Abstract

This study provides new insights into the structural changes in family firm executive teams around succession events. Specifically, we analyze the probability of hirings and turnover of executives in family firms with planned succession events compared to those without a succession. We distinguish furthermore between family-internal or family-external succession arrangements and analyze the hired and dismissed executives’ personal characteristics. We use data on 70,421 executive observations primarily working in SMEs (German “Mittelstand”) from the German Linked Employer-Employee Panel (LIAB) in the period 2009–2019. Applying probit regression models, we find that succession arrangements in family firms exhibit strong differences depending on the occasion, especially in terms of preparation for the type of succession. Family-internal successions are associated with greater continuity among executives, as the probabilities to leave the firms are generally lower. If executives leave a company before internal succession arrangements, they are typically of older age, suggesting a retirement-motivated dismissal. Furthermore, we find evidence that both the qualification profile of executives and their compensation vary depending on the path chosen for the longevity of the firm. Our study aims to establish an empirically strong foundation for future research on the effects of succession events on family firm executives and the resulting changes in firm behavior.

Introduction

In the multifaceted landscape of businesses, family firms are integral to most of the world’s economies (Astrachan and Shanker, 2003; Combs et al., 2018; Gagné et al., 2021). Family businesses are often characterized by a strong interlocking of ownership and management in one person or an owning family, which results in longer CEO tenure and a long-term dynastic orientation, where the owner usually intends to transfer the firm to the next generation (Basco and Calabrò, 2017). These dynamics—particularly the preservation of socioemotional wealth (SEW) and legacy concerns—shape succession processes and distinguish family firms from non-family firms (Berrone et al., 2012; Gómez-Mejía et al., 2007; Zellweger and Astrachan, 2008). Non-family firms typically lack these emotionally driven factors central to succession decisions (Bennedsen et al., 2007; Lumpkin and Brigham, 2011, p. 50). Although prior research has compared family and non-family firms, it often overlooks the heterogeneity within family businesses. Focusing exclusively on family firms allows for a nuanced analysis of succession events, capturing dynamics absent in non-family organizations.

In this context, Socioemotional Wealth (SEW) becomes paramount in explaining the distinct behavior of family firms. SEW encompasses the emotional value that family members attach to their firm, which often includes preserving family legacy, maintaining family control over the business, and upholding family values (Berrone et al., 2012; Gómez-Mejía et al., 2007; Ruf et al., 2021b). This focus on SEW influences various aspects of family business management, from strategic decision-making, succession planning to retaining key employees. Additionally, the emphasis on SEW can impact the firm’s risk tolerance, with family firms often adopting more conservative strategies to protect the family’s socioemotional assets (Chrisman et al., 2012).

Research typically distinguishes between two forms of succession within the family context: family-internal succession, where the successor is a member of the owning family, and family-external succession, where a non-family successor is appointed (Wennberg et al., 2011). Family executives and close relationships with owner-managers are central to family firm identity (e.g. Bellow, 2004; Combs et al., 2010). Nepotistic practices—such as perceptions of unfair selection and imbalanced compensation (the “Fredo-effect”)—highlight distinctive challenges in these contexts (Kidwell et al., 2013). Focusing on the family dimension, our study captures both the continuity benefits and challenges associated with these practices, typically absent in non-family organizations.

Despite extensive research on business successions in family firms, there remains a gap in understanding how succession-events influence executive team structures. Research conducted by Bach and Serrano-Velarde (2015), Hutzschenreuter et al. (2012), and Zhang et al. (2021) has highlighted the pivotal role of executives in family-owned firms, where a less formal management approach and greater employee loyalty prevail, largely attributable to extended workforce tenures. Furthermore, Kollitz et al. (2019) have identified significant challenges in attracting non-family executives, underscoring the complex dynamics at play in the recruitment processes. Thus, executives play a crucial role during the preparation and implementation of succession processes within family firms, and changes in the companies’ management and ownership structures can have significant effects.

The current absence of academic knowledge regarding the impact of succession events on executive workforces in family firms has numerous implications. For example, dismissing executives could cause a loss of implicit and tacit knowledge also preserved in the SEW (Pont and Simon, 2025), which might impact company performance. Nonetheless, this interplay between SEW-preservation and business performance is complex. SEW can sometimes lead to decisions that are not entirely aligned with market logic, it can also foster a unique competitive advantage through the development of strong, long-term relationships with employees (Miller and Le Breton-Miller, 2005). Moreover, the exit of long-serving executives might result in a change of leadership style and thus the company culture. Finally, succession can cause a strain on financial resources when talent must be hired after succession. To address this gap, this article empirically examines if and how executive teams in family firms transform during succession processes and what personnel changes occur before and after the planned succession event. We therefore pose the following research questions:

What is the impact of family firm successions on executive team structures?

How does the succession mode (family-internal vs family-external) moderate this relationship?

Gaining a deeper understanding of the changes in executive teams around firm successions carries several significant implications. Firstly, the introduction of new management and executives is poised to shift strategic perspectives within the organization, as it introduces fresh insights and approaches (Hutzschenreuter et al., 2012). Additionally, the turnover of executives can lead to a substantial transformation of internal organizational knowledge (Hatak and Roessl, 2015). This process does not only involve the departure of experiential or tacit knowledge but also the infusion of new skills and insights by incoming executives (Villadsen, 2012). Moreover, the nature of succession—whether internal or external—can significantly influence the strategic objectives and orientation of the company. External successors might prioritize short-term profit goals, particularly if their focus is on refinancing the purchase price. Conversely, in internal successions, the emphasis often lies on family objectives and the preservation of socio-emotional wealth, which can profoundly influence the firm’s strategic direction.

In our study, we develop three hypotheses based on the current literature and theoretically anchored in the SEW framework. We test our hypotheses by examining the hiring and turnover rates of executives in family business in the context of succession events. We further distinguish between family-internal successions, aimed at transferring the firm to the next family generation (handing over the firm within the owner’s family, e.g. to son or daughter), and family-external successions, where the succession involves a planned transfer of control through the sale of the firm to individuals or entities outside the family (e.g. Schlömer-Laufen and Rauch, 2022; Wiklund et al., 2013). Our research utilizes a sample of 3293 predominantly small and medium-sized enterprises (SMEs), encompassing 70,421 executive observations from the German LIAB linked employer-employee panel data. This comprehensive survey covers a wide range of industries across Germany and offers a panel structure that enables us to analyze changes occurring before and after planned succession arrangements.

Our results show that the type of succession arrangement has a substantial impact on personnel movements within executive teams. In general, family-internal succession arrangements are associated with greater continuity among executives as they are less likely to leave the firms than in family-external successions, especially before the succession events. If executives leave the firm, they are typically of higher age, close to retirement age. In firms with family-external successions, the turnover rate before succession is also lower than in firms with no succession but increases afterward. In addition, we find evidence that both the skill profile of executives and their compensation vary depending on which succession plan is chosen. With our study, we contribute to the literature stream on personnel changes during family firm succession (Bach and Serrano-Velarde, 2015) by uncovering labor dynamics in executive teams around succession events. We also make family firms incumbent owner-managers aware of the necessity to plan their succession holistically. This does not only include the selection and training of the successor, but also the inclusion of all other relevant stakeholders in the succession process. Since non-family executives can take important roles in the succession process and induction of the successors as holders of tacit company knowledge, a strategic staffing of executive positions is of high importance.

The article has the following structure: We discuss the specifics of succession in family businesses in the context of executives for internal and external succession and develop three pathways into our hypothesis. We then describe our sample and methodology. Subsequently, we report the results of our analysis and test our hypothesis. Lastly, we conclude this article with a discussion and a practical as well as theoretical assessment of our research findings.

Research background and hypothesis

Family business succession

The investigation of family business successions has been central in family business research over the past decades (Daspit et al., 2016; Gagné et al., 2021) since they represent important milestones in the life cycle of family businesses. The change of control is a major challenge for family businesses. For companies that are managed by owner families, the focus is likely not only on purely business-related issues but also on aspects of SEW. Oftentimes, it is the wish of the owner (family) that the company remains in family hands and ideally transfers to one or multiple children (Bennedsen et al., 2007). From a resource-based and information economics-based view, the business transfer within the owner family is seen as the optimal succession solution (Cabrera-Suárez et al., 2001; De Massis et al., 2008) and is thus assumed to be the preferred mode among family businesses (Wiklund et al., 2013). Furthermore, Chung (2023) finds that the involvement of family members in the board and the longer tenure of the family candidate in the top management team (TMT) positively influence the CEO succession process.

Important aspects of succession include the organization of the transfer process, the role of the incumbents, the choice and preparation of the successors, the handover itself, and the respective outcomes after the transfer as well as environmental factors surrounding the succession (Daspit et al., 2016; Nordqvist et al., 2013). Successions should be well planned several years in advance to increase the probability of successful business continuation (Ip and Jacobs, 2006). Central factors motivating business succession within the family can be found in the contexts of specific inner-family mechanics, values and traditions (Ruf et al., 2021b). Trust and confidence in the entrepreneurs’ children (Gagné et al., 2021), primogeniture (Bennedsen et al., 2007; Calabrò et al., 2018) or traditions (Lu et al., 2021) play important roles in the predecessors’ reasoning. On the other hand, the failure of incumbent entrepreneurs to hand over businesses in a timely manner due to being clued to their roles and unable to let go (Brun de Pontet et al., 2007; Kets de Vries, 2003) can result in protracted form of succession arrangements (Umans et al., 2020).

In recent years, family-external succession has gained increased attention as the number of family-internal successions has declined (Freiling and Pöschl, 2023; Mahto et al., 2023; Meier and Schier, 2014; Schlömer-Laufen and Rauch, 2022; Wiklund et al., 2013). Causes for family-external successions are manifold and include the owner families’ structure, a lack of motivation and career paths outside the company within the next generation, or unattractive financial conditions (Combs et al., 2023; De Massis et al., 2008; Richards et al., 2019; Wiklund et al., 2013; Zellweger et al., 2011). In these cases, management buy-ins or buy-outs may become viable options to keep the company afloat outside the family (Howorth et al., 2004). Complete withdrawals from the business are particularly widespread among small to medium-sized companies (Bastié et al., 2018), where ownership and management are typically combined in one or few persons belonging to the same family. For larger companies, owner families might still retain strategic firm ownership and retreat to supervisory roles, while top-management positions are held by family-external managers (Chua et al., 2009). Regardless of the specific form, family-external successions offer opportunities for companies to strategically reposition themselves and break new ground, potentially impacting performance (Helfat and Bailey, 2005; Zhao et al., 2020). In this process, particular importance is attributed to the company executives. Executives have often grown or built up the company together with the previous owner, have special roots in the company and have a longer tenure in employment (Block et al., 2015).

