Abstract

Mobile banking services have been a significant breakthrough in the electronic banking system and have many potential demands for online banking services to connect with consumers. Although there has been a rapid expansion of information technology (IT) in banking, which offers multiple opportunities in the global market, massive growth has not been seen in India’s m-banking adoption. Several kinds of research on m-banking adoption have been conducted in various countries, and it has been observed that India has great potential for m-banking. Nonetheless, users are not quite sure about its use for a few reasons. The present study extends the applicability of technology acceptance model (TAM) constructs in connection with customers’ awareness, perceived risk and perceived trust to investigate the user’s behavioural intention of m-banking adoption. The authors tested the proposed framework by using regression analysis in SPSS 23 and collected a sample of 311 mobile banking users by using convenience sampling. In support of the previous studies, findings revealed that perceived usefulness, perceived ease of use, customer awareness, perceived risk and perceived trust significantly adopted m-banking services in the Indian context.

Keywords

Introduction

Implementing technological innovations such as m-banking has been a potential reason for competitive advantage for business in any industry (Sheng et al., 2011; Zhou, 2012). The banking industry has adopted various measures to fasten their business activity and save cost and time. There has been a large information technology (IT) requirement in the banking sector, thus confirming the profitability paradox in the industry (Gupta et al., 2018). M-banking refers to the facility to use banking services such as online transfers, checking account balances, downloading account statements, making bill payments and other financial activities via mobile phone (Cruz et al., 2010). An M-banking service reduces the cost of financial operations and provides greater convenience and flexibility to its consumers in terms of usage and accessibility (Hoehle et al., 2012; Montazemi & Qahri-Saremi, 2015). Growing acceptance of mobile phones and technologies indicated that the implementation of m-banking needs further study (Shankar et al., 2020; Singh & Srivastava, 2020; Srivastava & Singh, 2020). Due to their convenience, interactivity and usage time, cell phones are now considered as an appropriate medium to conduct financial transactions. On comparing the access and usage of the Internet on devices, smartphones’ penetration is intense (InMobi, 2019). Bank clients may perform banking services within fractions of seconds from anywhere. In support of mobile communication devices, M-banking can be understood as the provision and accessibility of banking services (Sinha, 2011). Mobile banking has overgrown as a revolutionary technology that has changed the banking system’s operations (Baabdullah et al., 2019). M-banking helps individual customers with their regular banking services and enables banking information to be easily and quickly accessible if necessary. In mobile banking, mobile phones are used as terminals for banking users to go for online transfers, check account balances, download account statements, make bill payments and other banking transactions (Brown et al., 2003). In India, M-banking was introduced in 2002 using smartphones or other mobile phones to send and receive messages. One of the significant advantages of using m-banking facility is that the account holder obtains the necessary details within a fraction of second. Requests for other programmes are often approved at the touch of a finger while checking accounts. Even as consumers face plastic money theft or fraud, mobile banking offers features such as hot debit and credit card listings. Equipping banking customers with omnipresent and real-time services is one of the most notable benefits of m-banking (Zhou, 2011), and it offers instant and interactive banking facilities (Gu et al., 2009). The Indian government has ordered all Indian banks to provide all their customers with m-banking facilities by the end of 2020 to facilitate digital transactions. Currently, m-banking is a financial business model launched by RBI, the country’s apex banking body. In India’s rural areas, where bank branches are in shortage, this form of banking has great potential (IBEF, 2019). In terms of digital transaction volume, in comparison to China and the USA, India is expected to increase further by 2023 (KPMG, 2019).

A survey conducted by BCG (2017) on digital banking stated that 56% of the users were not satisfied with the banks’ banking services, and 48% were dissatisfied with the online banking facility. Lack of knowledge and confidence in these banking networks, lack of channel accountability and insufficient security measures are the leading causes of low adoption of and high dissatisfaction with mobile banking and Internet platforms. It is also crucial for both researchers and practitioners to concentrate on considering the advancement in technology from the context of customer adoption (Alkhowaiter, 2020; Ananda et al., 2020). The essence and definition of conventional banking have been ultimately resurrected by M-banking and have shifted clients’ mentality from ‘nice to have’ to ‘need to have’. M-banking in India has a lot of potential, as evidenced from research comparing the ratio of m-banking consumers to bank branches across different countries (Marakarkandy & Daptardar, 2011). It is more critical to retain the existing clients than to acquire new clients in m-banking (Bhattacherjee, 2001; Devaraj et al., 2002; Gefen et al., 2003). Perceived usefulness (PU) and trust were identified as the major factors in predicting the customers’ intention to use m-banking in Saudi (Alalwan et al., 2018; Baabdullah et al., 2019). The Technology Acceptance Model (TAM) explains, how the PU and PEOU of any technology influence behavioural intention (BI) of the user, which further determines the actual usage of the technology. Other factors have been examined in previous studies, but perceived risk, perceived trust, and customer awareness of m-banking services have been identified as significant determinants (Agwu, 2012; Yu, 2009; Akturan & Tezcan, 2012; Tiwari & Tiwari, 2020; Safeena et al., 2011). Therefore, considering this as a research gap and extending this context to m-banking usage, this study proposes the TAM constructs’ applicability extended with customers’ awareness, PR and PT.

