Abstract

How do art entrepreneurs make decisions about adopting blockchain technologies? This study examines the link between non-fungible token (NFT) adoption and business outcomes. Through survey data from 35 Czech art market stakeholders, including curators, art dealers and galleries, we investigate the strategic decision to adopt NFT technology through the lens of digital entrepreneurship and digital affordance theory. Our results highlight the potential of NFTs in addressing historical challenges of the art industry, such as provenance tracking, authenticity verification and transaction transparency while also identifying challenges and adoption barriers, such as regulatory uncertainties. We also show that while respondents rate blockchain systems as potentially useful, the actual NFT adoption rate remains low. These findings provide actionable insights for stakeholders and contribute to entrepreneurship literature by investigating entrepreneurial decision-making in markets adopting digital innovations.

Introduction

The growth of the global art market over the past few decades highlights its capacity to adapt and thrive through periods of economic uncertainty, as well as through rapid technological innovations affecting art production and distribution.

Non-fungible tokens (NFTs) are one of these potential technological innovations (Dvouletý et al., 2025). They are ‘blockchain-enabled cryptographic tokens that represent ownership of unique digital objects’ (Chalmers et al., 2022, p. 2). Non-fungible refers to their differences compared to fungible cryptocurrencies like Bitcoin, where one unit is equal to another and is exchangeable for another unit. NFTs derive value from their individual characteristics and are not directly interchangeable with each other. NFT-based digital art is defined as limited-edition artwork, certified and authenticated through a registration in a distributed ledger technology, known as blockchain (Jia & Yao, 2024; Kumar et al., 2025).

NFT-based digital art has generated significant attention over the past few years (Dartanto et al., 2024; Dorostkar & Ziari, 2026), with a peak in 2022. A significant contraction quickly followed the peak, but NFTs have remained in the art landscape. The blockchain technology has the merit of potentially turning digital art, which would otherwise move by and large unrestricted by ownership claims, into a commodity and new revenue streams (Alacovska et al., 2025). NFT-based art can be transacted on virtual marketplaces, thanks to a transparent record of ownership and provenance. However, in the context of the current regulatory uncertainty, while NFTs do anchor the principle of ownability and verifiability, they do not provide clear legal property rights and are subject to different legislations in different countries.

Therefore, this leads us to question the practical value of NFTs for traditional art market stakeholders through the theoretical lens of digital affordance theory (Poposki, 2025). Are galleries and cultural institutions adopting NFTs? If not, does their reluctance stem from the early adoption challenges of transformative technologies, or are they rationally deciding to avoid the potential costs of transacting in highly speculative assets?

This research focuses on the economic opportunities generated by NFTs as well as the barriers to their adoption by art industry stakeholders, through the lens of digital affordance theory (Autio et al., 2018), serving us a conceptual framework to understand how new technologies, such as NFTs, can help to explore and exploit new opportunities in the arts industry (Mukhopadhyay, 2025). Specifically, we investigate how art entrepreneurs navigate innovation decisions under uncertainty by focusing on Czech galleries, curators and artists and their assessments of the strategic value of blockchain technology for their specific business contexts.

Theoretical Framework

In this study, we anchor the analysis of actors’ interactions with NFTs in digital affordances theory (Autio et al., 2018). Digital affordances represent the possibilities for actors to perform novel actions or functions or to use the existing actions and functions in novel ways. According to Chalmers et al. (2022, p. 2), digital affordances are ‘not deterministic technology features, but potentialities discovered and enacted by goal-driven actors’. This analytical framework allows us to study how art industry entrepreneurs might view NFTs as enabling new venture ideas and improving their economic outcomes.

We can distinguish two main types of digital affordances that emerge from NFT adoption. One is the principle of ownability: the benefits stemming from the secure and immutable record of ownership. Indeed, the art market has historically struggled with transparency and fraud prevention, challenges that blockchain technology is uniquely positioned to address (Abbate et al., 2022). Second, NFTs might allow for novel actions thanks to the principle of verifiability. It consists of the ability to evaluate and validate asset ownership and therefore ‘offer protection against spoofing, tampering, denial of service, repudiation, or other security attacks’ (Chalmers et al., 2022, p. 2).

Digital affordance theory is particularly interesting from the art entrepreneurship perspective, as the focus is not on new digital features per se, but rather on the capacity and willingness of the entrepreneurial actors to discover new action possibilities and to engage in the pursuit of a new venture idea. For our study, the theory offers the conceptual foundation for understanding traditional art industry stakeholders’ evaluation of NFT technology and their willingness to adopt it and for exploring new market opportunities.

More broadly, digital affordances sit within the conceptual framework of digital entrepreneurship as developed by Nambisan et al. (2017). Digital entrepreneurship is marked not only by less-bound entrepreneurial processes but also by a ‘less predefined locus of entrepreneurial agency’ (Nambisan et al., 2017). Indeed, we argue that NFTs have the potential to facilitate greater international collaboration and standardization of practices in a traditionally fragmented market. By introducing a unified digital ledger, NFTs may contribute to fostering cross-border partnerships and creating a more integrated global art market. Additionally, digital artwork can be exchanged on cryptoart marketplace platforms, facilitating the influx of end users on both sides of the transactions, further increasing the internationalization and decentralization of art markets (Chandra & Coviello, 2010).

