Abstract

Mobile money (MoMo) services have become an integral part of the banking system in developing countries. Research is needed to understand the implications of taxing this financial technology sector and inform public policy. The current MoMo tax literature is limited by its focus on personal factors while neglecting institutional factors. The present study develops an integrated model of individuals’ attitudes toward MoMo tax payments and their intentions to use MoMo services while paying related MoMo taxes. To test the model, we analyze survey data collected from 892 participants across 16 regions of Ghana using structural equation modeling. Our findings indicate that perceived trust in government and perceived tax burden are significant determinants of attitudes toward MoMo tax payment, while perceived tax burden is influenced by perceived trust in government. Similarly, perceived tax burden mediates the effect of perceived trust in government on attitudes toward MoMo tax payments. Furthermore, the perceived usefulness of MoMo services is determined by perceived ease of use of MoMo services, whereas MoMo services use/tax payment intentions are determined by perceived trust in government, attitudes toward MoMo tax payments, and perceived usefulness of MoMo services. Finally, perceived usefulness of MoMo services mediates the effects of perceived ease of use on MoMo services and MoMo service use/tax payment intentions. We discuss explanations for these findings and provide practical, theoretical, and research implications.

Introduction

Mobile Money (MoMo) services offer convenient and secure alternatives to traditional banking and have transformed financial transactions in regions with limited access to formal financial institutions (Koomson et al., 2021; Pobee et al., 2023). In recent years, several governments have introduced legislation to tax MoMo transactions. In Ghana, the Payment Systems and Services Act, 2019 (Act 987), established a regulatory framework for the fintech industry to facilitate the digital delivery of MoMo and other financial services. This legislation was followed by the Electronic Transfer Levy Act (Act 1075) in March 2022, which imposed a 1.5% E-levy (MoMo tax hereinafter) on the total daily amount of electronic transactions exceeding GH¢100.00 (roughly USD8), whether for value-added services, product sales, or simple money transfers to family and friends. The decision to tax MoMo transactions with no additional monetary value, such as those supporting family and friends, is surprising because it conflicts with MoMo’s core utility as a solution to financial exclusion (Arestoff & Venet, 2017; Donovan, 2012; Mbiti & Weil, 2015; Morawczynski & Pickens, 2009). Immediately after the introduction of the MoMo tax in Ghana in 2022, monthly MoMo volume sank to its lowest value ever (¢71.4 billion) and has yet to surpass the highest monthly volume (¢90.5 billion) prior to MoMo tax introduction. 1 This decline in MoMo use raises the question of whether the MoMo tax provides alternative funding to the government at the expense of financial inclusion.

To address this question, this paper investigates the factors influencing attitudes toward MoMo tax payments and intentions to use MoMo services in Ghana. Identifying the factors that shape individuals’ attitudes and intentions toward MoMo usage and related tax payments is crucial to determine whether the MoMo tax impedes the adoption of MoMo services. In Ghana, the MoMo tax is automatically deducted once a MoMo transaction is authorized; hence, the behavioral attitudes and intention to use MoMo services are directly tied to the behavioral attitudes and intentions to pay the MoMo tax, as the user has no control over the decision to pay the tax. Although the greater financial inclusivity and ease of use of MoMo services compared to traditional banking systems positively influence their adoption (Akinyemi & Mushunje, 2020; Hornuf et al., 2024; Narteh et al., 2017; Osei-Assibey, 2015; Tobbin, 2010; Tobbin & Kuwornu, 2011), attitudes about compliance with the MoMo tax may negatively affect the uptake of MoMo services. Tax compliance is influenced not only by trust in the tax recipient, as validated by the stewardship and governance literature (Taing & Chang, 2021), but also by the perceived burden of existing taxes (Ali et al., 2001; Yamamura, 2014). Consequently, individuals who have lower trust in government or a stronger perception that current taxes are burdensome may seek to avoid MoMo tax payments by limiting their use of MoMo services.

Furthermore, the literature on the dynamics of trust in MoMo services has focused on trust in MoMo service providers (Baganzi & Lau, 2017; Bongomin et al., 2019; Narteh et al., 2017; Osei-Assibey, 2015; Tobbin, 2010; Tobbin & Kuwornu, 2011) and MoMo agents (Johnen et al., 2023), largely omitting empirical analyses of the impact of trust in the MoMo tax recipient (i.e., the government). Exceptions are studies by Amoah et al. (2023) and Anyidoho et al. (2023), who showed that trust in government promotes MoMo adoption. This scarcity of relevant work prevents a complete understanding of the impact of tax payments on MoMo adoption. Moreover, studies of the influence of MoMo taxes on individual usage intentions have predominantly used the MoMo tax rate as the independent variable (Anyidoho et al., 2023; Mensah et al., 2022; Mpofu, 2022; Pobee et al., 2023). This stream of MoMo tax literature confirms that the likelihood of tax compliance decreases when current MoMo tax is considered burdensome. However, the influence of an individual’s perception of their existing tax burden prior to MoMo tax introduction (which is unlikely to be affected by the MoMo tax rate) on MoMo adoption (and hence MoMo tax compliance) has not been examined.

Another unaddressed issue is whether attitudes about MoMo tax payment drive MoMo usage intentions after MoMo tax introduction. Because MoMo services improve the overall well-being of underprivileged groups (such as those with low education levels or incomes, women, older people, and the unbanked) and also enhances ease of financial transactions with less cost among the already financially included groups such as people with high education or levels of incomes, men and the banked (Amoah et al., 2020; Della Peruta, 2018; Gai et al., 2018; Koomson et al., 2021; Narteh et al., 2017; Pobee et al., 2023; Senyo et al., 2022), these groups may develop favorable attitudes and intentions towards MoMo usage. However, empirical evidence on whether these groups may develop similar favorable attitudes towards MoMo tax payments and MoMo service use/tax payment intentions post MoMo tax introduction is not available.

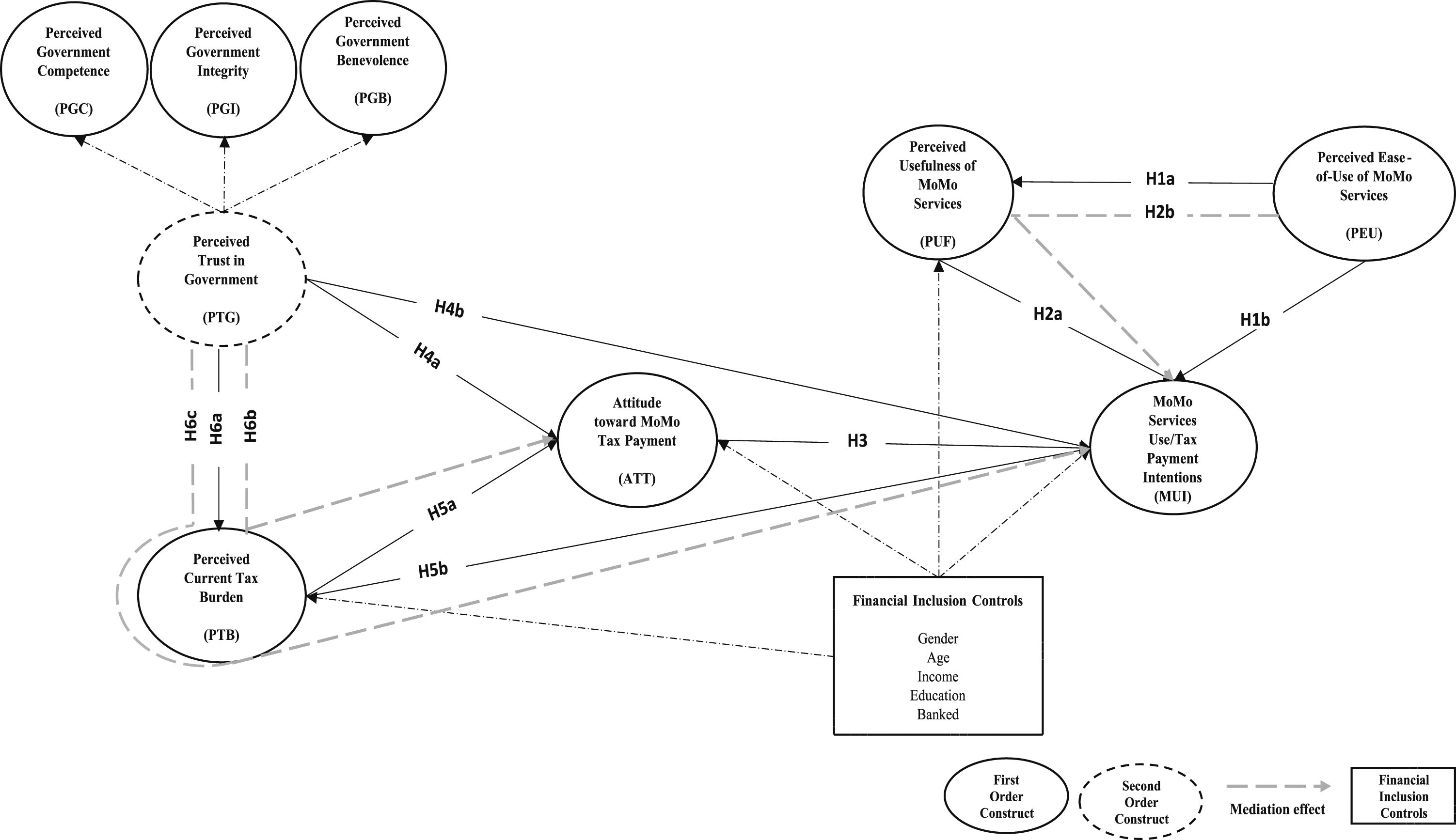

These gaps in the literature give rise to three key research questions; First, do trust in government and current tax burden influence attitudes toward MoMo tax payment and the intentions toward MoMo usage and payment of related taxes? Relatedly, does trust in government influence the perception of current tax burden? Second, do perceptions of MoMo services’ usefulness and ease of use influence intentions toward MoMo usage and payment of related taxes? And third, do attitudes toward MoMo tax payment lead to intention to use MoMo services and payment of related taxes?

