Abstract

Third party compliant reporting standards govern how mining companies disclose technical information. These reporting standards apply to any public issuer. Mineral resources and mineral reserves are critical in determining the size and quality of the asset base as well as the market value of the company itself. Moreover, companies must present a qualifying technical report in accordance with existing reporting standards as a necessary step, required by lenders and financial institutions. This paper examines issues with public reporting of industrial minerals and the challenges this sector faces garnering the same recognition as other mineral commodities. Differing perspectives regarding main elements of the reporting standards of industrial minerals are presented. These findings prepare the ground for further discussion on what needs to be improved, and how these changes could be achieved.

Introduction

Industrial minerals play a significant role in our daily lives and economies. This is clearly illustrated by their use in nearly every economic activity, including agriculture, manufacturing, and construction, among many others. The diversity of industrial minerals, in terms of both the different types of minerals and the number of markets they serve, make them important to the growth of any nation's economy. It has been suggested that the degree of involvement by a country in trade and production of industrial minerals are used as an indicator to measure the maturity of a country's industrialisation. In most developed nations, industrial minerals companies always face serious challenges in acquiring investment dollars, as potential investors are not able to properly evaluate industrial mineral projects.

Before mining companies can finalise any financial deal publicly, or in some cases privately, financial institutions require mining companies to prepare a qualifying technical report. These reports address mineral inventory estimates and exploration results. Estimates of mineralisation are categorised into two categories: mineral resource and mineral reserve (MRMR). The classification of MRMR is based on geological confidence, technical feasibility, and economic viability under reasonably forecasted cost and price structures. Mineral resource and mineral reserve estimates are important because they determine a mining company's financial results as well as their mineral asset base.

Mining companies must present their qualifying technical reports in accordance with existing reporting standards. The primary goal of these standards is to provide a minimum standard for disclosure of scientific and technical information. They also serve to establish definitions (e.g. mineral resource and mineral reserve), as well as other reporting requirements. These standards include factors such as content, timeline, and necessary checks that must be in place to ensure that technical and scientific disclosure is based on information prepared by a qualified person (QP). Moreover, these standards were developed to ensure that there are standard procedures that create a fair basis for comparison of different mineral projects. Over the last 10 years, interests in enhancing the public reporting standards of MRMR and exploration results have increased internationally. Motivation includes intensive international competition for investment funds, mining industry's history of attracting deceitful promoters such as Bre-X Minerals Ltd, and the success of the Joint Ore Reserves Committee (JORC) code in Australia.

Industrial minerals by definition

About 60 commodities are nominated as industrial minerals. Jeffrey (2006, p. 3) describes these materials as ‘building blocks of our way of life’. These materials are used in almost all aspects of human industrial activity including manufacturing, agriculture, and construction, among many others.

Earth scientists have yet to develop a universal definition for industrial minerals. A widely used definition for an industrial mineral is ‘any rock, mineral, or natural occurring substance of economic value, exclusive of metal ore, mineral fuels, and gemstones: one of the non-metallics’ (Bates, 1969, p. 3).

In general, industrial minerals are classified based on their consumption and use, into two main groups: chemical minerals and physical minerals. Chemical minerals are sources for chemical elements or components. For example, salt and lime are the primary sources for calcium, sodium and chlorine. All chemical minerals share one common characteristic: these minerals are marketed on the basis of chemical content and degree of purity. Therefore, chemical minerals are very similar to commodities that are sources for products with highly substitutable raw materials at comparable price.

Physical minerals are valued for their performance specifications. Although chemical compatibility with the end product is inevitable, physical minerals are generally used to improve the properties and value of the end products. For these minerals, meeting general market specification in most cases is not adequate. An industrial mineral producer should be able to meet the specific end-user requirements, and the end-user, in most cases, is the one who determines the required specifications. The main physical specifications requested by end users for physical minerals include; particle size, brightness, particle shape, colour, absorption, hardness, electrical conductivity and specific gravity.

Mineral resource, mineral reserve and importance of public reporting of MRMR

Estimates of mineralisation are classified into two categories: mineral resource and mineral reserve. The classification of MRMR is based on geological confidence, technical feasibility, and economic viability under reasonable forecasted cost and price structures.

