Abstract

This study evaluates the impact of self-help group (SHG) intervention and entrepreneurial traits of SHG members on the economic and socio-cultural empowerment of rural women. A purposive sampling method has been used to collect a sum of 344 responses from the SHG of women who are engaged in entrepreneurial income-generating activities in their village. A linear regression model has been used to analyse the data. The study found and argues that SHG interventions have a positive association with the economic and socio-cultural empowerment of rural women. The parameters identified and analysed in the study are helpful to the stakeholders to make policy decisions to strengthen all the factors, which are responsible for the success and growth of SHG in general and the micro-enterprise of SHG women entrepreneurs, in particular.

Introduction

Human development corresponds to the progress and empowerment of women. Their socio-economic development is essential for the sustainable growth of the economy. The Constitution of India guarantees the right to equality (Article 14) to all citizens for sustainable development. In this era, an increasing ratio of women participation in labour force can be observed, but, economically empowered women are still facing various personal and societal and organizational barriers in the path of their career advancement (Sharma & Kaur, 2019).

According to the Global Gender Gap Index published by World Economic Forum (2016), existence of gender inequality persists globally high in the areas of health, education, economics and politics. Further, a concern has been raised in United Nation’s Sustainable Development Goals to reduce poverty and promote social and economic development along with environmentally sustainable development (UN, 2017). Gender equality has been raised as an important concern to eradicate poverty (Kim, 2017). Past studies argued that the underlined causes of gender inequality are deeply rooted in our culture and more contextualized approaches are needed to handle the issues (Kim, 2017; Song & Kim, 2013). Therefore, the concept of microfinance and self-help groups (SHGs), has been much encouraged by various developing countries and used as an effective tool to eradicate poverty and improve gender equality (Ghosh, 2012; Laha & Kuri, 2014).

Despite increasing rates of economic growth, gender inequality persists in India. Women represent almost 48% of the total population of India (Census Data, 2011), but they constitute only 20.5% of the employment market (UN Human Development Report, 2020). Out of this, almost 60% of women are employed in agriculture and related sector (Madgavkar et al., 2019). Thus, the presence of women in employment and decision-making remains far less than men. India’s gender inequality is also reflected in its sex ratio which has dropped to 833 females per 1,000 males in some states of the country (Census Data, 2011). Likewise, in the gender inequality index, which is a composite metric of gender inequality using three dimensions, i.e., reproductive health, empowerment and the labour market, India ranked 123 out of 162 countries (UN Human Development Report, 2020). Gender inequality creates higher poverty, weaker governance and lower living conditions (Hubbard, 2001).

To improve the status of women, it is important to transform women’s abilities, by providing them access to economic and financial resources. The government of India has taken many steps towards women empowerment, the microfinance programme is considered to be one of the effective tools of formal financial service and plays a great role in socio-economic development, especially for rural women (Ghosh, 2012; Laha & Kuri, 2014). To bring a change in the socio-economic condition of rural women, SHGs are the most empowering tool for the deplored class (Kundu & Chakraborty, 2012). SHGs are self-governed peer controlled and small informal associations of the poor, usually from socio-economically homogeneous families who are organized around savings and credit activities (National Commission for Women, 2004). Access to microfinance facilities through SHGs has increased the economic, social, political and psychological empowerment of rural women (Khan et al., 2020).

In India, SHGs are supported and endorsed by government organizations and non-government organizations (NGOs). The major programme which, involves financial intervention by SHGs is the SHG–bank linkage programme launched by National Bank for Agricultural and Rural Development (NABARD). Apart from NABARD, microfinance institutions (MFIs) are providing lending to SHG. The SHG–bank linkage programme had led to an improvement in the income and consumption level of the members (Hundekar, 2020).

Most SHGs are women groups with membership ranging between 10 and 20 (Kumar et al., 2021). The members of the group are given loans from their collected savings and the funds are externally sourced from the banks (Mula et al., 2013; NABARD Report, 2021). The financial support from SHG would encourage rural women to involve in income-generating activities. The development of SHG has brought the prospects of delivering formal banking services to the doorstep of poor rural women in India and thereby the advantage of obtaining financial services. The functioning of SHG substitutes conventional banks and fulfils the requirement of easy and accessible financial services for poor rural women. With the support of the SHGs, poor rural women are assisted to start some productive income-generating businesses and thus contribute towards their economic and social empowerment. The operation of SHG has remarkably brought access to financial services to poor rural women and henceforth progress towards self-reliance and empowerment. Achieving gender equality and women’s empowerment is integral to each of the 17 sustainable development goals (SDGs) (UN, 2017) and active working of SHGs definitely provides the foundation to accelerate a sustainable world.

In India, SHGs are encouraged and supported by government agencies, NGOs or banks. The major programme involving financial intermediation by SHGs is the SHG–bank linkage programme (SHG–BLP) launched by the NABARD in 1992 (Panda, 2016). The SHG–BLP programme has made sizeable progress over time and it continues to be the backbone of the Indian microfinance environment with 112.23 lakhs SHGs covering 13.8 crore households with savings of Rs 37,477 crore as on 31 March 2021 (NABARD Report, 2021). Apart from banks, there are MFIs providing lending to SHG. The self-group supervises and grants loans to its members from their contributory savings and externally sourced funds from the banks. The approach towards the SHG has progressed as a pivotal medium to administer microcredit to poor rural women for carrying out entrepreneurial activities (Ghosh, 2012; Laha & Kuri, 2014).