We answer these questions by integrating the core tenets of the technology acceptance model (TAM), namely, the perceived usefulness and ease of use of MoMo services with tax burden and government trust frameworks. We capture trust in government by assessing individuals’ perceptions of the government’s competence, integrity, and benevolence, while tax burden is measured by individuals’ perceptions of how burdensome their current tax obligations are. We conduct our analyses using survey data collected from 892 respondents in Ghana and co-variance based structural equation modeling (CB–SEM).

To the best of our knowledge, this study is the first to integrate the elements of technology adoption, tax burden, and trust in government in an empirical examination of MoMo services and their promises of enhancing financial inclusion in the post-MoMo tax environment. In doing so, our study addresses a limitation of recent MoMo studies, which predominantly use pre-tax data (Tetteh et al., 2023, p. 9), and provides an alternative framework for examining MoMo tax attitudes and adoption intentions. Additionally, we contribute to the literature by shedding light on the intricate relationships between trust in government, tax burden, attitudes toward MoMo tax and MoMo adoption while highlighting certain nuances addressing barriers to financial inclusion based on our model’s addition of financial inclusion controls. Our findings inform MoMo policymakers and service providers in designing interventions and strategies as related to t MoMo tax introduction.

Theoretical Background and Literature Review

MoMo Adoption in Africa and Ghana

MoMo services are mobile phone-based services that facilitate electronic money transfers through telecommunication networks to network subscribers. To receive or transfer money, a mobile phone user must register with an agent. The user deposits money onto his or her SIM card, which then shows as “e-money” in the user’s “e-wallet” (Baganzi & Lau, 2017) and can also be withdrawn in cash by the depositor. While accessible to all mobile users, MoMo services are primarily important for unbanked individuals (Della Peruta, 2018) and accelerate money transfers among marginalized populations in developing economies (Narteh et al., 2017). MoMo services hold significant potential for financial inclusion in Africa, where most of the population is unbanked. However, MoMo technology adoption remains low in Africa as a whole (Akinyemi & Mushunje, 2020; Kiconco et al., 2019; Kikulwe et al., 2014).

In Ghana, MoMo technology adoption has been relatively high in both the central regions (where conventional banking services are fully available) and the peripheral regions of the country (where conventional banking services are mostly absent). It is estimated that approximately 60% of residents of Ghana have MoMo accounts, 2 providing strong evidence of the positive effects of MoMo availability on financial inclusion (Senyo et al., 2022). At the individual and business levels, MoMo services facilitate distance payments and direct borrowing of money from the user’s phone without traditional intermediaries. At the government level, state institutions are using MoMo platforms to transfer allowances and support to individual citizens (WorldBank, 2020). However, similar to other countries with high rates of MoMo adoption, Ghana’s introduction of regulations, fees, and taxes, even on non-business-oriented MoMo transactions, is impeding the rate of adoption in new contexts and discouraging existing users from expanding their use of MoMo services (Anyidoho et al., 2023; Mensah et al., 2022; Ofosu-Ampong, 2024; Takyi, 2024; Tetteh et al., 2023).

Theoretical Perspectives on MoMo Adoption

Understanding people’s decisions to use MoMo services is critical for the success of MoMo platforms and their services (Johnen et al., 2023; Meli et al., 2022; Ofosu-Ampong, 2024; Takyi, 2024). MoMo adoption has been examined through the lens of information systems theories, such as technology adoption theories and models. These studies have primarily drawn on TAM, the unified theory of acceptance and use of technology (UTAUT), innovation diffusion theories, and trust frameworks (Mensah et al., 2022; Ofosu-Ampong, 2024).

Following the logic of the TAM, elements of various MoMo platforms, such as usefulness and ease of use, have been used to explain the adoption of MoMo services (Akinyemi & Mushunje, 2020; Narteh et al., 2017; Osei-Assibey, 2015; Tobbin, 2010; Tobbin & Kuwornu, 2011). A meta-analysis by Hornuf et al. (2024) indicated that TAM-related determinants are the most important drivers of mobile fintech adoption in Sub-Saharan Africa. They found that the higher perceptions of usefulness and ease of use of MoMo services are associated with a greater likelihood of MoMo adoption.

Closely related to this stream of the literature is research drawing on the UTAUT (Baganzi & Lau, 2017; Malinga & Maiga, 2020; Mensah et al., 2022; Pobee et al., 2023), which focuses on effort expectancy, performance expectancy, facilitating conditions, and social influence. The last three factors are expected to positively influence the likelihood of MoMo adoption, whereas effort expectancy is expected to have the opposite effect. Hornuf et al.’s (2024) meta-analysis indicated that UTAUT-related determinants greatly impact MoMo adoption.

A third stream of research theoretically integrates constructs from both the TAM and the UTAUT but is mainly anchored in innovation diffusion theories and trust constructs. Studies focused on innovation diffusion expect the likelihood of MoMo adoption to be high if the MoMo technology has a relative cost advantage and is compatible, observable, uncomplex and available for trial (Della Peruta, 2018; Narteh et al., 2017; Ofosu-Ampong, 2024; Osei-Assibey, 2015; Tobbin, 2010; Tobbin & Kuwornu, 2011). Research based on trust constructs anticipates that the likelihood of MoMo adoption will be high if the MoMo technology is trustworthy and perceived to be riskless (Baganzi & Lau, 2017; Narteh et al., 2017; Okello Candiya Bongomin & Ntayi, 2020; Tobbin & Kuwornu, 2011).

Although the above theoretical perspectives provide interesting and valid explanations for MoMo adoption, several aspects of current trends in the MoMo industry have received little or no attention in the literature. First, with the exception of recent work by Ofosu-Ampong (2024) and Takyi (2024), all studies of MoMo adoption were conducted prior to the introduction of important government policy initiatives that dramatically altered the MoMo industry, most notably the MoMo tax. Taxation influences several aspects of individual behavior. Because MoMo taxes automatically apply even to transactions intended to support family and friends, it is critical to examine the antecedents of people’s attitudes and intentions to continue using MoMo services and payment of related taxes.

Second, studies of the impact of trust in MoMo services have not considered the role of trust in the government that collects taxes on MoMo transactions. Despite the work of Tetteh et al. (2023) and Anyidoho et al. (2023), trust in government remains empirically uncharted in MoMo research, which has mainly focused on trust in MoMo service providers (Baganzi & Lau, 2017; Bongomin et al., 2019; Narteh et al., 2017; Osei-Assibey, 2015; Tobbin, 2010; Tobbin & Kuwornu, 2011) and MoMo agents (Johnen et al., 2023). This is a potentially critical factor because individual trust in government is relatively low in the developing economies where MoMo services are particularly vibrant. 3

