Abstract

The case study is based on Saudi Aramco, the largest state-owned oil company of the Kingdom of Saudi Arabia (KSA), which has become a world leader in hydrocarbons exploration, production, refining, distribution and marketing. The study analyses the organization’s strategies, product lines, domestic and global operations, key performance, recent initiatives for an IPO, and role in economic development and politics of the kingdom in the backdrop of global oil market. Through a combination of own facilities and joint ventures, Aramco produces a slate of refined products and high-value petrochemicals for domestic and international industries. The partnerships of the company with refining and marketing ventures across the globe has enabled it to go across the length of its value chain, from wellhead to the consumers. The separation of its operational decision-making and financial structure from the state intervention is one unique characteristic which might be linked to its sound financial performance and organizational excellence. On the other hand, the delay in its IPO indicates the possible problems that might arise from this influence.

Introduction

Fossil fuels, especially oil, have been the driver of industrialization and trade across the world (O’Sullivan & Sheffrin, 2003). Consequently, oil has affected the economic dimensions, political agenda and even culture of countries for more than a century (Berument, Ceylan, & Dogan, 2010; Bronson, 2008; Holdren, 2006; Jones, 2012). The Kingdom of Saudi Arabia (KSA) has emerged as a major regional player and a significant global one because of its ability to influence the price of oils. It is the largest oil producer and exporter (Cashin, Mohaddes, Raissi, & Raissi, 2014) with 18 per cent of the world’s proven petroleum reserves (OPEC, 2018a). However, there has been a controversy about the economy’s present and future oil capabilities (Al-Saleh, 2009). The KSA affects the world oil market by its national oil company (NOC) Saudi Aramco, that has remained number one in the Petroleum Intelligence Weekly’s annual world oil company ranking since the ranking began in 1988 (Energy Intelligence, 2015; Kobayashi, 2007). The reason for success of such enterprises might lie in their profit and market-oriented management, which is autonomous in daily operations; on the other hand, they receive protection from the government and clear directions from ‘a limited number of elite players’ (Hertog, 2010). Based on this theoretical framework, the objective of the case study is to analyse the business model and strategies of Saudi Aramco to understand how it is able to meet its financial goals, along with performing its social and national responsibilities. The study has been organized as follows: The next section presents the world oil market along with the impacts of OPEC and position of KSA in it. The third section explores Aramco’s strategies, activities, product lines, domestic and global operations, and key performance, while the fourth discusses its efforts targeted to economic development and politics of the KSA, with profound qualitative analysis. The last section discusses future planning of the organization in the backdrop of opportunities and challenges, before concluding the study with implications.

An Overview of the Global Oil Market

Currently, fossil fuels, namely, oil, gas and coal, hold a dominant position in global energy mix and are expected to retain this dominance in future, though with a declining share. Together oil and gas will meet more than half of the global energy needs, with 52 per cent share, during 2016–2040 (World Oil Outlook, 2017). The world oil reserves are unevenly distributed between 70,000 fields, among which 507 fields are classified as giant and account for 60 per cent of conventional oil production, while the top 110 producing fields generate over 50 per cent of global supply (Owen, Inderwildi, & King, 2010). Nonetheless, the total volume of oil reserves has been contradictory, since different sources have measured it in different ways (Owen et al., 2010).

OPEC’s Influence

The Organization of the Petroleum Exporting Countries (OPEC) is an inter-governmental body created at the Baghdad Conference in 1960 by Iran, Iraq, Kuwait, Saudi Arabia and Venezuela (OPEC, 2018b). The five founding members were later joined by Qatar (1961), Indonesia (1962), Libya (1962), the United Arab Emirates (UAE; 1967), Algeria (1969), Nigeria (1971), Ecuador (1973), Gabon (1975), Angola (2007) and Equatorial Guinea (2017). Currently, with 14 member countries, 1 OPEC focuses on coordinating and unifying petroleum policies among its members, in order to secure fair and stable prices for petroleum producers; and an efficient, economic and regular supply of petroleum to consuming nations (OPEC, 2018b). When OPEC was formed, the global oil market was dominated by the Seven Sisters 2 multinational companies. The members of the Seven Sisters controlled around 85 per cent of the world’s petroleum reserves. With the weakening stronghold of the Seven Sisters, creation of OPEC by oil-exporting states, as well as the Arab oil embargo after Arab–Israeli war in 1973, oil prices jumped from US$2.50 a barrel in 1972 to about US$12 a barrel in 1974. Eager to capture the window of opportunity, governments in many developing countries expropriated the foreign oil firms operating in their geographic territory. Since then, industry dominance has shifted to the OPEC cartel and state-owned oil and gas companies in emerging-market economies, such as Saudi Aramco (Saudi Arabia), Gazprom (Russia), China National Petroleum Corporation (CNPC, China), National Iranian Oil Company (NIOC, Iran), PDVSA (Venezuela), PETROBRAS (Brazil) and PETRONAS (Malaysia). These state-owned firms control almost one-third of the world’s oil and gas production and hold more than one-third of its total oil and gas reserves (Hoyos, 2007). During the 1970s, OPEC rose to international prominence in supporting the oil sector, as its member countries took control of their domestic petroleum industries and played a major role in pricing of crude oil in world markets. The cartel introduced a group production ceiling divided among the member nations and a Reference Basket for pricing, as well as significant progress with OPEC/non-OPEC dialogue and cooperation, which was essential for market stability and reasonable prices in this decade. An innovative OPEC oil price band mechanism helped strengthen and stabilize crude prices in the early 2000s. However, a combination of market forces, speculation and other factors transformed the situation in 2004, by pushing up prices and increasing volatility in a well-supplied crude market. Trade patterns has continued to shift, with demand growing further in Asian countries and shrinking in the Organization for Economic Co-operation and Development (OECD). 3 With the growing global focus on multilateral environmental issues and expectations for a new UN-led climate change agreement, OPEC continues to seek stability in the market, and plans to further improve its dialogue and cooperation with consumers and non-OPEC producers (OPEC, 2018c).

