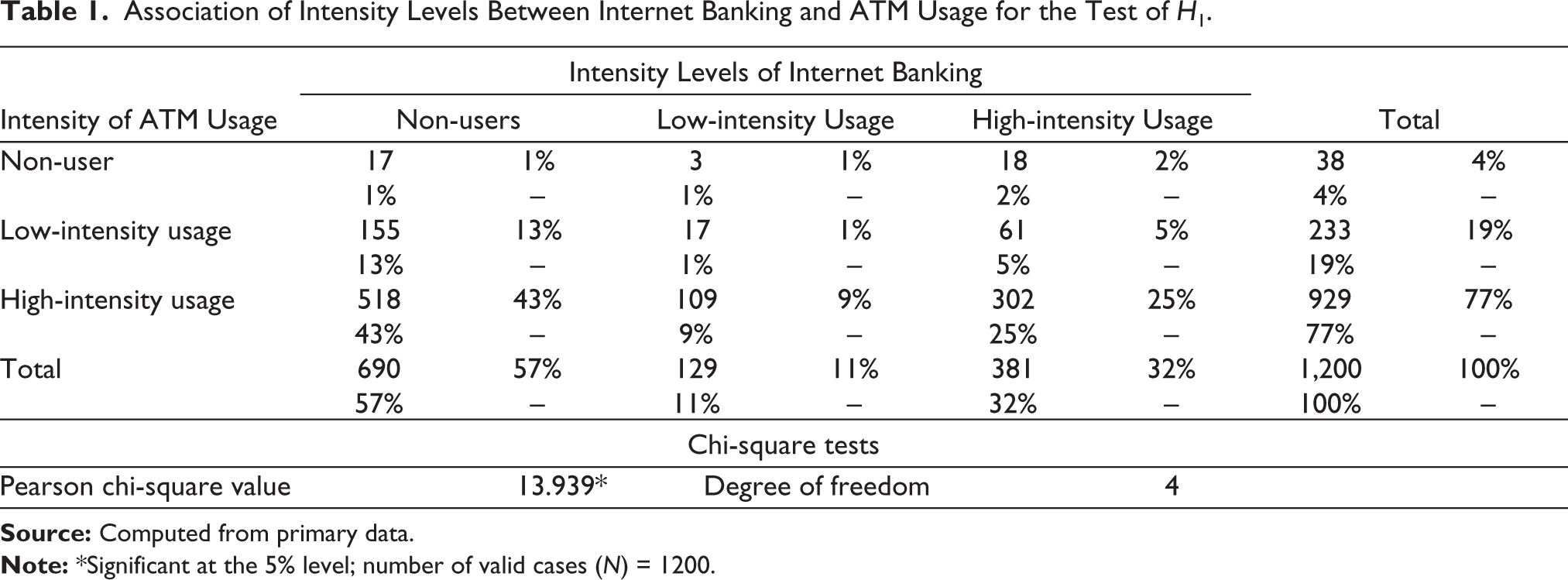

The kind of association that exists between intensity levels of ATM usage and intensity levels of internet banking usage amid the COVID-19 pandemic among banking customers was defined in H1, and its results are shown in Table 1 as the outcome of chi-square analysis and the corresponding cross-tabulation.

Association of Intensity Levels Between Internet Banking and ATM Usage for the Test of H1.

From the results shown, it can be inferred that the chi-square value of 13.939 with 4 degrees of freedom has been found to be significant at the 5% level. Hence, hypothesis 1 is rejected, and significant levels of association could be established between the intensity levels of ATMs and the intensity levels of internet banking usage amid the COVID-19 pandemic. From the cross-tabulation, it can be inferred that the high-intensity levels of ATM usage is associated significantly with non-usage of internet banking applications among banking customers amid the COVID-19 pandemic.

The Relationship Between Intensity Levels of Internet Banking Usage and Bank Branch Visit amid the COVID-19 Pandemic