The credit provided by banks under the SHGBLP assists poor women to build their economic capacity by utilizing self-employment (Sultana, 2017). NABARD’s initiative to promote SHGs for entrepreneurial activities with formal training evolves the knowledge and competence of its members and it can become a helping pathway in decreasing the issue of rural unemployment (Mula et al., 2013). The women entrepreneur’s growth act as a catalyst for women’s empowerment (Deka, 2018). Women’s empowerment and their material well-being can be possible only if women have access to the resources (Sharma, 2019).

Therefore, the main objectives of the paper are to evaluate the interventions of SHGs in improving the economic and socio-cultural empowerment of rural women and to examine the effect of entrepreneurial traits among SHG members in improving economic and socio-cultural empowerment. Nevertheless, a large portion of the studied sample of SHG members is with maximum educational qualification of 12th standard (intermediate). Therefore, the past studies remained unclear about highly educated women of rural India, as it is ascertained that a higher educational level decreases the chance of becoming an SHG member (Mohapatra & Sahoo, 2016). The perceived reason for a rural woman to become a member of SHG is more or less accomplished after joining SHG. It is determined that if a rural woman has the support of credit from SHG, she can take initiative to establish any small business. The findings indicate that the greater the financial intermediation services provided by SHG, the higher the chance of women being more empowered.

Literature Review

SHG Interventions and Economic Empowerment

Access to financial resources introduces a possible choice for the greater empowerment of women (Gasparre, 2011; Gordon, 2020). Empowered women can make better decisions in their lives (Gordon, 2020). Past literature indicates that women are transforming their social roles from being passive to active participants in the economic mainstream (Banerjee et al., 2015; Bent, 2019). Accessibility to microfinance through the SHG is a process-oriented rural development action plan to support the gesticulation for the upliftment from a social and economic point of view (Laha & Kuri, 2014; Panda, 2016). The microfinance admittance to rural women has accelerated the economic and social empowerment of women (Addai, 2017).

Microfinance is the dedicated financial service provided for the below-poverty and low-income households (Mahapatra & Dutta, 2016). The concept of microfinance has a positive impact on the rural and vulnerable (Banerjee et al., 2015). The microfinance programme gives access to credit to women who are living below the poverty line. They can set up enterprises and earn livelihoods for their family (Bent, 2019). It facilitates women to generate income and secure social and economic security (Mahapatra & Dutta, 2016). Microfinance is responsible to bring about considerable change in the empowerment level of SHG women (Hundekar, 2020). The SHG model has become an instrument in the development and empowerment of marginalized rural women in India (Jakimow & Kilby, 2006). There is a positive impact on various aspects of women’s empowerment through SHG membership. Microcredit is an effective transformative development tool for poor women (Banerjee et al., 2015). The usage of the loan itself emerged as a strong determinant of women’s empowerment rather than loan procurement (Garikipati, 2013). Women have better control over the management of loans as well as over their income (Kumar et al., 2021). Thus, the involvement of the SHG women in the community-led programmes has also directed them towards empowerment (Kumar et al., 2021). Thus, the authors propose the first hypothesis as follows:

H1: There is a positive association of SHG interventions with the economic empowerment of rural women.

SGH Interventions and Socio-cultural Empowerment

The SHG–bank linkage programme in India is fundamental in securing the balanced development of poor women (Kropp & Suran, 2002). Microfinance through SHGs has emerged as a viable means of socio-economic empowerment of women (Ramakrishna, 2010). It enhances the socio-economic stature of backward and economically marginalized women. It brings about skill development, courage, confidence and leadership among women (Sultana et al., 2017). Microfinance programme brings sustainability of financial income for women and thus helps in reducing gender inequality in society and improves respect and social standing among peers (Bent, 2019). Economic empowerment entrusts poor people to comprehend their daily lives ahead of their mere survival and increased participation in decision-making process. Economic empowerment brings about changes in social status (Kumari & Eguruze, 2022). It enhances their self-confidence to act individually and collectively to work forward for bringing societal change to the mindsets of their community and make them socially empowered (Malhotra & Schuler, 2005).

Women in SHGs help in reframing and improving the community development processes (Tesoriero, 2005). The SHG–bank linkage programme in India not only provided self-employment but also helped in social development and become a tool for the balanced development of poor women (Korpp et al., 2002). Therefore, the second hypothesis has been proposed as:

H2: There is a positive association of SHG interventions with the socio-cultural empowerment of rural women.

Entrepreneurial Traits and Economic Empowerment

Economic growth can be adequately accomplished if women have an opportunity towards entrepreneurship and also access to retail their products (Véras, 2015). The presence of many factors, for instance, favourable environment, internal conditions, individual traits and conducive external supporting agencies facilitate an individual to become an entrepreneur (Kuratko et al., 1990.) The definition given by Schumpeter (1934) describes entrepreneurs as visionaries and innovators who creatively disrupt traditional methods and create new practices or processes of doing business. The characteristics of an entrepreneur are often attributed to the success of a small business (Kumari & Eguruze, 2022).

Zhao and Seibert (2006) examined a positive relationship between entrepreneurship and personality traits. Personality traits are the pattern of individuals’ thoughts and emotions that influences their behaviour (McCrae & Costa, 2003). It helps in describing individuals thinking and behavioural pattern (Parks-Leduc et al., 2014). The core start for identifying the traits of an entrepreneur comes from the identification of the big-five broad categories of personality traits (McCrae & Costa, 1987). Thus, the entrepreneurial behaviour of individuals is influenced by their traits. Studies also identified entrepreneurial traits as a catalyst to enterprise success (Jaroliya & Gyanchandani, 2021; Pattanayak & Kakati, 2021).

