Abstract

This article examines the South African financial system for start-up companies, and focuses particularly on the support provided by the Khula indemnification scheme. Most research rests on the assumption that a lack of finance is the sole impediment to success of start-ups; however, it is unclear whether such government intervention can indeed foster successful entrepreneurial activity. We show that the current system provides profit-making opportunities for both banks and consultants, but lacks a focus on sustainable business development. There are incentives to create companies not in an attempt to be profitable, but rather as a means to gain access to government or government-backed money. We question whether a lack of finance is the primary obstacle to the formation of businesses. Instead, we argue that it is a lack of accountability and an insufficient application of business tools such as basic cost accounting that make entrepreneurs less creditworthy.

Introduction

Small, medium and micro companies (SMMEs) are often presented as a means to overcome poverty (Beck et al., 2004; Venter & Neuland, 2005). Many initiatives from international agencies like the World Bank Group engage with developing economies in supporting their SMMEs to accelerate growth and to create employment. South Africa, considered the leading economy in sub-Saharan Africa, is no exception. After the abolition of apartheid and the free elections of 1994, South Africa looked to the potential of SMMEs to spur economic development, and in March 1995 the government released its White Article on National Strategy for the Development and Promotion of Small Business in South Africa (South African Government Information, 1995). However, high unemployment persists and had reached 25 per cent in March 2011 (South African Reserve Bank, 2011). Co and Mitchell (2006: 348) state that, ‘it is not surprising, therefore, that it is now widely held that the only way for South Africa to effectively address unemployment and revitalize the economy is through the rediscovery of the entrepreneur who takes risks, breaks new ground and innovates’. The role of the government in supporting the growth of start-ups, however, is ambiguous (Lerner, 2009); for example, Reid and Smith (2000) showed that access to government grants has little or even negative influence on the performance of start-up companies.

The aim of this article is to review one specific government initiative on SMMEs and to analyse how successful they have been in achieving their stated goals. The support system for SMMEs in South Africa is vast and includes different levels of government involvement, private business initiatives and not-for-profit organizations. This article focuses on a very specific element of government support, namely, the Khula indemnity scheme for bank loans to SMMEs. We wish to contribute to an understanding of government initiatives for entrepreneurship in emerging markets as most current literature targets government initiatives in developed nations. This is important as there are conditions specific to emerging markets, which suggests that analysis must be sensitive to these specificities and not just apply approaches derived from developed economies uncritically (Smallbone & Welter, 2001).

We identify three groups of actors relevant to understanding and analysing this programme: the government agency Khula, which offers the indemnification programme; the banks that give credit to prospective entrepreneurs; and third-party consultants, whose services for prospective entrepreneurs are financed by the Department of Trade and Industry. Our study critically analyses the impact of this programme and questions the assumption that a lack of capital is the only impediment to success. Further, we aim to contribute to the wider debate about the purpose and impact of government intervention in the field of entrepreneurship.

The article is structured as follows. We begin by reviewing the obstacles and challenges to the development of start-ups in emerging markets, with a special focus on South Africa. The next section provides an overview of policy development with regard to SMMEs in South Africa. This is followed by a description of the Department of Trade and Industry and its agency, Khula, which administers the credit indemnification programme. We then describe the credit indemnification process and the different views and perceptions of the key actors. The article concludes with an analysis of the credit indemnification scheme.

Method

We conducted a total of 14 in-depth, semi-structured interviews with key personnel from Khula and four major banks, and with six individual consultants. At Khula, we conducted interviews with decision-makers at the provincial level who have contact with clients. In the banks, we focused on credit agents and their managers. In addition, we conducted interviews with third parties, such the Chamber of Commerce and consultants. The interviews were conducted in the first half of 2009, over a period of three months. The first part of the interviews focused on the self-understanding of the managers in the institutions. In the second part we asked specific questions relating to the types of business plan or support they offer to the entrepreneurs. The interviews, lasting between 45 minutes and an hour-and-a-half, were recorded and transcribed. We were looking for agreement and dissonance in ascribed meanings and procedures between the different institutions. Further, we tried to capture our interviewees' understanding of the other institutions and their contribution to overall effectiveness in enhancing entrepreneurial success.

