Abstract

A mining company has entered into contractual commitments to supply certain quantities to clients in each time period. The planned production would be sufficient unless major problems that interrupt production occur. To overcome these difficulties, the Company may be able to obtain more of the commodity: from its strategic stockpile (if there is sufficient there), by buying it on the spot market or for some commodities such as gold and uranium, by leasing it. Two sources of uncertainty, the spot price of the commodity and the occurrence of serious production incidents are considered. Multistage stochastic programming with recourse was used to solve this problem, because in addition to providing the dollar value of the project, it gives decision-makers the ‘roadmap’ to reach the optimal value. A case study over a 5-year period is used to illustrate the proposed procedure.

Keywords

Introduction

This paper focuses on strategic planning to deal with major production incidents; that is, incidents which prevent the mine from producing for several months or more. An incident could be due to technical problems such as high-wall failures in open-pit mines, or roof falls in underground mines, or to natural disasters such as fires, floods or earthquakes. Alternatively, it could be caused by industrial disputes (e.g. prolonged strikes by mine employees or by other groups such as dockers), or by delays in obtaining permits (environmental permits, export permits).

Major production incidents are far more common than is thought. In the 4-year period starting in February 2007, at least four such incidents occurred in Australia alone. First, exceptionally heavy rainfall in February–March 2007 forced the closure of the Ranger uranium mine for several weeks and affected production for the next 18 months. In November 2007, the NE batter at the Yallourn East Field Mine collapsed. A section 500 m long by 80 m high containing 6×106 m3 of material fell into the pit. According to the official enquiry (Sullivan, 2008), the failure were due to water pressure in joints. In September 2010, a partial mine collapse occurred at Navigator's Bronzewing mine in West Australia (Latimer, 2010). No one was hurt, but a drill rig was damaged and future ore sources in pit were covered. From late 2010 until February 2011, coal production in central Queensland was disrupted by Cyclone Yasi and flooding, causing a loss in export earnings worth $9·5 billion AUD according to Bloomberg. Taken individually, these incidents were unfortunate and unforeseeable; taken collectively, mine managements should have contingency plans in case of such incidents.

This raises several questions: what options are available to management, and how can their worth be evaluated and be optimised. The types of options vary from operation to operation. The case of the Ranger mine is instructive. Mining operations ceased on 27 February and the processing plant was shut down on 28 February. Operations were restarted on 7 March in the mine and on 12 March in the processing plant. According to an official press release on 2 April 2007, the shutdown and re-start of the processing plant resulted in the loss of approximated 300 tonnes of uranium oxide production. In addition the elevated water level in the mine resulting from the high rainfall will restrict access to ore in the second half of 2007 and into 2008. In the first half of the year and for some of the second half ERA will process high grade ore that was mined during 2006 and stockpiled on the surface. Based on currently available water treatment and disposal capacity, production in 2007 is likely to be similar to 2006, while production in 2008 is likely to be 25% to 35% lower than in 2006. Sales for the two years 2007 and 2008 are expected to be generally in line with production. So while operations only stopped for a short time, the incident led to a drop of 25–35% in revenue. The impact would have been even greater except for the ore stockpile on surface. Retrieving the material stored in the stockpile proved to be a valuable option for ERA, but it was not the only option available to management. The press release went on to say: ERA has identified a number of potential opportunities to reduce the impact of the weather event, including accelerating the treatment and disposal of water. These options are currently being studied ….

The Company that commissioned this study had been faced with a major production incident and wanted to study the strategic and operational options that were open to it in case a similar event occurred in the future. Two versions of the study were carried out: a confidential one for the Company itself and an expurgated version which retains the key features but without any proprietary information. The second version is presented here. After several discussions with the Company's management, we agreed upon the following description of their situation. The Company had entered into contractual commitments to supply certain quantities of its product to clients in each time period, which would normally have been covered by the planned production. In the event of a production incident, the Company could have recourse to the force majeure clause in the contract but wanted to avoid this, because it would damage its reputation as a reliable supplier. Several ways of making up the shortfall were identified: buying on the spot market, leasing material or taking material from its strategic stockpile (if there is sufficient).