The primary objective of this study is to explore the additional constructs in mobile banking services that can be tested along with TAM’s constructs. Furthermore, a better understanding of PR, trust and awareness in the m-banking adoption plays a vital role in determining user behaviour.

Literature Review and Development of Hypothesis

With respect to the conduct of banking transactions, m-banking cannot be taken as a facility that has reached a global point of development and has a low rate of acceptance and diffusion, particularly in developing countries (Cruz et al., 2010; Hassan & Wood, 2020; Tran & Corner, 2016; Zhu et al., 2021). The Indian banking industry can benefit from other key indicators, such as the government’s decision to promote cashless transactions and the idea of digital India. In 2019, m-banking users worldwide surpassed 1.75 billion, and a developing economy such as India has seen rapid progression (Juniper Research, 2014). TAM has been widely used as a prominent extension of Ajzen and Fishbein’s research work known as the theory of reasoned action (TRA), which Davis developed in 1986 (Suh & Han, 2002). It was specially tailored to predict an individual’s IT acceptance behaviour (Davis, 1989). Its explanatory power ranged between 40% and 60% of the total variation in users’ intention to use technology (Gu et al., 2009). TAM needs to be integrated with the appropriate situation-related variables for improved understanding of IT acceptance (Hsu & Lu, 2004). Researchers integrated and used TAM in the m-banking context in various countries (Brown et al., 2003; Islam et al., 2011; Luarn & Lin, 2005; Püschel et al., 2010; Sangle & Awasthi, 2011; Wessels & Drennan, 2010). As per TAM, users, attitude plays a dominant role in influencing BI towards any service affected by PU and PEOU (Davis, 1989).

TAM’s basic constructs do not entirely replicate users’ work environment’s multiplicity and should be improved and extended (Wessels & Drennan, 2010). Hence, the current research incorporated customer awareness (CA), PR and PT as additional constructs along with TAM’s fundamental constructs. Researchers considered it a risk to influence mobile users’ acceptance (Brown et al., 2003; Gupta & Dhami, 2015; Riquelme & Rios, 2010). Since m-banking is an emerging channel in India, the customers may perceive this channel as risky to perform financial transactions. Customers may also perceive the m-banking channel as incompatible with their lifestyle, professional style and current banking needs. The perception of risk may be higher than offline depending on the experience and skill of the customers. The current research considers explicitly the risk related to the user’s perceived security and privacy. Therefore, m-banking user’s awareness, PT and PR are incorporated along with PU and perceived ease of use (PEOU) to explore its adoption.

Perceived Usefulness and Perceived Ease of Use

PU can be understood as ‘the degree to which a person agrees that using a particular system would augment his or her job performance’, and PEOU is defined ‘as the degree to which a person believes that would be free of effort’ (Davis, 1989). PU and PEOU were found to be strong predictors of m-banking users in India, Malaysia, Korea, Yemen, Turkey and Taiwan, which was also verified in the sense of online games and services (Akturan & Tezcan, 2012; Amin et al., 2008; Gu et al., 2009; Hsu & Lu, 2004; Kumar et al., 2020; Lin, 2011; Mutahar et al., 2018; Sharma et al., 2017). PEOU is described as accessing a less-effort system (Davis, 1989). According to studies on PEOU, it is found to have a positive effect on using online banking technology (Al-Somali et al., 2009; Jouda, 2020; Mortimer et al., 2015; Mouakket, 2009; Singh & Srivastava, 2020). Therefore, we measure the impact of ease of use on behavioural intention to use m-banking services. PU of m-banking technologies affects PEOU, which affects their acceptance (Akturan & Tezcan, 2012; Kumar et al., 2017). Customers’ ease of use of any technology is a critical element in using Internet banking and mobile banking service (Chawla & Joshi, 2020; Hassan et al., 2021; Lee et al., 2005). Contrary to that, m-banking is not directly impacted by PEOU but indirectly by PU (Wu & Wang, 2005). Customers’ views about ease of use contribute to the perception of the usefulness of the technology for banking services, which indirectly affects the purpose and use of m-banking services (Mutahar et al., 2018; Püschel et al., 2010). On the other hand, ease of use is judged by the website’s complexity and design which prevents customer from using the services (Lichtenstein & Williamson, 2006). If consumers are comfortable with specific innovations, they can make full use of technology and understand its advantages in a better way (Jouda, 2020). The above consideration has, therefore, been taken into consideration, and the following hypotheses have been suggested:

