Abstract

Advancement in information and telecommunication technologies (ICTs) has helped open governance to public participation. The participation of the citizens in government is essential for transparent and sustainable governance. This study examines the relevance of e-governance in promoting transparency and accountability concerning the government’s fiscal activities. The study, employing the variation in the open budget index using the fractional probit model, finds that the adoption and use of e-governance enhance and promote budget transparency. This evidence conforms with governments’ growing adoption of ICTs in serving and communicating their fiscal activities to the public.

Introduction

The information and communication technologies (ICTs) exert tremendous influence in both public and private organisations, including governance. Technological advancement has made it possible to use ICTs tools to promote governance at all levels around the world. This is what is known as e-governance or, in the more recent term, digital governance. E-governance opens up government services and enhances popular participation in governance by the people. It promotes seamless government operations and helps eliminate challenges inherent in providing government services occasioned by man-to-man interactions, mainly due to corruption and denial of services to certain people (Elbahnasawy, 2014). The elimination of challenges in government services brings transparency, accountability, efficiency and sustainability to the government (Twizeyimana & Andersson, 2019). This ensures that good governance, which culminates in development in all facets of life, is achieved. Good and accountable governance relies on a sustainably participatory government. Such governance encourages input and participation of the people in fiscal allocation decisions. Openness in the government budget is demanded to ensure that the government is transparent and accountable to the people. Transparency strengthens institutions and ensures that governance conforms to international best practices. It also raises the level of political collaboration where stakeholders consider themselves as partners in progress. Besides, market discipline requires modern governments to be transparent to attract funds from international markets (Wang et al., 2014).

In many countries, traditional fiscal institutions and legislative processes over budgets are less transparent than expected. The principal-agent problem plagues the process; many under-the-table dealings that are not in the best interest of the citizens are involved. The information asymmetry between the political class and the governed may impose an unnecessary cost on the citizens (Alt & Lassen, 2006; Mourão, 2008). This has necessitated the demand for direct participation by the citizens to ensure transparency. E-governance can enhance the participation of the people in governance and budget processes and help realise the objectives of the demand for accountability (Justice et al., 2006). Cicatiello et al. (2017) document political determinants of fiscal transparency. The study identifies three institutional factors that influence fiscal transparency: control over the legislature, ideological orientation and political competition, which essentially reinforces the findings of Wehner and de Renzio (2013). On their part, Wehner and de Renzio (2013) find significantly positive effects of free and fair elections and democratically elected legislature on fiscal transparency. They argue that fiscal transparency improves budgetary outcomes, reduces corruption and creative accounting; and lowers local government debts by encouraging public oversight (Mourão et al., 2023). On the other hand, von Hagen and Harden (1995) stress the importance of institutional rules.

This study explores the relationship between budget transparency and e-governance. By enhancing disclosure, e-governance may better explain budget transparency. The study relates the Open Budget Index (OBI) as a measure of budget transparency to measures of e-governance and some other covariates using the fractional probit (FPROBIT) model (Papke & Wooldrige, 1996, 2008). The augmented regression test (Davidson & Mackinnon, 1993) reveals that the concern about endogeneity does not exist. The study establishes that e-governance indeed improves fiscal openness/budget transparency. It shows and reinforces the view that e-governance has far-reaching implications for governance. ICTs have a vast influence on governance and information disclosure. The application of ICTs to governance, e-governance is vital in reducing corruption and theft of public funds, promoting disclosure and accountability and facilitating transparent procurement (Andersen, 2009; Banerjee et al., 2020; Khan et al., 2021; Lewis-Faupel et al., 2016; Yfantis et al., 2021). Thus, e-governance is a sine qua non to budget transparency.

Employing technology in governance eliminates corruption (Andersen, 2009) by ensuring that the actions of public officers are traceable. This eradicates haphazardness in governance occasioned by discretionary decisions that are out of tune with laid-down procedures. It could reduce wastage in governance and enhance openness in fiscal operations. It can also strengthen the people’s confidence in the government as the information released through the communication channels is traceable and verifiable (Lean et al., 2009; Welch et al., 2005). Budget transparency helps prevent practices that could lead to government failure (Ríos et al., 2016). E-governance could guarantee people’s access to budgets in modern times because of the volume of budget documents, unlike the traditional budget-making and implementation arrangements. Adopting e-governance could increase political participation in any country (Gil-Garcia et al., 2020; Zafarullah & Ferdous, 2021). Moreover, the study finds that e-governance will increase the use of online platforms to provide and access services by people (Zafarullah & Ferdous, 2021).

Besides, this study examines if institutional factors are important in explaining budget transparency. The study finds that institutional factors are critical to budget transparency, in line with Wehner and de Renzio (2013) and von Hagen and Harden (1995). The study suggests that freedom of expression and the demand for and provision of accountable government, which are elements of good governance, are essential for budget transparency. High institutional qualities are generally suitable for budget transparency, while corruption is terrible. The national statistical capacity, mainly the reliability of a nation’s statistical information, goes a long way in determining the openness of fiscal details. Demand for accountability from the government requires some level of education and human capital development. Educated people are more likely to press the government for openness and accountability and use e-governance channels. Hence, countries with good human capital stock may enjoy high budget transparency.

