Abstract

Australia stands to benefit from the current global security–sustainability nexus, or the convergence of Western actions to meet both security and sustainability objectives, which are centred around the supply of critical raw materials (CRM). Australia is the largest producer of lithium, the third largest producer of cobalt, and the fourth largest producer of rare earth elements resources in the world. However, Australia’s realist pragmatic response to increasing tensions between the United States and China over CRM, which is exacerbating the trend towards resource nationalism, does not provide assurance for its national security. The article examines Australia’s resource liberalism which has embedded CRM mining companies and exports in Chinese dominated global supply chains. Despite limited efforts to emulate the great powers in industrial policy and enthusiasm for joining Western-led agreements, these do not protect Australia from great power rivalry, nor does its resource liberal orientation through open investments, CRM exports, and partnerships ensure its national security.

Keywords

Introduction

In 2024, global temperatures breached the 1.5° average above pre-industrial levels for the first time (Tollefson, 2025). Based on current mitigation strategies and actions, we are on track to limit global warming to 3.1° this century (United Nations Environment Programme [UNEP], 2024), which is well beyond the safe limits for humanity. The impacts of climate change on human security are uncontested (Ide, 2023; McDonald, 2021a; Swain et al., 2023). Some scholars now articulate the need for planetary security to facilitate global adaptation and mitigation for securing human habitation (Dalby, 2024; McDonald, 2021b). Traditional concepts of state-based security regarding threats and the use of force have not easily incorporated a changing climate, although the threats posed to national security and international stability are now recognised (McDonald, 2024, p. 314). In articulating how Australia’s ‘realist pragmatic’ position in the global security–sustainability nexus leaves it (economically) vulnerable we follow Ide’s (2023) expansive definition of national security as ‘the ability to preserve the nation’s physical integrity and territory; to maintain its economic relations with the rest of the world on reasonable terms; to preserve its nature, institutions and governance from disruption from outside; and to control its borders’ (p. 28). At present, state actions to reign in greenhouse gas emissions remain insufficient (UNEP, 2024), with the only positive change being the rapid uptake of renewable energy, with solar PV, wind energy, and lithium-ion batteries driving the shift to electrify energy systems and electric vehicles (EVs; Intergovernmental Panel on Climate Change, 2023). The energy transition is however both more mineral and energy-intensive, relying on critical raw materials (CRM) for renewable technologies (International Energy Agency [IEA], 2021; Kramarz et al., 2021). 1

Traditional national security concerns over accessing CRM have proliferated. CRM are generally defined as metals and minerals that currently have no viable substitutes and have a high supply risk given import dependence and vulnerabilities to supply disruptions (emphasis added; Hotchkiss et al., 2024; Vivoda & Matthews, 2024). 2 They are essential for the energy transition, as well as defence, space, agritech, communications, computing, medicine, and other emerging high-tech industries (Australian Government, 2023a; Bazilian et al., 2023; Kalantzakos, 2020; Nakano, 2021; Vivoda et al., 2024). On 10 October 2025, China expanded export controls on rare earth elements (REE), of which it has a near monopoly, including holmium, erbium, thulium, europium, and ytterbium, bringing the number of restricted REE to 12 (of 17; Reuters, 2025a). This came after China restricted trade in seven ‘heavy’ REE and permanent magnets in April, requiring exporters to have a special export licence and restricting those able to trade in CRM for dual use. 3 Such actions were a retaliation to U.S. President Trump’s pronounced ‘liberation day’ tariffs. Earlier, in February, China targeted export controls on CRM including tungsten, tellurium, bismuth, molybdenum, and indium in response to the United States’ imposition of 10% tariffs on Chinese imports, in a slow boiling trade war between the two states that began in 2018 (Moritsugu & Wu, 2025). This ratchets up the global race to secure CRM because many minerals like REE are also ‘strategic’ minerals that states consider vital for their national security (IEA, 2021, 2022; Johnson et al., 2025), particularly for modern weapons systems and defence capabilities such as aircraft, submarines, and unmanned aerial vehicles (Bazilian et al., 2023; Lopez, 2024; Nakano, 2021). 4 China’s actions also mimic U.S. restrictions on Chinese companies accessing semiconductor technology, which is vital for the fourth industrial revolution and central to U.S.-China strategic competition (discussed further below, Reuters, 2025a).

Geopolitical tensions amidst a climate crisis fits what Thea Riofrancos (2023) calls the security–sustainability nexus, where the demand for CRM meets states’ environmental and national security objectives. Australia is a beneficiary of growing international CRM demand and is seeking to take advantage of its natural endowments (Mudd et al., 2024). It is the world’s largest exporter of lithium, the third largest producer of cobalt, and the fourth largest producer of REE resources. Despite this, outside of political commentators (Coyne & Campbell, 2023; Zhang et al., 2024), little is written on Australia’s geostrategic position in a changing global security-sustainability landscape (c.f. Vivoda & Matthews, 2024; Vivoda et al., 2024; for political economy perspectives see Coe et al., 2025; Wijaya & Hayes, 2025; Wijaya & Jayasuriya, 2024, 2025).

This article fills the gap on the national security implications of Australia’s aim to supply CRM to its irreplaceable security ally the United States, and to ‘like-minded states’ (Ali et al., 2022), while remaining enmeshed in CRM supply chains dominated by China (Hayes et al., 2025). It argues that Australia’s ‘realist pragmatic’ geopolitical position makes it vulnerable, especially given its commitment to resource liberalism and economic interdependence in an era of great power rivalry. This is a qualitative case study of Australia’s positioning in the security–sustainability nexus (Potter, 2017). Australian foreign policy has often relied on ‘descriptive methods to produce historical narratives, arenas for popular debates or theoretical accounts’ (O’Keefe, 2023, p. 1). Here, we use document analysis of primary sources, including government reports, defence reports and strategies, and newspaper articles, backed by secondary sources including the grey literature, to demonstrate inconsistency between, and therefore vulnerability in, Australia’s international geopolitical and economic orientations. The government documents are reports produced by the Australian government to identify national security threats including climate change, and the policy tools they promote to respond to CRM demand.

The article proceeds in five parts. First, the argument is made that Australia’s realist pragmatic foreign policy is shaping its geopolitical response to the race for CRM, which is conceptualised in the second section as the global security–sustainability nexus. Third, the article documents the strategies used by states including resource nationalism for achieving their objectives. Section ‘Australia’s National Security and Resource Liberalism’ then examines how Australia has, despite replicating some industrial policies established elsewhere, nevertheless retained its resource liberal stance and economic openness within a rapidly changing international landscape. Section ‘Challenges for Australia’s National Security in the Global Security-Sustainability Nexus’ then details how these activities do not necessarily meet Australia’s national security needs given that foreign owned companies dominate Australian mining, and CRM companies are enmeshed in Chinese dominated global supply chains (Hayes et al., 2025). This leaves Australia particularly vulnerable to the changing relations between the great powers. Section ‘Conclusion’ concludes.