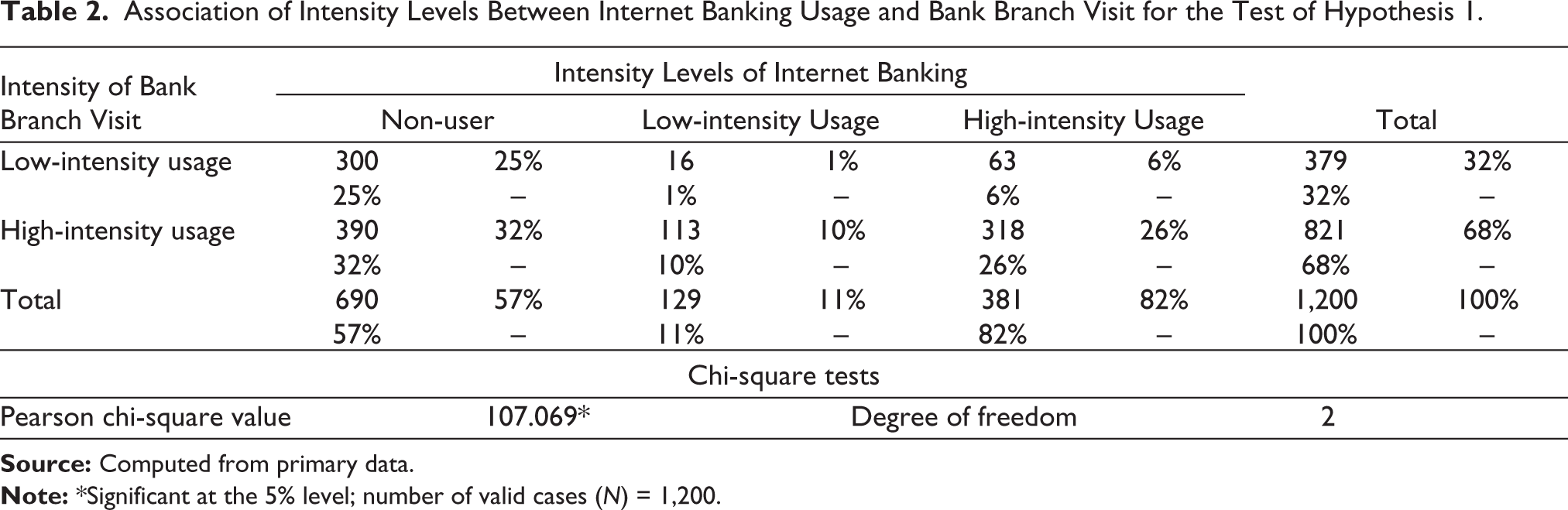

The kind of association that existed between the intensity levels of internet banking usage and bank branch visits amid the COVID-19 pandemic among banking customers was defined in hypothesis 1, and its results are shown in Table 2 as the outcome of chi-square analysis and corresponding cross-tabulation.

Association of Intensity Levels Between Internet Banking Usage and Bank Branch Visit for the Test of Hypothesis 1.

From the results shown, it can be inferred that the chi-square value of 107.069 with 2 degrees of freedom has been found to be significant at the 5% level; therefore, hypothesis 2 is rejected, and hence, significant levels of association could be established between the intensity levels of internet banking usage and bank branch visits amid the COVID-19 pandemic. From the cross-tabulation, it can be inferred that the high-intensity levels of bank branch visits are associated significantly with non-usage of internet banking applications among banking customers amid the COVID-19 pandemic.

The Relationship Between Intensity Levels of Internet Banking and Mutual Fund Investment amid the COVID-19 Pandemic

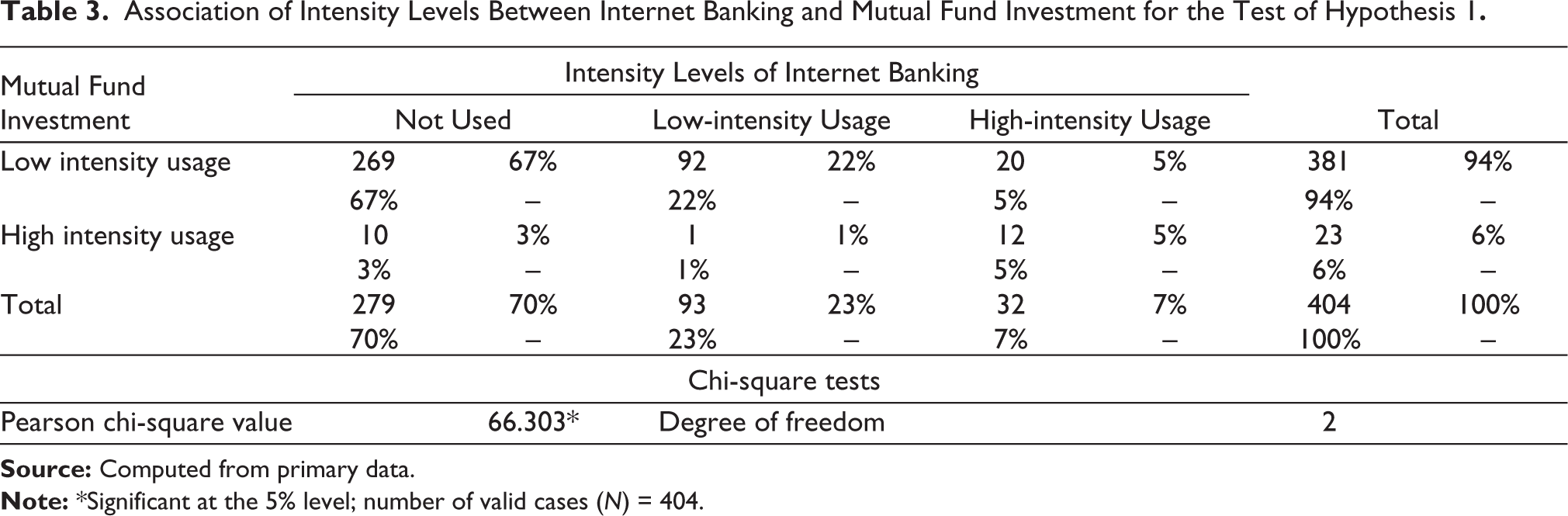

The kind of association that existed between intensity levels of mutual fund investment and intensity levels of internet banking usage amid the COVID-19 pandemic among banking customers is defined in hypothesis 1, and its results are shown in Table 3 as the outcome of chi-square analysis and corresponding cross-tabulation. From the results shown, it can be inferred that the chi-square value of 66.303 with 2 degrees of freedom has been found to be significant at the 5% level; therefore, hypothesis 1 is rejected, and hence, significant levels of association could be established between the intensity levels of mutual fund investment and the intensity levels of internet banking usage amid the COVID-19 pandemic.

Association of Intensity Levels Between Internet Banking and Mutual Fund Investment for the Test of Hypothesis 1.

From the cross-tabulation, it can be inferred that the low intensity levels of mutual fund investment are associated significantly with the non-usage of internet banking applications among banking customers. However, 94% of mutual fund investors are identified as having low-intensity levels of mutual fund investments through online banking mechanisms.