Additionally, the study seeks to know the effect of e-governance on budget transparency in specific regions. For regions that are represented explicitly in our model with dummies, e-governance has a lower impact on budget transparency for Asian countries. In contrast, the interaction term for African countries is not statistically significant, which may imply that other factors, such as the conditionalities of donor agencies and lenders, may be driving budget transparency in Africa. This study also complements others that have examined the issues of budget/fiscal transparency. The rest of this study is organised as follows: The section ‘Budget Transparency and E-governance’ discusses the roles of e-governance in good governance and how e-governance and budget transparency are connected. The ‘Data and Methodology’ section focuses on methodology and data. The section ‘Discussion of Results’ discusses the results, while the study is concluded in ‘Conclusion’ section.

Budget Transparency and E-governance

Assessing the Roles of E-governance

The governed have always wanted information about the government. Citizens are concerned about how their taxes are spent. The Universal Declaration of Human Rights by the United Nations subsumes freedom of expression. Article 19 of Human Rights clearly expounds the people’s rights to information and freedom of expression. Since the declaration, nations around the world have enacted laws either labelled as Freedom of Information Act or Right to Information Act to facilitate their citizens access to information (Krah & Mertens, 2020). However, these acts do not guarantee access to information, especially in countries where a lack of transparency and accountability is a culture of the public sector (Baroi & Alam, 2021). Thus, the parliamentary efforts of enacting the Information Act could not really achieve their objectives in many countries. This may have motivated the recommendation of the integration of e-governance into the Bangladeshi Right to Information Act to improve governance (Baroi & Alam, 2021).

E-governance addresses the deployment of information and telecommunication technologies (ICTs) for governance to promote service delivery and development (Justice et al., 2006; Krah & Mertens, 2020; Sein, 2004). This approach to public service delivery is a measure to eliminate challenges in getting public services to the people, reduce trust issues between the government and the governed (Yfantis et al., 2021), enhance good governance (Nanda, 2010), and bring about development (Aker & Mbiti, 2010; Ojo et al., 2013; Sein, 2004). It is borne out of the challenges of incentives and accountability in delivering and accessing public services. Where the service delivery process is not transparent, there are incentives on the part of the government’s agents/representatives to withhold/deny services for many reasons, such as discrimination, bribery, punishment, extortion, unobservable action and inadequate supervision. Thus, e-governance is a tool for transparent services, government accountability and effectiveness in public service delivery (Banerjee et al., 2020; Baroi & Alam, 2021), promoting trust between the government and the governed.

The rationale for the adoption of e-governance is mainly good governance (Nanda, 2010). It is a governance process that encompasses accountability, transparency, efficiency, stability, popular participation and inclusiveness. Good governance ensures that no one is left behind/denied access to what is offered to the public by the government and that governance is done in a sustainable manner. Open governance is achieved through processes that reduce human influence and interactions, which suppress accountability and promote corruption, in public service delivery. The adoption of internet and mobile technologies in rendering services and providing information about governance opens up government activities, which are hitherto shrouded in secrecy. Thus, e-governance is one of many tools adopted to mitigate corruption in governance, especially through blockchain technology (Yfantis et al., 2021). Singh et al. (2010) find that e-governance improves the citizen-government relationship and reduces corruption. This further lends credence to the view that corruption is at the heart of poor service delivery and development outcomes in many countries, which e-governance can help eliminate.

E-governance promotes openness (Banerjee et al., 2020; Lewis-Faupel et al., 2016). Mistry (2012) finds that the adoption of e-governance loosens the grip of corruption over an entity. He identifies three enablers of corruption as discretionary power of the public officers, the existence of opportunities for economic rents in government business, and weak institutions, which likely result from the existence of economic rents. These enablers of corruption are threats to transparency and accountability in governance. This results in bad governance and governance outcomes. The enablers of corruption can be checked if attention is focused on eliminating discretionary power through e-governance (Banerjee et al., 2020; Mistry, 2012; Yfantis et al., 2021). Corruption blossoms in an environment where government information is not transparent and made available to the public at regular intervals. Access to information about the government’s activities is enhanced through e-governance.

The elimination of human interaction in public service through online service delivery saves time, eliminates wastage and reduces administrative burden (Singh et al., 2010). Thus, e-governance can enhance the quality of the bureaucratic processes by reducing the possibility of extortions made possible by man-to-man interactions (Banerjee et al., 2020; Lewis-Faupel et al., 2016; Yfantis et al., 2021). Service delivery through e-governance can be traced, unlike man-to-man service delivery, where the destruction of documents is possible, making tracking human actions almost impossible (Andersen, 2009; Justice et al., 2006). Officers who are responsible for services provided on e-governance platforms are conscious of their electronic footprints/monitoring. So, they are cautious in the way they relate with the public. This ensures transparency in the provision of services. The conditions of services are disclosed online for all to see without discrimination or favouritism. The violation of service delivery conditions on online platforms can be quickly investigated, and punishment can be meted out to the affected officer(s). All of these promote good governance through transparency and accountability. In all, good citizen-government interactions are made possible.

E-governance enhances the bureaucratic process by bringing it to a quality standard. This raises the level of efficiency in resource use. E-governance can eliminate unnecessary duplication in both human and material resource uses (Banerjee et al., 2020; Lewis-Faupel et al., 2016). More so, fewer employees are needed to operate the e-governance service outlets or contact points for resolving issues in service delivery. The efficiency gain also translates to a reduction in costs to both the government and users of services as service users spend less time accessing public services (Justice et al, 2006). The efficiency gain brings about the sustainability of good governance. One of the aims of good governance practice is to promote a good relationship between the government and the governed (Nanda, 2010). This entails trust-building with citizens in governance, which involves transparent decision-making by the government regarding public life such as procurements, financial allocations and budget processes. Being open requires carrying the public along in governance processes. Openness builds and promotes trust in government as access to government information is facilitated. This will increase the citizens’ political participation and ensure that the government’s policies enjoy public support (Singh et al., 2010). ‘Participation and collaboration have the potential to improve accountability and increase citizen engagement in government decision making (Gil-Garcia et al., 2020)’.