Customer Awareness

According to Rogers (2010), ‘consumers go through a process of knowledge, persuasion, decision and confirmation before they are ready to adopt a product or service’. In technology adoption, awareness is essential; it contains guidance about its existence, usage and various benefits it provides (Aloudat et al., 2014). According to Sathye (1999), the customer will follow various steps before adopting or accepting any product. These steps include knowledge about the product, persuasion, judgement and final confirmation for the product. When the customer is having a perception of the commodity, it will lead to its acceptance or rejection. To attract mobile banking, banks must implement proactive actions and plans (Mutahar et al., 2018). Customers would notice a service that provides the highest value. Therefore, banks must make customers aware of these products’ availability and clarify how mobile banking services can add relative value to other products or competitors to embrace mobile banking (Safeena et al., 2011). The formation of knowledge of services or products among consumers is an essential feature of implementing an innovative service or product. The research findings suggested that the more the customers are aware of the information on services’ benefits, the more are their chances of adopting online banking facility (Hassan et al., 2021; Pikkarainen et al., 2004). Besides, in their study, Sathye (1999) showed that customers’ low level of awareness would result in non-adoption of online banking facilities.

Perceived Risk

PR refers to ‘certain types of financial, product performance, social, psychological, physical, or time loss when consumers use technology’ (Forsythe & Shi, 2003). Though the m-banking channel is beneficial, compatible and easy to use, the degree of usage is determined by the level of risk associated with performing financing transactions on this channel (Chen, 2013; Laforet & Li, 2005; Yang & Zhang, 2009). Empirical studies found that customers’ PR of m-banking channel influences their attitude, intention and adoption of online and m-banking services negatively (Brown et al., 2003; Mohapatra et al., 2020; Safeena et al., 2011; Sathye, 1999; Zhou, 2012). The perception of risk is derived from a customer’s sense of confusion or anxiety about actions and the magnitude of the potential adverse effects of that behaviour (Kim et al., 2009; Luo et al., 2010; Mandrik & Bao, 2005; Shin, 2010; Swinyard & Smith, 2003). Also, with different offers from various unorganized suppliers using different technologies, the m-banking world’s complexity has left consumers confused, thus reducing their trust in information security. Since m-banking is a growing channel in India, the users’ intention to use the m-banking channel despite the risk associated with it needs to be investigated (Gaur & Ondrus, 2012; Jones, 2014). Some studies found that PR is a significant factor affecting BI of users to adopt Internet and mobile banking (Hassan et al., 2021; Im et al., 2008; Susanto et al., 2020; Wu & Wang, 2005). Customer’s perception of risk in m-banking involves banks’ security system, authentication procedures and the bank’s privacy guarantee. Hence, the current study, therefore, suggests the following hypothesis:

Perceived Trust

Trust refers to ‘a positive belief about reliability and dependency on anyone or any object’ (Soares et al., 2012). Trust is significant for any business relationship and plays a crucial role in m-banking, as it decreases the risk of uncertainty (Alalwan et al., 2018; Baabdullah et al., 2019; Gu et al., 2009; Lu et al., 2011; Palvia, 2009; Wang et al., 2015; Zhou, 2013). In the highly competitive financial services sector, the focus is on faith to create good, long-term customer relationships (Sankaran & Chakraborty, 2021; Sekhon et al., 2014). Outstanding support has been given to the impact of trust as an essential antecedent on BI (Chandra et al., 2010; Kumar et al., 2020; Lu et al., 2011; McKnight et al., 2002; Shaw, 2014; Shin, 2010) in the sense of mobile payments. Besides, some of these studies have found that PT is one of BI’s key antecedents (Chandra et al., 2010; Kumar et al., 2017; Shin, 2010; Tarhini et al., 2019), replacing the value of conventional variables for acceptance of technology such as PU. Similarly, building customers’ trust is also necessary for m-banking service providers (Zhou, 2011). Another aspect impacting consumers’ trust is the proper development of trust-building arguments displayed on websites (Kim & Benbasat, 2006). The same assumptions are applied in the case of mobile banking. Banks need to have strong and robust technological advancements to establish trust over the banks’ online services and facilities. Trust is one of the most significant variables in online banking services (Alalwan et al., 2018; Baabdullah et al., 2019; Hassan et al., 2021; Shankar et al., 2020; Sharma et al., 2017; Shen et al., 2010; Vatanasombut et al., 2008).

