Abstract

The discussion of sustainability reporting rarely addresses the inherent paradox within this concept—tremendous costs associated with sustainability efforts and lack of direct return on these investments. This study contributes to the discussion on sustainability by studying this paradox from the linguistic standpoint in order to answer a simple question: Why are sustainability reports produced? The study’s main contribution is evaluation of the place of sustainability reporting in the corporate communication genre: whether sustainability reporting is a vehicle of fair and objective sustainability disclosure or whether sustainability reporting belongs with marketing and promotional communication.

Since the United Nations raised the profile of sustainability and sustainable development in political, economic, and social agendas in the 1980s, corporations are expected to publicly disclose their sustainability practices. Sustainability disclosure and reporting became an important genre of corporate communication—with dedicated agencies, consultants, rankings, and even awards. But what is the goal of this communication? What are the main reasons these sustainability reports are produced? On one hand, sustainability reporting can be seen in the larger context of corporate disclosure and investor relations, aimed at enhancing understanding of the company’s business models and its value; on the other hand, it may be seen as marketing and promotional communication. This study seeks to contribute to better understanding of this issue by studying it from the linguistic standpoint.

The original proponents at the United Nations introducing the idea of sustainability realized that sustainable development practices are exceedingly expensive and would come at tremendous costs to businesses. They did not expect corporations to be very accommodating and called for complex and stringent regulations in order to ensure compliance from businesses in the area of sustainability: Environmental regulation must move beyond the usual menu of safety regulations, zoning laws, and pollution control enactments; environmental objectives must be built into taxation, prior approval procedures for investment and technology choice, foreign trade incentives, and all components of development policy. (World Commission on Environment and Development, 1987, p. 57)

This is not surprising, as the cost of environmental compliance can be prohibitively high even for the largest corporations, comprising billions of dollars per year; for smaller companies compliance may mean bankruptcy (Becker et al., 2013;Pashigian, 1984).

However, if sustainability compliance is financially ruinous, it would seem that scores of sustainability disclosures would be full of negative news, such as massive expenses forced on corporations by complex governmental regulations with unclear direct benefits to current shareholders and customers, in some cases even threatening the existence of the business itself. Yet, a simple glance at a sample of sustainability reports will quickly show that this is usually not the case. It is difficult to find a more upbeat corporate report than a typical sustainability report. A significant body of research around this phenomenon explains this paradox through the concept ofgreenwashing, or intentional or unintentional exaggeration of claims of sustainability (Chen & Chang, 2013;Guo et al., 2017;Szabo & Webster, 2021). From the greenwashing standpoint, sustainability reports are not vehicles of disclosure of sustainability investments of the company, but instead a tool to appease interested stakeholders and persuade them of the company’s sustainability efforts without having to actually spend money on them. If this is the case, it is no surprise that sustainability reporting, as a genre, would tend to focus on good news only and, as a result, rely on the narrative of optimism in its language. This study puts this assumption to the test by analyzing the level of deployment of linguistic strategy of optimism in corporate sustainability reports in comparison with other corporate reports.

Literature Review

Sustainability

The termsustainable development, or simplysustainability, is generally traced back to the 1987 United Nations report,Our Common Future, which defines it as “development that meets the needs of the present without compromising the ability of future generations to meet their own needs” (World Commission on Environment and Development, 1987, p. 41). The Secretary General of the United Nations Javier Perez de Cuellar established the World Commission on Environment and Development chaired by Gro Harlem Brundtland in 1983. The result of the work of this commission was theOur Common Futurereport, unofficially also known as theBrundtland Report.

The foundational principle of this definition is preserving our habitat while improving our standard of living—a noble desire, yet often called impossible as improving standards of living for the ever-increasing number of people demands an ever-increasing amount of resources and, thus, invariably leads to the depletion of the natural capital (Gatto, 1995;Moffatt, 1994).

Several attempts over the years were made to make the concept of sustainability more meaningful by developing a precise framework for measuring and operationalizing the concept. These frameworks were developed from a variety of standpoints and approaches. Among those frameworks are the Triple Bottom Line; the Natural Step; the Ecological Footprint; ESG: Environmental, Social, and Governance; and many more. The Triple Bottom Line focuses on the need of an organization to measure its bottom line not only in terms of financial profits but also in terms of its impacts on the environment and the society. The Natural Step also combines ecological perspective by measuring substances extracted from the Earth’s crust, increase in new substances produced, and degradation of the ecosystem, with societal perspective by measuring health, participation in society, competence development, fair treatment, and meaning making. The Ecological Footprint framework focuses on measuring on the use of natural resource by the organization as well as its impact on the nature. Finally, ESG proposes measuring and managing organization’s efforts in three key areas: environmental, social, and corporate governance (for more, seeMarshall & Toffel, 2005).