The Nexus Between Budget Transparency and E-governance

The budget processes and fiscal institutions have tremendous implications on budget performance and budget sustainability, including budget transparency. Cicatiello et al. (2017) conclude that control over the legislature, ideological orientation and political competition are determinants of fiscal transparency. Weingast et al. (1981) posit that the budget will be higher when those who make budget decisions do not bear the budget’s full burden. In other words, the traditional budget process without an e-governance arrangement, which citizens do not have direct control over and make inputs, can impose huge considerations on them through the tax implications of a budget (Alt & Lassen, 2006; Mourão, 2008). Where a powerful legislature exists, a budget can be raised against the wish of the government (Alesina & Perotti, 1996; Von Hagen & Harden, 1995) and the governed. Though Alesina and Perotti (1996) and Hallerberg and Marier (2004) observe that a budget performs better when the government’s executive branch has control of the budget, neither the legislature nor the executive can be trusted without public scrutiny. This underscores the agency problem in governance due to moral hazard concerning political representatives’/public officers’ decisions about public spending. This indicates that the traditional budget processes and institutions that assume public input through their elected representatives may not serve the public’s interest. Hence, there is a need for public participation to ensure transparency in public spending by citizens who bear the burden of government decisions through tax payments. The e-governance arrangement will make possible public participation in governance. Open government involves participation, collaboration and the role of ICTs (Gil-Garcia et al., 2020).

According to the World Bank Budget Transparency Initiative (World Bank, 2015, p. 1), ‘budget transparency refers to the extent and ease with which citizens can access information about and provide feedback on government revenues, allocations, and expenditures’. Budget transparency requires the citizens to have unfettered access to the information contained in a budget. The information has to be presented in a simplified form that an average citizen can analyse and comprehend. International Budget Partnership (IBP), a global think-tank organisation that saddles itself with the responsibility of assessing countries’ level of budget transparency through surveys and publishes OBI biennially uses comprehensive, timely, accessible budget information in eight critical areas for OBI. The organisation requires that countries prepare and publish these documents: a pre-budget statement, an executive’s budget proposal, an enacted budget, a citizen budget, in-year reports of the budget performance, a mid-year review, a year-end report and the audit report of the budget (Adamtey, 2017). Surveys on the availability of these documents and the adequacy of information in them constitute criteria used to rank a country’s level of budget transparency.

In modern times, the volume of budget documents practically makes it impossible to have printed versions of the required documents distributed to every member of society to meet the IBP’s requirements. However, a cost-efficient approach exists to get the public informed about the budget and its goals for a fiscal year. E-governance through various e-channels represents a more affordable alternative for a broader dissemination of budget information. Justice et al. (2006) posit that e-governance holds the promise to achieve budget transparency and citizen participation which the New York Bureau of Municipal Research wanted to achieve before the First World War by hosting the public to an elaborate budget presentation. Thus, it is a veritable and cheap alternative to town hall budget presentations. However, town hall budget presentations and public engagement are still practiced in some developing countries. Politicians enjoy opacity in government fiscal activities. This makes budget transparency demand-driven. On the other hand, e-governance is supply-driven to deliver services and encourage participation in government. The primary goals of opening a public budget, among others, include mitigation of corruption, efficiency and sustainability of resource use, building and enhancement of trust in government, decentralisation of powers and participatory government, which can be achieved through incorporating blockchain technology in e-governance (Yfantis et al., 2021).

