Abstract

This article provides a comprehensive comparative analysis of India’s newly implemented Labour Codes against the established US labour law framework. Drawing from over a decade of global practitioner experience, the study deconstructs complex legal statutes such as the Code on Wages, the Industrial Relations Code and the Code on Social Security. The analysis highlights critical divergences in gratuity eligibility, wage structures and gig worker protections. Written in plain English to ensure accessibility for non-legal professionals, this research utilises comparative tables and practical examples to equip human resources (HR) leaders with the clarity needed to navigate the evolving cross-border employment landscape.

Introduction

For decades, the Indian labour law landscape was a labyrinth of 29 central laws and over 100 state regulations, a compliance nightmare that often stifled growth. In contrast, the USA has operated on a more decentralised, market-driven model rooted in the ‘at-will’ employment doctrine. As of late 2025, with the full operationalisation of India’s four new Labour Codes, the gap between these two massive democracies has both narrowed and widened in fascinating ways. This article decodes these statutory shifts, offering practical examples and clear comparisons for both employees and managers.

The Six Pillars of Change

To understand the shift, we must look at the specific pillars of the new Indian reforms and measure them against their American equivalents.

The Paycheck Paradigm: Code on Wages Versus Fair Labour Standards Act (FLSA)

In the USA, the FLSA is the bedrock. It sets a federal minimum wage ($7.25/h) and mandates overtime pay of 1.5 times the regular rate for hours worked over 40 in a week (FLSA, 1938).

The Indian Shift Involves the ‘50% Rule’

Gazette of India (2019) redefines ‘Wages’ to standardise pay structures. Historically, Indian employers split salaries into numerous allowances (house rent allowance (HRA), conveyance, special allowance) to keep ‘Basic Salary’ low—often only 30%–40% of total pay. This lowered their liability for Provident Fund (PF) and gratuity contributions. The new code mandates that ‘Basic Pay’ must constitute at least 50% of the total remuneration. If allowances exceed 50%, the excess is added back to the ‘Basic’ component for calculating statutory benefits. Consequently, take-home pay decreases due to higher PF deductions, but retirement savings and gratuity payouts increase significantly.

The Wage Code Expanded: Universal Reach and Faster Exits

Beyond structure, the new Code fundamentally changes who is covered and how quickly they must be paid. India’s repealed Payment of Wages Act, 1936, provided protection only to employees earning below ₹24,000 per month. Those earning above this threshold, including senior management, had no legal recourse under the Act for delays in salary payment. The new Code eliminates this threshold, applying to all employees.

While the FLSA applies broadly, it includes specific ‘white-collar exemptions’ for executives. India’s new rule covers all employees, removing the ‘manager vs. workman’ distinction for wage payments.

The ‘Exit’ Speed: Two-day Settlement

Under India’s new Code on Wages, when an employee is dismissed, retrenched or resigns, all payable wages must be settled within two working days of their separation—whether due to removal, dismissal or resignation.

This requirement matches the strictest US state laws, such as California’s. Most US states and federal law only require payment by the next regular payday. With this measure, India has set a new global benchmark for settlement speed.

The Gratuity Revolution

The most significant shift for contract employees in India concerns changes in gratuity eligibility. Gratuity is a statutory benefit—a long-service bonus—paid to employees upon leaving an organisation.

Previously, under the Payment of Gratuity Act, 1972, an employee had to complete five continuous years of service to become eligible. Departure after 4 years and 11 months resulted in no payout.

New India Rule (Gazette of India, 2020b): Fixed-term Employees (FTEs)

The new Code drastically reduces the eligibility period from 5 years to 1 year for FTEs hired for specific contract periods, such as a 2-year project. For permanent employees, the 5-year vesting period remains unchanged.

In contrast, the USA has no federal law mandating gratuity. Severance pay is entirely a matter of company policy or private negotiation.

Hiring and Firing: Industrial Relations Versus At-will Employment

This is perhaps the most culturally distinct area.

The US model: ‘At-Will’ employment: In 49 out of 50 US states, employment is ‘at-will’. This means that an employer can dismiss an employee for a good reason, a bad reason or no reason at all, provided that the dismissal is not discriminatory.

The Indian model: The rise of fixed-term employment: India has never embraced ‘at-will’ employment. Gazette of India (2020a) introduces a middle ground through FTE. Employers can now hire workers for a specific period (e.g., 2 years) with all statutory benefits. When the term ends, the employment concludes automatically, with no formal dismissal process or requirement for retrenchment compensation.

Practical implication: This allows Indian companies to hire for projects without the long-term liability of permanent employment, similar to using contractors in the USA, but with stronger statutory benefits for the worker.

The Gig Economy: Social Security Code Versus Independent Contractors

The ‘Uber driver’ dilemma is a global challenge. In the USA, gig workers are classified as independent contractors (often called 1099 workers). This status typically excludes them from statutory employee benefits such as employer-provided health insurance or unemployment pay. India, however, has adopted an innovative approach through its Code on Social Security, 2020, which serves as a global pioneer by explicitly extending a safety net to gig and platform workers. A key mechanism is the aggregator fund, which mandates that companies like Zomato, Swiggy or Uber contribute 1%–2% of their annual turnover into a government-managed Social Security Fund. This fund is designated to provide health and accident insurance for gig workers.

Maternity Benefits: A Stark Contrast

The disparity in parental support arguably represents the widest gap between the two nations. In India, under the Maternity Benefit Act (subsumed within the Social Security Code), eligible employees are entitled to 26 weeks of paid leave for their first two surviving children and 12 weeks for the third child onward, with the cost borne entirely by the employer. Conversely, in the USA, the Family and Medical Leave Act (FMLA, 1993) provides eligible employees with 12 weeks of unpaid leave. Eligibility is restricted to those who have worked at least 1,250 h in the past year for an employer with 50 or more employees within a 75-mile radius.

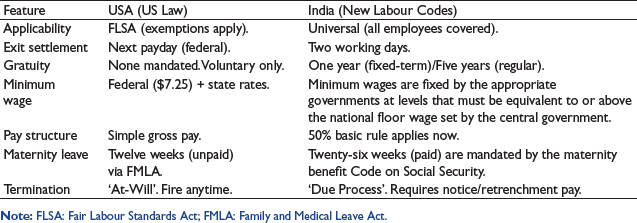

Comparative Summary Table

Conclusion

For the multinational manager, the lesson is clear: US employment logic does not apply in India. US managers operating in India must recognise that FTEs are now entitled to gratuity, and budgets must account for this liability. Conversely, Indian managers in the US must understand that ‘at-will’ employment is a reality; thorough documentation serves primarily as a defence against discrimination claims rather than as a procedural requirement for termination itself. Ultimately, India’s new Labour Codes represent a significant leap toward modernising its workforce, bringing structure to the gig economy and flexibility to hiring, all while maintaining a robust social security framework.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Disclaimer

The views, opinions and interpretations expressed in this article are solely those of the author and do not necessarily reflect the official policy, position or legal standing of his current organisation or any other organisation with which the author is affiliated. This article is intended for general informational and educational purposes only and does not constitute legal advice. Readers are advised to consult with qualified legal counsel or compliance experts regarding specific employment law matters, organisational policy changes or the application of these codes to their specific circumstances.

Funding

The author received no financial support for the research, authorship and/or publication of this article.