Abstract

The dominant role played by financial services within liberal market economies, and the 2008 economic crisis, has variously been depicted as the product of regulatory failure, ‘irrational exuberance’, the over-prioritization of shareholder value or as part and parcel of an epochal change in social and economic life. Current regulationist thinking suggests that recent developments represent a long period of systemic experimentation, evolution and change, which dates back to the end of the long boom in the 1970s. In this article, we introduce and discuss current regulationist thinking regarding systemic crisis, evolution and change, and follow on with a more detailed look at the diversity and varied outcomes associated with a key area of the financial services sector, private equity (PE) and public to private buy-outs of listed corporations (PTPs). We have chosen this area because of the critical importance of capital for innovation at the same time as investment horizons have generally become more short term, and the challenges that exist in reconciling these competing needs and agendas. We conclude that, as with any innovation and experiment, the outcomes of private equity are mixed. This would suggest that the emerging financial architecture that will inevitably comprise any return to growth will, in part, incorporate aspects of private equity. Indeed, to the extent that private equity buy-outs involve the acquisition of firms in distress, they may have a positive contribution to make in resolving the problems of recession and financial crisis. The failure of unsustainable experiments does not mean, however, that renewed growth will simply result through natural selection: it depends on continued innovation and experimentation across the entire economy, coupled with relevant formal and informal socio-economic regulation.

Introduction

The dominant role played by financial services within liberal market economies, and the 2008 economic crisis, has variously been depicted as the product of regulatory failure, ‘irrational exuberance’, the over-prioritization of shareholder value or, indeed, as an integral element of an epochal change in social and economic life (Boyer, 2009; Dore, 2009). Current regulationist thinking suggests that recent developments represent part of a long period of systemic experimentation, evolution and change, which dates back to the end of the long boom in the 1970s, and can be traced to a range of internal and external pressures, including significant changes in the costs of natural resource inputs (Lipietz, 2009). Such arguments are echoed in key areas of the business history literature, which argues that waves of particular types of activity are followed by periods of adjustment and consolidation (Hannah, 2005). Both these schools of thought would suggest that, within any long period of adjustment, certain rules and actions will cease to be viable, but that others will constitute elements of an emerging architecture of governance and practice. Innovations and experiments may take place at both the level of the firm and in broader societal governance: changes in one area are likely to impact back on the other. Hence, in using the term ‘innovation’, we are referring to three distinct phenomena. First, there is innovation in the formal and informal rules generally governing what corporations do in specific settings. Second, there is innovation in terms of the introduction of new products and techniques of production (Aglietta & Riberioux, 2005). Third, there is innovation in terms of original forms of financing, such as private equity and venture capital (ibid). These three phenomena are closely interrelated, and, in subsequent sections, we explore their interconnectedness.

In this article, we introduce and discuss current regulationist thinking regarding systemic crisis, evolution and change. Recently regulationist theory has been expande d and developed to take account of the co-existence of different firm types and ownership structure within the same institutional architecture (Boyer, 2012). This reflects broader interest in the bounded nature of diversity within national capitalist archetypes, reflecting sectoral and regional variations in institutional coverage, and the uneven and experimental nature of systemic change (Wood & Lane, 2012). As Jessop (2012) notes, there are important variations in practices, even if there are dominant trends within the global capitalist system. At the same time, the co-existence of differing capabilities and competencies may reflect complementarities or pathologies (Jessop, 2012: 216).