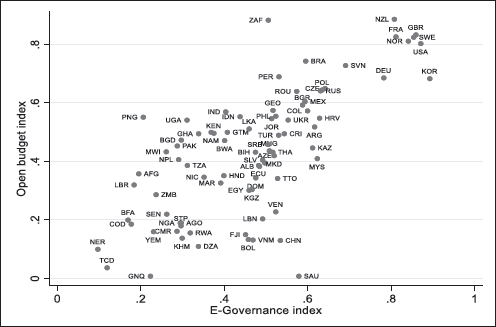

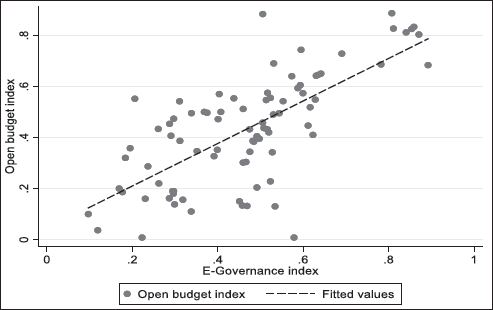

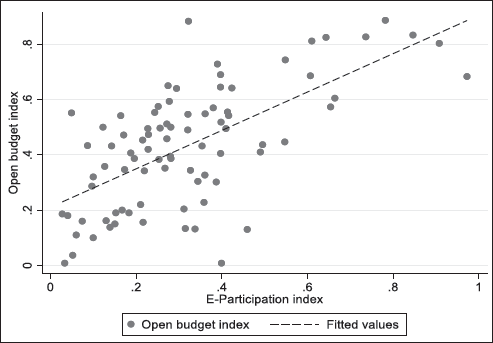

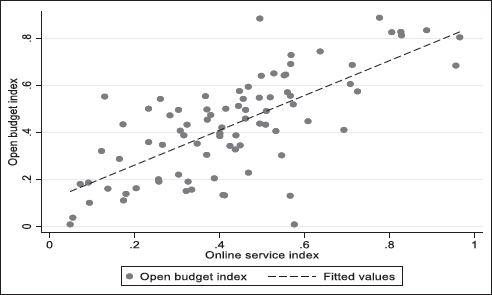

The stated goals of budget transparency inherently establish a nexus between e-governance and budget transparency. Figures 1–4 provide a bird’s-eye view of the relationship between the e-governance index and OBI (which measures budget transparency), including the relationship between e-participation and OBI and the online service index and OBI. There is a positive relationship between OBI and e-governance, including e-participation and online service index. The scatter plot in Figure 1 shows that countries that run open budgets are equally doing well in using e-governance. Many of these countries are also the world’s leading countries in terms of good governance and development outcomes. It appears e-governance helps these countries in promoting budget transparency. By extension, the level of e-governance-enabled transparency will likely reduce corruption, thereby making the budget work for the people. It is possible to improve development outcomes through e-governance which will effectively help mitigate corruption and corrupt tendencies (Aker & Mbiti, 2010; Andersen, 2009; Mistry, 2012; Sein, 2004; Twizeyimana & Andersson, 2019). By contrast, some developing countries that have attained a moderately high score in the e-governance index fall below average in their OBI, namely Saudi Arabia (SAU), China (CHN), Malaysia (MYS), Trinidad and Tobago (TTO) and Venezuela (VEN).

A Scatter Plot of the Average E-governance Index and Open Budget Index of Countries, 2005–2018.

Scatter Plot Overlaid with a Two-way Linear Regression Fit Showing the Predicted Value of Open Budget Index by E-governance Index.

Scatter Plot Overlaid with a Two-way Linear Regression Fit Showing the Predicted Value of Open Budget Index by E-participation Index.

Scatter Plot Overlaid with a Two-way Linear Regression Fit Showing the Predicted Value of Open Budget Index by Online Service Index.

Various services’ processes are published under the e-governance regime, which cannot ideally be manipulated against any citizen or in favour of any corrupt bureaucrat to extort public service users (Elbahnasawy, 2014; Yfantis et al., 2021). By and large, when the budget is transparent, there is efficiency, effectiveness and sustainability in the use of government’s resources as both the governed and the government monitor the use of public resources. Availability of budget information is critical to building and enhancing trust in government. Timely access to and accurate budget information can help citizens make useful inputs into the governance process and enhance collaboration with the government for the state’s benefit. E-government can open up the government’s fiscal activities and enhance citizens’ participation in government.

Data and Methodology

Data

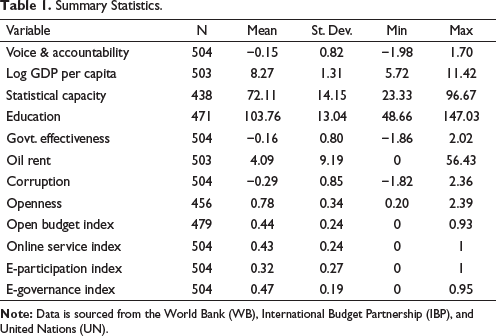

The data for this study is secondary data on a few countries across the world’s geo-political zones. The data is collected by research-focused development and think-tank organisations such as IBP, the United Nations Department of Economics and Social Affairs (UNDESA) and the World Bank (WB). The OBI score is a score obtained by a country in budget transparency measures over 100. This is reported by the IBP biennially. The e-government, e-participation and online service indexes are bounded between 0 and 1. They are scores obtained by countries from the survey conducted by UNDESA and associated United Nations’ (UN) agencies that access the use and adoption of e-governance. The e-governance index is a composite index of four major indexes, among which are e-participation and online service indexes. The e-governance index (EGOV) components are individually generated, and the average of these indexes is computed to obtain an e-governance index for a country. Because the e-government, e-participation and online service indexes are bounded between 0 and 1, the OBI score is converted to an index of a similar unit. This ensures that the dependent and the main independent variables in our model are in the same unit.

The OBI and EGOV are available biennially between 2005 and 2018, but the year of release of the data alternates, which is not the same. While OBI is available for 2006 to 2017, the EGOV is available for 2005 to 2018. This informs the decision to collapse the data, including the covariates for the regressions into six periods. The summary statistics of the data are displayed in Table 1. The data indicates that the adoption of EGOV is around the average of 0.47, while OBI on average is 0.44 around the world. A correlation analysis of the data for this study was carried out to obtain the correlation matrix. The results show that no correlation coefficient is above 0.8 for all the independent variables. Though the correlation coefficient for government effectiveness and corruption is high, the correlation coefficients for all other variables are below 0.7. Due to the concern about autocorrelation and heteroskedasticity, the robust option is exploited for our panel data estimates to take care of our concerns having transformed the data by collapsing it into six periods.

Summary Statistics.