Demand, Supply and Price Fluctuations

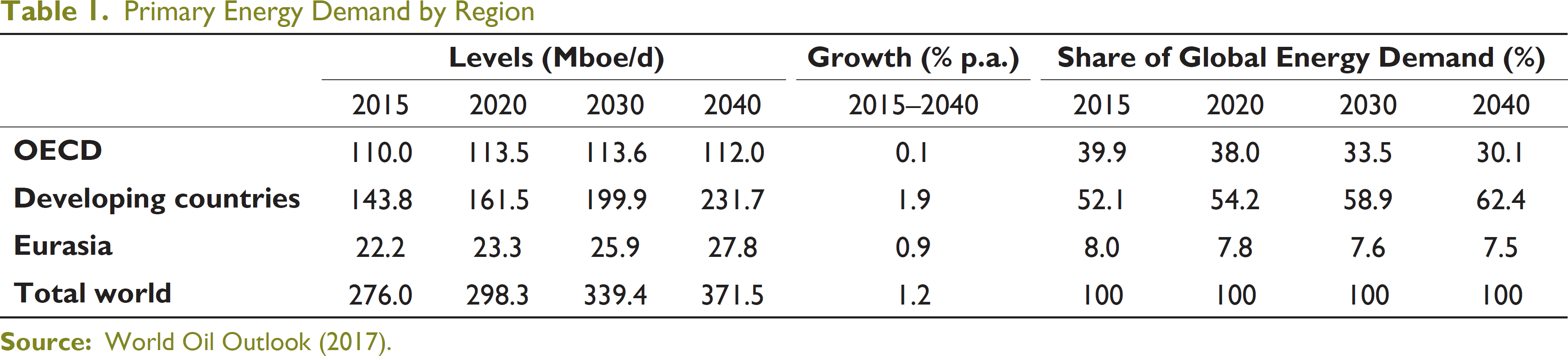

The global demand for primary energy has been forecasted to increase by 40 per cent, rising from 276 Mboe/d in 2015 to 372 Mboe/d by 2040. Developing countries’ energy demand will rise by 1.9 per cent per annum (p.a.) compared to that of 0.1 per cent and 0.9 per cent in the OECD regions and Eurasia, respectively, as shown in Table 1 (World Oil Outlook, 2017). The overall oil demand in medium term, that is, 2016–2022, is predicted to increase from 95.4 mb/d to 102.3 mb/d; during the long term, the demand is expected to further increase from 15.8 mb/d to 111.1 mb/d in 2040. Nevertheless, the overall demand has been forecasted to decelerate steadily to a level of 0.3 mb/d every year between 2035 and 2040, resulting from decreasing population and GDP growth; structural shift of the global economy; along with efficiency improvements and fuel switching by energy policies and/or technological improvements, specifically in the road transportation sector (World Oil Outlook, 2017).

Primary Energy Demand by Region

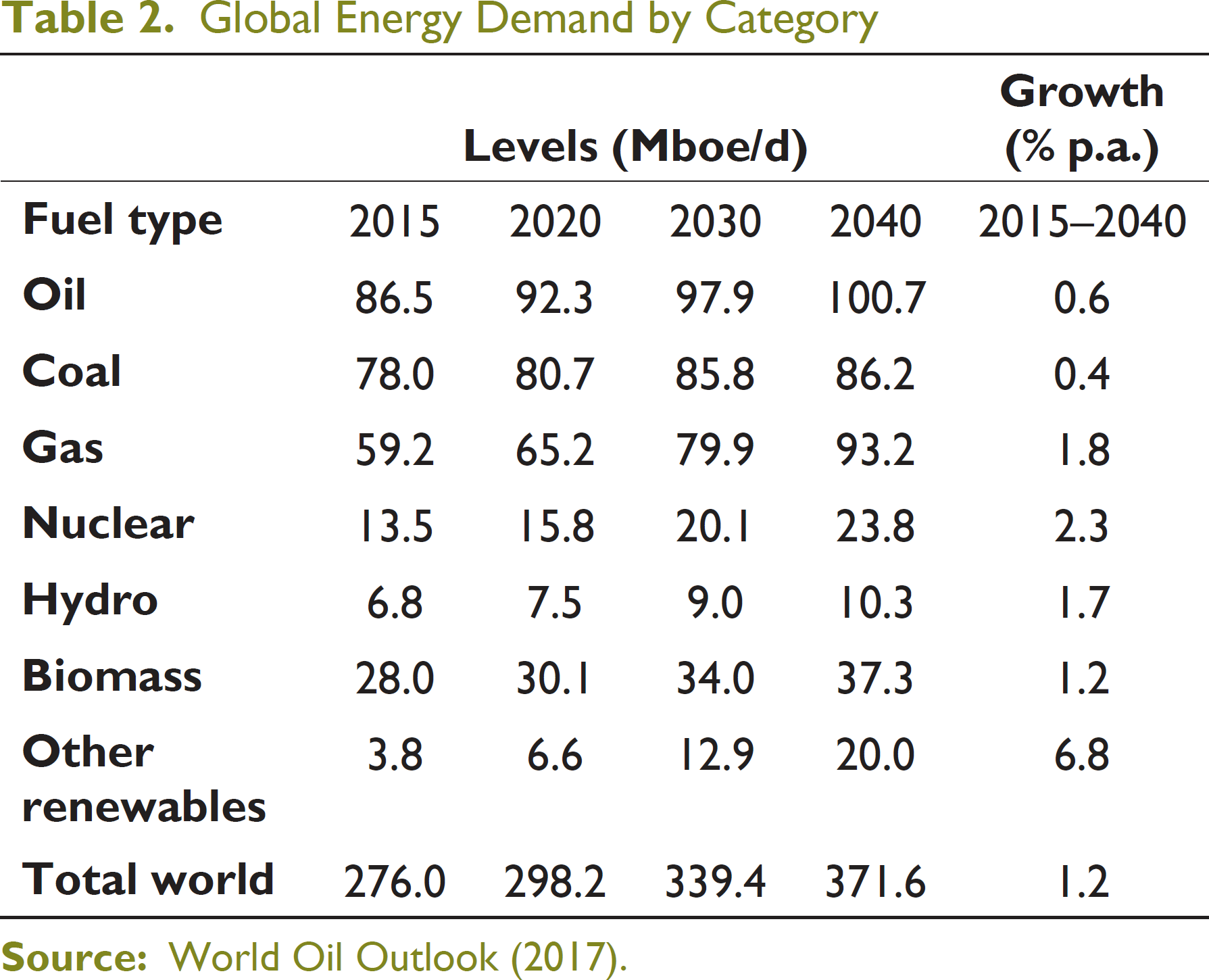

The largest contributor to the global energy mix will be natural gas; its demand is expected to increase by almost 34 Mboe/d, reaching a level of 93 Mboe/d by 2040, as shown in Table 2. The fastest growing energy category is other renewables, mainly wind, photovoltaic, solar and geothermal energy, which has been projected to have an average annual growth rate of 6.8 per cent (World Oil Outlook, 2017).