The mineral resource definition under the CIM definition standards is as follows:

‘a mineral resource is a concentration or occurrence of diamonds, natural solid inorganic material, or natural solid fossilized organic material including base and precious metals, coal, and industrial minerals in or on the Earth's crust in such form and quantity and of such a grade or quality that it has reasonable prospects for economic extraction. The location, quantity, grade, geological characteristics, and continuity of a mineral resource are known, estimated or interpreted from specific geological evidence and knowledge.’ (JORC, 2004, p. 4).

Based on geological assurance, mineral resources’ are classified into three categories: inferred, indicated, and measured. As geological confidence increases, inferred resource becomes an indicated resource, and subsequently into measured resource.

A mineral reserve is ‘the economically mineable part of a measured or indicated mineral resource demonstrated by at least a preliminary feasibility study’ (CIM Ore Reserve Committee, 2005, p. 5). The supporting study must consider detailed information regarding mine planning, metallurgy and processing, economic and any other relevant factors.

Mineral reserves’ are classified into two categories: probable mineral reserve and proven mineral reserve. Probable and proven mineral reserve are respectively part of the indicated mineral resource and measured mineral resource which are economically minable and supported by at least a preliminary feasibility study (SAMREC, 2007). The supporting study for estimate should demonstrate that the economic extraction of the deposit is justified in case of probable mineral reserve, and is justified in case of proven mineral reserve.

Mineral resource and mineral reserve are critical in the determination of mining company's mineral asset base. It is, therefore, important how mining companies estimate and report their MRMR to the public.

Third party compliant reporting standards govern how mining companies must disclose their technical information regarding their mineral assets. These reporting standards apply to any public issuer (Canadian Securities Administration, 2005). For example, when a mining company raises money from a private placement, the company is required to comply with any and all reporting standards. Another example is that if a company raises funds under an offering memorandum before being publicly listed, the company also needs to similarly comply. Preparing a qualifying technical report has proven to be a necessary step, required by lenders and financial institutions before finalising any financial deal publicly or privately. As a result, the importance of reporting standards has increased and will likely continue.

Several countries have established standardised reporting instruments for MRMR and are presented in Table 1.

Nations’ MRMR reporting instruments

Reporting standards and industrial minerals

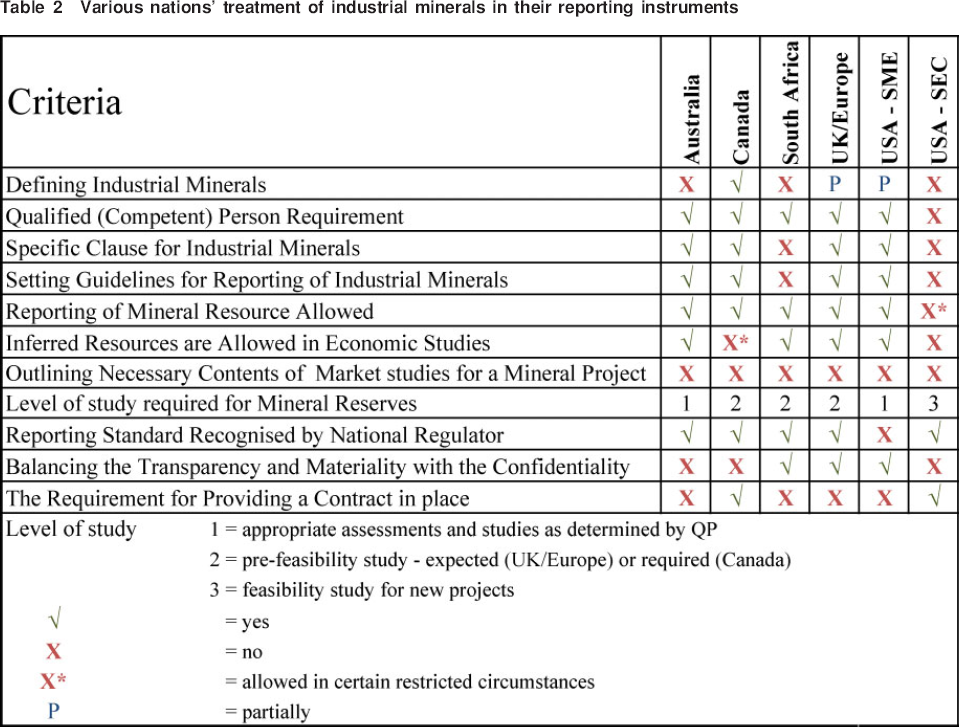

Reporting standards in most countries are very similar (i.e. 90–95% compatible) with respect to industrial minerals. There are differences, however, between these standards because each addresses their public reporting with respect to its host country regulatory requirements (Weatherstone, 2007). These differences are summarised in Table 2.