Empirical Model

The following empirical model is specified for this study:

where i and t index country i and time t, respectively. The empirical model relates the OBI to EGOV, including a set of covariates to identify the effects of EGOV on OBI. Each OBI represents the index of budget transparency for a particular time, while EGOV represents the e-government index for each period in this study. The

Budget transparency aims to eliminate/reduce the secrecy surrounding state finances (Wehner & de Renzio, 2013) and can reduce public debts when citizens are actively interrogating the state’s fiscal activities (Mourão et al., 2023). E-governance can enhance budget transparency as budget information can be sent to the public via the internet and mobile technologies, and inputs into the budget can be made via the same channels (Ojo et al., 2013). To test the hypothesis that e-governance aids budget transparency, the OBI is regressed on the e-governance index and other covariates, as stated in Equation (1) above. The robustness of the results from the estimation is checked by introducing components of EGOV, the e-participation and online service indexes in place of EGOV in the econometric model. Other covariates employed in the study are defined below. Voice and accountability is a measure of good governance. This is the closest measure to the human rights to information and freedom of expression. The score of this measure ranges from −2.5 to +2.5. It is one of the WB six measures of good governance. Three of these measures are employed in our model. These institutional factors are important for budget transparency (Adamtey, 2017). In the words of Campos and Pradhan (1996), ‘institutional arrangements affect incentives governing the size, allocation and use of budgetary resources and improve transparency and accountability—binding key players to particular fiscal outcomes and making it costly for them to misbehave’. The choice of voice and accountability as a measure of good governance is because it is considered that freedom of expression and demand for accountability are major pillars of good governance that impact fiscal outcomes.

Government effectiveness is another measure of good governance in the model. An effective government would probably avoid issues that plague budgets. This is chosen to represent a myriad of concerns in governance that cannot be accounted for in the model due to lack of data. The myriad of concerns includes legislative oversight by the legislature, which debates and approves budget proposals (Ríos et al., 2016). The ease with which a nation can control corruption, the higher is the level of transparency and effectiveness in government business in that nation. A corrupt government will do everything to avoid making open its finances. GDP per capita is a measure of the size of a nation’s economy, and it is obtained from the WB online database. More productive economies are likely to adopt e-governance in rendering services and interacting with the public. Carlitz et al. (2009) suggest that income level determines the level of budget transparency. The log of GDP per capita is employed in the model estimation to control for the sizes of countries’ economies’ budget transparency. Statistical capacity is a measure of a country’s power of accuracy in producing and disseminating statistical information about its activities. This is also obtained from the WB online database. The statistical capacity of a nation can reveal the level of openness of a country. This level of openness is important for realising budget transparency. Many corrupt nations do not have adequate statistical information as they might have many things to hide.

Oil corrupts, and most oil-producing nations lack all the tenets of good governance (Badeeb et al., 2017). The variable oil rent is included among the covariates to check the effect of reliance on oil rent on budget transparency. As reported by the WB, oil rent is the difference between the worth of crude oil produced at world prices and the total cost of production. The difference is then expressed as a percentage of the GDP to show a nation’s reliance on oil rents. Education, measured by gross primary school enrolment, is included among the covariates to assess the effect of minimum human capital development on budget transparency. Since transparency is usually demanded by the people, the proportion of the population exposed to basic education will influence the level of budget transparency. Openness is the level of trade openness of an economy. Trading and open economies tend to be transparent. Openness is demanded by trading partners to know and weigh the risks associated with the economy they are trading with. This interaction may force a trading economy to be transparent with its fiscal activities. All the variables are expected to impact budget transparency positively except corruption and oil rent. We include regional dummies for African and Asian countries in our model to see how these regions are performing in terms of budget transparency. Besides, the interaction terms are included to know the effect of e-governance on budget transparency in the regions. The countries’ regional groupings in this study are based on the five groups of the UN Department for General Assembly and Conference Management. These groups are African, Asia-Pacific, Eastern Europe, Latin America and the Caribbean and Western Europe and other developed nations.

Econometric Issues and Estimation Strategy: Pooled OLS, GLM and Fractional Probit

The pooled OLS exploits efficiently both within and between variances of data. Under this method, the intercept and the slope estimates are the same for all countries. This estimation technique’s basic requirement is that the independent variables and the error term are contemporaneously uncorrelated. Under the orthogonal assumption, the estimate of coefficients by OLS is consistent and unbiased. We conducted augmented regression (Davidson & Mackinnon, 1993) with concern for endogeneity in the OLS estimates by regressing e-governance, e-participation and online service indexes separately on log fixed broadband subscription and log population density. We included the residuals in the model where e-governance, e-participation and online service index are the main variables of interest. The augmented regression (Durbin-Wu-Hausman) test indicates that the residuals are not significantly different from zero. Thus, endogeneity is not a problem in our estimates.

However, due to the nature of the dependent variable for this study, OLS and other linear static estimators might not be appropriate for estimating the data. The OBI is a bounded index between 0 and 1. Since OBI is a bounded variable, standard linear models may not provide the covariates’ accurate effects on the OBI (Papke & Wooldrige, 1996, 2008). The challenges with OLS, including other linear models for fractional data, are analogous to the problems of a linear probability model for dichotomous data (Papke & Wooldrige, 1996). Therefore, the OLS is used as an approximate benchmark model to which other econometric models, Generalised Linear Models (GLM) and FPROBIT, are compared.