Australia’s Realist Pragmatism and Geopolitical Positioning

Australian foreign policy has generally been described as ‘realist pragmatism alongside a ‘middle power’ identity often underpinned by progressive ideals’ (Abbondanza, 2021; Bisley et al., 2022). The realist tradition framing Australia’s engagement with the world has three pillars: a preoccupation with Australia’s specific geographic place in the world, a systemic pessimism about global stability, and pragmatism focused on ‘understanding the essential attributes of the situation itself, rather than using the situation to inquire into the general nature of the international system’ (Wesley, 2009, p. 324). This stems from both policymaking and knowledge generation in Australia on international relations and foreign policy. We argue this continues in relation to Australia’s political but not economic positioning in the global security–sustainability nexus (the latter is detailed below), contributing to what Jayasuriya (2021) calls ‘geopolitical festishism’. Despite arguments for Australia to engage in ‘progressive realism’ to better respond to climate change (Bisley et al., 2022), Australian foreign policy is dominated by ‘inertia and path dependency in foreign policy’ with a highly militarised strategic culture (Beeson et al., 2025; O’Keefe, 2023, pp. 2–3). Throughout its history, Australia has ‘tied itself to “great and powerful friends”’, originally the United Kingdom, then the United States, as a means of ensuring its security (Rees, 2024, p. 91). Scholars recognise this orientation as being driven by ‘exaggerated threat perceptions’ from the region (O’Keefe, 2023, p. 25) and a ‘fear of abandonment’ (Gyngell, 2017; He & Feng, 2024). This fear has been exacerbated by China’s rise, concerns of U.S. disengagement in the region, and nativist policies under the Trump administration (Rees, 2024). 5

In 2021, Australia ‘revolutionised’ its defence positioning by signing the ‘AUKUS’ trilateral security partnership with the United Kingdom and United States (Beeson et al., 2025), to ‘develop and transfer military capabilities’ for ‘integrated deterrence’ within the region. Comprised of two pillars, with Australia committing $368 billion to receive eight nuclear powered submarines under pillar 1 from the United States by the 2040s (Broinowski, 2024). Pillar 1 has already come under critical scrutiny over the viability and practicality of the agreement (Rees, 2024), even before the U.S. government decided to review, and then recommit, to the agreement (Reuters, 2025c). Pillar 2 ‘serves as a platform for advanced technology cooperation’ (Broinowski, 2024) with scholars concerned that the agreement gives the United States unparalleled access to sensitive Australian information and territory with little guarantee in return, undermining the very state sovereignty that the agreement is designed to protect (Beeson et al., 2025).

Under pillar 2, Australia seeks to work with its allies and partners on reducing China’s lead in dual-use technologies, many of which depend on critical minerals (Broinowski, 2024). There is little public information about how critical minerals will feed into pillar 2, leading former Australian defence minister Beazley (2024) to argue that critical minerals need to have its own pillar, driven by Australia, to secure its national interest. Indeed, there is relatively little reference of the strategic role critical minerals will play in either the 2023 National Defence Strategic Review or the 2024 National Defence Strategy, although the 2023 Critical Minerals Strategy identifies the importance of critical minerals in national defence and economic security. Again, not much detail is provided.

In October 2025, Australia and the United States signed a ‘Framework for Securing of Supply in the Mining and Processing of Critical Minerals and Rare Earths’ (Australian Government, 2025a). This includes ‘outlining mechanisms for project financing, potential price floor arrangements, and coordination on downstream processing and off-take agreements’ (Wijaya & Jayasuriya, 2025, p. 1) beginning with approximately $1 billion each committed to specific CRM mining projects in Australia within 6 months, with an $8.5 billion project pipeline projected (Australian Government, 2025b). This builds on the 2023 ‘Australia-United States Climate, Critical Minerals and Clean Energy Transformation Compact’, which includes aims to diversify and expand clean energy supply chains and establish a ‘responsible, sustainable, and stable supply of critical minerals’ (Australian Government, 2023c).

For Wijaya and Hayes (2024) and Wijaya and Jayasuriya (2024, 2025), these agreements are evidence of an interlocking technology-mining-energy complex within a ‘militarised neoliberalism’ where advanced technologies and defence capabilities are geared towards mining for the extraction of surplus on a transnational scale. While they state that this departs from the security–sustainability nexus, how this is so is not specified (Wijaya & Jayasuriya, 2025, p. 4). 6 Although the United States may be undermining the rules-based order, particularly in relation to free trade, it has always operated to advance (private sector) innovation through national security (Weiss, 2014). The following section outlines the global security–sustainability nexus, or where (most) states’ environmental and national security objectives dovetail, before detailing how states are seeking to obtain CRM via resource nationalism through industrial and sustainability policies, and the mismatch between Australia’s geopolitical positioning and its open economic orientation.

The Global Security–Sustainability Nexus

The transition away from fossil fuels towards renewable energy presents an opportunity for all states to increase their energy security by becoming independent from conventional energy suppliers (International Renewable Energy Agency [IRENA], 2019a). However, such a shift entails a significant increase in the use of CRM, whose mineral deposits are often more site-specific than fossil fuels (Carr-Wilson et al., 2024) and may depend on (few) states with refining and processing capability (IEA, 2025). The World Bank has estimated that more than 3 billion tonnes of minerals and metals will be required for renewable energy and storage technologies by mid-century. This includes a more than 450% increase in demand beyond 2018 production levels for graphite, lithium, and cobalt, a more than 200% increase for indium and vanadium, and around a 100% increase in demand for nickel (Hund et al., 2020, p. 73). 7