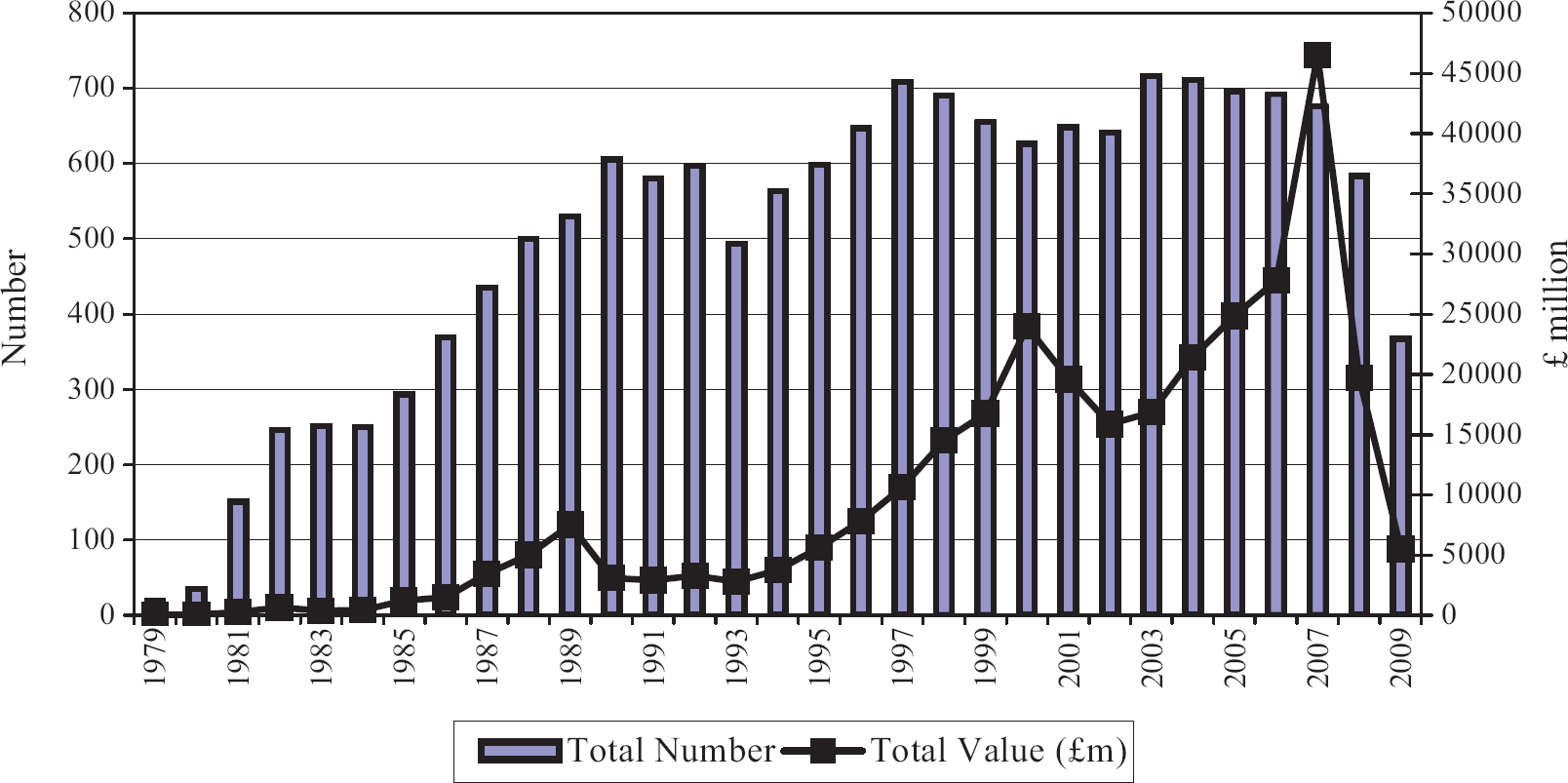

We follow this discussion with a more detailed look at the diversity and varied outcomes associated with a key area of the financial services sector, private equity (PE) and public to private buy-outs of listed corporations (PTPs). We have chosen this area because of the critical importance of capital for innovation at the same time as investment horizons have generally become more short term, and the challenges that exist in reconciling these competing needs and agendas. PE and PTP transactions present a particularly interesting context in which to examine these issues. They have become an increasingly important mechanism to rapidly and radically restructure listed corporations worldwide (Cumming et al., 2007; Kaplan & Stromberg, 2009). PTPs were especially a feature of the first private equity wave in the US in the 1980s and became especially important during the second wave, which reached its apogee in 2007 and has since declined sharply in the wake of the financial crisis (CMBOR, 2009). This trend is shown in terms of both the number but especially the value of deals in Figure 1, which is based on data collected by one of the authors through the Centre for Management Buyout Research (see below). As explained in more detail below, PTPs involve PE firms, backed by borrowings, acquiring a significant or majority equity stake in a listed corporation. Private equity firms are typically active investors who take board seats and benefit from fuller and more timely information on the current trading of their portfolio businesses. Private equity firms have been accused of asset stripping, profiting from the re-selling of assets within short periods of time (asset flipping) and instigating restructuring within firms that negatively impacts employment and employee remuneration. They have also been associated with the use of high leverage, often in the form of exotic debt instruments such as securitization and high yield debt that places particular constraints on firms and reduces tax charges (TSC, 2007). In this article, we explore positive (in terms of knowledge and innovation, and performance effects in specific areas and contexts) and negative (regulatory failures, irrational exuberance and excessive leverage, again in specific areas and contexts) features of this phenomenon, returning to this analysis in the concluding sections.

UK Buyout trends.

The article primarily concentrates on the case of the UK and the US, although some of the issues and trends pointed to have – owing to supranational pressures and the increased mobility of capital – broader relevance. In line with recent regulationist concerns with diversity within national institutional regimes and the experimental nature of change at both macro- and micro- levels (Boyer, 2006, 2012), we focus on diversity in practices and outcomes, common trends and key variations, and the wider systemic implications thereof.

Regulation theory: Understanding crises in historical perspective

Originating in economics, regulation theory has become one of the more influential – and nuanced – paradigms for understanding the relationship between institutions, firms and society (Jessop, 2001a: ix). What sets regulation theory apart from rational choice economics is that it rejects the notion that it is possible to provide a general ahistorical explanation for socio-economic life; rather, it holds that economi c growth represents the product of prevailing institutional frameworks and informal rules (which together constitute regulation) in operation over a particular time period (ibid: x). However, such frameworks and rules do not continue working forever: ultimately, the combinations of economic and extra-economic institutions and associated accommodations break down, leading to an extend period of transition and experimentation, prior to a new period of growth (ibid: xi). This mirrors thinking within the business history literature that points to long-term cycles in ownership and control relations, and the connection to economic growth, crisis and adjustment (Hannah, 2005), and approaches that locate relations within and between firms in terms of economic long waves (Kelly, 1998). In other words, regulation theory explores both the episodic crisis tendencies in modern capitalism, and ‘the likely sources of crisis resolution’ (Jessop, 2001a: xi).

The regulatory basis for periods of growth does not stem primarily from the law and state (cf. La Porta et al., 2002), but rather from the wide range of institutional factors and other mechanisms (including values, networks, procedures and modes of calculation) indirectly and directly involved in underpinning firm performance and overall growth (ibid: xi). To regulationists, an accumulation regime represents a complementary pattern of production and consumption that is reproduced over a period of time; the mode of regulation represents the ensemble of rules and informal ways of doing things that stabilizes the accumulation regime; in other words, the complex adjustment process linking production with social demand (Agleitta, 1976; Boyer, 2001: 19; Jessop, 2001b: xxvii). Where these and dominant industrial paradigms complement each other, they may secure for a period of time, a long wave of growth (Aglietta, 1976; Jessop, 2001b: xxviii). The economic crisis of the 1970s saw a breakdown of a paradigm centring on the Keynesian state, Fordist industrial production and a virtuous circle of wage increases and consumption; this represented the product of intensifying global competition, changes in input costs and the shelf life of existing policy prescriptions (Boyer, 2001: 23). Within liberal market economies, this led to a range of innovations in policy and practice, encompassing deregulation of rules governing financial institutions, changes in labour–management relations, tax reforms and so forth (ibid: 24). Aglietta and Riberioux (2005: 186) point to ‘waves of innovation’ modifying old forms of economic activity and creating new ones. This suggests a joint process of technological advance, innovation in firm finance and changes in shareholder behaviour and expectations. More specifically, they suggest two primary driving forces, the increased role of ICT and market finance, which have cross-fertilized and strengthened each other (ibid: 19).

However, at whatever level, these innovations have not succeeded in providing the basis for resilient growth and increasing general prosperity on the level encountered in the 1950s and 1960s; rather, this has led to both endemic speculative bubbles, with consumption being underpinned by debt (ibid). The implications of this are first, that neo-liberal predictions in the 1990s and 2000s of stable renewed growth and, indeed, the suspension of the business cycle were misplaced – as has been proven by subsequent events; even during those years, growth was poor by historical standards (ibid).