Global Energy Demand by Category

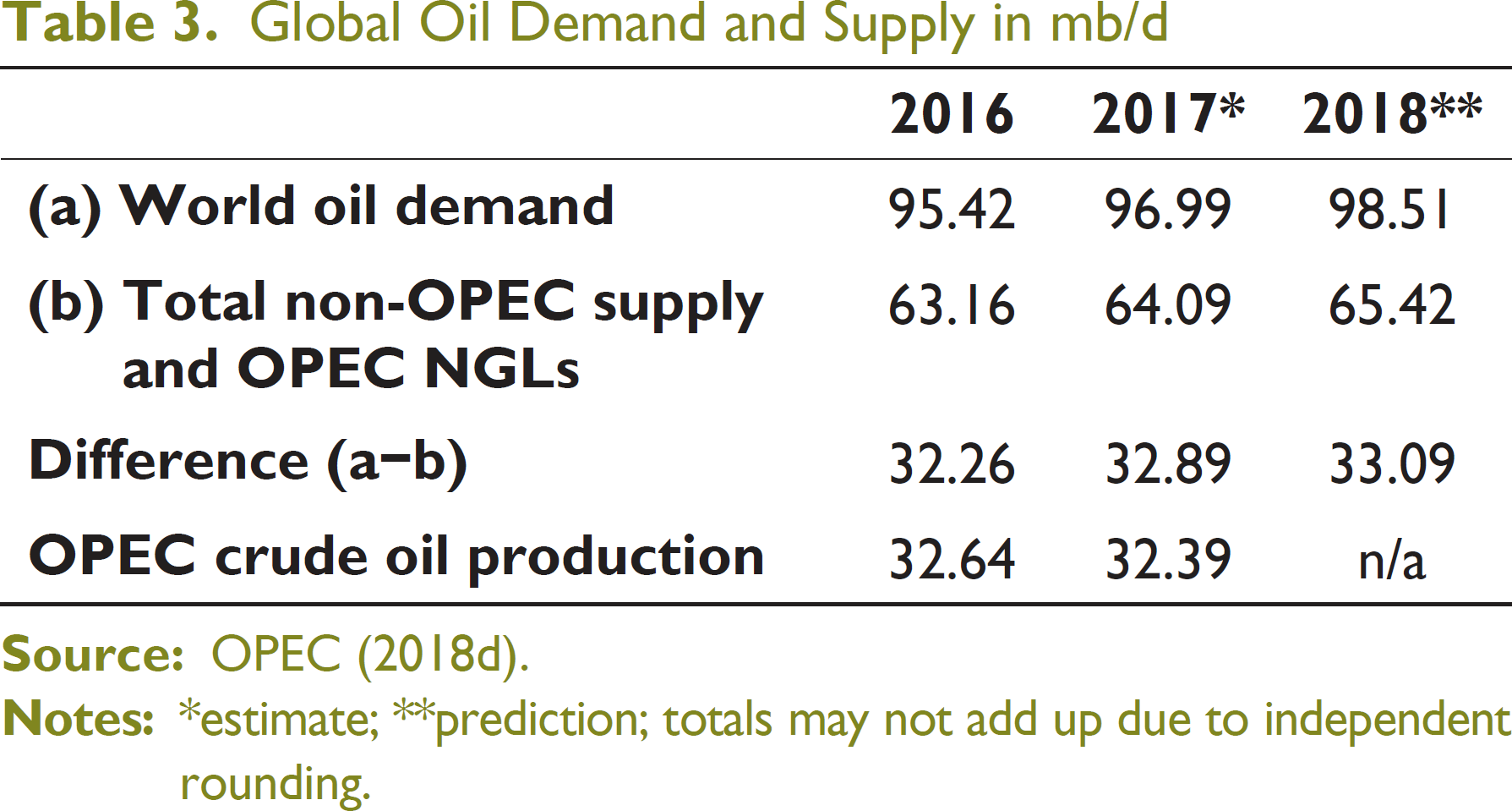

On the other hand, global oil supply will reach 58.94 mb/d during 2018 (OPEC, 2018d); supply from OECD countries will experience the largest growth, increasing from 1.28 mb/d to become 26.80 mb/d, whereas supply from developing countries is expected to grow to 12.05 mb/d from 11.91 mb/d in 2017. The forecasted demand–supply is presented in Table 3.

Global Oil Demand and Supply in mb/d

Oil is produced around the globe at differing quality and with varying costs. While there are over a thousand types of crude oil, the price of a barrel varies considerably depending on its origin. Previous studies propose that the oil price shocks and supply disruptions have significant impacts on global economy (e.g., see, Farzanegan & Markwardt, 2009; Hamilton, 2009; Kilian, 2008). Furthermore, the price of oil has gone through many ups and downs with time. The crude oil price in the 1970s had been as high as over US$40 a barrel, then became very volatile after a sharp decline in the 1980s and remained low at US$20 a barrel at the end of 2001. Within the next six years, real oil price tripled turning the nominal price to an all-time high of US$145 a barrel in mid-2008, only to be followed by an even more severe collapse (Hamilton, 2009) because of global financial turmoil and economic recession. Escalating social unrest in many parts of the world affected both supply and demand throughout the first half of the current decade, although the market remained relatively balanced. Prices were stable between 2011 and mid-2014, until a combination of speculation and oversupply caused them to fall in 2014. Members of OPEC and other oil-producing nations reached an agreement to collectively reduce their daily output by 1.8 million barrels at the end of 2016; the mutual effort to cut production/exports, however, did not affect oil prices immediately for a number of reasons. One such reason is that the cartel still exported at high levels, much of which came from Libya and Nigeria, two countries exempted from the cuts (Cunningham, 2017). Finally, the oil prices have started to go up slowly in 2017, whereas the trend is expected to continue in 2018.