Yet, the challenge remained as the concept remained elusive. For example,Norman and MacDonald (2004)concluded that the Triple Bottom Line may be just a “good old-fashioned single bottom line plus vague commitments to social and environmental concerns” (p. 258). Such vagueness and ambiguity allow companies to make claims about sustainability that may or may actually not be a reflection of sustainable development. This also highlights the importance of sustainability reporting and the information found in these reports in order to evaluate what the corporations are actually doing.

Sustainability Reporting

Sustainability reporting as part of a broader corporate reporting is a function of investor relations.Laskin (2018a)states that one of the key purposes of investor relations is to provide full and timely disclosure in order to enable investors and shareholders as well as other relevant stakeholders to better understand the business model and the fair value of the company (for an overview of investor relations, seeLaskin, 2018c). Sustainability activities have an effect on the company’s valuation and, as a result, are part of such disclosure.

The beginning of sustainability reporting is generally associated with the rapid increase in the external pressure from various stakeholders (Kolk, 2008). These stakeholders are eager to better understand the true impact of organizations, whether positive or negative, toward sustainable development (Neu et al., 1998). In fact, Global Reporting Initiative (GRI), one of the leaders in standardizing sustainability reporting, identifiesimpactas one of the central concepts of its sustainability reporting standards, defined as “effect an organization has on the economy, the environment, and/or society, which in turn can indicate its contribution (positive or negative) to sustainable development” (GRI, 2020, p. 27).

Sustainability reporting is then defined as “an organization’s practice of reporting publicly on its economic, environmental and/or social impacts, and hence its contributions—positive or negative—towards the goal of sustainable development” (GRI, 2020, p. 3). The language of sustainability reporting calls for objectivity, as its stated goal is to provide “a balanced and reasonable representation of an organization’s positive and negative contributions” (GRI, 2020, p. 3). This once again places sustainability reporting squarely in the domain of broader corporate reporting, with its function of fair and timely disclosure of all relevant information to help outside stakeholders make informed decisions about the organization.

Unlike other corporate reports that rely on standardized reporting practices, such as financial reporting, there are many different competing formats that corporations can choose to align with in their sustainability reporting. Among the most recognized are the following: GRI, the International Integrated Reporting Council, and Sustainability Accounting Standards Board. Another important distinction is that sustainability reporting is voluntary. Despite this lack of mandate, however, more and more companies produce sustainability reports. For example, a recent study byGovernance & Accountability Institute (2020)showed that 65% of all companies in Russell 1000 Index produce sustainability reports; if the sample is limited to 500 largest companies, the number of companies producing those reports increases to 90%. The growth in sustainability reporting is commonly celebrated, as it is suggested that such an increase has a correlation with increased importance and role sustainability plays in the corporate world.

The Language of Optimism in Sustainability Reporting

The discussion of sustainability rarely addresses the inherent paradox within this concept—tremendous costs associated with sustainability efforts, on one hand, and lack of direct return from these investments, on the other hand. In fact, environmental regulations are estimated to be costing U.S. corporations billions of dollars (Associated Press, 2019;Eberhart, 2020). Yet, almost any sustainability report is full of praise and acclaim of this very costly investment. It would be understandable if these investments were actually necessary to improve the quality or quantity of products or services, yet quite often this is not the case either. In fact, if corporations would find sustainability necessary on their own, there would be no need for extensive and complex environmental regulations to force the corporations to be more sustainable (Palmer et al., 1995).

As it stands now and from the early days of sustainability, corporations are required to adhere to the norms of sustainability by governmental regulations at enormous costs to their shareholders (World Commission on Environment and Development, 1987). In fact, research shows that corporations that invest in sustainability and receive recognition for their sustainability efforts may get punished by their shareholders rather than being awarded by them (Fisher-Vanden & Thorburn, 2011;Jacobs et al., 2010;Stern, 2007). This contradiction is commonly based on the fact that the interest of the company, its managers, and the shareholders may diverge from the interests of secondary publics, including even “well-organized and vocal interest groups” (Neu et al., 1998, p. 265).

However, we maintain that this paradox is exactly what can explain the phenomenon of the sustainability reports. Literature suggests that the company’s management is incentivized to protect the company from the information that can cause the company’s stock to be undervalued (Alves & Silva, 2021;Jensen, 2005). This view comes in contradiction with the ultimate goal of the investor relations professions of achieving fair valuation (National Investor Relations Institute [NIRI], 2003). AsLaskin (2018b)explains, theoretically speaking, investor relations officers should be as eager to communicate negative information as much as positive in order to help investors achieve better understanding of the company, but practically, it may be more beneficial to use the disclosure to frame the results positively and manage future expectations.