The aim of this research project was to evaluate these options for fulfilling its contractual commitments. We chose to use multistage programming with recourse to solve this problem (Beasley, 2000; Birge and Louveaux, 2000; Kall and Mayer, 2005; Thênié and Vial, 2008). In addition to providing the dollar value of the project, it gives the Company the ‘roadmap’ to reach the optimal value, that is, how much material should be produced from the mine, how much to buy/sell on the spot market, how much to add to/subtract from the stockpile, how much to lease and if all else fails, what the shortfall would be, for each time period as a function of the current spot price and production status. This information could be used to decide whether it was worthwhile building up a strategic stockpile, and if so, how large it should be.

The rest of the paper is structured as follows. The next section gives a formal description of the problem; the state variables and the control variables are defined and the objective function to be maximised is presented. A brief review of multistage programming is given. We explain why the state variables have been discretised. Once this is performed, the problem simplifies to a linear programming problem. So it would be easy for mining companies to implement the method. A geometric Brownian motion is used to model the evolution of the commodity price. After describing how to set up the branching trees for the prices and for the production incidents, we outline where data on option prices can be obtained in order to estimate the key parameter, the price volatility. The results of the case-study are then presented. These give the values of the control variables at each time period, as a function of the current (and past) commodity prices and the state of the mine (in production or not). To be more specific, these are the amounts that the Company should buy/sell on the spot market, that it should acquire on the lease market or that it should take from or add to the stockpile. Most of the time, the results are intuitively obvious, but in some cases the optimal solution is counter-intuitive. For example, although the mine is producing enough to meet the contractual commitments, it is best in the long run to buy on the spot market and store the material on the stockpile irrespective of whether the price is high or low. Without having carried out the optimisation, few mine managers would do this. The discussion and conclusions follow in the last section.

The problem

The Company has entered into binding contractual commitments to supply clients with the quantity of its product CC(t) at a set of times: t1, t2, t3, … T. The contract price CP(t) is usually less than the spot price S(t). The Company wishes to evaluate this project over a period of T years.

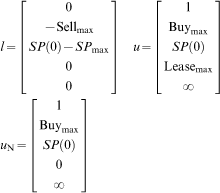

Let Q(t) denote the maximum quantity that could be produced at time t. If there is surplus production (Q(t)>CC(t)), the surplus can be stored on the stockpile, or sold on the spot market at the prevailing price S(t). Alternatively the company may decide to reduce its production; that is, produce only a proportion of Q(t). If the production does not cover its contractual commitments, the Company could take material from the stockpile (if there is enough), or buy it on the spot market at the prevailing price S(t) or lease it. In the latter case interest must be paid at the lease rate LR. For simplicity, we assume that the Company reimburses the amount leased in the following time period and that it does not lease material in the last time period. Let SP(t) denote the quantity in the stockpile at the end of time period t, with SP(0) being the initial quantity and SPmax being the maximum capacity of the stockpile. Finally if after having exhausted all other possibilities, the Company still does not have enough to cover its commitments, there would be a shortfall SF(t), which would damage the Company's reputation as a reliable supplier. In addition, in situations like this, head office management puts pressure on individual mines to increase their production, which often leads to suboptimal decisions to high-grade production with deleterious long-term effects. For all these reasons, a heavy penalty is included in the event of a shortfall, equal to 10S(t) per unit of shortfall. This effectively constrains the computer model to seek out alternatives.

State variables and the control variables

The viability of the project is affected by two sources of uncertainty: the spot price S(t), of the commodity and the maximum quantity Q(t), that can be produced given the current production status. These two factors reflect the state of nature and are assumed to be outside the Company's control. Let ξ(t) = [Q(t)S(t)] denote these two state variables.

In order to meet its contractual commitments the Company has the option of varying the variables which are under its control. To be more precise, it can vary four of these five variables. Let x(t) be a vector containing these control variables:

proportion of Q(t) to be produced

quantity to be bought on the spot market (if it is bought, the value is positive, if it is sold, the value is negative)

quantity to be taken from the stockpile (if it is taken from the stockpile the value is positive; if it is added to the stockpile, the value is negative)

quantity to be leased

shortfall2

Objective function to be maximised

The next step is to define the objective function to be maximised. In this example it is the expected net present value NPV. Alternatively the downside risk/upside potential (Dimitrakopoulos et al., 2007) could have been used. Another possibility would have been the Cashflow at Risk (Stein et al., 2001; Riegger and Dusic, 2005). This is similar to the value at risk used by banks for risk management, and is used in some large corporations such as electricity companies. If cashflow at risk or downside risk or upside potential had been used, the objective function would have been more complicated.

