Abstract

The paper evaluates the contracting problem between a platform and a seller under information asymmetry where the seller holds private information about his/her cost for product quality. Price per product is influenced by seller’s product quality and platform’s service quality. Cost-sharing contract is more desirable as it induces a higher level of qualities and generates higher profit for the platform compared to revenue-sharing contract. The product quality and platform’s service quality vary negatively with the ad-valorem tax imposed on price of the product. We then introduce advertising in our model and observe that the level of advertising is lower under information asymmetry.

Introduction

The present era is marked by an exponential growth of the e-commerce sector. The e-commerce sales reached $ 4.28 trillion in 2020, and it is expected to grow to $ 5.4 trillion in 2022. 1 The global website visits grew substantially from 16.07 billion in January 2020 to 22 billion in June 2020. 2 Moreover, the Covid-19 pandemic led retail e-commerce revenue to grow at a striking rate of 25%. 3 The growing platform market is subject to several disputes over sales proceeds sharing between platform providers and sellers who continue to argue over getting unfair share of revenue (Sur et al., 2019). Thus, contract design between them has been one of the most important business decisions in the space of digital market (Sur et al., 2019).

We emphasize the contract design between a platform and a seller targeting the customer pool through the intermediary platform where price per product that a consumer pays is influenced by seller’s product quality and platform’s service quality. Under complete information, a simple contract can help the platform to squeeze out all the first-best profit, giving the seller only his/her reservation value. However, under information asymmetry when the seller holds the private information about the cost for product quality, the efficient seller can achieve higher profit than the reservation level at the cost of the platform. Next, we introduce the ad valorem tax in our model where the government levies per unit tax on price paid by a consumer. Sensitivity analysis emphasizes the effect of tax on product quality, service quality and profit of the platform.

The rest of the study proceeds as follows. The detailed review of the literature along with the major contributions of our study to the literature has been provided in the second section. We establish the basic framework with two possible kinds of sellers in the third section. The fourth section explores two common forms of contract structure and examines the effect of tax on contract variables for both types of contracts. The fifth section compares the findings obtained for two contracts. The sixth section introduces the effect of advertising on our analytical model. Ultimately, the seventh section draws the conclusion of the paper.

Review of Literature

There exists a gamut of literature concerning the contracting problem of retail platform and supply chain networks. Ma et al. (2013) regarded a supply chain in their study where demand is affected by retailer’s marketing effort and manufacturer’s quality effort. The paper discussed different kinds of contracts and concluded that the two-part tariff contract with both kinds of cost-sharing (CS) (marketing cost and quality cost) by the members of supply networks coordinates the members well and increases the total profit. Zhang et al. (2019) discussed two types of contracts, revenue-sharing (RS) and fixed fee contracts in platform-manufacturer setting and figured that fixed fee contract leads to higher quality compared to RS. Roger and Vasconcelos (2014) studied the moral hazard for two-sided platform in infinite horizon structure and found that registration fees along with transaction fees alleviate moral hazard. Ma et al. (2017) analysed the optimal contract in the presence of information asymmetry for supply chain where the manufacturer influences the demand by investing on corporate social responsibility. Mukhopadhyay et al. (2008) studied the contracting problem with information asymmetry for mixed networks where manufacturer not only sells through retailer but it also directly targets the consumer pool. Babich et al. (2012) explored the buyback contract problem with one supplier and one retailer who has private information about the state of demand.

The contribution of our study is that we discuss a crucial topic regarding the coordination problem between two agents of the platform and derive the optimal choices for the platform and the seller for the two most commonly adopted agreements, RS and CS contracts under asymmetric information, an issue that has not been received exhaustive and in-depth research attention in literature pertaining to online platforms. In addition to this, we keep the service quality of platform as an endogenous choice under contracting decisions which has not previously been studied in the existing literature on online platforms, to the best of our knowledge.