The GLM and FPROBIT are more efficient in estimating Equation (1) because the outcome of interest ranges between 0 and 1 (where y satisfies 0 ≤ y ≥ 1, as in the dependent variable in this study). The GLM fits the linear model as a probit function where the dependent variable is distributed as Bernoulli using the Newton–Raphson (maximum likelihood) optimisation. This model will generate estimates similar to that of the fractional response model, all other things being equal because they are quasi-likelihood estimators. Like GLM, the FPROBIT model fits the model where the outcome of interest is a fractional variable. Though it is possible to choose between probit and logistic functions under any of GLM and FPROBIT, it appears the probit conditional mean function has some advantages over the logistic conditional mean function, which include simplicity of the computation of the estimates and the possibility of inclusion of unobservable regional specificity in the model (Papke & Wooldrige, 2008). It thus appears more suitable for this study.

Discussion of Results

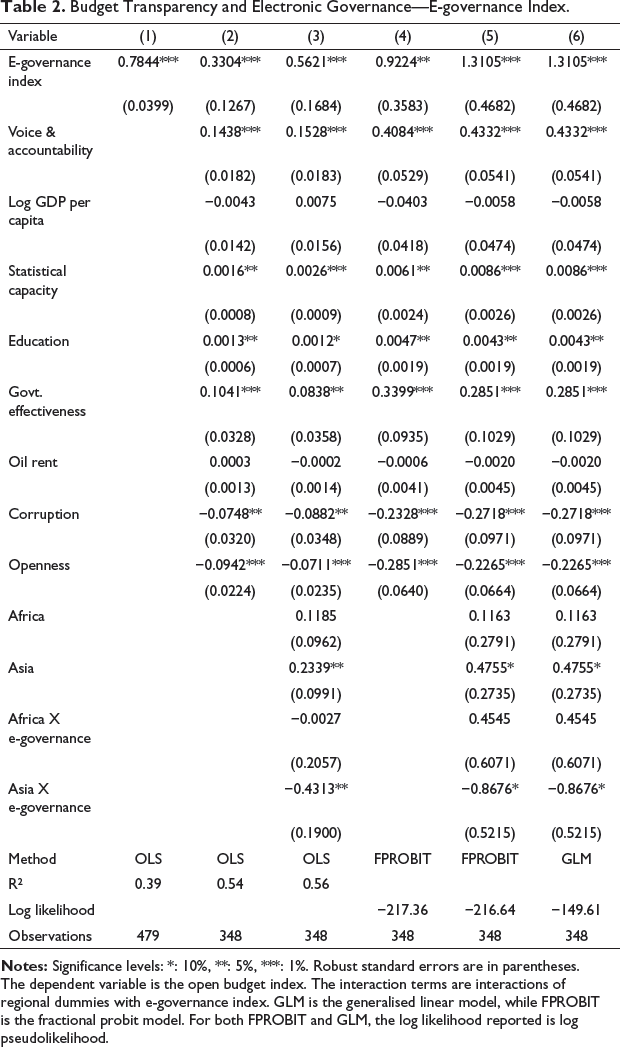

The results of econometric estimations are presented in this section. The results are shown in Tables 2–4. The parsimonious model in column 1 of Table 2 indicates that e-governance is positive and statistically correlated with budget transparency. The estimates in columns 2 and 3, Table 2 demonstrate that e-governance is positively correlated with budget transparency. The model in column 2 has all the variables in our model with regional dummies, while the model in column 3 includes interaction terms. The results in columns 4–6 from FPROBIT and GLM also show that e-governance is positively correlated with budget transparency. Though the GLM and FPROBIT models’ results are similar, the FPROBIT model estimates the model better than GLM with a log-likelihood of −216.64.

Budget Transparency and Electronic Governance—E-governance Index.

Thus, our analysis will focus on the results of the FPROBIT model. The result of the FPROBIT generates 0.4658 as the marginal effects of e-governance. This suggests that a change in the e-governance index will lead to an improvement in budget transparency by about 47%. This huge impact arising from the application of various ICTs tools can limit human efforts and prevent the manipulation of the government finances in favour of vested interests. Voice and accountability is statistically significant across the estimators, as shown in Table 2. Voice and accountability does matter for budget transparency. Citizens who can freely express themselves and press the government for accountability will demand budget transparency. Participation in governance is easier when people have the freedom to express themselves and this can greatly improve budget transparency (Gil-Garcia et al., 2020; Krah & Mertens, 2020). The productivity of an economy measured by log GDP per capita is not statistically significantly correlated with budget transparency. In other words, large GDP per capita, in itself, does not improve budget transparency.

The statistical capacity of a nation correlates positively with budget transparency. This suggests that countries with high-quality statistical reports might not be hiding information from the public and they are more likely to be transparent in their fiscal activities. Human capital is critical to development; countries with a good number of educated people are likely to be more transparent in fiscal activities because of the population’s quality than a country populated by illiterates. The illiterate population cannot hold the government to account and demand accountability. This may account for the positive correlation between education and budget transparency.

Corruption is harmful to overall developmental objectives. The estimates in Table 2 show that corruption is statistically significant and negatively correlated with budget transparency. This conforms with our a priori expectation as endemically corrupt countries will not open their fiscal books to the public. Many oil-producing countries are poorly ranked in the corruption index, including Malaysia, Saudi Arabia, Trinidad and Tobago and Venezuela. As shown in the scatter plot in Figure 1, they are rated high in the e-governance index, but they are poorly rated in budget transparency. The effectiveness of the government in power matters for the openness of fiscal activities in any country. The increase in government effectiveness leads to improvement in budget transparency. Oil rent appears not to have an impact on budget transparency as the variable is not statistically significant. Contrary to the expectation, openness is negatively correlated with budget transparency. The dummy for Asian countries and the interaction of Asia with e-governance are statistically significant. This implies that Asian countries appear to be transparent with their budgets, but the impact of e-governance on budget transparency is smaller in these countries. The dummy and the interaction terms for African countries are not statistically significant. This may be speaking to the situation in Africa where aids are tied to specific governance conditions in recent decades. Thus, other factors could be responsible for budget transparency in Africa.