Model Development and Hypotheses

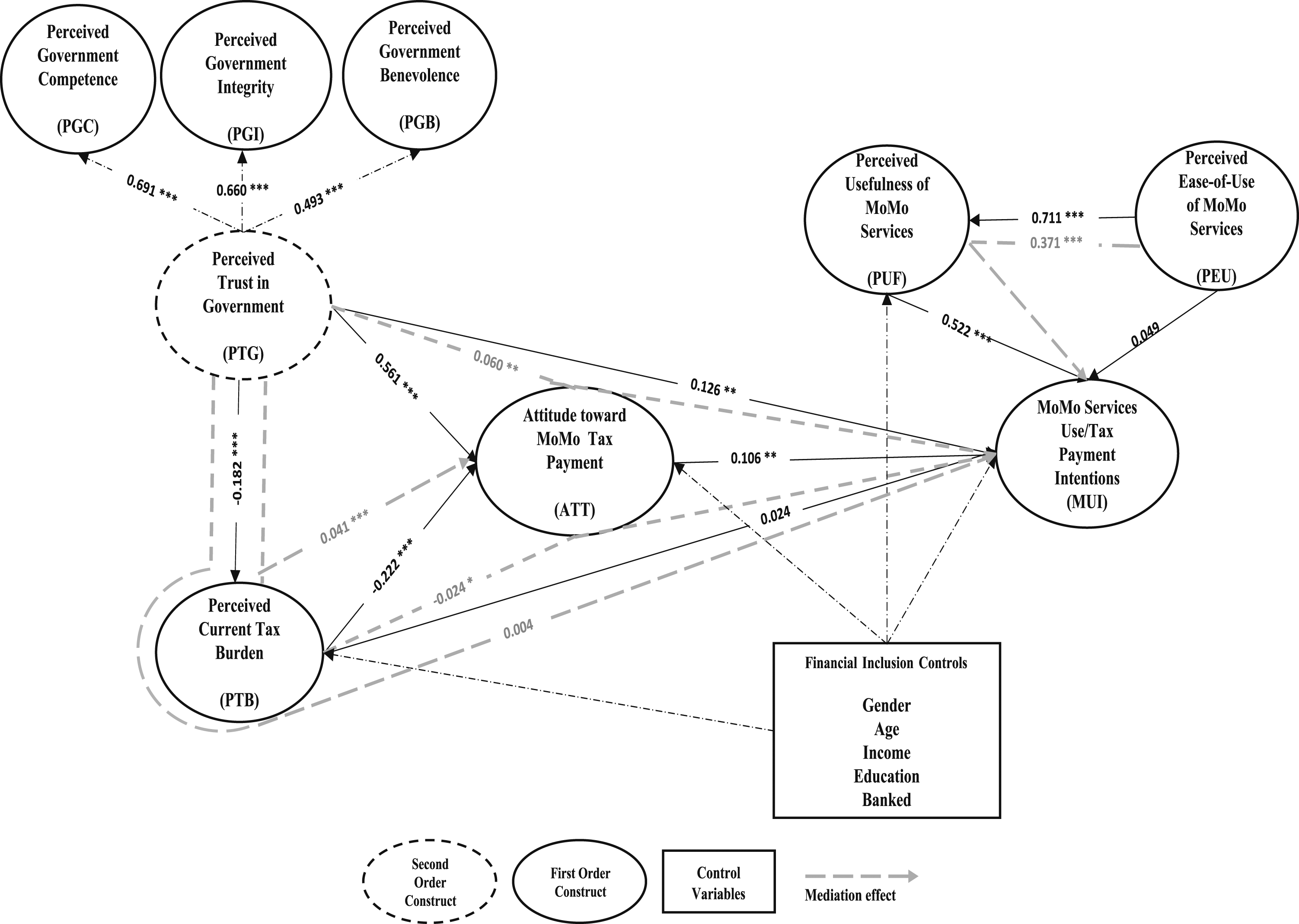

To answer the research questions and further elucidate the effects of relevant factors that have already been established in the MoMo literature, we propose an integrated model explaining individual MoMo usage and its relationships with tax payment attitudes and intentions. We develop the model by identifying critical factors from the tax burden literature, the government trust literature, and the TAM and include control variables for financial inclusion—age, sex, income, education, and unbanked.

First, we argue that because the MoMo tax is automatically deducted at the source (i.e., once a MoMo transaction is authorized, the MoMo user has no control over whether to pay the MoMo tax), behavioral attitudes and intentions to use MoMo services are linked to the behavioral attitudes and intentions to pay the MoMo tax. Hence, our model predicts both MoMo usage and MoMo tax payment simultaneously.

Second, as confirmed in the trust and tax compliance literature, trust in government significantly increases individuals’ likelihood of paying taxes (Murphy, 2004; Scholz & Lubell, 1998; Taing & Chang, 2021) while reducing their perception of the tax burden (Yamamura, 2014). Third, due to the relative novelty of the MoMo tax and its financial implications for MoMo users, we anchor our work in the theory of planned behavior (TPB) (Ajzen, 1991). Specifically, we argue that individuals may not develop the intention to use MoMo services amid tax introduction unless they have already preliminarily formed a favorable attitude toward MoMo tax payment. Fourth, since MoMo services are an innovative technology, we also incorporate elements from the TAM (Davis et al., 1989) and argue that individuals’ use of MoMo services may be predicted by their perceptions of the ability of MoMo services to enhance their existing financial transactions and the efforts needed to perform such transactions.

In summary, the proposed model integrates the existing tax burden perceptions of MoMo users and their perceived trust in government to predict their attitudes toward MoMo tax payment and intentions to use/pay MoMo tax. The model also integrates TAM constructs capturing MoMo users’ perceptions of the usefulness, ease of use and attitudes toward MoMo tax influence on MoMo usage intentions.

Perceived Usefulness and Ease of Use

Perceived usefulness and ease of use are the most important factors predicting mobile fintech adoption in Sub-Saharan Africa (Hornuf et al. (2024). These two variables have been explored by drawing on the TAM framework to explain users’ behavioral intentions in technology adoption (Baah-Peprah, 2023; Davis et al., 1989; Venkatesh & Davis, 2000). Perceived usefulness is the extent to which an individual thinks that using a system will enhance their performance, whereas perceived ease of use is the amount of effort required to use a system (Venkatesh & Davis, 2000). Accordingly, we define the perceived usefulness of MoMo services as the extent to which MoMo users think that MoMo services enhance their financial transactions. Similarly, we define perceived ease of use of MoMo services as the degree to which MoMo users believe that all processes involved in conducting a MoMo transaction require little effort.

In line with Davis et al. (1989) and Venkatesh and Davis (2000), various studies have confirmed that higher levels of perceived usefulness and ease of use increase an individual’s intention to use MoMo services (Akinyemi & Mushunje, 2020; Narteh et al., 2017; Ofosu-Ampong, 2024; Tobbin, 2010; Tobbin & Kuwornu, 2011). Moreover, TAM posits that the effect of perceived ease of use on intentions is mediated by the perceived usefulness of the system, and technology adoption and behavioral studies have confirmed this effect (Baah-Peprah, 2023; Gefen & Straub, 2000; Venkatesh & Davis, 2000). However, this mediation effect has not been explored in the MoMo context. We therefore hypothesize the following:

The perceived ease of use of MoMo services positively influences (a) the perceived usefulness of MoMo services and (b) intentions to use MoMo services.

The perceived usefulness of MoMo services (a) positively influences intentions to use MoMo services and (b) mediates the relationship between perceived ease of use of MoMo services and intentions to use MoMo services.

MoMo Tax Attitudes

The association between attitude and intention is relevant for explaining tax-related compliance intentions, and this knowledge can be used to improve tax-related systems in which a positive tax attitude influences tax behavioral intentions (Taing & Chang, 2021). Because MoMo services enhance the overall well-being of underprivileged groups, including the less educated, women, the elderly, the unbanked, and low-income individuals (Amoah et al., 2020; Della Peruta, 2018; Gai et al., 2018; Koomson et al., 2021; Narteh et al., 2017; Pobee et al., 2023; Senyo et al., 2022), it is reasonable to assume that individuals in these groups developed positive attitudes toward MoMo services prior to the introduction of the MoMo tax. However, there is no empirical evidence on whether these attitudes translate into intentions to conduct MoMo transactions that incur MoMo taxes.

For less-privileged individuals, such as unbanked individuals, MoMo services may provide the only means of conducting financial transactions. However, even privileged groups, such as banked individuals, may be negatively impacted by effects of the MoMo tax, such as higher MoMo transaction costs and tax burdens. It is unlikely that an individual will engage in MoMo services without at least some preliminary consideration of attitude judgements. Regardless of an individual’s identification as privileged or less privileged, a favorable attitude toward MoMo tax payments may lead to intentions to use MoMo services and pay the related tax.

Thus far, we have theorized that intentions to use MoMo services and pay its related taxes are planned behaviors that are influenced by favorable attitudes toward MoMo tax payments, as posited by TPB (Ajzen, 1991). In addition, behavioral research on the adoption of mobile services reveals that attitude significantly influences mobile service adoption behaviors (Gopi & Ramayah, 2007), and this effect has been validated for multiple alternative finance platforms, including crowdfunding (Baah-Peprah, 2023), mobile banking services (Amoah et al., 2020), and MoMo services (Ofosu-Ampong, 2024). Although taxation was not considered, Ofosu-Ampong (2024) confirmed that attitudes toward MoMo services positively influence MoMo adoption.

In line with TPB, we define attitudes toward MoMo tax payments as a MoMo user’s overall evaluation of how favorable MoMo tax payments are. We argue that the extent to which an individual uses MoMo services is contingent upon how favorably they view the MoMo tax and have positive expectations about it, giving rise to the following hypothesis:

A favorable attitude toward the MoMo tax positively influences intentions to use MoMo services while paying the MoMo tax.

Government Trust

Trust is an important determinant of MoMo adoption. Prior to the introduction of the MoMo tax, studies of MoMo adoption focused on users’ trust in the MoMo service provider and in MoMo agents (Baganzi & Lau, 2017; Narteh et al., 2017; Okello Candiya Bongomin & Ntayi, 2020; Tobbin & Kuwornu, 2011). With the introduction of the MoMo tax, another MoMo stakeholder—the government—enters the discussion of trust. Among the few empirical studies of trust in government and its implications for MoMo adoption, Tetteh et al. (2023), Amoah et al. (2023), and Anyidoho et al. (2023) have shown that individuals’ trust in government positively influences their usage of MoMo services.

Analyses of the role of MoMo users’ trust in government are anchored in the assumptions of stewardship theory, with government functioning as the steward of collected tax revenues. As trust is a significant factor influencing their attitudes and behavioral intentions toward online financial transactions in general (Baah-Peprah & Shneor, 2022), individuals’ trust in government acts as an antecedent of their financial commitment to the government’s policy (Scholz & Lubell, 1998). Here, trust significantly influences the likelihood of paying taxes (Murphy, 2004; Scholz & Lubell, 1998; Taing & Chang, 2021). This likelihood depends on positive attitudes and intentions toward tax compliance (Taing & Chang, 2021) and the assumption that the government will exercise competence, integrity, and benevolence in its accountability for the tax revenues collected. Accordingly, we hypothesize the following:

Trust in government positively influences (a) attitudes toward MoMo tax payments and (b) intentions to use MoMo services while paying the MoMo tax.