Our study contributes to the literature on contract design with the following results. The key finding obtained is that the optimal contract in presence of information asymmetry induces high type seller to supply product quality less than the first-best quality when service quality is endogenous. This result sets a major departure from the standard one-sided model which states the high type seller to provide first-best efficient quality in presence of information asymmetry. Additionally, the platform supplies lower level of service quality compared to first-best quality in presence of asymmetry. We then compare the optimal values of contract variables for two contracts and conclude that CS contract is more desirable as it induces higher level of product quality, service quality and platform’s profit compared to RS contract. Comparative static analysis shows the product quality, service quality and profit of the platform are negatively related to tax rate. A numerical analysis based on certain parameter values has been conducted to validate the analytical findings. Finally, we introduce advertising in our model and observe that platform uses more advertising signals in complete information case when it is certain about the type of the seller.

The Model

Consider a digital marketplace with one intermediary platform and one seller. The seller produces a product with quality ‘q’ at a unit cost of β and enters into a contract with the monopoly platform in order to sell the product to final consumer at a unit price P against a payment of a part of his/her revenue, α to the platform. The seller gives a fraction of his/her revenue to platform to be able to trade on it. Moreover, the platform is providing services to all the buyers and the service quality of platform is represented by ‘s’. The services offered by the platform to buyers can be considered as a composite measure for daily service level settled by platform like return and refund policy, replacement policy, delivery speed etc. All these come under the category of platform’s services. We assume, per unit price is a function of product quality, q and service quality, s;

This may be interpreted as consumers’ willingness to pay per unit of product where

The profit of the platform is influenced by the quality choice made by the seller. If choices are easily verifiable, the agreement between the seller and the platform would be pretty straightforward. However, when there is no way for platform to notice the seller’s choices then a contract must be designed in a way that elicits seller to choose the right action. Depending on the unit cost for quality of product, the following two types of seller can exist: efficient seller (h type) and inefficient seller (l type). An efficient seller can produce a product in a cost-effective way than the inefficient seller and thus incurs lower unit cost for producing the similar quality of product compared to the inefficient seller. Let,

Contract Design

Revenue-Sharing Contract

We discuss the form of contract where seller shares a portion of his/her revenue with platform indexed as α. When the platform exerts services with ‘s’ level of quality and seller of type i produces the product with quality

where

When β Is Observable (First-Best Case)

Optimal Contracting Problem.

A contract between a platform and a seller where both possess the complete knowledge of type of seller can directly state RS rate conditional on β. The contracting problem of the platform can be described as,

where the share of the revenue per product sold that platform receives from seller of type i is amounted to

Given the optimal quality chosen by sellers

Hence, optimal product quality levels chosen by sellers are,

In the optimum

When β Is Not Observable by Platform (Second-Best Case)

Optimal Contracting Problem

In this subsection, we consider the case where platform cannot differentiate the type of seller. If platform proposes an agreement similar to the first-best case in presence of information asymmetries, the seller of type h will end up choosing the contract intended for cost-inefficient seller without revealing his/her true type.

6

In that case the platform must form a contract in a way that elicits seller to reveal his/her true type voluntarily. For this purpose, the platform trusts on the revelation principle (Myerson, 1979), which ensures that the seller reveals his/her true type ‘i’ by choosing the contract designed for his/her type since by doing so, he/she will earn higher profit. Therefore, the revelation principle guarantees that the announced type of the seller is his/her true type. The essence of revelation principle with its truthful revelation property is captured by introducing an additional constraint, Incentive Compatibility (IC) Constraint in our model which assures a seller chooses the particular contract assigned to his/her true type. The characterization of platform’s problem which is to maximize its expected profit subject to IR and IC constraints is outlined as,

Constraints (5a) and (5b) that represent the individual rationality or participation constraints for the seller of type h and l respectively indicate a seller of type i must receive his/her reservation profit if he/she accepts the contract. Constraints (5c) and (5d) which constitute the IC or truth-telling constraints for type h and l seller respectively induce the seller to select that particular contract menu entitled to his/her true state. Let us consider constraint

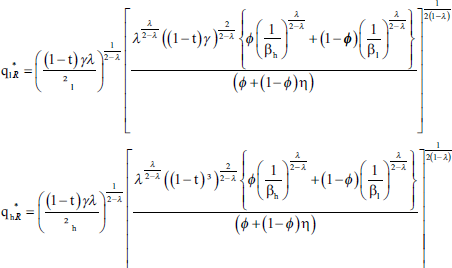

Therefore, the set of optimal contracts obtained by ignoring the constraints

where

The equilibrium contract dependent on type still induces h-type seller to exert higher product quality than the l-type as unit cost for producing similar level of quality is lower for type h than l-type. Thus the equilibrium quality-fee bundle for high type comprises of higher product quality and lower RS fee relative to the bundle for low type.