Saudi Arabia: The State of Oil

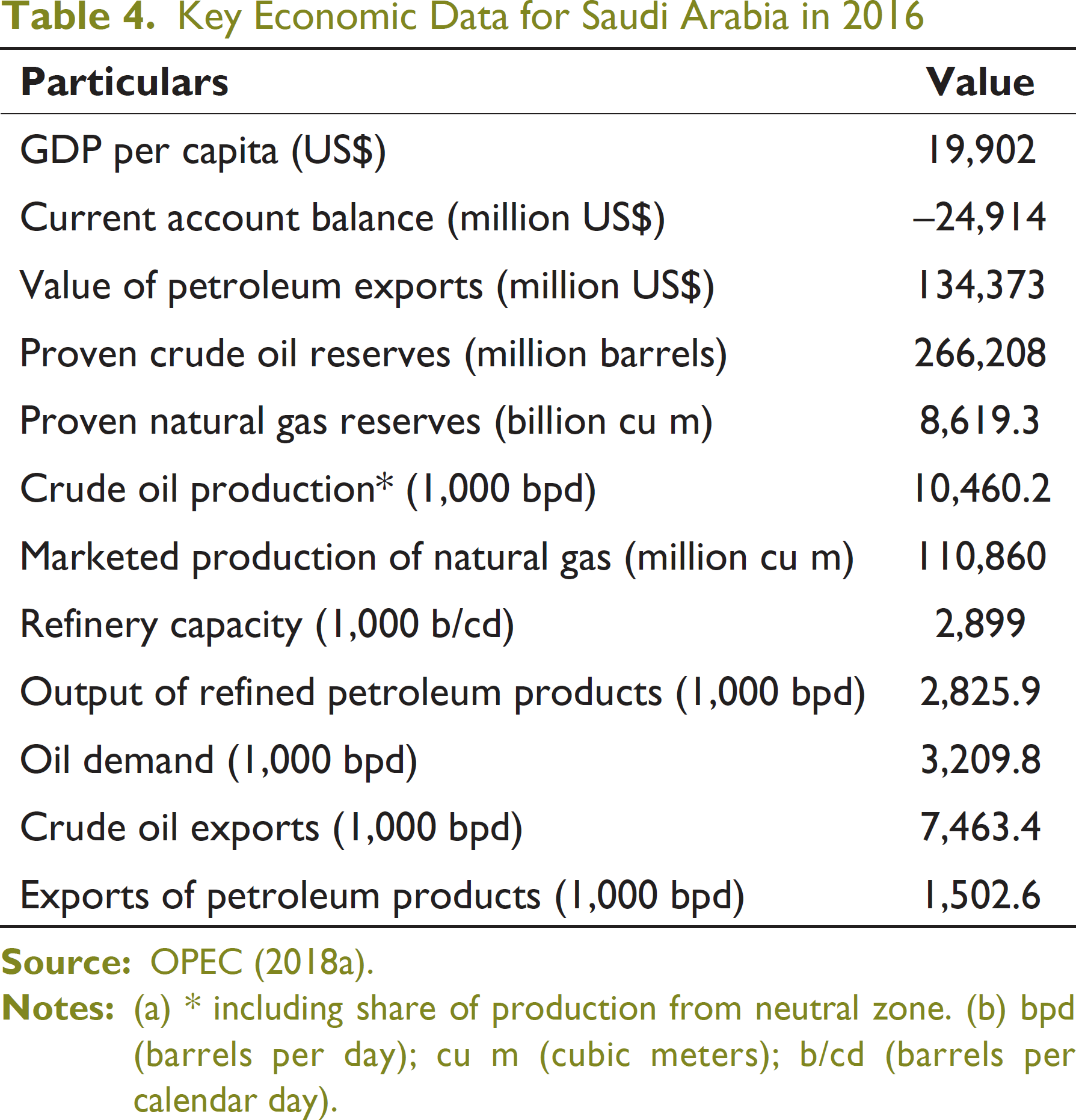

Oil was first discovered in the KSA, the second largest OPEC member country, in Dammam oilfield in 1938 (OPEC, 2018a). The oil and gas sector accounts for about 50 per cent of the economy’s GDP and about 85 per cent of export earnings. Table 4 highlights the macro-economic performance of the state. KSA also has the largest spare capacity and, thus, is regarded as a ‘global swing producer’ (Cashin et al., 2014). The economy has historically played a pivotal role within OPEC using its policy of maintaining spare capacity (Fattouh & Harris, 2017). Besides, it has become unique to provide incremental oil supplies during major emergencies, accidents or disruption of global supply. After the KSA had joined the World Trade Organization (WTO) in 2005, further trade opportunity was created for its petrochemical industry, particularly for exporting to China. Nonetheless, its rich geology has proven both a blessing and curse for the kingdom.

Key Economic Data for Saudi Arabia in 2016

The economy is oil-based with energy-intensive sectors, such as industry, building and transport. In addition, its domestic oil consumption has grown rapidly in the past four decades; with a ninefold increase, it grows at 5.7 per cent annually (Gately, Al-Yousef, & Al-Sheikh, 2012). In order to reduce its dependency on oil industry, the government has taken initiatives to promote the non-oil sectors by diversifying into power generation, telecom, natural gas exploration and petrochemical over the last two decades (Samargandi, Fidrmuc, & Ghosh, 2014). However, the economy, together with the non-oil private sectors, still relies on government spending that is fuelled by oil revenues. Additionally, its industrial and diversification strategy has primarily been based on developing energy intensive industries, and adding value by extending the value chain to refining, petrochemicals and industrial parks (Fattouh & Harris, 2017). An abundance of oil has also inhibited its democratizing trends through effects such as taxation, spending, repression and modernization (Ross, 2001, 2012). Likewise, oil wealth leads to authoritarianism, economic instability, corruption and violent conflict (Karl, 2004). The fast pace of urbanization and an unprecedented expansion of the government’s role for economic development have turned the KSA into a ‘rentier-corporatist’ state 4 (Ehteshami & Wright, 2007), while the nation has a long way to go to introduce liberal reformation (Brumberg, 2002).

Saudi Aramco: The Organization

Saudi Aramco has become a world leader in hydrocarbons exploration, production, refining, distribution and marketing over the past 80 years with average daily crude production at 10.5 million bpd and natural gas reserves at 298.7 trillion scf (Saudi Aramco, 2018a). Its major export shipping terminals are located at ports on the Arabian Gulf and Red Sea, while domestic demand is met through a kingdom-wide network of strategically situated refineries. Aramco is headquartered in Dhahran, Saudi Arabia, and has operations throughout the kingdom. The organization employs more than 65,000 workers worldwide. Its subsidiaries and affiliates are located in China, Egypt, Japan, India, the Netherlands, the Republic of Korea, Singapore, the UK as well as the USA.

Origin, Vision, Mission and Strategies

Aramco’s origin can be traced back to the oil shortages of the First World War and the exclusion American companies from Mesopotamia by Great Britain and France under the San Remo Oil Agreement of 1920. The US Republican administration had initiated an Open Door policy in 1921, and consequently, SoCal was among the US firms seeking new sources of oil from abroad. Through its subsidiary company, the Bahrain Petroleum Co (BAPCO), SoCal struck oil in Bahrain in 1932. This event heightened interest in the oil prospects of the Arabian mainland. In 1933, an oil concession agreement was signed between KSA and SoCal. California Arabian Standard Oil Company (CASOC), a subsidiary company, was created to manage the concession in the same year. The first test well was drilled at Dhahran in 1935. In 1936, Texas Oil Co (Texaco) purchased a 50 per cent stake of the concession. Its first success came with the seventh drill site in Dhahran in 1938. This well immediately produced over 1,500 bpd, giving the company confidence to continue. To more accurately reflect the KSA’s new-found prominence among oil-producing nations, the name of the company was changed to Arabian American Oil Company, Aramco, in 1944 (Jaffe & Elass, 2007).