Various nations’ treatment of industrial minerals in their reporting instruments

Almost all of reporting standards, except the SAMREC code, indicate the extra clauses are required when defining industrial minerals. Industrial minerals are defined differently by all reporting standards and guidelines reviewed. This becomes confusing for stakeholders.

All the reporting standards identically define a QP and require their involvement and supervision in preparation process of technical reports. Considering the significant characteristics differences between industrial minerals and other sectors, a QP for industrial minerals requires not only an understanding of geology, mining techniques, and process technology, but also of markets that the material is used in, the particular process that is required to meet the market requirements, and logistics costs. Therefore, it is worthwhile to re-examine the definition of QP and the experience relative to an industrial mineral project. Additionally, by developing more specific standards and definitions for industrial minerals, stakeholders may be better equipped to prepare and/or interpret technical reports.

Definitions of MRMR and their classifications are conceptually identical in all standards. They have, however, different policies with regard to disclosure of different categories of MRMR. The CIM Standards and the SME Guide would allow reporting of exploration information only if it clearly states that the reported estimates are conceptual (CIM Ore Reserve Committee, 2005; SME, 2007). The SAMREC code, the PERC code, the CRIRSCO standards and the JORC code would not allow reporting of exploration information (JORC, 2004; CRIRSCO, 2006; SAMREC, 2007; PERC, 2009) unless the exploration information includes sufficient material for investors balanced judgment (Vaughan and Felderhof, 2002).

The SEC and the CIM require inferred mineral resources to be excluded from the basis of economic evaluations, while other standards allow disclosure of inferred resources when caution is exercised with its full disclosure (Vaughan and Felderhof, 2005). Except the SEC Guide 7, other standards would allow reporting of Mineral resource. One of the differences between these standards is the level of study required (Vaughan and Felderhof, 2002).

All the reporting standards put a strong emphasis on exploration and geology as a means to determine MRMR validity. It is important to review the main elements of MRMR estimation for industrial minerals and to evaluate if the current approach of reporting standards is applicable to industrial minerals. It is also worth highlighting the main modifying factors for industrial minerals and how they differ from base and precious metals. Although, conversion of mineral resources to mineral reserves for industrial minerals heavily depends on having a buyer and markets, reporting standards currently do not provide details for this information.

As explained above, there are significant differences between industrial minerals sector and metals sector. The metals sector deals with a clear market supported by metals exchanges, and qualifying technical reports can be used as a good tool to communicate with potential investors. Industrial minerals sector, however, deals with much more complicated market and in some cases evaluation of a deposit is not about mining as much as it is about marketing. It is important to prepare a technical report that not only covers critical economic aspects of an industrial mineral project, but also is presented in a way that is easy to understand for the most audiences, investors.

What needs to be changed for these instruments to become inclusive of industrial minerals?

The competition for investment in industrial minerals companies is intensive. Not only do they compete against other mining companies in other sectors, they also compete against all companies in other industries that are seeking investment dollars. Therefore, a better understanding of investment community decision making process by industrial mineral companies and improvements in communication with investors through technical reports increase the probability of financing.