8

The intuition is that a cost-effective seller (here, h type) will give a lower proportion of its revenue to platform and exert higher product quality and therefore, can expect a higher price per product sold. All these forces in turn contribute to earn higher profits by both the platform and the seller. This is a crucial insight of our study. To complete the investigation on two state framework under RS contract, it can be examined that both the constraints

Comparing Two Regimes Under Revenue-Sharing Model

In this subsection, we compare the results obtained under two regimes of RS contract. We validate the theoretical findings by employing a numerical study with the parameter values as:

With platform has to spend the information rent in presence of information asymmetry, it invests less on service quality than in the first-best regime. Thus, we obtain a strictly lower level of service quality when platform is uncertain about the type of seller. Therefore,

We find an interesting observation regarding the quality of the product sold. If service quality is exogenously given, then the high type seller is provided with the efficient first-best product quality and the optimum bundle for low type seller contains less quality in presence of information asymmetry than under complete information. Thus, the results derived with exogenous service quality are similar to the one-sided market outcomes. However, when we make the service quality endogenous to the system, the findings get altered. With endogenous service quality, the profit maximizing level of product quality for h type seller is strictly smaller under incomplete information case than in first-best regime, that is,

A fundamental and most important point that arises from our study is that the optimal product quality for each type of seller and service quality of platform in the second-best framework are necessarily distorted from the full observable level.

Cost-Sharing (CS) Contract

We analyse a CS model where seller not only offers a portion of his revenue to platform but platform also shares a fraction of product quality cost of seller.

9

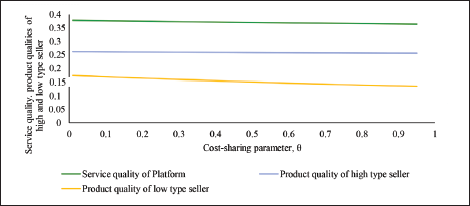

The fraction of product quality cost that seller bears is indexed as θ while the platform shares the remaining fraction,

When β Is Observable (First-Best Case)

Optimal Contracting Problem

Under full information, the platform knows the specific type of seller and thus it proposes the definite contract allotted to the specific type. The platform’s optimal contract problem is illustrated as,

Equation (6) describes the expected profit of the platform under complete information model of CS contract. As discussed earlier, the platform in this case not only receives α portion of revenue from seller but incurs

The equilibrium bundle for high type seller under full information symmetry case of CS agreement comprises higher product quality compared to the bundle for low type.

When β Is Not Observable by Platform (Second-Best Case)

Optimal Contracting Problem

In this subsection, we interpret the optimal contract for the case where the platform cannot exactly know the type of the seller. As explained earlier for the case of RS contract, the high type seller may imitate the low type as he has an incentive to choose the contract pair designated to the low type seller. Thus a contract should be designed in a way that compel seller to truthfully reveal his true type when information asymmetry is present. We begin our analysis by only considering constraints

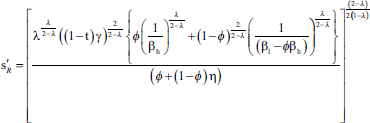

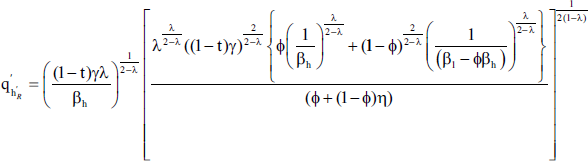

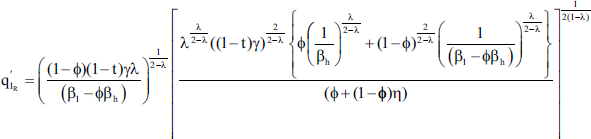

The optimal solution of the above optimization problem can be expressed as

The equilibrium bundle for high type comprises higher product quality and lower RS fee relative to the bundle for low type. It can be easily verified that both the constraints