The outcome of entrepreneurship can only be ensured if there is a degree of empowerment that creates a true feeling of participation (Deka, 2018; Karki & Risal, 2022). The financial management skill and the group identity of the women borrowers have a direct and significant relationship with the development of rural women entrepreneurs (Afrin et al., 2010). The loans provided to SHGs by banks help in developing the capabilities of poor women through self-employment (Sultana et al., 2017). Further, it improves her decision-making power, independence and ability to be mobile, which are also essential for the empowerment of women (Rathiranee & Semasinghe, 2015, Singh et al., 2022). In addition to it, the entrepreneurial traits of an entrepreneur enhance the possibility of the success of the enterprise (Pattanayak & Kakati, 2021) and re-enforce the process of empowerment. The entrepreneurial traits of risk-taking, confidence, hardworking and accountability among the SHG women enhance the degree of empowerment among them (Kumari & Eguruze, 2022). Therefore, this study explores the SHG intervention and the entrepreneurial traits of SHG women in empowering rural women’s economic status and proposes the following hypothesis:

H3: There is a positive association of entrepreneurial traits with the economic empowerment of rural women.

Entrepreneurial Traits and Socio-cultural Empowerment

Past literature supports that a micro-enterprise of SHG women forms an integral part of securing a balanced development of poor women in the economy (Addai, 2017; Mula et al., 201; Sharma, 2019). Women-controlled enterprises not only boost economic growth but also have desirable socio-economic outcomes (Nziku & Henry, 2020. It assists in generating employment for several people within their social system. The involvement of rural women in entrepreneurial activities has a positive impact on their lives and their families (Kumari & Eguruze, 2022). It adds to the family income, enhances their capabilities, increases decision-making ability and improves their status in the family as well as in society (Laha & Kuri, 2014; Nziku & Henry, 2020). Rural entrepreneurial ventures help in the social development of women in India (Kumar, 2016; Patel & Chavda, 2013). Studies also highlighted the entrepreneurial activity of women through a community-based sustainable business model economically, socially and culturally empowered rural women (Haugh & Talwar, 2014; Kumari & Eguruze, 2022). The engagement of women in entrepreneurial activities improved their intra-household power relations to a great extent and thus reduced preference for males and domestic violence (Hazarika & Goswami, 2016). Thus, the study proposes the following hypothesis:

H4: There is a positive association of entrepreneurial traits with the socio-cultural empowerment of rural women.

The microfinance programme through the SHG helped in enhancing women’s role in households as well as in society (Gordon, 2020). The joining of rural women in the SHG microfinance programme promoted income generation (Moyle et al., 2006). This directly promotes and supports the functional aspects, capability and efficacy of the SHG (Kumar et al., 2018). The SHG participation helps in the improvement of collective competency, self-capability, proactive approach, self-respect and self-evaluation of the general health, prosperity and welfare of rural women (Moyle et al., 2006). The studies also support that SHG interventions in rural women contributed to increased savings with timely loan repayment (Panda, 2009; Parida & Sinha, 2010). Thus, the study formulates the following hypothesis.

H5: There is a meaningful variation in the income and saving status of SHG women since joining the SHG.

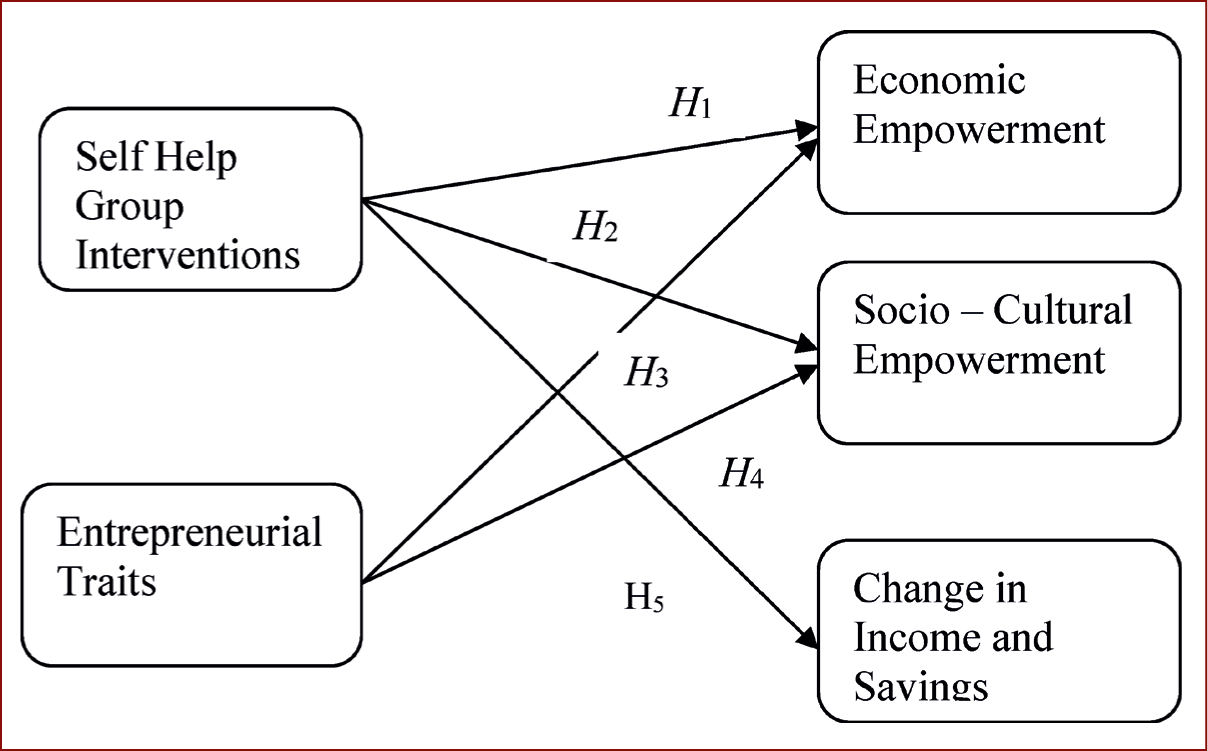

Figure 1 depicts the conceptual model of the study. The model proposes that SHG intervention is positively associated with the economic and socio-cultural empowerment of rural women. As discussed above, the authors also propose a positive association between entrepreneurial traits and the economic and socio- cultural empowerment of the SHG members. The model also depicts that SHG interventions will have a positive association with the change in income and savings of rural women.