Relationship Between Intensity Levels of Availing Insurance Services and Utilisation of Online Insurance Services in the COVID-19 Pandemic

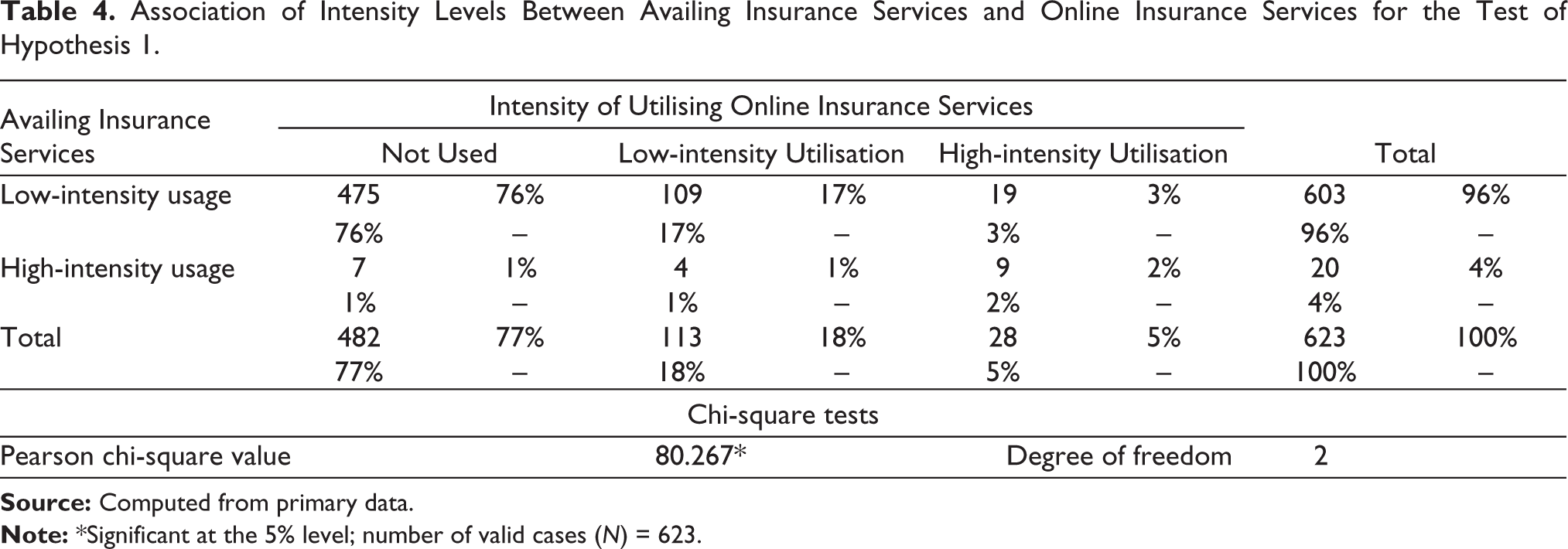

The kind of association that exists between intensity levels of availing insurance services and intensity levels of utilising online insurance services amid the COVID-19 pandemic was defined in hypothesis 1, and its results are shown in Table 4 as the outcome of chi-square analysis and corresponding cross-tabulation.

Association of Intensity Levels Between Availing Insurance Services and Online Insurance Services for the Test of Hypothesis 1.

From the results shown, it can be inferred that the chi-square value of 80.267 with 2 degrees of freedom has been found to be significant at the 5% level; therefore, hypothesis 1 is rejected, and hence, significant levels of association could be established between the intensity level of availing insurance services and the intensity levels of utilising online insurance services amid the COVID-19 pandemic. From the cross-tabulation, it can be inferred that a low-intensity level of availing of insurance services is associated significantly with non-utilisation of online insurance services among banking customers (Joseph & Stone, 2003). However, 96% of insurance policyholders are identified as having low intensity levels when availing insurance services amid the COVID-19 pandemic.

