Abstract

This study investigates 389 expatriates in the UAE to examine their financial literacy level, relationship between the financial literacy and demographic characteristics. A questionnaire was used to study the financial literacy of expatriates from Asia, Africa, Europe, and North America. The findings reveal that the financial literacy of expatriates is low, with an average answering only 52 per cent of the questions correctly. The low level of knowledge would limit their ability to make informed decisions. The study finds age, marital status, gender, country of origin, income, experience, education, employment status, work place activity, and household situation influence financial literacy and hence calls for initiatives to improve financial literacy among expatriates and for further research in this direction.

Introduction

In recent years, there has been an increasing interest in financial literacy which is becoming extremely important to expatriates working in Gulf countries. Expatriates plan long-term investments for their children’s education and decide on managing day-to-day expenses as well as long-term financial planning. Michael Noctor, Sheila Stoney, and Robert Stradling (1992) define financial literacy, as making informed judgments and effective decisions regarding the use and management of money. The financial literacy assesses how an individual deals with money in payment of bills and planning the budget. In the same vein, Commonwealth Bank Foundation (CBF) (2004, p. 1) defines financial literacy as, “the ability to balance a bank account, prepare budgets, save for the future and learn strategies to manage or avoid debt.” Roy Morgan conducted Australia’s first national survey on financial literacy on behalf of the Australian and New Zealand (ANZ) Bank (Roy Morgan Research [RMR], 2003) and it defines financial literacy as, “enabling people to make informed and confident decisions regarding all aspects of their budgeting, spending and saving and their use of financial products and services, from everyday banking through to borrowing, investing and planning for the future.” In light of recent events in financial literacy, it is becoming difficult to ignore the existence of financial incompetency of expatriates working in Gulf countries.

Financial literacy focuses on better planning for retirement life, gradual wealth accumulation and better financial decision-making. Financially, illiteracy makes people prone to making mistakes in financial decisions. Various stakeholders, such as government, universities, public, and private sector groups, are interested in improving financial literacy. Other factors that have generated interest in financial literacy include low savings rates, growing insolvency rates, debt levels, and increased responsibility among individuals for making-decisions that affect their economic futures (Servon & Kaestner, 2008).

The issue of financial literacy has received considerable attention. Evidence suggests that financial literacy is among the most important factors for an individual’s standard of living, financial security and family relationships. There is increasing concern that some individuals are being disadvantaged on increased mortgage borrowings; higher cost of living; and inappropriate use of credit cards which have resulted in an increase in delinquencies, personal bankruptcies and insolvencies (Organisation for Economic Co-operation and Development [OECD], 2005). Governments and relevant stakeholders are interested in promoting financial stability and obtaining broader macroeconomic outcomes (Rocha, Arvai & Farazi, 2011). Other research suggests that financial problems are often the basis for mental illness, divorce, and other unhappy experiences (Kinnunen & Pulkkinen, 1998). On the other hand, with high levels of financial literacy, individuals can benefit from better understanding of financial concepts, household well-being, and better financial decisions (Cole, Sampson, & Zia, 2009, 2011). It is therefore likely that negative outcomes are most often associated with people having low financial literacy and such people make poor decisions and failed to measure the impact results from their decisions.

Situating UAE on Financial Literacy

Since the formation of the United Arab Emirates in 1971, the state-led strong economic growth and regulations have been attracting opportunities and success seekers from around the globe to join the development path in the country. Remarkably, expatriates from 160 countries are working in UAE and employed in banking, construction, and other businesses. Since 1971, five population censuses have been conducted at the federal level and as of April 2015, the last comprehensive population census available was that of 2005. At the end of the year 2010 (last available data), the total resident population of the UAE stood at 8,264,070 persons. 1 Foreign nationals thus made up 88.5 per cent (7.3 million). Top-ranking nationalities in the UAE were Indians, by far the largest national community with 2.6 million; Pakistanis (1.2 million); and Bangladeshis (0.7 million). Emiratis would thus be ranking third in numbers with 1.085 million nationals. 2

The Abu Dhabi Policy Agenda 2007/2008 developed Abu Dhabi Economic Vision (2030) to ensure all stakeholders in the economy move in tandem. This involves focusing on four key priority areas, namely, economic development, social and human resources development, infrastructure development and environmental sustainability, and optimization of government operations. It is not surprising, therefore, that financial literacy is a principal subject of discussion in the UAE, with a portion of the UAE’s economic development program aimed at producing a financially knowledgeable society that would prop up a sustainable, diverse economy by 2030. Banks and institutions, such as the Emirates Foundation 3 and the Abu Dhabi Council for Economic Development as well as private firms collaborate in introducing financial literacy curricula in schools to make students manage their finances.