Executives in family firms

Executive teams are central to company operations, acting as the vital conduit between management and the workforce by engaging in mediation, delegation, and the organization of work processes (Finkelstein et al., 1996). Within family businesses, the function of executive teams distinctly varies from their counterparts in non-family enterprises, shaped by the distinct familial dynamics governed by SEW. This unique attachment and emotional value placed on the family business profoundly influence how executive teams operate and are structured in these organizations. In family businesses, networks between owner families and employees are typically more informal, affecting the proximity and interaction with executives (Schell et al., 2018). This informality often leads to smoother transitions in leadership and stronger ties to core family members, resulting in less frequent turnovers within the executive team. Non-family executives in family firms frequently assume roles akin to family members, integrating deeply into the fabric of the company (Chua et al., 2009). This integration is particularly evident in small and medium-sized family businesses, where executive teams usually comprise a few individuals besides the owner-managers. These teams are crucial in resolving conflicts and navigating between family interests and economic goals (Rosecká and Machek, 2022).

Furthermore, non-family executives in family firms often share similar age demographics with the owner-managers and have been instrumental in running and growing the businesses over many years. This longevity fosters close, enduring bonds with the companies and its employees, enhancing the stability, and resilience of the executive teams. In mixed executive teams, non-family executives significantly influence the companies and play a vital role in business successions (Barnett et al., 2012). Their presence and participation in the succession process can ensure continuity and preserve the SEW, which is often a primary concern for family businesses.

Preliminary research has explored behavioral patterns in organizations where executive teams influence the succession process or are impacted by it (Daspit et al., 2016). This research underscores the importance of understanding the dynamics of executive teams in family firms, particularly in the context of SEW. The preservation of SEW may lead to specific patterns in executive team composition and behavior, such as prioritizing internal succession, maintaining long-term relationships with executives, and ensuring that the succession process aligns with the family’s values and legacy.

Furthermore, to conceptually frame executive team changes during succession, we distinguish between two theoretically meaningful staffing mechanisms: external recruitment and internal promotion. While these pathways are distinct in their implications for leadership renewal, our empirical data do not allow us to differentiate them systematically. Specifically, our dataset records the entry of new executives but does not capture prior employment history or the origin of the appointment, preventing us from identifying whether a new executive entered the position through internal promotion or external recruitment. Nonetheless, the theoretical distinction remains important. External hires may introduce fresh capabilities and support strategic change, but they can also disrupt existing team dynamics and increase uncertainty (Andrus et al., 2019; Keil et al., 2022). In contrast, internal promotions typically signal continuity, trust, and the preservation of firm-specific tacit knowledge—factors closely tied to SEW in family firms. However, promotions may also reflect entrenched loyalties or non-meritocratic preferences, with mixed implications for performance (Kelleci et al., 2019). Acknowledging these dimensions helps to frame our analysis of executive turnover within the broader strategic and socioemotional dynamics of succession in family businesses.

Family-internal succession and executives

Drawing on the Resource-Based View (RBV; Barney, 1991), we argue that planned family-internal succession is a strategic action designed to preserve key firm-specific resources—such as human capital, tacit knowledge, and SEW—which are critical to maintaining long-term organizational stability and legacy. In family firms planning family-internal succession, there exists a critical period of stability preceding a succession event, ideally aimed at ensuring a seamless transition for the succeeding family-internal generation. This stability is pivotal for maintaining the continuity and smooth functioning of the business operations prior, during and after the delicate phase of leadership change. These successions often entail the continuation of work by the next generation, fostering familial closeness with employees (Schell et al., 2018). In many instances, successors in family businesses have cultivated enduring relationships with long-serving employees by growing up alongside them and, in some cases, even considering them as extended family. This intimate bond has significant implications for the structural dynamics within executive teams.

Family-internal successors may exhibit hesitancy toward instigating immediate changes within management teams, preferring to retain long-serving employees. The familial ties and shared history between the owner family and employees may create a reluctance to disrupt existing team structures. Moreover, successors can also benefit from established managers within the company as invaluable repositories of knowledge and orientation during their initial years of leadership (Cabrera-Suárez, 2005; Daspit et al., 2016). Therefore, incumbents have strong incentives to retain these experienced individuals as mentors. Non-family executives themselves may perceive the success of the succession process and the continuity of the company as personal obligations (Pearson and Marler, 2010). Consequently, family firms undergoing family-internal successions should witness minimal turnover within their executive teams before succession events. These arguments lead us to the following hypothesis

H1a: Family firms with a planned family-internal succession will exhibit lower executive turnover in the pre-succession phase than family firms without a planned succession event.

Following succession events, family-internal successors prioritize maintaining existing team structures, benefiting from the tacit knowledge and experience of non-family executives (Weimann et al., 2020). Non-family executives are regarded as an integral part of the succession process, fostering business continuity and providing invaluable insights. Also, after the succession event, the strategic intent to maintain continuity persists. Although some adjustments in the executive team are inevitable during the transition, the newly appointed family leader, having been groomed internally, is more likely to seamlessly integrate into the firm’s existing culture, and maintain established relationships (Jayantilal et al., 2023). This continuity ensures that critical tacit knowledge is retained, and that the organization’s SEW is safeguarded. Consequently, the post-succession phase is characterized by reduced disruptions and a smoother transition, leading to a lower rate of executive turnover compared to firms without succession events. In essence, the continuity provided by an internal successor not only minimizes the immediate impact of leadership change but also contributes to the long-term stability of the firm’s executive team.

Within the RBV framework in family businesses, retaining key personnel after succession is viewed as a strategic action, especially by successors from within the family. This view perceives such personnel as critical resources that contribute to sustaining competitive advantages and ensuring firm stability. Recognizing the disruptive nature of succession events, family firms may opt to retain their specialized human capital to ensure operational continuity and preserve institutional knowledge (Chiang et al., 2022). Rather than seeking immediate changes within the executive team, successors build upon the existing personnel framework, leveraging the unique strengths, and expertise of long-serving executives. This approach not only mitigates the risks associated with turnover but also reinforces the successors’ commitment to preserving the firms’ legacies and sustaining their competitive advantage. These arguments lead us to the following hypothesis:

H1b: Family firms with a planned family-internal succession will experience lower executive turnover in the post-succession phase than family firms without a planned succession event.

Family-external succession and executives

In contrast to family-internal succession, family-external succession signals a potential departure from entrenched family values and legacy. Such a shift can diminish non-family executives’ sense of belonging and organizational identification, thereby increasing uncertainty about their future within the firm. Drawing on SEW and insights on founder influence, research indicates that when family influence is diluted—even if only partially—the resulting disruption can lead to higher turnover among key executives (Campopiano et al., 2020; Tabor et al., 2018; Vardaman et al., 2018), which can have, in turn, significant impact on firm performance (Shen and Cannella, 2002).

Family-external successions introduce a paradigm shift within family firms, often leading to significant alterations in the composition and strategy of executive teams. However, the mere anticipation of giving the firm out of family hands can create apprehension among existing executives. This uncertainty undermines their organizational identification and can result in increased turnover relative to firms without succession plans. Literature further indicates that such preemptive instability is particularly pronounced when the transition challenges the firm’s longstanding family identity (Minichilli et al., 2014). Moreover, the anticipation of a new leadership style and the potential for strategic redirection under an external successor might lead to a cautious approach toward executive team changes. Existing executives, aware of the forthcoming transition, might reassess their fit with the anticipated new organizational direction, increasing turnover intentions before the succession event. Thus, we hypothesize:

H2a: Family firms with a planned family-external succession will exhibit higher executive turnover in the pre-succession phase compared to family firms without a planned succession event.

Following a family-external succession, the executive team’s composition is expected to shift significantly. New leadership, lacking a shared history with the firm, may not value the established traditions, opting to implement their strategic vision and management style instead (Schepker et al., 2017). This transition typically involves hiring new executives that align with the successors’ strategic objectives and that possess the requisite skills for firms’ intended strategic renewal. These new executives, unencumbered by previous organizational ties, can support the new owner-managers’ legitimacy, and facilitate the adoption of new operational paradigms (Karaevli, 2007). In the post-succession phase, the disruptive impact of a leadership change is often amplified. When a firm opts for a family-external successor, the absence of longstanding familial relationships can undermine non-family executives’ organizational identification, increasing turnover intentions. Moreover, the erosion of family identity following an external succession exacerbates uncertainty among top managers, further destabilizing the leadership team (Vardaman et al., 2018). Naldi et al. (2013) indicate that decisions aimed at preserving SEW, such as maintaining family leadership and legacy, can negatively impact firm performance under formal regulatory pressures, potentially contributing to instability within the executive team. Additionally, when the new strategic vision diverges from the firm’s traditional values, non-family executives may feel alienated, further intensifying turnover (Tabor et al., 2018).

Long-standing members of the executive team, identifying with the incumbent’s era, may choose to retire, or seek new opportunities, perceiving the succession as a natural conclusion to their tenure (Hayes et al., 2005). This turnover provides the family-external successors to sculpt executive teams that resonates with their strategic vision, emphasizing technical expertise and industry-specific knowledge and historical organizational networks. Collectively, this suggest that the post-succession phase in family firms undergoing family-external succession is marked by higher executive turnover, driven by disrupted relationships, diminished family identity, and the loss of key non-financial assets.

These arguments lead us to the following hypothesis:

H2b: Family firms with a planned family-external succession will exhibit higher executive turnover in the post-succession phase compared to family firms without a planned succession event.

Family-internal versus external succession and executives

The stability of the executive teams before succession events in firms with family-internal successions is a reflection of the firms’ commitment to preserving SEW. Lu et al. (2021) highlight how family CEOs’ traditionality positively influences the selection of family members as successors, a decision that is closely tied to the preservation of Kalm and Gomez-Mejia (2016), who elucidate how family firms’ decision-making and succession planning are influenced by the desire to preserve non-financial aspects that hold emotional value for the family, further highlight this preference for family successors. Basco and Calabrò (2017) show that the importance placed on family standing attributes over managerial competence, moderated by the number of family members working in the firm, underscores the mechanism of SEW preservation in the context of successor selection.

Given this backdrop, the period before the succession event is marked by fewer changes within the executive team, as existing executives and the incumbent owner-manager aim to preserve the firm’s operational integrity and uphold established traditions and values. This leads to the following hypothesis:

H3a: Family firms with a planned family-internal succession will exhibit lower executive turnover in the pre-succession phase compared to family firms with a planned family-external succession.

Following family-internal successions, the continuity of family leadership further contributes to the stability of the executive team’s composition. Contreras-Lozano et al. (2022) suggest that directors’ attitudes toward succession, significantly related to the socioemotional aspect of the family business, affect executive team dynamics, emphasizing the role of SEW in these processes. Hauck and Prugl’s (2015) investigation of innovation activities during family-internal succession reveals that socioemotional factors can both facilitate and hinder strategic decisions during succession phases, reflecting the complex impact of SEW on executive team stability.