Tax Burden

Taxing electronic commerce is challenging. In their quest to improve their revenue base by imposing new taxes, governments in developing countries risk restricting the development of new e-markets and the involvement of the community in the evolution and growth of these e-markets (Bongomin et al., 2019; Jones & Basu, 2002). These unintended consequences of taxation may shrink the tax base, leading to an uneven effect and, in the long run, jeopardizing the already fragile economies of these countries (Jones & Basu, 2002). Such consequences are usually magnified when the community participating in the e-market perceives their existing tax obligations as burdensome (Yamamura, 2014).

The long-term detrimental consequences of general taxation of e-markets should serve as a warning for implementing MoMo taxes. The governments of developing economies view taxation of MoMo transactions as a game changer for revenue inflows (Mpofu, 2022). However, reducing or eliminating taxes enhances financial inclusion and provides individuals with basic financial services. Here, Muthiora and Raithatha (2017) and Anyidoho et al. (2023) have argued that exempting MoMo services from taxation is necessary to promote financial inclusion and to facilitate payments for goods and services, which may indicate prices that already include taxes such as VAT.

The literature confirms that MoMo taxes negatively moderate the effect of intention on actual usage of MoMo innovation (Pobee et al., 2023), and MoMo tax exemption positively moderates the relationship between MoMo adoption and financial inclusion (Bongomin et al., 2019). Conversely, MoMo taxation significantly influences MoMo adoption (Anyidoho et al., 2023; Ofosu-Ampong, 2024; Takyi, 2024), and removing MoMo taxes positively influences MoMo users’ actual behavior toward MoMo services (Mensah et al., 2022; Ndung’u, 2019). Rojas-Suarez and Pacheco (2017) argued that MoMo users may try to avoid paying the MoMo tax by making fewer MoMo transactions. However, Mpofu’s (2022) comprehensive critical review found mixed results on the impact of MoMo taxes on MoMo services adoption.

Bongomin et al. (2019) and (Rojas-Suarez & Pacheco (2017) found that taxes levied on MoMo transactions that are above standard rates significantly reduce the usage of MoMo services. However, a tax rate that is considered high in one country might not be considered high in another. MoMo tax rates vary greatly even in regions with similar economies, including in Sub-Saharan Africa. For example, the MoMo tax rate is 0.02% in Cameroon, 0.05% in Uganda, 2% in Zimbabwe, and 1.5% in Ghana. Though heterogeneity in MoMo tax rates between countries may explain Mpofu’s (2022) mixed findings on the impact of MoMo taxes on MoMo adoption, examining MoMo users’ perceptions of their existing tax burden prior to MoMo tax introduction might eliminate the confounding effect of tax rates and enable a critical assessment of the effect of MoMo taxation that can be generalized across contexts.

The general tax literature confirms that the likelihood of tax compliance is negatively related to the perceived burden of taxation (Ali et al., 2001; Yamamura, 2014). Thus, we argue that MoMo users who believe their tax burden is relatively high will have less favorable attitudes toward MoMo tax payments and may avoid paying the MoMo tax by limiting their use of MoMo services. This argument is underpinned by two theoretical foundations. First, TPB (Ajzen, 1991) suggests that an individual is affected by their belief in the ease of completing a task, that is, perceived behavioral control. Therefore, we assume that when MoMo users perceive paying taxes as easy and not burdensome, they will exhibit greater tax compliance. Second, self-efficacy theory, which is part of TPB, and social cognitive theory (Heffernan, 1988) predict that an individual’s belief and self-confidence in their ability to complete a task enhance their intentions to do so. Accordingly, MoMo users who perceive that they can pay MoMo taxes are likely to use MoMo services. In other words, MoMo users who consider their current tax obligations to be burdensome will develop strategies to reduce their taxes, while the opposite will be true for MoMo users who do not consider their current tax obligations to be burdensome. Thus, perceived tax burdens will affect individuals’ attitudes toward MoMo tax payments and intentions to use MoMo services/pay the MoMo tax. Accordingly, we hypothesize the following:

Perceived current tax burden negatively influences (a) attitudes toward MoMo tax payments and (b) intentions to use MoMo services while paying the MoMo tax.

Furthermore, the degree to which an individual considers a tax to be burdensome is contingent on several perceptions, including trust. Notably, the tax literature confirms that people perceive their tax obligation as burdensome if they perceive that the taxes are not appropriate for the benefit of society (Yamamura, 2014). That is, taxpayers may consider the costs of paying taxes higher than the benefits they receive. On the contrary, taxpayers perceive taxes to be less burdensome when they trust that the government will efficiently use the taxes to maximize societal welfare (Yamamura, 2014). Accordingly, we hypothesize the following:

Perceived trust in government (a) negatively influences perceived current tax burden, (b) mediates the relationship between perceived trust in government and attitudes toward MoMo tax payments, and (c) mediates the relationship between perceived trust in government and intentions to use MoMo services while paying the MoMo tax.

Figure 1 summarizes the hypotheses in this study and control variables for financial inclusion: education level, gender, age, access to banking, and income (Amoah et al., 2020; Della Peruta, 2018; Gai et al., 2018; Koomson et al., 2021; Narteh et al., 2017; Pobee et al., 2023; Senyo et al., 2022). Summary of hypotheses.

Methods

Study Context

This study uses survey data collected from Ghana, a country coping with financial inclusion challenges but a fintech-ready context, nonetheless. Ghana is a unique institutional setting that differs from the often studied ‘Western, educated, industrialized, rich and democratic—WEIRED context’ (Henrich et al., 2010). Prior to the introduction of MoMo services in Ghana, remittances were mostly performed through bus drivers. Senders would visit a bus station and negotiate with a bus driver to take the money and deliver it to the recipient (for a fee). The amount would then be delivered to the recipient, who might wait for several hours due to the difficulty of predicting the arrival time of the bus driver. The introduction of MoMo services significantly eased these remittance hustles in Ghana. Accordingly, Statista (2023) 4 identified Ghana as a notable example of the increase in MoMo adoption in Sub-Saharan Africa. Furthermore, the Global Findex Report (2021) 5 indicated that MoMo has significantly enhanced financial inclusion in Ghana, as evident in the percentage of financially included individuals which increased from 41% in 2014 to 58% in 2017. Ghana has also demonstrated remarkable growth in MoMo transaction volumes, from approximately USD69 million in 2022 to USD123 million in 2023. 6 In terms of taxation, Ghana is among the pioneers in MoMo taxation, which was introduced by the government in the form of the ‘Electronic Transfer Levy Act’ (Act 1075). Hence our choice of Ghana as a study context allows us to observe MoMo use intentions and behavior, while exploring the implications of MoMo taxation.