Art Market Context

The art market can be generalized into its primary and secondary markets. The actors in the primary markets are contemporary artists, and the galleries represent them. An artist will create a piece of artwork that will be sold on the market for the first time, typically straight to a consumer. It is more typical for artists to gain gallery representation to strengthen their brand and reputation by inheriting that of the gallery for a predefined cut of the sale prices. Alternatively, the secondary market is auction houses and art dealers reselling established art pieces (Duncan & Klareld, 2024; Hobelsberger, 2021). With these functions, the galleries and art dealers assume the role of ‘intermediaries committed to creating the symbolic and economic value of art’ (Hobelsberger, 2021, p. 3). In other words, they select, value and distribute the artwork based on their subjective taste. However, to succeed, they need the resources and opinions of other reputable galleries with the clientele to sell to and help strengthen the artists’ brand, referred to as ‘cultural brokerage’ (Janssen, 2015).

How has technology entered the art market? While it created the rise of digital art, this by no means is the definition of the impact of technology in the art industry. From platforms to databases, the art industry is slowly seeing a digital transformation. During COVID-19, many businesses had to adapt their business practices to the lockdown legislation. The art market was resilient to economic turmoil when global sales dropped by 21% in 2020, but bounced back in 2021 by 29% (Artprice, 2021). Despite the market’s incredible performance, the industry’s digitalization is the most crucial outcome (Sidorova, 2024). According to a market expert at Sotheby’s (2021), digital tools have removed the existing barriers, and clients can now view or physically handle works in person prior to purchasing. According to Fernandes and Afonso (2020), in 2018, online sales in the art markets reached nearly $6b, representing 9% of the turnover in this sector. In 2022, online sales in the art markets reached $10.8b, an 80% increase (Read, 2023). This aligns with the notion that people are generally more comfortable purchasing art online. On the other hand, earlier findings showed that people would only be inclined to purchase art online in the lower to mid-price range, while art cannot be purchased in higher price ranges (Adam, 2014). However, a new record is broken yearly regarding the highest value of artwork sold online.

In 2020, the House of Fine Art (HOFA Gallery) demonstrated its innovative approach by embracing digital innovations in the art world. As one of the first prominent galleries to utilize NFT technology, HOFA showcased works by celebrated artists such as Banksy, Jeff Koons and Damien Hirst, creating hybrid exhibitions that combined virtual and physical art experiences. These initiatives underscored HOFA’s role in leading the art market’s adaptation to changing consumer behaviours and technological advancements during a pivotal time for the global art industry (Choudhury, 2019).

Therefore, we outline the primary functions NFTs can bring to the art market, which are divided into two main components—organizational and financial—as NFTs are inherently traceable and tradeable. Organizational functions include managing authors’ royalties, provenance and authenticity. Financial functions include purchasing, cooperative financial arrangements, fractional ownership (Abbate et al., 2022) and live market prices of artwork. The role of NFTs could be versatile in creating a unified platform for the art market. Giannoni et al. (2023) classified the potential benefits of blockchain technology for art galleries in the following way:

Provenance and authenticity: Blockchain ensures the immutability of records related to artwork ownership and creation, aiding in proving authenticity and tracking provenance. Ownership and transfer: Blockchain enables secure and transparent recording of ownership and facilitates seamless transfers. Fractional ownership: Platforms like Maecenas allow for fractionalizing artworks, enabling multiple investors to own shares in high-value pieces. Transaction transparency: Blockchain creates a tamper-proof digital ledger, ensuring transparency in art transactions. Digital and physical asset management: Blockchain integrates physical artwork and digital certificates, linking physical objects with corresponding blockchain records. Artist royalties: Smart contracts ensure that artists receive royalties from secondary sales, addressing long-standing inequities in the art market. Standardization and collaboration: Blockchain helps standardize practices across markets and encourages collaboration among galleries, collectors and institutions. Fraud prevention: Blockchain’s secure and verifiable records address issues of forgery and fraud in the art market.

Wilson et al. (2022) present a valuable discussion of blockchain’s role in the art market, emphasizing both its transformative potential and the inherent complexities of adoption. Central to their argument is the idea that blockchain, particularly through NFTs, has redefined fundamental aspects of the art market by addressing historical challenges such as provenance tracking, authenticity verification and transaction transparency. Through the use of immutable ledgers, blockchain provides a means of ensuring that each step in an artwork’s journey is securely recorded, reducing the chance of forgery and fraudulent claims. For galleries and collectors, this represents a significant step forward in building trust and efficiency within the market.

Beyond these immediate concerns, Wilson et al. (2022) note structural issues surrounding blockchain adoption in the art market. They highlight a lack of regulatory oversight as a significant challenge, noting that the absence of clear legal frameworks creates uncertainty for galleries, collectors and investors. This is particularly important given the cross-border nature of art transactions, where differing national regulations can complicate the use of blockchain-based solutions. Regulatory gaps also leave the market vulnerable to fraudulent practices, undermining the trust that blockchain is designed to enhance. This pertains to uncertainties regarding the legal status of NFTs, the enforcement of contracts and the protection of intellectual property.