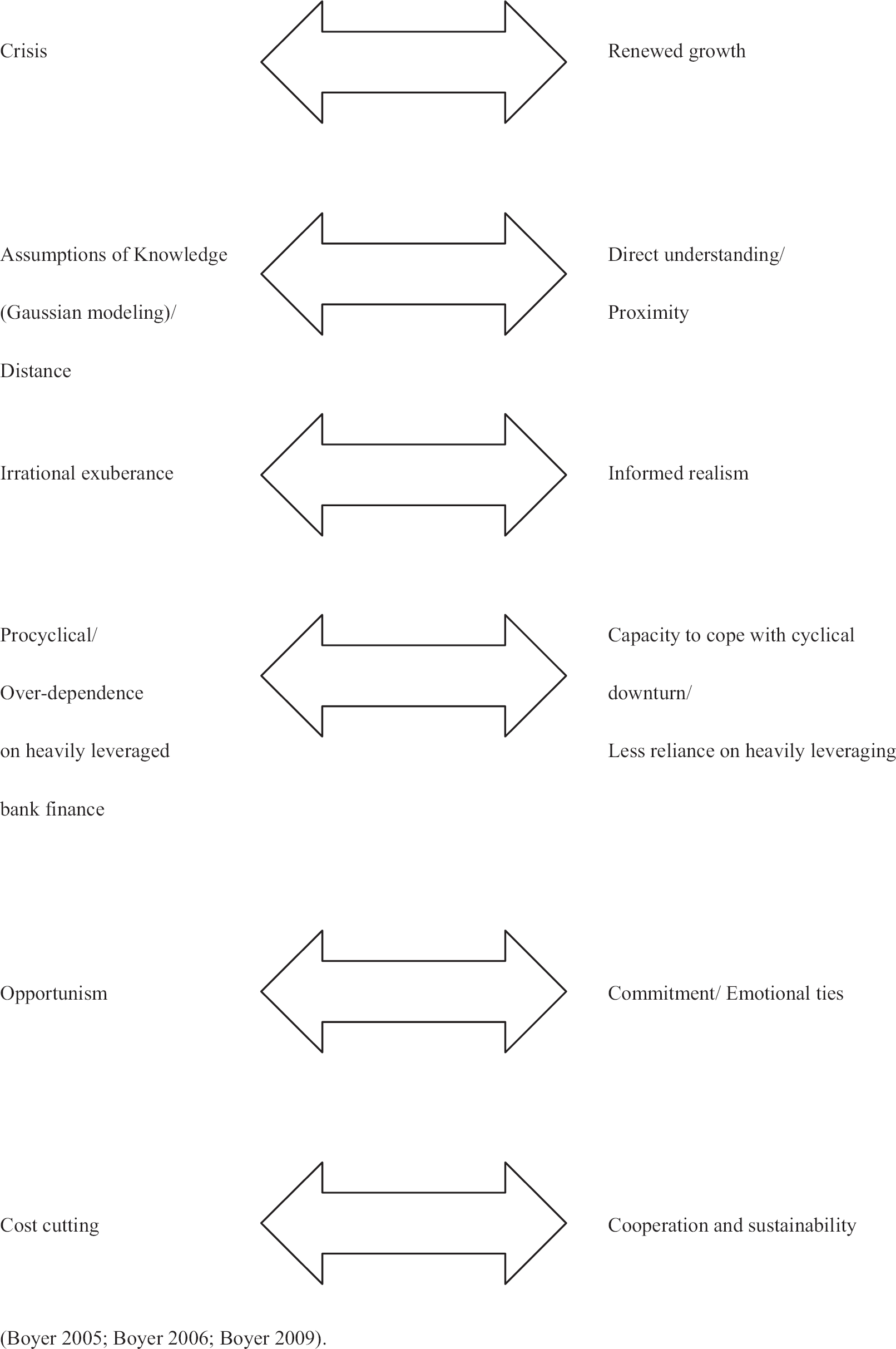

This would also challenge strands of thinking within the broad literature on financialization, which depicted the period as a distinct and coherent – even if evolving –phase with homogenizing outcomes (Engelen et al., 2008) Second, the 1970–present period cannot be seen as a coherent mode of regulation at all, given this mediocre performance and endemic instability (Wolfson, 2003: 259). Rather, the period may be viewed as one of sustained experimentation and adjustment: the assembly of rules and practices encompass both the causes of the present crisis and functional innovations that are likely to be a feature of a renewed period of growth. Figure 2 summarizes some of the key dimensions of the 2008 crisis highlighted above and, by implication, key aspects of renewal at firm level.

Dimensions of firm-level crisis and renewal.

Experimentation and change: Understanding the basis of innovation and crisis

In contrast to the work of writers such as Aglietta, Boyer (2006), who, influenced by classical institutional writings, accords somewhat more attention to the process of institutional design at key historical moments, whether by accident or deliberate choice, and the nature of complementarity. He suggests that a wide variety of mechanisms may generate complementarities, not only including innovations at firm or industry level, but also systemic reforms (ibid: 16). Further, complementarities may be the unintended outcomes of unpredictable parallel historical processes (ibid: 22); that is, growth may often be a process of accident rather than design. Complementarity may be imposed through top-down design; more often, it may be discovered ex post (ibid: 26). In other words, an emerging regime will reflect the upshot of a long period of ‘trials, errors and learning’; complementarities are likely to be discovered when a system enters decline or crisis (ibid: 26). Institutions that are supposed to be functional through design rarely prove to be so (ibid: 42). What this all points to is that systemic evolution – as in the natural world – is rarely linear, but more often about experimentation and rupture, interposed with periods of coherence (Hollingsworth, 2006).

On the one hand, each stage of this process may result in negative feedback loops, exacerbating negative tendencies. On the other hand, each stage is not associated only with one, but also a range of other experimental interventions, some of which will have more positive effects (Boyer, 2009). In other words, changes in regulation and practice led not only to renewed crisis, but new ways of doing things that, in some cases, are likely to work better than the old, and which are likely to persist into a new period of growth (Boyer, 2006; Hollingsworth, 2006).

Endometabolism, that is, the inner development of tensions within a particular institutional architecture is a major source of systemic change; change will involve recombination of rules, layering and conversion of convention and practice (Boyer, 2006: 54). A key question arises as to what direction systemic evolution is likely to assume. We would reiterate that at least part of the basis of any renewed period of growth is already in place. The eventual return to growth is likely to reflect the outcome of innovative experiments in ownership, in ways of managing present and redefined social relations, as well as certain aspects of both deliberate and unforeseen changes in regulations, rather than coherent policy design on its own. This has led to increasing emphasis on both trends and variations in firm-level relations encountered in recent regulationist work, imparting a greater concern for micro details in what was originally more of a macro approach (Hopner, 2005).

Early regulationist thinking suggested that key features of the Fordist era – both in terms of rules and firm-level practices – were shared across the advanced societies; in other words, there was an emphasis on common features of capitalism. This led to suggestions that Fordism would inevitably evolve into a post-Fordist era with, again, shared characteristics, which, it soon became apparent were mistaken (Jessop, 2001b). Rather, potentially viable alternative forms of capitalism coexist, both within and between contexts (Aglietta & Riberioux, 2005; Boyer, 2012). In other words, regulation theory has shifted from what was originally a theory focused on temporal difference to one that takes account of space and scale, albeit with a continued recognition of common pressures within the global capitalist ecosystem (Jessop, 2012).

Hence, Aglietta and Riberioux (2005: 259) highlighted the uneven consequences and risks of a focus on short-term shareholder value; at the same time, they suggested that, even in the US, the model has spread through a process of diffusion, rather than general substitution, with unlisted firms being partially shielded from this process. While this process brings with it many negative consequences (especially when compared to more stakeholder orientated forms of capital), they suggested that it may, in liberal markets, such as the US, lead to a virtuous circle of innovation-led growth, with venture capital shouldering risks of investing in emergent enterprises, in return for higher returns (ibid:96). They do, however, pose a caveat: the process depends on the ultimate stock market valuation of such companies, which may be marked by a ‘generalized craze’, given uncertainties in the value of innovations, and the challenges of effective regulation (ibid: 97).

Boyer (2005) argued that a systemic cause of crisis was that financial markets are actually more promise markets, rather than typical goods and services markets. Uncertainty associated with investments – and particularly innovative forms of investment – are matched with conventional financial valuations that, in practice, may lead to alternating periods of over-optimism and over-pessimism, with no guarantee of an ultimate convergence on a realistic basic value (Boyer, 2005; Boyer, 2009). Quite simply, it is assumed that financial valuations of a particular item in a perfectly operating market will converge. In reality, in a situation of imperfect knowledge, actors will tend to alternately under- or over-price (Boyer, 2009). The behaviour of bankers has been pro-cyclical: prone to take risks when times are good and be risk averse when times are bad, worsening the effects of any downturn (ibid). Again, this would suggest that those firms over-dependent on short-term bank finance will inevitably fare worse than those that are not. There is also the problem of ‘irrational’ exuberance on the part of specific categories of investor. The behaviour of financial players is often characterized by mimicry of others deemed successful, selective loss of memory in relation to previous crises and over-confidence in their own choices vis-à-vis those of other players (Boyer, 2005). In summary, in relation to innovations in ownership forms, one may see irrational exuberance, over-leveraging (if assets are over-priced) and a tendency to discard established informal regulations in response to either the promise of quick gains, or as a result of a rapid switch back to excessive pessimism.

