Abstract

The United Arab Emirates (UAE) is a popular destination for migrant workers worldwide, not just from Asia. Along with expanding the UAE’s economic activities, the amount of remittance outflows has increased dramatically, making it the second-largest remitting country, just behind the United States. This study looks into the important demographic factors that influence migrant remittance behavior in the Emirates. The examinations revealed that age, race, marital status, and a number of dependents are the most important factors influencing remittance behavior, while gender is found to be insignificant, proving the popular premise of female altruism to be incorrect. The findings are expected to assist policymakers in the government in devising ways and means to reduce remittance outflows as they have vital implications for some key macro-economic variables such as inflation and exchange rate as well as financial service providers in the UAE, in orchestrating a suitable promotional strategy to target suitable cohorts.

Introduction

The term demography was coined by Belgian statistician Achille Guillard in his publication Elements de statistique humaine, ou démographie comparée [Elements of human statistics, or comparative demography] in the year 1855 (Poston, Jr. & Bouvier, 2018). Since then, it has been widely used and has always piqued the interest of policymakers, statisticians, and scholars. One such important aspect of understanding the role of demography comes into play when we relate this term with migrants and their remittance behavior. When people move from their home country to a host country, they become a part of the latter’s society, and their actions impact the economy (Alkhathlan, 2013).

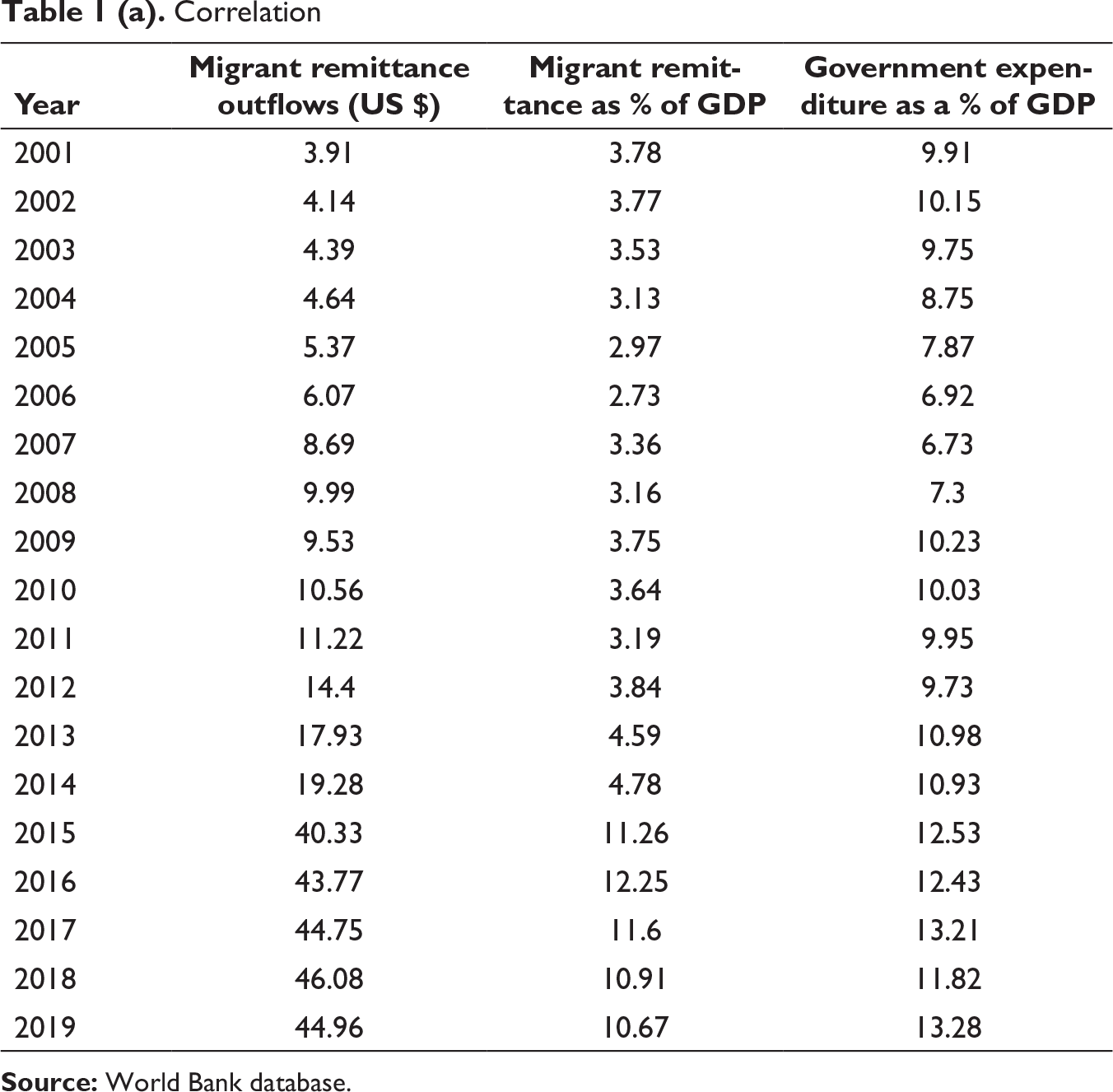

Correlation

Source: World Bank database.