Despite these challenges, Wilson et al. (2022) underscore blockchain’s opportunities for innovations. They argue that blockchain can do more than solve isolated issues when implemented strategically. It can radically reshape the art market by enabling greater inclusivity and democratization. For example, NFTs allow for fractional ownership, which opens high-value art investments to a broader audience. This financialization of art is particularly appealing to younger, tech-savvy investors who might otherwise be excluded from the market. Furthermore, Wilson et al. (2022) point out that blockchain’s real-time transaction capabilities and dynamic pricing mechanisms could revolutionize how art is valued and traded, creating a more responsive and transparent marketplace.

Wilson et al. (2022) ultimately advocate for a balanced approach to adoption. They stress the importance of integrating blockchain into the art market to complement its existing structures rather than disrupt them entirely. This involves addressing key risks such as volatility, sustainability and regulatory ambiguity, while also capitalizing on blockchain’s strengths in provenance, transparency and inclusivity.

The current EU legislation, MiCA (Markets in Crypto-assets Regulation), has consolidated many uncertainties regarding the crypto infrastructure and its legal implications. MiCA represents a groundbreaking regulatory framework aimed at harmonizing the governance of crypto assets across all EU member states, ensuring a consistent and transparent environment for digital asset transactions (European Securities and Markets Authority [ESMA], European Commission, 2023). MiCA introduces provisions that directly impact the art market, particularly through its treatment of NFTs. Although NFTs are not the primary focus of MiCA, the regulation includes mechanisms for addressing crypto assets’ classification, transparency and consumer protection (European Commission, 2023). By requiring platforms to disclose critical information about NFTs, such as provenance and ownership, MiCA enhances trust and legitimacy in blockchain-based transactions. This is particularly relevant in the art market, where the opaque nature of transactions has historically enabled fraud and money laundering.

For stakeholders in the art world, such as galleries, artists, collectors and NFT platforms, MiCA offers both opportunities and challenges. The regulation provides a standardized legal framework that builds confidence in blockchain technology, particularly for activities such as provenance tracking and transparent sales processes (Clifford Chance, 2023). However, smaller entities may face difficulties complying with MiCA’s strict requirements, such as enhanced disclosures and operational standards, which could increase administrative and financial burdens. Another limitation is that MiCA does not fully address unique challenges posed by NFTs, including intellectual property disputes and environmental impacts of blockchain technologies. The global nature of art markets also requires international collaboration to address cross-border issues that MiCA alone cannot resolve.

Data and Methodology

Data

This research targets key stakeholders in the Czech art industry, including artists, galleries and auction houses. These participants represent critical components of the traditional art market ecosystem. By focusing on physical artworks and traditional market channels, we narrow its scope to a subset of the global art market that remains largely unexamined in the context of NFTs.

The final sample collected throughout the second half of 2024 consists of 35 respondents, attempting to ensure representation across core industry participants. To maintain relevance with respect to the traditional art market, the sample selection criteria were established based on the selection criteria that respondents must actively engage with traditional channels of art transactions, such as galleries, auction houses or established networks of collectors and artists. This focus reflects the role of these entities as intermediaries that shape market practices, enforce provenance and facilitate sales in both primary and secondary markets (Hobelsberger, 2021). Also, participants were required to perform roles directly related to curating, organizing exhibitions, transacting artworks or conducting administrative work associated with art management. These activities are integral to the operational and financial dynamics of the art industry and are therefore central to the study’s examination of NFT impacts (Brown, 2023). Finally, a minimum trading volume of 300,000 CZK annually was required, ensuring that the sample represents commercially active entities within the art market. This threshold guarantees an economic significance of the selected participants and ensures the research captures the perspectives of those most likely to engage with NFT technologies for operational or financial benefits (Wilson et al., 2022).

The sampling strategy ensures the inclusion of key decision-makers and influencers within the Czech art market, providing actionable insights for both practitioners and policymakers. We used purposive sampling to target curators, art dealers, artists and galleries that met the predefined research criteria. Convenience sampling was utilized through professional networks and online platforms. Snowball sampling was then used to expand the respondent pool to reach the final amount of 35 respondents.

Research Objectives

The primary objective was to investigate the potential of NFT technology to impact art industry actors, focusing on four critical dimensions—operational efficiency, artist representation, economic outcomes and market trends—with the help of quantitative research.

First, the research examines operational efficiency by exploring whether NFTs enhance key processes such as provenance tracking, ownership verification and fraud prevention. In terms of artist representation, we focus on whether NFTs improve visibility and enforce rights such as royalties. We hypothesize that increased utilization of NFTs enhances artists’ representation by improving visibility, ensuring royalty enforcement and protecting rights in the art market. NFTs, as a tool for tokenizing traditional art, empower artists by streamlining provenance tracking and ensuring transparency in secondary market transactions.