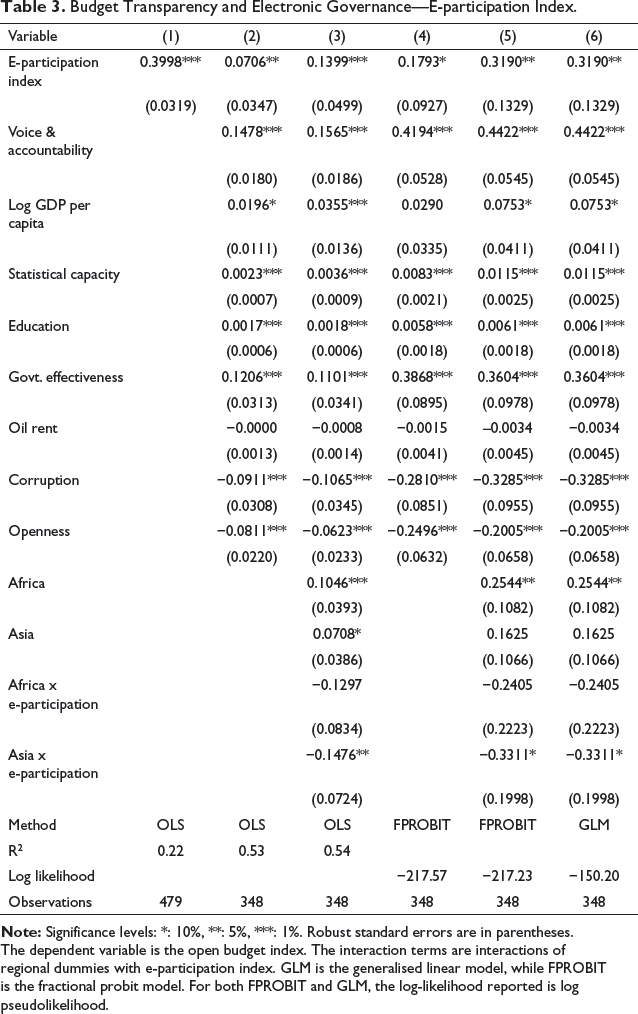

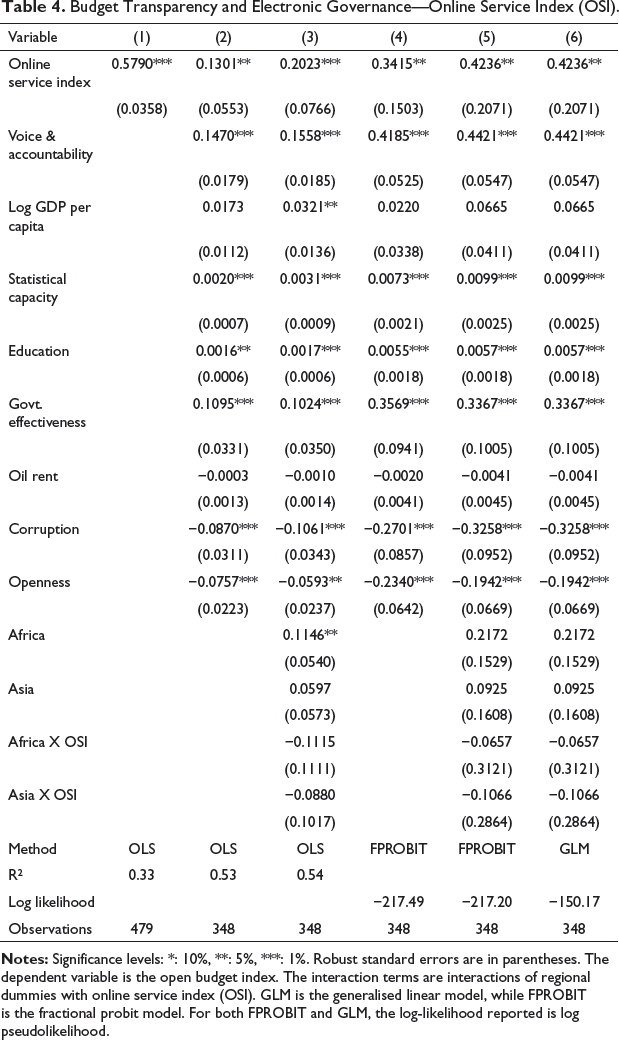

The relationship between e-governance, e-participation and online service indexes has been explained in subsection ‘Data’. E-participation and online service indexes are components of the e-governance index. E-participation shows the levels of participation of citizens in the government’s activities through electronic and online platforms. On the other hand, the online service index indicates the degree to which citizens are served through online platforms. These are vital elements of e-governance, they constitute the means to participate and determine government responsiveness by the citizens (Zafarullah & Ferdous, 2021). To test the robustness of the results in Table 2, the e-governance index is proxied by the e-participation index and online service index in the results in Tables 3 and 4, respectively.