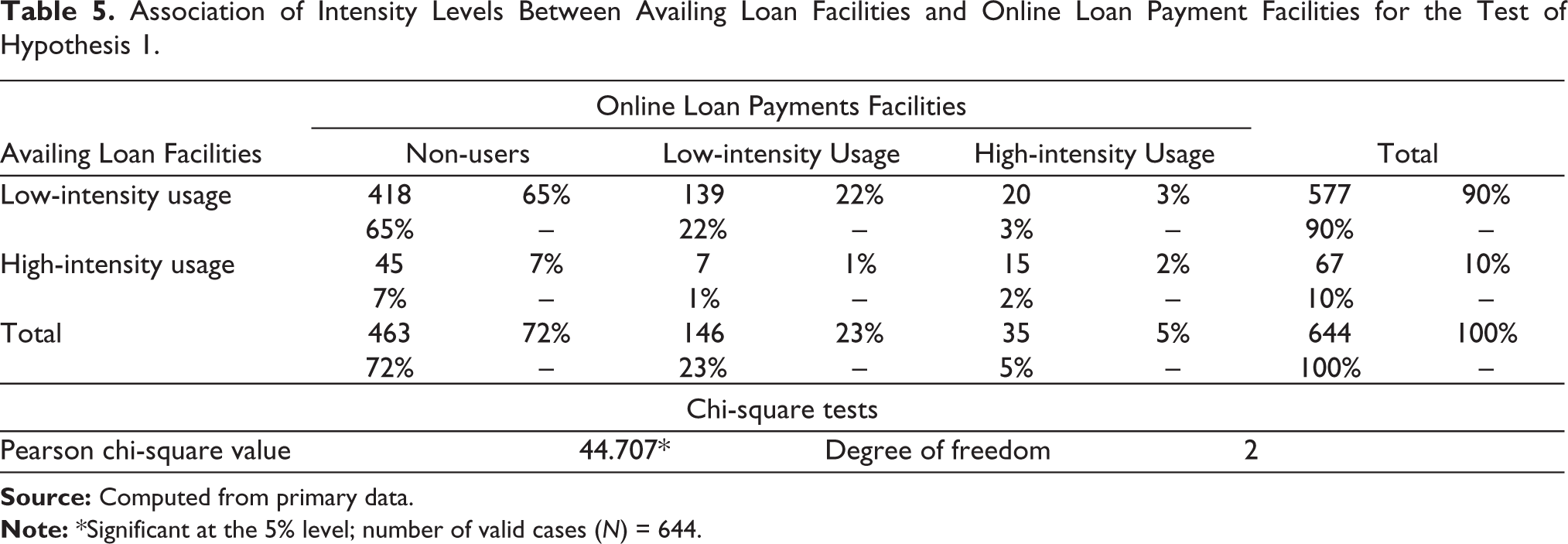

Relationship Between Intensity Levels of Availing Loan Facilities and Online Loan Payment Facilities amid the COVID-19 Pandemic

The kind of association that exists between intensity levels of availing loan facilities and online loan payment facilities amid the COVID-19 pandemic was defined in hypothesis 1, and its results are shown in Table 5 as the outcome of chi-square analysis and corresponding cross-tabulation.

Association of Intensity Levels Between Availing Loan Facilities and Online Loan Payment Facilities for the Test of Hypothesis 1.

From the results shown, it can be inferred that the chi-square value of 44.707 with 2 degrees of freedom has been found to be significant at the 5% level; therefore, hypothesis 1 is rejected, and hence, significant levels of association could be established between the intensity level of availing loan facilities and availing online loan payment facilities amid the COVID-19 pandemic. From the cross-tabulation, it can be inferred that the low intensity level of availing loan facilities is associated significantly with non-utilisation of online loan payment facilities amid the COVID-19 pandemic among banking customers. However, 90% of banking debtors are identified as having low intensity levels in availing loan facilities offered amid the COVID-19 pandemic.

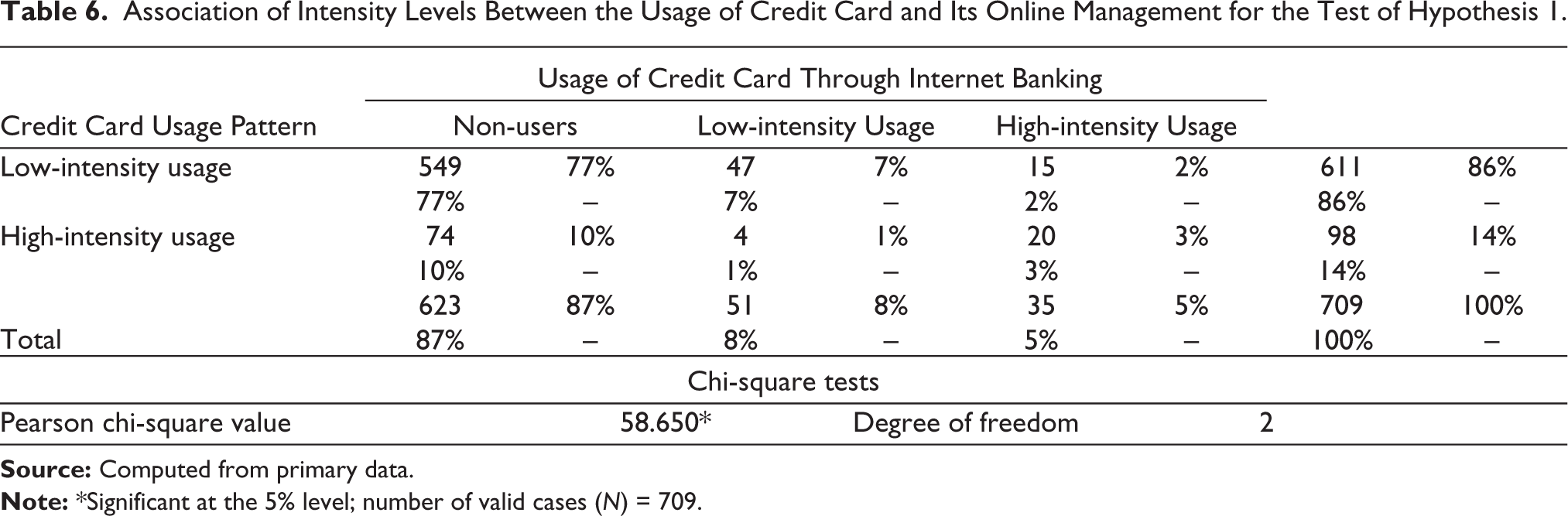

The Relationship Between Intensity Levels of Credit Card Usage and Its Online Management amid the COVID-19 Pandemic

The kind of association that exists between intensity levels of credit card usage and its online management amid the COVID-19 pandemic was defined in hypothesis 1, and its results are shown in Table 6 as the outcome of chi-square analysis and corresponding cross-tabulation.

Association of Intensity Levels Between the Usage of Credit Card and Its Online Management for the Test of Hypothesis 1.