Conceptual Model.

SHG–bank linkage programme has been promoted by government agencies and non-government agencies (NGOs). The fundamental objective of this programme is to create self-employment opportunities for rural women and thus enhance their income-earning capacity. Rural women are involved in various income-generating activities like handicrafts, garments, grocery shops, dairy, poultry, weaving, small enterprises for soaps, detergents, footwear, bamboo products, artworks, embroidery, selling vegetables and fruits, tea stalls, or any traditional business (MEPMA Study, 2018). The research gap of this study arises from the previous literature on explaining the role of an SHG in empowering rural women. Though various studies focus on the economic and social welfare of poor women through SHGs, the impact of the consistent functioning of SHGs on women empowerment is not extensively covered. Likewise, the effect of entrepreneurial activities of SHG members on women empowerment was analysed, previous studies did not examine the impact of entrepreneurial traits of SHG women on empowerment. Therefore, this study explores the SHG intervention and the entrepreneurial traits of SHG women in empowering rural women’s economic status. The present study attempts to examine the role of certain individual entrepreneurial traits among rural women on their economic as well as socio-cultural empowerment.

Methodology

Data Collection

The study used a survey method to collect the data. The study used a purposive sampling method. A structured questionnaire has been prepared and distributed among the members of the SHGs to collect their responses. The questionnaire includes items to measure the economic empowerment, socio-cultural empowerment, entrepreneurial traits and other demographic characteristics of the SHGs members. The brief details on the survey items and respondents’ selection criteria have been presented below.

Survey Items

The appropriate indicators for measuring women’s empowerment are based on past literature (Ibrahim & Alkire, 2007; Kabeer, 1999; Malhotra & Schuler, 2005). The selected indicators incorporated from the studies assess the three aspects. First, the intrinsic aspects of agency and empowerment; second, the indicators identify the change in empowerment levels over time; third, the choice of the indicators is in line with the indicators, which are often used in research to adequately measure empowerment. Based on the above criterion, the study selects a set of indicators for measuring women’s empowerment. Women empowerment is operationalized using 40 items measuring economic and socio-cultural aspects of empowerment.

The economic empowerment of women is measured with autonomy on the expenditure and increase in income using 19 items. The socio-cultural empowerment of women is measured using 21 items representing five factors, i.e., mobility and confidence, commitment to educate children, household decision-making, participation in social networks and financial decision-making.

The entrepreneurial traits identified are the traits of small and medium business owners. The entrepreneurial traits are measured using business knowledge and the need for achievement by using 19 items (Sorensen & Chang, 2006).

The perceived reasons for becoming members of SHG are measured using 11 items denoting three factors, i.e., improvement in status, creating assets and financial support. The financial intermediation services provided by SHG in the study are measured through 11 items denoting two factors namely financial intermediation services and financial intermediation system. The functioning of SHG is operationalized using 25 items measuring four factors, i.e., entrepreneurship development, loans and leadership, operational practice and organizational practice of SHG. The usefulness of SHG training is measured using 12 items of two factors, i.e., entrepreneurship development training and management of loan training.