Obstacles and challenges to the development of small business

Barriers to the start-up and growth of SMMEs have long been a subject of research. This topic gained particular attention when the countries of the former Eastern bloc opened up their economies after 1990 and saw SMMEs as a promising route to both provide new employment and create economic growth (Roberts & Tholen, 1998). Outside of Central and Eastern Europe, research by Almus and Nerlinger (2000) supported this approach in relation to Germany, and likewise did Farinas and Moreno (2000) in relation to Spain.

Previous work on barriers to business activities have identified the challenges to SMMEs as including (Smallbone & Welter, 2001); first, formal barriers such as high taxes (Bohata & Mladek, 1999; Bartlett & Bukvic, 2001; Hashi, 2001) and the regulatory environment (Hashi, 2001); second, informal barriers including the implementation of regulations (Jancauskas, 2000; Bartlett & Bukvic, 2001) and corruption (Bohata & Mladek, 1999); third, environmental barriers such as a lack of finance (Pissarides, 2000; Bartlett & Bukvic, 2001; Hashi, 2001); and, fourth, a lack of skills on the part of entrepreneurs, key personnel or both (Roberts & Tholen, 1998).

Government support is often structured around environmental barriers, particularly the lack of finance (Kaivanto & Stoneman, 2007). In developed and emerging economies alike, SMMEs find it difficult to tap into financial resources to fund their activities. However, knowledge of the effects of policy initiatives on SMMEs is very limited and few studies have analysed their impact. Audretsch and Fritsch (2002), for example, investigated how private sector R&D in the US was supported through the Department of Defense's Small Business Innovation Research (SBIR) Program. They found evidence of R&D being stimulated and efforts to commercialize outcomes being enhanced. This initiative is strongly engaged in both public and private research initiatives and therefore goes beyond purely financial support.

In Japan, Honjo and Harada (2006) studied the effect of the SMME Creative Business Promotion Law (CBPL) on SME development. This law was designed to support start-ups, R&D and the commercialization of products and services. The initiative included policy tools, such as subsidies, loans and tax breaks, provided that the business plan was approved by prefectural governors. The study found that approved SMMEs showed an increase in assets, and further that there was an impact on the growth of younger SMMEs. In general, there is agreement that financial constraints are detrimental to the growth of SMMEs (Chittenden et al., 1996; Becchetti & Trovato, 2002; Carpenter & Petersen, 2002).

Aidis (2005) takes a wider view arguing in favour of examining the interrelatedness of business barriers, suggesting that studying one barrier in isolation from others is of little use. This is most obvious in the case of a lack of both finance and business skills. Banks may be reluctant to lend money to entrepreneurs who seem to be financially illiterate. To relieve the problem of underdeveloped business skills, assistance programmes are often offered to novice entrepreneurs. For example, in the US between 1987 and 1996, micro-enterprise assistance programmes grew from fewer than ten to more than 200 (Schreiner, 1999). Previous studies suggest that intervention or support at the start-up stage is indeed capable of reducing high failure rates (Deakins et al., 2000). Such interventions are expensive in both money and other resource commitments for sponsors and service providers, and in terms of the entrepreneurs' time (McMullan et al., 2001). It is worth noting that the policies we have examined to date have been drawn largely from developed economies. We now turn to the South African experience.

Policy development in regard to SMMEs in South Africa

The South African government's policy for SMMEs was encapsulated in the 1995 White Article on National Strategy for the Development and Promotion of Small Business in South Africa. The rationale underpinning the article was that:

With millions of South Africans unemployed and underemployed, the Government has no option but to give its full attention to the fundamental task of job creation, and to generating sustainable and equitable growth. Small, medium and micro-enterprises represent an important vehicle to address the challenges of job creation, economic growth and equity in our country (p. 2).

Ten years later, in 2005, the Department of Trade and Industry (DTI) issued its Integrated Strategy on the Promotion of Entrepreneurship and Small Enterprises. The article attempted to identify the success factors of the small business sector and sought stronger engagement to enhance the performance of the sector. The aim was to remove constraints on new ventures so that they could withstand the challenges of competing against big business. The focus was on maximizing opportunities through a favourable legislative environment.