From the results shown, it can be inferred that the chi-square value of 58.650 with 2 degrees of freedom has been found to be significant at the 5% level; therefore, hypothesis 1 is rejected, and hence, significant levels of association could be established between the intensity levels of credit card usage and its online management amid the COVID-19 pandemic. From the cross-tabulation, it can be inferred that the low intensity level of credit card usage is associated significantly with non-utilisation of its online management features amid the COVID-19 pandemic among banking customers. However, 86% of credit card users are identified as having low-intensity credit card usage pattern.

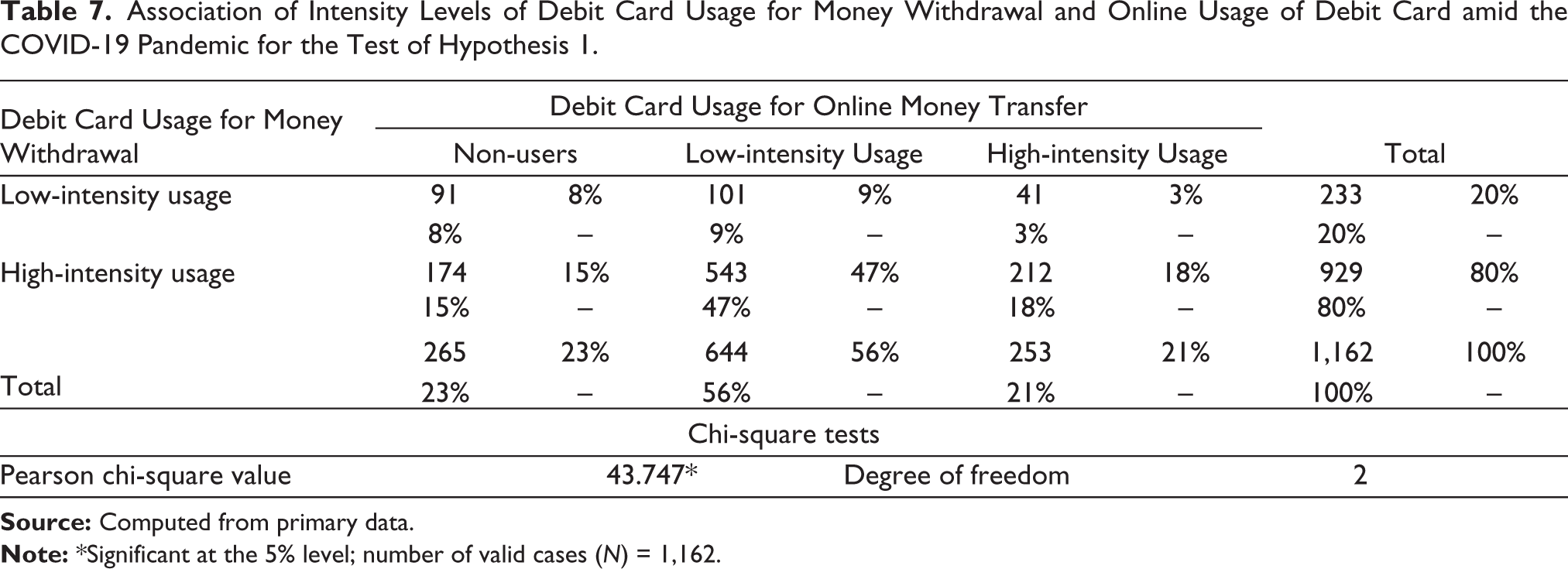

Relationship Between Intensity Levels of Debit Card Usage for Money Withdrawal and Online Usage of Debit Card amid the COVID-19 Pandemic

The kind of association that exists between debit card usage for money withdrawal and online usage of debit cards amid the COVID-19 pandemic was defined in hypothesis 1, and its results are shown in Table 7 as the outcome of chi-square analysis and corresponding cross-tabulation.

Association of Intensity Levels of Debit Card Usage for Money Withdrawal and Online Usage of Debit Card amid the COVID-19 Pandemic for the Test of Hypothesis 1.

From the results shown, it can be inferred that the chi-square value of 43.747 with 2 degrees of freedom has been found to be significant at the 5% level, therefore, hypothesis 1 is rejected, and hence, significant levels of association could be established between debit card usage for money withdrawal and online usage of debit cards amid the COVID-19 pandemic. From the cross-tabulation, it can be inferred that the high-intensity levels of debit card usage for money withdrawal are associated significantly with low-intensity levels of debit cards for online money transfers amid the COVID-19 pandemic among banking customers. In this regard, 80% of ATM users who withdraw money physically are identified as having high intensity ATM usage pattern amid the COVID-19 pandemic.