The third focus of the research is on economic outcomes, analysing whether NFTs lead to increased sales, enhanced financial stability or diversified revenue streams for key stakeholders such as galleries, curators and dealers. With the art market increasingly being viewed as a financial asset class, the role of NFTs in creating new investment opportunities, such as fractional ownership, is of particular interest. The study seeks to quantify the economic benefits of adopting NFTs and assess whether these benefits are distributed equitably among stakeholders or concentrated among a few major players. We hypothesize that NFTs create new economic opportunities by facilitating fractional ownership models, allowing collectors to purchase shares in physical artworks. This innovation democratizes art investment, broadening the buyer base and injecting liquidity into the market (Wilson et al., 2022). For galleries, tokenization offers a dual advantage: it provides new revenue streams while preserving the unique value of physical artworks. Moreover, the disintermediation enabled by blockchain reduces transaction costs, as galleries can interact directly with collectors without relying on intermediaries (Giannoni et al., 2023). However, economic challenges remain, such as regulatory compliance and the technical costs of NFT integration, which this research seeks to address. This hypothesis explores the perceived financial benefits of NFT adoption within the Czech art market, emphasizing the role of NFTs in enhancing economic stability and diversifying income sources (Brown, 2023).

Lastly, the research investigates market trends, particularly the potential of NFTs to facilitate greater international collaboration and standardization of practices in a traditionally fragmented market. Tokenizing traditional artworks with NFTs might allow galleries and curators to extend their reach globally while maintaining their focus on physical art exhibitions. By bridging the gap between local and global markets, NFTs enable stakeholders to connect with international collectors and buyers more seamlessly (Ko et al., 2022). Blockchain further contributes to the standardization of market practices by introducing consistent frameworks for pricing, provenance and royalties. Additionally, NFTs support sustainable growth in the art market by facilitating collaborations across countries, enhancing both the accessibility and the inclusivity of art trade (Giannoni et al., 2023). This hypothesis explores whether Czech art market stakeholders perceive NFTs as a mechanism for globalization and partnership development within the industry.

The study deliberately excludes digital-only platforms such as OpenSea or Rarible to ensure that the findings directly apply to the traditional art industry. This approach aligns with the research objective of understanding how NFTs integrate into established practices, rather than how they function in a solely digital context.

In addition to analysing competitors in the market, this study includes an interview with the company ArtChain, which has a partnership with GESTOR, a Czech organization specializing in the management and protection of intellectual property rights within the creative industries.

Survey Design

The survey used in this research was designed to capture key aspects of NFT utilization within the art industry, featuring 24 questions divided into five major categories and four additional questions addressing respondent characteristics and objective measures. This structure ensures a comprehensive approach to understanding the relationship between NFTs and various art market dynamics. The inclusion of questions on respondent characteristics, such as gallery size, annual revenue and primary focus areas (e.g., physical artworks or digital integration), provides critical objective measures to contextualize the responses. The survey employed Likert-scale questions for the majority of its sections, with a 5-point scale ranging from ‘strongly disagree (=1)’ to ‘strongly agree (=5)’. It simplifies the aggregation and analysis of data, allowing for effective statistical interpretation. Cronbach’s α coefficient assessed the internal consistency and reliability of survey items. Values above 0.70 are considered acceptable for explanatory research, while values above 0.80 suggest good reliability (DeVellis, 2012). All sections of our survey (NFT utilization, fraud detection, economic impact, artist representation, market trends and collaboration) showed strong internal consistency, with Cronbach’s α coefficients ranging between 0.83 and 0.92.

NFT utilization serves as the core independent variable in this research, covering the frequency and extent to which stakeholders in the art industry engage with blockchain technologies to tokenize artworks, conduct transactions and manage provenance. Economic impact serves as the main dependent variable in this research, focusing on whether the adoption of NFTs has influenced financial outcomes for galleries, curators and other stakeholders. Specifically, this variable examines changes in revenue, valuation and financial stability. To measure the economic impact, the survey included questions assessing whether stakeholders observed increased revenue, improved valuation of their collections or challenges in integrating NFTs into their financial models. The alignment between NFTs and economic performance builds on theories of digital entrepreneurship and digital affordances (Autio et al., 2018; Nambisan et al., 2017).

Results

In this section, we present relevant descriptive statistics, such as respondents’ characteristics, followed by the results of the main quantitative analysis. Finally, results from the case study will complete the analysis by adding qualitative insights into practical implementation challenges.

Descriptive Statistics

Survey responses represent diverse roles within the art market. Administrative positions constitute 30% of respondents, followed by managers and curators at 27% each. Owners represent 5%, while artists comprise 11% of the sample. This distribution highlights the prominence of smaller entities within the Czech art market while still reflecting the input from more established, larger galleries. All respondents were located in Prague. Regarding market focus, 51% of respondents engage with both primary and secondary markets, indicating a dual focus on contemporary and historical artworks. The primary market alone accounted for 27%, and artists accounted for 11%.

A majority of the galleries surveyed (76%) reported annual revenues in the range of 300,000–1,000,000 CZK for 2023. An additional 19% respondents achieved revenues between 1,000,000 and 5,000,000 CZK. No galleries reported revenues exceeding 5,000,000 CZK. This revenue distribution reflects the financial realities of galleries across different scales in the Czech art market.