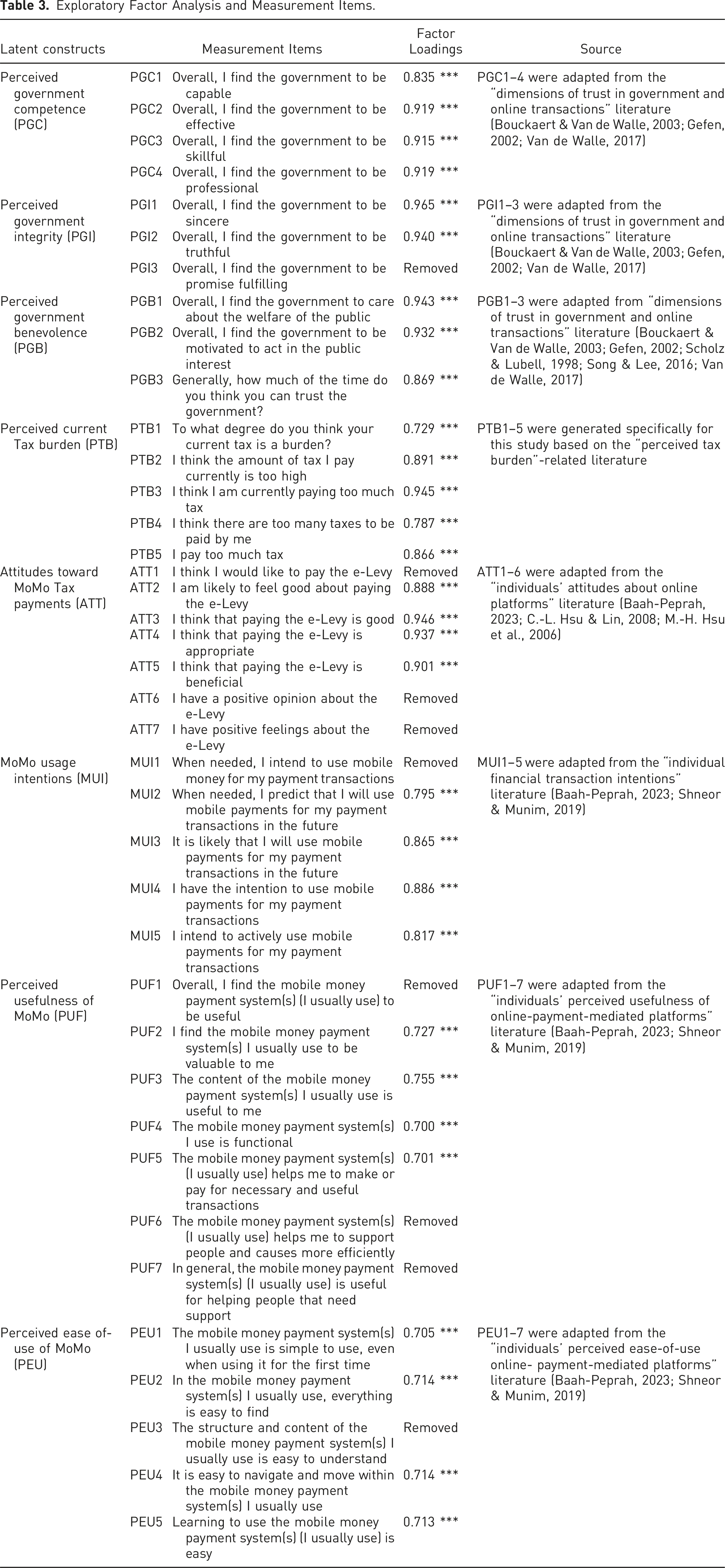

Measurement Items and Scale Generation

Our research model relies on multi-item measurements. Accordingly, previously validated measurement items from the literature were adapted with minor wording changes to better fit the MoMo context as detailed in Table 3. Measurements were conducted on seven-point Likert scales, where 1 indicated strong disagreement with the statement and 7 indicated strong agreement with the statement. The items were revised in rounds of review, and based on feedback from a pilot study of potential respondents.

Data Collection and Sampling

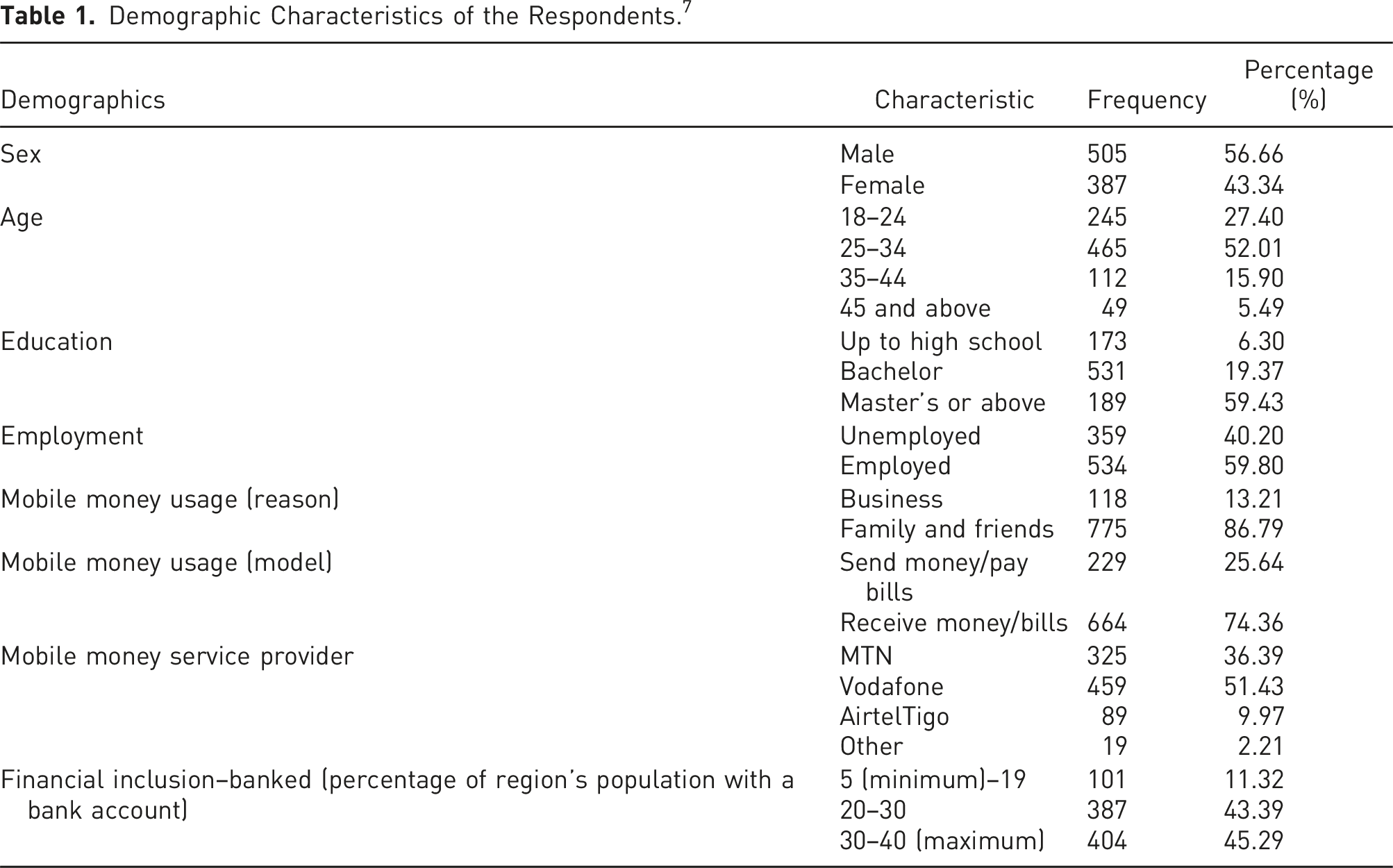

We data collected via an online survey of Ghanaian adults in 2023, while using the SurveyXact software. Participants responded to a questionnaire based on their experience of using MoMo services. Local collaborators distributed the survey via online platforms to the general population in all 16 regions of Ghana, as well as engaged in follow-ups and reminders. Because the survey included a long list of questions in English, respondents were offered an internet data token with a value of 1 euro. The survey was conducted following best practice recommendations as outlined by several researchers (Cook et al., 2000; Porter & Whitcomb, 2003; Roberts & Allen, 2015).

Demographic Characteristics of the Respondents. 7

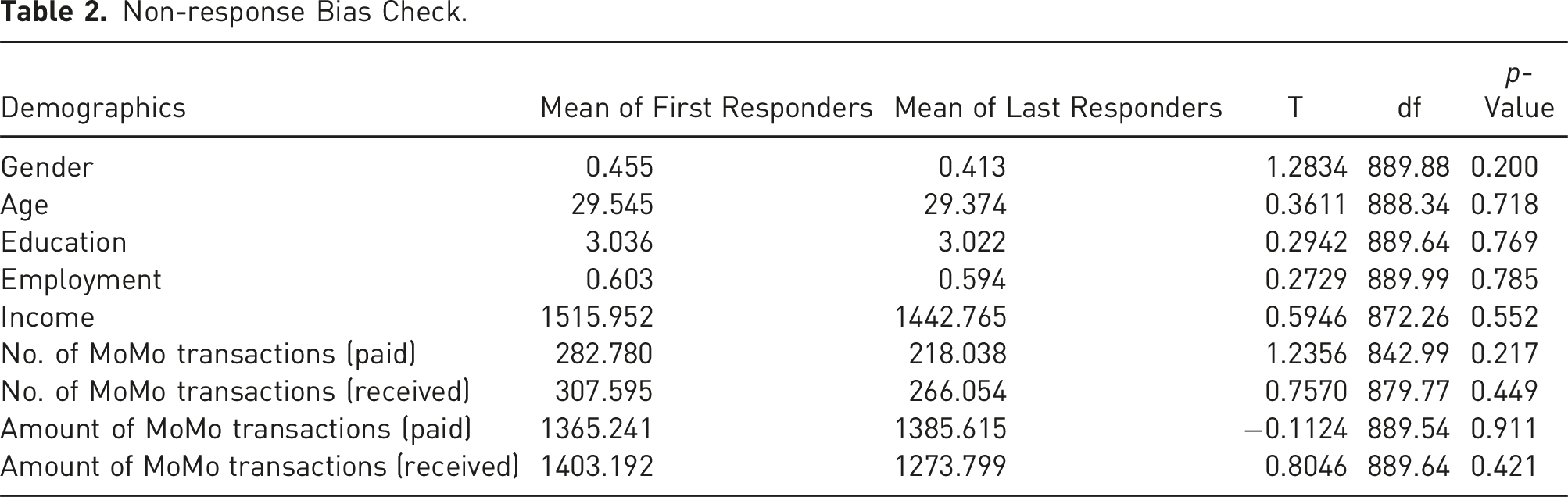

Non-response Bias Check

Non-response Bias Check.

Normality Check

A normal data distribution test is required for SEM estimations. We therefore evaluated the normality of our data. We used the Mardia (1970) test to examine multivariate normality and found that the data were non-normally distributed. For robustness, we further assessed the univariate normality of each measurement item using the Shapiro and Wilk (1965) test and found the absence of univariate normality, with all p-values below the .05 significance threshold. Because none of the variables exhibited characteristics of a normal distribution, following the recommendations of Rosseel (2012), we employed the Satorra-Bentler rescaling method, also known as robust maximum likelihood, for all SEM estimations. For CB–SEM, the lavaan package in the R software suite was used.