Research Methodology

Data Collection Procedure and Measurement Development

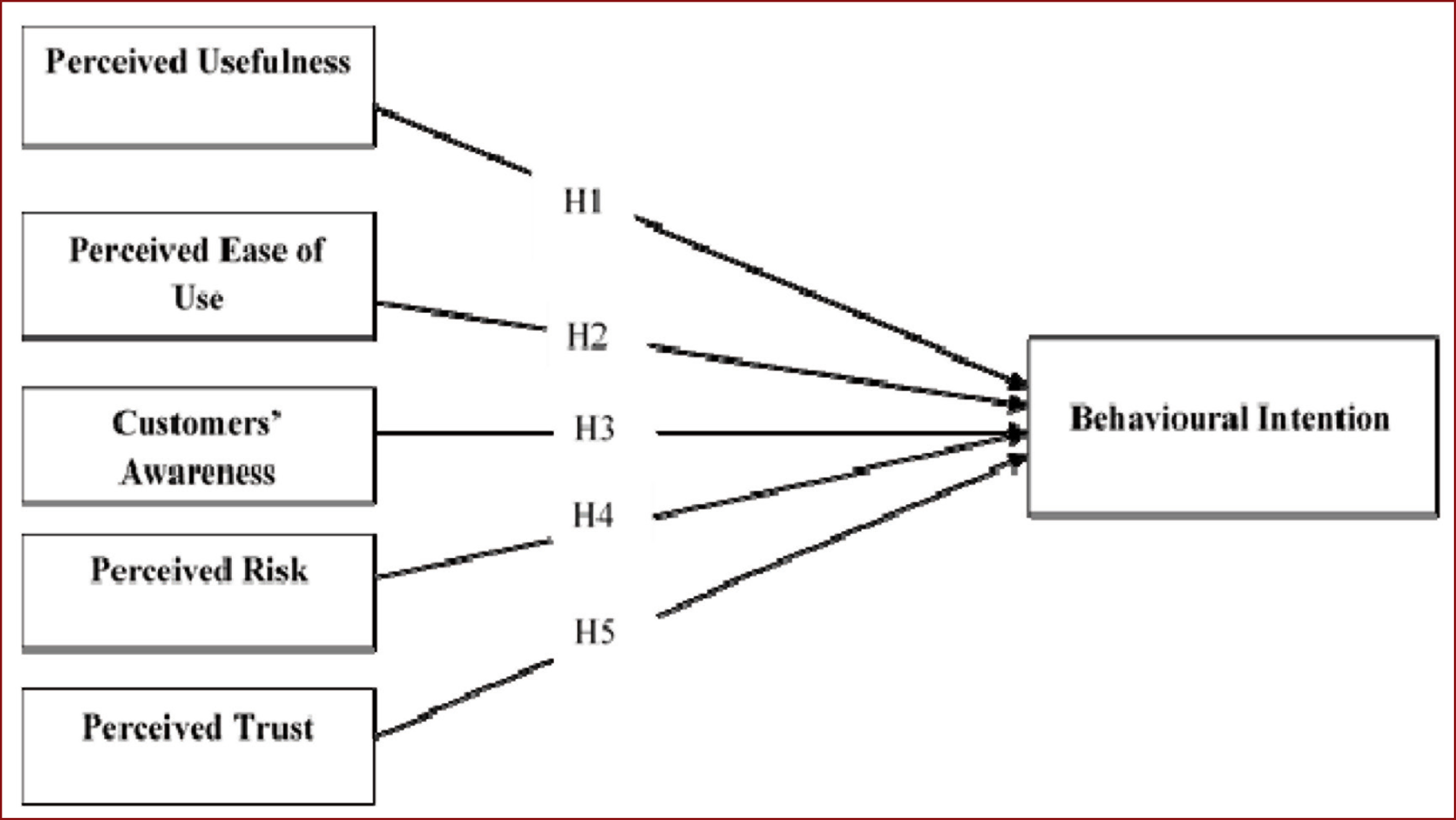

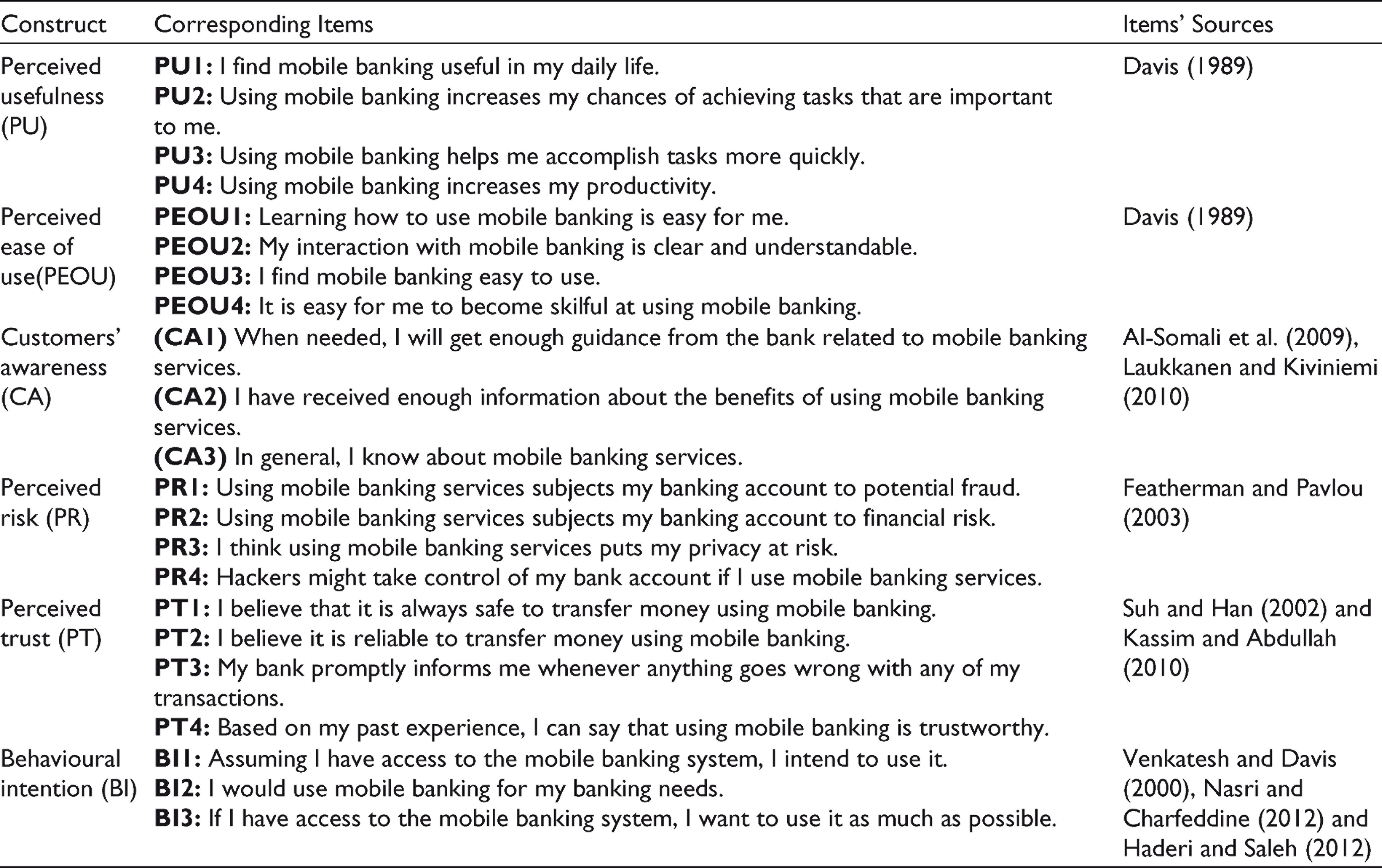

This study was causal, and a standardized questionnaire was adopted and modified as a tool for data collection. Convenience sampling method was used for data collection. Previous studies in different countries on mobile banking adoption used the convenience sampling method (Chiu et al., 2017; Zhang et al., 2018). The proposed framework in Figure 1 was assessed using regression analysis in SPSS 23. Furthermore, a pilot study was conducted on a selected 60 customers to verify the instrument’s reliability. In this study, we considered 6 variables and a sample size of 311 respondents for data collection. The questionnaires were given to the customers of the banks who were using mobile banking services at Agra Region (UP) and National Capital Region (NCR) of Northern India via online (Google docs. form) mode. The measurement items of the selected variables were adopted from the previously validated studies. The details of the various constructs along with items are shown in Table 1). A 5-point Likert scale ranging from (1) ‘strongly disagree’ to (5) ‘strongly agree’ was selected to measure responses in the present study.