Sustainability reports help resolve this contradiction. The company still communicates the information about its sustainability activities, but it removes it from the annual report, a regulated document aimed at investors and other members of the financial community. This helps the company resolve the tension between the pressure from the shareholders and the secondary stakeholders by creating two separate communication channels targeting these separate entities—the annual report, which in recent years has become either just a 10-K annual report or a 10-K wrap annual report (Laskin, 2018b), and a glossy, magazine-like sustainability report. Since sustainability information is not part of a regulated disclosure and corporations can choose content and format for their sustainability reports at will, these reports may sound very promotional or optimistic, almost like a piece of advertising or public relations rather than corporate reporting.

Two additional factors also have a strong influence on the overly optimistic nature of sustainability reports. First, sustainability reports are aimed at a general audience and, as a result, rarely provide details and specifics behind their environmental claims. Second, because of significant costs of adhering to even the minimum environmental regulations with little or no immediate direct return, corporations tend to focus on words and not actions; in other words, they are investing in sustainability reporting more than in sustainability itself.Kim and Lyon (2015)observe that corporations “may have an incentive to exaggerate their environmental accomplishments through their information disclosure strategies, i.e. to greenwash” (p. 635).

The concept of greenwashing has been extensively studied in the literature, and it is usually recognized as part of a decoupling process that indicates a separation between symbolic gestures and substantive actions or, simply speaking, a gap between words and deeds (Kim & Lyon, 2015; Prasad & Holzinger, 2013; Siano et al., 2017; Walker & Wan, 2012). Greenwashing can also be recognized by the language used, as it tends to employ overly optimistic language focused on positives only. Thus, greenwashing literature has parallels with research on selective disclosure where positive information is exaggerated and negative information is downplayed (Jahdi & Acikdilli, 2009;Laskin, 2018b;Porter & Kramer, 2006;Thoms et al., 2020). However, in previous research, such selective disclosure has usually been studied based on the content rather than based on the language used. Yet, “managing expectations is a rhetorical function . . . thus, analysis of such communication must be based on a rhetorical paradigm” (Laskin & Samoylenko, 2014, p. 199).

As a result, this study claims that it is important to study the usage of words in corporate sustainability reports to form attitudes and induce actions (Burke, 1970). FollowingSymon (2008), who suggests “analyzing linguistic strategies of argumentation as individuals seek to convince an audience of a construction of reality congruent with their interests” (p. 78), the study analyzes the usage of linguistic strategies in corporate sustainability reports in order to determine if such reports are overly optimistic or not. Indeed, if the goal of sustainability reports is greenwashing rather than disclosure, then it can be expected that such reports would be overly optimistic to showcase only positive aspects of how sustainable a corporation is, while problems, costs, and challenges can be omitted.