NFT Utilization

The average score for NFT utilization 1 was 2.18 (standard deviation = 0.97), indicating a low level of adoption among respondents, with scores ranging from 1.25 to 4.00. This variation suggests diverse levels of engagement with NFTs across galleries. The mean response for actively engaging with NFTs to tokenize artworks is 1.86, indicating minimal adoption. Similarly, the mean response for NFT transactions as a regular part of gallery operations is even lower at 1.59, suggesting that most respondents do not frequently use NFTs in their operations.

In contrast, there is a higher mean response of 3.51 regarding the perception of blockchain-based systems as useful tools for managing provenance and ownership records. This suggests that while respondents may not actively utilize NFTs, they recognize the potential utility of blockchain for specific art market applications.

However, the process of ownership verification through NFTs remains underutilized, as indicated by a mean response of 1.73. This highlights a gap between blockchain technology’s perceived benefits and practical implementation within the surveyed galleries. This is an important result in terms of digital affordances: while art entrepreneurs foresee entrepreneurial opportunities in NFTs in their sector, they choose not to utilize these possible new functions and actions. More research is thus needed to understand the obstacles to NFT adoption: Is it symptomatic of challenges in early-stage innovation adoption? Do actors who adopt NFTs really benefit from better business outcomes? We will investigate this correlation in the next section.

NFT Utilization and Economic Outcomes

Economic Outcomes

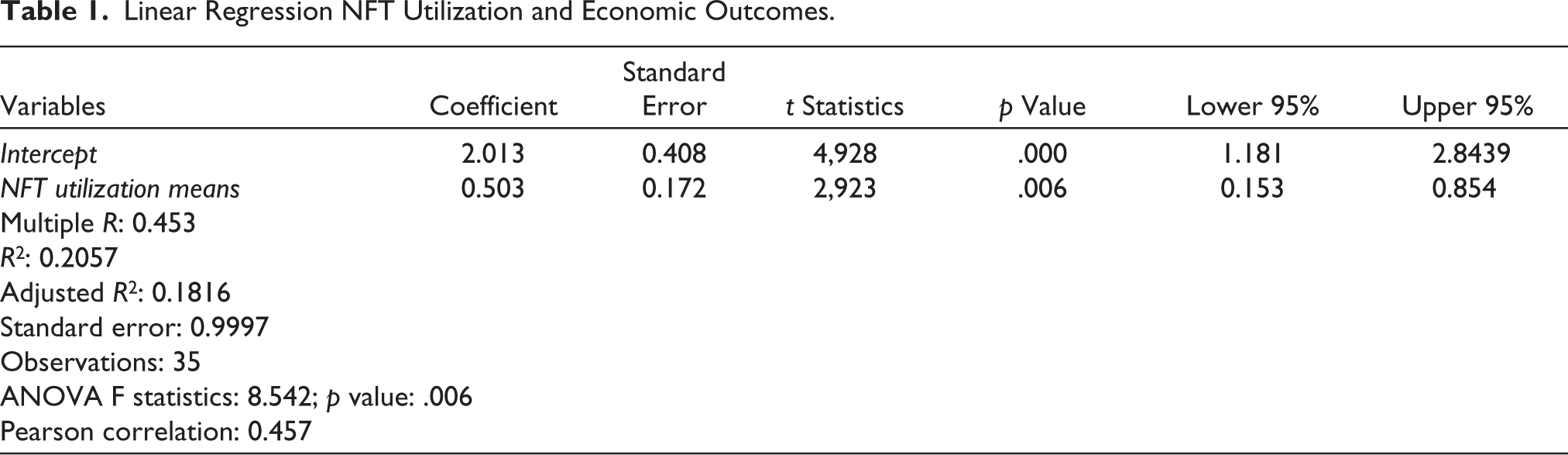

The regression analysis offers key insights into the relationship between NFT utilization and economic impact. To measure the economic impact, the survey included questions assessing whether stakeholders observed increased revenue, improved valuation of their collections or challenges in integrating NFTs into their financial models. 2 The R2 value of 0.206 indicates that NFT utilization accounts for approximately 20.6% of the variance in economic impact, suggesting a moderate level of explanatory power for this independent variable. The adjusted R2 value of 0.182 further supports the model’s relevance. The ANOVA results, with an F-statistic of 8.546 and a p value of .006, demonstrate statistical significance, confirming that the observed relationship between NFT utilization and economic impact is unlikely to be due to random variations.

The regression coefficient (see Table 1 and Figure 1) for NFT utilization is β = 0.504, reflecting a moderate positive relationship with economic outcomes. This indicates that a one-unit increase in NFT utilization corresponds to an estimated 0.504 unit increase in economic outcomes scores. The associated p value of .006 supports that this relationship is statistically significant. Additionally, the standard error of 0.172 and the 95% confidence interval (0.153, 0.855) suggest a robust estimate of the coefficient, supporting its reliability for interpretation. The Pearson correlation coefficient (r = 0.457) further supports these findings, indicating a moderate positive linear relationship between NFT utilization and economic outcomes. Collectively, these results suggest that higher adoption of NFTs is associated with improved financial outcomes in the art market. Alternatively, better economic outcomes may lead to diversifying new methods of expanding their technological advancements.