Budget Transparency and Electronic Governance—E-participation Index.

Budget Transparency and Electronic Governance—Online Service Index (OSI).

The results from all estimators, and results explicitly in column 5 of Table 3, show a positive correlation between the e-participation index and budget transparency. From the FPROBIT model, the computed marginal effects for the e-participation index are 0.1137. It means that a change in the e-participation index will produce about a 12% change in budget transparency. Participation is the nucleus of democracy. Where citizens can freely engage the government, the likelihood of opacity in government finances is likely to be low. The vigilance of the people will likely prevent the government of the day from engaging in reckless spending that may harm future generations (Mourão et al., 2023). Overall, e-participation appears to capture the current development around the world about the new approach to public management, where many countries are introducing various e-participation platforms to encourage citizens to make inputs into governance, including public spending. The results in Table 3 are similar in direction and magnitude to the results in Table 2, except that the Log GDP per capita and the dummy for Africa are now statistically significant.

The results in Table 4 indicate a growing adoption of e-service by governments across the world. Specifically, the result in column 5 indicates a positive and statistically significant relationship between the online service index and budget transparency. The marginal effects for the online service index are 0.1510. The marginal effects predict that a change in the e-service index will result in over 15% change in budget transparency. The e-service index’s coefficient and marginal effects are larger than those of the e-participation index, which could be a pointer to the widespread use of online services in governance. This new trend is expected to continue into the distant future. Events around the world, especially after the pandemic lend support to the migration of services online. However, the widespread use of e-service may not necessarily imply an improvement in e-participation (Baroi & Alam, 2021; Zafarullah & Ferdous, 2021). The results in column 5 and Table 4 maintain the same direction and signs as in Table 2, except that the dummies and the interaction terms are not statistically significant.

Conclusion

The involvement of the people is crucial to good governance in any country. This requires that the people are well informed about the state’s activities, especially the government’s fiscal side, and they are also participating through regular contributions to the state’s policies. The budget is about people. They need to be informed, and the government needs their input. These requirements confer legitimacy on the government and ensure the stability of the state. Public participation in governance is suppressed under the traditional budget process. The process assumes public participation through elected representatives in the parliament. However, the traditional budget process is fraught with agency problems. The people’s representatives might not disclose all the material facts of the state’s budget to those they represent. E-governance could eliminate this agency problem and pave the way for the people to interrogate the state’s fiscal activities. The public should be able to demand transparency in the government’s finances without fear of being attacked/muzzled by the government’s apparatus of force. There must be freedom of expression to demand accountability from those elected or appointed to run the state.

The government must willingly surrender information on the state of the nation’s budget to the people. There must be pre-budget information, implementation updates and review and post-budget performance analysis, which are deemed conditions for transparency by the IBP. These are required to be laid before the people to educate them on the activities of the state. The government operates an opaque budget where the IBP conditions are not satisfied. Under this situation, the budget is prone to manipulation at the expense of the state and citizens. Running an open budget system in modern times is easier when the government employs electronic governance. Members of the public can be reached through electronic means. This eliminates opacity in government business, especially as it affects the government’s fiscal side and strengthens people’s confidence in their government.

This study shows that operating a system of electronic governance is germane to budget transparency, which is absent in the traditional budget process. The e-governance encourages and allows inputs from the citizens to public budgets as against the traditional budget process, which relies on indirect participation. This study’s findings are robust to other measures of e-governance, such as the e-participation index and online service index. The adoption of e-governance and e-participation of the people through electronic governance are key determinants of budget transparency. The timely release of statistical information, which can be demonstrated through the nation’s statistical capacity, is also critical to budget transparency. This suggests that many nations that run opaque governments may also maintain a weak statistical capacity. This view directly links the timely release of statistical information to electronic means, making it relevant for budget transparency.

Human capital is the bedrock of any progressive development, without which development will come to a halt. As shown in this study, this is relevant to budget transparency. A society that is populated by highly educated people will demand openness and accountability from the government. They can always use electronic resources through which the information released by the government can be accessed. Besides, voice and accountability and government effectiveness are crucial institutional factors in budget transparency. Opacity in governance, a bad governance practice, is indeed linked with corruption. This study finds that poor control of corruption does not bode well for budget transparency, as nations plagued with corruption maintain a poor budget transparency record. This is peculiar to countries that are dependent on natural resource rents. Because of the flow of natural resource wealth and the corruption it engenders, the governments of natural resource-dependent countries are known for hiding budget information from the public even when they embraced electronic governance, as shown in Figure 1 in the case of Saudi Arabia, Venezuela and Trinidad and Tobago.

Nations are encouraged to embrace electronic/digital governance to promote budget transparency and good governance. There may be challenges to the implementation of the e-governance project. Where there is endemic corruption, it might not eliminate the problem. People who are saddled with e-governance project implementation may choose to abuse their positions, including holding the government and the people to ransom. Notwithstanding the abuse concern, it promises a better deal for the governed and the state.

Footnotes

Acknowledgement

My sincere appreciation goes to the Director of UNU-EGOV, Delfina Soares. Also, I thank Professors Linda Veiga and Luís Barbosa for their support.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

This article, which benefited from the FCT funding with reference number UMINHO/BI/456/2018, was developed while I was a visiting fellow at the United Nations University Operating Units on Policy-driven Electronic Governance (UNU-EGOV), Guimarães, Portugal.