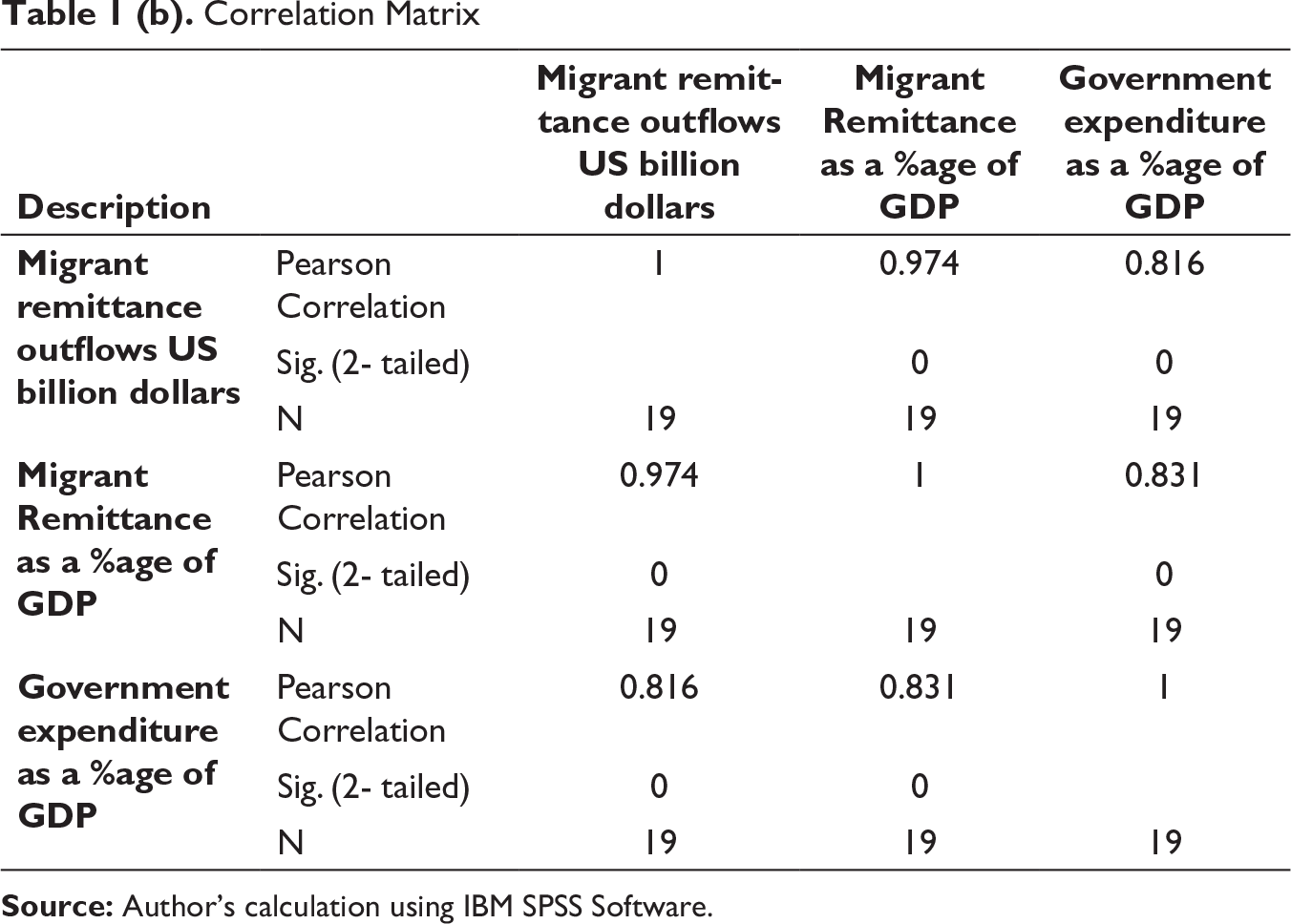

Correlation Matrix

Source: Author’s calculation using IBM SPSS Software.

Tables 1(a) and 1(b) show the migrant remittance outflow, remittance outflow as a percentage of gross domestic product (GDP), and government expenditures as a percentage of GDP in the UAE during 2001–2019. It depicts a high correlation of 0.974 between migrant remittance outflows and migrant remittance as a percentage of GDP, a correlation of 0.816 between migrant remittance outflows and government expenditure (percentage of GDP), and a correlation of 0.831 between migrant remittance as a percentage of GDP and government expenditure (percentage of GDP), which mean that when the government increased its’ expenditure it has caused an increase in economic growth and led to increasing outflows of workers’ remittances from the country (World Bank, 2020).

Researchers in the past have highlighted that as the cost of living in a country increases, it affects the migrant remittances negatively (Naufal & Vargas-Silva, 2009). Moreover, as indicated in the Tables 1(a) and 1(b), existing research also argued that a higher remittance affects key economic indicators like enhancing deflationary pressures, thereby making the government spend more to boost the economy (Alkhathlan, 2013; Termos et al., 2013), which further puts pressure on monetary and fiscal policy and affects exchange rate stability (Naufal & Termos, 2009; Termos et al., 2016). Thus, there is a growing need to examine the variables that lead to remittance outflows to assist the policymakers in their endeavors to devise suitable plans to encourage migrants to invest in the host country.

Over the years, remittances have been one of the most appealing areas for researchers to examine (Al-ubaydli, 2015; Gupta & Hegde, 2009; Heshmati, 2013; Naufal & Genc, 2018; Taylor & Filipski, 2011). However, most researchers concentrated on the effect of remittances on receiving countries and the impact on the rate of economic growth (Heshmati, 2013; Hossain et al., 2017; Jankovic & Gligoric, 2013; Nurse, 2019; Ustubici, 2012). Even though there are studies that look at the influence of remittance outflows on sending countries as well, concentrating on the short-term and long-term effects of remittance outflows on sending countries’ micro and macroeconomic variables (Alkhathlan, 2013; Jena & Sethi, 2020; Naufal & Genc, 2018; Naufal & Termos, 2009; Naufal & Vargas-Silva, 2009), the available literature is still limited.

Remittance outflows began to become important when they were discovered to be influencing the macroeconomic variables of the sending countries (Alkhathlan, 2013; Konan & Zué, 2020; Naufal & Genc, 2018; Termos et al., 2013). From the perspective of the sending country, the researchers attempted to investigate the variables that stimulate migrant remittance action (Naufal & Vargas-Silva, 2009; OECD, 2018; Ruiz & Vargas-silva, 2009; Vargas & Huang, 2006). Even though this is a fascinating area for study, there have not been sufficient studies on the effect of remittance outflows on the sending economy. Thus, the article’s novelty stems from the fact that it is descriptive in nature, explaining the effect of demographic variables on remittance outflows from the UAE, an area that, to the authors’ knowledge, has still not much explored. The findings are expected to have practical implications for the policymakers, regulators, and service providers who facilitate remittances and investments, to prepare their policies to control remittance outflow and target suitable cohorts for their services, respectively. Keeping in mind the aforementioned objective, the study tries to answer the research question: Whether the demographic characteristics of the migrants play a significant role in framing their decision to remit from UAE?

Remittances are cash or in-kind transfers made by migrant workers to their home countries to help their families or dependents meet their financial needs (Adams & Cuecuecha, 2013; Chaudhary, 2020; OECD, 2018). According to the available literature, remittances can also be described as the portion of migrant workers’ earnings sent back to their home country from their place of employment (Kirdar, 2012). Furthermore, remittances have been steadily increasing over the last decade, with the countries of South Asia receiving the majority (Hasan, 2006; Hossain et al., 2017; Nurse, 2019). According to estimates, nearly 80% of the Emirati population is made up of migrants from various countries, and the country has one of the highest remittance outflows in the world (UN, 2020; Viewswire, 2018; Viewswire et al., 2008; World Bank, 2020). Furthermore, the UAE is home to almost all of the world’s major nationalities, who come to work and earn a living to support their families back home (World Bank, 2020). Many countries around the globe depend heavily on remittances from abroad to achieve the desired level of sustainable development and capital accumulation (Heshmati, 2013; Hossain et al., 2017; International Fund for Agricultural Development, 2017; Nurse, 2019). Although researchers in the field have defined several variables as factors influencing the decision to remit, demographic characteristics have consistently been one of their most important constructs (Blue, 2004; Jayaraman, 2019; Naufal & Vargas-Silva, 2009; Ruiz & Vargas-silva, 2009; Vanwey, 2004; Vargas & Huang, 2006).

Some of the authors argued that gender and age are the most significant demographic variables influencing the decision to remit and that education and occupation are not among the factors that have their influence (Jayaraman, 2019). Few researchers indicated that altruism is the emotion that triggers frequent remittances and this emotion is the main factor responsible for gender playing a significant role in remittance decision because females are more altruistic in nature than males and hence, females remit more than males (Vanwey, 2004). Other researchers argued that the advent of Generation Z is to account for the shrinking gap between males and females in decision-making situations (Jiri, 2016). This argument is also supported by some recent additions to the literature. The researchers argued that in the same situation involving Generation Z, males and females have similar preferences (Khan et al., 2020). Even though it was observed in one of the studies involving migrant workers from Mexico that males appear to remit more than females, this contradicts the claims made by the supporters of the theory of altruism (Amuedo-dorantes & Pozo, 2006) and supports some of the recent literature on financial habits of females (Cwynar, 2021). As a result, it would be fascinating to investigate how gender influences remittances from the UAE.