Linear Regression NFT Utilization and Economic Outcomes.

Scatter Plot for Economic Outcomes and NFT Utilization.

Market Collaboration

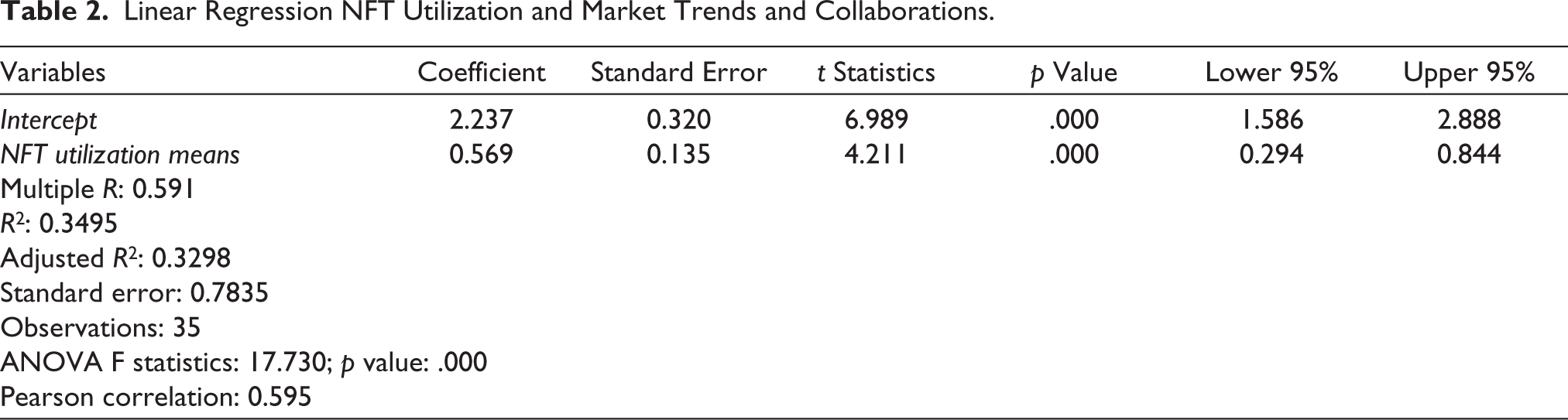

Another relevant result is a significant correlation between NFT utilization and market collaboration assessment 3 (β = 0.569, p = .00018) reported in Table 2 and Figure 2. The R2 value of 0.350 indicates that NFT utilization evaluation explains 35% of the variance in collaboration trends assessment, demonstrating some explanatory power. The adjusted R2 value of 0.330 further validates the robustness of the model by accounting for sample size and predictors. The ANOVA results reveal an F-statistic of 17.73 (p value = .000), signifying a highly statistically significant relationship. This suggests that the observed association between NFT utilization and market trends and collaborations is unlikely to be due to random variations, reinforcing the validity of the findings.

Linear Regression NFT Utilization and Market Trends and Collaborations.