In the 2005 article, the DTI also revealed the political aspect of its intended intervention. Fostering new players in economic activity was seen as critical to addressing the ‘historically skewed patterns of socio-economic quality of life’. This is one of the conditions that can be seen to be specific to the South African condition. The government adopted a very liberal approach to SMMEs and saw restrictive bureaucratic requirements as the main obstacle to their development. This was done under the patronage of the DTI, which, up to the present day, has a strong influence on the situation of SMMEs. It facilitates a wide range of products and services such as loans and incentive grants that play an important role in enabling access to finance for small enterprises. Khula Enterprise Finance Limited facilitates access to finance and has developed a variety of financing products, including credit guarantee schemes in which it has partnered with the country's major commercial banks to allow lending to small enterprises. The Thuso Mentorship Scheme offers support for business plan development and other advisory assistance to small enterprises seeking to access finance under Khula's Credit Indemnity Scheme.

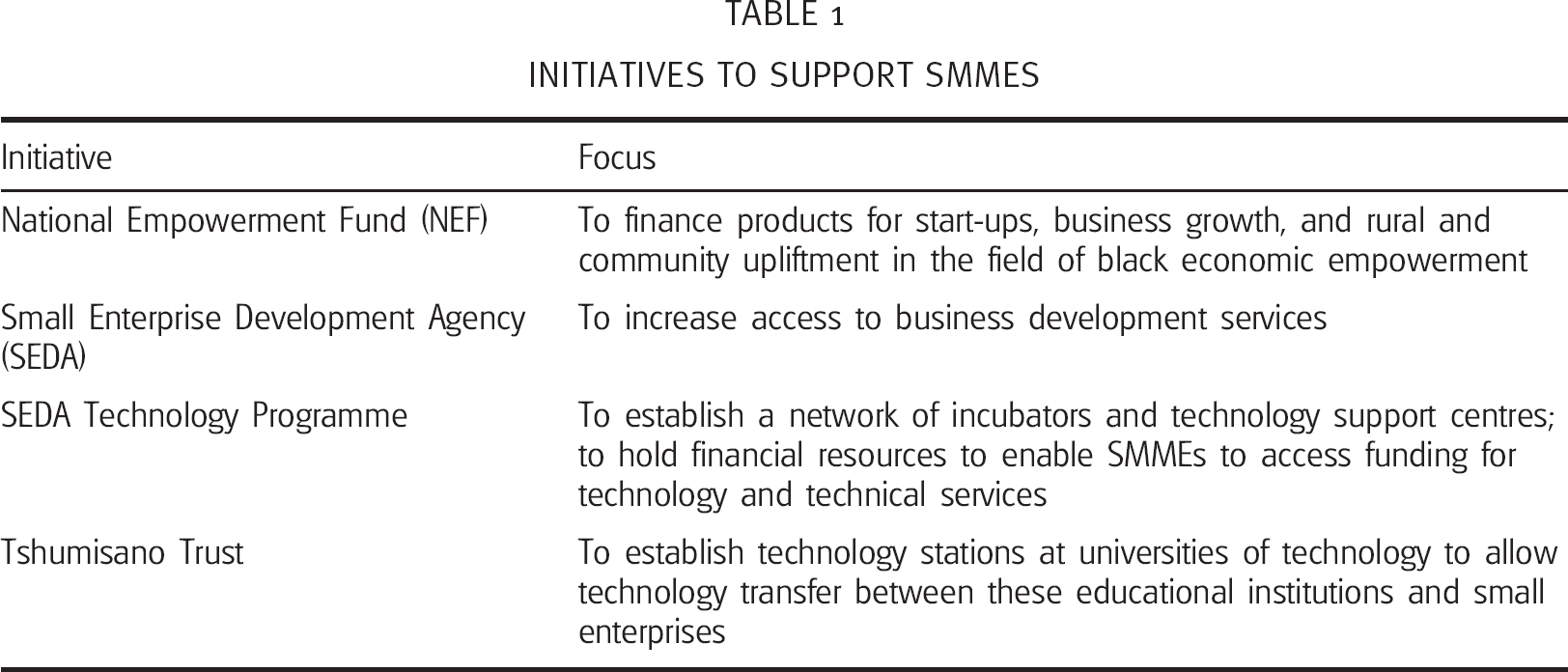

The DTI's initiative was very ambitious. It was planned to address what was seen as market failure, and was aimed in particular at: micro-enterprises; informal enterprises; enterprises owned by black people, women and youth; growth-orientated enterprises; and enterprises in priority sectors like tourism, construction, agriculture, cultural industries and information and communications technology (ICT). The proposed policy was geared towards improving the efficiency of government small business support services by, for example, the integration of the activities of different entrepreneurship and small-enterprise promotion institutions, as well as a stronger collaboration with the private sector. A number of the initiatives are summarized in Table 1.