More positive features can arise where managers have not just transferable but also emotional and intellectual sunk capital in the firm, such as where they acquire the firm through a management buy-out (MBO) (Gilligan & Wright, 2010). The creation of wealth is ultimately a collective enterprise, requiring ‘the effective coordination of competencies’ outside of narrow contracting via both cooperative forms of work organization and informal rules and commitments (Marsden, 1999; Boyer, 2005). Again, this is likely to make for superior performance outcomes.

In periods of growth, institutions and practices are rarely perfectly aligned, and there are coterminous pressures towards systemic reinforcement and systemic decay (Hancke et al., 2007). Even though there may be interposing long-term periods of growth and crisis, there is no evidence to suggest that these interludes may be of even or fixed duration. Especially during periods of crisis, both negative and positive complementarities can co-exist, with any tendency in a specific direction being self-reinforcing (see Boyer, 2006; Lane & Wood, 2012). In this specific case, the tension exists at a range of levels, a common theme being between cooperative action and realism, on the one hand, and adversarial short-termism and speculation, on the other. During such a process, interests that are not in direct competition may seek to work together to reinforce emergent ways of doing things, or simply concentrate on adversarial competition with their own direct competitors (see Amable & Palambarini, 2009: 138–139).

What this means is that given uncertainties, certain categories of investor – those with more direct knowledge of and interaction with the target of investment – are better equipped to cope than others. This would point to uneven outcomes, even during a period of crisis. Furthermore, there is the issue of agency. A strong prioritization of shareholder value does not always result in a management that serves the best interests of owners – or, for that matter, other stakeholders (Boyer, 2005). Rather, the diffusion of stock options and financial market incentives that were supposed to discipline managers, in practice often made for great opportunism (ibid). Thus, the trade-off of managerial power for great wealth led, in many cases, to an abrogation of responsibility for the wellbeing of the firm, to the ultimate detriment not only of wages but also to owners themselves (ibid); the opposite of the ‘empire building’ manager much derided in areas of the finance literature may be the equally undesirable footloose and uncommitted opportunist. Conventional approaches to understanding agency are themselves rather selective in their understanding; it is not just about binding management to short-term share prices, but about deepening commitment to the wellbeing of the organization; a corporate purpose focused on the production of high quality goods and services and customer satisfaction may not immediately boost share prices, but is likely to be in the long-term interests of shareholders themselves (McSweeney, 2008). In other words, the problem of agency is not just one of discipline: it is of ensuring managers have not just transferable, but also emotional and intellectual sunk capital in the firm, such as in the case of an owner manager or under a more beneficial MBO. The creation of wealth is ultimately a collective enterprise, requiring ‘the effective coordination of competencies’ outside of narrow contracting via both cooperative forms of work organization and informal rules and commitments (Marsden, 1999; Boyer, 2005). All these factors are interconnected.

As with any other dimension of the broad financial industry, private equity represents a diverse – and in many cases – experimental model. While venture capital may have beneficial effects (even if it also poses costs; Aglietta & Riberioux, 2005), there is much more controversy surrounding private equity at large (TSC, 2007). Yet, it can be argued that the role of innovative forms of firm finance at other stages of the organizational life cycle is at least of equal importance to that at the start-up phase. Hence, in the following sections, we explore the extent to which different types of private equity are linked to differing organizational outcomes in relation to the above typology.

Reviewing the empirical evidence

The process of experimentation and change takes place both at the levels of policy and practice. The continuing reconfiguration of regulatory forms and what firms do reflect fundamental changes in the logics of consumption and finance (Hatchuel, 2004: 2–3): hence, our focus on a particularly innovative emerging area of the financial services industry as an example of the experimentation and evolution at the level of practice, and the associated regulatory issues and dilemmas. Increasingly mobile finance capital and the need for capital for innovation place great pressures on the firm; innovation may be the key to survival in highly competitive markets, yet short-term investment horizons and the resultant reigning in of managerial autonomy and a reluctance to take a firm's human capabilities seriously makes innovation more difficult (Hatchuel, 2004: 2–3; cf. Boyer, 2006).

A reconciliation of finance and innovative capital (which private equity seeks to do) may heighten pressures on the firm (towards only investment for innovation, but only for short-term returns) or open up new challenges and possibilities for ‘robust strategies of innovation and cooperation’ (Hatchuel, 2004: 3). At the same time, it is recognized that innovation is taking place in a range of areas and levels: a look at private equity alone can only provide an incomplete picture, with crisis and new forms of sustainability unfolding at a range of systemic levels and locales.

The evidence presented below is drawn from two main sources. First, we draw on primary data compiled by the authors at the Centre for Management Buyout Research (CMBOR). The CMBOR database of PE backed buy-outs in the UK and Europe has been compiled from a wide range of sources, including biannual surveys of financiers, press reports, stock exchange circulars etc. and contains market trends information from the late 1970s onwards (CMBOR, 2011). The database has no lower or upper size cut-off, enabling the full size range of buy-outs to be examined. Second, we draw on a review of the practitioner and academic PE literature to present secondary findings on the nature and impact of PE. In what follows we cite both CMBOR and specific studies to provide data supporting the arguments we advance.

The features of private equity

LBOs, MBOs and MBIs

To obtain finance for investment, private equity (PE) firms raise a fund in which the principal investors are institutional investors, as well as the PE fund managers themselves (Gilligan & Wright, 2010). The PE fund comprises equity capital invested in a portfolio of private companies, and is generally designed to generate capital gains from the sale of investments rather than income from dividends or fees. The PE fund is typically structured as a limited partnership with a finite life (usually ten years with a possible two-year extension); all investments have to be made and realized within this period. It has a general partner (GP), the private equity fund managing firm, with unlimited liability for the liabilities of the partnership and a number of limited partners (LPs), the institutional investors, whose liability is limited to the amount of their equity investment in the partnership. The GPs are rewarded through a management fee (generally 1–2 per cent of the funds raised depending partly on fund size) and through a share of the profits in the fund (known as carried interest), which may be up to 20 per cent of the profits over and above some pre-agreed rate of return (the hurdle rate).

Private equity deals are heterogeneous (Wood & Wright, 2010). In a leveraged buy-out (LBO) PTP, typically a publicly-quoted corporation or a large division of a group is acquired by a PE firm and is taken private – a term that has been used loosely and broadly. A buy-out may involve inside management as significant equity holders (a management buy-out, MBO) or only new external management or the PE firm (a management buy-in, MBI, or investor-led buy-out, IBO; Robbie & Wright, 1995). Although superficially similar to MBOs, Robbie and Wright show that MBIs carry greater risks, as incoming management do not have the benefit of the insiders' knowledge of the operation of the business.

While LBOs of listed corporations (public-to-privates, PTPs) have attracted considerable attention, they account for only a small proportion of private equity transactions by volume; rather, it is divisional buy-outs, family firm buy-outs and, increasingly, secondary buy-outs that are more common (CMBOR, 2009). In a secondary buy-out, an initial buy-out is refinanced with a new ownership structure including, typically, a new set of private equity financiers, while the original financiers and possibly some of the management exit (Wright et al., 2007).