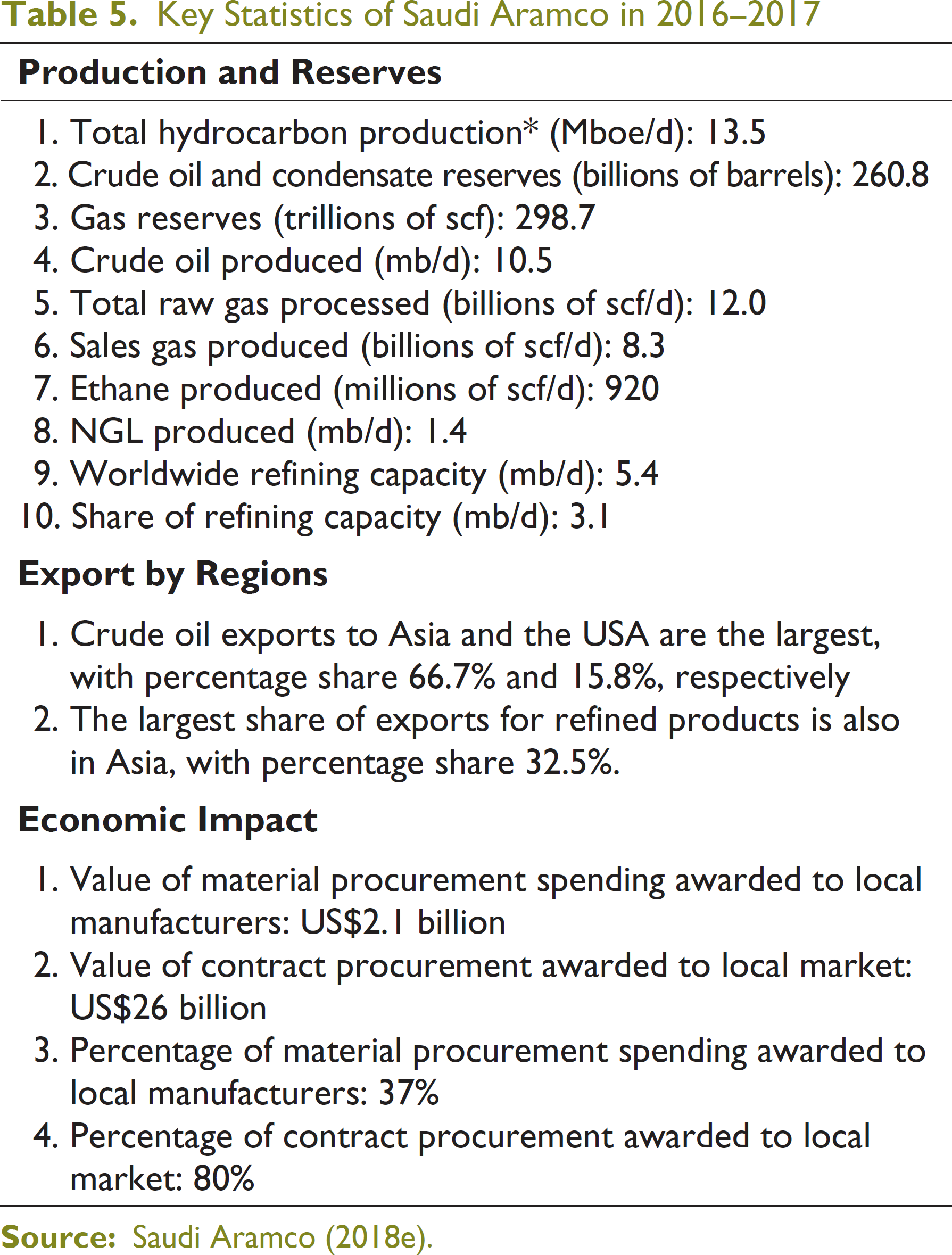

The KSA government wanted to nationalize the oil facilities of the kingdom in 1950, thus pressuring Aramco to agree to share profits by a 50:50 ratio. The government bought a 25 per cent participation interest in Aramco in 1973, increasing it to 60 per cent the following year. In 1980, it increased its participation interest in Aramco’s crude oil concession rights, production and facilities to 100 per cent. In November 1988, the council of ministers approved a charter for a new national oil enterprise—the Saudi Arabian Oil Company (Saudi Aramco). A royal decree was issued to change the name and take over the management and operations control of the KSA’s oil and gas fields from previous Aramco and its partners. Initially, the company had not planned on refining oil. As the government wanted to have only one company dealing with oil production, a royal decree was sanctioned to merge the operation and facilities of Samarec into Aramco in 1993. Headquartered in Jiddah, Samarec was responsible for refining, international product marketing and distribution of petroleum products throughout the KSA. The following year, an Aramco subsidiary acquired a 40 per cent equity interest in Petron Corp, the largest crude oil refiner and marketer in the Philippines. Since then, Saudi Aramco has taken on the responsibility of refining and distributing oil in the KSA. In 1951, the company discovered the Safaniya oilfield, the largest offshore field of the world that time. Later in 1957, the discovery of smaller connected oil fields confirmed the Ghawar field as the world’s largest onshore field, with reserves estimated at 80 billion barrels. Aramco has continued to excel in organizational performance to become the world’s leading integrated energy and chemicals enterprise, a top refiner and a creator of energy technologies, with its core mission of being the reliable supplier of energy to the kingdom and the world. From producing approximately one in every eight barrels of the global crude oil supply, the company is driven by its core belief that energy is opportunity. As the global population grows, economies expand and standards of living increase, energy is an essential enabler of opportunity. With strategic intent: ‘In 2020, Saudi Aramco is the world’s leading integrated energy and chemicals company, focused on maximizing income, facilitating the sustainable and diversified expansion of the Kingdom’s economy and enabling a globally competitive and vibrant Saudi energy sector’, the organization functions are guided by corporate values: integrity, safety, accountability, excellence and citizenship. Vertical integration has been one of Aramco’s consistent strategies. Having sophisticated refining capacities within its own network enables the company to turn low quality crude oil grades to more value-added petroleum products (Saudi Aramco, 2018c). Key performance indicators of Saudi Aramco are presented in Table 5.

Key Statistics of Saudi Aramco in 2016–2017

Core Activities and Product Line

The oil operations of Saudi Aramco take place over a vast region spanning 1.5 million sq. km, and cover all areas of the kingdom, including the territorial waters of the Arabian Gulf and Red Sea. Its major facilities are Abqaiq, Haradh, Khurais, Khursaniyah, Manifa, Nuayyim, Qatif, Shaybah, etc. Through effective planning and cutting-edge technology, Aramco continues to find new fields, add reserves and develop more efficient methods to produce and process oil and gas. Most of its gas and oil exploration takes place at the Exploration and Petroleum Engineering Center (EXPEC). Aramco Research Center in Houston works on upstream technologies for conventional and unconventional resources to support the organization’s discovery and recovery goals. The company plans to invest about U$40 billion in a year over the coming decade to strengthen its upstream and downstream businesses by sustaining its oil production capability at 12 million bpd and creating spare production capacity of 2 million bpd. It has recently signed agreements worth nearly US$4.5 billion with several oil and gas service contractors to design oil and gas megaprojects with the target of enhancing the company’s energy sustainability, diversify the Saudi economy and expand gas production in the KSA. In addition, Aramco emphasizes on creating and implementing ideas, such as, offering reliable access to affordable energy, reducing carbon dioxide emissions, realizing more fuel-efficient vehicles and conserving water resources. Since Dammam Well 7 began producing commercial quantities of crude oil, the core product line of Aramco has been crude oil. The current product portfolio of Saudi Aramco includes gasoline, diesel, crude oil, sulphur, LPG, propane, butane, natural gasoline (NG), gas, ethane, kerosene, fuel oil, paving asphalt, etc. Additionally, its affiliates supply quality Group I, Group II and Group III base oils around the world. Its fully owned subsidiary Saudi Aramco Trading Company (ATC) focuses on trading petroleum products with to integrate base oil producing affiliates and develop global base oil product slates under the Saudi Aramco brand, so that the organization can meet 14 per cent of global base oil demand. Aramco has also created a subsidiary company, Vela International Marine, to handle shipping to North America, Europe and Asia.

Operational Partnership

Strategic collaboration is at the core of Aramco’s business model. Through a combination of wholly owned facilities and joint ventures, Saudi Aramco produces a slate of refined products and high-value petrochemicals for consumers as well as industries, both domestic and international.

The construction of Saudi Aramco Total Refining and Petrochemicals Company (SATORP), a joint venture between Saudi Aramco and Total (France), has been completed in 2013. The company has a Saudization rate of nearly 65 per cent. The SATORP refinery is also the first producer of petroleum coke and paraxylene in the Kingdom.