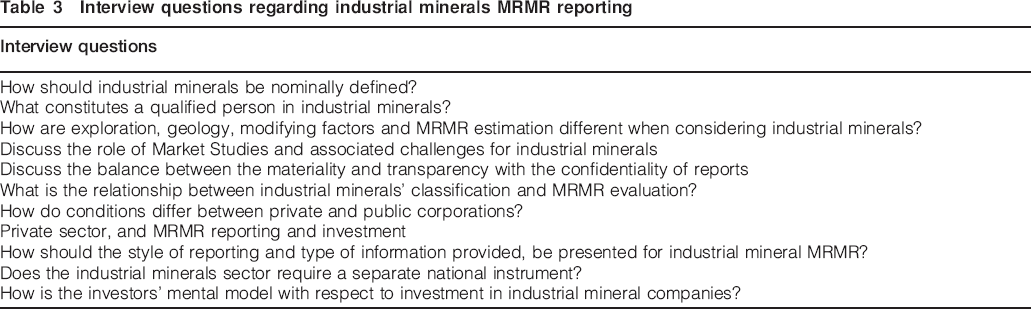

The analysis presented in this paper is based on 34 interviews conducted with the following group of experts including: QPs, CIM Ore Reserve Committee, JORC code committee, PERC code committee, SAMREC committee, CRIRSCO members, professional advisors for investment community and mining sector, senior level mangers and presidents of industrial mineral and other mining companies, TSX and TSX Venture managers in mining sector, Canadian mining regulators, investors, and CSA Mining Technical Advisory and Monitoring Committee. These experts are from Canada, Australia, the UK, South Africa and the USA, with quite diverse experiences in terms of type of work and time spent in the industry.

The questions posited are found below in Table 3.

Interview questions regarding industrial minerals MRMR reporting

Different reporting standards and guidelines have different approaches in terms of defining industrial minerals as discussed above. This becomes a confusing issue for stakeholders of the sector, because it is not clear if a mineral is an industrial mineral or not. This issue was raised during interviews with several stakeholders worldwide. It became clear that most of the interviewees do not share a common definition for industrial minerals. It is for the benefit of all reporting standards to incorporate a universal definition for industrial minerals, as it provides a common ground for comparison.

The QP concept is one of the main pillars of reporting standards for any mineral project. Although it is conceivable that there are situations where a QP evaluating an industrial mineral project may not be necessarily an engineer or geoscientist, the definition of QP seems to be sufficiently general to handle industrial minerals. It would be useful to add to all standards a statement of relevant experience.

All regulatory codes have a strong emphasis on exploration and geology as a means to determine MRMR validity. Exploration for industrial minerals is not as important as it is for base and precious metals. The current guidelines and standards properly address exploration for industrial minerals.

Geology for industrial minerals tends to be relatively straightforward. All industrial minerals, however, require a valid and up-to-date market study for MRMR estimations. For resource estimation, experts often do not complete a full market study; having a conceptual market for the mineral, and a rough idea of major costs, such as transportation and mining, is adequate to complete resource estimates.

Modifying factors are the factors that convert mineral resources to mineral reserves. Most of the interviewees from Canada were not familiar with the term ‘modifying factors’ because unlike the JORC code, neither CIM definition standards nor NI 43-101 defines them adequately.

The two key components in the conversion of mineral resources to mineral reserves are securing buyer(s) and the state of markets. Without them any industrial mineral is only a geological occurrence. For mineral reserve estimation, detailed and comprehensive market studies are required.

Most regulatory codes do not direct QPs as to how a market study must be completed, nor do they provide standards for how QPs report essential information. Completing a comprehensive market study for a given mineral reserve is quite challenging.

Industrial minerals are diverse and, in some cases, too technical to be understood by the general public. There are few experts in this sector that makes finding QPs with appropriate expertise difficult for both companies and investors. Without being prescriptive, providing general broad guidelines for MRMR estimation and market studies could be a benefit of the sector. These recommendations, however, should not compete with existing standards. Qualified persons should be able to exercise their expertise and use whatever method they think appropriate.

Balancing materiality and transparency with the confidentiality of the reports is challenging. Three aspects including the size of companies’ lack of industry knowledge of confidentiality, and understanding how to balance transparency with confidentiality demand sincere reflection.

The size of a company often plays a significant role in what information is confidential or material in nature and what is not. The larger the company, the easier it is to deal with confidentiality issues. A small company trying to raise funds might need to disclose some contractual information to funding agencies. Large companies like Rio Tinto and BHP Billiton report their industrial mineral projects to the public openly.

There is a lack of general knowledge in the industrial mineral industry about what materiality is and the options that are available. This has created a following false perception that if a company reports publicly; the company has to disclose sensitive information. This would subsequently damage the company by losing its competitive advantage. This falsehood has caused many companies to stay private, despite their immediate financial needs. There are no formulas or written rules in terms of when or if an industrial mineral company should go public. While taking into account the advantages and disadvantages of going public, a company must carefully consider whether they would really benefit from public exposure. Every situation is unique and depends on many factors, including future strategies and goals and ultimately the availability of capital.

Investors are the most significant target audiences for technical reports. It is, therefore, important to ensure qualifying technical reports are prepared for the right audiences. Qualified persons who prepare technical reports should be able to freely exercise their expertise and include what they feel is necessary. In addition, choosing the reporting style is a very project specific. It depends on the stage that a company is at and the focus of the company.