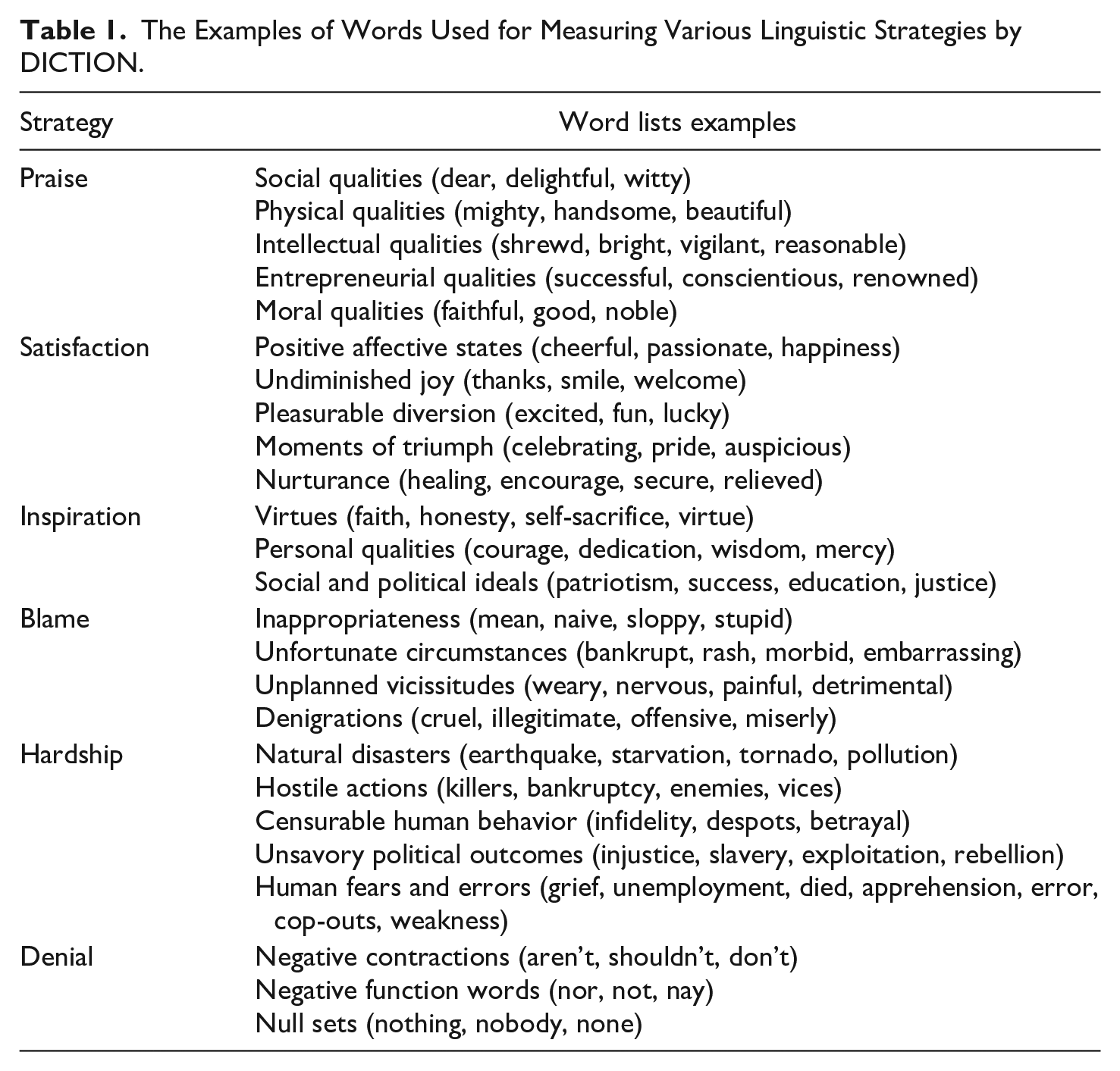

The conceptualization of linguistic strategies comprising optimism is based on a significant body of work conducted by Hart and his colleagues (for overview, seeHart, 2014a,2014b). According toHart (1984), operationalization of optimism is based on inclusion of three positive linguistic strategies and exclusion of three negative linguistic strategies.

First, optimism includes the language ofpraise, where the text has affirmations, isolating social qualities, physical qualities, intellectual qualities, entrepreneurial qualities, and moral qualities (Hart, 1984). As a result, the study proposes the first hypothesis:

Second, optimism includes a linguistic strategy ofsatisfactiondefined as terms associated with positive affective states, undiminished joy, pleasurable diversion, moments of triumph, and words of nurturance (Hart, 1984). As a result, the study proposes the second hypothesis:

Third is a linguistic strategy ofinspiration. Inspiration in this context is defined as abstract virtues deserving of universal respect and as such most of these terms focus on the desirable moral and personal qualities as well as social and political ideals, for example, faith, honesty, dedication, justice, and so on (Hart, 1984). As a result, the study proposes the third hypothesis:

In addition to these three strategies, optimism has three negative linguistic strategies: a strategy ofblamethat is composed of terms designating inappropriateness, unfortunate circumstances, unplanned vicissitudes, and outright denigrations; a strategy ofhardshipthat is composed of terms defining natural disasters, hostile actions, censurable human behavior, unsavory political outcomes, and human fears and errors; as well as a strategy ofdenialthat is based on a dictionary of negative contractions, negative functions words, and null sets (Hart, 1984). As a result, the study proposes the following hypotheses:

As a result of combining the results from these six linguistic strategies, the language of optimism can be represented through the following formula:

Based on this formula, the study proposes the seventh hypothesis:

Confirming or rejecting the seven hypotheses proposed in this study can add to the conversation on the role and function of sustainability reports in the overall genre of corporate communication. These findings may have significant implications for investors and analysts who rely on such reports, for corporations producing those reports, for rating agencies who rank and evaluate those reports, and for the governments who oversee the reporting process.

Method

The study relies on a content analysis method for data collection. Content analysis is a popular research method in management and communication fields as it allows researchers to process large volumes of data, allows to conduct the analysis at the time convenient to researchers, including reanalyzing the data, and is unobtrusive (Babbie, 2016;Neuendorf, 2017). Perhaps, most importantly, content analysis provides an opportunity to study the meaning behind the actions, to study “the values, sentiments, intentions, and ideologies” (Morris, 1994, p. 903). At the same time, content analysis studies based on the linguistic paradigm are quite rare in the management and business literature (Green, 2004;Laskin, 2018b;Sydserff & Weetman, 2002). As a result,Sillince and Suddaby (2008)call for scholars of managerial, organizational, and strategic communication to increase theorizing from the standpoint of linguistics and rhetoric.

This study uses a computerized content analysis by relying on DICTION software, employing a computer algorithm to examine textual content instead of human coding. This approach eliminates one of the key weaknesses of content analysis—the lack of reliability of human coders. In addition, DICTION’s primary function is the measurement of five key linguistic strategies in written communication, one of which is optimism, which creates a perfect match between the tool and the purpose of this study, which is measuring optimism in sustainability reports (DICTION, n.d.-b).