This continuity starkly contrasts with the disruptive nature of external successions, where the lack of shared history and SEW preservation may lead to broader changes in executive teams as the new leaders seek to imprint their strategic visions. Thus, the following hypothesis is proposed:

H3b: Family firms with a planned family-internal succession will experience significantly lower executive turnover in the post-succession phase than family firms with a planned family-external succession.

Data and methods

Sample

For our analysis, we use the “Linked-Employer-Employee-Data of the IAB” (LIAB) provided by the Institute for Employment Research of the Federal Employment Agency in Germany (IAB). The dataset combines German official social security insurance data on individuals with establishment data from the IAB-Establishment Panel Survey (Ruf et al., 2021a). 1 The individual data are taken from the Integrated Employment Biographies dataset (IEB). The IEB merges official information on employment subject to social security, marginal employment, unemployment and social benefits, registered jobseekers, and participants in employment or training programs. All employees and trainees subject to social security are covered by the data, whereas certain types of civil servants (“Beamte”), self-employed, and family workers are not considered. In total, more than 80 percent of all employed persons in Germany are included in the IEB.

The IAB Establishment Panel is a representative large-scale annual establishment survey that covers about 16,000 establishments every year, beginning in 1993 in West Germany and extended in 1996 to the former East Germany. The IAB Establishment Panel is the starting point for drawing the LIAB’s personal data. First, establishments are selected from the IAB Establishment Panel that have a valid survey in the respective year (1993–2019). Then, all persons that were employed in one of these establishments on June 30 of the respective survey year are drawn from the IEB. The LIAB thus includes survey data on all establishments surveyed in the IAB Establishment Panel between 1993 and 2019. Overall, the LIAB contains 370,252 observations of 76,103 establishments and 59,198,740 observations of 13,077,307 individuals working in the observed firms at the date of surveying.

We restrict our sample to those firms for which we have information on family business status, business succession and executive employees. The 2012 survey of the IAB establishment panel contained several additional questions concerning family influence in the firm and a planned family business succession in the foreseeable future. The classification as a family business depends on a self-assessment of the firms. Based on these questions, we excluded all firms that are not family businesses. For those businesses with a planned succession, we investigate the period of 3 years before to 3 years after the planned succession for each observation. Thus, firms with a succession year later than 2016 are excluded to avoid probable biases in the data, resulting in an observation period for planned succession events from 2012 to 2016 (corresponding data encompasses the timeframe 2009–2019). Family firms without a planned succession were kept as a benchmark group to control for general hiring and dismissal effects unrelated to business successions.

Moreover, we solely concentrate on firms’ executives. We identify executives by the “German Classification of Occupations 2010” (Bundesagentur für Arbeit, 2010) as workers in managing and supervising jobs with complex specialist respectively highly complex activities. 2 Furthermore, we dropped all establishments with less than two executives and five employees because they are unlikely to have an executive team consisting of multiple members.

Following these inclusion criteria, we ended up with a sample of 70,421 executives in 3293 establishments. Of the 3293 establishments, 245 stated to carry out a business succession between 2012 and 2016. This includes 163 planned successions within the owner families and 81 family-external successions. This is in line with statistical estimates of the overall distribution of family-external and family-internal business successions in Germany over the past years. (Kay et al., 2018; Kay and Suprinovič, 2013). All other observations contain family firms without planned succession events, which serve as a control group.

Probit regression model

We investigate the probability of recruitments and turnover of executives in firms with family-internal, family-external, or no succession by conducting a multivariate regression analysis. In the case of a succession event, we further investigate differences before and after succession (including the succession year). In our regression model, the level of observation is the executive. Hence, we conduct two separate probit regressions for the events of interest, which are turnover on the one hand, and hires or promotions on the other hand. Both events are compared with executives that stay in the establishment over the whole period of observation as base category (“stayers”). We estimate separate regressions instead of a pooled multinominal model because of different relevant covariates. For example, years in current job are not relevant for hires or promotions while they probably are in the case of dismissals. Due to the construction of the IAB Establishment Panel survey data, a dismissal drops from the sample whereas hires are added to the sample when joining the firm.

In light of the binary nature of the endogenous variable we use a probit regression model (Wooldridge, 2010, p. 665):

with P(.) as probability of state y = 1 depending on the vector of covariates x and Φ as a normal distribution function. The model estimates parameter vectors β for recruitments/promotions respectively turnovers using stayers as base category. Instead of the estimated parameters, we use marginal effects, which are calculated as follows:

where xk is the particular variable k of the covariates x, βk is the related parameter and φ as the density function.

Our analysis is especially interested in employment decisions depending on the event and type of business successions. Therefore, we create a variable that summarizes the timing of recruitments and dismissals (before or after succession) and the type of succession (family-internal or family-external). All other covariates (see 3.3.2) are interacted with this variable, resulting in parameters that are estimated separately for each of its expressions in the three probit estimates. This allows to calculate different outcomes for both the timing of employment changes and the type of succession. Then, average marginal effects according to equation (2) are calculated from the regression outcome.

Variables

Dependent variables

Our dependent variables are binary variables for the respective events of interest, which are turnover on the one hand, and hires and promotions on the other hand. First, executives are assigned as turnover if they leave the firm during the observed period. Second, executives are assigned as hires if they join the firm in the same period, or as promotions when they are already employed in the firm and become executives in that period. In a first step, we conduct a regression with a dummy that jointly identifies hires and promotions as new executives. In a second step, an additional probit model examines hires and promotions separately to indicate differences among both groups of new executives.

Independent variables

In our model, we include a vector of covariates containing several variables that might influence the probability of recruitments and dismissals.

First, we control for executives’ wages, as high labor costs could influence hiring and dismissal decisions and new family-external owners may try to reduce labor costs by replacing executives. Conversely, there could also be a considerable need for human capital after the handover of the business, resulting in an increase of salaries because of new and highly qualified managers. Therefore, we use the daily income (ln. daily income) as a covariate in the probit regression. The LIAB dataset contains the daily remuneration of the respective employees up to the maximum rate of social security contributions. Due to the high level of compensation, this limit applies in particular to executives. Therefore, we impute the censored values for compensation by estimating Mincer-type models of executive pay (cf. Cahuc et al., 2014, p. 215ff.) and replace the censored values by the values estimated in the model.

Employees’ age can also influence executive turnover during a business succession. Family businesses tend to enter into long-term employment relationships with their employees, which could lead to a rather old firm’s management team at the time of succession. If ties to the previous owning families are cut during the succession process, the reason for long-term employment may also no longer exist, and we will observe a larger labor turnover where younger executives replace older ones. We use a dummy variable indicating whether the executive is older than 55 years (Age: older than 55 years) to control for a close retirement. Additionally, a corresponding dummy for executives younger than 40 years is included (Age: younger than 40 years). We use dummies instead of a continuous age variable to catch the particular effects on older and younger executives

Moreover, we control for working experience as an indicator for potentially higher productivity by using two additional measures. The number of years in employment (Ln. years in employment) reflects the total working experience, whereas the number of years in the current job (Ln. years in current job) reflects the experience related to the specific position. The first variable is closely related to the age of the executives and catches simple linear age effects. The latter variable is not used in the regression of hirings or promotions because the new executives have not worked in this specific position so far.

Furthermore, we control for executives’ formal education by a variable that equals one if a person holds at least a Bachelor degree from a university (University degree). Moreover, we control for the gender of executives (Female = 1). Finally, the size of the executive team (Ln. number of executives), the firm size (Ln. number of employees), and ten industry dummies are used as additional covariates.

Since the value of the endogenous variable does not change in our data, and most covariates are constant (e.g. gender or degree) or increase by one with each year (e.g. experience or age), we forgo to use a panel estimator. Further, a pooled regression increases the risk of collinearity among the covariates as they are rather similar for one individual. Instead, we chose one observation in the panel for each particular executive. Therefore, we use the last observation year for dismissed executives, and the first observation year for newly hires managers and a random observation within the observation period for those who stay in a firm. Using averaged data would result in a loss of variation and thus a likely greater difficulty in estimating the model. Because of the imputation of wage data described above, we use only full-time employees in the regression.

Results

Descriptive statistics

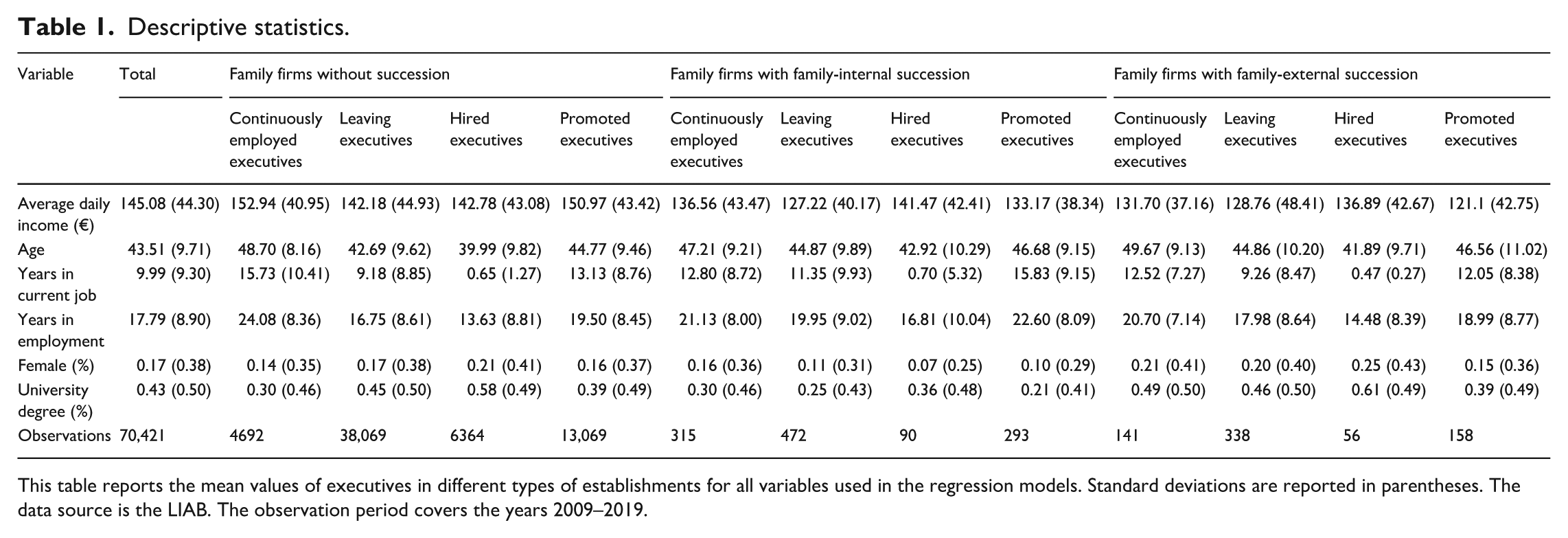

Table 1 contains the individual descriptive statistics of the executives included in our sample. Furthermore, it compares executives of firms without succession with executives of firms with family-internal or family-external succession. The three types are furthermore split up into executives that stay in the establishments, those that leave the firm, and those that are newly hired or promoted, respectively.