The purpose of this study is to assess the impact of financial literacy on demographic variables with special reference to the expatriates in UAE. This study, hence, examines the effect of expatriate demographics specifically on the basis of age, marital status, gender, country of origin, income, experience, education, employment status, work place activity and household situation on managing personal finances among expatriates in UAE. This article reviews the financial literacy literature in the next section and the following section reports the research methodology in terms of the data collection and analytical method. The penultimate section reports the findings and discusses the results and final section summarizes and concludes.

Literature Review

While a wide variety of definitions of the term “expatriates” have been suggested, such as immigrants, migrants, or foreigners, this article will use the term “expatriates” and in the common usage, the term has come to be used for people who live out of their home land.

The literature review is divided into two parts. The first part deals with international studies conducted across the globe and the remainder of the part focus on the UAE efforts on financial literacy correlating with the financial literacy of the expatriates. A review of the literature is made on various parameters to cover the relationship between education, literacy, and financial well-being and a demarcation is made on foreign and the UAE studies. There is an extensive literature which examines the impact of demographic factors on financial literacy.

International or Foreign Studies

A large body of literature on financial education has attempted to examine financial capabilities, attitudes, behaviors, and knowledge. A number of authors have considered the effects of financial literacy on financial behavior of individuals (e.g., Atkinson & Messy, 2011, 2012; Holzmann, Mulaj, & Perotti, 2013; Kempson, Perotti, & Scott, 2013a, 2013b).

The Money SENSE Financial Education Steering Committee (Monetary Authority of Singapore, 2005), established by the government, conducted the first financial national literacy survey in Singapore. The main aim of this study measured whether Singaporeans are knowledgeable about common financial products and whether they have been making informed financial decisions. The findings showed that Singaporeans have a strong attitude toward financial planning, basic money management and investment matters.

For Australia, ACNielsen Research (2005) surveyed adult financial literacy and found that people who have lower education, unemployed, or unskilled workers have zero or very little financial literacy. Subsequently, Beal and Delpachitra Study (2002) conducted the first literacy survey in Australia carried out by the National Foundation of Education Research (NFER) on behalf of NatWest Group Charitable Trust. The study revealed that students with higher financial literacy scores were more likely to be male, have greater work experience, have a higher income, and have a lower aggregate risk preference. While the study showed that students with higher general financial knowledge and skills were more likely to be studying business, be male, work in a more highly skilled occupation and have more work experience. The results were in line with the earlier survey conducted by Chen and Volpe (1998).

More generally, ANZ Bank Study (Roy Morgan Research, 2003) conducted a national survey of adult financial in Australia. One of the clearest findings from the survey is the strong correlation between financial literacy and socio-economic status. The lowest levels of financial literacy were associated with those having lower education, low income, low savings, and unemployed or skilled workers. Commonwealth Bank (CBF) study (2004a) was the first study to examine the correlation between financial literacy and outcomes for individuals and the Australian economy. The study also highlighted that people with low rates of financial literacy have a greater rate of unemployment, lower income, and are more likely to struggle to pay mobile phone, credit card, and utility bills. The findings of all three Australian studies show that there is a definite lack of financial skills and knowledge among people with certain demographic characteristics.

For the USA, OECD (2005) reviewed international literacy on finance in 12 developed countries and found that financial illiteracy is rampant in most of the surveyed countries. Chen and Volpe (1998) conducted a survey among 924 college students from 13 colleges in various states in the USA and found that students with a low level of financial knowledge are more likely to make incorrect financial decisions. Volpe, Kotel & Chen (2002) surveyed 530 online investors to examine their investment literacy and relationship between literacy and online investor characteristics to test questions based on investment concepts and results showed older investors were more knowledgeable than those who are younger. Women had lower level of financial literacy than men and investors with graduate degrees were more knowledgeable than those with some high school or college education. Lusardi and Mitchell (2007) conducted a study on financial literacy, retirement planning in 2004 in the USA. The study showed that financial illiteracy happened due to poor planning and found certain groups of the population, such as women, elderly, and those with low education levels, were more financially illiterate than others.

In UK, the Adult Financial Literacy Advisory Group (AdFLAG) undertook a study to determine “how to promote better access to financial education to young people and adults” (UK Adult Financial Literacy Advisory Group [AdFLAG], 2000, p. 10). The results revealed undisputed link between the need for adequate basic skills in numeracy and literacy and financial literacy. The study recommended that short-term financial literacy education should be built around employment, education, housing, financial services, and communication with particular focus on younger people, older people, single parents, and people with disabilities.

Previous research in the area of financial literacy has revealed that workers, university students, and households are important factors to consider when seeking to understand the financial literacy of the individuals (Beal & Delpachitra, 2003; Beckmann, 2013; Brown & Graf, 2013; Chen & Volpe, 1998; Harris, Loundes, & Webster, 2002; Hilgert, Hogarth, & Beverly, 2003; Jang, Hahn, & Park, 2014; Karunarathne & Gibson, 2014; Van Rooij, Lusardi, & Alessie, 2011).