Respondents’ Selection Criteria

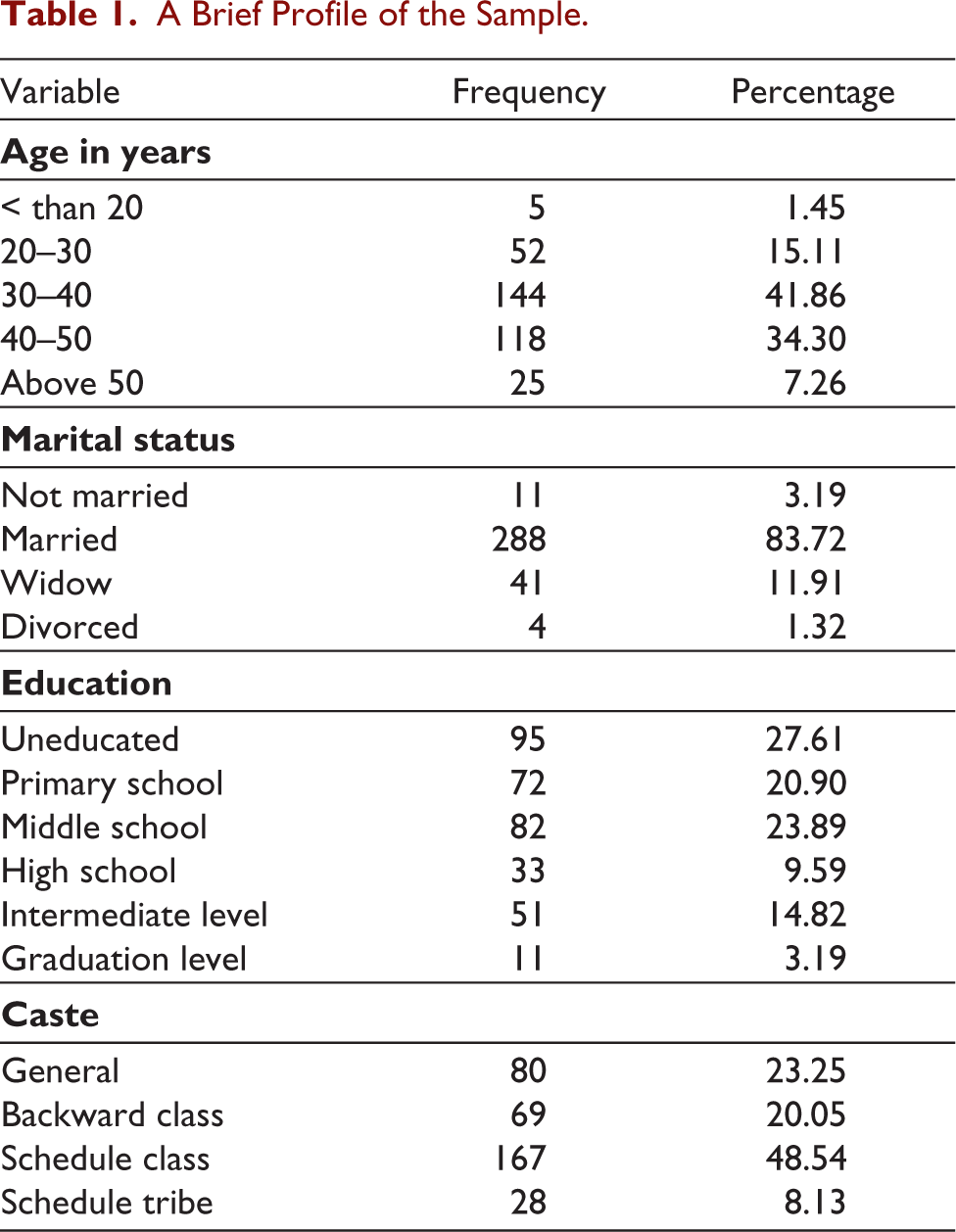

The data for the study has been collected from the Medak district of Telangana State in India. The study adopts a cluster with a random sampling technique for the selection of respondents. Medak district was selected as the sample district because of its geographical location and industrial proximity to the city of Hyderabad and also the opportunity to start a micro-enterprise in the district.

There are 295 self-help enterprises in the district and they are involved in the manufacturing of textiles, paper plastic plates, handicrafts, soaps, detergents, footwear, bamboo products, milk products, artworks and embroidery works etc. A total of 193 self-help enterprises are selected from eight mandals in 15 villages, out of 295 self-help enterprises in the district. The total sample respondents for the study are 344 SHG women who were engaged in entrepreneurial income-generating activities in their village. The selections of the SHG women respondents were according to the proportional allocation of self-help enterprises in each village. The data were collected from those members of SHGs, who had completed at least one loan cycle and had invested some part of the loan in their business through a structured questionnaire. The questions and the items in the questionnaire were targeted to measure the key variables of the study. The respondents were requested to rate the statements on each variable on a five-point scale from 1(strongly disagree) to 5 (strongly agree).

The selected respondents are the members of the SHG for more than ten years and they have borrowed money more than once from their SHGs. The amount of the loan was within the limits of ₹3,000 to ₹50,000. The savings of the SHG women respondents ranged from ₹5,000 to ₹12,000. 60.3% of the SHG women respondents are below the age of 40 years. Almost 84% of the respondents are married. Half of the SHG women respondents are illiterates and around 39% of them have completed primary-level education. Almost 75% of them belong to the backward class (OBC), scheduled caste (SC) and scheduled tribe (ST; see Table 1).

A Brief Profile of the Sample.