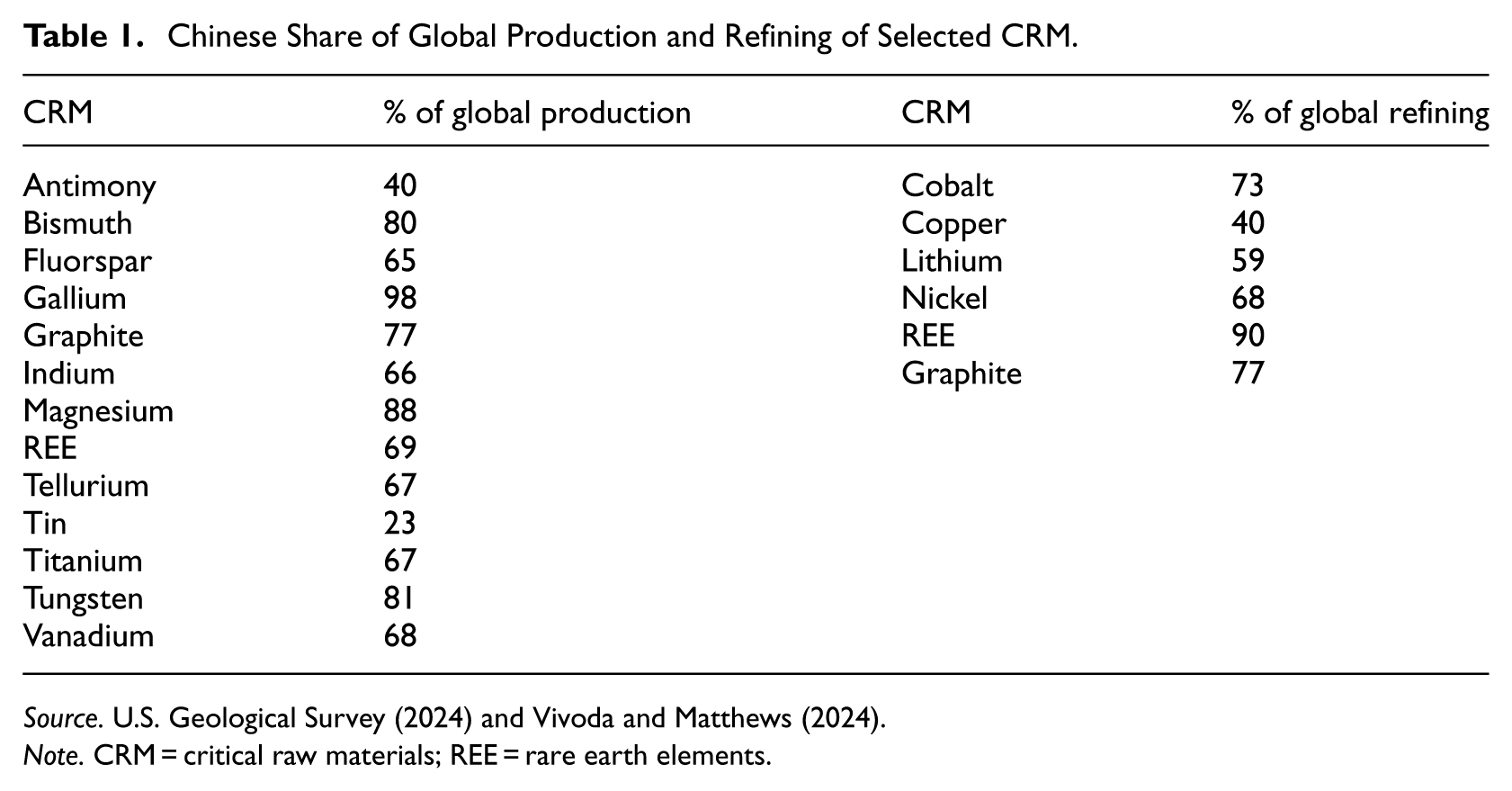

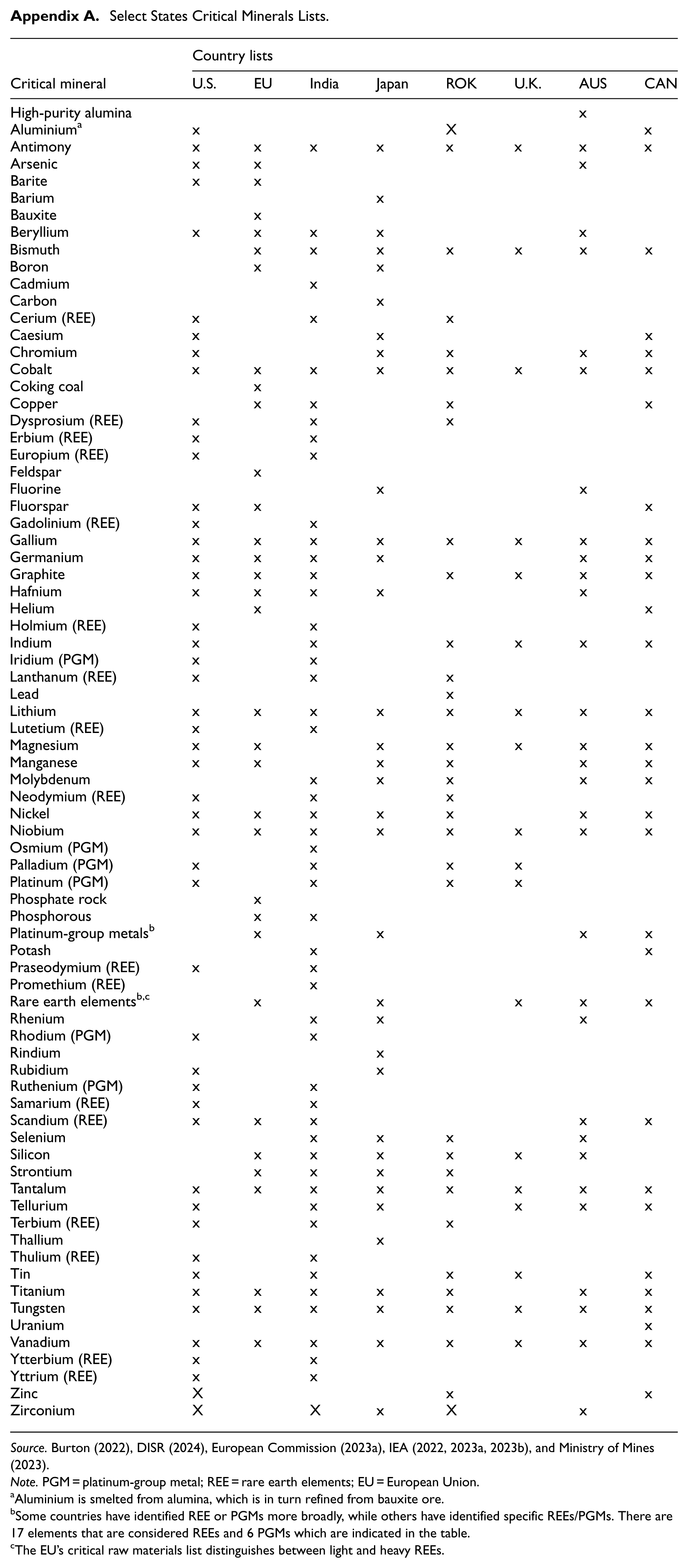

As outlined earlier, the demand for CRM is now a national security concern for many states; most notably the United States (Vivoda et al., 2025), the European Union (EU; Ali et al., 2022; Franks et al., 2025), and Japan (Lee & Kawaguchi, 2025). The EU, and states including the United States, Japan, India, Korea, Canada, and Australia each have their own critical minerals list, with scholars identifying more than 50 CRM that appear across different states’ lists, including lithium, copper, cobalt, graphite, nickel, platinum-group elements, and REE (Carr-Wilson et al., 2024; see Appendix A). 8 As demonstrated in Table 1, China dominates the production of many CRM, including gallium, magnesium, and tungsten; and it also dominates the processing of REE, copper, cobalt, nickel, lithium, and graphite.

Chinese Share of Global Production and Refining of Selected CRM.

Source. U.S. Geological Survey (2024) and Vivoda and Matthews (2024).

Note. CRM = critical raw materials; REE = rare earth elements.

The United States relies on China for 26 of the 50 CRM it listed as critical in 2022 (Burton, 2022) 9 ; while the EU’s reliance on China is even more pronounced (Vivoda, 2023). This has led to growing concerns that China could leverage its position in supply chains for geopolitical purposes as a form of ‘weaponised interdependence’ (Farrell & Newman, 2019; Johnson et al., 2024; Kalantzakos, 2020; Vivoda & Matthews, 2024).

Scholars have argued that China’s dominance of CRM mining, refining, and processing demonstrates the importance of geopolitics and Chinese statecraft (Kalantzakos, 2020) for its own energy security (Sun & Ji, 2025); probed the concept and practice of ‘friend-shoring’ (Vivoda & Matthews, 2024) and the Minerals Security Partnership (MSP) as a Western response to China (Vivoda, 2023); highlighted the limitations of international trade law (Cotula, 2023–2024); and examined the possibility of emerging geopolitical trade blocs (Vivoda et al., 2024). Riofrancos (2023) more comprehensively captures this, labelling the West’s response to Chinese dominance as a security–sustainability nexus, where the West uses an ‘interlocking set of policies and justifications’ for promoting the extraction of CRM in the Global North including resource nationalism (detailed further below), while emphasising their environmental credentials in mining (p. 20). 10 In other words, Western states are now employing a range of strategies to ‘de-risk’ and reorient their supply chains from an (over)reliance on China (Coe et al., 2025; Gabor, 2021; Nakano, 2021) to meet national security concerns around decarbonisation, energy access (via CRM supply chains), economic dominance (of semiconductors, for example), and military preparedness (advanced weaponry and military systems). 11 The following section details state’s activities within the global security–sustainability nexus to help show how Australia’s realist pragmatism within the global security–sustainability nexus may undermine its national security.

The Global Security–Sustainability Nexus in Practice

Strategies used by the West to overcome Chinese dominance in CRM extraction, refining, and processing include contesting China’s CRM restrictions in the World Trade Organization (WTO), while advancing their own ‘resource nationalism’ through promoting domestic and international industrial and sustainability policies to build up domestic supply (via ‘on-shoring’ or ‘re-shoring’); seeking alternative supplies of critical minerals from allies or like-minded countries and encouraging re-regionalisation (‘friend-shoring’ and ‘near-shoring’); and engaging in bi- and multilateral agreements to diversify their supply chains (Ali et al., 2022; Vivoda, 2023). Resource nationalism refers to a wide range of policies, policy instruments, and activities ‘through which the state seeks to enhance its influence over the development of the resource sector’ (Haslam & Heidrich, 2016, p. 1). The concept of resource nationalism has evolved over time (Obaya, 2021), but broadly speaking, it entails directing ‘economic activity in the mining and energy sectors towards politically defined national goals’ (Wilson, 2015, p. 399) and is increasingly widespread (Johnson et al., 2024).