Irrational exuberance

Institutional investors worldwide became increasingly persuaded of the attractions of private equity as an asset class. Institutional investors in the US were also persuaded that there were potentially attractive returns from investing in funds targeting the less-developed PE markets outside the US and the UK, which were generally less competitive and offered greater perceived opportunities for restructuring deals. As a result, the amounts going into PE funds increased dramatically as the funds themselves increased their global reach. In the US, commitments to private equity partnerships ranged between 1.14 and 1.57 per cent of total stock market capitalization in 2006–2008 compared to a maximum of 0.6 per cent in 1987 during the first private equity wave and in the late 1990s (Kaplan, 2009).

As the private equity market matured, greatly enhanced competition between funds helped push up entry multiples. In order to complete large deals, megafunds lowered their IRR expectations by some 5–10 per cent (ibid). By 2008, there was a marked increase in the failure of large PE-backed buy-out deals to complete. For example, concerns were raised about the proposed debt burden in BCE contributing to its abandonment (Gilligan & Wright, 2010).

Buoyant investment conditions, with plentiful supplies of finance and pressure on PE funds to invest in an environment of ever-more marginal deals, contributed to investments being made with limited rigorous analysis of the underlying drivers of future performance improvements presented in business plans. Extensive outsourcing of due diligence by private equity firms may also have contributed to insufficient understanding of the quality of business plans (Wright et al., 2010).

There is extensive evidence that PTPs completed in the first private equity wave of the 1980s generated significant increases in profitability, but this does not appear to have been the case for more recently completed PTPs (see Kaplan & Stromberg, 2009). The substantial growth in secondary buy-outs appears to have been con fronted by major challenges in generating further value beyond the relatively easy value extraction in the first buy-out. The median equity IRR on secondary buy-outs appears to be half that obtained in trade sale exits and a fifth of that in IPO exits (Nikoskelainen & Wright, 2007).

As future value options became more challenging, it became increasingly difficult to justify high purchase costs of increasingly marginal deals. In some cases, deals were only completed on the basis of lower return expectations. Against a background of high stock market valuations, the average bid premia on UK PTPs in the period 2004 to 2007 were in the mid-20 per cents compared to generally well in excess of 30 per cent over the period 1997–2003 (CMBOR, 2011).

While this outcome was not generally anticipated, there is less evidence of a negative feedback loop here. Rather, there is evidence of a greater realism percolating the sector, with choices being informed by the lessons of failure, rather than through efforts to replicate success.

High leverage

Traditional senior debt typically involves a seven-year amortizing loan, often with a capital repayment holiday of up to two years during which only interest is paid. Both interest and capital repayments are serviced from cash flows, as such limiting the amount that can be borrowed. Increased borrowings were achieved by adding to this ‘A’ tranche of senior debt, a ‘B’ tranche or even a ‘C’ tranche where capital repayment either began after the ‘A’ tranche was paid off or as a bullet repayment at the end of the loan period (Gilligan & Wright, 2010).

In the build-up to the peak of private equity markets, increasing volumes of senior debt were available at favourable margins. Lenders competed to offer more debt for deals by reducing the price and maximizing the amount available. The average points above LIBOR for A, B and C tranches of senior debt fell in 2005, and by 2007 were still well below 2004 levels (CMBOR, 2011). The amount of debt available for larger deals was also increased through the use of collateralized debt obligations (CDOs) or collateralized loan obligations (CLOs) funds. A CDO fund is a pooled investment vehicle that invests in a diversified group of debt assets. To finance its investments, the pool vehicle issues bonds/notes to investors. The servicing and repayment of these notes is linked directly to the performance of the underlying assets. Second lien debt also developed as an alternative to traditional mezzanine financing and is effectively a tranche of senior debt with some contractual subordination and because of this offers a higher yield (Gilligan & Wright, 2010).

Lenders typically specify and closely monitor detailed loan covenants to help ensure that the buy-out maintains its ability to service the debt. MBO lending agreements traditionally contained both more and a greater variety of accounting-based and non-accounting covenants than general bank lending agreements, the most important traditionally being minimum cash flow-based interest coverage ratio covenants, net worth covenants and dividend covenants (Citron et al., 1997). During the second wave, banks were encouraged to loosen and reduce the number of covenants, so-called covenant-lite or cov-lite arrangements, both in order to lend more and because they were able to pass on risk to hedge funds and other investors (Gilligan & Wright, 2010). Figures from S&P show that, in the first five months of 2007, the average number of covenants per leveraged loans was 3.8, down from 4.2 in 2004 (TSC, 2007).

These trends resulted in the overall volume of debt being invested in private equity buy-outs and increases in leverage ratios, especially for larger deals in the lead-up to the crisis; this may have constituted a negative feedback loop. As a result of the increased availability of cheap and different forms of debt, it is no surprise that the average share of debt in the financial structures of buy-outs rose sharply. Correspondingly, Debt/EBIT multiple in private equity buyouts with a transaction value above £100 million doubled from 2003 to its peak in 2007(CMBOR, 2011).

Increased regulation

During this period, private equity had a low public profile. Private equity buy-outs were dominated by mid-market deals that were not household names (CMBOR, 2011). Generally buoyant economic conditions meant few buy-outs occurred where there was need for major restructuring through significant job losses. If buy-out firms were unionized, there was little negative impact on employee relations (Bacon et al., 2010). In the heyday of liberal financial markets, private equity deals were seen as contributing to an entrepreneurial culture.

After many years of relatively benign treatment, the second private equity wave was marked by increased external pressures. The potentially negative effects of highly leveraged deals came under scrutiny from the International Monetary Fund, the Organization for Economic Cooperation and Development, the European Central Bank and the UK Financial Services Authority.

In exporting Anglo-American financial practices into Continental Europe, private equity was regarded by some critics as a direct threat to the European social model of worker participation by achieving performance improvements through restructuring buy-outs at the expense of workers' terms and conditions, seeking to reduce employment costs, downgrading working conditions and threatening jobs (IUF, 2007; PSE, 2007; TUC, 2007). Debates on this issue have ranged from public hearings to proposed legislative reform in, among other places, the European Parliament, the German Bundestag and the UK House of Commons (TSC, 2007). The Trade Union Advisory Committee of the OECD pressed the Group of Eight in 2007 for action on private equity.

In response to criticisms about lack of transparency, the industry in the UK through the Walker Report introduced proposals for private equity firms investing in large deals to report annually on their investment approach and the companies in their portfolios. These larger portfolio companies were required to disclose the identity of their private equity owners and to publish six-monthly reviews of their performance, including factors likely to affect future development, much of which was in line with requirements for listed corporations. While there has been a high level of compliance with these disclosure requirements, some critics charge that self-regulation does not go far enough (Gilligan & Wright, 2010).

Following the European Commission's (EC) high-level consultation on the issue in February 2009, the EC initially proposed a Directive on Alternative Investment Fund Managers in April 2009, with a view to implementation by 2011, though this has since been delayed. It is estimated that complying with the Directive would impose costs of £25,000 to £30,000 on each of 5,000 European portfolio companies, potentially reducing the funds available for the private equity industry to acquire and help turn around troubled firms in the recession, and advantaging other firms that may seek to acquire failing competitors yet may be less effective at turning around troubled companies (ibid). The proposed Directive has been seen by critics of the PE industry as inadequate and by the private equity industry as imposing unnecessary costs and red tape. Although at the time of writing debate continues, it is unlikely that pressure for formal regulation of private equity will go away. In the light of the credit crisis, regulation of private equity at the very least seems likely to be part of a stronger general approach to regulation across all financial markets (Woolfe, 2009), a self-reinforcing process.