Every industrial mineral company must disclose their assets, MRMR, in one way or another. In the authors’ view, it is particularly beneficial for privately held companies to report their MRMR in accordance with established and accepted standards. This should not only help them to be better understood by the investment community, but also improve the overall consistency of public reporting of industrial mineral projects.

Preparing technical reports and complying with reporting standards seem to be a challenge for industrial mineral companies, small and medium size companies in particular. It seems logical to conclude that the current reporting standards and guidelines do not appropriately address the public reporting needs of the industrial minerals sector.

How do we improve existing reporting structures to accept industrial minerals?

It is for the benefit of all reporting standards to incorporate a universal definition for industrial minerals since it provides a common ground for different stakeholders of the industrial minerals sector. A proposed definition is:

‘any rock, mineral, or natural occurring substance of economic value, exclusive of metal ore, mineral fuels, and gemstones; these minerals are often sold based on their chemical and physical specifications and their marketability. These minerals also are distinguished on the basis of volume and grade’.

In addition, a list of minerals considered industrial minerals, should be provided in the appendix of any defining document. This list needs to be revised on a regular basis to its completeness.

Experts tend to recognise CIM definition standards as the first and main reference for definitions used in qualifying technical reports. The CIM definition standards, however, does not include the definition of industrial minerals. This definition, therefore, will be more effective if it is incorporated into the CIM definition standards itself, rather than the CIM best practice guidelines.

An explanation is required to provide a clear idea about who can be a QP for industrial minerals. The proposed explanation includes:

‘a QP for industrial minerals requires not only adequate experiences with geology, mining techniques, and process technology, but also with markets that the material is used in, the particular process that is required to meet the market requirements, and logistics costs’.

It would be useful to add the definition of ‘modifying factors’ in order to create consistent worldwide. The two key components in the conversion of mineral resources to mineral reserves for industrial minerals are securing buyer(s) and the state of markets. Market studies are the most important modifying factor. For mineral reserve estimation of most of industrial minerals detailed and comprehensive market studies are required.

Being proscriptive, in terms of how a QP must complete a market study, may not be appropriate because every mineral deposit is unique and requires different marketing techniques. That being said, there must be standards that mandate format and content of technical reports, as is the case with Canada's NI 43-101 regulation.

In qualifying technical reports it is important to address uncertainties in the modifying factors and assuming a risk based approach for MRMR estimation. It is for the benefit of all stakeholders to add a requirement for QPs to address the risks involved in their estimates and in a common format for comparison.

As a result of this study, it became clear that if an industrial mineral company meets most other listing requirements and a QP has indicated that there will be markets for their products, then there is no reason to mandate the company to provide a sales contract. Providing a comprehensive prospectus report to indicate that the company will get a sales contract and/or receiving letters of intent from customers might encourage regulators to remove this requirement.

Stronger communication by the regulators is required to reverse the wrong perception of the balance between materiality and transparency with confidentiality. Perhaps wording should be added to other reporting standards that indicate companies have such an option to discuss the issue with the regulators. There is not a black and white solution and all the stakeholders must consider their entire context. No company should give away any competitive information or trade secrets, but giving prospective investors sufficient information, will validate the business.

Conclusions

It seems logical to conclude that the current reporting standards and guidelines do not appropriately address the public reporting of industrial minerals. The authors, however, reject the notion that new sets of standards and guidelines are required because of the differences between industrial minerals and metal sector. Financial institutions are already familiar with reporting standards and they use QPs’ qualifying reports as quality insurance that has made fund raising process simpler for mining companies. Introducing new standards creates inconsistent technical reports with other mining sectors that make it more complicated for the investors. Moreover, the economic and diversity of the commodities reminds us to keep the standards high.

Industrial mineral companies are facing serious challenges in terms of gaining capital. They have to compete not only with other mining companies, other mineral commodities, but also with all public companies in other industries that are seeking investment dollars. Third party compliant reporting standards that govern how mining companies must disclose technical information concerning their mineral assets need to accurately reflect the uniqueness of the industrial minerals sector.

This paper has presented a study that highlights the different mineral resources and mineral reserve reporting needs that are not being met with existing instruments, available to the world's developers. By using informative narratives elicited from a broad section of the guardians and professional practitioners the authors have developed a suite of recommendations for improvements.