Furthermore, researchers in a recent study of non-resident Indians residing in the United States concluded that age was a major factor influencing the frequency of remittances (Jayaraman, 2019). This is consistent with previous research, which suggests that age is a key demographic variable influencing remittance activity, with older migrants remitting more than their younger counterparts (Amuedo-dorantes & Pozo, 2006) and is consistent with the recent works on the financial habits of younger population (Cwynar, 2020). As a result, it seems reasonable to investigate how migrant workers’ remittance activity is affected by their age in the UAE. Thus, the following hypotheses can be made: age of the migrants significantly affects the decision to remit from the UAE (H1); and gender of the migrants significantly affects the decision to remit from the UAE (H2).

Researchers have previously claimed that race and ethnicity are important factors influencing remittance behavior (Amuedo-dorantes & Pozo, 2006; Drinkwater, 2007). Researchers claim that the global migrant percentage is rapidly changing, with people of Asian descent accounting for 36% of the overall migrant population, leaving migrants from Europe and Latin America behind (Connor et al., 2013; Gupta & Hegde, 2009; Jayaraman, 2019; Mumtaz & Smith, 2020). This argument is supported by World Bank data on foreign remittances received, which shows that India and China are the top two countries receiving remittances from abroad, respectively (World Bank, 2020). Researchers have concluded on several occasions that the majority of total foreign remittances go to Asian countries, followed by European nations and when it comes to growth in international remittances received, African countries are at the top of the list (Amoyaw & Abada, 2016; Hasan, 2006; World Bank, 2020). In the past, researchers have looked into the influence of education levels and attempted to relate them to an individual’s financial behaviors (Lusardi & Mitchell, 2014; Natoli, 2015, 2018). They claim that a lack of formal education is often linked to a lack of financial literacy, contributing to poor financial decisions (Bourova et al., 2018; Capuano & Ramsay, 2012; Lusardi et al., 2020; Lusardi & Mitchell, 2011). Education has also been described as a significant demographic factor influencing remittance behavior by researchers in the field of migrant studies (Natoli, 2015, 2018). However, the authors of a recent report on non-resident Indians in the United States found that education is not a primary demographic factor influencing their decision to remit (Jayaraman, 2019). Thus, the authors believe that it would be worthwhile to examine how race and education level of migrants in the UAE affect their remittance behavior, where people of almost all the races of the world work and in almost every sector, hence the hypotheses that: race or ethnicity of the migrants significantly affect the decision to remit from the UAE (H3); and education level of the migrants significantly affect the decision to remit from the UAE (H4).

Over the years, researchers in migrant studies have argued that one of the major factors affecting the decision to remit is migration (Pinger, 2009; Ruiz & Vargas-silva, 2009; Simpson, 2017). They have also identified that there are several reasons responsible for migration such as unemployment, economic and political conditions of the home country, and the need to provide financial support to counter widespread poverty (Bouoiyour & Miftah, 2015; Pinger, 2009; Simpson, 2017). The researchers have also argued that migration plays a significant role in framing the remittance behavior of the migrant (Song & Liang, 2018). Some studies have highlighted that the inflow of remittances enhances capital formation and investment in the home country (Heshmati, 2013; Jankovic & Gligoric, 2013). The researchers have further argued that altruism plays a major role in framing the remittance behavior of migrants abroad (Amuedo-dorantes & Pozo, 2006; Ruiz & Vargas-silva, 2009; Vanwey, 2004; Vargas & Huang, 2006).

The examinations done in the past have given an insight that the marital status and number of dependents back home are the key demographic characteristics framing the intention to remit (Drinkwater, 2007; Gupta & Hegde, 2009; Jayaraman, 2019). Researchers have also argued that if more members of the family of the migrants are there in the host country, it has a negative impact on the remittance outflows (Markova & Reilly, 2007). The researchers also argued that the access to social security and the chances to get permanent residency in the host country for the dependents also affected the remittance behavior (Kirdar, 2012; Markova & Reilly, 2007). However, in the case of migrants in the UAE, the chances to get permanent residency for self and dependents is very rare, and similarly, the social security benefits available are also bare minimal, hence it would be interesting to examine how the reason for migration, marital status, and number of dependents frame the remittance behavior of migrants in the UAE. Thus, it can be assumed that: migration significantly affects the decision to remit from the UAE (H5); marital status significantly affects the decision to remit from the UAE (H6); and the number of dependents in the home country significantly affects the decision to remit from the UAE (H7).

The researchers in the field argued that one of the major motivations to migrate is the potential to earn higher wages (Bjuggren et al., 2017; Simpson, 2017). Several studies were conducted in the past wherein a strong relationship was established between income and remittance frequency (Drinkwater, 2007; Gupta & Hegde, 2009; Jayaraman, 2019). In one of the studies on the remittance behavior of Bulgarian migrants, the researchers even concluded that those earnings more tend to remit 20% more amount as compared to those earnings low (Markova & Reilly, 2007). However, in one of the other studies, the authors argued that even though income is an important demographic characteristic affecting remittance behavior, they rejected that those earnings more tend to remit more frequently on the ground that migrants from Somalia tend to remit more even though their income is much less (Carling, 2008). The researchers further argued that altruism and an effort to ensure social security for the dependents affect the frequency to remit rather than income (Kirdar, 2012; La & Xu, 2017; Song & Liang, 2018; Vanwey, 2004). In one of the recent examinations on the remittance behavior of migrants in Canada concluded that income affected remittance, but there is no relationship between higher income levels and frequency to remit (Amoyaw & Abada, 2016). In one of the studies on the UAE argued that the cost of living affects the disposable income and thereby amount remitted (Naufal & Vargas-Silva, 2009). The UAE is home to one of the largest populations of migrant workers across the globe (UN, 2020; World Bank, 2020), it would be quite desirable to examine income as a variable affecting the remittance and percentage of remittance done by migrants. Thus, the next research hypothesis framed as, income of the migrants significantly affects decision to remit from the UAE (H8).

A Note on Methodology

The study targeted migrant workers working in various parts of the UAE. The data were collected using a structured questionnaire during November 2020 and February 2021. The sampling technique adopted was stratified to ensure participation of various age groups, gender, income level, and education level to ensure that various nationalities participate in the survey. The questionnaire was administered through face-to-face interviews and later, with COVID-19 restrictions in place, using various social media channels such as Facebook messenger, LinkedIn, and WhatsApp as a shared link of Google form. The experience of working in various organizations in the UAE has helped the authors in targeting an adequate sample size for the study and in the collection of data through personal interviews.

Sample Profile of respondents

Source: Author’s calculation using IBM SPSS Software.