Data Analysis and Empirical Results

We created a structural model using CB–SEM to analyze the measurement and structural models. CB-SEM was chosen over partial least squares SEM (PLS–SEM) based on the purpose of the study, model complexity, and characteristics of the data. CB–SEM works well with complex models and large sample sizes (Rosseel, 2012). In addition, CB–SEM is more effective than PLS–SEM when the purpose of the research is theoretical integration of several constructs comprising multiple measurements (Deng et al., 2018; Henseler et al., 2015; Rosseel, 2012).

Measurement Model Assessment

We first confirmed the reliability and validity of the measurement model by performing exploratory factor analysis (EFA) and confirmatory factor analysis (CFA). We also assessed the potential for multicollinearity among the constructs because SEM considers random measurement error, which increases the risk of collinearity among latent constructs and less stable parameter estimates (Grapentine, 2000).

Exploratory and Confirmatory Factor Analyses

Exploratory Factor Analysis and Measurement Items.

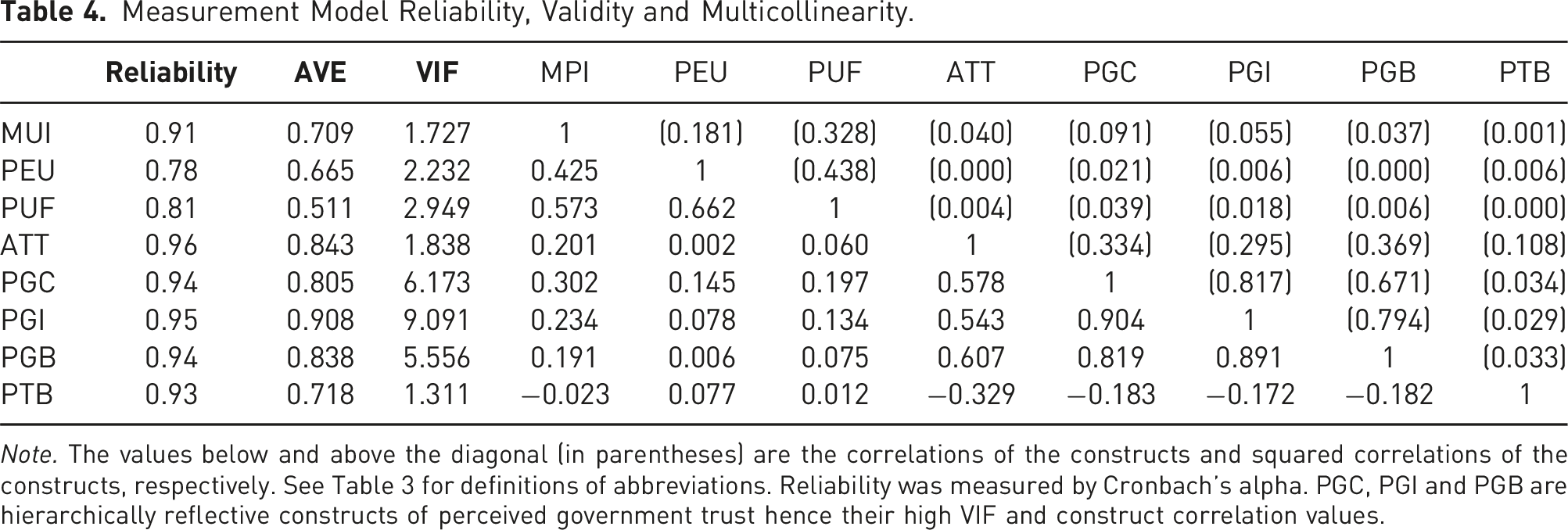

Measurement Model Reliability, Validity and Multicollinearity.

Note. The values below and above the diagonal (in parentheses) are the correlations of the constructs and squared correlations of the constructs, respectively. See Table 3 for definitions of abbreviations. Reliability was measured by Cronbach’s alpha. PGC, PGI and PGB are hierarchically reflective constructs of perceived government trust hence their high VIF and construct correlation values.

Common Method Bias

The use of the same measurement scale throughout the survey may raise concerns regarding common method bias. Accordingly, we followed the procedures suggested by Podsakoff et al. (2003) to examine whether our data suffered from such bias. We used Harman’s single-factor approach and created a single factor with all measurement indicators in the EFA without rotation. The proportion of the data explained by the single factor was 24%, far less than the maximum threshold of 50%, eliminating concerns about common method bias in our data.

Reliability, Validity and Multicollinearity

Reliability is defined as the extent to which individual items provide the estimated value of the latent construct (Gefen et al., 2000; Hair et al., 2014). To confirm the reliability of the constructs, we assessed the composite reliability (see Table 4) of all latent variables, resulting in Cronbach’s alphas that were all well above 0.70 (Cronbach, 1951).

To confirm that all latent constructs were distinguishable from each other (discriminately valid), we employed the divergent validity criteria proposed by Fornell and Larcker (1981) and performed a robust assessment of the SEM constructs. As shown in Table 4, the divergent validity of the constructs in our model was confirmed, as the squared correlation value of each construct was less than its average variance extracted (AVE) value. In addition, all AVE values were above the threshold of 0.50 (Bagozzi & Yi, 1988; Fornell & Larcker, 1981).

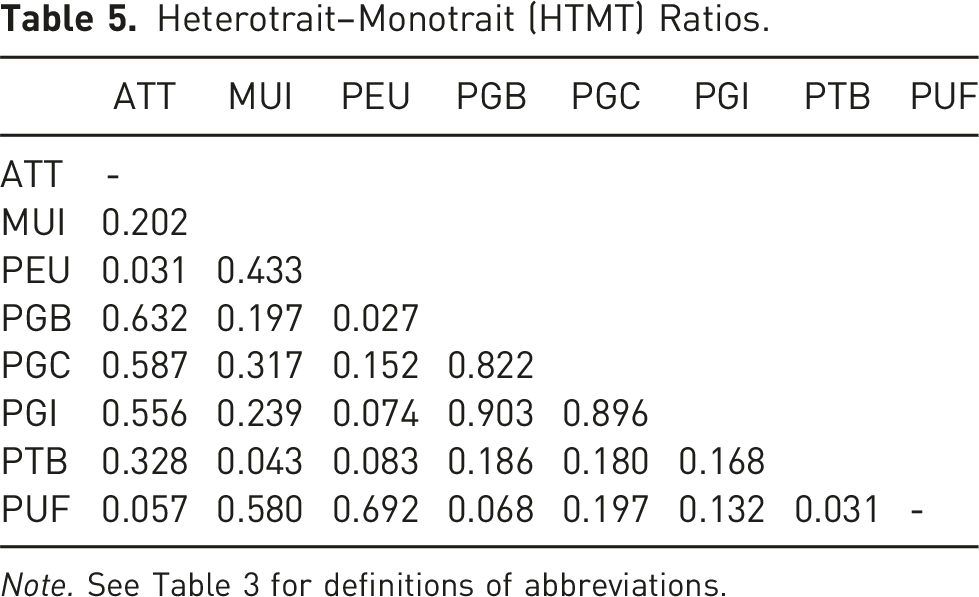

Heterotrait–Monotrait (HTMT) Ratios.

Note. See Table 3 for definitions of abbreviations.

Second-order Construct Assessment

As shown in Table 4, there are high correlations between perceived government competence, integrity, and benevolence, in line with trust theory (Gefen, 2002). Perceived government competence, integrity, and benevolence also have high VIF values >3 (0.6173, 9.091 and 5.556) and high HTMT ratios (0.903, 0.822 and 0.896), indicating excessive multicollinearity (García et al., 2015; Henseler et al., 2015; O’brien, 2007). These results confirm that perceived government competence, integrity and benevolence are three underlying dimensions of trust (Gefen, 2002; Hardin, 1991; Mayer et al., 1995) that need to be combined into a second-order construct (Bradley & Henseler, 2007; Chin et al., 2003), following best practices (García et al., 2015; O’brien, 2007).

Weights of the First-order Constructs on the Designated Second-order Construct.