Examples of resource nationalist approaches include full or partial nationalisation, partial equity stakes or public private partnerships, the establishment of state-owned enterprises, changes in royalites and taxation, and making changes to property rights and approval processes (Haslam & Heidrich, 2016, p. 2). As Wilson (2015) observes, resource nationalist approaches will be ‘conditioned’ by existing political and institutional arrangements, thereby giving them a path dependent character (see also Kaup, 2010). Recognising this, states with liberal economies will often favour market-based solutions (e.g. taxation) in contrast to ‘statist’ forms of resource nationalism seen elsewhere. Wijaya and Jayasuriya (2025) do not think states’ actions constitute resource nationalism (, p. 6) but do not elaborate why. These strategies invoked by the United States and Europe are briefly discussed before situating Australia within this changing landscape. 12

First, trade conflicts over CRM are already evident. Tensions can be traced back to 2010 when China restricted exports of REE to Japan purportedly to manage its environmental impact (Liu et al., 2016). The restriction was widely seen in the West as a response to the territorial dispute over the Senkaku/Diaoyu Islands in the East China Sea and the detention of a Chinese fishing boat captain (Franks et al., 2025; Gholz & Hughes, 2021; Kalantzakos, 2020). REE prices then spiked following the incident, which led to concerns about supply chain concentration and resource dependence (Eggert et al., 2016). The United States, among others, took China to the WTO’s dispute settlement mechanism over the export restrictions of REE, tungsten, and molybdenum (DS431), who was found to have engaged in non-competitive behaviour. Additional dispute consultations in the WTO include the EU, Mexico, and the United States against China’s export restrictions on bauxite, coke, fluorspar, magnesium, manganese, silicon carbide, silicon metal, phosphorous, and zinc in 2009; the EU and United States against Chinese restrictions over antimony, chromium, cobalt, copper, graphite, indium, lead, magnesia, talc, tantalum, and tin in 2016; and the EU against Indonesia over nickel, coal, iron ore, and chromium in 2019 (IRENA, 2023).

Once the U.S.-China trade war began, President Xi Jinping’s visit to a REE processing facility in Jiangxi was viewed by the United States a message of Chinese dominance. In 2020, Xi emphasised the need to increase the world’s dependence on China to ‘develop powerful retaliation and deterrence capabilities against supply cut-offs by foreign parties’ (as cited in Nakano, 2021, p. 2). In 2021, China expanded export controls on magnesium, tungsten, and graphite to limit the supply of minerals used in electronics, weapons, and other defence technologies. In 2022, the U.S. passed the CHIPS Act prohibiting funding recipients from expanding semiconductor manufacturing in China and countries defined by U.S. law as posing a national security threat. In response, China restricted exports of antimony, gallium, and germanium, reinforcing the vulnerability of the global supply chain (Glencross, 2024; Lv & Munroe, 2024). As noted earlier, in 2025 U.S.’ tariffs have contributed to China invoking further CRM export restrictions.

Second, competition over CRM has ushered in a return to resource nationalism through overlapping and in some cases interlocking inward (domestic) and outward (international) industrial and sustainability policies. Inward or domestically focused industrial policy includes the U.S.’ Inflation Reduction Act (IRA, U.S. Government, 2022), the EU’s Critical Raw Materials Act (CRMA, 2024/1252), and the Australian Future Made in Australia Act (FMIA, Australian Government, 2024a, detailed in the next section). This is most evident in the United States, where the IRA aimed to spur a national EV market through tax credits, stipulating that 80% of critical minerals in batteries are extracted or processed by the United States or states with a free trade agreement with the United States (Trost & Dunn, 2023). 13 This stipulation aimed to ensure that tax credits would not benefit companies with investments from ‘foreign entities of concern’ (FEOC) such as China (Rappeport, 2023; U.S. Senate Committee on Energy and Natural Resources, 2022).

Soon after this was announced, the EU and Korea both considered taking the United States to the WTO over breaching foreign product discrimination rules (Jung, 2022; Yonhap, 2022). U.S. efforts to ensure that critical minerals for EVs were not sourced from FEOC led to widespread lobbying by EV firms, leading to a delay of critical mineral sourcing and processing rules until March 2023 (Oh, 2023). EV firms operating in the United States are seeking to increase the number of states on the critical minerals suppliers list (Choi, 2023). Additionally, the Trump administration has begun negotiating partial equity stakes deals in CRM companies to support domestic capacity (Nair, 2025).

U.S. efforts to rebuild domestic capacity and diversify supply chains have increased since China’s 2010 REE embargo, albeit to limited effect (Nakano, 2021). Both the Trump and Biden administrations signed executive orders to develop national manufacturing capacity and reduce supply chain vulnerabilities (Nakano, 2021; Vivoda, 2023), while the Defence Production Act (DPA; U.S. Government, 1950) has been invoked to allow the president to direct businesses to prioritise production on national security grounds to bolster industry (Vivoda & Matthews, 2024). 14 More recently, provocative statements by the United States on buying or taking Greenland and establishing a special envoy for Greenland (Aikman, 2025; Madhani, 2025), and Russia’s offer to make a deal with the United States over Ukrainian critical minerals, raise the stakes for accessing CRM for American national security (Korolov, 2025).

Interlocking inward industrial and sustainability policies are also evident in the EU. As part of efforts to reduce existing dependencies and diversify CRM supply chains, the EU’s Act sets annual benchmarks for domestic capacity for the extraction, processing, and recycling of CRM, which it aims to achieve by 2030. This includes targets of at least 10% of EU annual consumption for extraction; at least 40% of EU annual consumption for processing; at least 25% of EU annual consumption for recycling; and a cap of 65% on EU annual consumption from a single third country (European Commission, 2024). Targets for recycling are intended to further develop the EU’s stated intention of moving towards a circular economy. The Act also forms part of the EU’s Green Deal Industrial Plan, which aims to increase the competitiveness of the net zero industry in Europe, while also recognising the need for open trade for resilient supply chains (European Commission, 2023b).

Similar to United States efforts to increase self-sufficiency and supply chain resilience are evident in Europe, for example, with the European Commission’s Strategic Foresight Report 2022 (European Commission, 2022; Glencross, 2024; Vivoda & Matthews, 2024). Concern about supply chain resilience and market distortions are now coupled with commitments to achieve net zero by 2050 and align with the EU’s 2019 Green Deal and moves towards a circular economy (Nakano, 2021). As Glencross (2024) observes, the EU’s position on CRM security has shifted from initially promoting trade liberalisation and the creation of a ‘level playing field’ via enforcing international trade rules (e.g. through the WTO) to address supply chain distortions. There is now a greater focus on building supply chain resilience and diversification to reduce supply chain dependency (Glencross, 2024), although the European Commission does not explicitly single out Chinese competition as the United States does (Nakano, 2021, p. 18). 15

Outward focused or extra-territorial sustainability policies are also being invoked by the West to mitigate the environmental and social impacts of CRM supply chains. Current efforts by the EU through its Corporate Sustainable Due Diligence Directive (2024/1760) and Waste and Battery Waste Directive (2023/1542), and the United States formerly with its Dodd Frank Act (2010) legislation have also sought ways to place restrictions on the import of CRM that do not meet environmental and human rights standards (Park et al., 2024), while Australia seeks to advance itself as a leader on environmental, social, and governance (ESG) issues at the beginning of the CRM supply chain (Australian Government, 2023a; Sinclair & Coe, 2024; see below). As discussed in the following section, Australia’s foray into industrial policy and its sustainability settings have not markedly impacted its liberal approach to resources.