UAE Studies

Despite the importance of financial literacy, there remains a paucity of evidence on financial literacy among the expatriates in the UAE. The present study tries to fill the gap in the literature by investigating demographic factors of expatriates in the UAE with their financial literacy level. Al-Tamimi and Bin Kalli (2009) examined the financial literacy based on a sample of 290 UAE individual investors participating in the local financial markets and explore the relationship between financial literacy and investment decisions. The results indicate that financial literacy was about 41 percent and that females had lower levels of financial literacy than males. Ibrahim and Alqaydi (2013) studied the financial literacy of the UAE residents who uses bank loans and credit cards for borrowings. The data were collected from 412 individuals working with different organizations and it found that individuals who borrow less have strong financial attitude. The results also displayed that individuals with strong financial literacy borrow less from credit cards.

In the UAE, policy makers have recognized financial literacy as an important area to develop saving and spending habits among its population. Developing financial literacy through financial education has become an important area to develop and teach proper financial planning. At present, there is no baseline data available in the UAE with regard to financial literacy, even though efforts to promote financial literacy through financial education have been going on for several years. At present what is the existing level of financial literacy that expatriates in the UAE possess? Does this financial literacy level differ with the demographics of the expatriates?

Methodology and Data

Questionnaire Design

The questionnaire consists of 19 questions and is divided into two sections. Section A comprises 10 questions to elicit demographic variables, such as age, marital status, gender, country of origin, income, experience education, employment status, work place activity, and house-hold situation. Section B is devoted to financial literacy and it consists of nine exam type questions and pertains to ATM, inflation, balance after 1 year, safe returns, time-based returns, groups facing difficulty, risk, retirement, and asset returns as identified from the reviewed literature. Since, most of the questions are pivotal to the financial management, answering half of them correctly indicates a low financial literacy among the respondents.

To check the validity, a pilot study was conducted face-to-face with selected 10 respondents to know the relevance of the questionnaire. Feedback was received from the eight reviewers, who made suggestions regarding content and format of questions. Based on their comments, recommendations, and inputs, we made changes to improve the questionnaire.

Sampling and Data Collection

The sample considered in this study is a subset of the large population of expatriates in UAE. The non-probability convenience sampling is adopted in the present study. The questionnaire was administered to the expatriates working in different capacities in the UAE. The total number of distributed questionnaires was 600 and 450 expatriates filled in the questionnaire; out of this, 69 were eliminated because of the incomplete data or response bias of extreme values. The retained questionnaires represent an effective response rate of around 64.83 percent of the total sample.