Constructs and Corresponding Items

Data Analysis

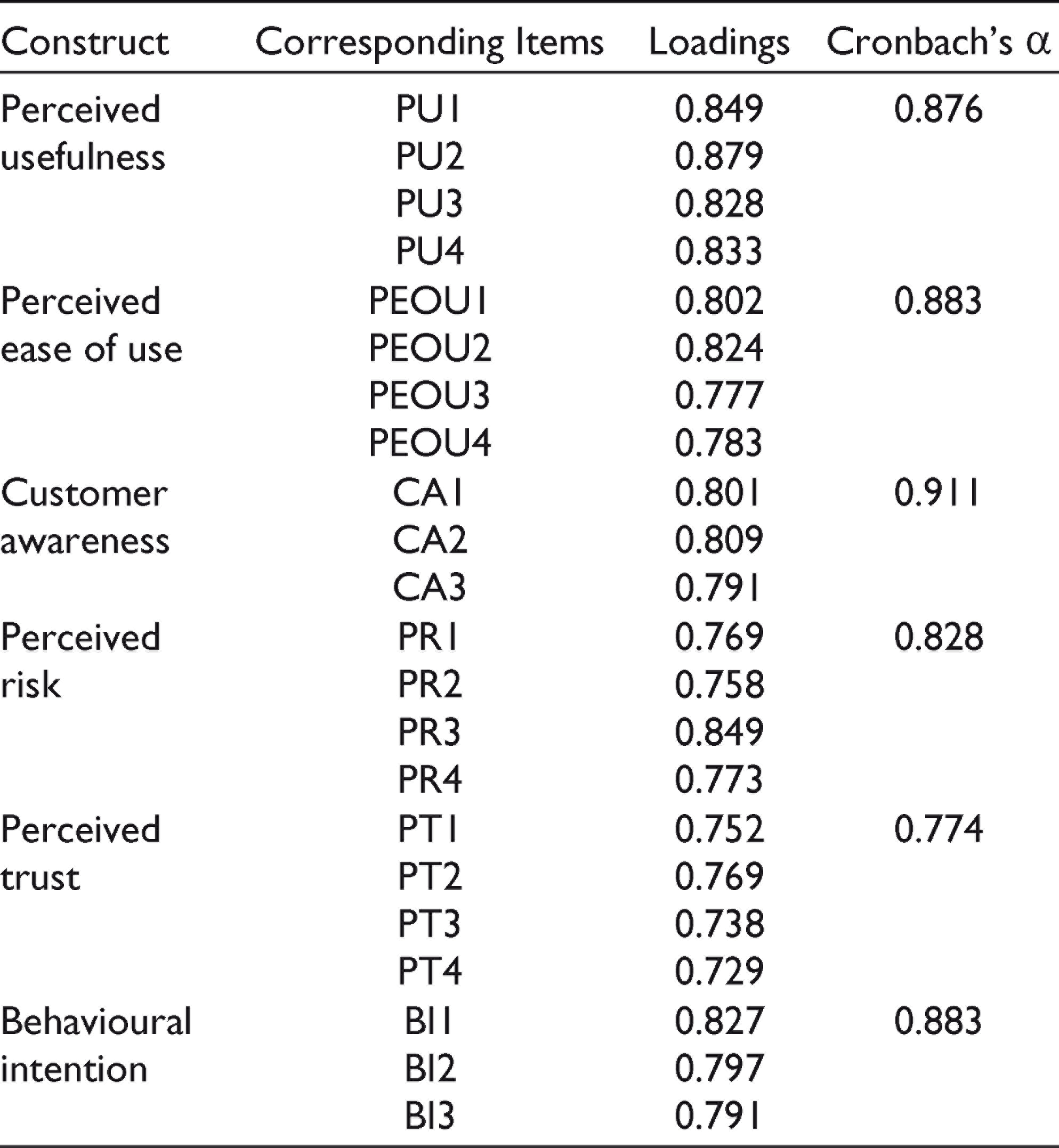

The item loadings and value of Cronbach’s alpha presented in Table 2. The coefficient of Cronbach's alpha should have a minimum cut-off value of 0.70 to be considered as valid measures of the variables (George & Mallery, 2003; Pallant, 2020).

Construct, Loadings and Value of Cronbach’s Alpha (α)