Finally, the West is engaging in outward focused or international efforts to ‘friend-shore’ global supply chains to allies for extracting and processing CRM. Friend-shoring refers to ‘a strategy where countries with shared values or interests, not limited to liberal democracy and respect for human rights, collaboratively harmonise policies to motivate companies to establish and sustain supply chains’ (Vivoda & Matthews, 2024, p. 466). This is exemplified by the MSP established in mid-2022, which includes the United States, the EU, Australia, the United Kingdom, Canada, Finland, Germany, Sweden, France, Japan, and South Korea as founding members (Vivoda, 2023). The prominence of Western countries and their allies has led the MSP to be dubbed the ‘metallic NATO’ (Vivoda & Matthews, 2024). This strategic alignment with allies and like-minded partners is not only about reducing vulnerabilities in mineral supply chains through diversification but also aims to address geopolitical, economic, and environmental objectives, and provide one avenue to rebuild manufacturing capabilities (Vivoda & Matthews, 2024).

Friend-shoring has been criticised as a form of increased protectionism (see Vivoda & Matthews, 2024), with the potential for Chinese countermeasures (Organisation for Economic Co-operation and Development, 2023). However, there is arguably already a trend towards greater protectionism, as exemplified by the above-mentioned trade disputes. This protectionist trend is seemingly underway via resource nationalism particularly in the Global South including Chile, Bolivia, Mexico, and Indonesia (IRENA, 2023; Nem Singh, 2023; Vivoda, 2023). Friend-shoring is further criticised for potentially creating trade bottlenecks and price increases associated with a greater reliance on selective nations and relocating manufacturing activities (e.g. Mills, 2022), in addition to the (re)emergence of distinctive trade blocs, which would negatively impact economic growth and decarbonisation. The WTO, for example, has previously warned that the world dividing into two trade blocs could reduce global GDP by 5% (World Trade Organization, 2022). However, as Vivoda and Matthews (2024) argue, friend-shoring is aimed at supply chain diversification, and could reduce bottlenecks and the prospect of volatile trade disputes due to less vulnerability to economic coercion.

There has also been a move towards re-regionalisation or ‘near-shoring’ which Ali et al. (2022, p. 15285) consider a ‘hybrid form of industrial relocation’ across several countries. Currently, membership of the MSP is essentially strategic and could push the world closer towards ‘two polarised spheres of influence’ (Vivoda, 2023, p. 3). Inclusion of others, particularly outside the OECD, remains an open question, as many developing countries are in China and/or Russia’s sphere of influence through their own CRM contracts, the Belt and Road Initiative, or through BRICS+ (Vivoda et al., 2024). Wang and Sun (2021) argue that a trend towards localisation and regionalisation has been evident since the 2008 global financial crisis and has in part been spurred on by the increasingly competitive relationship between China and the United States. How Australia promotes CRM exports and protects its national security within the global security–sustainability nexus is discussed next.

Australia’s National Security and Resource Liberalism

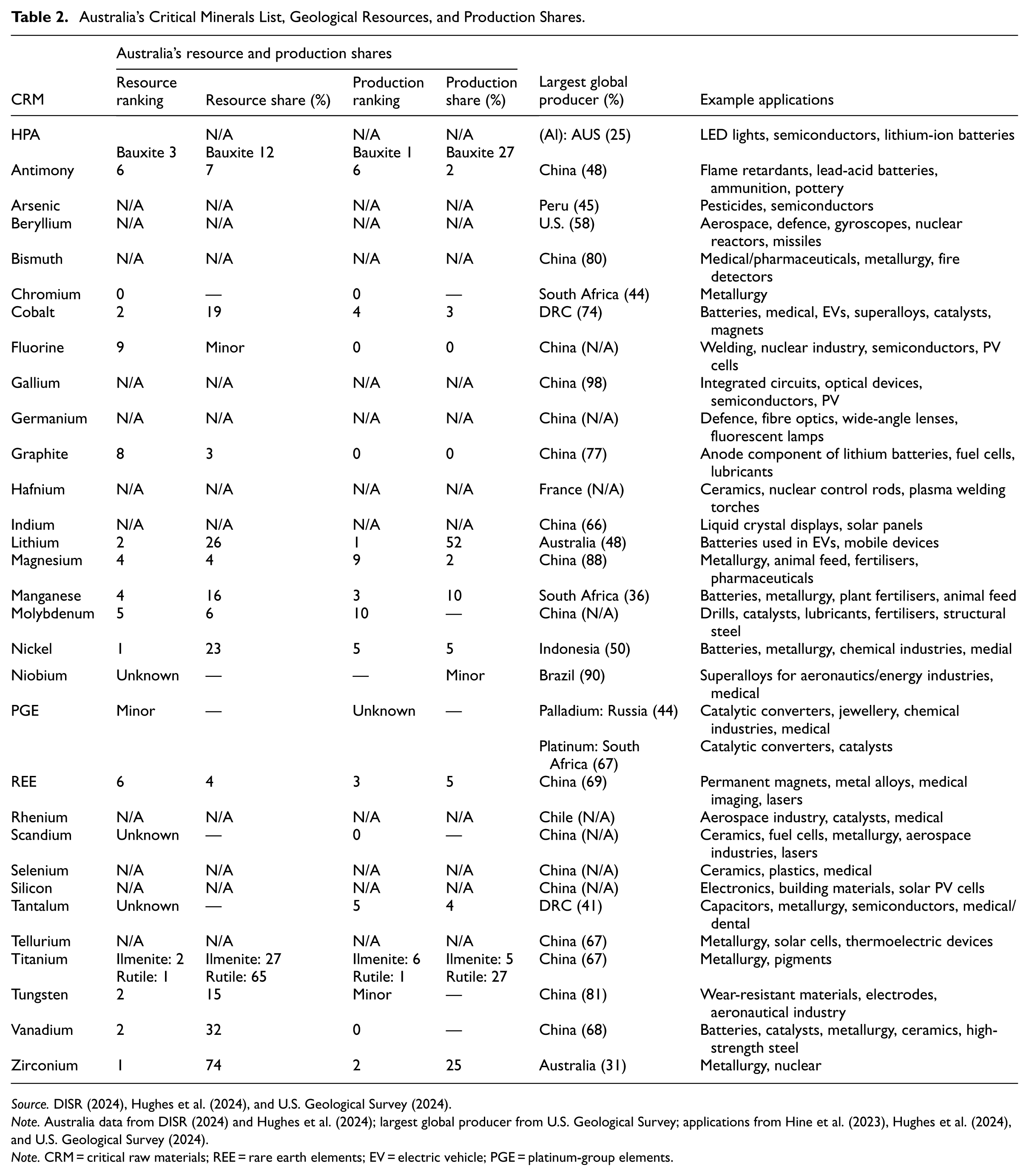

Australia’s recent shift to promote CRM mining and processing continues its foreign policy based on realist pragmatism, where China is viewed as a threat, of being pessimistic of international stability, and of needing to maintain the United States as its indispensable ally via bilateral and multi/minilateral agreements and partnerships. In 2023, Australia updated its critical minerals strategy and CRM list to meet the economic opportunities from growing international demand and diversification strategies (Australian Government, 2023a; Department of Industry, Science and Resources [DISR], 2024, see Table 2). It is also positioning itself within the global security–sustainability nexus as a reliable and sustainable CRM partner. In Australia, the FMIA (Australian Government, 2024a) seeks to invest $22.7 billion in a suite of policies for transitioning Australia to a ‘clean energy superpower’. Australia also plans to develop its sovereign capabilities by leveraging its position as a resource rich country with strong ESG credentials (Australian Government, 2023a). This recognises not only the geopolitical threats to Australia but also from a changing climate. Australia recognised climate change as a threat in 2013, even though only marginally (Wik & Neal, 2025, p. 56). As Ide (2023) points out, the changing climate is unlikely to threaten Australian national security in terms of its physical integrity, ability to control its national borders, maintain reasonable economic relations, and preserve its nature, institutions, and governance from disruption (see also Watson, 2008).