Data Analysis and Results

The Profile of the Study’s Respondents

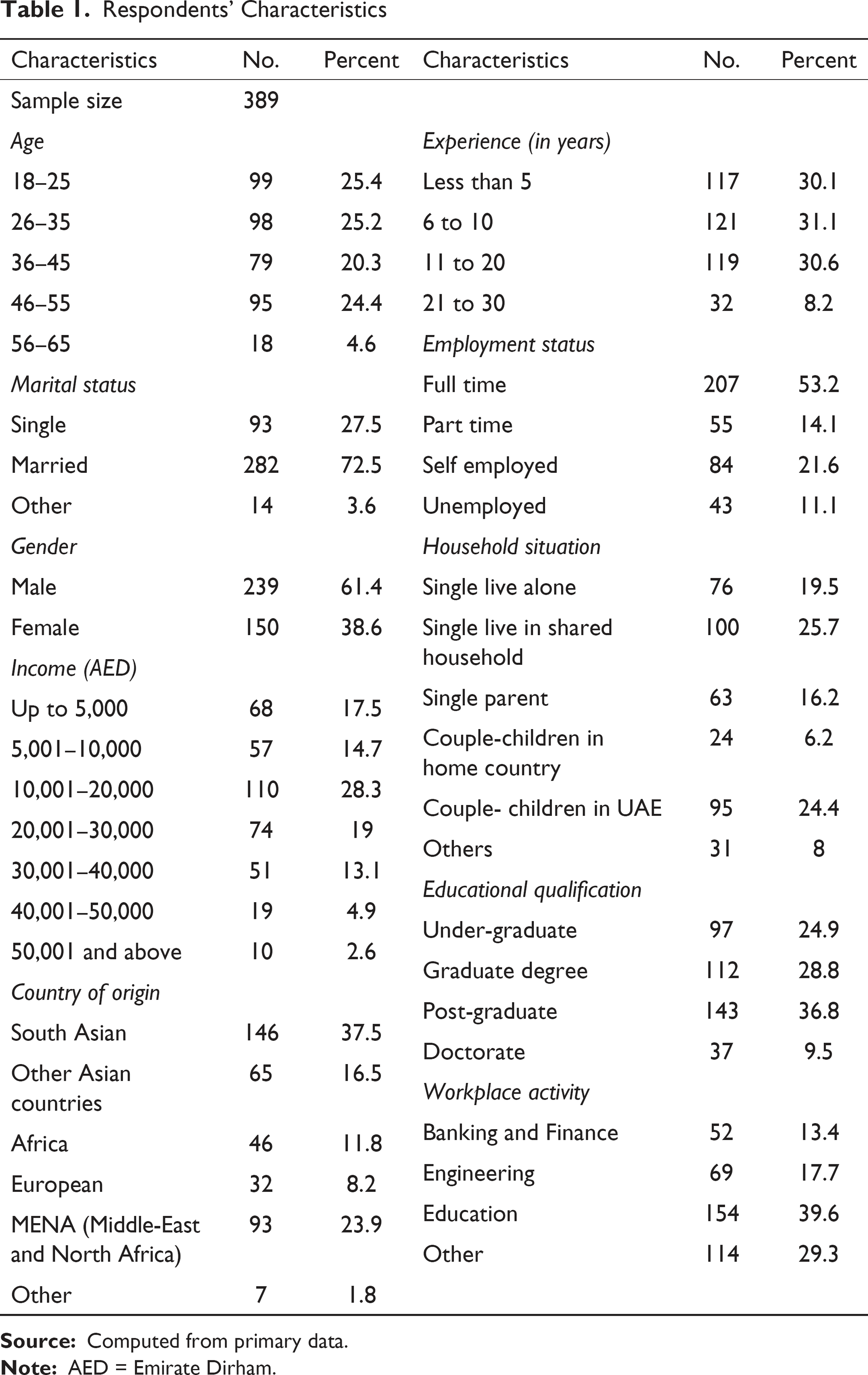

The questionnaire asked each respondent to provide demographic data, such as age, marital status, gender, country of origin, income, experience, education, employment status, work place activity, and house-hold situation. Table 1 provides descriptive statistics for the respondents’ characteristics. From the analysis, majority 61.4 percent of the respondents were male while female represented 38.6 percent of the respondents in the study. With regard to age, 20.3 percent were between 36 to 45 years with the rest evenly distributed among other age groups. On the status of the marital status, 58.1 percent were unmarried and the rest are from married and another category. With respect to country of origin, 37.5 percent are South Asian, 23.9 percent from MENA region, 16.5 percent from other Asian countries, 11.8 percent from Africa, 8.2 percent from European countries, and the rest 1.8 percent from other countries.

Respondents’ Characteristics

As for income, about 17.5 percent received income up to AED 5,000 and 82.5 percent received more than AED 5,000. As for education, 9.5 percent of the respondents had a doctorate, 24.9 percent under-graduate with no or little education, 28.8 percent were graduates, and the remaining 36.8 percent had post-graduate degree. About 53.2 percent of the respondents were full-time employees, 21.6 percent were self-employed, 14.1 percent were part time, and 11.1 percent were unemployed. With respect to work place activity, 13.4 percent were with banking and finance, 39.6 percent in education, 17.7 percent in engineering, and 29.3 percent in other sectors, respectively. In terms of work experience, 8.2 percent of respondents had 21 to 30 years of work experience with the rest evenly distributed among other categories of experience. For household situation, 19.5 percent of the respondents were single or were living alone, 25.7 percent in shared household, 24.3 couple with their children in UAE, and 8 percent in another category.