Descriptive statistics.

This table reports the mean values of executives in different types of establishments for all variables used in the regression models. Standard deviations are reported in parentheses. The data source is the LIAB. The observation period covers the years 2009–2019.

Descriptive statistics show some remarkable differences across the different firm types and executive subgroups. Compared to establishments without a business succession, firms with a succession pay on average lower salaries across almost all subgroups. Companies with family-external successions show the lowest average values in almost all subgroups. The average executive in our sample is around 43.5 years old, has nearly 10 years of employment experience in the current job and almost 18 years of total employment experience. In all types of firms, the age of dismissed executives is on average larger than the age of hired but lower than the age of promoted executives. This indicates that most executives do not leave their companies for retirement reasons but to start a job at other companies. Furthermore, dismissed executives have typically less years of experience than promoted ones but more than newly hired managerial staff, which indicates that a replacement is not necessarily connected with a generational change. Probably there is a need for experienced executives that know the firm structures and accompany the transformation process. Although some of the firm’s management changes, a core of experienced managers remains in the company. However, hired executives usually have a higher formal education in terms of a university degree compared to managers that leave the firm, are promoted internally, or stay in the company. Finally, only 17% of all executives in our sample are female.

Multivariate results

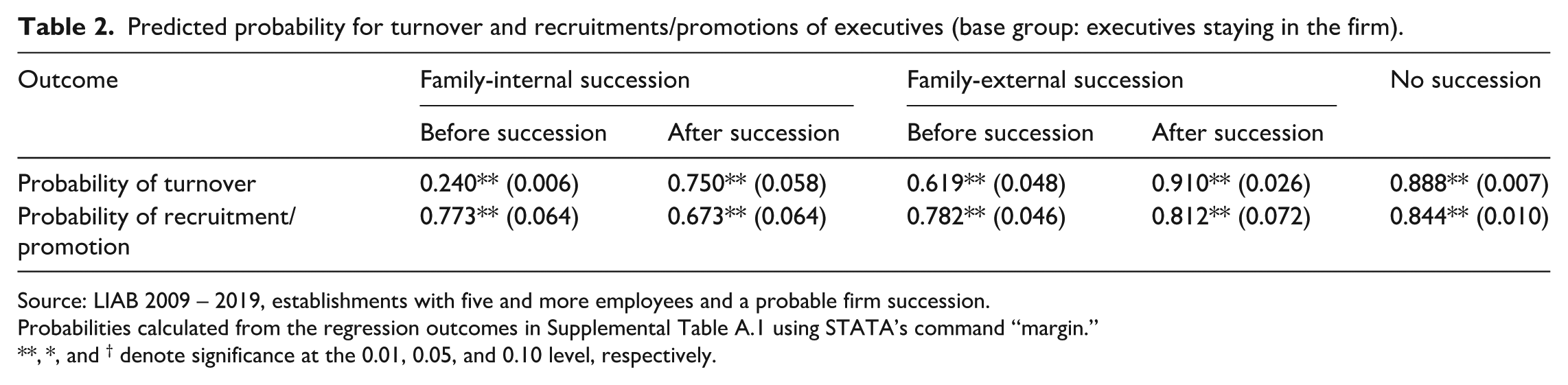

The key results of the probit regressions are presented in Tables 2 to 8. We derived the predicted probabilities and average marginal effects from the outcome of the multivariate estimations. 3 Since it is not possible to interpret the estimated parameters of a probit regression model directly, these are presented in the appendix (please see Supplemental Table A.1). First, Table 2 contains the predicted probabilities of recruitments and turnover for family-internal and family-external successions both before and after the succession events, and for companies without a succession, respectively.

Predicted probability for turnover and recruitments/promotions of executives (base group: executives staying in the firm).

Source: LIAB 2009 – 2019, establishments with five and more employees and a probable firm succession.

Probabilities calculated from the regression outcomes in Supplemental Table A.1 using STATA’s command “margin.”

**, *, and † denote significance at the 0.01, 0.05, and 0.10 level, respectively.

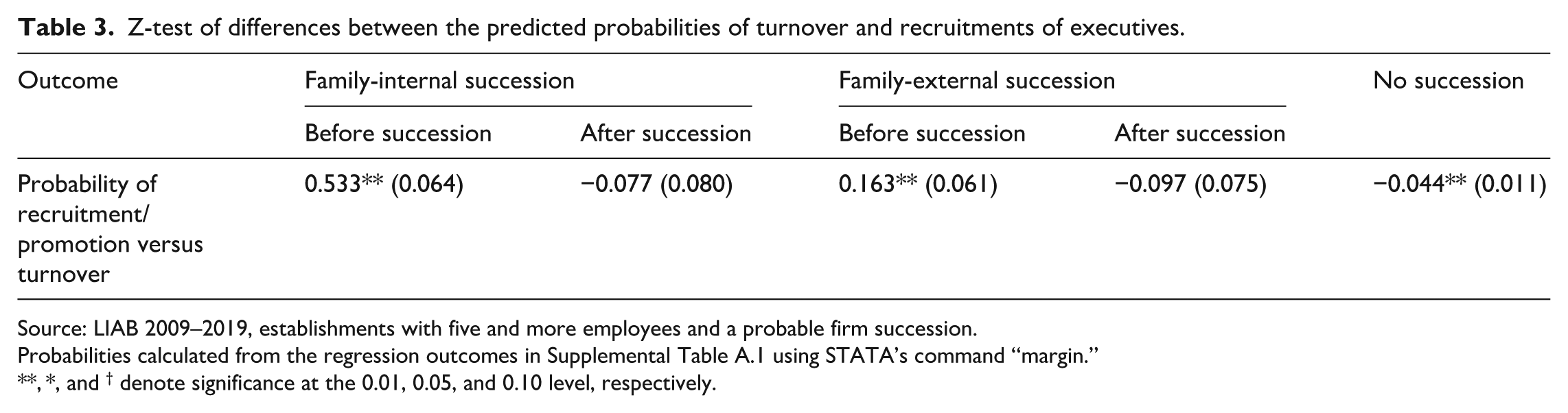

The subsequent tables report whether the observed differences between the different types of succession or time periods are statistically significant. Table 3 reports the results of z-tests concerning the differences between turnover and recruitments before and after the date of succession. For both types of succession, the probabilities of turnover are significantly lower than the probabilities of hirings or promotions before a succession but not afterward. However, in firms with family-internal successions turnover is less likely before successions by 53.3% compared to 16.3% for family-external succession arrangements. In contrast, firms without succession show a small but statistically significantly larger probability for turnover.

Z-test of differences between the predicted probabilities of turnover and recruitments of executives.

Source: LIAB 2009–2019, establishments with five and more employees and a probable firm succession.

Probabilities calculated from the regression outcomes in Supplemental Table A.1 using STATA’s command “margin.”

**, *, and † denote significance at the 0.01, 0.05, and 0.10 level, respectively.

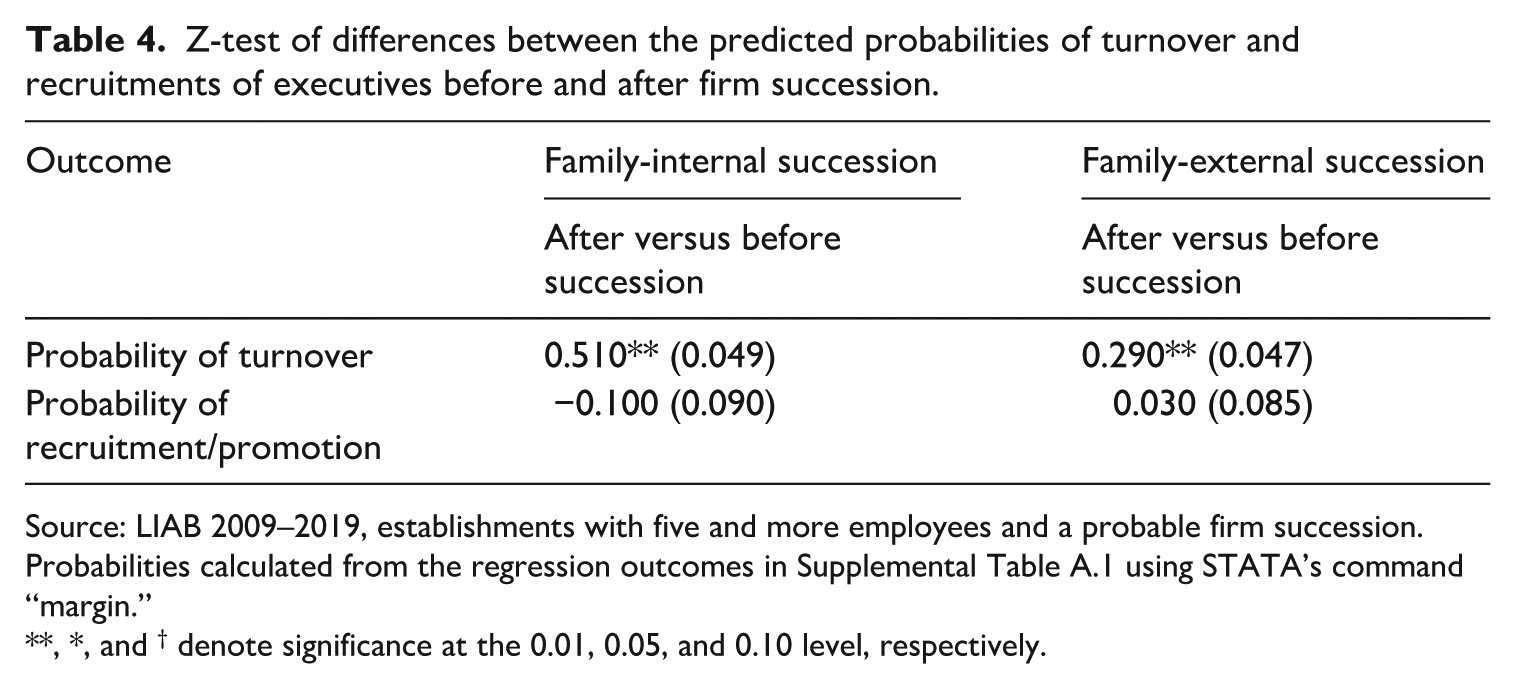

Table 4 examines the statistical significance between the periods before and after the handover for the two succession types. For both types, family-internal and family-external successions, probabilities of turnover are significantly smaller before than after succession. The decline is much larger in the first type of firms compared to the latter (51% vs 29% points). In contrast, there is no significant difference for recruitments and promotions between the two periods.