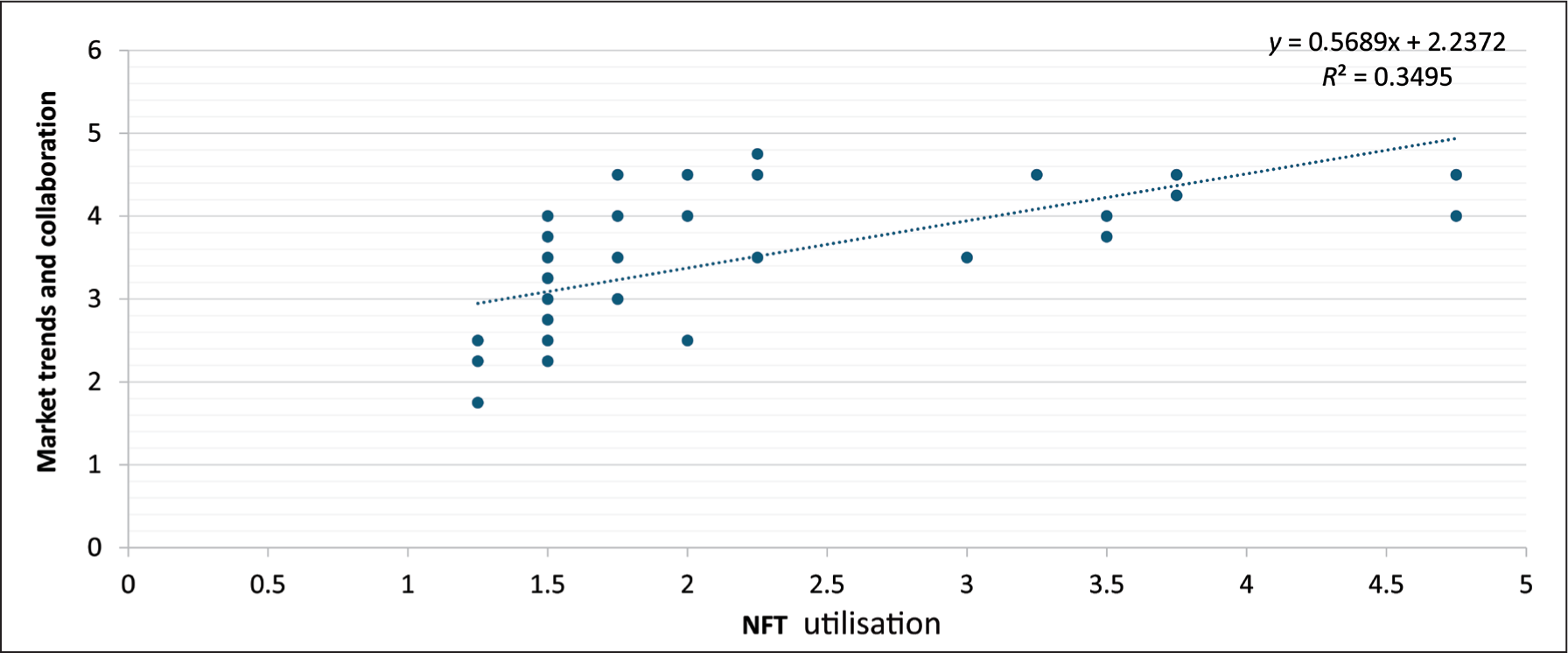

Scatter Plot for Market Trends, Collaboration and NFT Utilization.

The regression coefficient for NFT utilization is β = 0.569, indicating a positive relationship. This implies that for every unit increase in NFT utilization, there is an average increase of 0.569 units in market trends and collaborations. The p value of .000 further supports the statistical significance of this relationship. Additionally, the 95% confidence interval (0.294, 0.844) provides strong evidence of the reliability of the coefficient estimate. The Pearson correlation coefficient (r = 0.595) supports the regression findings, indicating a moderate-to-strong positive linear relationship between NFT utilization and market trends and collaborations. This further highlights the role of NFT utilization in driving advancements in collaboration and globalization within the art market. On the other hand, it could explain that galleries which seek out new collaboration opportunities are more likely to explore new technologies, such as utilizing NFT technology.

The Artists; Representation and Fraud Prevention

Similarly, we studied the role of NFT utilization in the artists’ representation 4 and fraud prevention 5 with the help of regression analysis. However, the regression analysis results revealed no statistically significant relationship between NFT utilization and artists’ representation outcomes (p value = .966) and fraud prevention assessment (p value = .286). Therefore, for parsimonious reasons, we do not report the full regression results in the article (they are available upon request) and call for more in-depth research with the help of longitudinal data in the future.

Insights From a Platform Founder

To enrich the findings that had already been provided, we further asked a representative of one specific platform, that is, ArtChain, based in Prague, to provide additional insights via answering several questions 6 (the transcript is available upon request). The following text provides a summary of the key insights. The founder, Albert Bahbouh, established ArtChain to address critical gaps in provenance tracking within the art market. Albert Bahbouh identified that traditional methods of verifying artwork authenticity often rely on expensive equipment and labour-intensive processes, making them inaccessible for smaller galleries. Through ArtChain, Bahbouh aims to democratize access to these technologies by leveraging blockchain to simplify and automate provenance verification while still valuing the human touch in authentication. This aligns with the previous discussion on blockchain’s role in enhancing accessibility and operational efficiency for galleries of all sizes.

According to Bahbouh, one of the major challenges in the art market is its resistance to adopting new technologies. Many galleries still use outdated tools like Excel for inventory management, and scepticism about blockchain’s practicality remains high. To address this, ArtChain offers a free art management system as an entry point for galleries. This low-risk introduction gradually familiarizes users with blockchain features, reducing barriers to adoption. Bahbouh’s approach reflects strategies discussed to overcome technological scepticism and encourage innovation dissemination within the relatively conservative arts markets.

In one of the replies, Bahbouh emphasized accessibility and affordability as core values of ArtChain. By integrating blockchain technology into a free art management system, the platform removes the need for costly equipment and additional staff, making advanced tools available to even the smallest galleries. This focus on accessibility aligns with the thesis’s emphasis on creating technological solutions that lower entry barriers and foster adoption.

The role of authenticators and validators is central to ArtChain’s ecosystem. Bahbouh detailed how the platform is building a network of skilled experts to verify artwork authenticity, acting as decentralized nodes within the blockchain system. These validators undergo rigorous vetting to ensure credibility and maintain trust in the network. This decentralized yet credible approach ties directly to the thesis’s exploration of blockchain’s potential to disrupt hierarchical structures in the art market while maintaining trust and reliability.

Bahbouh also highlighted the impact of ArtChain’s partnership with the Czech regulatory body responsible for tracking and distributing artist royalties. He noted that royalty collection has traditionally been a complex and inefficient process, but ArtChain’s blockchain technology automates tracking and simplifies distribution. This collaboration not only resolves a key inefficiency but also supports the thesis’s focus on how blockchain can ensure fair compensation for artists and streamline market processes.

Overcoming scepticism about blockchain has been a challenge, particularly given its association with speculative NFT trends and its innovative nature. Bahbouh shared that starting with a practical and accessible entry point, such as the free art management system, has been crucial to building adoption among galleries. Once galleries experience the tangible benefits of the system, they are more willing to explore blockchain’s advanced features. This strategy aligns with the thesis’s analysis of how practical demonstrations can reduce resistance and promote adoption.