Financial Literacy of Expatriates in UAE

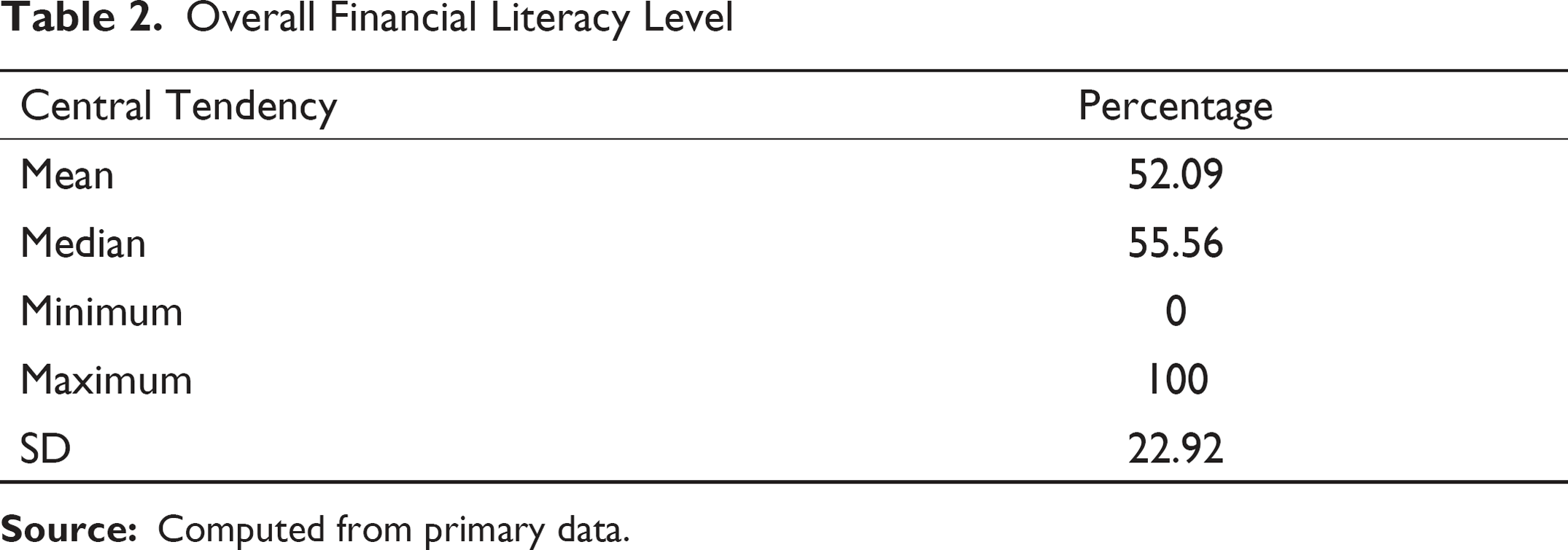

Table 2 presents the overall respondents’ scores on the financial literacy test. Considering the questions are basic and easy, answering 52.09 percent of questions correctly, and suggesting that the respondents’ knowledge about financial literacy is not sufficient. The descriptive statistics show that the median score is 55.56 percent.