Z-test of differences between the predicted probabilities of turnover and recruitments of executives before and after firm succession.

Source: LIAB 2009–2019, establishments with five and more employees and a probable firm succession.

Probabilities calculated from the regression outcomes in Supplemental Table A.1 using STATA’s command “margin.”

**, *, and † denote significance at the 0.01, 0.05, and 0.10 level, respectively.

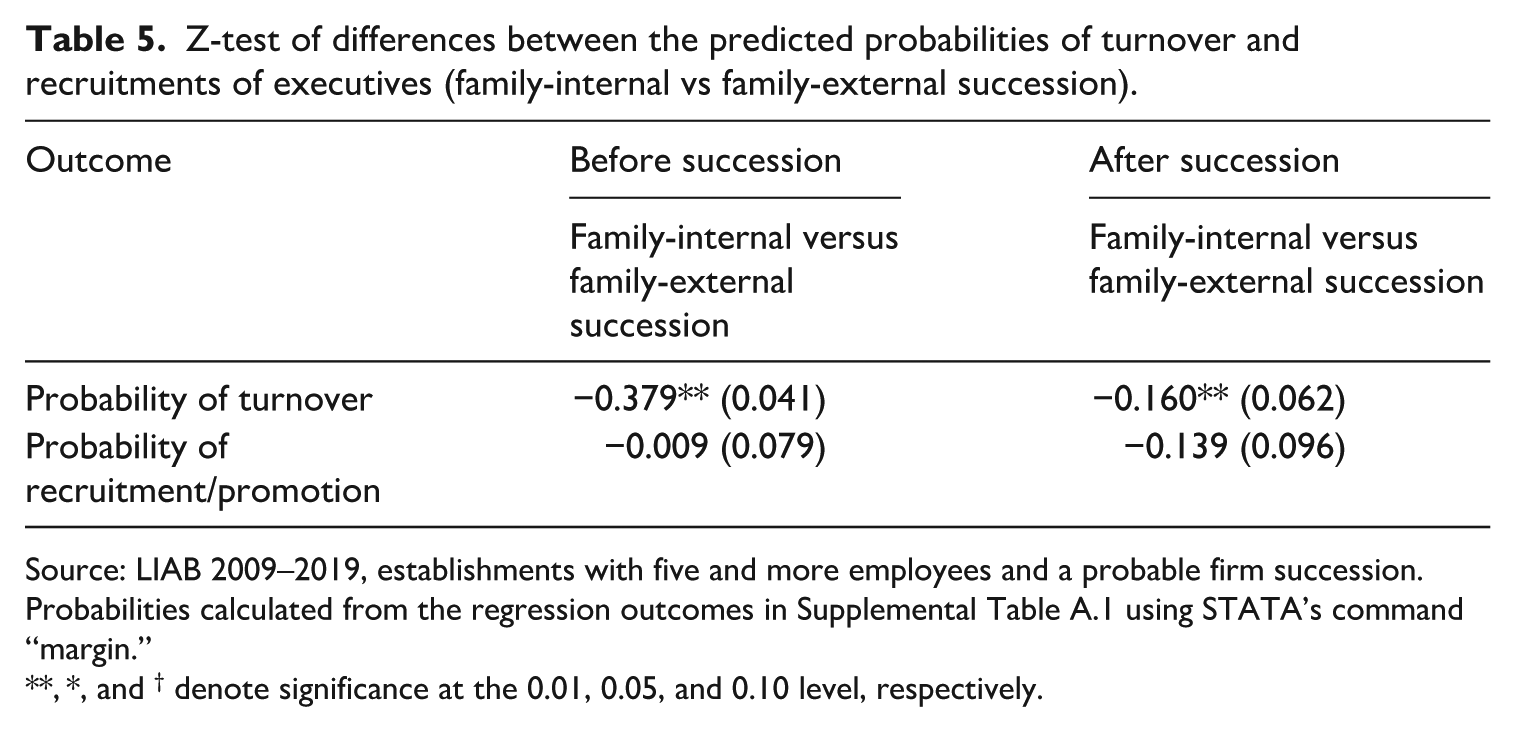

Table 5 investigates differences in the predicted probabilities between firms with family-internal versus family-external successions, dependent on the observation period. The probabilities of turnover is significantly lower for firms with family-internal successions than for firms with family-external successions both before and after the handover (37.9% and 16.0% points, respectively). On the other hand, the probabilities of recruitments and promotions do not differ significantly before or after the succession. This result supports hypothesis 3a and 3b, as all the values determined are negative. Although only the results for layoffs are significant, a clear picture emerges that the fluctuation around the time of succession is lower for family-internal handovers.

Z-test of differences between the predicted probabilities of turnover and recruitments of executives (family-internal vs family-external succession).

Source: LIAB 2009–2019, establishments with five and more employees and a probable firm succession.

Probabilities calculated from the regression outcomes in Supplemental Table A.1 using STATA’s command “margin.”

**, *, and † denote significance at the 0.01, 0.05, and 0.10 level, respectively.

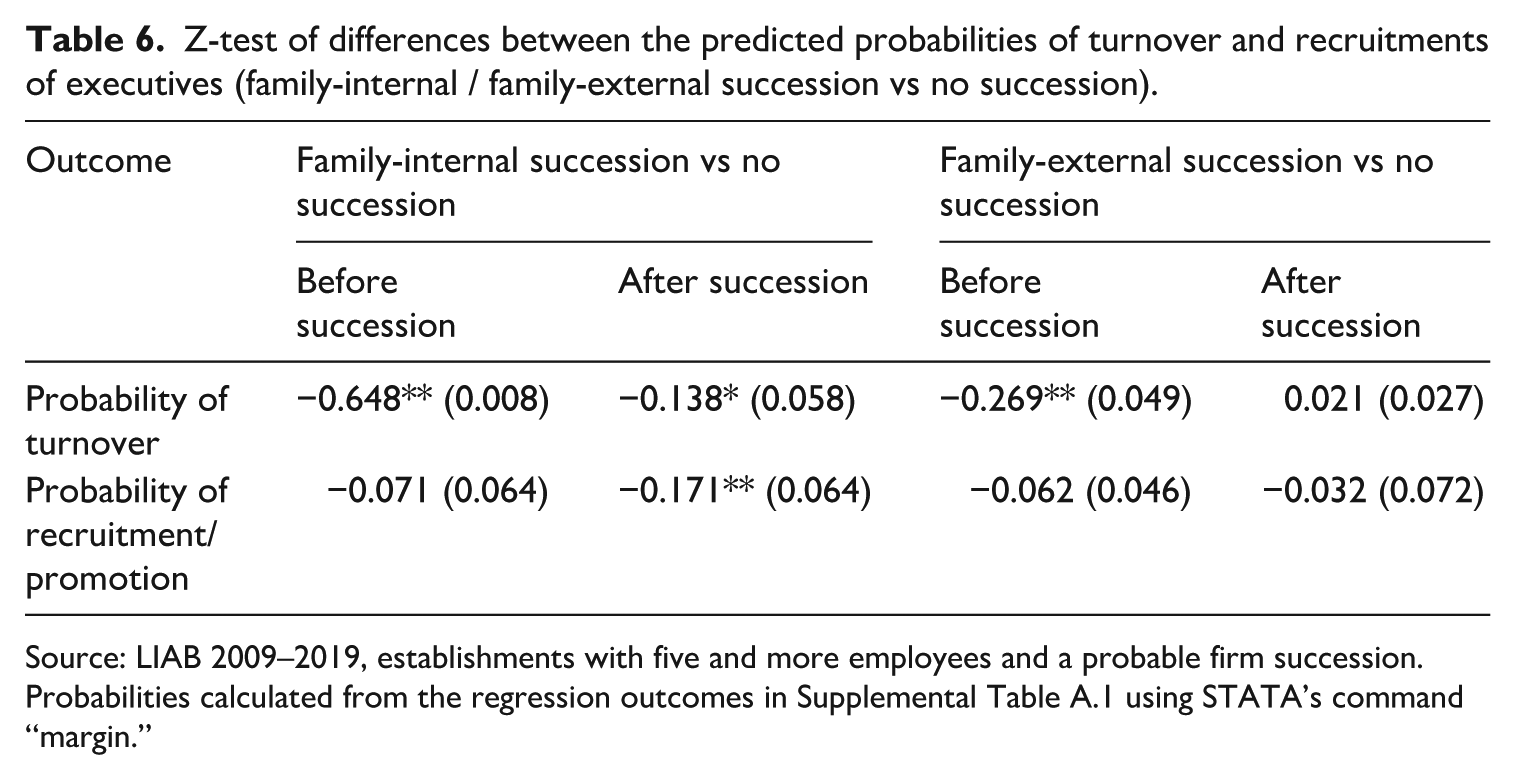

Finally, we compare the probabilities of recruitments and turnover in family firms with succession events to family firms without a succession (Table 6). Both succession types show significantly lower probabilities of turnover before the succession events of 64.8 and 26.9% points, respectively. After the handover, firms with a family-internal succession show also both a lower probability of turnover and hirings or promotions of executives compared to firms without succession. These results indicate that there seems to be less executive turnover in firms around family-internal successions. However, we do not find higher dismissal or hiring rates in firms with family-external successions after the succession compared to firms without succession. The values in the columns for intra-family succession confirm the assumptions of hypotheses 1a and 1b. Although the difference in the probability of hiring new employees or promoting existing employees before succession is not statistically reliable, the sign is in the expected direction. Hypotheses 2a and 2b for external succession are less supported. We can describe a lower labor turnover only in the period before the handover, which is also only statistically relevant for turnover. After the handover, no higher employment activity can be described.

Z-test of differences between the predicted probabilities of turnover and recruitments of executives (family-internal / family-external succession vs no succession).

Source: LIAB 2009–2019, establishments with five and more employees and a probable firm succession.

Probabilities calculated from the regression outcomes in Supplemental Table A.1 using STATA’s command “margin.”