INITIATIVES TO SUPPORT SMMES

There are also several NGOs and corporate institutions providing their own support programmes for start-ups such as the youth enterprise support programmes of South African Breweries (SAB Kickstart), Anglo-Zimele, and Shell Petroleum (Shell LiveWire). Major banks have also begun sponsoring financial-literacy programmes, mostly targeting high-school students.

We continue by describing Khula Enterprise Finance Limited, which administers the DTI credit indemnity scheme.

Khula Enterprise Finance Limited

Khula was established by the Department of Trade and Industry in 1996, soon after the first democratic elections in 1994. It was founded to address some of the difficulties that start-ups faced when they applied for finance. As many of the new entrepreneurs did not have any capital for collateral, banks rejected their applications for credit. Despite a business's potential and its likely ability to pay back the debt, the banks often denied funding. The problem is rooted in South African history. The majority of the population was excluded from economic activity and was never able to acquire assets. As workers were paid minimum wages, sometimes below the bread line, the accumulation of capital was extremely difficult. Thus with no assets behind a business plan, no matter how promising, banks were reluctant to lend. To overcome this historical inequality, the government set up a fund that would offer indemnities to private banks – Khula. Although a bank would still make the lending decision, Khula would indemnify the bank in the event of losses.

Khula describes itself as a development finance institution, focusing on small business. It acts as an independent agency of the DTI and plays a primary role in the growth of SMMEs. This position was achieved through ‘adapting to prevailing market forces within the sector and changing its approach to meet the demands of what has become an increasingly valuable sector in the development and growth of the South African economy’ (Khula, 2007: 3).

However, by 2007 problems were becoming apparent. In 2007, Khula achieved a net profit of US$4.53 million (the exchange rate on December 2007 was US$/ZAR 6.84). Its capital was US$146 million and the value of its investment property amounted to US$22.1 million. Khula's core business commitment at the end of 2007 thus totalled US$68.27 million. The year 2007 was the first to see more approvals going to retail financial intermediaries (US$43.56 million) than to the commercial banks (US$38.9 million). The net profit was driven by increased revenues earned on business loans and financing activities and significant growth in the fair values of investment property. The rise in earnings from business loans and other activities was largely due to rising interest rates. US$1.9 million had been received as fees for the indemnity, and US$2.19 million as interest for lending operations. The bulk of the revenue was achieved through investment income (US$8.92 million) and net fair value gains on financial and other assets (US$5.7 million). In 2006/07, the ratio of claims paid to net earned fees was 146 per cent (2005/06 206 per cent). Its unexpired risk reserve was raised by US$1.87 million to a total of US$7.3 million.

In its 2010 annual report, Khula stated that, ‘although the need for assistance remained unabated, Khula did not have the capital resources required to maintain the impetus of its lending’ (Khula, 2011: 32). Further, increasing numbers of applications have been declined by banks despite the backing of Khula. Further, Khula ‘cannot commit to new approvals without capital from its shareholder. Although approvals were planned to reach about R700 million [US$102.2 million], this was unachievable’ (Khula, 2011: 33). In 2010 the indemnity fees that Khula collected for its service fell by 28 per cent. There are obvious weaknesses in Khula's business model and it struggles to deliver the support to SMMEs that it is supposed to provide.

In the next section, we analyse the process of the indemnification and highlight strengths and weaknesses of the system.

The application process

The first step for Khula is to screen the applicant and the business idea. The assessment is based on how the business model and development plans correspond to the financial plans. At this stage, the Khula's level of expectation is quite low, as one of the employees in charge of evaluating business ideas explains:

We look at if the person has done the homework on their business. Too many are coming to us to say we are wanting to start a business and then they have done nothing about it. We do not expect you to have all the answers, but we just want to know that he's got an idea (Employee, Khula).