We examine the contract values

Comparing Two Regimes Under Cost-Sharing Contract

In this subsection, we present the comparison between the two regimes under CS contract and perform a numerical analysis with parameter values

Since the platform has to forgo a part of its profit to acquire the hidden information regarding the true type of the seller under incomplete information case, it chooses to invest less on service quality and that’s why service quality with asymmetric information

A result identical with one-sided market has been derived in incomplete information model of online platform when service quality is exogenously specified (say,

Thus, the high type seller is required to supply the optimum first-best level and low type seller supplies a lower level of product quality with incomplete information compared to the first-best regime when service quality is exogenously given. However, the outcomes modify when we allow quality of service to vary in our model. With the endogenous level of service quality, the optimum level of product quality for h type seller under information asymmetry is significantly lower than the first-best quality. So, we notice a significant departure under information asymmetry regime from one sided market outcome. The equilibrium contract-pair for h type seller contains lower product quality and lower revenue payment to platform than the first-best outcome and l type seller is required to provide smaller level of product quality and higher amount of revenue to platform in case of incomplete information compared to the first best outcome. Both the Figures 8 and 9 show that each type of seller provides higher level of product quality under full information regime than the information asymmetry case. Thus,

Sensitivity Analysis: Revenue-Sharing and Cost-Sharing Contracts

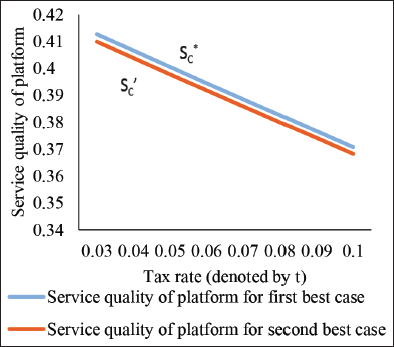

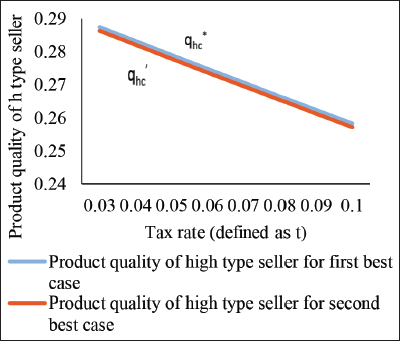

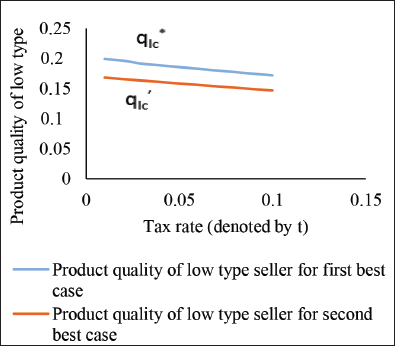

Let us now find the effect of tax on service quality, product quality and profit of platform for both the RS and CS contracts. Proposition 3 outlines the results obtained using comparative static exercise.

The product quality supplied by each type of seller deteriorates as ad valorem tax on product price rises under each information regime of both contracts.

The optimum service quality falls unambiguously as tax on product price increases.

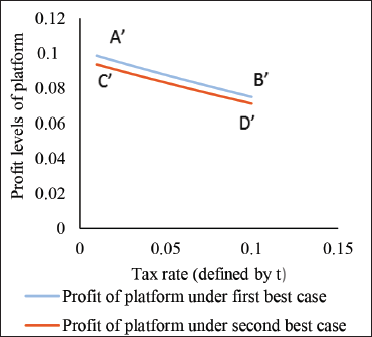

The equilibrium level of profit of the platform decreases with tax imposed on product price.