Negative and positive feedbacks, impacts and outcomes

This section looks at how knowledge and innovation, developments in the wider economy and ownership changes have produced positive and negative feedbacks with indeterminate results.

Knowledge and innovation

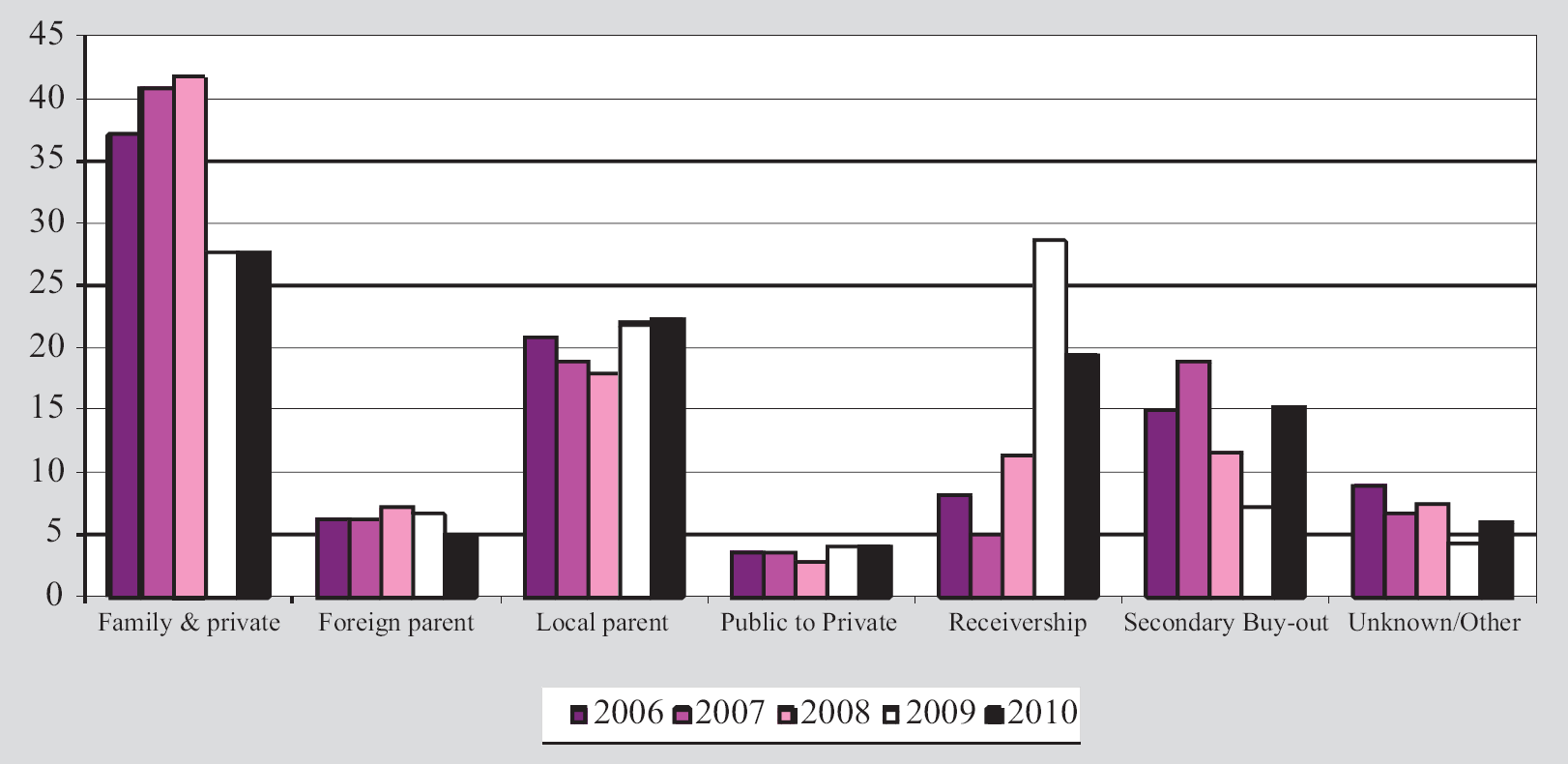

Figure 3 shows the relative importance of the different types of sellers of firms that have been acquired in private equity-backed buy-outs over the five-year period 2006–2010. A plentiful supply of attractive companies from private owners, divisional exits from corporates and secondary buy-outs was initially available, but in the later years there was a marked decline in the relative importance of buy-outs involving family firms as owners of these companies became reluctant to sell unless they really had to in the environment of reduced asset valuations following the 2008 crash (Figure 3). Post-crash, buy-outs from companies in bankruptcy proceedings (administration or receivership in the UK system) became relatively more important as private equity firms had a greater role to play in restructuring firms in distress in this macroeconomic climate.

UK vendor sources.