If Khula has reservations about the quality of the business plan or if there is no business plan at all, Khula sends its clients to external service providers who help the applicant to translate his or her business idea into a presentable business plan. The organization is aware that this process carries the danger of a decoupling between the potential entrepreneur and the business plan, which may come to more strongly reflect the criteria of Khula and particularly of the banks. Despite Khula being aware of this potential problem, managers in the organization admit that many of its applicants simply lack the skills to do the financial planning themselves:

Let's be realistic. It's an assumption, but one has to be able to give me some sort of indication as to why they got to that assumption, what does he think, what are they going to do to get to that 500 000 Rand turnover within his first trading month. The entrepreneur that runs the business doesn't have the financial skills. A lot of it is dependent on my service provider to put those numbers together, obviously with the help of the client, and if I look at those numbers and I'm not happy, I will ask my service provider to give me details as to how they arrived at those figures (Regional manager, Khula).

If Khula sees a reasonable chance that the bank may be satisfied with the business plan and the application, the applicant is referred to the bank. The bank's criteria for evaluating the plan are in line with Khula's approach, namely, establishing the experience and expertise of the applicant and endorsing the feasibility of the idea. The bank will also offer support in drafting a business plan.

Interviewees from the banks claimed that they were ‘very selective’ and had a good sense of whether a person had the potential to be an entrepreneur. In the context of mass un(der)employment, the question of conscript or volunteer to the ranks of the entrepreneur is important. If the person has chosen this route simply because there are government incentives to start a business, it might well be that the applicant will walk away from the venture as soon as an opportunity for conventional employment arises:

At the moment we have a lot of clients going into business because of push strategies, unemployment or retrenchment or whatever the case may be. The first opportunity for more secure employment comes along and he exits the business to go and work for a larger corporation (Branch manager, Bank B).

Once the bank agrees to fund the proposal, it applies to Khula's head office for the indemnity. The client is carefully screened to ascertain whether he or she meets all the criteria and Khula checks the bank's risk assessment.

As the prospective entrepreneur only covers a small portion of the cost of consulting for the business plan or complementary studies, there are incentives to over-consume the services offered. Also, many of the entrepreneurs have little idea of what to expect and find it hard to evaluate the quality of the service they have received. As one of the business consultants put it:

You pay R200 [US$30], and you get a voucher for a business plan. Pay another R200 for another voucher and you get a feasibility study. That sounds great. However, many of the service providers offer quick fixes and do both in two days. They are getting paid hundreds of thousands of Rand each month. To my knowledge, the department spent around R8 million for service providers. Less than 1 per cent of those business plans these guys set up actually made it up to the application desk (Consultant C).

The processes involved in applying for funding and for indemnity are extensive –sometimes more than the applicant expects.

Risk assessment

The successful applicant has to make a contribution – either in cash or in assets – a minimum of between 2 and 10 per cent, depending on how much money he or she needs. The bank then judges the risk and makes a final decision. Khula indemnifies the bank against write-offs, meaning that the bank would first have to liquidate all assets from the client before it can approach Khula for indemnification.

Even if Khula provides indemnity, the banks reported that they were exposed to significant risk:

There are checks and balances that we need to cover and look at because they can repudiate our claim for numerous reasons. Just to give you an example, a client needs to offer up to 10 per cent; if they are looking for one hundred thousand they need to offer up, let's say in this case, ten thousand Rand cash, a client says that, that was a gift from a relative. Khula says that's fine – give us the gift letter. The client gives the gift letter from the relative, the business fails and the bank submits a claim to Khula. Khula would do their investigation as in any claim to discover that there was a transfer of funds of ten thousand Rand from one business, that the client was also a member of, into the new business account. It wasn't a gift at all and the client was a member of quite a number of businesses for interest, which wasn't allowed by Khula. It is the bank's responsibility to do those checks upfront, so there is a joint responsibility upfront (Branch manager, Bank C).

From 1 million to 3 million we are covered only to 70 per cent so we need to find 30 per cent tangible cover, but otherwise we are covered (Branch manager, Bank B).

One potential field of conflict for the banks regards the pricing of risk. As the largest portion of the credit the bank grants to its applicants is indemnified by Khula, an issue exists regarding how much interest the bank should charge:

The interest rate is prime plus 2 per cent; that's a legal agreement. Whether the banks stick to that agreement is another matter. I think the banks feel that the risk is not adequately covered, but at the moment the agreement between the bank and us is that the rate would be prime plus 2 per cent (Regional manager, Khula).