Yanbu Aramco Sinopec Refining Company (YASREF) is a joint venture with Sinopec (China). This world-class petroleum refinery, with capacity of 400,000 barrels per day, is located in Yanbu Industrial City (Saudi Aramco, 2018b).

Rabigh Refining and Petrochemical Company (Petro Rabigh) is Aramco’s integrated refining and petrochemical venture with Sumitomo Chemical (Japan). It also contains the Technical Learning Academy to train young operators and equip the Saudi workforce with advanced skills. Aramco has continued its partnership with Sumitomo in marketing and construction activities for the RabighPlus Tech Park, an industrial zone integrated with Petro Rabigh where manufacturers can establish factories to create products from the petrochemical feedstock produced in the latter.

Jazan Refinery and Terminal with 400,000 bpd refinery and terminal facilities will be the industrial heart of the Jazan Economic City project. It is also the part of a broad plan to drive sustainable economic development in the kingdom along with to create employment opportunities for Saudis.

Sadara Chemical Company is a joint venture with Dow Chemicals Company and one key element of Aramco’s intent to become a leading global chemicals producer. Located in Jubail Industrial City, Sadara has the capacity of producing 3 million tons of performance plastics and high value chemicals every year. The company commenced its production in 2015. Sadara and its integrated PlasChem value park will become a hub for chemical conversion plants, manufacturer and associated service industries. The project is expected to enhance the kingdom’s capability in producing diversified chemical commodities and create direct and indirect jobs for the Saudis (Saudi Aramco, 2018b, 2018c).

Global Presence

The partnerships of Aramco in refining and marketing ventures in China, Japan, South Korea and the USA has enabled the company to go across the length of its value chain, from wellhead to the consumers.

In the Fujian Province, the company has an equity ownership in a joint venture called Fujian Refining and Petrochemical Company Limited (FREP) with ExxonMobil, China, Petroleum and Petrochemical Company Limited (Sinopec) and the Fujian provincial government. To serve its Chinese crude oil clients better, Aramco has expanded its Asian headquarters in Beijing and branch offices in Shanghai, Xiamen and New Delhi. It has also established Beijing Research Center in 2015. Currently, its crude oil exports account for nearly 10 per cent of China’s demand (Saudi Aramco, 2018b).

The investment of Aramco in S-OIL (South Korea), one of the country’s leading refiners, complements its downstream ventures in China and Japan and creates new opportunities along the value chain in the major energy markets in Asia.

In 2015, Aramco signed an agreement with PT Pertamina, the NOC of Indonesia, to formalize key business principles for the joint ownership, operation and upgrade of the Cilacap Refinery located in Indonesia. The proposed upgrade is expected to allow the refinery to process more sour crude oils, meet high-quality product specifications and produce basic petrochemicals and lubricant base oils (Saudi Aramco, 2018d).

Management and Leadership in Aramco: Roles and Responsibilities

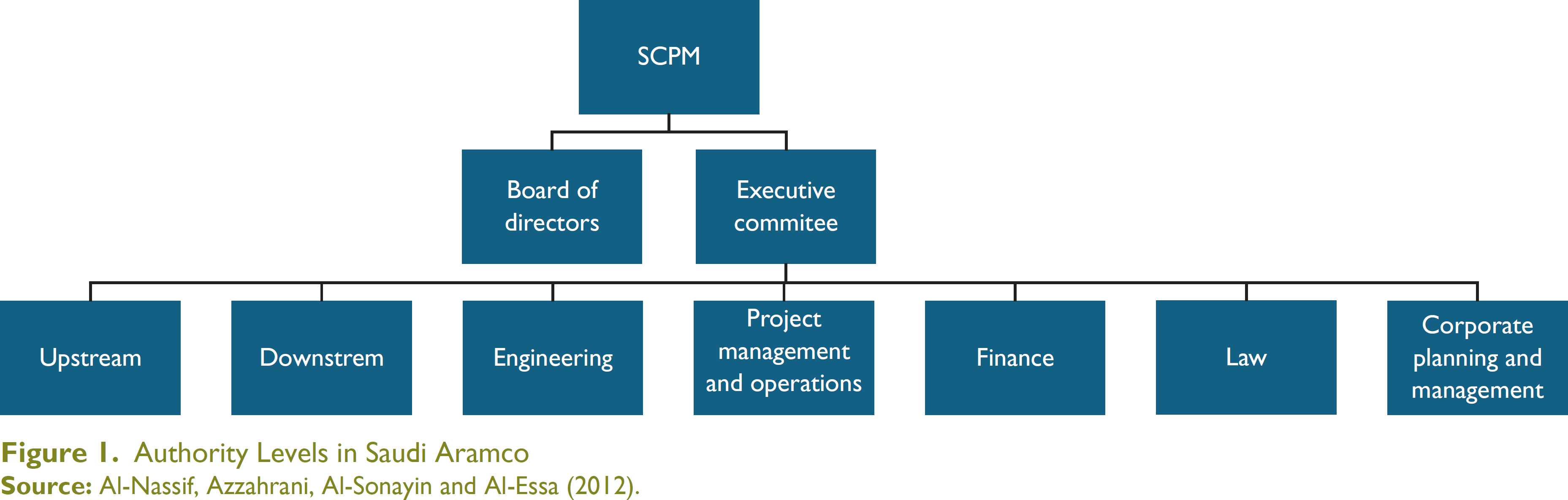

The management is organized in different levels (as shown in Figure 1). The Supreme Council for Petroleum and Mineral Affairs (SCPM) is the highest authority and consists of members from both the government and private sector. The second level of authority, the board of directors, is chaired by the minister of petroleum and mineral resources. The board is responsible for long-term planning, budgeting and decision-making, along with the company’s executive management committee, which is headed by the king and chief executive officer (CEO). Next, the large organization is divided into seven business lines, upstream operation, downstream operation, engineering, project management and operations, finance, industrial relations and law, and corporate planning and management. These are headed by the senior vice presidents, each delegated with the authority to plan and manage the activities in their own business function.

Aramco’s culture is a paradox between American multinational and local Saudi. Unlike the American, Saudi society is characterized by formality and hierarchy, in which individual initiative is not encouraged and group loyalty is considered very important. One reason for existing balance could be that Saudi executives, in the combination of American and Saudi managers, took the reins in less than a decade, after the government had purchased the business (The New York Times, 2018). Its present culture promotes innovation, research and development (R&D) as well as development of human capital. It also invests in new technology that can deliver greater levels of operational efficiency, enhanced performance and environmental benefits. A good example is Aramco’s R&D effort on improving oil use efficiency in the transportation sector that currently accounts for one-fifth of the global primary energy demand, and the share is anticipated to increase by 30 per cent–40 per cent within 2040 (Saudi Aramco, 2015).