Multiple Regression Analysis

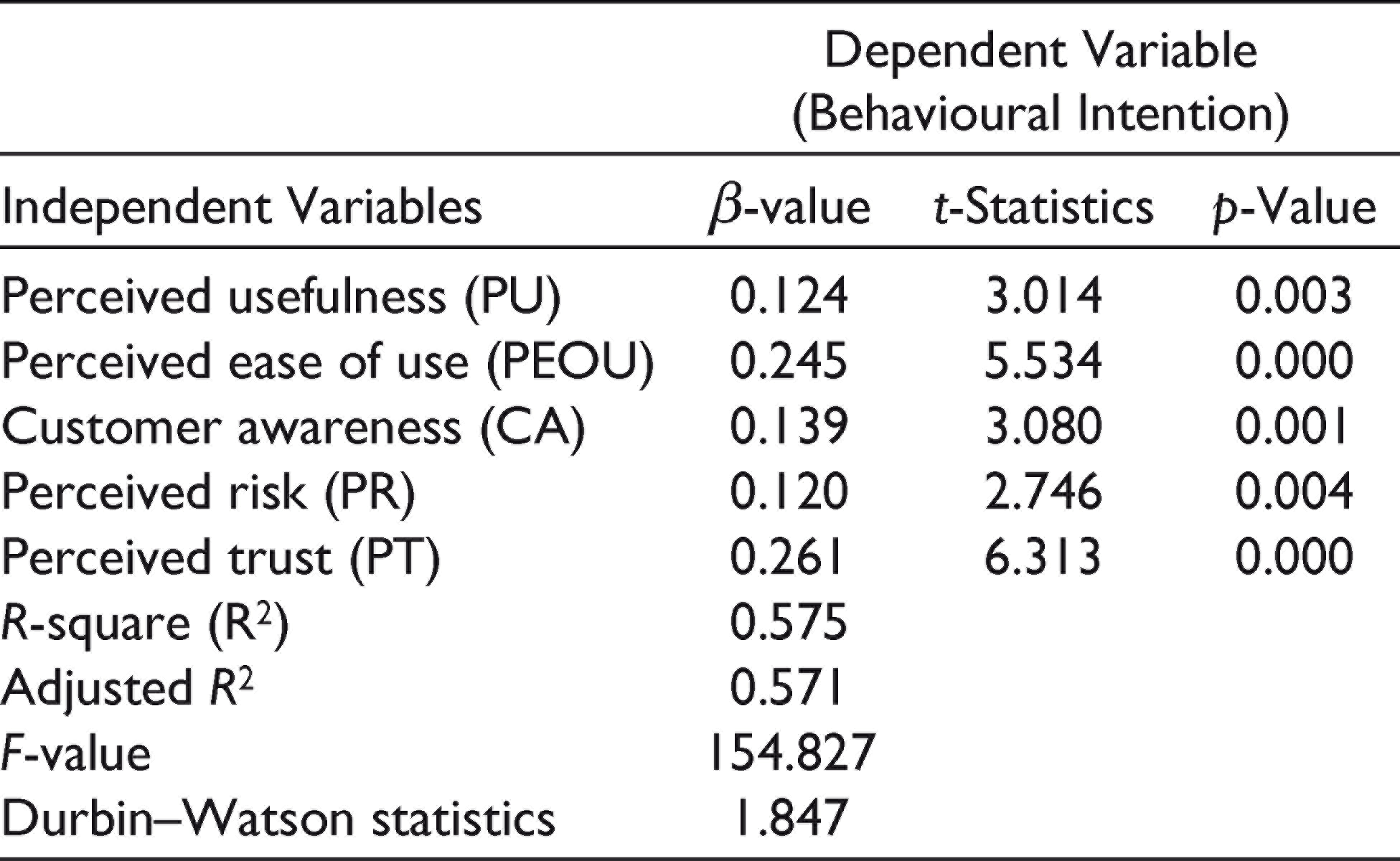

This test was applied to identify the cause-and-effect relationship between PU, PEOU, CA, PR and PT as independent variable and BI as dependent variable of the study using SPSS 20 (Field, 2009).

The value of R2 is 0.575, which indicates the independent variable explains 57.5% variance on BI; in other words, independent variable contributes 57.5% to dependent variable. The model used for regression has a good fit, as indicated by F-value 154.827, which is significant at a 5% level of significance. Hence, the null hypothesis is rejected, and further analysis can be conducted, as both variables are related, in other words, the model is found to have high predictability.

Therefore, the regression equation is estimated as follows:

BI = 0.804 + 0.107(PU) + 0.230(PEOU) + 0.116(CA) + 0.093(PR) + 0.187(PT) + e

Model summary indicating that the independent variable like PU, PEOU, CA, PR and PT and dependent variable BI have a cause-and-effect relationship which is checked with adjusted value of R-square i.e., 0.571 and good fit, indicated by F-test value of 154.827 (Table 3), which is significant at 5% level of significance. PU (β = 0.124; p-value = 0.003), PEOU (β = 0.124; p-value = 0.000), CA (β = 0.124; p-value = 0.001), PR (β = 0.124; p-value = 0.004), and PT (β = 0.124; p-value = 0.000) as independent variables have a significant cause and effect relationship with BI as dependent variable, these relationships are significant at a 5% level of significance. The results of hypothesis testing is presented in Table 4.