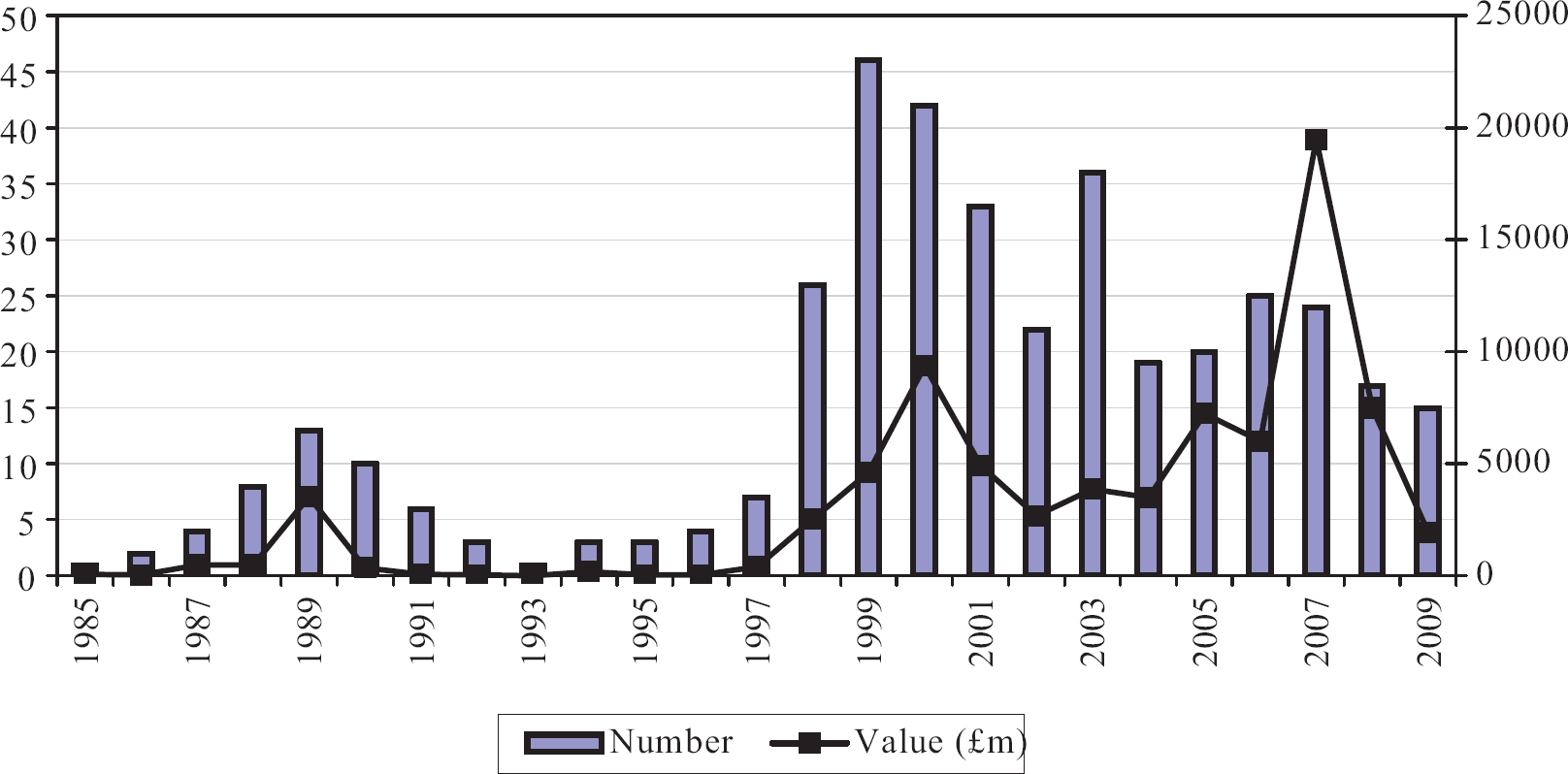

PTPs also grew over the last 25 years, and were particularly strong in terms of the value of transactions in the 2006–2007 period (Figure 4). In the PTP market, initial attractive opportunities were offered to buy smaller listed corporations with limited liquidity where institutional investors with relatively high holdings were looking to exit and where founders remained as key shareholders but were disillusioned with the stock market (Weir et al., 2005). Subsequently, there was a tendency towards investor-led or institutional buy-outs (IBOs) of larger public companies, suggesting that the opportunities to restructure listed corporations by taking them private were greater than initially thought (CMBOR, 2011).

UK PTP trends.

The growth in general M&A activity as firms sought to reconfigure themselves to meet the demands of the global marketplace also created opportunities to buy out unwanted divisions. Buy-outs became a more widely accepted succession option among larger family controlled firms, which were sometimes stock market listed (ibid). Experienced intermediaries and financiers devoted greater attention to courting vendors in these kinds of companies to persuade them of the attractiveness of the buy-out option.

The period was also marked by a rapid growth in secondary buy-outs (ibid). Although private equity providers had previously been reluctant to purchase companies from each other, attitudes changed as pressures on maturing private equity funds to repay cash to LPs or incur penalties led to an increased supply of potentially attractive targets for newly raised funds.

Initially, few PE houses were competing for targets, although this changed post dot.com. Experienced PE funds were able to build on their networks to identify proprietary deals. As the second wave developed, with larger, increasingly global funds, targets were becoming available to PE bidders. Among the largest buy-out bids ever made, nearly all took place in the period 2006–2007 (Gilligan & Wright, 2010). Consequently, the value of buy-outs as a share of all UK M&A activity rose from a low of 18.3 per cent in 2000 to reach a record 63.4 per cent in 2007 (CMBOR, 2009).

In the crisis of 2008–2009, vendor price expectations remained high despite the stock market collapse and the consequential effects on company valuations (CMBOR, 2011). The increased challenges in growing and turning around buy-outs are exacerbated since many PE fund executives and portfolio managers have not experienced the unique adverse current economic conditions. Rather, they have experienced a long period of growth since the mid-1990s. In an environment in which it becomes more difficult to drive required cost savings and where there is demand to add value through market development and operational management, the traditional PE value-adding skills of financial monitoring and cost cutting look increasingly limited (Wright et al., 2010). In other words, there is a potential gap between the real value of existing capability and knowledge bases and present conditions. This represents an example of unintended outcomes: developed skills and capabilities may have become less relevant in the light of changed material circumstances. There may be a similar gap between the perceived and actual value of such capabilities, fuelling a negative feedback loop.

Developments in the wider economy

For much of the decade from 1997, macroeconomic conditions were buoyant. GDP growth was sustained throughout the period. These conditions provided the basis for profitable growth of companies in general and private equity deals in particular. The advent of the 2008 crisis and the accompanying recession meant a sharp increase in failure of buy-outs. For example, the number of PE backed buy-outs in the UK entering receivership rose by a quarter in 2007 to 50, with a similar number in 2008 (CMBOR, 2009). A recent study of the population of private corporations in the UK also found that PE-backed deals completed post-2003 were not significantly more likely to fail than other firms (Wilson et al., 2009). Further analysis shows that, during the recent severe global recession, PE-backed buy-outs experienced higher growth, productivity and profitability, and improved working capital management, relative to comparable firms that did not experience such a transaction (Wilson et al., 2012).

This evidence suggests that the process is pro-cyclical but also that there may be a counter-cyclical advantage consistent with PE firms being more actively involved in taking timely action to assist their investees. This would suggest that, while potentially contributing to the overall performance of firms, private equity does not confer any particular disadvantages over other categories of investor in times of recession.

During the mid-1990s, IPOs were the most important exit route for larger buy-out investments, followed by trade sales (CMBOR, 2011). As buoyant conditions both in the wider economy and in the private equity market continued to develop from the late 1990s, the range of exit options widened. Corporates became more active acquirers of private equity deals. The annual number of trade sale exits from larger PE-backed buy-outs from the second half of the 1990s was generally more than twice what it had been in the first half of the decade (ibid). The growth in the level of capital invested in PE funds and an increasing number of PE funds entering the market also provided a ready demand for deals being exited from other PE firms' portfolios. PE funds became more willing to undertake larger secondary buy-outs. The number of secondary buy-outs of PE-backed deals in 2007 was eight times that of a decade earlier in 1997. The total value of secondary buy-outs peaked in 2007 at £11 billion, 20 times the 1997 level (ibid). As the market matured, there was also an increase in tertiary and fourth time around buy-out. The substantial rise in the stock market over this period was associated with significant increases in company valuations. Increased availability of private equity funds bidding for a limited number of attractive deals also helped bid up prices for companies exiting as secondary buy-outs. A number of PE portfolio companies exit within two to three years. International evidence indicates that some 12 per cent of PE deals exit within two years (Wright et al., 2010).

This may have represented a positive feedback loop, but with unintended consequences: relative ease of exit led, perhaps, to over-exuberance, with the onset of the crisis making exits much more difficult. Exit opportunities narrowed in 2008 and 2009. In the first half of 2009, exits amounted to a total of £960 million against a peak exit value of £26.9 billion in 2006 (CMBOR, 2009). IPOs of PE-backed deals disappeared and trade sales fell by almost a half. Following the adverse impact of the credit crunch on the borrowing capabilities of PE funds, the number of secondary buy-outs more than halved in 2007 as did their value, to 29 and under £5 billion, respectively (ibid).