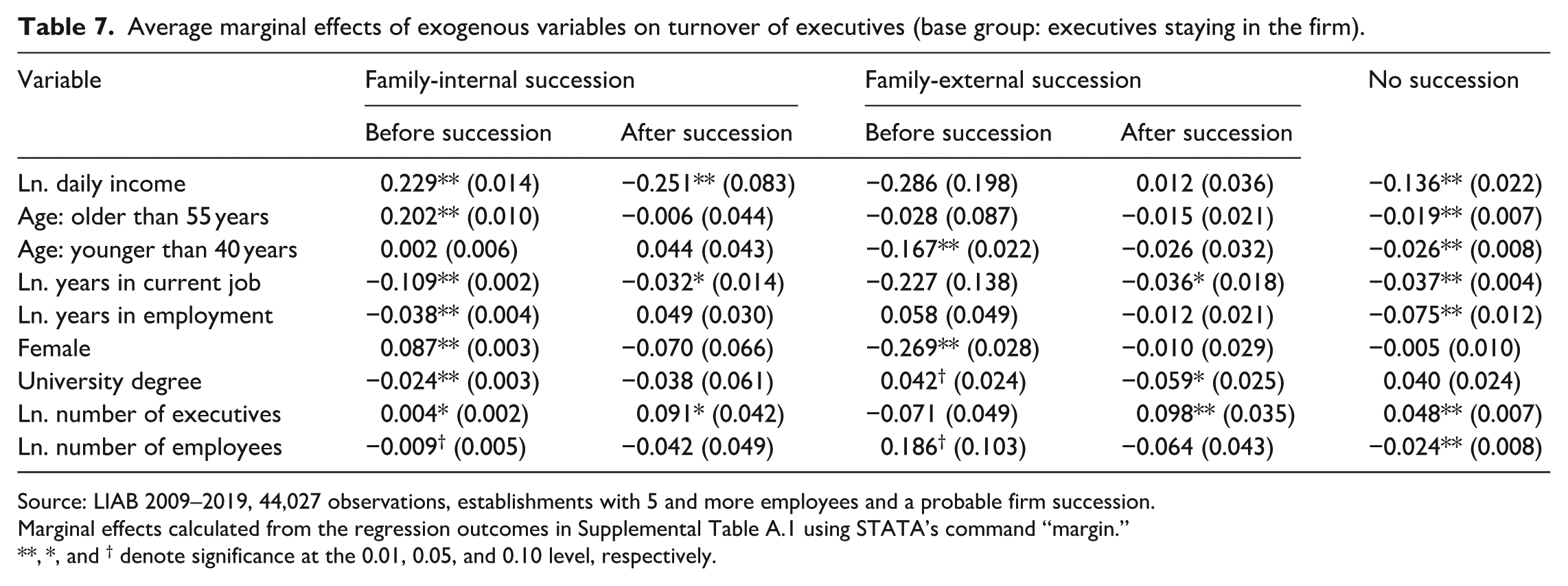

Next to the predicted probabilities, we calculated the average marginal effects of the exogenous variables on recruitments and turnover (Tables 7 and 8). Table 7 contains the effects on turnover. In firms without a succession process, all presented variables with the exception of the shares of female executives and executives with a university degree report a statistically significant impact on the probability of turnover. Higher income, executives older than 55 or younger than 40, a longer working experience in establishment, and the number of employed employees in the establishment decrease the probability of leaving the firm. On the other hand, the firm’s executive team size increases the probability to move out of the entity. However, we cannot indicate from the data if those persons were leaving voluntarily or involuntarily. For both types of successions, we also find some statistically significant effects on the personal level. In firms with a family-internal succession, executives older than 55 years and with a higher daily income show a higher probability to leave the firm before the succession event. These findings contradict the results for firms without a succession event, where a higher age and higher remuneration are related to lower probabilities of turnover. Moreover, with the exemption of firms before an external succession, a higher number of executives increases the probabilities for turnover before successions, whereas a higher number of total employees has mainly the opposite effect. In firms with external successions, younger executives are less likely to leave the company before the succession events. Additionally, like in firms without succession, the number of years in the current job decrease the probability to leave the firms. In the case of general employment experience, this is only true before an internal succession. While there is a significant 8.7% larger probability for female executives to leave a firm before family-internal succession, the corresponding value before a family-external hand over indicates a 26.9% lower value. The opposite occurs for executives with a university degree. Here the estimates show a negative probability before the change of ownership within the family and more frequent turnover in family-external solutions.

Average marginal effects of exogenous variables on turnover of executives (base group: executives staying in the firm).

Source: LIAB 2009–2019, 44,027 observations, establishments with 5 and more employees and a probable firm succession.

Marginal effects calculated from the regression outcomes in Supplemental Table A.1 using STATA’s command “margin.”

**, *, and † denote significance at the 0.01, 0.05, and 0.10 level, respectively.

Average marginal effects of exogenous variables on recruitments/promotions of executives (base group: executives staying in the firm).

Source: LIAB 2009–2019, 31,542 observations, establishments with 5 and more employees and a probable firm succession.

Marginal effects calculated from the regression outcomes in Supplemental Table A.1 using STATA’s command “margin.”

**, *, and † denote significance at the 0.01, 0.05, and 0.10 level, respectively.

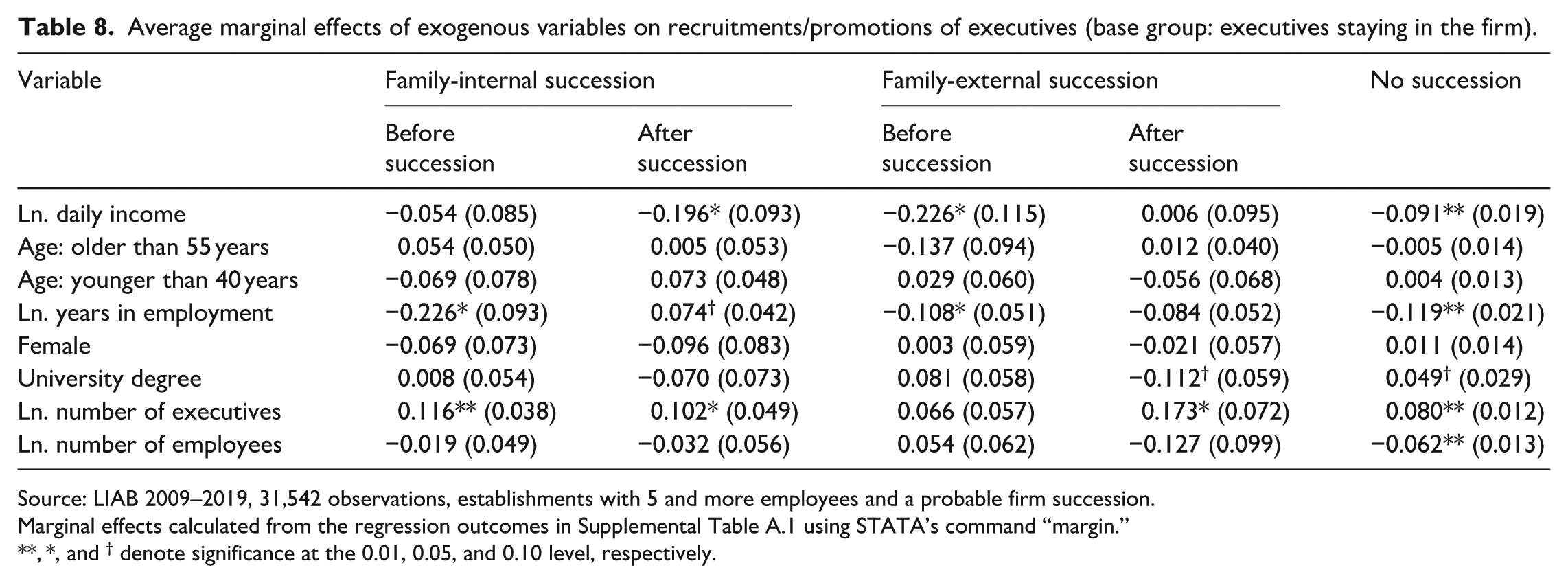

Table 8 contains the corresponding results for the probabilities of becoming a new executive in the firm. As the years in the current job begin with the hiring or promotion event, we exclude this variable from the regression. Looking at general work experience, we find significant negative effects on hirings or promotions for family firms without a succession and for family firms with a succession before but not after the succession event; that is, before the handover, the firms hire or promote executives with lower work experience. Being female or holding a university degree have no major significant influence on the probability of recruitments. Moreover, the results show that the salaries of new executives are comparably lower in firms with family-internal succession after the succession, and in firms with family-external succession before the succession. The negative effect for firms without a succession suggests that firms replace their dismissed executives by less experienced and thus less costly new ones. Surprisingly, unlike in the case of turnover, we do not find significant effects for the hiring of young respectively older executives. Moreover, the number of executives in the establishment seem to be a positive indicator for job turnover.

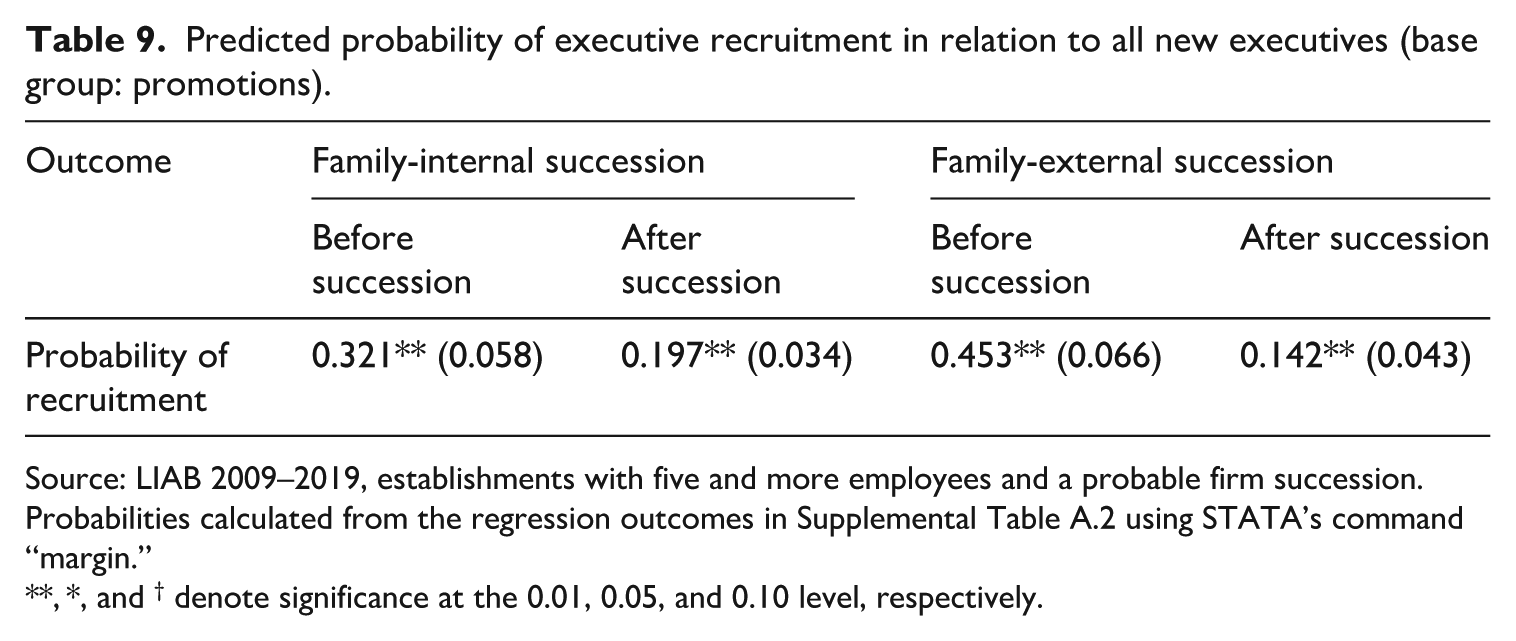

To examine the differences between hires and promotions, we conducted further estimations with a subsample including only promotions and hires in firms with the intention of transferring a business. The estimates contain the same covariates as before. However, the dependent variable now takes the value one when a new executive is hired from outside and zero when a new executive is promoted from inside the firm. Thus, the estimated parameters describe differences between promotions and hires. In total, this subsample includes nearly 600 new executives. Supplemental Table A.2 in the appendix contains the parameters estimated in this way. In firms with family-internal succession, about one-third of new managers are recruited externally, whereas two-thirds are promoted internally before the transfer of the firm (Table 9). The figure drops to below 20% after the business handover. In companies with a family-external succession, around 45% of new executives are hired before the handover and less than 15% after the handover.