Results of Multiple Regression Analysis

Result of Hypotheses Testing of Effect of PU, PEOU, CA, PR and PT on BI

From the above results of the hypothesis, we may conclude that among the adoption factors of m-banking, PEOU and PT are ranked as highest, followed by CA, PU and PR. The results have suggested that consumers have found the technology interface simple, clear, easy and friendly, which makes them comfortable and helps them understand the advantages of adopting m-banking services (Kumar et al., 2020; Mehrad & Mohammadi, 2017). The results concluded that consumers who found m-banking services as trustworthy, having all the necessary protocols embedded in it, are more likely to understand and use it. The higher the level of trust among consumers, the more likely they are to use M-banking (Engwanda, 2014; Khan et al., 2021; Kumar et al., 2020; Shankar et al., 2020). Previous literature has suggested that if the consumers are duly informed about the services and their benefits, there are more chances of adopting online banking facility (Hassan et al., 2021; Pikkarainen et al., 2004).

Our study found a significant relationship between PU and BI in line with the previous studies of Kumar et al. (2020), Chawla and Joshi (2020), Hassan et al. (2021) and Singh and Srivastava (2020). It shows that if consumers find the m-banking services beneficial, their perception of acceptance is high with the high level of familiarity with smartphones and their applications; this service is also perceived as easy and useful. This result can be attributed to the fact that consumers are becoming increasingly concerned about losing their money while using mobile banking. They believe that when they use m-banking, their privacy is constantly in jeopardy. As a result, the higher the PR, the less likely users will adopt or use m-banking regularly.

Findings, Discussion and Implications

This study contributes to the existing literature and extends the TAM applicability in m-banking adoption as a medium of service. Prior researchers have stated that expanding the original TAM model by incorporating additional constructs improves the explanatory capacity (Baabdullah et al., 2019; De Leon, 2019). It is extended with critical factors such as customer awareness (CA), PR and PT, which are the critical elements for m-banking adoption in the Indian context.

The findings of this research have implications for banks and financial institutions, the IT department, government, researchers and other stakeholders for increasing the adoption of mobile banking services. This study will offer insights to banking service providers in their decision-making while solving consumer grievances and improving customers’ intention behaviour using m-banking services. The significant impact of PEOU and PU on customers’ adoption suggests that the more clients think that m-banking could be learnt easily, the more they would think its usage to be helpful (Mehrad & Mohammadi, 2017). Lack of trust and security concerns in banking hinder the adoption of m-banking by users, as m-banking technology involves risk in banking transactions. Customers’ awareness also significantly impacts the adoption of m-banking services, indicating that awareness reduces the customers’ doubt for non-adoption of m-banking services. Practical action for creating awareness among consumers related to the functionalities, benefits and usage of the service needs to be taken to attract more users to adopt m-banking. This research also suggests that if the usage of m-banking is to be increased, the developers of m-banking applications should give due importance to trust. Banks should create an environment of trust among their customers to gain their confidence in banking facility (Kumar et al., 2017). Consumer knowledge and awareness about technology-related banking services will create trust and wards using m-banking services. CA and knowledge can considerably streamline the effort banks invest in acquiring the right kind of customers (Nambiar et al., 2018). Banking service providers should minimize the risk involved and maximize m-banking services’ usefulness to positively impact and accept the services.

Our study found that PU, PEOU (Alalwan et al., 2018; Chawla & Joshi, 2020; Hassan et al., 2021; Kumar et al., 2020; Püschel et al., 2010; Singh & Srivastava, 2020), CA (Alkhaldi, 2017; Hassan et al., 2021; Mutahar et al., 2018), PR (Gupta et al., 2017; Laukkanen & Kiviniemi, 2010; Mohapatra et al., 2020; Susanto et al., 2020) and PT (Engwanda, 2014; Kumar et al., 2020; Lin, 2011; Shankar et al., 2020; Tarhini et al., 2019) were found to be significant in m-banking adoption.

The findings indicate that banking service providers should develop trust, risk awareness, usefulness and ease of use to encourage mobile banking adoption. More specifically, marketers need to ensure that m-banking services are safe and risk-free and more effective than traditional banking channels.

Future Scope, Conclusion and Limitations of the Study

This study is conducted to acquire deeper insights into various antecedents of customers’ BI to adopt an m-banking facility for their banking and financial transactions. There are limitations to this study, that is, scholars need to investigate the constructs in different geographical and consumer contexts, which helps generalize the results. The authors try to extend the existing TAM with CA, PR and PT to get more comprehensive insights on BIs of m-banking users. Furthermore, in this study, the moderating effect of demographic variables such as gender, age, income level and education were not tested, which could be considered in future studies concerning m-banking adoption. This study can be extended to other technical services such as m-education, m-health, e-wallets, social media usage and self-servicing technologies (SST) in developing markets like India. Future studies can also incorporate variables such as service quality, social influence and other facilitating conditions to get a broader perspective.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.