Abstract

We investigate how academic entrepreneurs who maintain their primary paid jobs at academic institutions while engaging in entrepreneurial activities differ from other entrepreneurs in choosing funding sources and exit modes. We suggest that academic entrepreneurs prefer to exit through acquisitions instead of initial public offerings to mitigate the role conflict arising from competing academic and industrial institutional logics. We also argue that ventures founded by academic entrepreneurs are more likely than other ventures to receive funding from corporate venture capital investors because such investment relationships can help them achieve their preferred exit mode of acquisition by effectively disclosing the value of their technological resources to potential acquirers. We test our arguments using a sample of U.S. medical device ventures.

JEL CLASSIFICATION: L26; M13; G24

Introduction

Academic institutions have become increasingly engaged in entrepreneurial activities by commercializing the research output and associated intellectual property developed by faculty and researchers (Bercovitz & Feldman, 2006; Siegel & Wright, 2015). Among the various means of university commercialization, academic entrepreneurship has emerged as a core component (Agarwal & Shah, 2014; Hayter, 2016; Kenney & Patton, 2011; Shane, 2004; Wennberg et al., 2011). Accordingly, a growing body of research has examined these entrepreneurs—faculty and researchers who establish ventures while remaining employed by academic institutions (hereafter, academic entrepreneurs)—and documented systematic differences between their ventures and those founded by nonacademic entrepreneurs (Fini et al., 2022; Fischer et al., 2019; Roche, 2023; Roche et al., 2020).

A key insight from this literature is that academic entrepreneurs are embedded in an academic institutional logic that emphasizes the advancement and open diffusion of fundamental knowledge (Klingbeil et al., 2019; Merton, 1973; Perkmann et al., 2019; Sauermann & Stephan, 2013; Stuart & Ding, 2006). This embeddedness differentiates them from other entrepreneurs even at the point of entry into entrepreneurship. Whereas many entrepreneurs are primarily motivated by financial rewards, academic entrepreneurs often pursue entrepreneurship to enhance their academic reputation by diffusing their research outcomes through commercialization (Balven et al., 2018; Hayter, 2015; Hossinger et al., 2020; Huyghe et al., 2016).

While academic entrepreneurs possess a distinctive mindset grounded in academic institutional logic, prior research comparing academic and nonacademic ventures has emphasized other characteristics, such as founders’ expertise and their access to university resources (Bolzani et al., 2021; Fuller & Rothaermel, 2012; Park et al., 2024; Roche et al., 2020). As a result, it remains unclear how academic institutional logic shapes academic entrepreneurs’ managerial decisions along the growth path of their ventures. In this article, we address this gap by examining how academic entrepreneurs’ strong commitment to academic institutional logic makes their ventures differ from those founded by nonacademic entrepreneurs in the choice of funding sources and exit modes—decisions that represent critical milestones in a venture’s life cycle (Pauley, 2025; Wasserman, 2003). In doing so, we focus on the role conflict experienced by academic entrepreneurs as they escalate their involvement in entrepreneurial activities and face increasing pressure to conform to an industrial institutional logic (Sauermann & Stephan, 2013; Zhang et al., 2021; Zou et al., 2023). Specifically, we theorize that exiting through an acquisition entails less role conflict than exiting via an initial public offering (IPO), thereby increasing academic entrepreneurs’ preference for acquisitions. We further argue that this exit orientation leads them to choose corporate venture capital (CVC) rather than independent venture capital (IVC) as a funding source, because CVC investors are better positioned to facilitate acquisition outcomes.

We test these theoretical arguments in the US medical device industry, a setting characterized by substantial faculty entrepreneurship (Zhang, 2009) and established firms’ active CVC investments in small ventures (Chatterji, 2009; Dushnitsky & Lenox, 2005; Katila et al., 2008; Medicare Payment Advisory Commission [MedPAC], 2017). Our theory and findings contribute to two bodies of literature. First, we contribute to research on academic entrepreneurship, which has provided important insights into the discrepancies between academic and industrial environments (Bercovitz & Feldman, 2008; Jain et al., 2009; Lam, 2011; Rasmussen, 2011; Shane, 2004). We extend this literature by identifying role conflict, stemming from academic entrepreneurs’ strong adherence to academic institutional logic, as a defining characteristic. We further suggest that such role conflict exerts a persistent and significant influence on multiple milestone decisions, including the choice of funding sources and exit modes. Second, we extend prior work on the antecedents of CVC investments, which has mainly focused on firm- and industry-level drivers and constraints on CVC investment (Basu et al., 2011; Dushnitsky & Lenox, 2005; Dushnitsky & Shaver, 2009; Katila et al., 2008; Weniger & Jarchow, 2023). Our results show that CVC financing decisions can hinge on founders’ role-based career considerations and exit intentions.

Literature Review

Academic Entrepreneurship

Academic entrepreneurship has emerged as an important mechanism through which knowledge generated within universities is transferred to industry (Grimaldi et al., 2011; Hsu & Kuhn, 2023; Mowery & Shane, 2002; Siegel & Wright, 2015). This rise was spurred by policy changes (e.g., the Bayh-Dole Act in the United States) that granted universities and researchers ownership of the outcomes of publicly funded research (Siegel & Wright, 2015). Universities commercialize knowledge through a range of mechanisms, including patenting and licensing, university–industry collaboration, and the creation of university spinoffs (Anon Higon & Diez-Minguela, 2024; Bercovitz & Feldman, 2006; Fuller & Rothaermel, 2012; Hsu & Kuhn, 2023; Martínez-Noya & Narula, 2018; Marx & Hsu, 2022; Mindruta, 2013). Among these mechanisms, academic entrepreneurship, in the form of university spinoffs, has become a prominent means by which universities commercialize their technologies (Bercovitz & Feldman, 2006; Perkmann et al., 2013). Although various definitions of university spinoffs exist in the literature, we focus specifically on ventures founded by academic entrepreneurs—defined as university faculty and university-affiliated researchers who maintain their academic positions (Fini et al., 2022; Fischer et al., 2019; Roche, 2023). We adopt this definition for our theoretical and empirical context because these actors play a primary role in generating and disclosing the scientific knowledge that constitutes the basis of academic entrepreneurship (Ching et al., 2019; Jain et al., 2009; Lach & Schankerman, 2008; Roche et al., 2020). 1

Consistent with increasing attention paid to these ventures founded by academic entrepreneurs, prior research has examined how they are different from more conventional forms of entrepreneurial ventures. Specifically, some studies emphasize academic entrepreneurs’ scientific expertise as a key dimension along which their ventures differ from those founded by nonacademic entrepreneurs, as their entrepreneurial activities tend to be anchored in their cutting-edge, discipline-specific knowledge bases (Fuller & Rothaermel, 2012; Park et al., 2024). The influence of this specialized expertise is particularly pronounced in the context of new technology-based firms (NTBFs), where academic ventures frequently operate (Colombo & Grilli, 2010). These firms typically derive competitive advantage from advanced technological knowledge and the commercialization of scientific discoveries, particularly in knowledge-intensive sectors, such as biomedicine and information and communications technology (García-Cabrera et al., 2021; Garg et al., 2025; Ruiz-Jiménez & Fuentes-Fuentes, 2016; Sánchez-González & Herrera, 2014). Therefore, academic entrepreneurs often focus on technological knowledge in early development stages, which are, in general, intended to generate product (rather than process) innovations in high-technology industries (Agarwal & Shah, 2014; Feldman et al., 2002; Roche et al., 2020; Shane, 2004; Stuart & Ding, 2006).

Other scholars further note that academic entrepreneurs benefit from privileged access to scientific resources and institutional networks that are typically unavailable to nonacademic entrepreneurs (Bercovitz & Feldman, 2006; Roche et al., 2020). These resources include laboratories, research infrastructure, and university-based support mechanisms that facilitate early-stage experimentation and knowledge development (Bolzani et al., 2021). Moreover, technology licensing offices (TLOs) provide crucial support in securing intellectual property protection, which is particularly beneficial for science-based ventures (Colombelli et al., 2016; Fini & Grimaldi, 2017; Phan & Siegel, 2006). Consistent with this view, Ching et al. (2019) show that faculty-led ventures are more likely than nonacademic ventures to pursue control-oriented appropriation strategies, adopting more formal intellectual property protection, often with the support of TLOs, rather than relying primarily on market-based execution.

Although these dimensions help characterize academic entrepreneurs and their ventures, the feature that most distinctly differentiates them from nonacademic entrepreneurs is the role conflict arising from their simultaneous involvement in academic and entrepreneurial environments (Choi et al., 2024; Jain et al., 2009; Zhang et al., 2021). Accordingly, we review research on institutional logic and role conflict in the context of academic entrepreneurship.