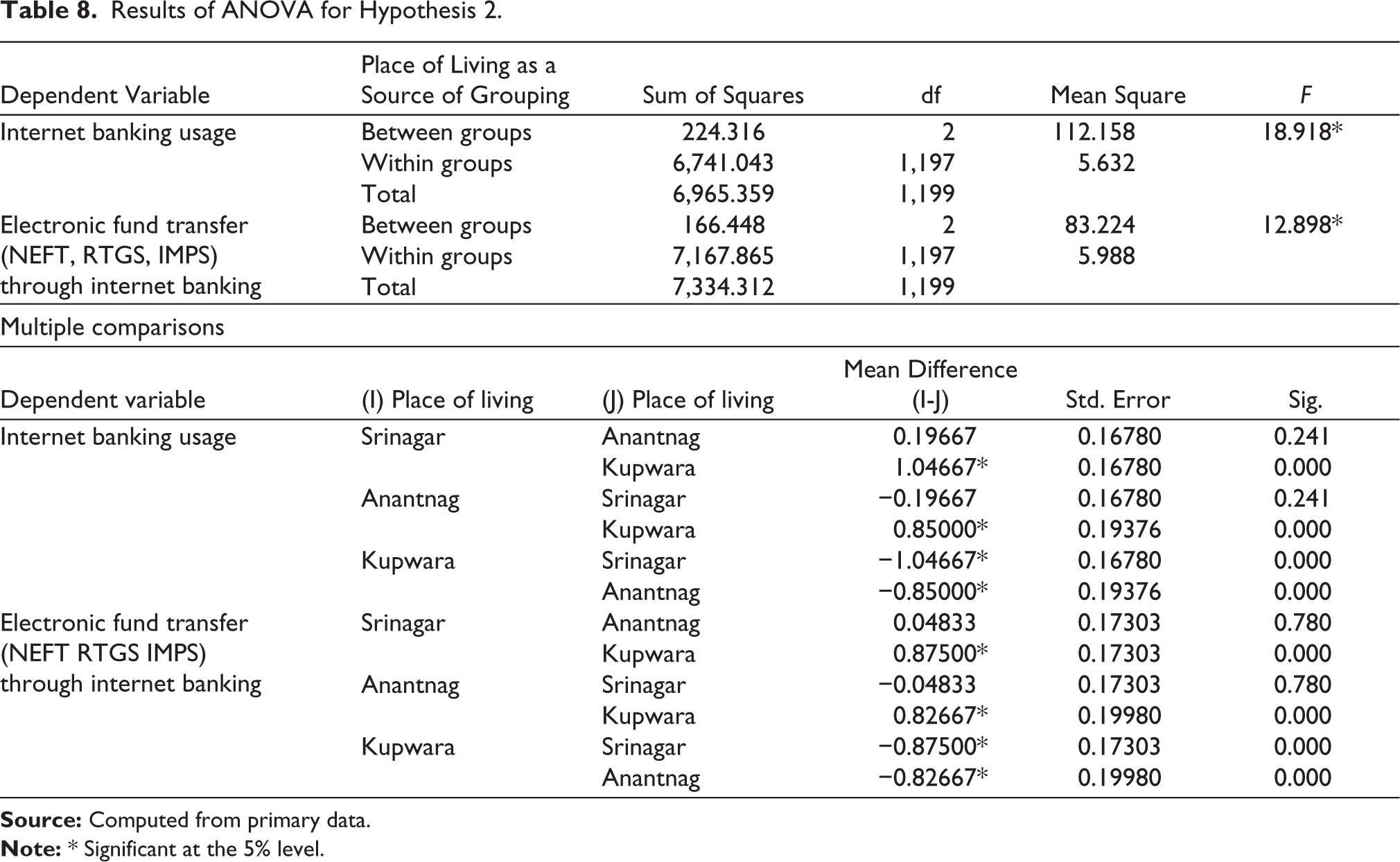

From the results of this one-way ANOVA model shown in Table 8, it can be inferred that the F values of 18.918 and 12.898, corresponding to the intensity of internet banking and electronic fund transfer between the customers of three different banking destinations such as Srinagar, Anantnag and Kupwara, are found to be significant at the 5% level. Hence, hypothesis 2 is rejected at the 5% level of significance. This result clearly shows that there exist significant variations in the usage of online financial services, such as the intensity of internet banking and electronic fund transfers, between the customers of three different banking destinations, such as Srinagar, Anantnag and Kupwara. These propositions established in the present work go in line with the earlier reported findings on online financial services on certain similar types of banking customers geographic relationships. In order to identify the exact variations between different sampling areas, multiple comparisons were made with the LSD method, and its results are provided along with Table 8, where the variations are noted as follows:

Results of ANOVA for Hypothesis 2.

Variations in the Usage Levels of Internet Banking Between Customers’ Banking Destinations

Based on the value of the mean differences found in Table 8, it can be inferred that the highest adoption levels of internet banking are identified with the banking destination of Srinagar, the next highest adoption levels of internet banking are identified with the banking destination of Anantnag and the lowest adoption levels of internet banking are identified with the banking destination of Kupwara. From the details provided in Table 8, it can be noted that the variations in the usage levels of internet banking between the customers from banking destinations of Srinagar and Kupwara are found to be significant at the 5% level. Similarly, such significant variations exist between the banking destinations of Anantnag and Kupwara. These results suggest that the different banking destinations are significantly related to the usage levels of internet banking among the banking customers. These results confirm the earlier reported findings. More specifically, the levels of urbanisation in the banking destinations play a major role in the adoption levels of internet banking applications among the customers.

Variations in the Adoption of Electronic Fund Transfer (NEFT, RTGS, IMPS) Between Customers’ Banking Destinations

Based on the value of the mean differences found in Table 8, it can be inferred that the highest adoption levels of electronic fund transfer (NEFT, RTGS, IMPS) through internet banking are identified with the banking destination of Srinagar, the next highest adoption levels of electronic fund transfer (NEFT, RTGS, IMPS) through internet banking are identified with the banking destination of Anantnag and the lowest usage levels of electronic fund transfer (NEFT, RTGS, IMPS) through internet banking are identified with the banking destination of Kupwara. From the details provided in Table 8, it can be noted that the variations in the usage levels of electronic fund transfer (NEFT, RTGS, IMPS) through internet banking between the banking destinations of Srinagar and Kupwara are found to be significant at the 5% level. Similarly, such significant variations exist between the banking destinations of Anantnag and Kupwara. These results suggest that the different banking destinations are significantly related to the adoption levels of electronic fund transfer (NEFT, RTGS, IMPS) through internet banking among the banking customers. These propositions established in the present work go in line with the earlier reported findings on electronic fund transfer (NEFT, RTGS, IMPS) on certain similar types of banking customers geographic relationships. More specifically, the levels of urbanisation in the banking destinations play a major role in the adoption levels of electronic fund transfer (NEFT, RTGS, IMPS) through internet banking among the customers.