Looking ahead, Bahbouh envisions ArtChain becoming a trusted standard in the art market. Whether galleries use it as their primary inventory system or integrate it with existing tools, the long-term goal is to enhance transparency, trust and collaboration across the global art market. Bahbouh’s vision ties into the thesis’s exploration of blockchain as a transformative tool capable of creating a fairer, more efficient ecosystem.

Finally, Bahbouh highlighted the potential of ArtChain to standardize fragmented market practices and reduce fraud through transparent provenance tracking. He underscored transparency as a top priority, noting that the lack of clear provenance and opaque transactions erodes trust in the market. This focus aligns directly with the thesis’s argument that blockchain can address these critical pain points, creating a more equitable and trustworthy art market for all stakeholders.

Discussion and Conclusions

This article provided insights into the strategic decisions of art industry stakeholders regarding NFT technology adoption (Guan et al., 2025; Mukhopadhyay, 2025; Pradana et al., 2025). Overall, it can be said that there exists a gap between the perceived utility of blockchain systems and actual NFT utilization. It reflects a prudent evaluation of technologies offering theoretical potential but presenting implementation challenges, legal uncertainties and market volatility concerns (Dey & Ghose, 2025; Dvouletý et al., 2025). This finding supports Chalmers et al.’s (2022) recommendation that NFTs should be approached with caution, given current market conditions.

The analysis identified specific correlations between NFT utilization and economic outcomes within the Czech context and contributed thus to the regional body of knowledge (Prokůpek, 2024; Tichý & Petrová, 2024). Art stakeholders appear to recognize specific affordances while questioning the practical value for their particular business contexts. It is a matter of interpretation, whether to view low adoption rates as barriers preventing beneficial innovation or as sound risk assessment by informed and rational art industry actors dealing with potentially speculative innovation. These findings have several implications for cultural entrepreneurship research and practice. First, adopting digital innovations in traditional industries requires understanding the industry-specific constraints, such as cultural values, established relationships and risk tolerance levels. Second, the gap between affordance recognition and realization suggests that technology potential alone is insufficient: entrepreneurs must also address practical implementation challenges.

In terms of stakeholders, our results suggest that the current regulatory uncertainty might be a factor in the actors’ strategic decision not to invest in blockchain-based technology. Addressing issues around the NFTs’ legal ownership status, as well as inconsistencies across jurisdictions, seems to be the necessary precondition to broader NFT adoption in the art industry. The article also offers a stakeholder perspective advocating for the adoption of digital solutions to help solve the typical challenges in the traditional art industry, such as provenance and authentication, royalty management, market access and trust. The provided insights align with the digital affordance theory (Abaddi, 2025), which highlights that the gradual integration of innovation (NFTs) can be an effective strategy to scale up the art business and expand its outreach to the global audience. Progressive digital implementation can lead to reducing information asymmetries and process inefficiencies within existing industry frameworks.

Lastly, the authors need to discuss the limitations of this research and, relatedly, ideas for future research. The main limitations of this article are linked to its focus on a single regional market (the Czech Republic), a relatively small sample size (N = 35) and a cross-sectional design (one-time data collection). Future research should examine longer-term adoption patterns as blockchain technologies mature and regulatory frameworks develop. Cross-national comparisons would be beneficial in exploring regional differences in NFT adoption and its outcomes. Longitudinal studies tracking changes in adoption rates and impacts over time would provide deeper insights into the evolving role of NFTs in the art market. Additionally, qualitative research, such as interviews or focus groups with artists and gallery owners, could offer nuanced perspectives on the barriers and opportunities presented by this emerging technology.

Despite the abovementioned limitations, the findings provide new knowledge into how traditional cultural industries evaluate emerging technologies (Woronkowicz, 2021). They contribute to a better understanding of entrepreneurial decision-making under uncertainty in established markets (Kurdoglu et al., 2023) and illustrate the broadening locus of entrepreneurial agency as proposed by the theorists of digital entrepreneurship (Autio et al., 2018). Our findings also align with the general caution in assessing NFTs’ disruptive and transformative nature. Most discourse around blockchain-based digital art is promissory, focused on potential future effects, rather than on current tangible effects, which seem to be rather small since the bust of 2022. Our findings also invite caution, and their ambition is to reflect on strategic choices rather than to decry actors’ unwillingness to innovate.

It seems equally important to reflect upon this research in the broader environmental and social reflection on digital technologies. Indeed, digital entrepreneurship studies should not lose sight of ethical concerns surrounding the rapid pace of digital progress. While digital solutions undeniably offer increased efficiency and lower costs to businesses, they are intensive in resources and therefore generate negative externalities in terms of environmental damage and treatment of vulnerable workers in both the Global North and South (Bega et al., 2021; Rao & Liefner, 2023). As we welcome the capacity of blockchain-based digital platforms to disintermediate transactions, our assessments should not omit to account for the low-paid invisible labour and the ethical concerns it raises, as noted recently by Cassili (2025).

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.