At the same time, computerized content analysis has its own limitations and is not appropriate for every type of research question (for more, seeMcKenny et al., 2013;McKenny et al., 2018;Short et al., 2010).Hart and Childers (2005)propose that one of the suitable research questions for computerized content analysis, and DICTION software specifically, can be the deployment of communicative strategies. As a result, this study, focused on the linguistic strategies deployed in corporate sustainability reports in order to express optimism, relies on the computerized content analysis performed by DICTION software.

DICTION is one of the most widely used computerized content analysis software used in the academe (Short & Palmer, 2008). Hundreds of books, book chapters, peer-reviewed journal articles, monographs, and papers have relied on DICTION for data analysis. Several studies provide comparisons of various computerized content analysis instruments in organizational research, indicating the important role such software can play extracting meaning from language (Alexa & Zuell, 2000;Short et al., 2018). Several studies focused specifically on DICTION and its validity and reliability (for review, seeHart, 2014a,2014b). DICTION has been used to study various linguistic strategies in a variety of contexts: political speech (Tortola & Pansardi, 2019), corporate communication (Bligh et al., 2004), education (Abelman, 2014), and so on. Several studies specifically applied DICTION to study corporate reports (Abdelrehim, 2014;Laskin & Samoylenko, 2014;Ober et al., 1999;Yuthas et al., 2002). Many other studies used DICTION in a variety of contexts (for more, seeDICTION, n.d.-a).

As explained above, the language of optimism is composed of six linguistic strategies. In order to identify each of these strategies, the DICTION software uses predefined dictionaries to create lists of words related to these strategies, scans the texts against these lists, and converts the resulting relatedness into frequencies that can then be processed as numbers. The word lists are provided by the DICTION software. SeeTable 1for examples of words used for identifying the linguistic strategies of optimism.

The Examples of Words Used for Measuring Various Linguistic Strategies by DICTION.

A significant benefit of content analysis is its ability to compare the results of analyzing specific content with other available content. In organizational research, content analysis can be used to compare a corporation with industry norms or with wider trends. DICTION generated expected normal ranges based on prior analysis of over 50,000 various texts. Applying DICTION to linguistic strategies of optimism in sustainability reporting allows us compare the deployment of linguistic strategies in these texts with the normal range of typical usage of these strategies. The norm is calculated as a mean of all the text analyzed. The normal range is encompassed within +1 and −1 standard deviations from the found mean. Therefore, results within ±1 standard deviation of the expected mean will be within the normally expected range. However, if the result is outside ±1 standard deviation from the mean, the difference can be treated as significant—such a result is outside the expected normal range.

Perhaps even more useful is the fact that it is possible to select the type of the norm that the content is being compared to: from celebrity news to newspaper editorials to political speeches to poetry. It is customary to expect different levels of deployment of various linguistic strategies in different narratives—music lyrics rarely sound the same as news releases. As a result, when selecting a norm, DICTION allows researchers to choose a specific genre to compare their text against. This study uses DICTION’s category of corporate reports as the most appropriate normative comparison for corporate sustainability reports. Indeed, if sustainability reports are expected to serve as a disclosure vehicle similar to other forms of annual corporate reporting, the means should be in similar ranges.

Since the norm for optimism in corporate reports is rather low, the lower border of the normal range was reaching zero. In the case of positive strategies, such asPraise(normal range 0-5.13),Satisfaction(0-1.99), andInspiration(0-7.14), this did not pose a problem during the analysis. It was also not an issue for the combined measure ofOptimism(normal range 47.92-52.50). However, for negatively coded strategies,Blame(0-2.36),Hardship(0-3.78),Denial(0-6.18), this created a methodological challenge because the hypotheses stated that the study expects the results below the norm. It would be impossible to have a frequency below zero. To resolve this methodological challenge, the study split the normal range in half—the result in the lower half (below the mean) of the normal range would be considered supporting Hypotheses 4 through 6; and the result in the upper half of the range or outside the range would be considered not supporting these hypotheses.

DICTION standardizes the score for each of these six variables by comparing these results with the expected means. As a result, when these standardized scores are combined, it creates the standardized overall measure ofOptimismthat can be compared with the optimism scores of other corporate reports.

The sample of reports for the study is based on the ranking of the best sustainability reports,The Global 100. This ranking of the world’s most sustainable corporations has been calculated every year since 2005 by Corporate Knights and announced at the World Economic Forum in Davos with the vision to “provide information empowering markets to foster a better world” (Corporate Knights, n.d.). The ranking includes only publicly traded companies with revenues of no less than 1 billion dollars. The scores are based on the publicly available data in 21 key performance indicators from areas such as resource management (including energy usage, renewable energy usage, water usage, waster production, etc.), employee management (employee turnover, injuries, and fatalities, women in management, etc.), financial management (including paying sufficient amount in taxes, spending money on innovation, supporting pensions, etc.), clean revenues (percentage of products and services that are categorized as clean), and supplier performance (Corporate Knights, 2020).