Institutional Logics and Role Conflicts in Academic Entrepreneurship

Institutional logics are socially constructed and historically patterned sets of practices, values, assumptions, rules, and beliefs that provide meaning to actors, underpin their identities, and designate what is legitimate within a given domain (Friedland & Alford, 1991; Thornton & Ocasio, 2008; Thornton et al., 2012). As individuals internalize a particular logic, it becomes integrated into their self-concept, strengthening identification with the relevant role and increasing the likelihood that their behavior aligns with the logic’s prototypical values and norms (Christensen et al., 2004; EstradaCruz et al., 2019; Norman et al., 2005). Because academic entrepreneurs typically identify primarily as scholars employed in academic institutions, their cognitions and behaviors are shaped predominantly by an academic institutional logic (Choi et al., 2024; Giunti & Duberley, 2023; Jain et al., 2009). This logic emphasizes the advancement of fundamental knowledge, autonomy in research, rewards in the form of peer recognition and reputation, and the open publication of research outcomes (Merton, 1973).

The predominance of academic institutional logic in academic entrepreneurs’ mindsets stems from the prolonged and intensive academic training and socialization they undergo prior to founding ventures (Jain et al., 2009; Latour & Woolgar, 1979; Merton, 1957). Consistent with this view, prior research shows that academic entrepreneurs differ from other entrepreneurs in their motivation for engaging in entrepreneurial activities (Jain et al., 2009; Rasmussen, 2011; Vohora et al., 2004). Although they value financial rewards, academic entrepreneurs are largely motivated by nonpecuniary goals, such as enhancing their academic reputation by diffusing research outcomes through commercialization (Hayter, 2015; Hossinger et al., 2020; Krabel & Mueller, 2009) and supporting their primary academic roles (Balven et al., 2018; Huyghe et al., 2016; Lam, 2011).

In contrast, an industrial institutional logic emphasizes profit-oriented problem-solving, restricted information disclosure, bureaucratic control, and the private appropriation of economic returns (Fini & Lacetera, 2010; Murray, 2010; Sauermann & Stephan, 2013). As academic entrepreneurs increase their involvement in business, they become increasingly exposed to this institutional logic and eventually find themselves in a challenging position in which they are required to satisfy incompatible norms and expectations simultaneously (Balven et al., 2018; Rizzo et al., 1970; Zhang et al., 2021). In such circumstances, academic entrepreneurs cannot readily switch between the two institutional logics, not only because their underlying orientations are fundamentally opposed but also because cognitive schemas are path-dependent (Ashforth et al., 2000; Bartunek & Rynes, 2014; Choi et al., 2024; Toubiana, 2020). Consequently, although the intensity may vary across individuals, they almost inevitably experience role conflict (Casteleijn-Osorno & Hytti, 2025)—tensions arising from the normative and cognitive incongruence between the two institutional logics (Bartunek & Rynes, 2014; Jain et al., 2009; Perkmann et al., 2019).

When individuals feel cognitive strain resulting from role conflicts, they tend to alleviate it by prioritizing one institutional logic—and its associated role—at the expense of the other (Pratt & Foreman, 2000; Wry & York, 2017). In a similar vein, Choi et al. (2024) argue that academic entrepreneurs often resolve role conflict by reducing the salience of the relatively less central entrepreneurial identity. Building on these insights, we next explain how academic entrepreneurs’ embeddedness in both academic and industrial institutional logics gives rise to role conflict that shapes subsequent managerial decisions along the venture’s life cycle, including exit strategies and funding choices.

Hypotheses Development

Academic Entrepreneurship and Exit Modes

Exits are one of the most critical events in entrepreneurship because wealth creation, which is the primary objective of entrepreneurship (Arora et al., 2021; Bowen et al., 2023; Certo et al., 2001), is mainly achieved through exit events. When entrepreneurs plan their exit to reap the returns from their entrepreneurial activities, they have, in general, two alternatives: acquisitions, in which they sell their ownership in their ventures to incumbents, and IPOs, in which they take their private ventures into the public stock market (Bowen et al., 2023; Gaba & Meyer, 2008; Pahnke et al., 2023). Given these choices, entrepreneurs often develop exit plans at an early stage during which the future orientation of their ventures is formed. These intended exit plans affect the decisions that entrepreneurs make along the growth of their ventures, for instance, with respect to resource acquisition, financing, and commercialization (DeTienne & Cardon, 2012; DeTienne et al., 2015; Fauchart & Gruber, 2011). A survey by PricewaterhouseCoopers supports these points, indicating that 77% of the founders of technology ventures in Canada plan their exit modes at an early stage and develop their business plans accordingly (Dasilva, 2016).

Although both acquisitions and IPOs enable entrepreneurs to realize returns from their venture activities and function as new channels for raising capital for venture growth, they differ in important ways. After an IPO, the venture continues to exist as an independent company, whereas after an acquisition, the control and ownership of the venture are transferred to the acquiring company (Pahnke et al., 2023; Poulsen & Stegemoller, 2008). Because of these differences, the two alternative exit modes differ widely in the extent to which the entrepreneurs are expected to be involved in their ventures during and after the exit events (Bayar & Chemmanur, 2011). Also, compared with the process of acquisition, the IPO process tends to involve higher costs and is likely to be riskier and lengthier because of government regulations, advisory fees, and potential underpricing of the initial equity sales (Poulsen & Stegemoller, 2008). Completing an IPO itself is challenging, and managing a public firm after an IPO requires an entrepreneur to address more complex business issues and handle more diverse demands from various stakeholders than managing a private firm. Thus, exiting through an IPO requires entrepreneurs to escalate their commitment to the venture and develop higher levels of managerial capabilities relative to exiting through an acquisition.

These different requirements of the two exit modes generate different levels of role conflict and, accordingly, shape academic entrepreneurs’ exit mode preferences. Exiting through an acquisition often enables academic entrepreneurs to maintain or return to their primary academic positions, thereby attenuating role conflict. By contrast, exiting through an IPO not only requires them to deepen their commitment to the venture—at the expense of their time, attention, and effort devoted to their primary academic roles—but also demands a more business-oriented mindset and more advanced managerial skills, thereby heightening role conflict. Because academic entrepreneurs often manage such conflict by reaffirming the academic institutional logic over the industrial one (Choi et al., 2024; Jain et al., 2009; Klingbeil et al., 2019; Perkmann et al., 2019), they should be more likely than nonacademic entrepreneurs, who do not experience such conflict, to favor acquisition over IPO as an exit route. Moreover, since ventures often obtain higher valuations through IPOs than through acquisitions (Gompers & Lerner, 2004), nonacademic entrepreneurs are likely to emphasize financial returns and thus have weaker incentives to prefer acquisitions over IPOs. Therefore, relative to nonacademic entrepreneurs, academic entrepreneurs are likely to have a stronger preference for acquisition over IPO as an exit mode.

Academic Entrepreneurship, Information Asymmetry, and CVC Investments

Thus far, we have proposed that academic entrepreneurs are more likely than other entrepreneurs to prefer an acquisition exit over an IPO, because the former is more conducive to resolving role conflict than the latter. This logic also implies that academic entrepreneurs will make upstream choices that increase the likelihood of realizing their preferred exit route.

Because information asymmetry between potential acquirers and target ventures is widely viewed as a pivotal obstacle to acquisitions (Capron & Shen, 2007; Cuypers et al., 2017; Ragozzino & Reuer, 2007), academic entrepreneurs’ upstream choices are likely to reflect efforts to alleviate this informational friction. For example, Roh et al. (2023) show that acquisitions in high-technology industries entail significant information costs and risks, emphasizing that mutual knowledge development prior to the acquisition facilitates faster deal completion, which would otherwise be a time-intensive process for both sides. Entrepreneurs typically have more fine-grained knowledge of the quality of their ventures’ resources and future prospects than potential acquirers do (Shane & Stuart, 2002; Zaheer et al., 2010). Moreover, because entrepreneurs control what information they disclose during negotiations, they can leverage this informational advantage to secure higher valuations (Arikan, 2004; Capron & Shen, 2007). At the same time, this informational advantage can heighten acquirers’ concerns about adverse selection and overpayment (Capron & Shen, 2007; Reuer & Ragozzino, 2008). As a result, acquirers may bid at a discount or refrain from acquiring private ventures whose underlying resources are difficult to evaluate (Shen & Reuer, 2005). Consistent with this logic, Ragozzino and Reuer (2007) argue and show that the likelihood of acquiring an entrepreneurial venture increases when acquirers can rely on credible information sources or signals, such as the venture’s affiliation with reputable market constituents.