Overall Financial Literacy Level

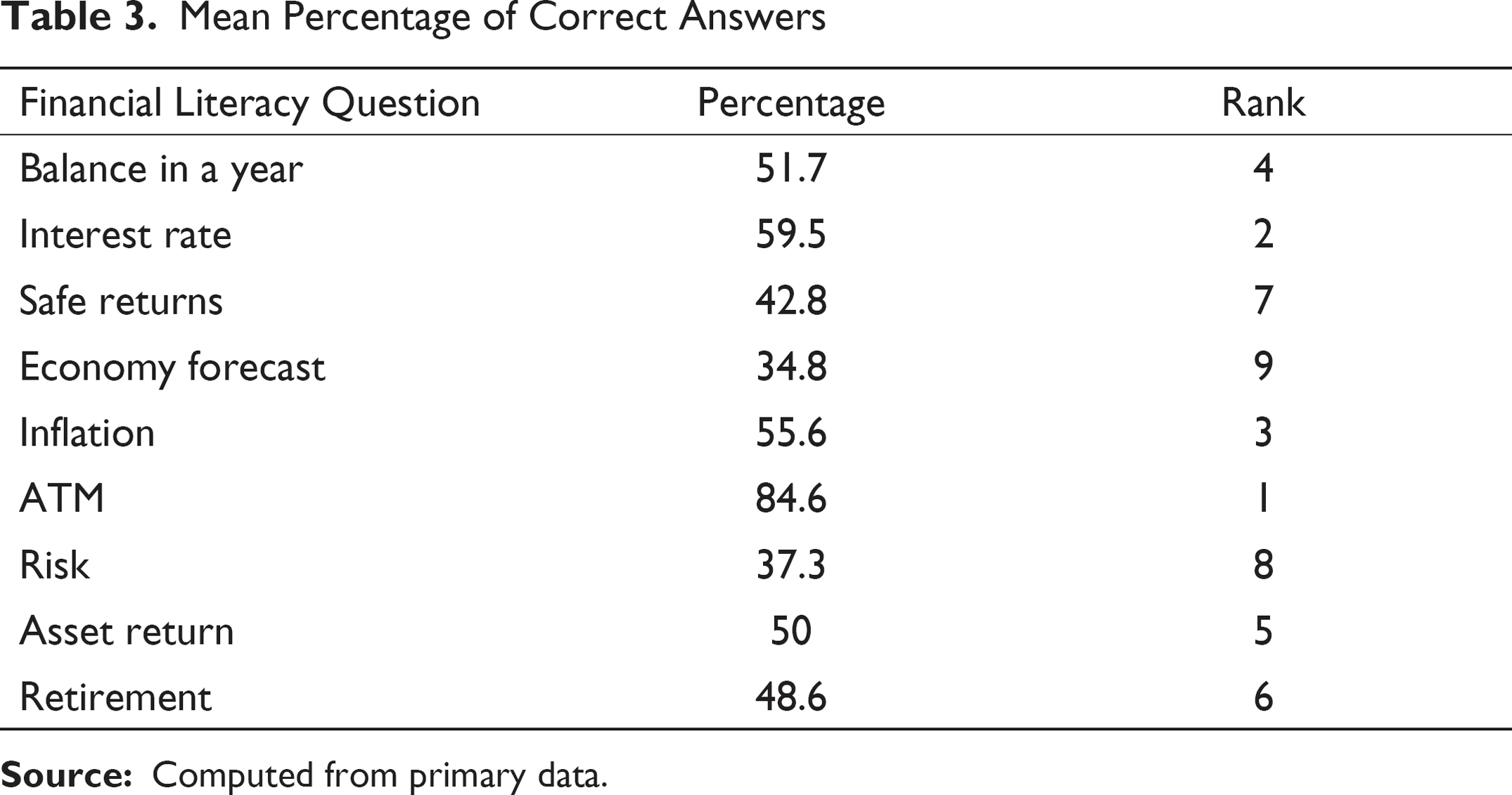

Table 3 summarizes the questions and their correct responses with their ranks. It is evident from it that highest rank 1 with 84.6 percent respondents answered correctly when asked question about ATM. This augurs well that respondents are well aware of the working of ATM machines. Eight other questions on the basis of ranks sorted in highest scores are rank 2 with 59.5 percent to interest rate, rank 3 with 55.6 percent given to inflation. Remaining six questions scored lower than the median with rank 4 is balance after 1 year with 51.7 percent. Asset returns with 50 percent is given rank 5, rank 6 with 48.6 percent to retirement, rank 7 with 42.8 percent is given to safe returns, question on risk is answered by 37.3 correctly with rank 8 and the last rank 9 with 34.8 percentage is about economy forecast.

Mean Percentage of Correct Answers

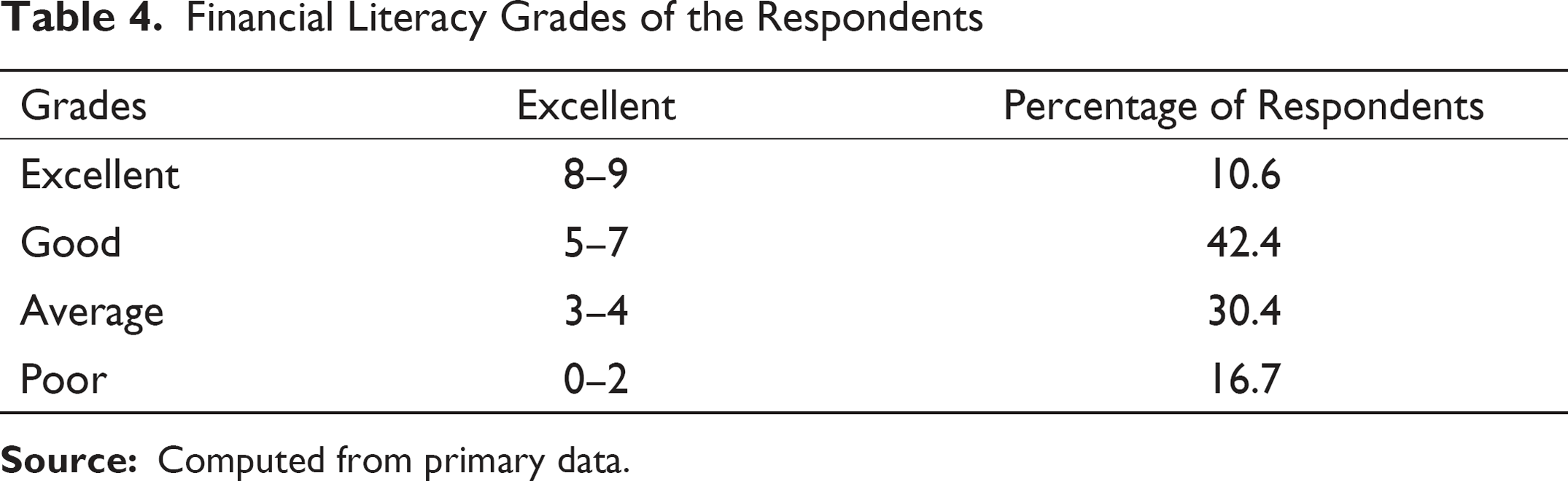

Respondents’ knowledge in the survey is graded into four grades, such as excellent, good, average and poor based on their performance in the test, which is presented in Table 4.