Firm ownership

Evidence from several countries, particularly in relation to deals completed in the 1980s, indicates substantial average improvements in profitability and cash flow measures over the interval between one year prior to the transaction and two or three years subsequent to it. Evidence for the US, primarily relating to LBOs of listed corporations, is provided by Kaplan (1989), Singh (1990), Muscarella and Vetsuypens (1990) and Smart and Waldfogel (1994). UK (Wright et al., 1992) and French (Desbrieres & Schatt, 2002) studies, mainly relating to divisional and family firm buy-outs, support these findings. Studies in both the UK (Wilson et al., 2012) and the Netherlands (Bruining, 1992) indicate significantly higher increases in profitability in inside management-led management buy-outs (MBOs) than in comparable non-MBOs. Again, owner-managers with extensive existing experience of the firm (MBOs) are less likely to discount the worth of human capital within the organization, as they are more likely to have a more accurate picture of its worth. In contrast, in MBIs the converse is more likely, with the potential for short-term value release being more likely to be prioritized over potential future value that might accrue from a firm's human capital; but often MBIs involve businesses that are more in need of a turnaround (Robbie & Wright, 1995). Evidence on improvements in profitability for the 1990s and 2000s is less convincing in respect of LBOs of public corporations but there is evidence that liquidity improves and significant returns to shareholders are generated (Guo et al., 2007; Weir et al., 2008).

The systematic evidence on the effects of buy-outs on employment is mixed and reflects the heterogeneity of deal sources and types. UK evidence from buy-outs completed over the period 1999–2004 shows that employment growth is higher for MBOs after the change in ownership and lower for MBIs. More detailed data indicates that employment in MBOs dips initially after the buy-out but then continues to rise, on average. In contrast, for MBIs, the employment level remains below the pre-buyout level. However, in both cases, the majority of deals show an increase in employment (Wright et al., 2007). Importantly, the effects of buy-outs on estimated employment growth rates are similar to those for traditional acquisitions (Amess et al., 2008). Cressy et al. (2007) find that employment in buy-outs falls relative to a control group for the first four years but rises in the fifth; initial rationalization creates the basis for more viable job creation. Davis et al. (2008) find that employment grows more slowly in PE cases than in their control group pre-buyout and declines more rapidly post-buyout. However, in the fourth and fifth years, employment mirrors that in the control group and buy-outs create more greenfield jobs.

US studies from the 1980s indicate a decline in the relative compensation of non-production workers. UK evidence from the late 1990s and 2000s shows that average growth in wage levels in MBOs and MBIs is marginally lower than in firms that have not undergone a buy-out (Amess & Wright, 2007, 2012). Why these differences between MBOs and MBIs? A buy-out would be unlikely to occur if the pre-buyout firm was out-performing its peers because there would be few performance gains to be obtained from restructuring. As on average MBO/MBI plants have lower total factor productivity before the buy-out than their non-buyout counterparts, it is not surprising that some initial labour shedding occurs. These findings are consistent with the notion that MBOs lead to the exploitation of growth opportunities, resulting in higher employment growth.

In contrast, MBIs were more likely to have been under-performing and require greater restructuring to restore viability; as such, pre-buyout employment levels may not have been sustainable for the business to survive (Robbie & Wright, 1995). Employees in UK MBO firms tend to have more discretion over their work practices than comparable workers at non-MBO firms, with skilled employees, in particular, having lower levels of supervision at MBO firms (Amess et al., 2007), while positive effects of private equity on employee relations have been noted (Bacon et al., 2010). This evidence points to particularly positive features of MBOs, an example of successful innovation, even if there are failures in innovations elsewhere in the system.

Discussion

Early regulationist theory focused on the crisis in the then-dominant Fordist production paradigm, and sought to explore the possibilities of a new production paradigm that would take its place (Jessop, 2001a). There was a gradual recognition that no single paradigm had replaced it (or indeed was likely to) and this was followed by a similar recognition that there was both considerable variety in terms of space and scale (Jessop, 2012). At the same time, there was a shift of focus from the process of production to the nature of competition between firms. Most notably, Aglietta and Riberioux (2005) argued that this was increasingly affected by the greater mobility of capital coterminous with technological advance, and encompassing increasing importance for the financial services sector. However, they also recognized that this process did not make a coherent or a systematically functional basis for a sustainable growth regime. Financialization thus did not represent a new epoch, albeit that in specific areas ‘virtuous circles of financial and technical innovation were possible (ibid). Boyer (2006: 39) notes that there is no single optimal configuration of institutions, even within knowledge-based economies. Practices may emerge and coalesce both to compensate for imbalances and to build on strengths (ibid). However, just because a practice persists does not mean that it is objectively functional, or that apparently successful practices inevitably diffuse across a system.

What the empirical material points to is diversity, with the coexistence of success and failure, positive and negative feedback loops, and unforeseen consequences. In part, the rise of private equity reflects limitations in more conventional capital markets. As Dore (2008) notes, ‘norm entrepreneurs’ in specific areas and sectors may challenge existing ways of doing things, and pioneer the emergence of alternative models. On the one hand, we found evidence of negative feedback loops, with imperfect information on the continued value and relevance of the knowledge and capabilities of specific private equity players following the onset of crisis. As noted above, there may similarly be a gap between the perceived and actual value of such capabilities, fuelling a negative feedback loop. At the same time, the empirical evidence points to a greater degree of ‘informed realism’ following the crisis. An initial positive feedback loop – relative ease of exit – appears to have evaporated: however, an unforeseen consequence may be greater realism. On the other hand, there are visible successes: most notably, MBOs appear to have the potential to enhance organizational capabilities; while the diffusion of best practice may be uneven, there is clear potential. Again, while greater difficulty in exit has been an unintended consequence of the crisis, this will necessitate that a greater proportion of value be created through business performance rather than excessive leverage, strengthening the relative position of those players that have the capability to do so.

Conclusion

This article highlights the contradictory trends apparent within an extended period of experimentation, innovation and crises; these trends are then applied to the case of private equity, a particularly innovative area of the finance industry. The performance of players within the private equity sector has varied greatly: the 2008 financial crisis appears to be contributing to a rationalization of the industry. At the same time, diversity has persisted within the type of buy-out, the organizational consequences and, indeed, ultimate firm performance. As with any innovation and experiment, the outcomes of private equity are mixed. Contrary to critics, a significant component of the industry cannot be readily located at the negative pole of the typology provided in Figure 2. Rather, specific innovations – such as in making MBOs more feasible –may, inter alia, help resolve the problems associated with ‘managerial abrogation’ and imperfect knowledge highlighted earlier in this article. This would suggest that the emerging financial architecture that will inevitably form part and parcel of any return to growth will, in part, incorporate aspects of private equity. Indeed, to the extent that private equity buy-outs involve the acquisition of firms in distress, they may have a positive contribution to make in resolving the problems of recession and financial crisis. And, the failure of unsustainable experiments does not mean, however, that renewed growth will simply result through natural selection: it depends on continued innovation and experimentation across the entire economy, coupled with relevant formal and informal socio-economic regulation.

Footnotes

Acknowledgement

The authors are indebted to the insightful comments of the anonymous referees and the guidance of the editor.