Australia’s Critical Minerals List, Geological Resources, and Production Shares.

Source. DISR (2024), Hughes et al. (2024), and U.S. Geological Survey (2024).

Note. Australia data from DISR (2024) and Hughes et al. (2024); largest global producer from U.S. Geological Survey; applications from Hine et al. (2023), Hughes et al. (2024), and U.S. Geological Survey (2024).

Note. CRM = critical raw materials; REE = rare earth elements; EV = electric vehicle; PGE = platinum-group elements.

Nevertheless, there are points of vulnerability. Threats to Australia’s critical infrastructure and defence capacity from climate change exist (Ide, 2023, p. 38). Australia’s most recent defence white paper identifies climate change as a driver of state fragility and regional instability (Australian Government, 2016). There is also recognition that climate change will create pressures on defence infrastructure, for example due to sea level rise and extreme weather events. However, the white paper only addresses these security concerns in a cursory manner. Similar acknowledgements can be seen in the 2024 National Defence Strategy (Australian Government, 2024b), which identifies climate change as a ‘compounding security risk’ (p. 14), requiring a potentially greater role for the Australian Defence Force in humanitarian assistance in the region, where it ‘aim[s] to remain the partner of choice for the Pacific family, including in security cooperation’ (p. 47). 16

Greater emphasis is put on climate change vulnerabilities in the 2023 Defence Strategic Review, which has a specific section on ‘Climate change and support to domestic disaster relief’. This section also identifies the economic benefits associated with the energy transition, noting that ‘Australia has the potential to benefit substantially from global decarbonisation if we can harness our renewable and mineral resources and drive investment in clean technology supply chains and energy intensive industry. Defence also needs to focus on clean energy transition’ (Australian Government, 2023d, p. 41). Arguably, Australia’s ability to ensure its critical infrastructure and defence capacity rests not only on mitigating and adapting to the changing climate but also re-evaluating how its liberal resource orientation fits within the great power rivalry evident in the global security–sustainability nexus.

Australia’s efforts via the FMIA may seem to fit a resource nationalist frame at first glance. Since the release of the first critical minerals strategy, the government has provided significant financial support to the critical minerals industry. Initiatives include a $200 million commitment to the Critical Minerals Accelerator Initiative, $50 million for a virtual Critical Minerals Research and Development Centre, and a $2 billion Critical Minerals Facility announced in 2021 (Australian Government, 2022). To coordinate these efforts, the Australian government established the Critical Minerals Facilitation Office in 2020 to provide strategic and policy advice, develop the National Critical Minerals Development Roadmap, and to position Australia as a key player in the global supply chain. Other recent initiatives include $225 million for Geoscience Australia’s Exploring for the Future programme, $100 million for the Critical Minerals Development programme, and financial support through the National Reconstruction Fund (Australian Government, 2023a). In 2025, the Commonwealth passed legislation for providing tax incentives for CRM production, including tax offsets (from 2028 to 2040) and benefits for up to 10 years per project (Reuters, 2025a).

However, establishing an industrial policy to promote Australian exports and minerals processing remains marginal to its national security. This is because the structure of its economy, and mining sector specifically, are geared towards resource (neo)liberalism. Neither the taxation nor royalties from mining are likely to reap much benefit for the state (and therefore aid its infrastructure and defence), while CRM mining remains significantly less than traditional mining (Australian Government, 2025c; Hayes et al., 2025; Mudd et al., 2024). This is outlined in relation to the Australia’s efforts to maintain foreign investment in critical minerals mining and maintain off-take agreements with Chinese companies while supporting the MSP and Western friend/near-shoring agreements (discussed in the following section).

The Australian economy is relatively undiversified, with some describing it as a ‘third world economy with first world living standards’ (Edwards et al., 2022, p. 78; see also Growth Lab at Harvard University, 2024). Mining is the second largest sector of the Australian economy (12.5%) after health and education (Reserve Bank of Australia, 2024), with resources dominating exports (59.5%). Overwhelmingly, Australia’s exports are dominated by iron ore and coal, with only aluminium ores and concentrates (including alumina) making the top 10 (Australian Government, 2025c). The dominance of iron ore, coal, and gas contributed to decades of growth in the Australian economy, and the ‘commodities super boom’ of the 2000s was largely driven by Chinese demand. Despite sluggish productivity, the Australian economy was able to grow largely due to Chinese demand for iron ore and its provision of cheap imports (Cartwright, 2025).

Threats to critical infrastructure and defence capacity from climate change could be offset by an increase in mining taxes and royalties. Civil society groups have accused mining companies of aggressive tax avoidance strategies of approximately AUD 4 to 5 billion annually as part of a global tax justice campaign, which led to an Australian Senate Inquiry between 2015 and 2017. Nevertheless, efforts by the government to impose taxes on mining companies have largely failed (Mikler et al., 2019), while royalties for mining remain minimal (Mikler & Ryan, 2024). 17

Australian mining can be understood as following a resource liberal approach. 18 This is identifiable by upholding liberal trade policies, perpetuating an open direct foreign investment (FDI) regime, and by not placing conditions on firms, for example requiring local ownership or processing (Wilson, 2011, p. 286). From the 1980s, there was a strong consensus in Australia on the need for foreign investment (Hundt, 2020), with little change in Australia’s FDI regulatory architecture (Pokarier, 2019). Indeed, 90% of the Australian mining industry is foreign owned (Mikler & Ryan, 2024, p. 730). Australia’s position on FDI was challenged in the early 2000s by a wave of Chinese state-owned enterprises and sovereign wealth funds seeking investment in mining. Fearing market distorting behaviour driven by the prioritisation of Chinese interests, the Commonwealth government revised its foreign investment review guidelines signalling greater scrutiny of state-owned investors (Hundt, 2020). Although Chinese investors aimed to dilute the strength of mining firms and ensure long-term contracts and special pricing agreements, Australia’s policy stance did not restrict Chinese entry into the Australian minerals market (Wilson, 2011).

Laurenceson (2024) suggests that there is now a de facto ban on Chinese investment in CRM mining in Australia. In 2022 the Commonwealth government tightened its guidelines to require prospective investors to provide voluntary notification of their intentions, which would be considered under a new national security review. The non-statutory authority that advises the Commonwealth government, the Foreign Investment Review Board (FIRB), was also given the power to enforce divestment or apply conditions on the company (Hundt, 2020). In 2020 the Commonwealth government rejected a Chinese equity investment in Northern Minerals, an emerging REE company, and investment proposals in lithium and REE in 2023 (Laurenceson, 2024, p. 2). While there may be recent de facto restrictions in place for Chinese investment, the same is not so for other foreign investors (Coe et al., 2025).

Moreover, Australian CRM mines like Greenbushes (the world’s largest lithium mine) have significant foreign investment, rely on foreign technology for processing overseas, and are currently reliant on off-take agreements which embed Australia in Chinese global supply chains (Laurenceson, 2024; Sinclair & Coe, 2024). A recent study of lithium firms operating in Australia points out that Chinese investors are more willing to provide equity and long-term off-take agreements early in lithium mining projects as well as having cost and technical knowledge advantages over Western companies. For this reason, lithium mines in Australia will continue to be enmeshed in supply chains dominated by China (Hayes et al., 2025, p. 101692). In sum, despite subsidies and developing regional hubs for CRM mining (Coe et al., 2025), Australia does not utilise a full suite of policies that fit under a resource nationalist approach. This includes requiring higher royalties, taxes, duties, and outside the FIRB there has been no increase in regulatory requirements, no development of state-owned enterprises, no nationalisation of CRM mining companies, no technology transfer or research and development requirements, and no demand for increased mandatory or voluntary ESG initiatives among others (Haslam & Heidrich, 2016; Wilson, 2015). How this resource liberal economic position affects Australia’s national security is discussed next.