The intuition behind Proposition 3 is pretty straightforward. As ad valorem tax increases, the seller who receives

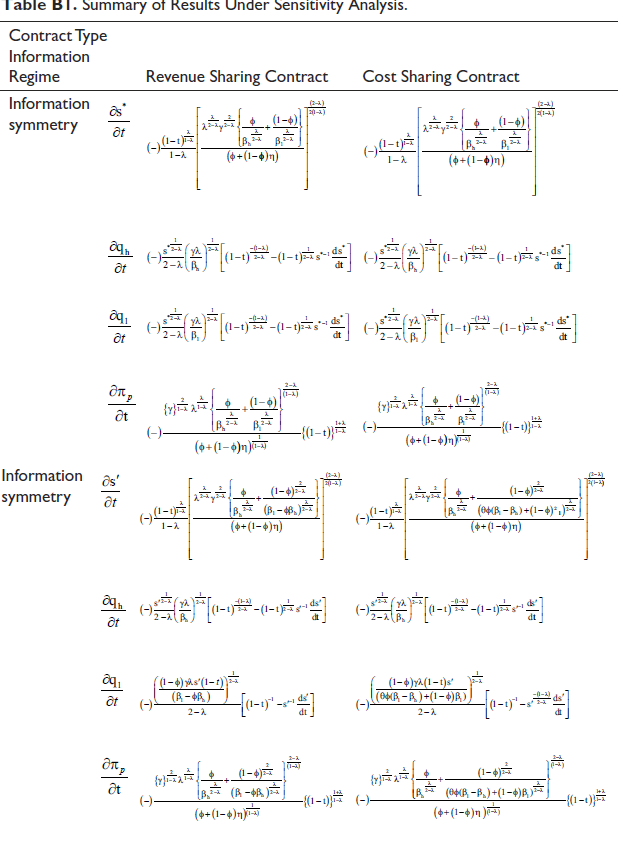

With revenue reduces with tax rate, seller now transfers lower level of his/her revenue to platform. Thus platform spends less on improving its service performance in each regime. Moreover, lower revenue earned per product by seller with rise in tax leads to lower payment of revenue to platform which in turn reduces the profit of the platform. The result for each information regime for either form of contract is summarized in Table 1 (see Appendix B for Table 1).