Structural Model Assessment and Hypothesis Testing

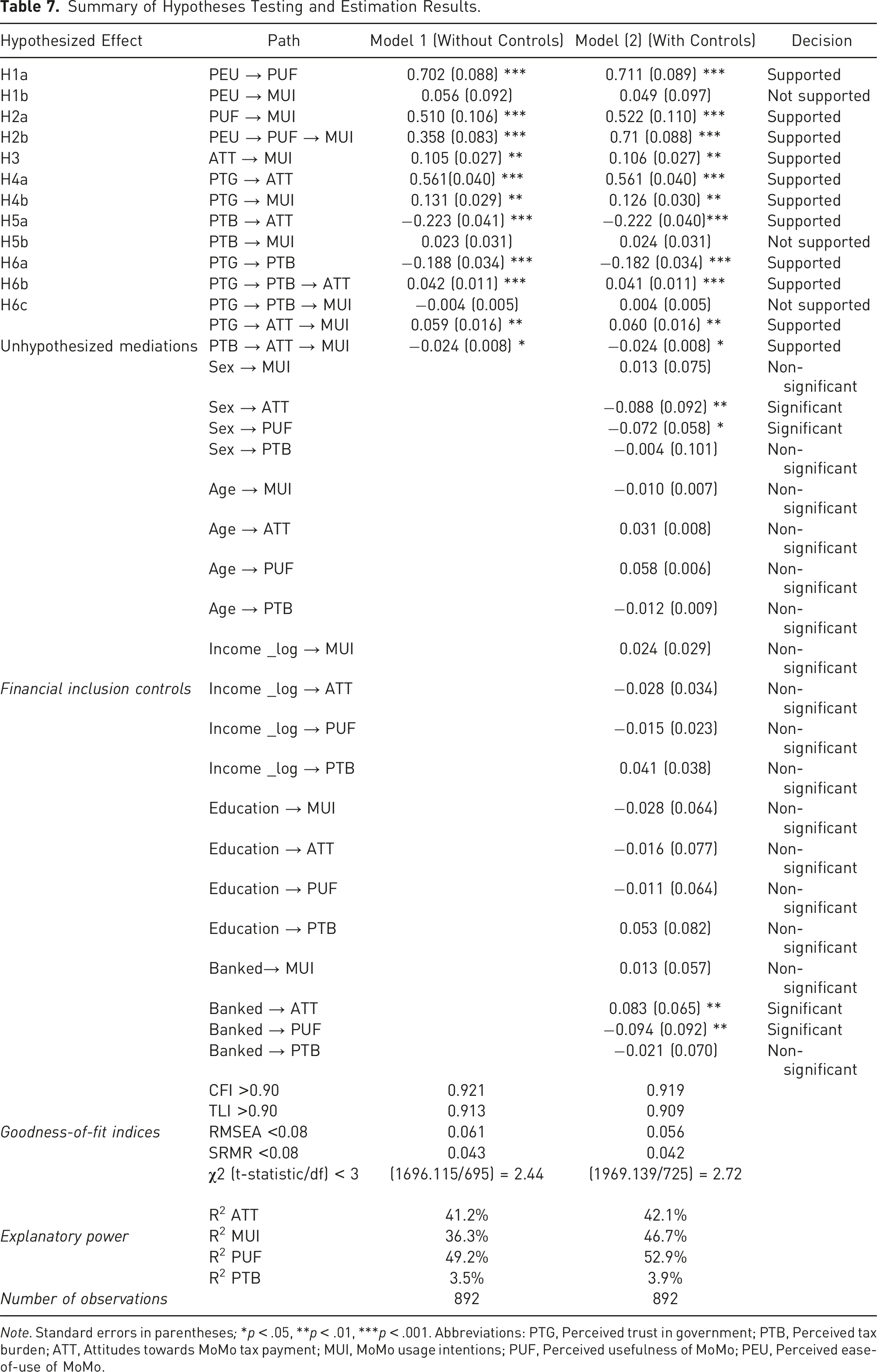

Summary of Hypotheses Testing and Estimation Results.

Note. Standard errors in parentheses; *p < .05, **p < .01, ***p < .001. Abbreviations: PTG, Perceived trust in government; PTB, Perceived tax burden; ATT, Attitudes towards MoMo tax payment; MUI, MoMo usage intentions; PUF, Perceived usefulness of MoMo; PEU, Perceived ease-of-use of MoMo.

Summary of overall results of structural model assessment.

First, our model explains 42.1% of attitudes toward MoMo tax payments; perceived trust in government has a positive and significant effect on attitudes toward MoMo tax payments, whereas perceived tax burden has a negative and a significant effect (supporting Hypotheses H4a and H5a, respectively). In addition, perceived tax burden significantly mediates the relationship between perceived trust in government and attitudes toward MoMo tax payments (supporting Hypothesis 6b).

Second, our model explains 46.7% of MoMo service use/tax payment intentions; perceived usefulness of MoMo services, attitude toward MoMo tax payments, and perceived trust in government all have positive and significant effects on this variable (supporting Hypotheses H2a, H3, and H4b, respectively). By contrast, perceived ease of use of MoMo services and perceived tax burden have no significant effects on MoMo service use/tax payment intentions (failing to support Hypotheses H1b and H5b, respectively). Nonetheless, perceived usefulness of MoMo services fully mediates the effect of perceived ease of use of MoMo services on MoMo services use/tax payment intentions (supporting Hypothesis H2b). We also find that perceived tax burden does not mediate the relationship between perceived trust in government and MoMo services use/tax payment intentions (failing to support Hypothesis H6c).

Third, our model explains 52.9% of perceived usefulness of MoMo services, which is positively and significantly affected by perceived ease of use of MoMo services (supporting Hypothesis H1a). Fourth, our model explains 3.9% of perceived tax burden, with a significant and negative effect of perceived trust in government (supporting Hypothesis 6a).

Finally, when examining the effect of financial inclusion controls, we find that the perceived usefulness of MoMo services and consequently attitudes toward MoMo tax payments are more positive among women than among men. In addition, respondents in regions with higher proportions of the banked population have lower perceptions of the usefulness of MoMo services but more favorable attitudes toward MoMo tax payments. The effects of the other controls are not significant.

Discussion

Overall, our findings capture the antecedents of attitudes toward MoMo tax payments and MoMo services use/tax payment intentions. We draw on TAM and extend it by examining the roles of perceived usefulness, perceived ease of use, attitude toward MoMo tax payments, trust in government and tax burden as instrumental factors predicting attitudes and intentions to use MoMo services amid the introduction of the MoMo tax.

First, among the two predictors of behavioral intentions from TAM (Davis et al., 1989), only perceived usefulness of MoMo services has a significant positive influence on MoMo service use/tax payment intentions. Perceived ease of use of MoMo services only influences such intentions indirectly through perceived usefulness of MoMo services. However, we find that the perceived usefulness of MoMo services is predicted by the perceived ease of use of these services. These findings align with those of prior studies (Akinyemi & Mushunje, 2020; Ofosu-Ampong, 2024) but also contradict prior findings on the relationship between ease of use and intentions reported by Tobbin and Kuwornu (2011) and Narteh et al. (2017). These studies found direct positive effects of ease of use on both usefulness and MoMo adoption intentions in Ghana (Tobbin & Kuwornu, 2011) and other selected African countries (Narteh et al., 2017). A meta-analysis of TAM (Yousafzai et al., 2007a, 2007b) and other studies outside the context of MoMo research (Baah-Peprah, 2023; Gefen & Straub, 2000; Keil et al., 1995) also confirm our findings.

The discrepancies between our findings and those of Tobbin and Kuwornu (2011) may be explained by changes in industry mechanisms since 2011, when there were limited (if any) MoMo usage experiences and the MoMo tax had not yet been introduced. Moreover, more than a decade of experience with MoMo technology may have dampened the importance of ease of use. Additionally, our sample is three times larger and more diverse than the sample in Tobbin and Kuwornu (2011)’s study, which targeted respondents at shopping malls (which are mostly visited by affluent people in Ghana). Our findings also contradict the recent work of Ofosu-Ampong (2024) possibly because our study sample is substantially larger than his and has wider national coverage across 16 regions and all walks of life. By contrast, Ofosu-Ampong sampled professionals (accounting and IT professionals), a group of people who may have little or no difficulty conducting MoMo transactions. Although Narteh et al.’s (2017) study also had a large sample, it was conducted before MoMo tax introduction. Here, unlike these prior studies (Narteh et al., 2017; Ofosu-Ampong, 2024; Tobbin & Kuwornu, 2011), use of MoMo in our study includes more than one task, where individuals need to consider intentions for both MoMo use and MoMo tax payment at the same time. This level of complexity may account for the opposing findings.

Second, the MoMo literature has underscored the relevance of MoMo services for enhancing the financial inclusion of underprivileged individuals, such as the less educated, women, older people, the unbanked and those with low incomes (Amoah et al., 2020; Della Peruta, 2018; Gai et al., 2018; Koomson et al., 2021; Narteh et al., 2017; Pobee et al., 2023; Senyo et al., 2022). The proportions of these groups that use MoMo services are significantly higher than those of their privileged counterparts, for example, the banked population. 8 Consequently, MoMo tax obligations may obscure the intentions of underprivileged groups to use MoMo services even if they have favorable MoMo tax payment attitudes. Nevertheless, this obscuration may not be strong enough to influence the effect of attitude on intentions (Ajzen, 1991). Here, we confirm that favorable attitudes toward MoMo tax payments is positively associated with MoMo services use/tax payment intentions. This finding is in line with the established predictions of TPB in explaining attitude and intention relationships in, for example, mobile service adoption behaviors (Gopi & Ramayah, 2007). It is also consistent with the literature on technological innovation adoption in other fields, including alternative finance technologies (Baah-Peprah et al., 2024; Shneor & Munim, 2019; Shneor et al., 2021), e-commerce technologies (Herrero Crespo & Rodríguez del Bosque, 2008; Pavlou, 2002), e-health treatment technologies (Rich et al., 2015), and e-tax systems (Taing & Chang, 2021).

Third, while trust in MoMo service providers and MoMo agents is critical in MoMo adoption intentions, the introduction of MoMo taxes has heightened the relevance of trust in another key stakeholder: the government. Although empirical explorations of this topic remain limited, the works of Tetteh et al. (2023), Amoah et al. (2023), and Anyidoho et al. (2023) confirmed a positive effect of government trust on MoMo adoption but measured trust using binary conditions of “yes or no” to a single statement such as “trust the government” (Amoah et al., 2023; Tetteh et al., 2023) or “misuse of collected taxes” (Anyidoho et al., 2023). Our study employed a multidimensional and hierarchical construct approach, which captures individuals’ trust in government with three ontological attributes of government: competence, integrity, and benevolence. Our empirical results confirm that trust in government positively impacts attitudes toward MoMo tax payments and MoMo services use/tax payment intentions. We also find that perceived tax burden significantly positively mediates the effect of trust in government on attitudes toward MoMo tax payments but not MoMo services use/tax payment intentions. These findings further strengthen earlier arguments that trust in government is a critical factor in MoMo usage (Amoah et al., 2023; Anyidoho et al., 2023; Tetteh et al., 2023) and favorable attitudes toward MoMo tax payments.