Financial Literacy Grades of the Respondents

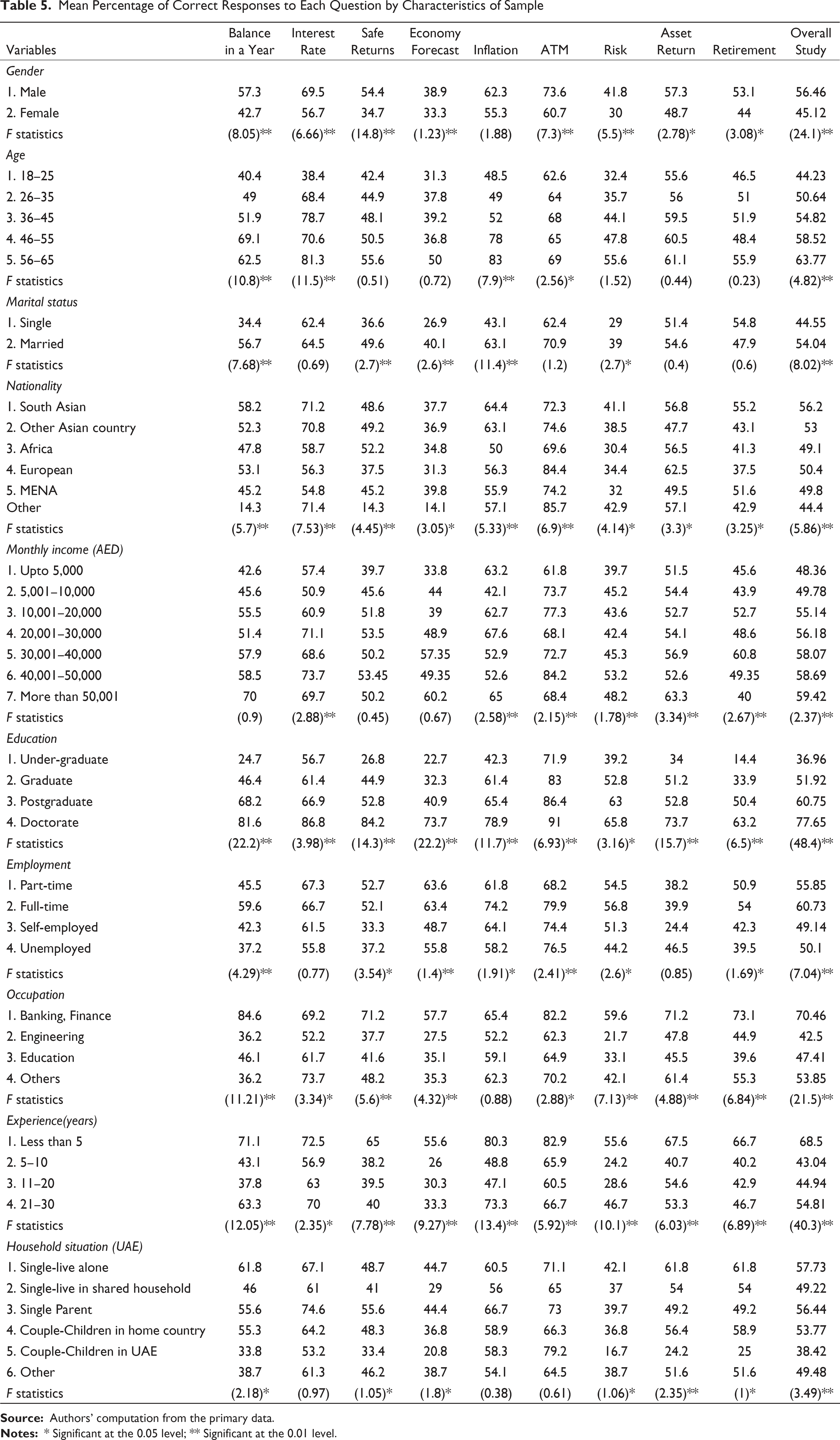

The objective of the study is to explore the relationship between financial literacy and demographics of the respondents using ANOVA. The mean percentage of correct responses for different subgroups and results of ANOVA are presented in Table 5.

Mean Percentage of Correct Responses to Each Question by Characteristics of Sample

Male respondents scored higher (56.46 percent) than the female respondents (45.12 percent) in the overall financial literacy test. The ANOVA shows significant difference between male and female across the sections and lower levels of financial literacy among women. All the nine areas of financial literacy show the same pattern with respect to the gender. The values of F statistics suggest that the differences in all the nine questions are highly significant. The result confirms the findings of previous studies (Chen & Volpe, 1998; Al-Tamimi & Kalli, 2009; Lusardi & Mitchell, 2011; Volpe, Chen & Pavlicko, 1996). All these studies document a significant gender gap in financial literacy.

Respondents in age group exhibit an increase in pattern of financial literacy with an increase in age. The mean percentage of older participants between 56 to 65 years (63.77 percent) is higher than the other younger participants. The F statistics suggest that the difference is statistically significant in five out of the nine questions and for the entire sample. The results confirm the findings found in previous research (Chen & Volpe, 1998).