Although there is an agreement with Khula to charge prime plus two, the banks considered this insufficient to cover the risk:

That has worked on a return on equity model, so we've got a model that we plug the loan into, which will say to what the loan to value can be. Obviously the more security the better and if there's Khula in there then we know it's pretty stable, then we'll give the client a better rate. And also our return: we look at a bench mark of RoE of 25 per cent, which is what our shareholders would expect to earn on that type of lending and a return on the asset of about 1.5 upwards. Anything below that, then we say this deal is not priced correctly, then we add more in order to get the RoE up (Branch manager, Bank B).

Assessing the entrepreneurial qualities of the applicant

For Khula, it is crucial to understand the entrepreneurial qualities of the applicant. Yet the process is anything but formalized and relies heavily on the individual analyst's perceptions. Experience in the industry, for example, is a strong asset:

I think that we all ponder on that question, who is an entrepreneur and what is an entrepreneur. I think the word is used a little bit too loosely. … But sometimes it's just gut feeling … remember that the most critical aspect is the jockey, in any credit assessment application, it's the jockey (the prospective entrepreneur) (Regional manager, Khula).

The banks demand that their customers have an in-depth knowledge of their own environment. The entrepreneur has to demonstrate that they have done the research necessary to understand supply chain management and pricing issues, as well as to identify their competitors and their target market:

Small businesses fail mainly due to management and not to external factors. It's all about management, bookkeeping, marketing, sales issues, and staffing issues. A very small percentage is coming from outside the business. The rest would be controllable, especially in the small business space (Branch manager, Bank A).

For the business consultants we interviewed, the lack of knowledge on the side of prospective entrepreneurs was their most prominent problem. The consultants we interviewed saw this point as more pressing than limited financial resources. Many of their clients had good and feasible business ideas, but had little to no understanding of how to run a business. According to the consultants interviewed, these potential entrepreneurs lack basic business skills. Further, the applicants could see a business opportunity but many of them found it difficult to correctly price their product:

Many of them get ripped off by their buyers. They say ‘cool, black business’. Then the customers are buying in big numbers and offering a much lower price per unit. The supplier is often so happy and overwhelmed by the big order that they do not realise that they are selling too cheap (Consultant A).

Mentorship

Khula is aware of the limited skill-set of many of its applicants. If Khula agrees to provide the indemnity, in an attempt to make sure that the indemnification does not need to be used, the client is granted access to a mentorship service. Khula employees visit the client at their premises and, in discussion with them, identify the weaknesses that they need to address.

More recently, Khula, together with the banks, is putting a lot more emphasis on the mentoring once finance has been granted. This includes quarterly checks by the business manager, which focus on management accounts and reviewing the accuracy of the projections in the business plan. A copy of the financial statement is submitted annually in order to review the progress of the business. At the end of their mentorship, Khula interviews the client on a one-to-one basis to establish how far the mentorship has been successful and there are procedures in place to review those receiving poor reports:

It's not always the mentor's fault, sometimes it's the client, and that is one thing that we have found: that it is generally resistance by client for someone to come in and assist them (Employee, Khula).

In addition to the consultants' view that Khula insures too many bad risks, the major criticism was the lack of support given:

I do not even want to use the word ‘mentorship’. Those programmes that are out there are worth nothing. They basically try to make sure that Khula does not have to pay. They do not explain anything. The business people do not learn how to run their business (Consultant B).

Khula's performance measurement

Khula measures its own performance by the number of applications that successfully pass the bank's assessment, which explains why they make use of consultants to aid business planning in order to endure that their clients overcome potential hurdles:

We try and make sure that we meet a target of a 50 per cent success rate; every second plan we send to the bank should be approved. That's been very difficult. I think a lot of the issues are that – now that the market we deal in is mainly focused on start-ups and start-ups are obviously a higher risk, that's the process (Regional manager, Khula).

The applications may be prone to overstatement and Khula has insufficient resources to follow up and validate information provided by the interviewees. Therefore Khula keeps close contact with the service providers who set up the business plans with applicants; they are able to gain deeper insights into the applicants' suitability by asking more probing questions.