Predicted probability of executive recruitment in relation to all new executives (base group: promotions).

Source: LIAB 2009–2019, establishments with five and more employees and a probable firm succession.

Probabilities calculated from the regression outcomes in Supplemental Table A.2 using STATA’s command “margin.”

**, *, and † denote significance at the 0.01, 0.05, and 0.10 level, respectively.

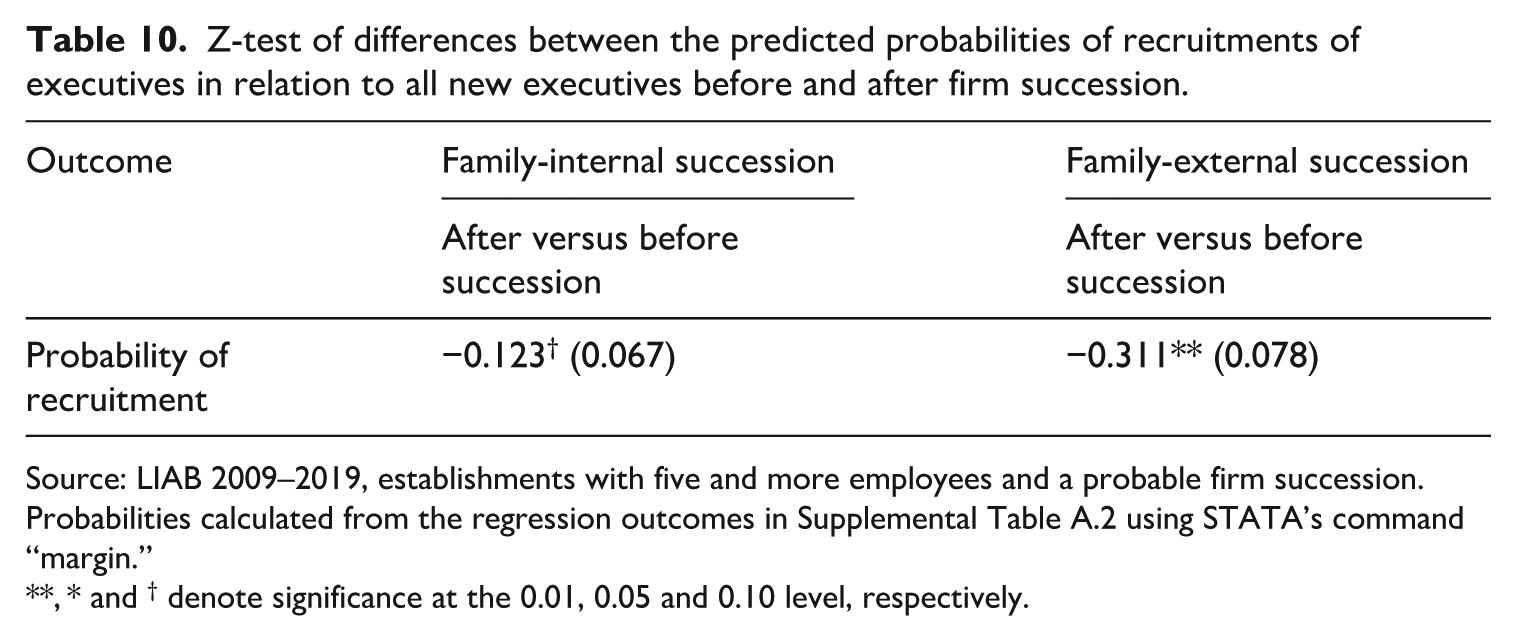

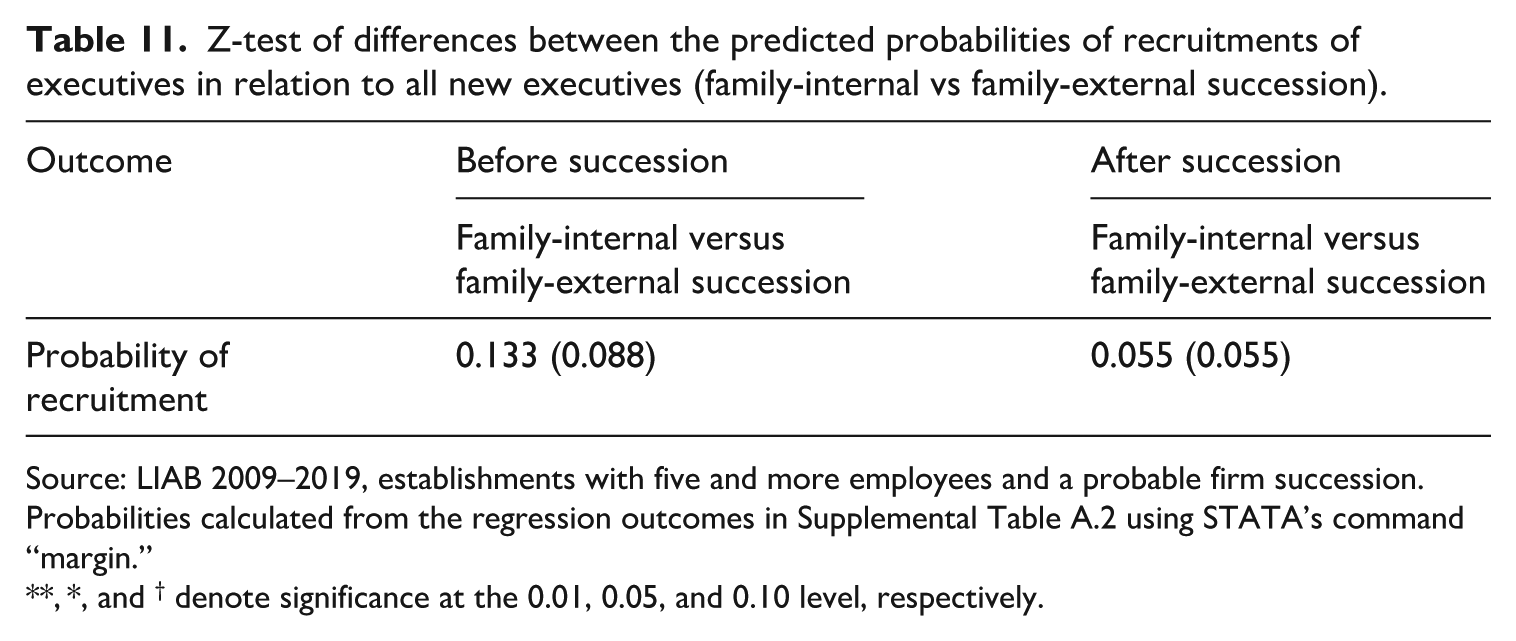

The results indicate that internal promotions are more important than new hires. This importance increases significantly after the transfer of the business. The differences between the two periods are significant for both types of succession (Table 10), whereas the differences between firms with family-internal and family-external succession are not significant (Table 11).

Z-test of differences between the predicted probabilities of recruitments of executives in relation to all new executives before and after firm succession.

Source: LIAB 2009–2019, establishments with five and more employees and a probable firm succession.

Probabilities calculated from the regression outcomes in Supplemental Table A.2 using STATA’s command “margin.”

**, * and † denote significance at the 0.01, 0.05 and 0.10 level, respectively.

Z-test of differences between the predicted probabilities of recruitments of executives in relation to all new executives (family-internal vs family-external succession).

Source: LIAB 2009–2019, establishments with five and more employees and a probable firm succession.

Probabilities calculated from the regression outcomes in Supplemental Table A.2 using STATA’s command “margin.”