Building on an information-asymmetry perspective in M&A, we argue that when academic entrepreneurs anticipate an acquisition exit, they may need to credibly convey the quality of their venture’s knowledge and technologies to prospective acquirers. One way to do so is to form collaborative arrangements with prospective acquirers prior to an acquisition (Shen & Reuer, 2005; Zaheer et al., 2010). A broad literature on interfirm relationships suggests that such preacquisition ties can help would-be acquirers learn about a target’s resources and reduce valuation uncertainty (Higgins & Rodriguez, 2006; Janney et al., 2021; Vanhaverbeke et al., 2002; Zaheer et al., 2010). Consistent with this view, research on CVC emphasizes that corporate investors often use CVC to identify future acquisition opportunities (Benson & Ziedonis, 2009, 2010; Chesbrough, 2002; Dokko & Gaba, 2012). Survey evidence similarly suggests that “early relationships with potential acquisition targets” and the “potential to acquire” are among the primary motives for CVC investing (CB Insights, 2015; Siegel et al., 1988). Through CVC relationships, corporate investors can obtain richer, firsthand information about a venture’s technologies, managerial processes, and operating routines, thereby enabling more informed assessment of potential synergies and more accurate pricing in a prospective acquisition. Integrating insights from the literature on information asymmetry in acquisitions with the CVC literature, we argue that academic entrepreneurs are more likely than other entrepreneurs to seek or accept CVC financing because it can reduce information asymmetry—and, in turn, attenuate prospective acquirers’ concerns about adverse selection and overpayment (Wolff et al., 2022). To the extent that academic entrepreneurs prefer acquisition as an exit route, CVC can also establish early relational ties that facilitate a transition from an investment relationship to an acquisition. Therefore, we propose the following:

Hypothesis 2 points to the key mechanism of our argument: academic entrepreneurs’ preference for exiting through acquisitions instead of IPOs underlies the proposed link between academic entrepreneurship and CVC financing. To validate this mechanism, we consider (1) heterogeneity in corporate investors’ objectives and (2) an exogenous market-level contingency that should moderate the positive relationship between academic entrepreneurship and CVC financing. 2

First, we exploit variation in corporate investors’ goal orientations by distinguishing between CVC programs that are primarily strategic and those that are primarily financial. While corporate investors often pursue strategic objectives aligned with the parent firm—such as accessing external innovation or cultivating acquisition opportunities (Benson & Ziedonis, 2009, 2010; Dokko & Gaba, 2012; Dushnitsky & Lenox, 2005; Mayya & Huang, 2025)—some CVC programs place greater emphasis on financial returns realized through exits, including acquisition by third parties or IPO (Gompers & Lerner, 2004). If academic entrepreneurs engage corporate investors in part to disclose the value of their ventures’ resources and increase their visibility to potential acquirers, they should be more likely to partner with strategically oriented corporate investors than with financially oriented ones.

Second, we consider a market-level contingency that captures the attractiveness of acquisition exits. When M&A markets are more active, the availability of potential acquirers and acquisition opportunities increases, reducing the marginal benefit of using corporate investment ties to facilitate information disclosure and attract acquirers. Accordingly, we expect the positive relationship between academic entrepreneurship and the likelihood of receiving CVC funding to be weaker when M&A markets are more active.

Methods

Empirical Setting and Data

The empirical setting of this study is the exit events and financing from CVCs of entrepreneurial ventures in the U.S. medical device industry 3 from 1995 through 2015. The U.S. medical device industry is an appropriate setting to test our hypotheses for several reasons. First, according to Zhang (2009), approximately 20% of new ventures in the medical device industry are founded by university employees, making it one of the most active industries in terms of academic entrepreneurship. While academic entrepreneurs in this industry may draw from a wide variety of disciplinary areas (e.g., biophysics, chemistry, and pathology) and hold several different positions (e.g., university professors, research scientists in academic laboratories, and physicians at university-affiliated hospitals), their primary jobs generally involve research- and education-oriented activities. These dual roles make the academic entrepreneurs’ role conflict and managerial constraints readily observable in this setting.

Second, innovation in the medical device industry relies heavily on tacit, clinically grounded knowledge. Academic researchers, particularly physicians, often identify unmet clinical needs through hands-on experience, and their insights are embedded in practice-based expertise that is difficult for outsiders to evaluate (Chatterji & Fabrizio, 2014, 2016; Chatterji et al., 2008; Katila et al., 2017; Pahnke et al., 2023). The invention of new technologies and devices in this field frequently requires a thorough understanding of the “complexity and precision of the scientific and engineering inputs” (Wu, 2013: 1271). As a result, potential acquirers might be unable to assess the exact value of such knowledge-intensive assets and hesitate to acquire a venture without close interactions (Coff, 1999). Therefore, how to disclose information about potentially valuable inventions can be a severe concern for academic entrepreneurs in this industry. These conditions underscore the relevance of CVC investments, which provide established firms with early exposure to external technologies and reduce information asymmetry when considering the acquisition of ventures, which is central to the underlying logic of our main arguments.

Finally, the industry is characterized by the coexistence of a small number of large incumbents and a wide base of entrepreneurial ventures that fosters complementarities between the two (Chatterji, 2009; MedPAC, 2017). On one hand, the industry is dominated by large incumbents that control advanced manufacturing capabilities, regulatory expertise, and distribution networks; these firms maintain diverse portfolios and account for the majority of industry revenues. On the other hand, about 95% of firms in this industry operate with less than $10 million in assets (Gravelle & Lowry, 2015). In particular, ventures typically focus on narrow therapeutic applications and invest heavily in R&D, often several times their annual revenues (Chatterji et al., 2008; MedPAC, 2017). Therefore, established companies, such as Abbott Laboratories, Boston Scientific, and Johnson & Johnson, actively seek external technological knowledge through CVC investments and acquisitions to expand their business scope (Cha et al., 2014; Devarakonda et al., 2024; Dushnitsky & Lenox, 2005; Katila et al., 2008; Pahnke et al., 2023; Ryu et al., 2025), while ventures rely on incumbents for complementary capabilities and exit opportunities.

Moreover, the industry’s unique risk profile and associated regulatory environment reinforce the need for complementarity. While medical devices generally undergo a less stringent approval process than biopharmaceutical drugs, the development risk varies across device categories (MedPAC, 2017). While medium-risk devices undergo a relatively streamlined premarket notification process (510(k)) by demonstrating substantial equivalence to existing products, high-risk devices, such as implantable or life-sustaining devices, follow a meticulous premarket approval process, which requires rigorous testing, biocompatibility assessments, and facility inspections (Galasso & Luo, 2021; S&P Capital IQ, 2014; Shin et al., 2025; Wu, 2013; Xiao, 2022). These requirements necessitate high-precision manufacturing and capital-intensive development cycles, which are challenging for small ventures to manage alone, heightening their reliance on incumbent firms. Reflecting this dynamic, the value of venture funding with CVC participation in the medical device industry has increased during the past several years, which accounts for approximately 20% of all VC investments in medical device ventures (EvaluateMedTech, 2017).

To construct our sample, we first use the VentureXpert database to identify 826 investor-backed medical device ventures founded between 1995 and 2010. Then, to classify ventures founded by academic entrepreneurs among those 826 ventures, we gather information on the career histories of their founders based on various data sources such as Bloomberg Businessweek’s executive profile, S&P Capital IQ, Crunchbase, Relationship Science, LinkedIn, and company websites. To collect data on exit events of our sample ventures, we also draw on the Thomson ONE database. To identify the corporate parents of CVC funds, we draw on various information sources such as Bloomberg Businessweek, S&P Capital IQ, and Factiva.

Based on the identified sample firms, we construct two datasets to examine our arguments. First, to test Hypothesis 1, which suggests a positive association between academic entrepreneurship and exit through an acquisition (vs IPO), we create a cross-sectional dataset (exit mode sample) that includes ventures that experienced exit events during our observation window and their exit modes. Second, to test Hypothesis 2, which predicts that academic entrepreneurship positively affects the likelihood of financing from CVCs, we closely follow the prior CVC literature (e.g., Katila et al., 2008) by creating a venture-funding round panel dataset (CVC funding sample). The panel dataset represents whether or not a venture receives funding from CVC investors at each funding round. In the panel dataset, our sample ventures are tracked from their lifetime initial funding round through the latest funding round during the sample period.

We augment those data with patent information from the U.S. Patent and Trademark Office and information on products from the medical device approval database of the U.S. Food and Drug Administration (FDA). We also use the Securities Data Company database to gather information about alliances. Finally, we further supplement these data with information from Compustat to measure some of the control variables (Castro et al., 2021).