Results of ANOVA indicate that the difference in financial literacy between single and married respondents is statistically significant at 0.01 level, except in the interest rate, retirement, ATM, risk, and asset return. The survey has a category “others.” However, the number of respondents in this category is small and is regrouped into “single” groups. Respondents from different countries’ have different levels of financial literacy. Results of ANOVA indicate that the scores are statistically significant at the 0.01 level. Respondents’ from South Asia scored highest (56.2 percent) on the overall study. Results of ANOVA indicate that the difference in financial literacy between single and married respondents is statistically significant at 0.01 level. However, the number of respondents in “other” categories is small and is regrouped into “single” group.

The ANOVA result for the entire sample suggests that participants with a higher monthly income answered more questions correctly than those with a lower income. The F statistics for the entire income sample is statistically significant at 0.01 level. Respondents with more education had a greater financial literacy than those with less education. Specifically, those with doctorates (77.65 percent) scored better than those with other education category. The F statistics for the entire income sample is statistically significant at 0.01 level. ANOVA results also confirm that certain occupational classes such as business and finance demonstrate more financial literacy than other categories. These differences are statistically significant at 0.01 level.

Employment is also significant at 0.01 level with the highest mean percentage of answers is observed in full time (60.73 percent) category. The survey has an employment category of “student” and “retired.” However, the number of respondents in these categories is small and is regrouped into “unemployed” group. In terms of respondents’ occupation status, respondents working with banking and finance experience are more knowledgeable than respondents working with other sectors and the overall ANOVA results are significant at 0.01 level. Respondents’ financial literacy level is compared with their household situation and work experience in UAE. Specifically, those who are single living alone and single parent scored better than those with children in UAE. In terms of experience less than 5 years scored highest in overall questions answered. The ANOVA results indicate that the differences in household situation and work experience are statistically significant at the 0.01 level.

Summary and Conclusion

The present study was designed to determine the effects of respondents’ characteristics on financial literacy. Overall, we find that the level of financial literacy of expatriates in the UAE is low. Our survey finds that an average respondent answers only half (52 percent) of the financial literacy questions correctly seems to indicate a deficiency in the knowledge of basic financial concepts. Analysis of the impact of demographic characteristics on financial literacy using ANOVA shows that age, marital status, gender, income, country of origin, education, workplace activity, work experience, employment status, and household situation influence financial literacy at varying levels of statistical significance.

The study examines financial literacy with reference to gender and finds lower level of financial literacy among women and this finding complements those of the earlier studies (Chen & Volpe, 1998; Al-Tamimi & Kalli, 2009; Lusardi & Mitchell, 2011; Volpe, Chen & Pavlicko, 1996). All these studies document a significant gender gap in financial literacy. The lower levels of financial literacy among women calls for customized financial literacy improvement programs for women as they could play a key role in securing the financial well-being of expatriates. Financial education programs aimed at women in the UAE may be imparted through various channels such as educational institutions, teaching finance basics at young age, local bodies, and engaging women as trainers.

One of the more significant findings to emerge from this study is that financial literacy improves with age. It is difficult to explain this result, but it might be related to the fact that people learn basics of money management either through reading materials or peer network. Addressing the money skill in the younger age can improve financial outcomes in future. The study also finds that the occupation or type of work has an influence on the level of financial literacy of expatriates. These results are corroborating the idea of Al-Tamimi and Kalli (2009) who suggested that high-income respondents who hold high educational degrees, and those who work in the field of finance/banking or investment had as expected a higher financial literacy level. This points to the importance education in building the financial literacy level.

Our study contributes to the empirical evidence that details the levels of financial literacy among expatriates in the UAE. The study also strengthens the case for investing in financial education of the young as an antidote to widespread financial illiteracy.

We analyzed the influence of only demographic factors on financial literacy, which is a drawback of this study. Other variables such as self-efficacy, cognitive level, and financial socialization of an individual may play an important role in determining the financial literacy. Future research focusing on these variables would be worthy and insightful. As this study restricted the expatriates in the UAE, a more robust sampling to study expatriate’s financial literacy in other Middle Eastern countries may be used in further studies. The financial literacy instrument used in this study is developed primarily for expatriates in the UAE incorporating specific questions tailored to test the financial literacy. Future research may also focus on developing financial literacy programs.

Footnotes

1.

2.

![]() . Data presented in the article were the most recent estimates supplied to the writers by origin countries’ embassies. In general, sending countries’ estimates cannot be as accurate as receiving countries’. In the UAE, EIDA is in the process of completing the recording of all residents, nationals and non-nationals, in the country in order to deliver ID documents to all.

. Data presented in the article were the most recent estimates supplied to the writers by origin countries’ embassies. In general, sending countries’ estimates cannot be as accurate as receiving countries’. In the UAE, EIDA is in the process of completing the recording of all residents, nationals and non-nationals, in the country in order to deliver ID documents to all.