The study used a purposive sample by examining the 2019 sustainability reports submitted by the top eight companies leading Corporate Knights’ 2020 Global 100 sustainability ranking: Orsted (wholesale power); Chr. Hansen (food and chemicals); Neste (petroleum); Cisco Systems (communication equipment); Autodesk (software); Novozymes (specialty chemicals); ING Groep (banking); and Enel (wholesale;Corporate Knights, 2020). Selecting the companies that are recognizable for their actual performance by a well-established ranking somewhat guarantees that they actually invest resources in sustainability and thus incur costs associated with sustainable activities. Thus, if they see the goal of sustainability reports as full and fair disclosure rather than greenwashing their reports would reflect both positive and negative aspects of sustainability initiatives.

Results

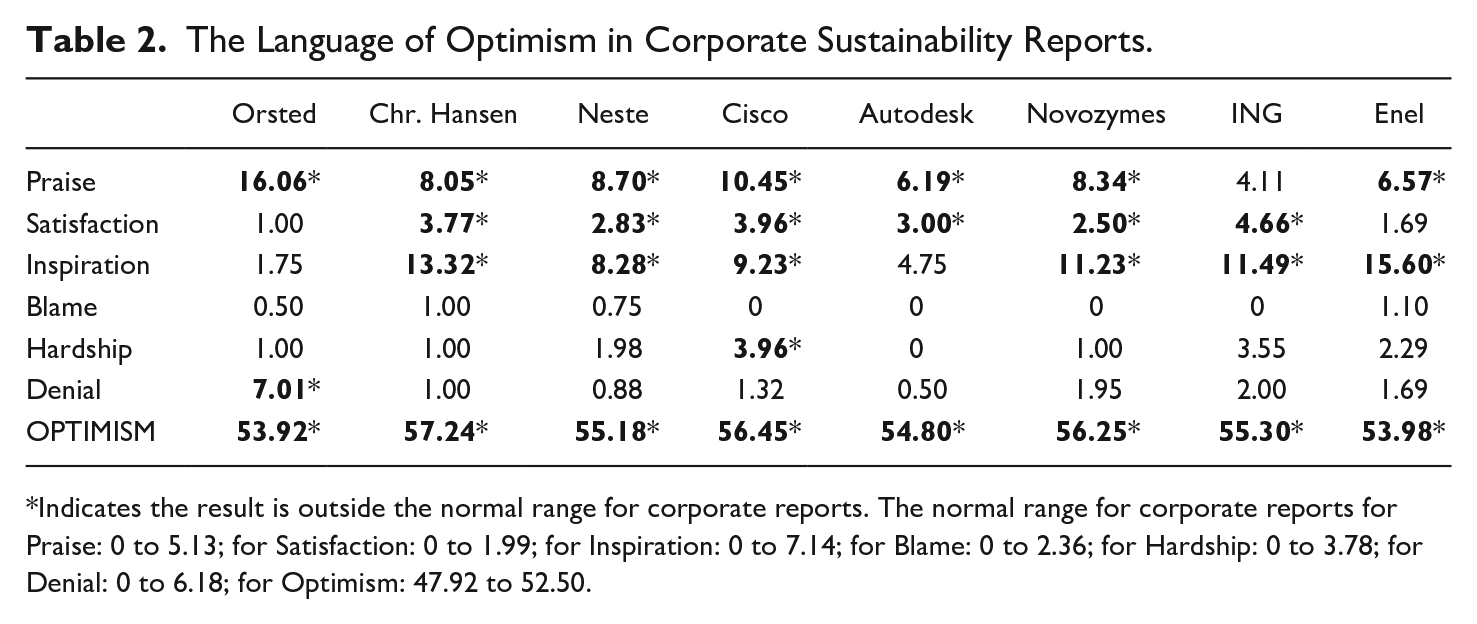

Hypothesis 1 proposed that sustainability reports would have a higher than normally expected level of linguistic strategies of praise. The hypothesis is supported for seven out of eight reports analyzed (seeTable 1). One of the reports,Orsted (2019), has more than triple the score (16.06) of the highest number in the normal range for corporate reports (5.13);Cisco Systems (2019)has double the score (10.45). This shows a very strong reliance on the language of praise in the corporate sustainability reports. Orsted’s (2019) report, for example, uses lots of praise when talking about its sustainability initiatives. The report praises its leadership: “that’s what the leadership is all about”; praises the company: “we have transformed . . . to a global energy leader”; praises the employees: “dedicated and talented”; and praises the overall industry: “inspire climate action beyond our own company.” The only sustainability report that stayed within the normal range for the variable of praise was ING Groep’s (2019) report (4.11).