Empirical Results

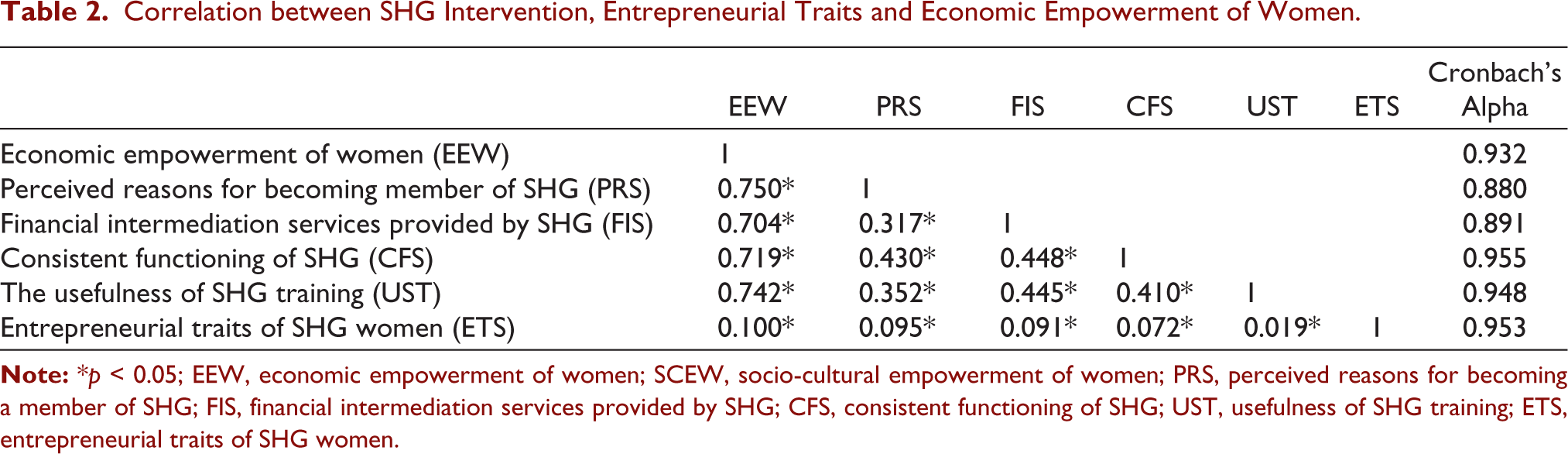

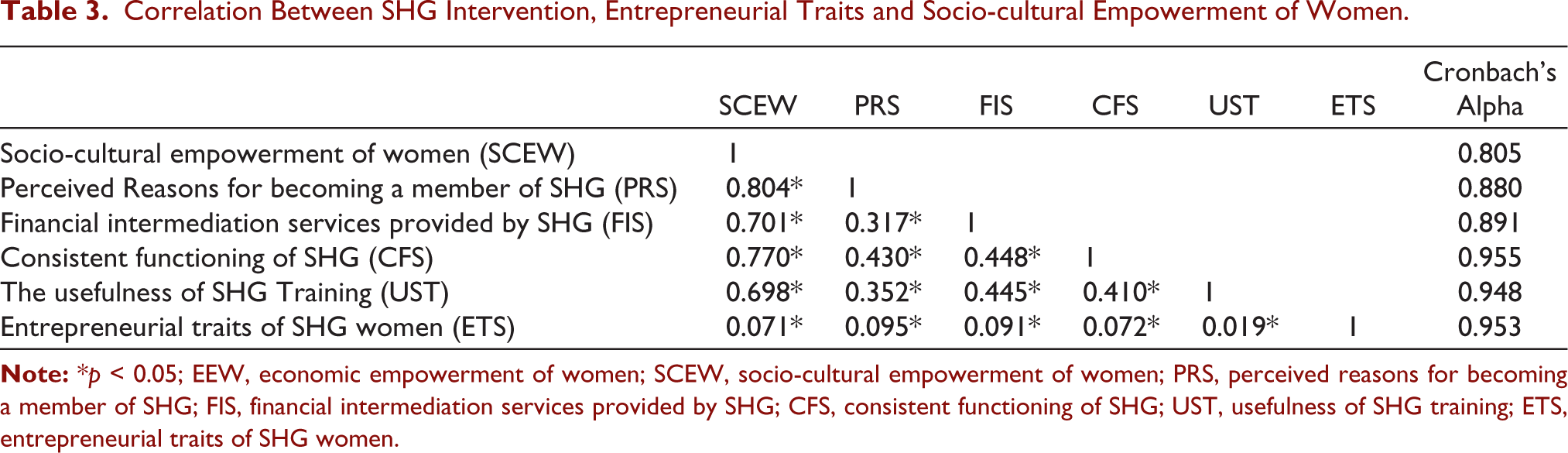

The analysis of the data has been done in three steps. In the first stage, exploratory factor analysis has been done to check the correlation among the items. The items with lesser loadings are removed from the scale (see Annexure 1). The reliability of each scale has been measured by checking Cronbach’s alpha value of greater than 0.5. The validity of each scale has been analysed by using Pearson’s bivariate correlation of each item of the questionnaire and the total score of each item, as the correlation is significant at the 1% level and therefore the questionnaire is considered to be valid (see Table 2). This study uses two multiple regression models to understand the women’s empowerment of SHG. In model 1, economic empowerment, and model 2, socio-cultural empowerment of SHG women have been measured.

Correlation between SHG Intervention, Entrepreneurial Traits and Economic Empowerment of Women.

Thus, in the second stage, correlation analysis has been done separately for both the model and the results show a significant correlation between the dependent and dependent variables of both models (see Tables 2 and 3).

Correlation Between SHG Intervention, Entrepreneurial Traits and Socio-cultural Empowerment of Women.

All the independent and dependent variables used in the regression analysis are constructed by taking the mean values of the items measuring the variable. At the third stage of the analysis, two multiple regression models are analysed to explore the association among all dependent (i.e., economic empowerment and socio-cultural empowerment of SHG women) and independent variables (i.e., perceived reasons for becoming member of SHG; financial intermediation services provided by SHG; consistent functioning of SHG; usefulness of SHG training and entrepreneurial traits of SHG women). The study also checks the basic assumption of regression analysis, i.e., normality and multicollinearity issues of the data. The variables meet the assumption of normality and multicollinearity as the tolerance and variance inflation factor values are within the cut-off limits.

Specification of Model 1

The multiple regression model 1 analyses the effect of SHG intervention and entrepreneurial traits of SHG women on economic empowerment and specified as economic empowerment of women (EEW) = f (SHG intervention and entrepreneurial traits of SHG women):

SHG intervention = perceived reasons for becoming a member of SHG (PRS), financial intermediation services provided by SHG (FIS), consistent functioning of SHG (CFS), and usefulness of SHG training (UST) and entrepreneurial traits of SHG women (ETS), socio-economic characteristics (SEC).