Challenges for Australia’s National Security in the Global Security–Sustainability Nexus

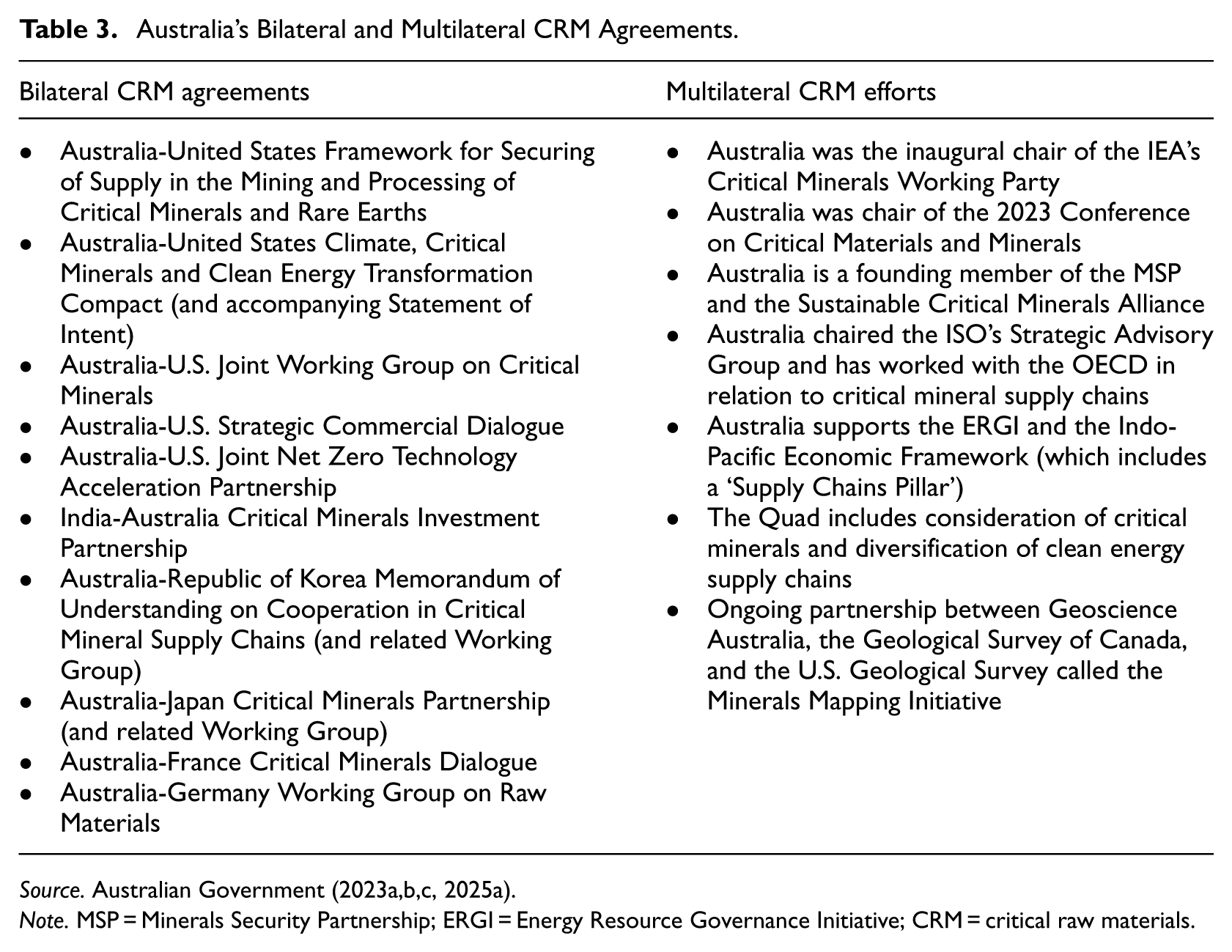

Much has been made of Australia’s interest in redirecting its exports by strengthening its political position with the United States, Japan, Korea, India, and the EU (Vivoda, 2023; Vivoda & Matthews, 2024). The critical minerals strategy aims to match Australia’s resource potential with allies and like-minded partners and fits a realist pragmatic approach to geopolitics, fed by the need to maintain an alliance with the United States to defend it from regional threats. To that end, Australia has entered into a series of CRM bilateral and multilateral agreements (Australian Government, 2023b, see Table 3). This is considered important for securing off-take agreements for CRM exports that also meet national security objectives. However, as commentators have pointed out, Australia’s positioning of itself as a leader in ESG requires willing buyers, many of whom are in competition with Australian CRM, and who are currently dependent on (non-green, cheaper) Chinese minerals (Hayes et al., 2025; Laurenceson, 2024, p. 7). The issue is twofold: how to generate a race to the top for green CRMs, and how to ensure that it is genuine. As a value proposition, the Australian government, like other Western states, explicitly promotes itself as ‘a world leader in ESG performance’ for CRM mining although this raises significant environmental and social risks for the West (Australian Government, 2023a, p. 19; Chaudary, 2025; Riofrancos, 2023; Rodon & Thieriault, 2024). Scholars are sceptical of Australia’s ESG branding particularly with respect to co-benefits for First Nations people (Sinclair & Coe, 2024). Indeed, there is concern that the urgency to navigate the global security–sustainability nexus may contribute to ‘regulatory fast-tracking’ of CRM mining which may undermine socio-environmental justice (Hine et al., 2023), which is significant given that 57% of CRM in Australia are located on Indigenous land where people have the right to negotiate (Burton et al., 2024). A recent undermining of an environmental regulatory oversight agency in the resource rich state of Western Australia demonstrates how Australia may undermine its own ESG claims (Lawrence, 2024). Further undermining its green credentials, in December 2025, the federal parliament amended the Environmental Protection and Biodiversity Conservation (EPBC) Act to enable the fast tracking of CRM mining projects that meet its national interest (Australian Government, 2025b). There seems to be little appetite for viewing Australian security as anything but through a realist national security framing.

Australia’s Bilateral and Multilateral CRM Agreements.

Source. Australian Government (2023a,b,c, 2025a).

Note. MSP = Minerals Security Partnership; ERGI = Energy Resource Governance Initiative; CRM = critical raw materials.

Efforts to diversify Australian CRM exports complicate our understanding of Australia’s national security threats. As has been noted previously, Australia is wedged in terms of its reliance on China as its largest economic partner and the United States as its main security ally (Wilkins, 2023). This exemplifies the predicament of having a resource liberal economy while using some industrial policies vis-a-vis CRM. In terms of the global security–sustainability nexus, any shift away from Chinese processing and refining of Australian CRM may slow the shift to renewables, which would exacerbate climate change and the national security implications to Australian infrastructure and defence. Setting aside the claim that Western mining would be more environmentally and socially beneficial, is concern over the increasing belligerence of the United States in relation to CRM, from which Australia may not be protected. This is especially so given that Australia has long courted the United States as a ‘great and powerful friend’ (Rees, 2024).