Measures

Dependent Variables

We have two different dependent variables in this study. For Hypothesis 1, the dependent variable, acquisition, is a binary variable, which takes the value of one if a venture exited through an acquisition and zero if it exited through an IPO. For Hypothesis 2, the dependent variable, CVC investment, is also a binary variable, which takes the value of one if a venture formed an investment relationship with a corporate investor in a given funding round and zero otherwise.

Explanatory Variable

Our independent variable (academic entrepreneurship) intends to capture the presence of academic entrepreneurs on a venture’s founding team. We empirically define academic entrepreneurs as individuals who perform research and/or teaching activities as employees of academic institutions at the time they found their own ventures and continue their roles at the academic institutions during their entrepreneurial activities. For example, Fred Lee was working as a professor of radiology and biomedical engineering at the University of Wisconsin-Madison when he cofounded NeuWave Medical in 2004; therefore, Fred Lee is identified as an academic entrepreneur. As a result, we identify 338 academic entrepreneurs among the 1,183 founders of our sample ventures. These academic entrepreneurs appear on the founding teams of 265 medical device ventures. To construct this variable, we count the number of academic entrepreneurs in each venture’s founding team and divide this figure by the total number of founders.

Control Variables

We incorporate several founder-, venture-, and industry-level control variables that could affect a venture’s choice of exit modes and/or funding sources. The first set of control variables is specific to the characteristics of the founders. Several studies have shown that entrepreneurs’ previous founding experience can increase the likelihood of exit events and funding from external investors because such experience can reduce the uncertainty about their ventures (e.g., Hsu, 2007; Paik, 2014). Therefore, we control for whether any of a venture’s founding members have previous founding experience based on the number of founding members with prior entrepreneurial experience divided by the total number of founders (serial entrepreneurship). In addition, we account for the socioeconomic and demographic characteristics of founding members because they can affect a venture’s funding and development process. We measure female entrepreneurship as the number of founders who are female (Guzman & Kacperczyk, 2019; Kanze et al., 2018) and foreign entrepreneurship as the number of founders who are from foreign countries (Kulchina, 2016, 2017) and then divide these values by the total number of founding members for each venture. To control for the extent to which the number of founders contributes to a venture’s growth (Eisenhardt & Schoonhoven, 1996), we also include the number of cofounders on each venture’s founding team.

Next, we include a set of venture-level control variables. To control for corporate investors’ concerns about the newness of small ventures (Carroll & Hannan, 2000; Stinchcombe, 1965), we include variables that can account for venture quality: venture age, measured as years since inception (Aggarwal & Hsu, 2009); the number of patents applied for (and eventually granted in later years) during the 4 years prior to a given year (venture patent count) (Hsu & Ziedonis, 2013; Long, 2002) and the number of medical devices approved by the FDA during the 4 years prior to a given year (venture device count) (Chatterji, 2009). In addition, to control for the effects of alternative means of financing, we include the number of alliances formed by a venture during the 4 years prior to a given year (venture alliance count) (Ozmel et al., 2013). In the United States, venture capitalists are concentrated in three states: California, Massachusetts, and New York (Gompers & Lerner, 2000), and they tend to invest locally (Fuller & Rothaermel, 2012). To control for this location effect, we include a binary variable, which takes the value of one if a venture is located in one of these states and zero otherwise (VC-dense states). Moreover, ventures located in the medical device clusters may benefit from access to specialized resources and knowledge spillover (Alcácer & Chung, 2014; McCann & Folta, 2011). We therefore include a binary variable (medical device cluster), which takes the value of one if a venture is located in any of the major medical device clusters identified in prior research (Emmons et al., 2006), including California, Florida, Illinois, Massachusetts, Minnesota, and Utah. We also include cumulative CVC investments, measured as the number of previous rounds in which corporate investors are involved, and the investment round to control for the need for additional funding.

Next, we include industry-level control variables that represent ventures’ needs for complementary resources. Small ventures often rely on established firms to obtain resources for downstream activities such as manufacturing and marketing (Rothaermel & Boeker, 2008; Teece, 1986). Therefore, following Katila et al. (2008), we control for ventures’ manufacturing resource needs, measured as capital intensity (fixed assets divided by sales), and marketing resource needs, measured as advertising intensity (advertising expenditures divided by sales) in a venture’s four-digit SIC industry during the past 4 years. Also, we consider the number of downstream alliances (i.e., manufacturing and marketing alliances) in a given four-digit SIC industry during the past 4 years (downstream alliance count) to reflect the extent to which small ventures in the industry need the resources associated with downstream activities (Katila et al., 2008). We also include industry fixed effects to account for industry differences at the four-digit SIC level and year fixed effects to account for unobserved macroeconomic conditions. Finally, in the CVC funding sample for Hypothesis 2, we include stage fixed effects to control for the development stages of ventures at the time of each investment round (i.e., seed, early, and later stage) (Dushnitsky & Shapira, 2010; Sørensen, 2007).

Estimation

To estimate the effects of academic entrepreneurship on the exit mode suggested in Hypothesis 1, we employ Heckman probit models based on the exit mode sample; Heckman probit models are a variation of Heckman’s (1979) selection model, where the second-stage (outcome) model is also a probit model. Among the 826 medical device ventures in our sample, 334 ventures experienced an exit event during the sample period. However, exit events might not take place randomly. If the ventures with exit experience differ systematically from those without exit experience in terms of certain unobservable factors, omitting the factors can introduce selection bias in estimating the effects of academic entrepreneurship on exit modes. Therefore, we use Heckman probit models to mitigate the concern about sample selection bias. In the first-stage (selection) models, we estimate the likelihood of exit based on probit models where the dependent variable is coded as one if a venture exits through either acquisition or IPO in the focal year and zero otherwise; to run the first-stage model, we use all of our sample ventures that had not experienced exit events (either acquisitions or IPOs) until the focal year as counterfactuals for those that exited in the focal year. As exclusion restrictions in the first-stage model (Hamilton & Nickerson, 2003; Wolfolds & Siegel, 2019), we use venture patent count and venture device count. In our case, exclusion restrictions should affect the likelihood of an exit event, but not the exit mode. These two variables clearly indicate the quality of a venture’s technological capabilities and future prospects (Chatterji, 2009; Hsu & Ziedonis, 2013; Long, 2002), which increase the likelihood of an exit event; however, there is no prior reason why these two variables make either acquisitions or IPOs more likely to be chosen than the other because ventures with such features are likely to be preferred in both exit markets.

To test Hypothesis 2, which predicts that ventures founded by academic entrepreneurs are more likely to receive CVC funding than other ventures, we employ random-effects models based on a panel dataset (CVC funding sample) consisting of venture-funding round observations (Katila et al., 2008). The random-effects specification is more appropriate for our context than the fixed-effects specification for two reasons. First, our main arguments concern the heterogeneity between ventures in terms of their founders’ career histories rather than within-venture changes over time (Certo et al., 2017). Second, although fixed-effects models require variance in independent variables, the value of our independent variable, academic entrepreneurship, does not vary across rounds (Jensen & Zajac, 2004). Nevertheless, random-effects models require a strong assumption that independent variables are not correlated with the estimated panel error term (Certo & Semadeni, 2006). Therefore, we also use generalized estimating equation (GEE) probit regression models because they do not require such a strong assumption (Katila et al., 2008). Moreover, GEE regression models account for autocorrelation that stems from multiple funding rounds for each venture (Certo et al., 2017). 4