Conclusion and discussion

The research shows that both the banks and Khula view themselves as being actively engaged in ensuring that a business proposal passes successfully through their internal assessment procedures. If the banks experience reservations about the business plan, they offer support to the applicant. Khula's approach to the prospective entrepreneur is often uncritical. In the first instance, no business plan is demanded; rather, all that is necessary is having a good idea. If Khula is unsure about the potential of the business plan, it brings in an independent business plan consultant. The drive to assure that as many applications as possible pass successfully through the system is spurred on by Khula's internal performance measurement system, based on the number of successful applications.

On closer examination, there seems to be a degree of mistrust between the different agents involved in the process. The banks have reservations about the reliability of the assessment of the applicant's assets, which results in concerns about the residual risk they bear. The consultants, on the other hand, see the mentoring programme on offer as ineffective.

We can now begin to explain the problem that Khula faced in 2007. Considering the system as a whole, it appears that Khula offered short-term aid with longer-term negative consequences. This is evidenced in the fact that there was a significant failure rate as applicants were unable to make effective use of their funds. In some cases, the interest payments eroded the capital base until they went bankrupt. As the entrepreneurs were only contributing a small percentage of the capital, they were incentivized to carry on longer than they would otherwise have done, or to take on more risks than they would have, if they had invested their own capital. Ultimately, Khula provides incentives for enterprises to be started up not purely because of their business ideas but as a means to get access to government or government-backed money.

Eventually, the problem of moral hazard becomes apparent. The experience of Khula was in line with prior research that states that the prospective entrepreneur's knowledge and suitability for the job is far more important than access to financial means. The lack of business acumen as the actual, and critical, hindering factor for start-ups confirms the findings of a 2010 Global Entrepreneurship Monitor (GEM) report (Herrington et al., 2011) on South Africa. This suggests that ‘questions also need to be raised about the quality of early-stage entrepreneurship in South Africa, particularly regarding the business and personal management skills of the entrepreneurs’ (p. 18).

Currently, there is no measurement in place to monitor mentors' input to the businesses they are paid to support – and in particular no incentive for the mentors to do more than the absolute minimum necessary. In response to this, Khula now engages with mentees to assess their level of satisfaction with the consultation. This reflects the findings of Yusuf (2010), who found very low satisfaction rates with their assistance programme among novice entrepreneurs and concluded that it might be very difficult for these entrepreneurs to voice their needs.

Government support through Khula converts SMMEs into an interesting and profitable business activity for banks and private consultants. Although it was agreed that the rate of interest is fixed at prime plus 2 per cent, banks charge a higher rate if they assess projects as more risky.

Determining the success of government initiatives such as Khula is a difficult task. Khula provides the resources and opportunity for potential entrepreneurs who might otherwise be unemployed. There surely are success stories in Khula's portfolio. Although Khula purports to operate on a commercial basis, the ratio between applications funded and fees earned suggests that Khula does not price risk correctly. As a consequence, Khula, and thereby the South African taxpayer, bears the burden of the failure of these early ventures. It could be suggested that the main beneficiaries are the banks and consultants. These findings stand in stark contrast to the positive reports on government initiatives found in previous research in other countries (Audretsch & Fritsch, 2002; Honjo & Harada, 2006). We suggest that the main reason for Khula's lack of success lies in its rather short-sighted approach. The main focus of its activities rests on the supply of capital for SMMEs, but the real problem, namely the lack of business knowledge, is sidelined and passed on to third parties. Problems with mentoring or consulting services for nascent entrepreneurs have already been described in earlier findings (Yusuf, 2010). Further, our findings also contradict a wide body of literature that blames the failure of SMMEs primarily on the shortage of financial resources. Rather, the lack of business acumen seems to be at least as much of an obstacle as the limited access to capital.

One area for improvement would be to change the short-term performance measurement of Khula to a more long-term orientated approach. Instead of measuring the number of applications approved, a focus on the three-year survival rate of the companies may be more promising. In conclusion, we suggest that the money spent on direct government initiatives to provide financial means to SMMEs would probably be better employed in educational initiatives, particularly as research has proven the connection between high levels of education and the high success rate of SMMEs (Dickson et al., 2008).