The Integration between Financial Goals and National Obligation

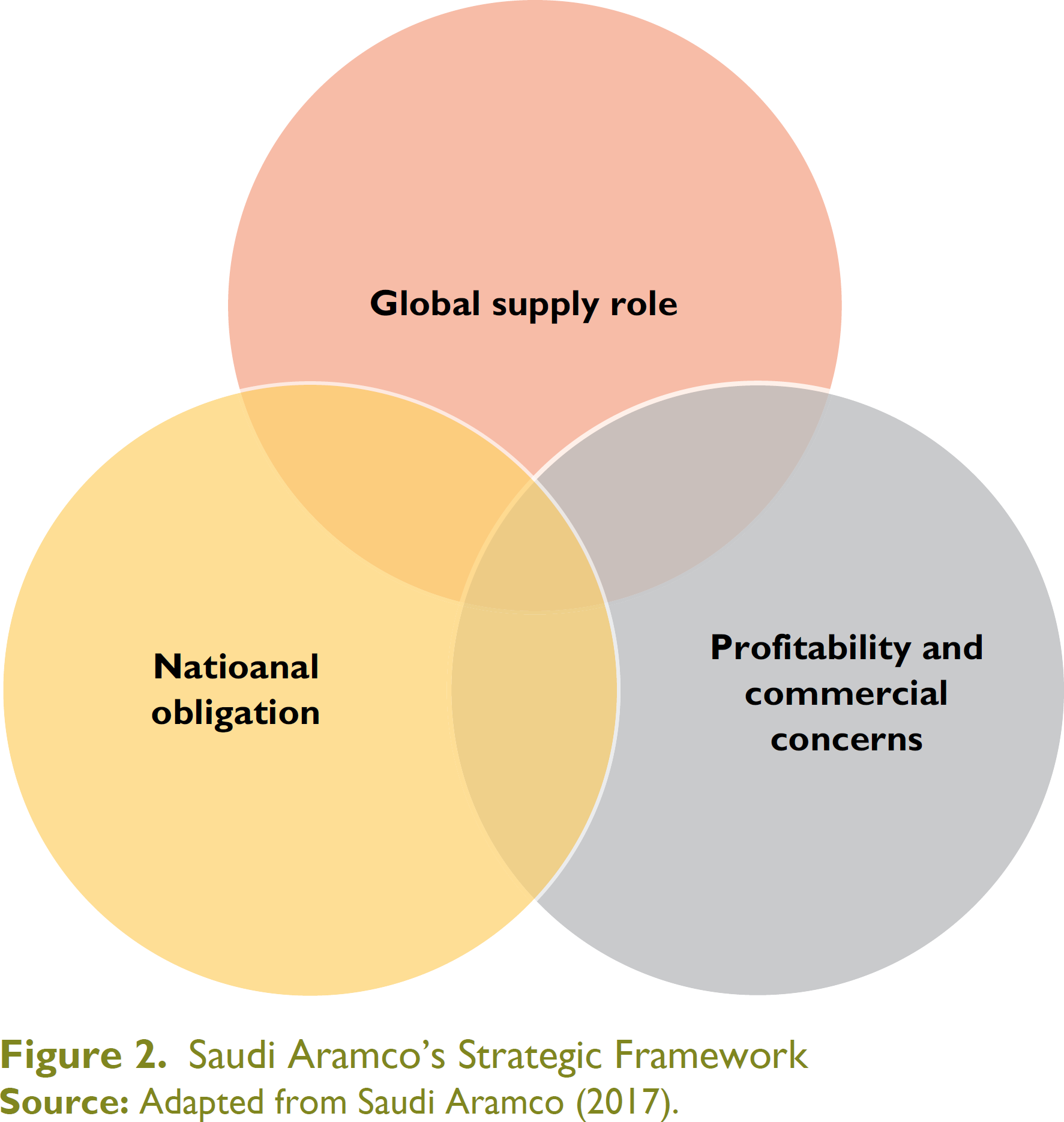

The strategic framework of Aramco (as shown in Figure 2) indicates corporate strategies focus on three prominent factors: (a) global supply roles, which include target markets, logistics, spare capacity, crude grades, refining and petro-chemicals, and so on; (b) national obligation covers both social responsibility and economic development; and (c) profitability and commercial concerns, such as corporate governance, value addition, cost management, etc.

The Saudi government decides the OPEC policy, oil production levels, capacity targets and domestic petroleum prices of the kingdom. Besides, the SCPM sets the broad policy and objectives of the company. In addition to SCPM, the Saudi Ministry of Petroleum and Mineral Resources is in charge of setting the policies and strategic objectives for the oil and gas industry of the kingdom and serves as its energy sector regulator. Moreover, the ultimate authority for all decisions related to oil and gas policy rests with the King of Saudi Arabia. As oil policy has such an enormous effect on the economy of the kingdom, it is set by consensus among the influential ruling family members after considerable consultation with experts in related fields. Conversely, Aramco can make decisions regarding the expenditure, investment project and other operational issues (Kobayashi, 2007). This clear separation makes the company’s relationship with the government uniquely amicable, ensures its operational autonomy and minimizes political interventions in its operational activities. One advantage Aramco has over other NOCs is that the company controls its own operating revenue by paying royalties and dividends from its earning to the state. Retained earnings are utilized to finance the organization’s usual operations. This independent fiscal structure and a rich corporate culture, inherited from its American origin, also contribute to its profit-maximization goals. The relationship between the government and Aramco is said to be based on mutual trust, for example, although the organization requires a final approval for its five-year plans from the SCPM, any proposed plans apparently have never been rejected by the council. The government takes almost 93 per cent of profit, while the company retains the rest 7 per cent (Maurer, 2010). Last of all, Aramco fulfils its social responsibility by creating jobs in the private sector, developing human resource and performing as a catalyst for the localization of KSA’s energy sector.

The Mixed Consequences of Coming IPO

In January 2016, Saudi government announced that Saudi Aramco would go public. Although the company seemed unprepared and its plans appear disorganized since then, an IPO will take place to sell 5 per cent stake of Aramco at the end of 2018, or in early 2019 (CNBC, 2018). According to the Saudi government, this IPO has been motivated by diversification of income and boosting the resources of the Public Investment Fund, bringing more transparency to the company, 5 and to fight corruption, that ‘might be circling around’ the organization (Fattouh & Harris, 2017). On the other hand, the organization is such an integral part of the kingdom’s society and culture that the sale of even a small part means a radical change. Besides, the idea of the company being listed on a foreign exchange has raised concern of Saudis that it would not be a Saudi company anymore. Partly to counter the suspicion, the primary listing had been in Riyadh stock market; Hong Kong, New York and London, however, was considered afterwards as possible venues due to their strategic importance (Reuters, 2018). According to the recent news, KSA’s Tadawul is the only confirmed listing exchange for the energy giant (CNBC, 2018). The stock market has received approval to join the benchmark FTSE Emerging Markets Index in last March, which is expected to push large volume of fresh international capital into Riyadh’s relatively small exchange. This improvement will also prepare Tadawul for the IPO. On the contrary, different parts of the Saudi government have discussed conflicting priorities for Aramco’s IPO, and there are signs that the government has exerted more control over Aramco’s fundamental decisions (The New York Times, 2018). The strength of the organization has lied in its independence to make its own decisions. Now it needs to wait for direction from the outside, even the identity of ‘shareholders’ is still vague. Moreover, the IPO is expected to bring massive changes in Aramco’s business model and governance. For instance, the IPO gives investors the right to the reserve base, both present proven and future potential, of KSA. The new leadership, however, may act as a bridge to the new vibrant economy since it would be less concerned about the key role of the energy sector in its diversification (Fattouh & Harris, 2017). Another major consequent is that once the company is listed on foreign exchanges, Aramco may not be engaged in activities that influence world oil prices