Results

Main Results

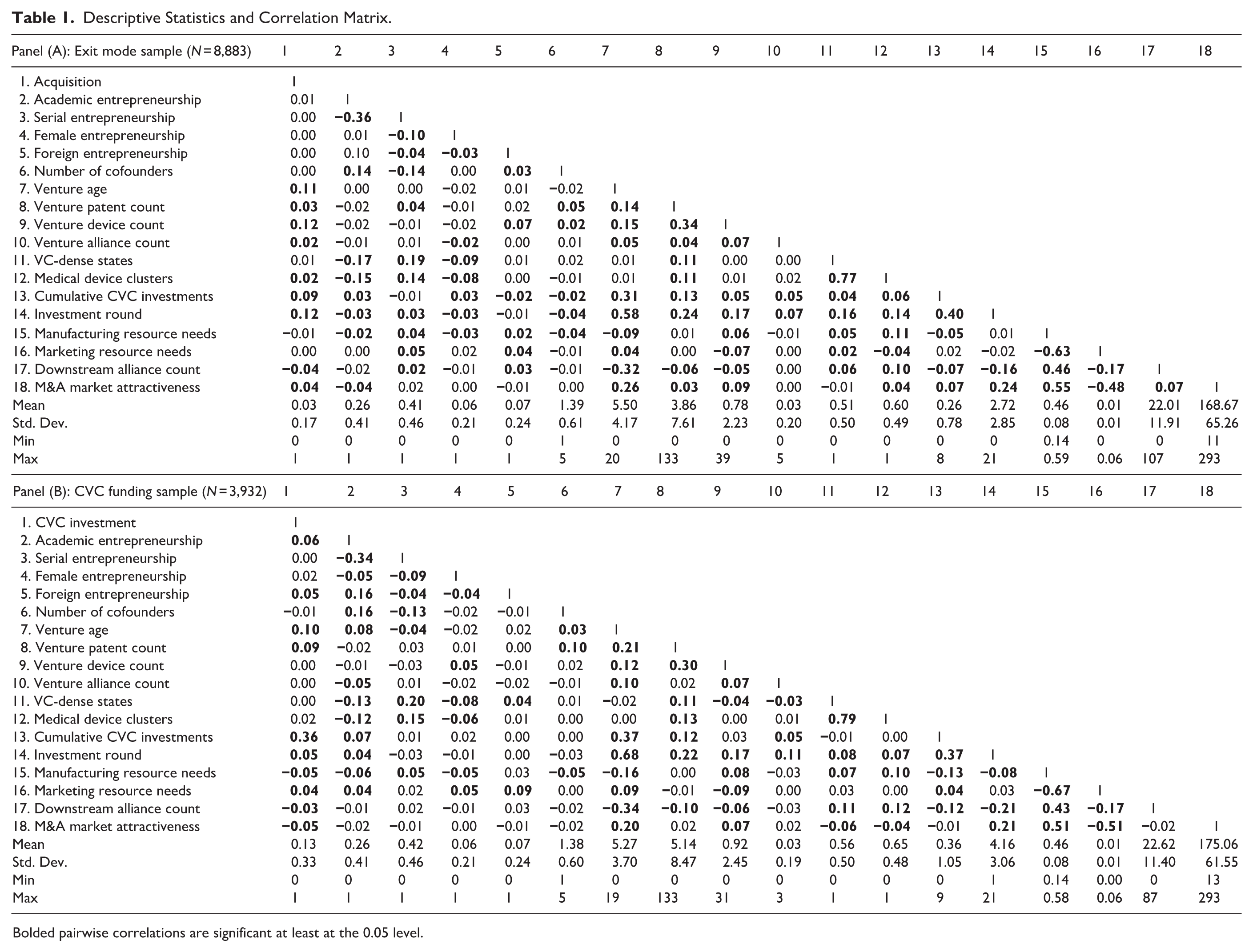

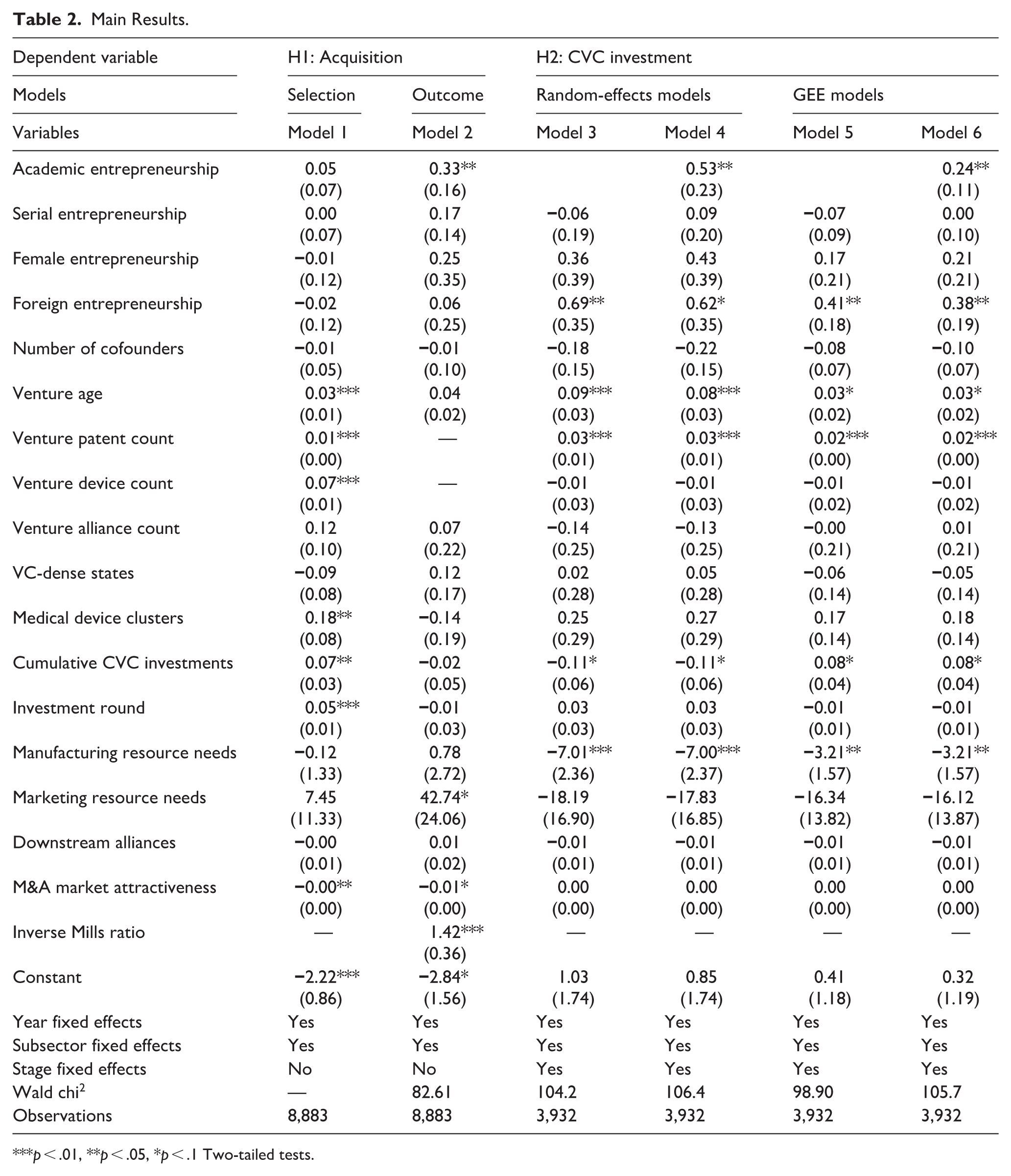

Table 1 reports the descriptive statistics and pairwise correlations between variables used in our analyses: Panels (A) and (B) contain the values for the exit mode sample and the CVC funding sample, respectively. Table 2 reports the main results for Hypothesis 1 (Models 1–2) and Hypothesis 2 (Models 3–10). In Model 1 (selection model), in which we estimate the likelihood of exit, we calculate the inverse Mills ratio and include it in Model 2 (outcome model) to control for possible selection bias. As expected, Model 1 shows that the coefficients of venture patent count and venture device count are positive and significant (b = 0.01, p = .002 and b = 0.07, p = .000, respectively), supporting the validity of these two variables as exclusion restrictions. Model 2 estimates the likelihood of acquisition (as opposed to IPO) as an exit mode and shows that the coefficient of academic entrepreneurship is positive and significant (b = 0.33, p = .045), supporting Hypothesis 1. The estimation also indicates that when the value of academic entrepreneurship increases from its mean to one standard deviation above the mean, the likelihood of acquisition increases by 9.3%.

Descriptive Statistics and Correlation Matrix.

Bolded pairwise correlations are significant at least at the 0.05 level.

Main Results.

p < .01, **p < .05, *p < .1 Two-tailed tests.

Table 2 also shows the results of the probit regression models with random effects (Models 3 and 4) and alternative specifications using the GEE probit regression (Models 5 and 6) employed to test Hypothesis 2. Models 3 and 5 are the baseline models that include only control variables. Based on these models, academic entrepreneurship is added to Models 4 and 6 to test Hypothesis 2. The coefficient of academic entrepreneurship in Model 4 (random-effects specification) is positive and statistically significant (b = 0.53, p = .019), which indicates that as the value of academic entrepreneurship increases, the likelihood that a venture receives CVC funding increases; therefore, Hypothesis 2 is supported. Regarding the economic significance of this effect, the estimates of Model 4 indicate that a one standard deviation increase in the ratio of academic entrepreneurs to founding members leads to a 46.8% increase in the likelihood of receiving funding from corporate investors. The results of the GEE probit regression models also show a positive and significant relationship between academic entrepreneurship and CVC investment (b = 0.24, p = .034 in Model 6), providing further support for Hypothesis 2.