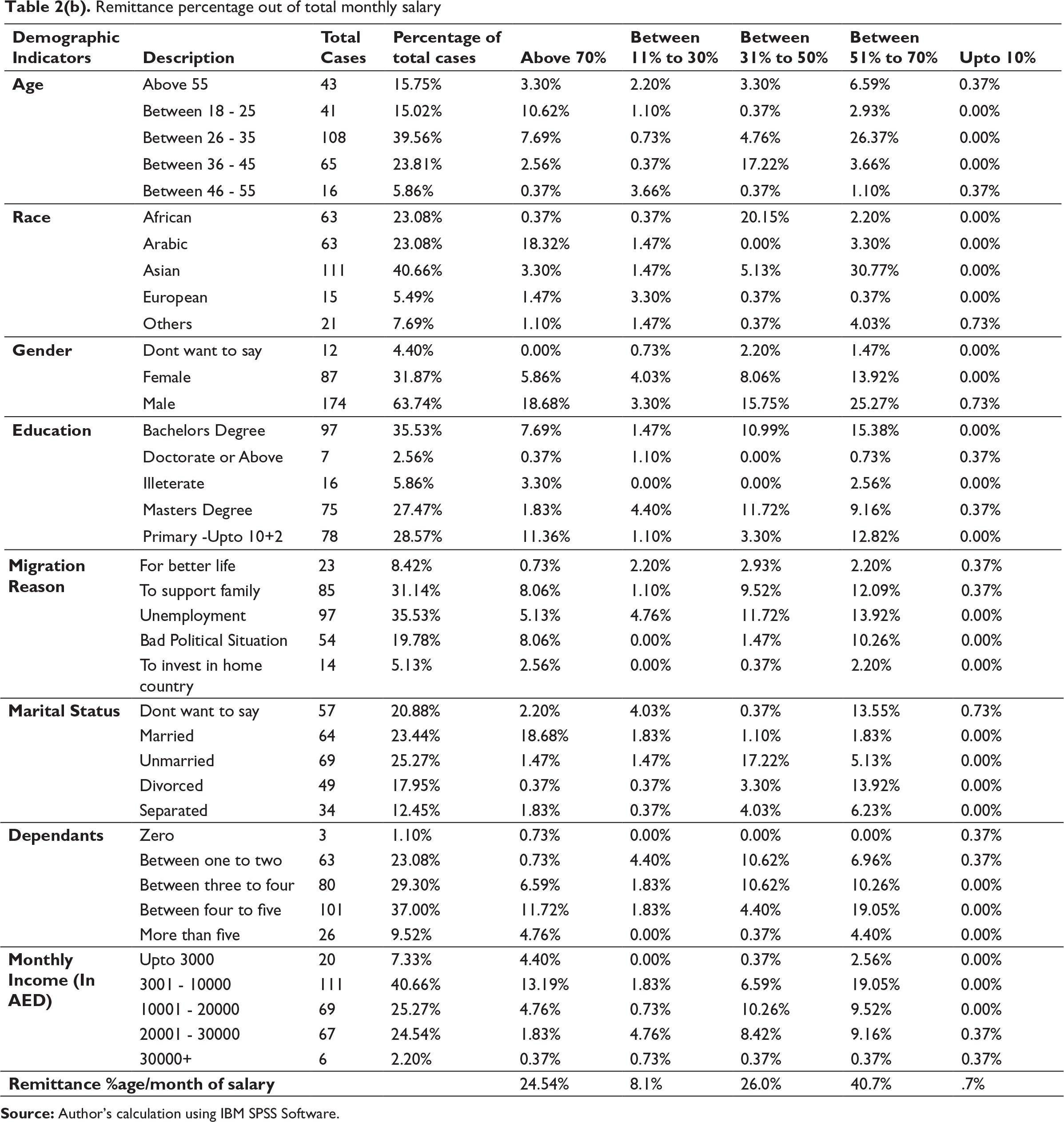

Remittance percentage out of total monthly salary

Source: Author’s calculation using IBM SPSS Software.

Table 2(b) further compliments Table 2(a), in explaining the sample characteristics, in terms of their total number and percentage in the sample and percentage of income remitted by each sub-cohort, like in the sample collected for age cohorts all the respondents fall between the sub-cohorts of 18 years to more than 55 years, with the majority of the respondents (39.56%) falling in the sub-cohort of 26–35 years and remitting a major portion of their income, 7.69% of the respondents belonging to this age group remit above 70% of their income; however, in the sub-cohort 18–25 years, 10.62% of the respondents claim to remit above 70% of their income. Similarly, the table tries to establish a relationship between other demographic cohorts.

Moreover, Table 2(b) further provide useful insights to the policymakers and service providers describing the remittance activity of each sub-cohort, which they can use for framing suitable policies to control remittance outflows or preparing a suitable marketing strategy, respectively. For example: (a) the age sub-cohorts provide valuable insights on how the population falling in the age group 18–35 years remits more money as compared to the older population; (b) further the Arabic and African races in the UAE remit a majority proportion of their income, and depending upon their participation in the sample we may claim that they are also there in considerable numbers in the UAE; (c) the sample depicted that males tend to remit more as compared to females; however, their participation in the sample is also much more than females; (d) the Table 2(b) portrays that people who are highly and professionally literate tend to remit less as compared to those who are illiterate or have received only primary education (employed in blue collar jobs); (e) those who migrated due to unemployment at the home country tend to remit more as compared to those who migrated due to bad political conditions; (f) respondents who are married tend to remit more as compared to those who are single or separated; (g) people with more number of dependents tend to remit more share of their income; and lastly (h) those who are earning less tend to remit more as compared to those who are getting higher salaries in the UAE.