Variations on Internet Banking Adoption Between Banking Customers’ Educational Status

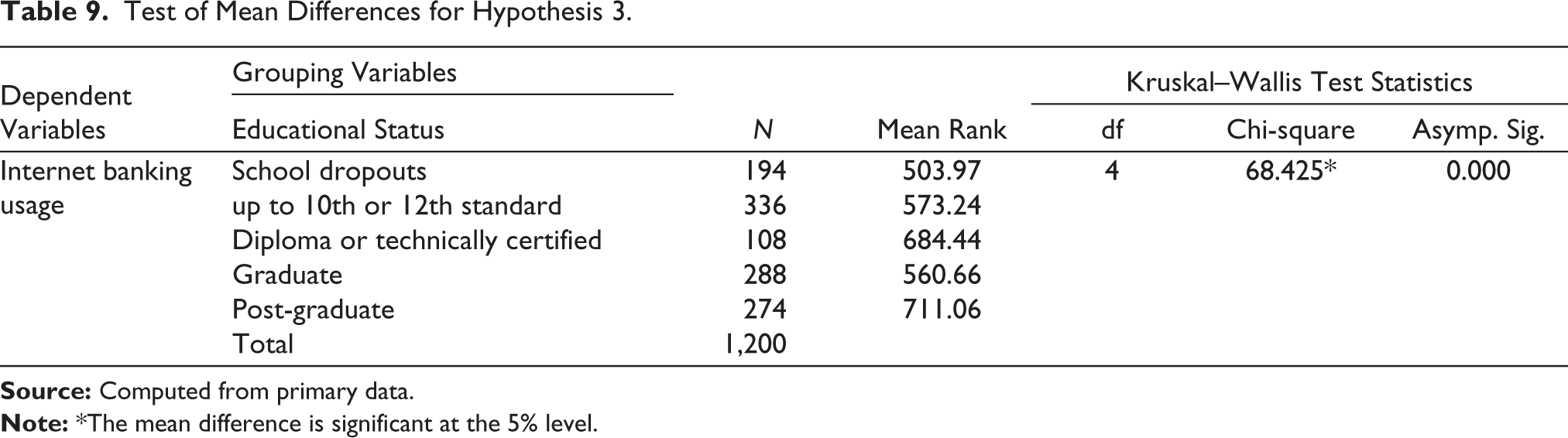

The variation in internet banking adoption between banking customers’ educational status is defined in hypothesis 3, and its results are shown in Table 9 as an outcome of the Kruskal–Wallis test. Since the descriptive details tested for internet banking usage across the five levels of educational status of banking customers are not found to satisfy a normal distribution pattern, the choice of a non-parametric statistical tool is made in this analysis.

To identify the variations in adoption of internet banking, banking customers’ educational status considered for this analysis is classified into the following five levels: school dropouts, up to 10th or 12th standard, diploma or technically certified, graduate and post-graduate. Based on the test results provided, it can be noted that the highest mean rank of 711.06 is obtained for the graduate category of banking customers, followed by diploma or technically certified with a mean rank of 684.44. The third highest mean rank of 573.24 is found with 10th or 12th standard banking customers, followed by graduates with a mean rank of 560.66. The lowest mean rank of 503.97 is obtained for school dropouts. Further, from the results shown in Table 9, it can be inferred that the chi-square value of 68.425 with 4 degrees of freedom has been found to be significant at the 5% level, and hence, hypothesis 3 is rejected. This result clearly shows that there exist significant variations in the usage of internet banking among banking customers’ educational status. These results confirm the earlier reported findings.

Test of Mean Differences for Hypothesis 3.

List of Findings

The major finding made through this work points to the highest adoption levels of ATM usage having the highest variations among other banking functions, with internet banking adoption occupying the third highest level of priority among banking customers. While ATM usage for checking account balances, money transfers and money withdrawals constitute major ATM-related activities for banking customers, physical banking options still remain the major form of customer banking practices, with the second highest adoption levels. The least variation in the adoption of banking functions among banking customers is found with mobile banking usage and the usage intensity of green cards for deposits in banks. As far as the adoption of financial products among banking customers is concerned, the highest adoption levels are found with the availing of loan facilities, followed by availing credit card facilities, availing insurance services and availing mutual fund investments, respectively. The least variation in financial product adoption among banking customers is found with mutual fund investments, followed by insurance services, the availing of loan facilities and availing credit card facilities, respectively.

In the present study, it is explored that banking customers who use ATMs at higher intensity levels for money withdrawal are found to be non-users of internet banking applications amid the COVID-19 pandemic. However, it has been explored that banking customers who visit the bank branch for banking functions were found to be non-users of internet banking applications amid the COVID-19 pandemic. It was found that 94% of banking customers who are mutual fund investors were non-users of internet banking applications amid the COVID-19 pandemic. However, 6% of mutual fund investors are identified as having low usage of electronic banking platforms amid the COVID-19 pandemic. While it was found that 96% of banking customers who were availing of insurance services were found to be non-users of online insurance services amid the COVID-19 pandemic. However, 4% of banking customers who are availing of insurance services are found to be users of online insurance services at low levels amid the COVID-19 pandemic.