Supplementary Analyses

We further explore the validity of our theoretical arguments and the underlying mechanism by considering (1) alternative dependent variables that reflect corporate investors’ goal orientation, (2) an exogenous boundary condition associated with external M&A market environments, and (3) university-specific characteristics. Moreover, we consider the possibility that alternative mechanisms might generate a seemingly positive relationship between academic entrepreneurship and the likelihood of CVC financing.

Corporate Investors’ Goal Orientation

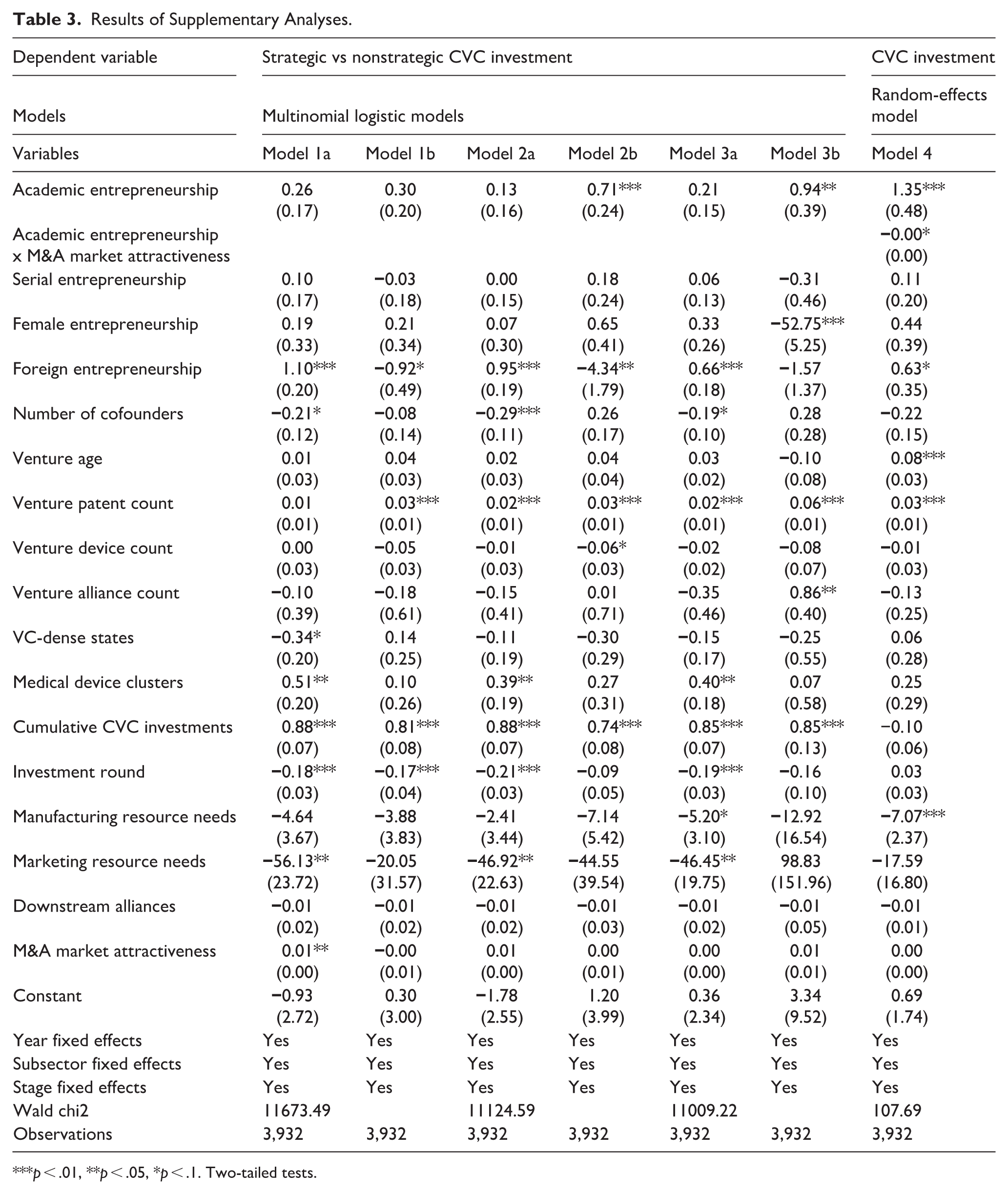

As described at the end of the theory section, we expect that if the mechanism that we suggest is in play, ventures founded by academic entrepreneurs are more likely to receive funding from corporate investors with a strong intention to acquire their portfolio companies than from corporate investors that focus on the financial returns of their investments. To distinguish these goals with regard to CVC investments, we rely on previous studies to identify CVC investors with a strategic goal orientation (Dokko & Gaba, 2012; Gaba & Meyer, 2008). Specifically, for each corporate investor, we measure strategic orientation based on the proportion of its portfolio companies that it acquired because acquisition indicates that corporate investors expect to gain potential synergistic benefits from their portfolio companies (Dokko & Gaba, 2012). Then, if the proportion is greater than two cutoff values, (1) the median value and (2) the highest quartile value of strategic orientation, we consider the corporate investor as having a strong strategic orientation. Finally, we define a given CVC investment as strategic if it is made by a corporate investor with a strong strategic orientation. As an alternative measure, we consider a given CVC investment in a medical device venture as strategic if it is made by a corporate investor whose parent firm is in the same four-digit SIC industry because the invested venture is more likely to generate synergies with the corporate investor’s parent firm when they belong to the same industry (Dushnitsky & Shaver, 2009). Based on these definitions, we create a categorical variable as an alternative dependent variable by dividing all observations into three groups: strategic CVC investment (coded as two), nonstrategic CVC investment (coded as one), and no CVC investment (coded as zero).

Table 3 presents the results of the multinomial logistic regression using this alternative dependent variable. Models 1a and 1b, which use the median of strategic orientation as the cutoff value, estimate coefficients for the likelihood of receiving nonstrategic CVC investment (Model 1a) and strategic CVC investment (Model 1b) in comparison to the default group, no CVC investment. These models show that academic entrepreneurship has a positive but insignificant coefficient in both models. However, Models 2a and 2b, which use the stricter definition of strategic orientation (highest quartile of strategic orientation), show that while academic entrepreneurship is positively associated with the likelihood of receiving strategic CVC investment (b = 0.71, p = .003 in Model 2b), such a significant relationship does not hold for nonstrategic CVC investment (b = 0.13, p = .427 in Model 2a). Moreover, a Wald test shows that the difference between the two coefficients is significant (p = .031), which is consistent with our suggested mechanism that academic entrepreneurs’ preference for acquisition as an expected exit mode may lead their ventures to receive funding from corporate investors with a serious strategic orientation. In addition, Models 3a and 3b, which define strategic corporate investors based on the same industry membership, show results consistent with those in Models 2a and 2b.

Results of Supplementary Analyses.

p < .01, **p < .05, *p < .1. Two-tailed tests.

M&A Market Attractiveness

If our theorized mechanism holds, ventures founded by academic entrepreneurs are more likely to receive CVC investments to disclose the information about their technologies in unattractive M&A markets because only a small number of potential acquirers are likely to be in the market. Conversely, ventures founded by academic entrepreneurs might have reduced incentive to receive CVC investments in attractive M&A markets where there are a large number of potential acquirers. To measure the attractiveness of the M&A market, we construct the M&A market attractiveness variable by counting the number of acquisitions of private companies in each four-digit SIC industry of the broad medical device industry during the past 4 years prior to a given year (Aggarwal & Hsu, 2014). 5