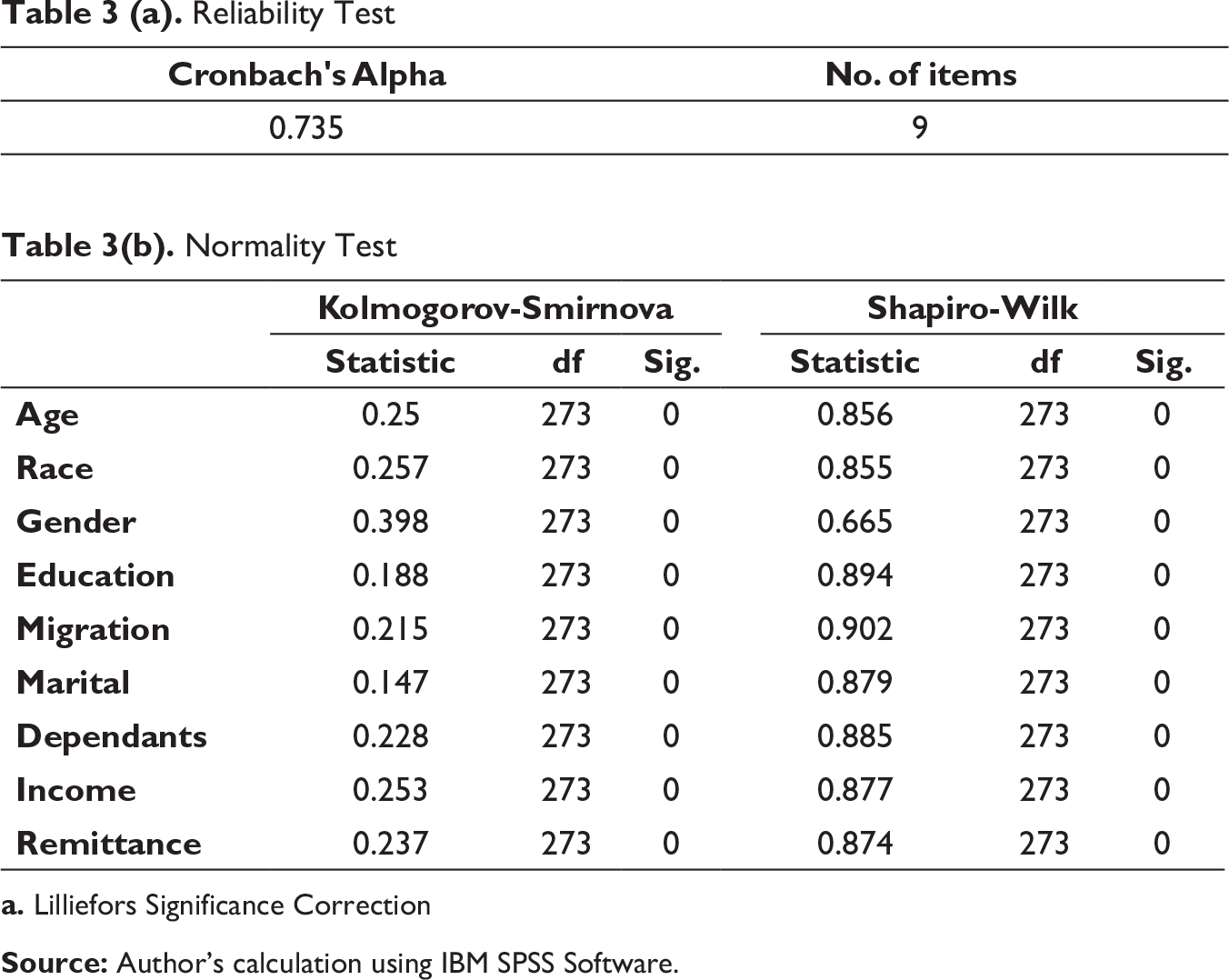

Reliability Test

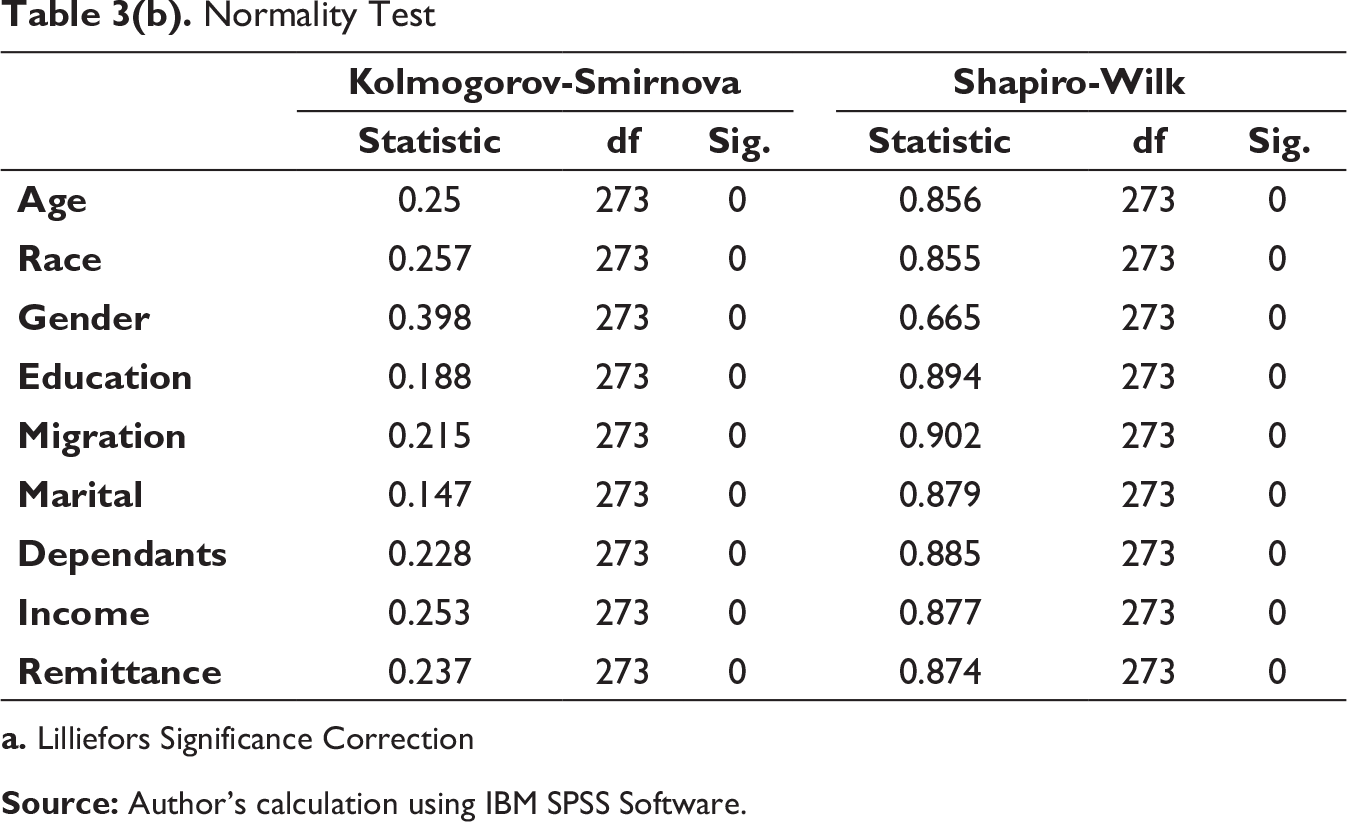

Normality Test

a. Lilliefors Significance Correction

Source: Author’s calculation using IBM SPSS Software.