It is found that 90% of banking customers who are availing of different categories of loan facilities were non-users of online loan payments amid the COVID-19 pandemic. However, 10% of banking customers who are availing of different categories of loan facilities are found to be users of online loan payments amid the COVID-19 pandemic. Therefore, it is found that 86% of banking customers who are credit card users were non-users of its online management features amid the COVID-19 pandemic. However, 14% of banking customers who are credit card users are found to be using its online management features amid the COVID-19 pandemic. It is found that 80% of banking customers who are debit card users were not using debit cards for online money transfers amid the COVID-19 pandemic. However, 20% of banking customers who are debit card users were found to be using its online management features amid the COVID-19 pandemic.

Significant variations were explored in the usage of online financial services, such as the intensity of internet banking and electronic fund transfers, between the customers of three different banking destinations, such as, Srinagar, Anantnag and Kupwara. The highest usage levels of internet banking are identified with the banking destination of Srinagar; the next highest usage levels of internet banking are identified with the banking destination of Anantnag and the lowest usage levels of internet banking are identified with the banking destination of Kupwara. The highest adoption levels of electronic fund transfer (NEFT, RTGS, IMPS) through internet banking are identified with the banking destination of Srinagar, the next highest adoption levels of electronic fund transfer (NEFT, RTGS, IMPS) through internet banking are identified with the banking destination of Anantnag and the lowest usage levels of electronic fund transfer (NEFT, RTGS, IMPS) through internet banking are identified with the banking destination of Kupwara.

Recommendations

The results of the present study revealed that the majority of banking customers were non-users of technology banking. The reasons why banking customers were not using the technology banking are discussed as follows:

Lack of Awareness

Information Gap: Some customers were not aware of the existence of internet banking or mobile banking services. This could be due to limited communication from financial institutions about these services or the customers not actively seeking information.

Limited Marketing: Financial institutions need to effectively market and promote their digital services to ensure that customers are informed about the benefits and convenience they offer.

Technological Barriers

Access Issues: Certain demographics, particularly those in less developed or rural areas, may face challenges related to technology access. Limited availability of smartphones, computers or reliable internet connectivity can hinder the adoption of digital banking.

Digital Literacy: Customers who are not comfortable using digital devices or lack digital literacy skills may be hesitant to embrace internet banking. Education and training programmes can help bridge this gap.

Security Concerns

Perceived Risks: Some customers may have concerns about the security of online transactions, fearing potential fraud or unauthorised access. Financial institutions must invest in robust security measures and communicate them effectively to alleviate these fears.

Data Privacy Concerns: Worries about the privacy of personal and financial information online can also deter customers. Clear communication about data protection practices can help build trust.

Preference for In-person Transactions

Familiarity and Trust: Some customers might prefer traditional banking methods because of the familiarity and trust associated with face-to-face interactions. Financial institutions could emphasise the security and convenience aspects of digital banking to address these concerns.

Limited Features or Functionality

User-friendly Design: If digital platforms are not user-friendly or lack essential features, customers may find them less appealing. Financial institutions should continually improve their digital interfaces based on customer feedback to enhance the user experience.

Educational Resources: Providing tutorials, guides and customer support can help users navigate digital banking platforms effectively.

Age and Demographics

Generational Divide: Older individuals may be less accustomed to using digital technology. Financial institutions can tailor their outreach to different age groups and provide assistance to older customers during the transition.

Suggestions

The highest usage levels of internet banking are identified with the banking destination of Srinagar, which is a smart city in central Kashmir; the next highest adoption levels of internet banking are identified with the banking destination of Anantnag, which is a district in South Kashmir and the lowest adoption levels of internet banking are identified with the banking destination of Kupwara, which is in North Kashmir near the line of control. Hence, the banking industry should focus most on the customers of backward areas regarding the usage of technological banking.

The present study has examined the situation of electronic banking adoption amid the COVID-19 pandemic, and hence, it is found that maximum customers are non-users of electronic non-financial products. The reason for non-usage of technology banking by majority of customers is a lack of awareness, technological barriers and security concerns. They use physical banking activities and don’t follow social distancing as suggested by the Government of India during March 2020. Therefore, it is the basic responsibility of the banking industry to motivate their customers and address their concerns regarding the usage of electronic non-financial products and electronic financial products, as maximum banking customers are non-users of electronic non-financial products and electronic financial products. If the banking industry will address the concerns of banking customers regarding the usage of technology banking, then only countries like India with a huge population can have technological, environmentally friendly banking and can face situations like the COVID-19 pandemic in the future.

Conclusion

Electronic banking usage is changing the physical usage of non-financial products and financial products worldwide. Today, the click of the mouse and mobile banking offer a lot of transactions regarding electronic non-financial products and electronic financial products. Still, the adoption rates of electronic non-financial products and electronic financial products are very low. It can be also inferred that during the COVID-19 pandemic situation, to follow social distancing, it became important for every citizen to use electronic banking platforms, but unfortunately, the majority of customers were found to be non-users of electronic banking platform transactions and instead of electronic banking platforms, they chose physical banking, which became a risk factor for the transmission of the coronavirus. The reason for non-usage of technology banking by the majority of customers is lack of awareness, technological barriers and security concerns. They use physical banking activities and don’t follow social distancing as suggested by the Government of India during March 2020. Therefore, it is the basic responsibility of the banking industry to motivate their customers and address their concerns regarding the usage of electronic non-financial products and electronic financial products, as maximum banking customers are non-users of electronic non-financial products and electronic financial products. If the banking industry will address the concerns of banking customers regarding the usage of technology banking, then only countries like India, with a huge population, can have technological, environment-friendly banking and can face situations like the COVID-19 pandemic in the future.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.