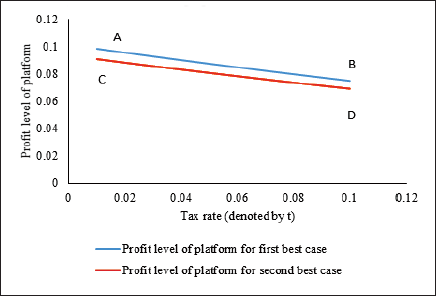

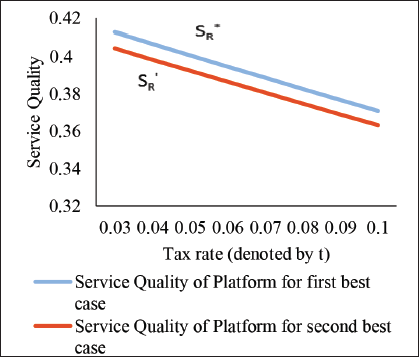

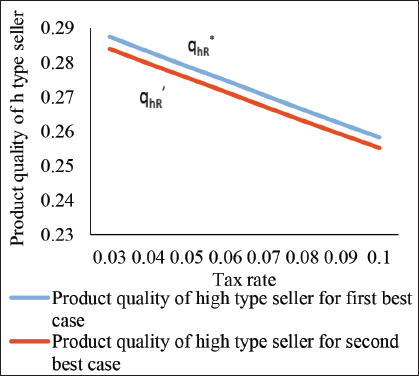

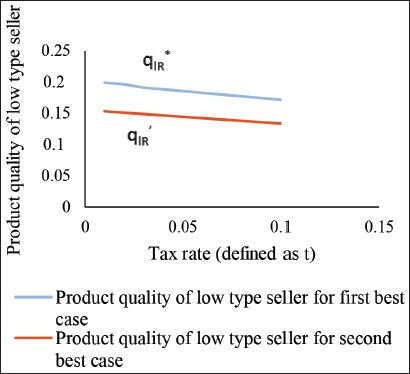

Figures 1 and 6 present the graphical illustration of the relationship between tax and profit level of platform under two regimes of RS and CS contracts, respectively. Both figures support the theoretical finding of negative association between tax and profit of platform as profit lines fall with tax rate. Figures 2 and 7 display the negative relationship between tax rate and service quality of platform under two contract regimes. Both Figures 3 and 4 validate the negative association between tax and product quality of each seller type diagrammatically and Figures 8 and 9 establish that product qualities vary adversely with tax rate.

Comparison Between Revenue-Sharing and Cost-Sharing Contracts

We note that optimal product quality provided by each type of seller and service quality of platform are greater for CS contract compared to the RS agreement in presence of information asymmetry. Thus,

Proposition 4 reveals that platform and each type of seller under RS contract actually underinvests on quality relative to CS contract in presence of information asymmetry. Moreover, by persuading the seller to accept CS contract, platform earns higher profit compared to RS contract. It may be possible that information asymmetry is mitigated to some extent in CS contract when platform not only shares revenue of seller but bears a part of product quality cost of seller as well. Platform can have a better grasp about the type of seller under the CS model as sharing the cost burden helps platform to realize the cost structure of each type of seller. The CS contract is more preferable as it induces the members of online platform to exert better performance. Due to the presence of CS element, seller enables to uplift its product quality provision. Better provision of product quality raises the price per product, which in turn increases the profit earned by both the platform and the seller. Intermediary provides improved services to its users as well under CS contract. Our model derives a crucial facet of contract design by comparing these two forms of contract.

Extension: Introduction of Advertising in the Model

Suppose the platform introduces advertising (defined as ‘a’) to expand the audience base and boost the sales volume. Advertisement helps platform to drive up sales in many ways by generating brand and product awareness among customers, informing them about promotional offers, daily offers, etc. We let,

Differentiating the above profit equation with respect to advertising level, a and making that equal to zero, we attain,

By solving the above first order condition, we get the advertising level under information symmetry case (

From the FOC for profit maximization with respect to advertisement, a, we have,

By solving (11), we get the advertising level under information asymmetry case (

Comparing the first order conditions for profit maximization of platform under first-best case (Equation (10)) and second-best case (Equation (11)) under the RS model, we conclude that the advertising level under first-best case,

Similarly, first-order conditions for both symmetry and asymmetry cases under the CS model are as follows:

By comparing these two conditions (equations (12) and (13)), we infer that platform will deliver higher amount of advertising under information symmetry regime (since

Conclusion

The existing literature pertaining to platforms has paid little attention to contracting relationship concerning the members of platform and impact of taxation under information asymmetry. The present study discusses the issue of contract design between an online platform and a seller when the willingness to pay per product is influenced by the platform’s service quality and quality of product supplied by seller. The model discusses the contracting problem for the case when the platform is not informed about the type of seller, which can be of either high type or low type based on unit cost of product quality. To analyse this issue of contracting, we explore two common forms of agreements: RS and CS. An interesting observation shows that at optimum, high type seller is required to provide less product quality under incomplete information compared to full information for both contracts when service quality is endogenously determined. Most importantly, with hidden information, platform achieves lower profit compared to the first-best profit as the platform gives up a portion of its profit in order to extract the hidden information about the type from the seller. The comparison between two contracts yields that CS contract secures more profit for platform by inducing every member of platform to supply greater quality relative to RS contract. The study then derives the effect of ad valorem tax on contract variables and obtains that product quality, service quality and platform’s profit fall unambiguously with increase of ad valorem tax rate.

We then introduce advertising in our model and find that the platform will invest more on advertising when it is fully informed about the type of the seller rather when it does not know the type. For the future analysis, we will examine the contract design for competitive platform setting and find how competitive setting changes the results found for monopoly platform.

Appendix

From (i) and (ii), we have,

Thus,

Or,

We know,

Or,

Summary of Results Under Sensitivity Analysis.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.