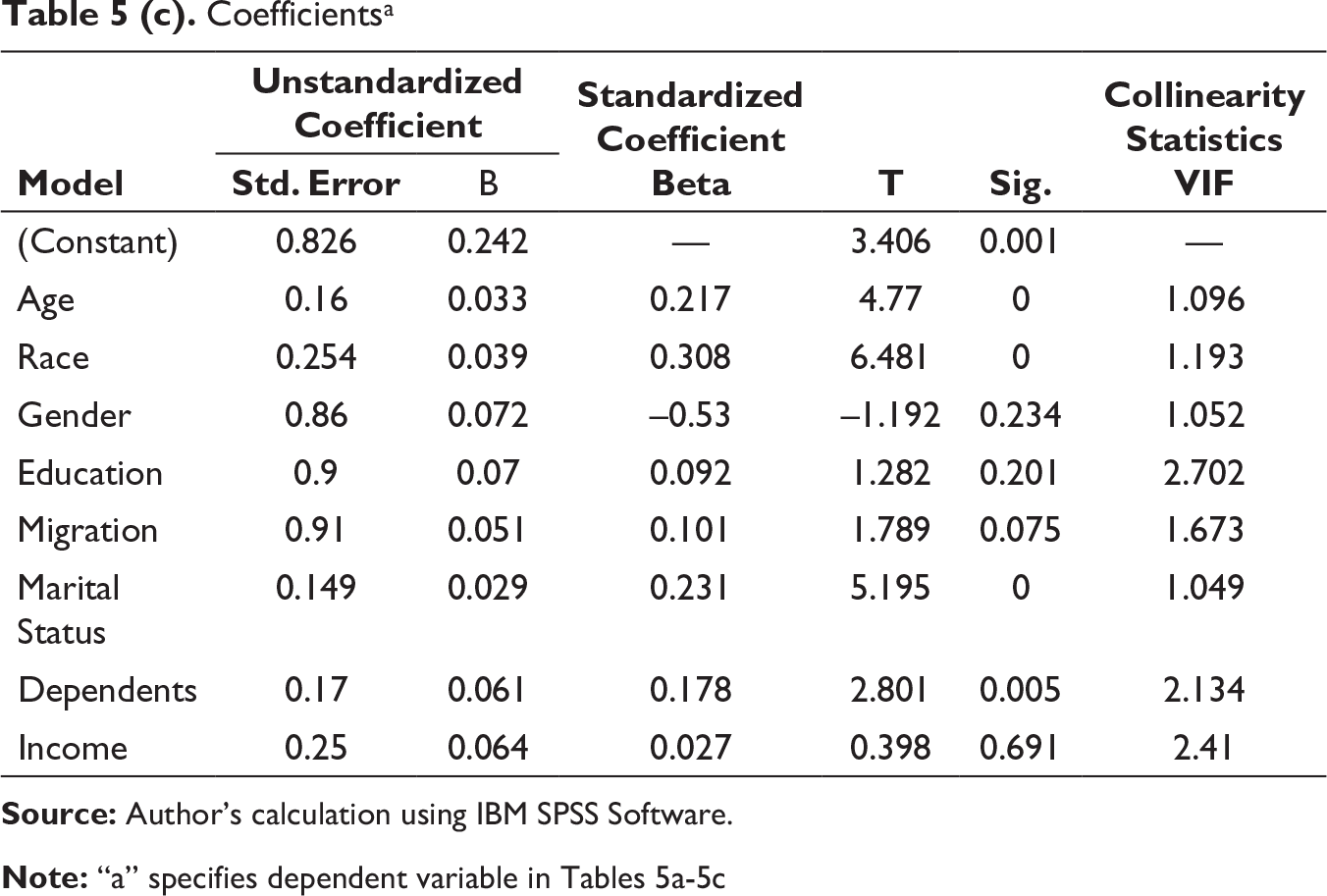

Once adequate samples are collected, the first step involved examining common method bias which was not found as due care is taken in this regard from the beginning of the study (Osakwe et al., 2016). Moreover, the respondents were given due confidence that their responses will be analyzed in a confidential manner (Podsakoff et al., 2003). The next step involved reliability testing of the variables and for this, Cronbach alpha is applied, and all the constructs used demonstrated a value of 0.735 (Table 3(a)), which falls under the acceptable criterion (Hair et al., 2011), thereby establishing the composite reliability of the construct used. The variance inflation factor values for the study fall under 1.049 and 2.702 (Table 5(c)), which are within the threshold of signaling any collinearity (Becker et al., 2015; Hair Jr et al., 2014). The study conducted normality tests of the constructs used, which concluded that all the variables used hints at non-normality (Table 3(b)) Hence, a non-parametric test chi-square is applied to examine the data.

Step two of the analysis involved linear regression analysis to process the data.

Findings

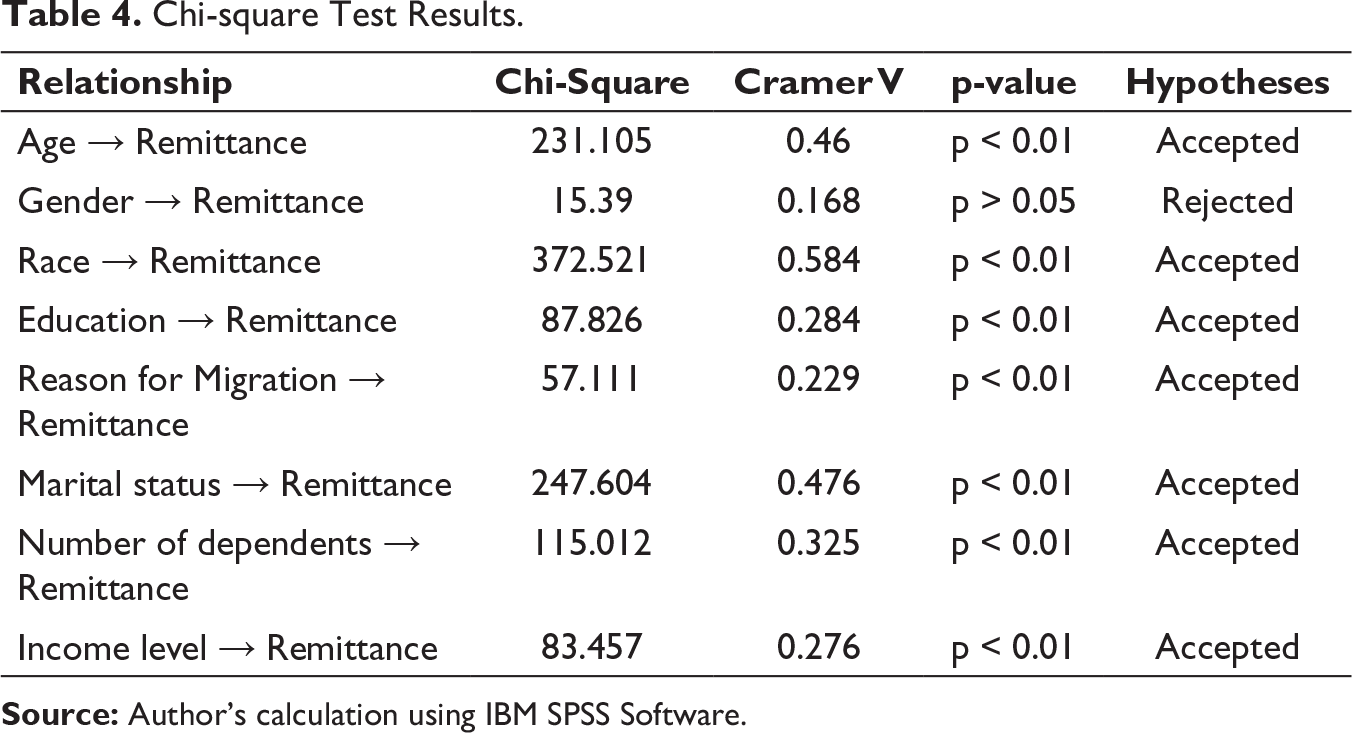

Based on the theoretical discussion, the direct relationship between the chosen variables and remittance behavior is analyzed by administering the chi-square test. The examination conducted on the cohort age ↓ remittance revealed (chi-square value = 231.105; p < 0.01), while the value of Cramer V = 0.460, which hints at a moderate size effect between the variables examined and further confirms the results of chi-square analysis (Sheskin, 2003). Thus, the examination supports H1 formulated for the study as accepted.