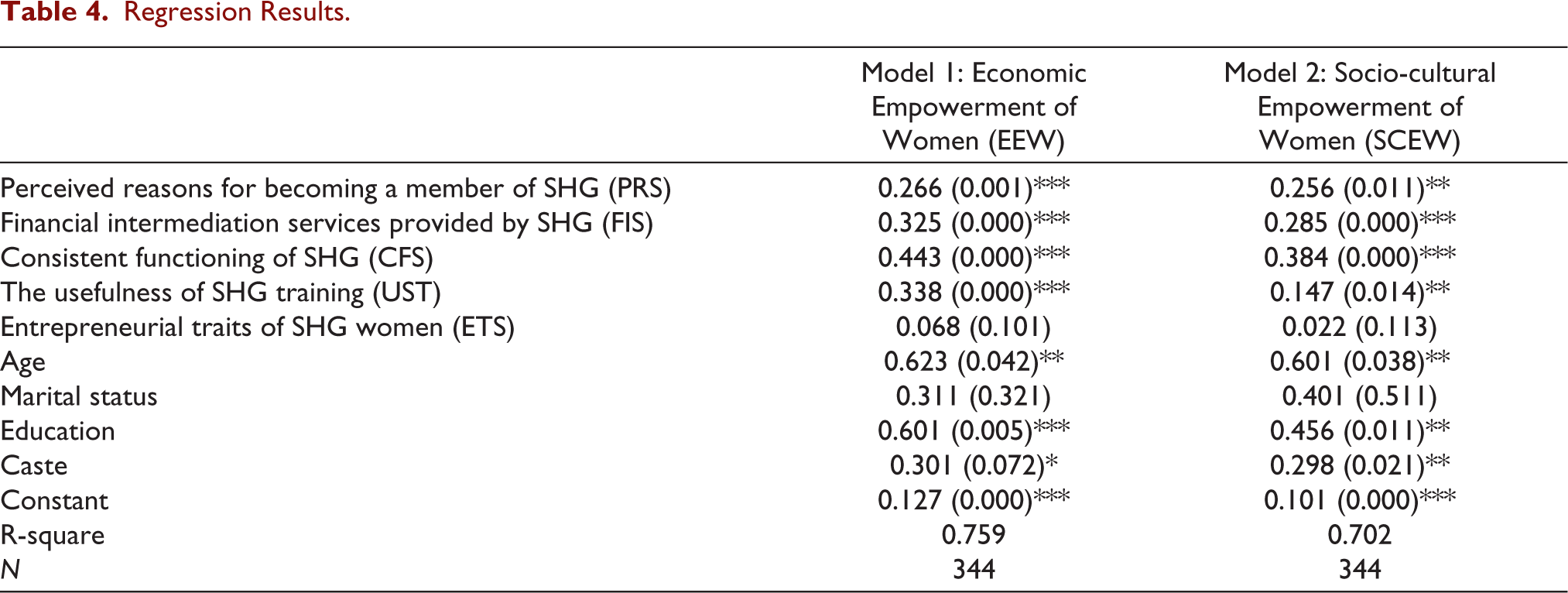

The multiple regression analysis of model 1 supports that almost 75% (R² = 0.759) of the economic empowerment of rural women is influenced by the SHG intervention and other socio-economic status which includes age, marital status, education and caste. However, the results of the regression analysis show no significant influence of entrepreneurial traits on economic empowerment. The strongest predictor is the consistent functioning of SHG (β = 0.443), followed by the usefulness of SHG training (β = 0.338), financial intermediation services provided by SHG (β = 0.325), and perceived reason for becoming a member of SHG (β = 0.266) (see Table 4).

Regression Results.

Specification of Model 2

The multiple regressions in model 2 analyse the effect of SHG intervention and entrepreneurial traits of SHG women on the socio-cultural empowerment of women. The model is specified as socio-cultural empowerment of women (SCEW) = f (SHG intervention and entrepreneurial traits of SHG women):

SHG intervention = perceived reasons for becoming a member of SHG (PRS), financial intermediation services provided by SHG (FIS), consistent functioning of SHG (CFS), and usefulness of SHG training (UST) and entrepreneurial traits of SHG women (ETS), socio-economic status (SEC).

The multiple regression analysis of model 2 supports that almost 70% (R² = 0.702) of the socio-cultural empowerment of rural women is influenced by the SHG intervention and other SEC which include age, marital status, education and caste. However, the results of the regression analysis show no significant influence of entrepreneurial traits on socio-cultural empowerment. The strongest predictor is the consistent functioning of SHG (β = 0.384), followed by financial intermediation services provided by SHG (β = 0.285), perceived reason for becoming a member of SHG (β = 0.256) and usefulness of SHG training (β = 0.147) (see Table 4).

Further, the study also compares the changes in income and savings position of the members after joining the SHG. The mean joining years of the selected members of SHGs in the study is 8 years. It is found that the income and savings status of the respondent SHG member has increased (see Table 5).

A paired t-test has been applied to further analyse and compare the changes in the income and savings position of respondent SHG women. The comparison of the mean income of respondents shows an increase of ₹548 per month after joining SHG. Likewise, the coefficient of variation of income is relatively less dispersed after joining SHG (see Table 6). A paired-sample t-test shows that there is a significant difference in the income level of SHG women since joining the SHG with t (343) = −49.602, p < 0.000.

The comparison of the mean savings of respondents shows an increase of ₹575 per month after joining SHG (see Table 7). Likewise, the coefficient of variation of savings is relatively less dispersed after joining SHG. A paired-sample t-test shows that there is a significant difference in the saving level of SHG women since joining the SHG with t (343) = −44.646, p < 0.000.

Comparison of Income and Savings Status of Respondent SHG Members.

Income Level of SHG Members.

Savings Level of SHG Members.

Discussion

The results of the multiple regressions in model 1 indicate a positive association among all the predictors of SHG interventions with the economic empowerment of rural women. However, the entrepreneurial trait is not having any significant association with the economic empowerment of rural women. Hence the results do support our assumptions in hypothesis 1 (H1) but do not support the assumption in hypothesis 3 (H3). This indicates that entrepreneurial traits possibly do not impact women’s empowerment directly. However, entrepreneurial traits can act as a moderator between the financial intermediation services provided by the SHG and women empowerment. The entrepreneurial traits of SHG women enhance the likelihood to manage and sustain the micro-enterprise successfully and profitability (Ghosh, 2015). The authors’ pursuit of the outcome is the result of limitation in data collection, as the data are collected for one time, and assumes that SHG members who are involved in some income-generating activity for a few years will slowly develop entrepreneurial traits.