Finally, while some studies have reported a negative effect of Ghana’s MoMo tax on MoMo adoption (Anyidoho et al., 2023; Ofosu-Ampong, 2024; Takyi, 2024), a meta-analysis by Mpofu (2022) provided mixed evidence. These inconsistencies may be partially attributable to a stronger emphasis of these studies on the MoMo tax rate than on MoMo users’ perceptions of their tax burden. The current study finds that MoMo users’ perceptions of their tax burden are crucial for examining the implications of the MoMo tax, especially since individual tax responsibilities and MoMo taxes differ significantly across countries. Our model shows that individuals’ perceived current tax burden negatively affects their attitudes toward MoMo tax payments and influences the effects of these attitudes on their intentions to use MoMo services/pay the MoMo tax. These novel insights and the suggestion of items for measuring perceived tax burden are important contributions of this work and a divergence from prior work, which has solely examined the presence of the MoMo tax (Anyidoho et al., 2023; Bongomin et al., 2019; Mensah et al., 2022; Ndung’u, 2019; Pobee et al., 2023; Rojas-Suarez & Pacheco, 2017; Takyi, 2024).

Overall, our findings suggest that MoMo taxation represents a financial inclusion paradox. Specifically, even though the perceived current tax burden does not directly influence MoMo services use/tax payment intentions, it may jeopardize the intended benefits of MoMo services, such as financial inclusion, and its claim as a means of alternative funding, by negatively influencing users’ attitudes toward MoMo services. These attitudes may in turn negatively influence usage intentions, hence exerting an indirect rather than direct negative effect on intentions.

Finally, it may be worthwhile mentioning some insights emerging from effects of control variables as related to the role of MoMo in financial inclusion. Compared with men, women have higher perceptions of MoMo usefulness but lower attitudes toward MoMo tax payments. These findings indicate that MoMo services enhance the financial inclusion of females, who traditionally dominate financially excluded groups, especially in developing economies. However, taxing MoMo transactions negatively affects females’ attitudes toward using MoMo services. Similarly, although respondents from banked regions exhibit higher MoMo tax attitudes than respondents from unbanked regions, the latter have higher perceptions of the usefulness of MoMo services than the former. These findings further support our argument that taxing MoMo transactions is an alternative funding paradox or financial inclusion paradox. Females continue to face greater financial exclusion than males, 9 and our findings could be used to guide policymakers in addressing barriers to females’ financial inclusion.

Conclusion

MoMo is becoming an integral part of the banking system in developing countries. To understand the implications of taxing Momo transactions and inform public policy, research is needed to examines personal, behavioral and psychological factors in tandem with institutional factors, such as citizens’ trust in government. Such an approach provides a more comprehensive framework for understanding MoMo usage, extending insights from earlier literature that has focused solely on personal or behavioral factors while neglecting perceptions of relevant institutions.

This study investigates MoMo usage intentions amid the introduction of the MoMo tax in Ghana and the attitudes toward MoMo taxation. This is achieved through the outlining and testing of a conceptual framework integrating technology acceptance, perceived trust in government, and tax burden perceptions. By applying SEM analytical techniques to survey data from 892 individuals from across all 16 regions of Ghana, we analyzed five factors relevant to MoMo adoption and tax payment: perceived trust in government, perceived tax burden, attitudes toward MoMo taxation, and the two main behavioral components of the TAM (perceived usefulness and ease of use).

Our empirical results reveal two significant determinants of attitudes toward MoMo tax payments (i.e., perceived trust in government and perceived tax burden), one significant determinant of perceived tax burden (i.e., perceived trust in government), one significant determinant of perceived usefulness of MoMo services (i.e., perceived ease of use), and three significant determinants of MoMo service use/tax payment intentions (i.e., perceived trust in government, attitudes toward MoMo taxation, and perceived usefulness of MoMo services).

Practical and Policy Implications

Our findings provide insights that can inform the formulation of tax policies, especially for taxing transactions via alternative financing services that play a role in enhancing financial inclusion. Inappropriate timing of tax introduction might jeopardize the relevance of these tools for financial inclusion. Taxes should be introduced when trust in government seems positive, thus improving compliance attitudes and intentions while reducing perceived tax burden. From a national policy standpoint, a country-level assessment of individuals’ trust in government may be relevant before making decisions on tax introduction. Here, to help mitigate some public concerns, governments may publish the achievements made thanks to taxes collected, such information may also be possible to convey digitally to digital taxpayers, which may both enhance trust in government and positive attitudes towards tax payment.

In addition, the findings on perceived usefulness and ease of use of MoMo services suggest that MoMo service providers should pay attention to improving the relevance of their technology and reducing user-related efforts. Including additional services such as loan facilities and credit scores while reducing the user effort needed to complete transactions is key to ensuring individuals’ continued use of MoMo services amid tax obligations. The addition of such services may enhance financial inclusion by acting as points of entry into the mainstream financing sector. For example, credit scores could be used to assess an individual’s creditworthiness when seeking traditional sources of funding, such as bank loans, rather than imposing collateral requirements. Given the effects of perceived tax burden, ease of use and usefulness observed in this study, it would be beneficial if tax policies on MoMo services allow deduction of interest paid on loans (loans taken from MoMo service providers by individuals) from MoMo tax obligations.

Theoretical Implications

This study has several theoretical implications. First, our integrated model extends the determinants of attitudes toward MoMo taxation and MoMo services use/tax payment intentions by including multidimensional government trust components. In doing so, this study provides a comprehensive understanding of the nuanced relationships between governance tax systems and fintech adoption broadly, and MoMo technology more specifically. Although prior work has established the relevance of individual theories for MoMo adoption, this study is the first to suggest an integration of several theories.

Second, we confirm that although taxing transactions via fintech services that promote financial inclusion, such as MoMo services, may represent an attractive source of government revenue (Mpofu, 2022), such taxation also represents a paradox thanks to its adverse effects on financial inclusion. Here, such taxation may jeopardize the benefits of MoMo services for financial inclusion, particularly among females, who exhibit higher perceptions of MoMo usefulness but less favorable attitudes towards MoMo tax payments than males. These findings contribute to the ongoing theoretical discussion on the implications of MoMo taxation broadly, and with respect to gender differences in financial inclusion. Furthermore, our findings that tax burden directly influences attitudes toward MoMo tax payments and indirectly influences MoMo services use/tax payment intentions are novel and further enhances the understanding of digital taxation payment intentions.

Third, this study contributes to an emerging stream of the literature that focuses on the impact of trust in government on FinTech services’ adoption, and MoMo service adoption as part of it. Trust is both a highly subjective psychological construct and ontologically attributable to one’s perceptions of the competence, integrity, and benevolence of others (Gefen, 2002; Mayer et al., 1995). Despite this complexity, the prior literature has examined MoMo users’ trust using binary measurements (Amoah et al., 2023; Anyidoho et al., 2023; Tetteh et al., 2023). The present study is the first to examine MoMo users’ perceived trust in government while fully anchoring its measurement in all the ontological attributes underlying the concept as suggested by trust theory.

Limitations and Directions for Research

While this study presents interesting insights and complements the theoretical arsenal for explaining attitudes and behavioral intentions in fintech adoption, it also has certain limitations that provide directions for future research.

First, although our study is based on a large sample covering all regions of the study context (Ghana), the generalizability of the findings beyond Ghana is limited. Studies in different national contexts are needed to validate the applicability of our theoretically integrated and extended model in explaining MoMo tax attitudes and MoMo services use/tax payment intentions. Comparative analyses of MoMo tax regimes that differ in terms of MoMo infrastructural environments, cultural contexts, and government trust levels would be particularly valuable. Similarly, future studies could compare countries with different levels of economic development while capturing various levels of channels of access to finance to determine whether MoMo is an “improvement-driven” fintech tool or a “necessity-driven” fintech tool.

Second, research on the adoption of mobile services has revealed that incorporating behavioral theories (such as TPB) in addition to traditional information system theories significantly enhances the understanding of mobile service adoption behaviors (Gopi & Ramayah, 2007). In addition, various versions of information systems theories, such as TAM2 (Venkatesh & Davis, 2000), propose relevant relationships between specific TAM and TPB variables, which have been validated for other alternative finance platforms (Baah-Peprah, 2023) and mobile banking services (Amoah et al., 2020). TPB has proved to be a strong theoretical lens for explaining tax-related compliance intentions and can be used to improve tax-related systems (Taing & Chang, 2021). It would be valuable to employ the full TPB as an alternative theoretical framework while complementing the effects of attitudes with those of subjective norms and perceived behavior control as prescribed by the theory.

Third, although our survey data were collected immediately after the introduction of the MoMo tax, and hence represents data from a unique point in time for assessing attitudes toward MoMo taxation and intentions toward continued MoMo usage, future studies may present longitudinal data based on changes in relevant policies, and following longer experience with such taxation.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.