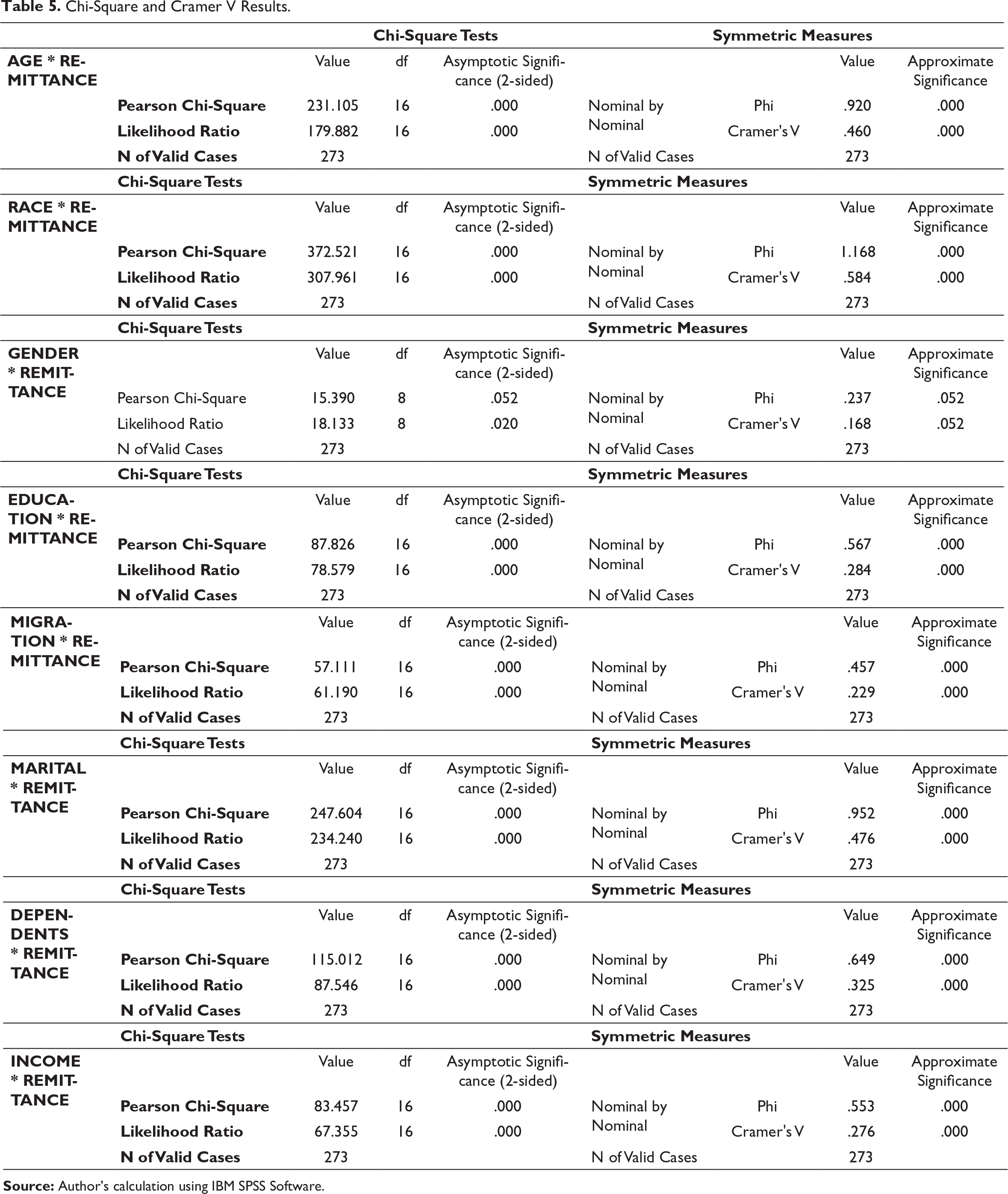

On the other hand, examination on the cohort race ↓ remittance revealed (chi-square value = 372.521; p < .01), and the value of Cramer V = 0.584, which also supports the result of analysis and displays a strong effect size between the variables under observation; hence, the analysis supports H3 as being accepted. Further, the authors examined the relationship between the cohort gender ↓ remittance and the examination revealed (chi-square value = 15.390; p > 0.05) and the value of Cramer V =0.168 also points at low effect size between the two variables; hence, the analysis leads to rejection of H2.

The examination done on the cohorts education ↓ remittance, reason for migration ↓ remittance revealed (chi-square = 87.826 and 57.111, respectively; p < 0.01) along with Cramer V = 0.284 and 0.229, respectively, which hints at low effect size between both variables with remittance; hence, H4 and H5 accepted with a small effect size.

Next, the relationships between the cohorts’ marital status ↓ remittance, number of dependents ↓ remittance were examined, and the examination revealed (chi-square = 247.604 and 115.012, respectively; p < 0.01) with Cramer V values = 0.476 and 0.325, respectively, all of which points at a moderate effect size between the variables and thus H6 and H7 stands accepted.

Lastly, the direct relationship between another key demographic cohort income level ↓ remittance was examined to achieve (chi-square = 83.457; p < 0.01) and Cramer V = 0.276, which pointed at a small effect size between the variables and thereby H8 stands accepted (Tables 4 and 5).

Once the initial analysis revealed the significance level between the variables under study, in the second step, the examination involved linear regression in analyzing the data (Tables 5(a)–5(c)).

Table 5(a) explains the R-statistics for the linear regression model under examination revealed the value of R = 0.708 and R2 = 0.501, which acknowledges that the model explains 50.1% of the variations in the data relatively good.

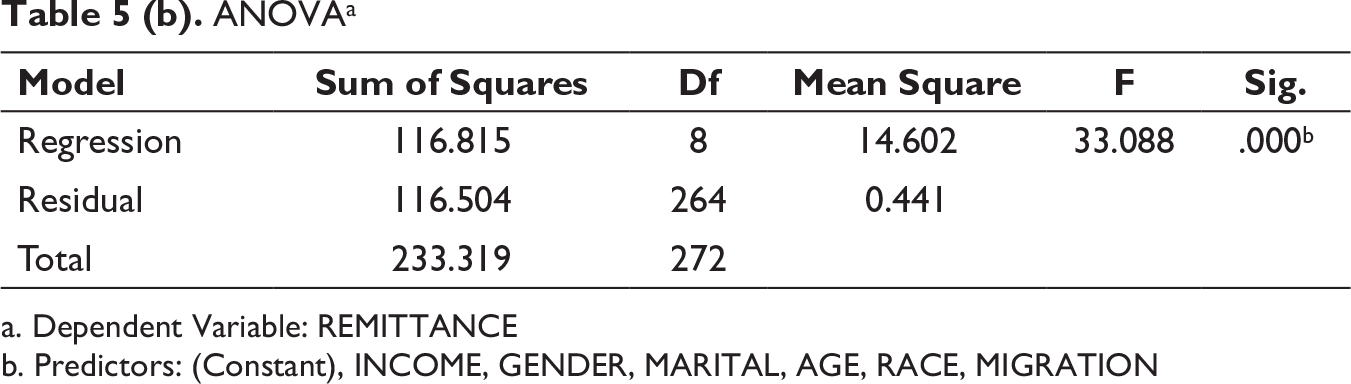

Table 5(b), ANOVA explains the F-test of the linear regression model nullifies the hypothesis that the model explains zero variance in the dependent variable (i.e., R² = 0). The F-test is highly significant (Significance p 0.000 < 0.05), which indicates that, overall, the regression model statistically significantly predicts the outcome (i.e., it is a good fit for the data). Generally speaking, if none of the independent variables are statistically significant, the overall F-test is also not statistically significant.

Table 5(c) explains the examination of all the independent variables under study using β-values, t-statistics, and p-values. The first cohort under examination age revealed β = 0.217, t = 4.770, and p = 0.000, which argues age as a significant variable affecting remittance behavior; thus, H1 is accepted as was the case during the chi-square-based examination. For the cohort based on gender, β = −0.53, t= −1.192, and p = 0.234, hence gender shows an insignificant relationship with remittance behavior; thus, H2 is rejected, which again supports the premise of the chi-square test. Examination of race cohort reveals β = 0.308, t = 6.481, and p = 0.000, which establishes race as a significant variable affecting remittance behavior of migrants; hence, H3 is accepted, which again verifies findings of chi-square tests. The next cohort based on education disclosed β = 0.092, t = 1.282, and p = 0.201, hence the findings contradict the findings of chi-square testing and thus H4 stands rejected. The next cohort in line is the reason for migration, which on examination revealed β = 0.101, t = 1.789, and p = 0.075, which again deviates from the findings of chi-square tests. Thus, under linear regression analysis, H5 stands rejected.

Chi-square Test Results.

Source: Author’s calculation using IBM SPSS Software.

Chi-Square and Cramer V Results.

Source: Author’s calculation using IBM SPSS Software.