However, the results of the multiple regressions model 2 indicate a positive association among all the predictors of SHG interventions with the socio-cultural empowerment of rural women and support hypothesis-2 (H2). Thus, the results are in line with the previous research (Haugh & Talwar, 2016; Kumari & Eguruze, 2021). However, the entrepreneurial trait is not having any significant association with the socio-cultural empowerment of rural women. Hence the results of the analysis do not support hypothesis 4 (H4). Thus, the analysis concludes that SHG intervention has a significant association with the economic and socio-cultural empowerment of SHG women. However, the results of the multiple regressions do not support any association between entrepreneurial traits and the economic and socio-cultural empowerment of SHG members. Accordingly, this finding does not support the previous research (Pattanayak & Kakati, 2021). The results of the analysis also support a significant intervention of age, educational level and caste of SHG members in their economic empowerment as well as socio-cultural empowerment (see Table 4). The diversity in group members’ castes and education brings about more variations and dynamism in terms of their skills and expertise (Kumar et al., 2018). Further, the analysis also concludes that there is a significant difference in mean income and mean saving of SHG women since joining SHG, hence supporting the assumption of hypothesis 5 (H5). Previous studies (Ghosh, 2012; Kumar et al., 2018; Mohapatra & Sahoo, 2016; Rathiranee & Semasinghe, 2015; Sultana et al., 2017) support the findings of SHG intervention contributes significantly towards the participation of women in the increase of the income of the household.

Conclusion

The study suggests that competent functioning and operations of SHG can become catalytic for women’s empowerment.

Entrepreneurial traits on their own may not have any meaningful impact on the economic and socio-cultural empowerment of women. Individual entrepreneurial traits enhance the chances to run and sustain the business successfully and profitably (Pattanayak & Kakati, 2021). Entrepreneurial traits by acting as a moderator can strengthen the relationship between the independent and dependent variables. This leads to self-employment, sustainable livelihoods, enhanced decision-making power, social dignity and better status for women, thus ensuring holistic social development as well. It creates realization and understanding among rural women about savings, education, health, environment, cleanliness, sanitation, family welfare, social forestry and so on.

In India, caste is considered one of the key components of socio-economic status (Roa & Ban, 2007; Mohapatra & Sahoo, 2016). For decades, it has been observed that Indian society is stratified into different castes, and the lower castes (i.e., OBC, SC and ST) have remained outside of the mainstream of society (Mohapatra & Sahoo, 2016). In this study, almost 75% of the respondents are from the OBC, SC and ST. Therefore, the authors conclude that there is a positive role of SHG intervention in the economic as well as socio-cultural empowerment of rural women who are excluded from the mainstream of society.

In addition, the educational level of SHG members is positively associated with their economic and socio-cultural empowerment. It is observed that the SHG initiative has assisted rural women to be economically and socially empowered. It has improved the socio-economic status of rural women (Kumar et al., 2018). It is also ascertained that the credit facility by SHG supports rural women to become entrepreneurial. The findings conclude that perceived reasons for becoming a member of SHG, financial intermediation services provided by SHG, consistent functioning of SHG and usefulness of SHG training have a positive and significant association with economic and socio-cultural empowerment of SHG women.

For the development of SHGs and SHG women entrepreneurs, it is important to formulate pragmatic policies, as self-employment through SHGs is favourable to the improvement of individual aspiration and entrepreneurial skills. SHGs should be encouraged to grow into an organization for financial intermediation along with the system of community networks instead of only as a mechanism for loan distribution for the reason that SHGs are a possible alternative to realize the goals of rural development and to bring about community cooperation and support in all rural development programmes.

Policy Implications

The parameters identified and analysed in the study could help the stakeholders to make policy decisions to strengthen all the factors, which are responsible for the success and growth of SHG in general and the micro-enterprise of SHG women entrepreneurs, in particular. The government could link technical training support, online marketing or funding from the industry or corporates as a component of their corporate social responsibility (NABARD Report, 2019). Likewise, educational institutions, as a constituent of their outreach programme, could provide basic accounting skills and business management training to SHG women entrepreneurs. This would also indirectly support the skill development initiative of the government of India. Furthermore, corporates could help SHG women entrepreneurs in improving the quality of their products as well as diversification.

Banks, NGOs associated with SHGs or any governmental agency or institution as a policymaker could initiate a strategic decision to adopt an integrated developmental policy and procedure that has training and instructions, institutional and financial support as an exhaustive arrangement to enhance the entrepreneurial capabilities and capacities of SHG women entrepreneur.

Limitations and Directions for Future Research

This study has a few limitations. First, this is a cross-sectional study and lacks an understanding of the long-term impact of SHG interventions. Thus, future studies can be done by using longitudinal data to check the long-term impact of SHG intervention and also to explore how SHG interventions can contribute to the development of entrepreneurial traits among rural women (Sharma et al., 2012) Secondly, the study also suffers from the limitation of omitted variables. Though a few demographic variables such as age, education, marital status and caste are considered, there could be a few other important socio-economic variables that may have a possible influence on our given variables. Hence, future studies must test the model by considering other social and economic variables as an antecedent.

Lastly, an assortment of studies is affected to understand women’s empowerment in terms of their access to money; however, further studies need to be conducted to relate empowerment with women’s health needs and leadership concerns, etc. Likewise, the impact of the formation of networking due to group lending on entrepreneurial activities such as identification of an opportunity, risk-taking attitude and the learning and information effects on the members of the group could be analysed. Also, to facilitate the acceptability of various microfinance schemes, research can be done to explore culturally sensitive implementation designs.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.