The Crucial Role of Aramco in Economic Development and Geo-politics

Nurturing the development of a globally competitive domestic energy sector is a keystone of Aramco’s approach to leverage its core activities. It also nurtures entrepreneurship in the kingdom by providing financial support and advisory assistance in areas such as business plan development, mentoring, consultation and the execution of business agreements. Being the main driver of the Saudi economy, the organization searches for opportunities that combines its business activities with the kingdom’s needs, for instance, it participates in infrastructural and public works projects. In addition, it assists in the implementation of Saudization by ensuring a certain percentage of its company workers are from KSA (Looney, 2004). Lastly, it has implemented training programmes to enhance professional and teaching skills, particularly in the areas of drilling and oil well maintenance. Its In-Kingdom Total Value Add (IKTVA) programme has been designed to increase the percentage of locally produced energy related goods and services through contracts with Saudi Aramco to 70 per cent by 2021, driving investment, economic diversification and job creation in the kingdom.

Aramco serves as a vehicle to achieve the foreign policy goals of Saudi Arabia by maintaining a certain level of spare capacity that permits the Riyadh (the capital) policymakers to influence global oil price trends. Three major occasions can be identified when geo-political considerations supplemented the business concerns for operational assessment and corporate efficiency evaluations in determining the company strategies (Jaffe & Elass, 2007):

The decision to expand capacity rapidly in 1990 after Iraq invaded Kuwait;

The decision to accelerate development of the border Shaybah field that crosses in the UAE; and

The marketing strategy to maintain its position as the highest foreign supplier on crude oil to the USA on a month-to-month basis.

The control over the oil reserves through Saudi Aramco has created a critical mechanism for the defence of Saudi Arabia. For example, the long-term relationship between Saudi Arabia and the USA has been characterized as a bargain of ‘oil for security’ (Bronson, 2008). Since the mid-1970s, the former has offered the supply of oil to the USA, even during crisis periods, such as the 9/11 terrorist attack and operation Iraqi Freedom. In return, the USA government has extended a security umbrella to Saudi Arabia that includes a commitment to its territorial integrity, to help the state combat against threats, such as the Soviet Union (former), Egypt, Iran, Iraq, etc., as well as recent Al-Qaeda. Although there are issues such as the Arab–Israel conflict, 1973 embargo, the Cold War and so on, the relationship continues to serve the mutual interest of both nations (Jones, 2012). Moreover, oil and war are interconnected in the Middle East, whereas the combination of corporate and political interests around oil has vital consequences on the character of political authority inside and around this region. Finally, Aramco plays a crucial role in setting crude oil prices for the kingdom’s export. The company has the logistics flexibility to change its destination markets and can do so by adjusting price formulas to stimulate more sales in one region versus another. In usual business environment, it sets price to optimize its earnings by segregating its sales between three major markets, the USA, Europe and Asia, and charging different prices to different markets.

Moving Ahead

Changes in industry trend and market conditions are common to the oil industry. Over time, markets favour agile and diversified organizations that operate efficiently. Keeping this in mind, Saudi Aramco looks forward to making smart choices on how it produces, uses and capitalizes on the important resources such as oil and gas. However, its future success largely depends on how efficiently the organizations can tailor its strategies to match with the diversification plans of Saudi Arabia. The state, as a member of Gulf Cooperation Council (GCC), 6 is participating in its goal to diversify the economic base of the member economies (Hertog, 2014). The KSA also plans to diversify its energy mix, and, so Aramco works on expanding its gas processing capacity to collect and process associated gas from the oil wells. The company also owns and operates the Master Gas System (MGS), which has made the economy self-sufficient for gas feedstock to its industries and generation of electricity (Jaffe & Elass, 2007).

Saudi Aramco serves as a major instrument of the Saudi government to influence the global oil market and the geo-politics related to oil reserves in the Middle East. The separation of its operational decision-making and financial structure is one unique characteristic of this NOC, which might be linked to its sound financial performance and organizational excellence. On the other hand, the recent events of IPO indicate the possible problems that might arise from excessive state intervention. The IPO is an occasion in which geo-political consideration outweighs financial goals; the Saudi government, however, should ensure that geo-political issues do not severely damage the business outcomes. Furthermore, the major challenges the company needs to confront are the decline in conventional oil production in future, possible changes in its business driven by the IPO and fluctuations in the external environment, both domestic and global. Besides, it needs to consider the impacts of its production and price level on its competitors, especially other Middle East and North African (MENA) countries, since these economies are interconnected through their labour markets and international trade linkages (Berument et al., 2010).

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors gratefully acknowledge the aid of InterResearch, Bangladesh, to fund the study.

1.

Ecuador suspended its membership in 1992, but rejoined OPEC in 2007. Indonesia had left the association in 2009, joined again in January 2016, but decided to suspend its membership once more in November 2016. Gabon terminated its membership in 1995, but rejoined the organization in 2016 (OPEC, 2018b).

2.

Seven Sisters is a term to describe the seven oil companies which formed the Consortium for Iran cartel and dominated the global petroleum industry between the mid-1940s and 1970s. The group comprised Anglo-Persian Oil Company (now BP), Gulf Oil (later part of Chevron), Standard Oil of California (SoCal, now Chevron), Texaco (later merged into Chevron), Royal Dutch Shell, Standard Oil of New Jersey (Esso, later Exxon) and Standard Oil Company of New York (Socony, later Mobil, now part of ExxonMobil). The companies shrank to four in the industry consolidation of the 1990s and now produce about 10 per cent of the world’s oil and gas, and hold just 3 per cent of the reserves.

3.

The OECD was formed in 1960, when 18 European countries together with the USA and Canada joined forces to create an organization dedicated to economic development. Today, its 35 member countries span the globe, from North and South America to Europe and Asia-Pacific. In addition to many of the world’s most advanced countries, OECD includes emerging countries such as Mexico, Chile and Turkey.

4.

Countries are termed as rentier states when they receive a large fraction of their revenues from external rents. For example, more than half of the public revenues in Saudi Arabia, Bahrain, the UAE, Oman, Kuwait, Qatar and Libya have come from the oil sales. Besides, Jordan, Syria and Egypt earn large locational rents from payments for pipeline crossings, transit fees and passage through the Suez Canal. The remittance of workers remittances have also been an important source of foreign exchange in Egypt, Yemen, Syria, Lebanon, Tunisia, Algeria and Morocco, although these rents go to the private actors initially. Then, the foreign aid to Israel, Egypt and Jordan can be considered a type of economic rent.

5.

The organization’s transparency is mainly internal, that is, limited financial disclosure is made outside the SCPM (Maurer, 2010).

6.

The GCC was formed in 1981 with six oil exporting states, namely, Saudi Arabia, the UAE, Kuwait, Qatar, Oman and Bahrain to foster economic, scientific and business cooperation.