Model Summary

ANOVAa

a. Dependent Variable: REMITTANCE

b. Predictors: (Constant), INCOME, GENDER, MARITAL, AGE, RACE, MIGRATION

Coefficientsa

Source: Author’s calculation using IBM SPSS Software.

Note: “a” specifies dependent variable in Tables 5a-5c

Discussion

The study aimed to analyze the framed research hypotheses to understand the relationship between key demographic characteristics of migrant workers in the UAE and their remittance activity. To the best of the authors’ knowledge and belief, this study is amongst the few in evaluating the aforementioned relationships in the context of the UAE. The novelty of the study lies in the examination itself as it would like to assist the policymakers in controlling the remittance outflow from UAE which can affect the macroeconomic indicators such as inflation, investment, and exchange rate stability of the sending country, as indicated by the researchers on many previous occasions (Baas & Melzer, 2014; Jena & Sethi, 2020; Naufal & Genc, 2018; Naufal & Termos, 2009; Termos et al., 2013). Further the findings are also meant to be useful for the service providers in the area of financial services.

When it comes to examining the impact of demographic characteristics on remittance behavior, many similar examinations are being conducted in various parts of the world (Amuedo-dorantes & Pozo, 2006; Blue, 2004; Drinkwater, 2007; Jayaraman, 2019). The findings revealed that the age of the migrants has a significant impact on the remittance activity of the migrants, which is in line with the findings of the previous research conducted in the context of migrants in the United States (Gupta & Hegde, 2009; Jayaraman, 2019), wherein the researchers argued that older migrants tend to remit more as compared to younger counterparts. Likewise, this study reveals that gender does not affect the remittance activity of migrants and is also supported by the available literature (Amoyaw & Abada, 2016), wherein the authors have argued that irrespective of gender, altruism is the major emotion responsible for remittance. The remittance from the UAE is also not affected by the gender of the migrant worker. This further hints at reducing the gender gap as prevalent in the available literature (Cwynar, 2020; Khan & Akhtar, 2020; Khan et al., 2020).

Moreover, the study also examined the relationship between race and remittance behavior and concluded that race and ethnicity significantly affect the remittance activity, which is also in line with the previous literature wherein the researchers concluded that people of Asian and African origin tend to remit more as compared to any other ethnicity (Amoyaw & Abada, 2016; Connor et al., 2013; World Bank, 2020) and is also clear from the descriptive mentioned in Table 2(b). Thus, the remittance activity of the migrants of various races in the UAE shows a similar tendency as shown by the migrant workers at other geographical locations.

The study further examined education as a demographic characteristic affecting the remittance activity, which conceptually seems an important characteristic when it comes to financial behavior (Capuano & Ramsay, 2012; Lusardi et al., 2020; Lusardi & Mitchell, 2011). But as per the literature available, this variable has shown different behavior in different studies conducted at different geographical locations and concerning different race of migrants (Amoyaw & Abada, 2016; Jayaraman, 2019; Natoli, 2015, 2018). However, in the context of the UAE, education was identified as a significant factor affecting remittance activity as per chi-square tests; however, the relationship is not as strong as other variables in the study as reflected by Cramer V, and thus, a further analysis using linear regression model establishes education as an insignificant variable affecting remittance behavior which is in line with the some of the published literature (Amoyaw & Abada, 2016).

Next in line comes an examination of the direct relationship between the reason for migration and remittance behavior, for which the constructs were adapted from the already published literature (Pinger, 2009). The examinations using chi-square revealed a significant relationship between reason to migrate and remittance activity; however, the relationship is not very strong, as suggested by a lower value of Cramer V (0.229). However, further examination using linear regression revealed that reason to migrate is an insignificant variable affecting remittance behavior, and thus, the finding supports some of the existing literature that the migrants are concerned more with other variables such as social security and insurance both in home and host countries (Kirdar, 2012). Nevertheless, the finding is against most of the existing literature which argued that reason to migrate is a key variable affecting the decision to remit (Bouoiyour & Miftah, 2015; Pinger, 2009; Song & Liang, 2018) and thus, offers crucial insights into the remittance behavior of the migrants in the UAE for the policymakers and service providers.

Further examination involving marital status and a number of dependents depicts a significant relationship with remittance behavior, and the value of Cramer V also hints at a very strong relationship between the two variables and is very much in line with the literature which argues that marital status and number of dependents affect the remittance activity of migrant workers (Amoyaw & Abada, 2016; Blue, 2004; Drinkwater, 2007; Gupta & Hegde, 2009; Markova & Reilly, 2007).

Lastly, the authors tried to examine the impact of income on the remittance activity of migrants in the UAE, as the previous literature pointed at a mixed result when it comes to accepting income as a factor affecting remittance activity, wherein most of the researchers have argued that income plays no role in affecting the frequency of remittances (Carling, 2008), while other factors are more significant than income (Amoyaw & Abada, 2016; La & Xu, 2017; Vanwey, 2004). As Cramer V fails to depict a strong relationship between the two variables in question, an examination involving linear regression clearly proved income as an insignificant variable affecting remittance behavior, supporting the existing literature.

Conclusion

The findings of the study provide many insights into the remittance outflows taking place in UAE. The discussion in the previous sections already highlighted that the UAE stands second in terms of total remittance outflows. In just over a decade, remittances have increased by almost 700% (World Bank, 2020). The growing remittance outflow, on the one hand, is an indicator of the growing UAE economy in the entire Gulf region as a preferred location for migrant workers; and on the other hand, it is also a cause of little concern as it affects the exchange rate stability, capital formation, and restricts the local spending which can affect the macroeconomic indicators of the UAE economy (Baas & Melzer, 2014; Naufal & Termos, 2009; Termos et al., 2016). Hence, it becomes important for the policymakers to examine the reasons which cause the remittance, to develop a suitable action plan to control the remittance outflow, and further promote investment and capital formation in the host country itself to ensure a stable exchange rate and also to check deflationary pressures (Alkhathlan, 2013; Termos et al., 2013). Evaluating key variables causing remittance outflows can also be desired by the service providers in the field to develop a suitable marketing strategy to target specific cohorts and sub-cohorts, which can help them generate more revenue.

However, like any other study, this study is also not free from limitations. Firstly, the sample size chosen to conduct the examination; the authors liked a larger sample size which was not possible due to the current COVID-19 restrictions. Secondly, since the study uses self-evaluating statements, there are chances of social response bias. The study also fails to address the impact of the current COVID-19 pandemic situation on the remittance behavior of the migrants, since the pandemic has severe economic, social, and psychological implications (Czech et al., 2020; Laato et al., 2020; Loxton et al., 2020; Talwar et al., 2020). Lastly, there may be several other variables other than demographic characteristics affecting the motivation to remit, which can be addressed in future endeavors.

Footnotes

Annexure

| S. No. | Questions | Please choose the most appropriate action | ||||

| 1 | What is your age? |

|

|

|

|

|

| 2 | What is your race? |

|

|

|

|

|

| 3 | What is your gender? |

|

|

|

||

| 4 | What is education level? |

|

|

|

|

|

| 5 | Which option best describes your reason for migration? |

|

|

|

|

|

| 6 | What is your Marital status? |

|

|

|

|

|

| 7 | What is the number of your (financial) dependent? |

|

|

|

|

|

| 8 | What is your monthly income (in AED) ? |

|

|

|

|

|

| 9 | What percentage of your income do you remit? |

|

|

|

|

|

Declaration of Conflicting Interests

Funding

The authors received no financial support for the research, authorship and/or publication of this article.