**, *, and † denote significance at the 0.01, 0.05, and 0.10 level, respectively.

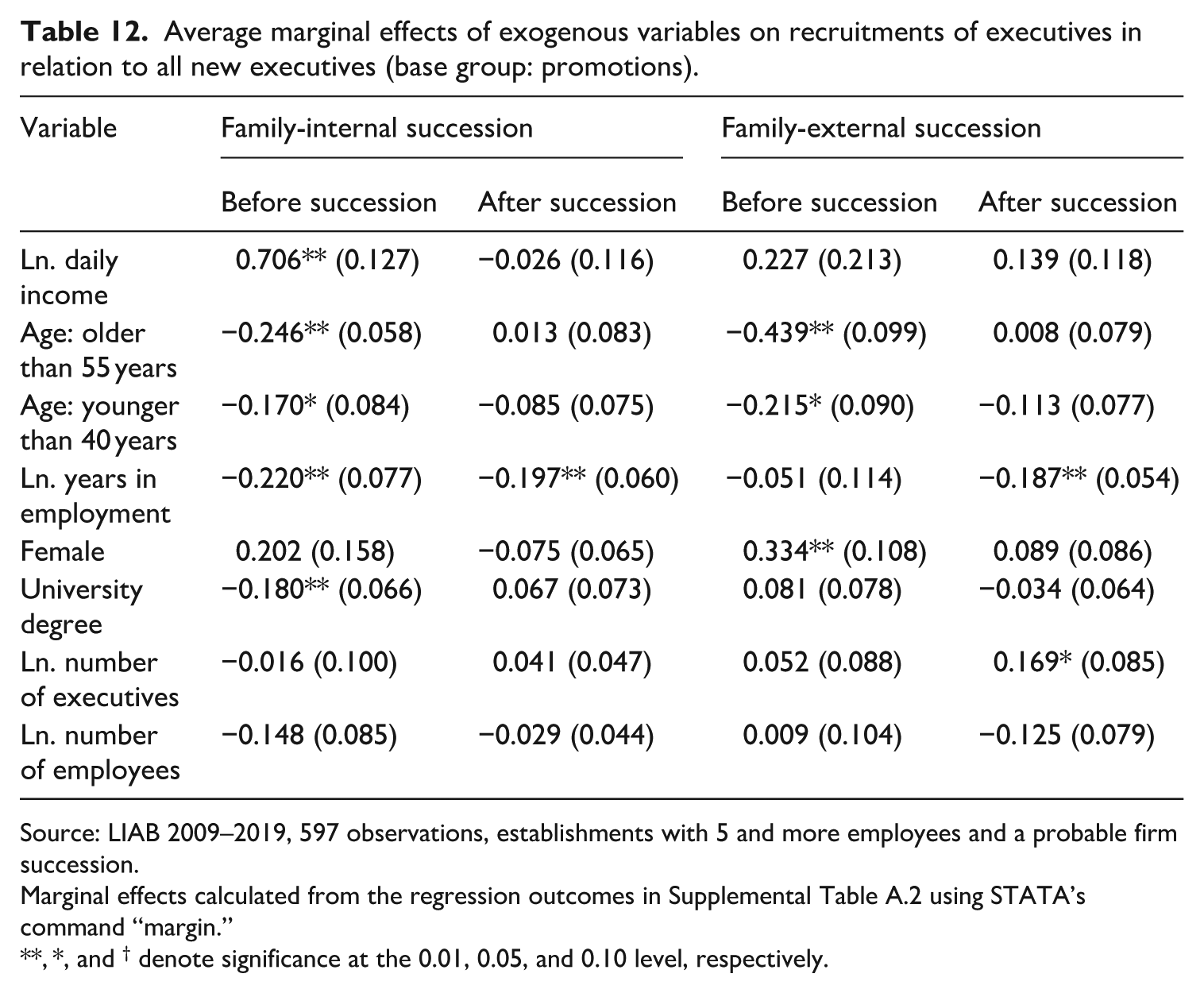

Table 12 contains the corresponding marginal effects. Prior to the business transfer, newly hired executives are more likely to be in the age group between 40 and 55 years than belonging to older or younger age groups. Furthermore, hired executives have in general less work experience than promoted executives. Specific to an intra-family succession, differences from promotions appear in pay and formal education. New hires receive significantly higher wages but have a lower share of college graduates. Firms with external successions show a higher likelihood of newly hired female managers instead of promotions. This can possibly also be attributed to the fact that there were rather few female executives before.

Average marginal effects of exogenous variables on recruitments of executives in relation to all new executives (base group: promotions).

Source: LIAB 2009–2019, 597 observations, establishments with 5 and more employees and a probable firm succession.

Marginal effects calculated from the regression outcomes in Supplemental Table A.2 using STATA’s command “margin.”

**, *, and † denote significance at the 0.01, 0.05, and 0.10 level, respectively.

Discussion and conclusion

Our study aimed to contribute to the literature on the effects of succession events on family firm executives and resulting changes in firm behavior by establishing an empirically strong foundation for future research. Specifically, we examined changes in executive teams around business succession events in family firms using a robust and large-scale dataset. Prior research has focused on intra-family dynamics or differences between family and non-family firms (Combs et al., 2018). Additionally, some studies have investigated the role of non-family executives in family firms and their impact on interpersonal relations and firm outcomes (Hiebl and Li, 2020). However, our study is one of the first to address turnover and new additions to executive teams in the context of succession events.

Our results show that changes in leadership and ownership can result in significant and structural changes within family firms’ executive teams. However, the extent depends strongly on the type of succession arrangement. Companies with a family-internal succession intention experience fewer disruptive changes in executive teams around the succession event than those with family-external succession or companies with no succession event at all, especially in the time before the succession event. In firms with family-internal succession, the probability of turnover in the 3 years before the succession event is around 38% lower than in firms with external succession and around 65% lower than in family firms without a succession. This suggests a deliberate strategy by family firms to preserve firm-specific resources such as institutional knowledge and SEW. In contrast, transferring firm leadership outside the family may introduce uncertainty regarding strategic direction and organizational culture, thereby increasing executive turnover. Additionally, our findings indicate that firms with family-internal successions continue to exhibit lower turnover rates after succession events. More specifically, turnover is 16% lower compared to family-external successions and 27% lower compared to firms without successions. However, hiring and promotion rates show fewer differences across succession types, suggesting that continuity strategies primarily influence executive retention rather than additions to the team.

These results suggest that family firms with a planned family-internal succession aim for continuity by keeping their executive teams together (Umans et al., 2020). Executives, who leave before the family-internal succession, are typically of comparably higher age, suggesting that they have reached retirement age. On the other hand, these firms retain experienced executives and thus keep tacit knowledge within the firm, which helps the successors to step into their new position and run their businesses successfully. The results therefore also show that longstanding executives in family firms have close connections with their companies. Hence, they want to accompany the leadership transformation to ensure that parts of their individual legacy are also transferred to the next generation (Memili et al., 2013). Having supportive and loyal relationships with the owner families and the successors, these executives have great impact on the succession process but also the outcomes (Umans et al., 2021).

For firms with family-external succession arrangements, for example, trade sales to new owner-managers, we do not find similarly strong differences to family firms without a succession. Although they also show significantly lower dismissal rates before the succession event, this figure increases significantly after the succession, which indicates that more executives leave their companies after the new leaders have taken over, either voluntarily, or involuntarily. This finding is in line with Bach and Serrano-Velarde (2015), who observe that new external CEOs face more job separations and wage renegotiations after they took over their new firms. However, the hiring rates of firms with family-external succession do not increase after the successions, which contradicts the assumption that new hirings or promotions are avoided before the succession and left completely to the new owners.

When investigating the hiring versus promotion decisions in family firms with succession events, we find that promotions are the predominant form of appointing new executive team members. However, the share of outside hires is higher before the succession than afterward in both firm types, which indicates that firms strengthen their executive teams with experienced outside candidates, who can add valuable resources and reduce the risk associated with the succession process (Lutz and Schraml, 2011).

Our central contribution to the field is to extend knowledge on the actual changes that occur within executive teams, depending on the planned succession event, and to highlight their intra-organizational implications. This study provides robust empirical evidence on how succession events shape executive team dynamics in family firms. By differentiating between family-internal and family-external successions, our research contributes to the literature on SEW and nepotism, highlighting both continuity benefits, and potential disruptions associated with succession planning. Specifically, we demonstrate that family-internal successions are associated with significantly lower executive turnover—a mechanism that preserves firm-specific human capital and legacy. These insights advance academic understanding and offer practical guidance for succession planning in family firms, laying a foundation for future research into the nuances of external succession strategies.

Next to contributions to the academic literature, our findings offer also important insights for family businesses owners facing succession, as they can be used to specifically counteract a possible loss of knowledge by long-serving executives (Massingham, 2018). Thus, owners must plan the upcoming succession holistically. This includes the selection and preparation of internal or external successors, as described in many succession guides, but also forward-looking personnel planning for key top management positions. Transparent communication with family and non-family members of the business about the planned succession mode and timelines is essential. This is especially important for family-external successions, where greater disruption among executives is likely. Therefore, to prevent a loss of tacit knowledge in the firm, family-external successors should be involved as early as possible to provide perspectives to existing employees.

Building on our empirical results, we propose three avenues for future research: Firstly, examining how shifts in executive teams during succession events impact family firms’ performance and innovation is essential, especially in the context of SEW. This exploration should consider objective performance measures such as profit, sales, and market share, to uncover deeper insights into the role of SEW in these dynamics. Secondly, the implications of executive changes on firms’ longevity and sustainability post-succession warrant investigation, with a focus on factors that contribute to long-term success. This includes examining how a stable and competent executive team can uphold the family’s emotional and non-financial goals, ensuring the firm’s enduring legacy. Lastly, understanding the supportive role of executives in aiding family-internal successors during the initial post-succession phases is crucial. This involves understanding how these relationships and transitions can be managed to preserve or enhance the family firm’s SEW, alongside investigating the necessary executive and personnel adjustments for successful succession.

Although our empirical results were derived from the analysis of a large and comprehensive data set, several limitations accompany this study. Our measure of executive turnover is based on changes in employment status from time t to time t + 1, which does not allow us to distinguish between voluntary departures and involuntary dismissals. Consequently, throughout the manuscript we refer to overall executive turnover rather than solely to dismissals. Furthermore, a more granular differentiation within family-external successions (e.g. insider/management-buy-out vs outsider/management-buy-in) would be insightful. However, our dataset does not permit such granularity. Thus, the inability to further differentiate the underlying reasons for turnover may affect the interpretation of our findings. This question could be possibly addressed by future research relying on personal-level survey data and could provide valuable insights about executives’ career expectations and personal concerns related to succession events. Another future research path is the examination of career and executive development programs for non-family employees in family firms.

Furthermore, we lack data on the owner families’ or potential external buyers’ structure and characteristics of each company. Factors such as the number of children, their educational and professional backgrounds or their respective motivation to become involved in the family business have great impact on the chosen mode of succession and the structure of the process (De Massis et al., 2008). They also impact the perceptions and decisions of non-family executives (Barnett et al., 2012). Recent examples of studies that investigate the composition and roles of different succession constellations and the impact on firm outcomes are Thevenard-Puthod (2022) or Campopiano et al. (2020). Future research could extend the understanding of the interdependencies between family structures and non-family (executive) employment.

Supplemental Material

sj-docx-1-gjh-10.1177_23970022251366579 – Supplemental material for From continuity to change: Executive team restructuring in family firms during succession events

Supplemental material, sj-docx-1-gjh-10.1177_23970022251366579 for From continuity to change: Executive team restructuring in family firms during succession events by Michael Graffius, Christopher Hansen and Arnd Kölling in German Journal of Human Resource Management

Supplemental Material

sj-docx-2-gjh-10.1177_23970022251366579 – Supplemental material for From continuity to change: Executive team restructuring in family firms during succession events

Supplemental material, sj-docx-2-gjh-10.1177_23970022251366579 for From continuity to change: Executive team restructuring in family firms during succession events by Michael Graffius, Christopher Hansen and Arnd Kölling in German Journal of Human Resource Management

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Data availability statement

The datasets analyzed during the current study are not publicly available due confidential data from the “Linked-Employer-Employee-Data of the IAB” (LIAB) provided by the Institute for Employment Research of the Federal Employment Agency in Germany (IAB). The dataset is available for associated IAB researchers or academics on reasonable request. This study uses LIAB version QM2 9319. For detailed information on the data please see DOI: 10.5164/IAB.FDZD.2103.en.v1. Data access was provided via remote data access from the Research Data Center/FDZ of the German Federal Employment Agency/BA at the Institute for Employment Research/IAB.

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.