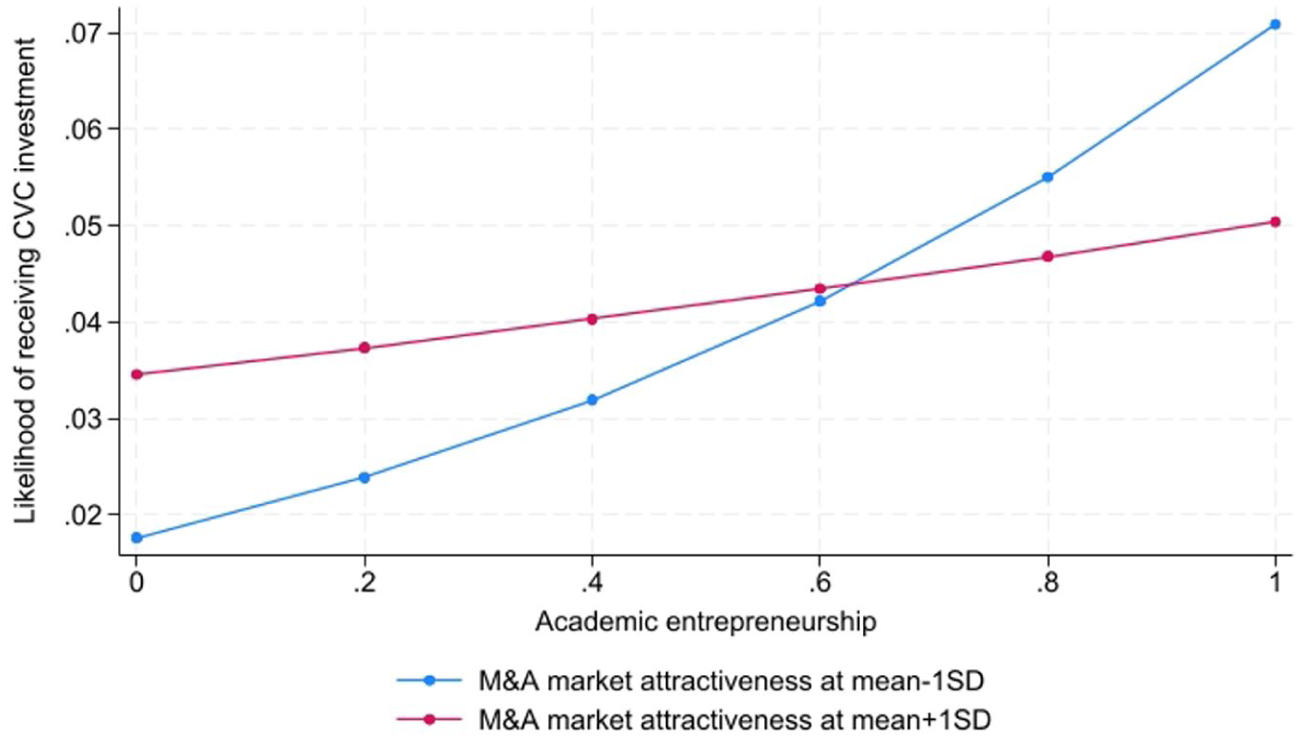

We estimate how M&A market attractiveness shapes the relationship between academic entrepreneurship and the likelihood of receiving CVC investments in Model 4 in Table 3. The negative and significant interaction term between academic entrepreneurship and M&A market attractiveness (b = −0.00, p = .052) lends preliminary support to our mechanism. Because the interpretation of interaction effects in nonlinear models (probit model in our study) cannot be ensured based on the sign and significance of the coefficient of the interaction term, we also plot the predicted likelihood of receiving CVC investments (Hoetker, 2007). In line with our argument, Figure 1 shows that when the external M&A market is unattractive (one standard deviation below the mean), the likelihood of receiving CVC investment noticeably increases with the ratio of academic entrepreneurship; however, the positive relationship between academic entrepreneurship and the likelihood of CVC financing becomes much less pronounced when the external M&A market is attractive (one standard deviation above the mean). For example, in an unattractive M&A market, when the ratio of academic entrepreneurs increases by one standard deviation from its mean value, the likelihood of CVC financing increases by 77.3%; however, in an attractive M&A market, an increase of one standard deviation from the mean value in the ratio of academic entrepreneurs leads to only a 16.7% increase in the likelihood of CVC financing. 6

Interaction effect between academic entrepreneurship and M&A market attractiveness.

University-Specific Characteristics

To further validate our findings, we address the possibility that university-specific characteristics may influence academic entrepreneurs’ choice of exit modes and funding sources. In particular, founders affiliated with research-active universities may experience greater role conflict associated with increasing their commitment to entrepreneurial activities. If this is the case, our proposed mechanism should be more pronounced among academic entrepreneurs from research-intensive institutions. To examine this possibility, we construct university-level measures of research activity by counting the number of medical-related patents produced by each university. Using this information, we identify academic entrepreneurs whose primary academic institutions fall within (1) the top 10% and (2) the top 50% of universities in terms of medical-domain patenting. We then construct new independent variables by using only academic entrepreneurs originating from these research-active universities and re-estimate our main models. We find that both Hypotheses 1 and 2 are supported when the independent variable is constructed using only academic entrepreneurs from the top 10% of research-active universities, whereas only Hypothesis 1 is supported when we use the top 50% cutoff. These results suggest that our main findings are primarily driven by academic entrepreneurs affiliated with the most research-intensive universities (results available upon request).

Alternative Explanations

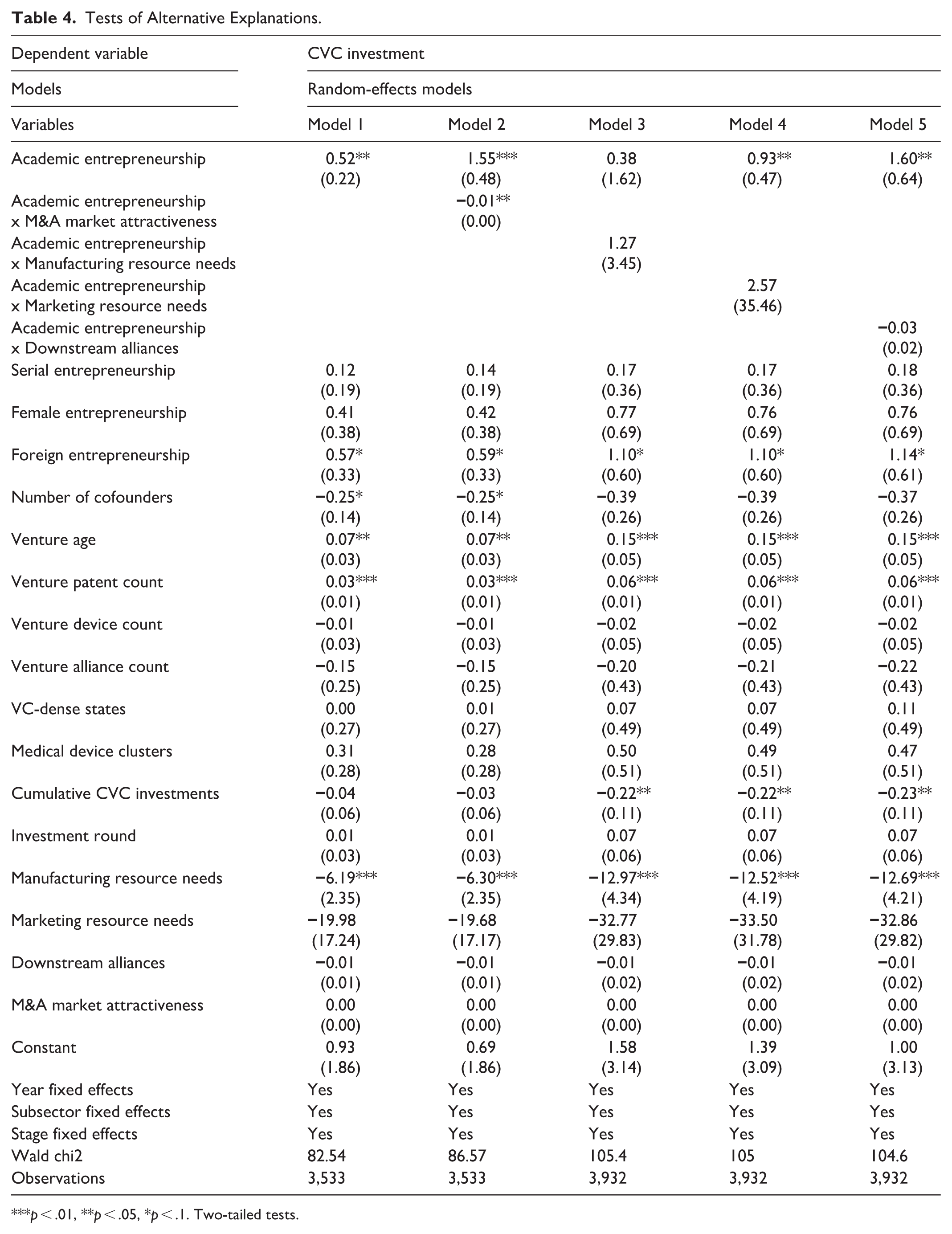

We address two alternative explanations that could drive the positive relationship between academic entrepreneurship and CVC financing: one from the corporate investor’s perspective and another from the ventures’ perspective. First, corporate investors are known to be more patient than IVC investors and thus might be more appropriate investors for very early-stage technologies (Chesbrough, 2002; Pahnke et al., 2015). Ventures founded by academic entrepreneurs tend to have technologies derived from the basic research of their founders, so their technologies are likely to be novel but immature (Feldman et al., 2002). Therefore, such technologies might simply be pursued to a larger extent by CVC investors, which usually have a longer investment horizon than IVC investors (Chemmanur et al., 2014; Fletcher, 2001; Galloway et al., 2017). To address this concern, in Models 1 and 2 of Table 4, we retest Hypothesis 2 and the moderating effect of M&A market attractiveness with a subsample excluding the observations associated with seed-stage ventures. If the positive relationship between academic entrepreneurs and CVC financing is mainly driven by CVCs’ long-term investment horizons and interests in novel (but immature) technologies, Hypothesis 2 and the moderating effect of M&A market attractiveness would not be supported in the subsample without seed-stage ventures. However, as can be seen in Models 1 and 2, the results remain consistent even in the sample consisting of ventures at later stages.