This is being borne out in relation to Australia’s trade with the United States. Three days after Australia handed over U.S.$500 million in its first tranche of the AUKUS security agreement for the purchase of nuclear submarines, the United States slapped a 25% tariff on Australian steel and aluminium exports (Jervis-Bardy & Butler, 2025; Needham, 2025). Although the Australian government hoped that this would be waived as it had been under the first Trump presidency in 2018, this was later increased to 50% alongside copper, while maintaining an otherwise flat 10% tariff in the last round of presidential executive orders (Doherty, 2025). 19 There are no longer any guarantees that the United States will play by the normal diplomatic rules. There is a real risk that Australia could become collateral damage in the intensifying strategic contest between the United States (its irreplaceable security ally) and China (its irreplaceable trading partner). The security implications are bleak: the AUKUS agreement may or may not provide Australia with nuclear powered submarines in the distant future, while providing the United States with forward deployment capability in Australia. Australia’s realist pragmatic approach does not entertain the view of the United States as an unreliable ally but continues to view China with suspicion. Its resource liberal orientation in CRM mining means that it remains reliant on Chinese investors, technology, and knowledge, but as a state, Australia has not used its mineral wealth to develop economic security. Irrespective of which Great Power is the greatest threat, Australia’s realist pragmatism has not fully grappled with the sovereignty implications of its geopolitical positioning. Despite its advantages, Australia’s national security remains vulnerable within the global security–sustainability nexus.

Conclusion

Australian foreign policy has a long been viewed through a realist pragmatism, courting the United States as a great and powerful friend to shield it from global instability and regional threats. Increasing tensions between the United States and China over CRM have contributed to Australia seeking mineral agreements with allies and like-minded partners as the demand for CRM increases. The global security–sustainability nexus, where CRM are needed for military, industrial, and energy transition purposes has led to international attempts to diversify global supply chains for CRM. Australia has, like other states, identified industrial policies to promote CRM mining with the aim of moving into processing and renewable energy technology. While this seeks to assure Australian national security as a means of consolidating its alliances and mitigating climate change, this does not necessarily provide economic security given China is its largest trading partner. It remains to be seen how Australia’s resource liberalism, with largely foreign owned mining companies, who are dependent on foreign technology, and embedded in Chinese supply chains, may be directed towards Australian national security aims.

This article has explored the intersection between resource liberalism and Australian national security by highlighting not only Australia’s economic dependence on mining but also its realist pragmatism of ensuring its allegiance to the Western aim of diversifying from dependence on China. Australia may be caught between what is best for itself as a nation, and what assists the Western alliance front as a whole. Moreover, central to the global security–sustainability nexus is the justification of mining in the West as having higher environmental and social standards for the energy transition. Australia has repeatedly articulated its value proposition as a stable country with high standards, although this has been challenged by scholars particularly in relation to First Nations and environmental impacts. Further research is being done to assess the extent to which CRM can be done more equitably and sustainably in Australia. None of this, however, addresses concerns with an increasingly belligerent hegemon and ally in an era of great power rivalry.

Footnotes

Appendix

Select States Critical Minerals Lists.

| Country lists | ||||||||

|---|---|---|---|---|---|---|---|---|

| Critical mineral | U.S. | EU | India | Japan | ROK | U.K. | AUS | CAN |

| High-purity alumina | x | |||||||

| Aluminium a | x | X | x | |||||

| Antimony | x | x | x | x | x | x | x | x |

| Arsenic | x | x | x | |||||

| Barite | x | x | ||||||

| Barium | x | |||||||

| Bauxite | x | |||||||

| Beryllium | x | x | x | x | x | |||

| Bismuth | x | x | x | x | x | x | x | |

| Boron | x | x | ||||||

| Cadmium | x | |||||||

| Carbon | x | |||||||

| Cerium (REE) | x | x | x | |||||

| Caesium | x | x | x | |||||

| Chromium | x | x | x | x | x | |||

| Cobalt | x | x | x | x | x | x | x | x |

| Coking coal | x | |||||||

| Copper | x | x | x | x | ||||

| Dysprosium (REE) | x | x | x | |||||

| Erbium (REE) | x | x | ||||||

| Europium (REE) | x | x | ||||||

| Feldspar | x | |||||||

| Fluorine | x | x | ||||||

| Fluorspar | x | x | x | |||||

| Gadolinium (REE) | x | x | ||||||

| Gallium | x | x | x | x | x | x | x | x |

| Germanium | x | x | x | x | x | x | ||

| Graphite | x | x | x | x | x | x | x | |

| Hafnium | x | x | x | x | x | |||

| Helium | x | x | ||||||

| Holmium (REE) | x | x | ||||||

| Indium | x | x | x | x | x | x | ||

| Iridium (PGM) | x | x | ||||||

| Lanthanum (REE) | x | x | x | |||||

| Lead | x | |||||||

| Lithium | x | x | x | x | x | x | x | x |

| Lutetium (REE) | x | x | ||||||

| Magnesium | x | x | x | x | x | x | x | |

| Manganese | x | x | x | x | x | x | ||

| Molybdenum | x | x | x | x | x | |||

| Neodymium (REE) | x | x | x | |||||

| Nickel | x | x | x | x | x | x | x | |

| Niobium | x | x | x | x | x | x | x | x |

| Osmium (PGM) | x | |||||||

| Palladium (PGM) | x | x | x | x | ||||

| Platinum (PGM) | x | x | x | x | ||||

| Phosphate rock | x | |||||||

| Phosphorous | x | x | ||||||

| Platinum-group metals b | x | x | x | x | ||||

| Potash | x | x | ||||||

| Praseodymium (REE) | x | x | ||||||

| Promethium (REE) | x | |||||||

| Rare earth elementsb,c | x | x | x | x | x | |||

| Rhenium | x | x | x | |||||

| Rhodium (PGM) | x | x | ||||||

| Rindium | x | |||||||

| Rubidium | x | x | ||||||

| Ruthenium (PGM) | x | x | ||||||

| Samarium (REE) | x | x | ||||||

| Scandium (REE) | x | x | x | x | x | |||

| Selenium | x | x | x | x | ||||

| Silicon | x | x | x | x | x | x | ||

| Strontium | x | x | x | x | ||||

| Tantalum | x | x | x | x | x | x | x | x |

| Tellurium | x | x | x | x | x | x | ||

| Terbium (REE) | x | x | x | |||||

| Thallium | x | |||||||

| Thulium (REE) | x | x | ||||||

| Tin | x | x | x | x | x | |||

| Titanium | x | x | x | x | x | x | x | |

| Tungsten | x | x | x | x | x | x | x | x |

| Uranium | x | |||||||

| Vanadium | x | x | x | x | x | x | x | x |

| Ytterbium (REE) | x | x | ||||||

| Yttrium (REE) | x | x | ||||||

| Zinc | X | x | x | |||||

| Zirconium | X | X | x | X | x | |||

Source. Burton (2022), DISR (2024), European Commission (2023a), IEA (2022, 2023a, 2023b), and Ministry of Mines (2023).

Note. PGM = platinum-group metal; REE = rare earth elements; EU = European Union.

Aluminium is smelted from alumina, which is in turn refined from bauxite ore.

Some countries have identified REE or PGMs more broadly, while others have identified specific REEs/PGMs. There are 17 elements that are considered REEs and 6 PGMs which are indicated in the table.

The EU’s critical raw materials list distinguishes between light and heavy REEs.

Acknowledgements

The authors would like to thank the Special Issue editors for hosting the workshop ‘Governing Critical Minerals and Energy Transition in the New Environment-Security Nexus’ Stockholm, 3–5 October 2024, and inviting us to contribute to this volume.

Ethical Considerations and Informed Consent Statements

Ethics approval was not required as all information is publicly available and no research was undertaken requiring ethics review and approval. Informed consent was also not required as there were no participants of the research, nor consent required for accessing information. All information was drawn from publicly available documents.

Author Contributions

Both authors contributed equally to data collection, data analysis, writing and referencing.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research has the support of the Sydney Environment Institute, the Faculty of Arts and Social Sciences, and the Net Zero Institute at the University of Sydney and funding by the Australian Research Council Discovery Grant DP230103043.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data are drawn from publicly available information.