Hypothesis 2 suggested that sustainability reports would have a higher than normally expected level of linguistic strategies of satisfaction. The hypothesis is supported for six out of eight reports analyzed. Here ING Groep’s (2019) report (4.66) was the leader with the score of more than double of the highest score within the normal range (1.99).ING Groep (2019)constantly highlighted its happiness with what they achieved already—these positive affective states are the foundation of the satisfaction variable. It uses many words connected to the satisfaction variable: successful, effective, encouraged, positive, and similar. Reading the report, one notices how the text focuses on what was already done rather than on what is being done or what will be done in the future. ING reported how it “sharpened our understanding of the potential impact of climate risk”; how it developed and approved its “high-level plan”; how it is a step ahead of “societal expectations”; and how it “played a leading role” (ING Groep, 2019). The company notes that it was “the first to say ‘no’ to coal-fired power” and “have helped finance billions worth of investments in renewable energy.” The CEO of ING concludes that “we are living up to our promise” and have “moved beyond commitments to action.” Two sustainability reports, however, stayed within the normal range for the variable of satisfaction: Orsted’s (2019) report (1.00) and Enel’s (2019) report (1.69).

Hypothesis 3 suggested that sustainability reports would have a higher than normally expected level of linguistic strategies of inspiration. The hypothesis is supported for six out of eight reports analyzed. This time Enel’s (2019) report (15.60) showed the highest score in relying on this linguistic strategy with the score of more than double of the highest score within the normal range (7.14). The score relies on words that reflect virtue and desirable qualities—for example, the report uses words like trust, responsibility, proactivity, and innovation. TheEnel (2019)report intentionally inspires readers with claims of making the world “more prosperous, more inclusive and more resilient, without leaving anyone behind”; “a revolution in the world of energy”; and “generating sustainable growth and creating value for all: customers, society, the environment and shareholders.” Two sustainability reports, however, stayed within the normal range for the variable of satisfaction: Orsted’s (2019) report (1.75) and Autodesk’s (2019) report (4.75).

Hypothesis 4 suggested that sustainability reports would have a lower than normally expected level of linguistic strategies of blame. The hypothesis is supported for all sustainability reports analyzed. In fact, four reports did not use this strategy at all:Cisco Systems (2019),Autodesk (2019),Novozymes (2019), andING Groep (2019). Enel’s (2019) report (1.10) had the highest score, but it was still less than half of the normally expected range score (0-2.36).

Hypothesis 5 suggested that sustainability reports would have a lower than normally expected level of linguistic strategies of hardship. Although seven out of eight reports were within the normal range (0-3.78), one report, Cisco System’s (2019) report, used the strategy more than normally expected (3.96). Only one report,Autodesk (2019), did not use this strategy at all, and three others, Orsted’s (2019) report (1.00), Chr. Hansen Holding’s (2019) report (1.00), and Novozymes’ (2019) report (1.00), scored in the bottom half of the normal range on the hardship linguistic strategy usage.

Hypothesis 6 suggested that sustainability reports would have a lower than normally expected level of linguistic strategies of denial. This hypothesis was generally supported as seven out of eight reports analyzed scored in the bottom half of the normal range (0-6.18) withAutodesk (2019; 00.50),Neste (2019; 00.88), andChr. Hansen (2019; 1.00) scoring the lowest. One report, however,Orsted (2019)scored (7.01), above the normally expected range.

Putting all these findings together, Hypothesis 7 suggested that sustainability reports would have a higher than normally expected level of optimism. The hypothesis is supported for all sustainability reports analyzed. The most optimistic reports were produced by Chr. Hansen (57.24), followed by Cisco Systems (56.45), and followed by Novozymes (56.25). SeeTable 2for the summary of the results.

The Language of Optimism in Corporate Sustainability Reports.

Indicates the result is outside the normal range for corporate reports. The normal range for corporate reports for Praise: 0 to 5.13; for Satisfaction: 0 to 1.99; for Inspiration: 0 to 7.14; for Blame: 0 to 2.36; for Hardship: 0 to 3.78; for Denial: 0 to 6.18; for Optimism: 47.92 to 52.50.

Discussion and Conclusion

The study focused on answering a question of why sustainability reports are produced. The results of the study show that corporate sustainability reports tend to be very optimistic documents. In fact, every single report this study analyzed showed higher than normal optimism scores, confirming the hypothesis that sustainability reports tend to be overly optimistic. The finding that these reports use linguistic strategies of optimism in significantly different ways from other comparable corporate reports raises a question regarding whether these sustainability reports are designed with a different function in mind. Is their function really to provide a full and truthful disclosure, or is their function to appease vocal stakeholder groups without actually making any changes in operations, as the greenwashing proponents would suggest?