Tests of Alternative Explanations.

p < .01, **p < .05, *p < .1. Two-tailed tests.

Second, it is possible that ventures founded by academic entrepreneurs prefer to form investment relationships with corporate investors simply because they have a greater need for the complementary resources available from corporate investors (Alvarez-Garrido & Dushnitsky, 2016; Katila et al., 2008). To address this concern, we investigate the moderating effects of three variables that represent the extent to which ventures need complementary external resources (manufacturing resource needs, marketing resource needs, and downstream alliance count) in Models 3–5 of Table 4. If academic entrepreneurs’ need for complementary resources drives the main results, the positive relationship between academic entrepreneurship and the likelihood of receiving CVC investments should be more pronounced among ventures with a greater need for complementary resources. However, Models 3–5 show that none of these three variables significantly shapes the positive relationship observed in the main results.

Discussion

Contributions and Implications

Building on prior research on academic entrepreneurship and CVCs, we investigate which exit modes academic entrepreneurs prefer and how these preferred exit routes, in turn, shape their ventures’ CVC financing. Our main analyses, based on exit events and CVC investments in the U.S. medical device industry between 1995 and 2015, support our predictions that ventures founded by academic entrepreneurs are more likely than other ventures to exit through acquisitions and to receive funding from corporate investors. Supplementary analyses using an alternative dependent variable (strategic CVC investment) and exogenous exit market conditions (M&A market attractiveness) provide further support for the proposed mechanism that academic entrepreneurs’ preference for acquisitions as an exit mode motivates them to pursue CVC financing.

Our theory and findings make several contributions. First, we contribute to the academic entrepreneurship literature by deepening the understanding of how academic entrepreneurs differ from other entrepreneurs. Prior studies in this research stream have primarily focused on entrepreneurial motivation (Balven et al., 2018; Hayter, 2015; Hayter et al., 2022; Huyghe et al., 2016; Krabel & Mueller, 2009; Lam, 2011) and on the types of technologies pursued in entrepreneurial activities (Agarwal & Shah, 2014; Feldman et al., 2002; Shane, 2004; Stuart & Ding, 2006). We extend this literature by highlighting the role conflict between a primary academic persona and a secondary commercial persona (Bousfiha & Berglund, 2025; Choi et al., 2024; Hayter et al., 2022; Jain et al., 2009; Zhang et al., 2021; Zou et al., 2023) as a central mechanism that differentiates academic entrepreneurs in critical managerial decisions along the venture life cycle, including the choice of funding sources and exit modes. This perspective also complements research on institutional logics in academic entrepreneurship, which has not explicitly examined how embeddedness in academic institutional logic, despite its importance as a defining characteristic of academic entrepreneurs, shapes the strategies of university spinoffs.

Second, this study adds to prior research on the determinants of CVC investments (Basu et al., 2011; Benson & Ziedonis, 2009, 2010; Dokko & Gaba, 2012; Dushnitsky & Lenox, 2005; Dushnitsky & Shaver, 2009; Gaba & Meyer, 2008; Katila et al., 2008; Weniger & Jarchow, 2023). Although prior research has examined a range of firm-, dyad-, and industry-level conditions under which established firms make CVC investments, it has paid relatively less attention to the investee’s side, specifically, to how founders’ individual characteristics, values, norms, and incentives shape entrepreneurial financing decisions (Beckman & Burton, 2008; Higgins, 2005). We extend this literature by theorizing and demonstrating that founders’ institutional identities and career options can systematically influence interactions between their ventures and external investors, including the likelihood of forming CVC relationships.

Third, we contribute to research on information asymmetry in venture acquisitions, where prior work has largely adopted the acquirer’s perspective and focused on how acquirers use signals to mitigate adverse selection and overpayment (Capron & Shen, 2007; Ragozzino & Reuer, 2007; Reuer & Ragozzino, 2008). In contrast, explicitly adopting the target’s perspective, we propose that when a venture has a clear preference for exiting through an acquisition, it can increase the likelihood of realizing this preferred exit mode by proactively alleviating buyers’ evaluation concerns, for example, by forming an early investment relationship with a potential buyer that allows the venture to credibly reveal the quality of its technologies.

Relatedly, our findings offer some managerial and policy implications. From a managerial standpoint, our findings suggest that academic startups can be especially attractive partners for corporate investors. Prior research characterizing engagement with CVC as “swimming with sharks” highlights that technology ventures often approach CVC relationships with heightened concerns about knowledge misappropriation (Katila et al., 2008). These concerns can increase transaction costs for corporate parents by prolonging negotiations and necessitating more extensive contractual safeguards (Roh et al., 2023). Our results imply that, relative to other technology ventures, startups founded by academic entrepreneurs may perceive lower hazards in engaging with CVCs, thereby reducing frictions and transaction costs in forming and governing these relationships. Accordingly, corporate investors may benefit from paying greater attention to academic startups as investment candidates and, when strategically appropriate, more proactively pursuing postinvestment pathways to acquisition.

Our findings also carry policy implications for universities and the broader research commercialization ecosystem. In our framework, CVC-academic entrepreneur ties can generate mutual gains: they facilitate acquisition-based exits that allow academic entrepreneurs to maintain and, when desired, return to their primary academic roles while enabling corporate investors to access and evaluate novel technologies with relatively lower transaction costs. To realize these potential gains, universities may wish to reduce institutional barriers that discourage faculty and university-affiliated researchers from founding ventures. For example, universities may need to more explicitly recognize and appropriately evaluate entrepreneurial experience and commercialization activities within performance evaluation and career advancement systems, thereby better aligning incentives with the goal of fostering productive university–industry collaboration (Bercovitz & Feldman, 2008; Owen-Smith & Powell, 2001).

Limitations and Future Research

As with all studies, ours has limitations that also suggest fruitful avenues for future research. First, although we find evidence consistent with the predicted effects of academic entrepreneurship on ventures’ financing and exit choices, our analyses cannot definitively confirm the underlying mechanisms proposed in this article. To validate our theoretical mechanism, we include a range of control variables at the founder- and venture-levels and conduct multiple supplementary analyses. However, these efforts cannot directly test causal relationships nor fully rule out alternative explanations. Future research could address this limitation by employing survey instruments to capture entrepreneurs’ internal motivations and decision-making processes directly or by developing research designs that more cleanly identify causal relationships between entrepreneurs’ heterogeneous career paths and their ventures’ developmental outcomes.

Second, the uniqueness of academic entrepreneurs constrains the generalizability of our findings to other entrepreneurial contexts. A central element in our theoretical framework is that academic entrepreneurs occupy dual positions, that is, as employees and as entrepreneurs, and typically seek to maintain, or at least preserve the option to return to, their employee role. By contrast, some individuals pursue part-time entrepreneurship primarily to test or preview their business ideas before transitioning to full-time self-employment (Folta et al., 2010). These entrepreneurs have relatively weak incentives to retain their employee positions and thus are unlikely to prefer exiting through an acquisition to exiting through an IPO. Future research could therefore deepen our understanding of hybrid entrepreneurs by examining how factors other than role conflict, such as income level, the relevance of prior experience, and the nonmonetary benefits associated with employment, influence the growth trajectories of their ventures, including their financing and exit choices.

Finally, while our study focuses on academic entrepreneurs’ exit strategy and external financing, future research could broaden the scope to consider how academic entrepreneurs’ embeddedness in academic institutional logic and the resulting role conflict affect other strategic decisions, such as team composition, patenting practices, product diversification, and the formation of strategic alliances. Moreover, although our focus lies on entrepreneurial decision-making and how founders’ career preferences influence their pursuit of CVC financing, future studies might also examine how external investors interpret and respond to the unique characteristics of academic entrepreneurs when selecting investment targets. Such work would offer a more comprehensive understanding of how academic institutional logic shapes entrepreneurial ecosystems from both the demand and supply sides of venture capital.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by the Yonsei University Research Fund (2022-22-0037).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data will be made available upon reasonable request.