Since the optimism was operationalized through three positively charged linguistic strategies (praise, satisfaction, and inspiration) and three negatively charged linguistic strategies (blame, hardship, and denial), it is possible to compare which types of strategies make a larger contribution to the optimistic tone of the reports. Looking at the positive strategies, it is clear that almost all of them are significantly outside the normal range. With just a very few exceptions, corporations in this study utilize words of praise, satisfaction, and inspiration when talking about their own performance in the area of sustainability. In fact, in quite a few cases, the positive results exceed the highest expected range for corporate reports by two or three times. At the same time, despite the facts that these achievements must have come at a cost, there is no comparable increase in the negatively coded strategies of blame, hardship, and denial—in fact, these strategies do not exceed the threshold. Specifically, for most of the reports, these negatively coded strategies score in the bottom half of the range, showing low or even nonexistent usage of these linguistic strategies.

The enormous gap between the reality of expensive and complex sustainable development and the rosy picture portrayed in the sustainability reports of corporations leading in the sustainability rankings is nothing new. It has been well documented, primarily through case studies. For example, the case of the Volkswagen emission scandal showed how the reality can differ from its portrayal in the sustainability reports. Volkswagen received multiple global sustainability reporting awards in 2012, 2013, and 2014, just as it was deploying the software for its diesel cars programmed to cheat the emission testing in order to violate provisions of the Clean Air Act (Allam et al., 2020).

This study, however, was able to go beyond case studies and look at the current top leaders of the sustainability reporting, the ones not in the midst of any scandals. Yet, it still found the same overly optimistic language and a lack of genuine discussion of difficulties or costs of sustainability. This may suggest that sustainability reporting as a genre belongs with marketing publications rather than with corporate reports. In this case, it should be treated as a piece of corporate promotional materials and not treated as a disclosure document. Based on the limited sample in this study, it is also possible to theorize that there may not be much of a difference between greenwashing and green disclosure, as both overstate the positives and downplay the negatives.

The study also suggests a cautiousness in celebrating the increased number of sustainability reports produced by global corporations. The increase in the number of sustainability reports may be a negative signal as it suggests the removal of this information from other corporate reports and slotting it into a niche for tailor-made consumption customized for specialized stakeholders. Sustainability reports also have less oversight and standardization in comparison with corporate annual reports, making it easier for companies to greenwash if they choose to do so.

Perhaps to improve their relationships with a variety of stakeholders, corporations may benefit from a more honest and more comprehensive discussion of their sustainability programs, including costs, challenges, and even failures. For example, when companies were learning how to build their relationships with shareholders, the instinct often was to hide the bad news and focus only on the good in order to push the price of the stock up at all costs. In fact, one of the earlier definitions of investor relations from the NIRI stated that the goal of investor relations should be an increase in the share price—arguably, a position that can explain a chain of accounting scandals in early 2000s (Laskin, 2018a). Today, however, NIRI calls on investor relations professionals to focus on fair market valuation by communicating all the relevant information, encouraging fairness and objectivity over a higher-share-price-at-all-costs approach (Laskin, 2018a). Probably, this is the direction where sustainability reporting should be developing: explaining true costs and challenges of sustainability, while also showcasing the benefits of these efforts.

These findings may have significant implications not just for the corporations who produce those reports but also for investors and analysts who rely on such reports. If investors realize that such reports are marketing communication rather than disclosure documents, they will treat them differently and approach them with restraint. Perhaps such reports can be a starting point for a conversation with a company’s management but not a final source of information. The same concern could apply to various ranking agencies, enforcement organizations, and governments who strive to evaluate and standardize the sustainability reporting processes.

Finally, with all the efforts the governments and nongovernmental organizations put in sustainability regulations and enforcement, it may be time to make sustainability reporting a required part of corporate disclosure with clear and universal guidelines, deadlines, and procedures. The laissez-faire approach to sustainability reporting does not seem to be working.

Limitations and Future Research

The study limited its sample to the 2019 sustainability reports submitted by the leaders in sustainability practices, as it was deliberately seeking the companies that invest significantly in sustainability. Thus, the sample included top eight companies in sustainability as measured by 2020 Corporate Knights ranking. Such a purposive sample, however, makes generalizations impossible. Future research should use probability samples to be able to describe larger populations of companies. This study, similar to other content analysis studies, was limited by the recorded content available for analysis. The software chosen for this study, DICTION, also has its own limitations. It primarily relies on vocabulary counts to determine the tone of a message but cannot interpret when words are used to mislead or indicate irony, sarcasm, or humor. As a result, any words used in an indirect manner will be counted as though used in their direct meaning. Furthermore, because DICTION cannot measure “how and why the words are chosen in text” (Short & Palmer, 2008), future studies should supplement DICTION studies with interviews and surveys of executives and others responsible for producing content. Future research could also use other methods, such as survey research, for example, to get access to information not recorded. Sustainability reporting is a topic of growing importance, and future research should also use qualitative approaches to add to the predominately quantitative studies that exist today. There is not enough linguistic research in the management literature, yet the language can have a strong effect on the interpretation of financial and nonfinancial information—as a result, more research needs to be based on the linguistic and rhetorical tradition.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Author Biographies