The Company's cash flow comes from the sale of the commodity through its long-term contracts and on the spot market, less the various costs which are:

the fixed and variable production costs, FC(t) and VC(t) which are assumed to be known. In the example these are taken to be constant over time (i.e. VC and FC)

the costs associated with leasing material (lease rate and the repayment during the following period)

the penalty in case of a shortfall.

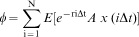

Let the corporate discount rate be r. The expected NPV over the project life T can be expressed as an integral in a continuous time framework or as a sum in a discrete time framework. The latter is used because the strategic decisions to buy/sell material or to lease it will only be made at selected dates. Suppose that these are evenly spaced: Δt, 2Δt, 3Δt, …. NΔt = T. The objective function can be written as

Here, the expectation is taken over all possible values of the state variables at the different times. After removing constant terms which do not affect the optimum, the objective function to be minimised is

Base case

The NPV for the base case is usually obtained by substituting the expected values of the state variables directly into the formula as shown below

is evaluated using the expected value of each variable

is evaluated using the expected value of each variable

Finding the optimum

The main methods for stochastic optimisation are:

optimal stochastic control (Markov decision processes/dynamic programming)

probabilistic or chance-constrained programming

stochastic programming with recourse (two-stage or multistage).

The third method seems more appropriate for strategic decision making. In two-stage programming with recourse, the decision maker chooses the initial value of the control variable (or variables) denoted by x at the outset, then observes the values taken by the state variables denoted by ξ, and then corrects the situation using a recourse variable y(x, ξ)

Simplifying the problem: discrete scenarios for the state variables

In this case the objective function simplifies to

The constraints on the system are linear

The value of the project to the Company is then

Modelling the spot price

For simplicity the spot price of the commodity at time t, S(t), is assumed to follow a geometric Brownian motion. Two parameters are required: the initial price S0 and the volatility σ2. In finance the implied volatility is always used, not the historic volatility of past prices. It is deduced from the prices of options (puts and calls) by inverting the Black and Scholes formula iteratively. So the problem is to obtain the option prices. For gold and oil these can be obtained from exchanges such as ICE in London or COMEX in the USA, or alternatively from investment banks’ websites because they sell the options on gold and oil to the public under the name of ‘warrants’. Options on precious metals such silver, platinum and palladium are traded through the COMEX. Data on option prices for base metals (copper, aluminium, nickel, lead, etc.) can be purchased from the London Metal Exchange. The COMEX is also one of the leading exchanges for copper (but not the other base metals). Both ICE and the COMEX provide option prices on coal and on iron ore. The situation is more complicated for uranium. Spot prices, forward prices and the lease rate can be obtained from specialised websites such as www.uxc.com and www.uranium.info (TradeTech), but to the best of our knowledge, no uranium options are traded.

A branching tree is set up to model the evolution of prices over time. At each time period the prices go up or down by a factor with probability pu and pd. We used binomial trees as given by Hull (2003). Different schemes exist for constructing trees with several branches. Appendix 1 in Derman et al. (1996) gives the formulas for constructing these trees.

Modelling the production incidents

To simplify the analysis we assume that the mine is either capable of working at full capacity or it has suffered a production incident over a given period, thereby reducing the annual production capacity by a certain percentage. The probability of an incident in any year is qd and that of full production is qu. Production incidents are assumed to be independent from one time period to another, and are independent of the commodity price.

Combining the two sources of uncertainty

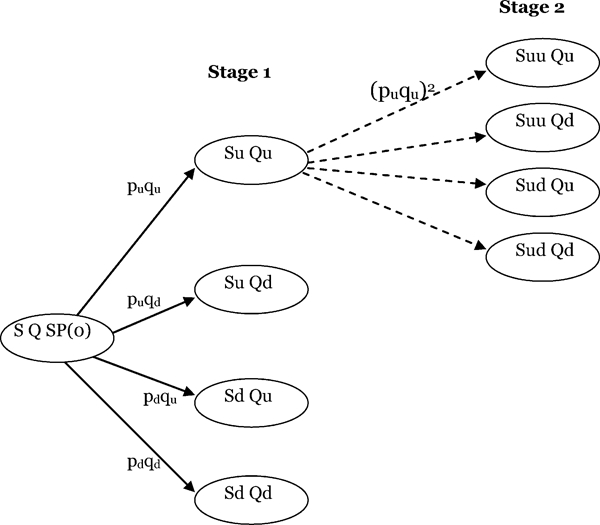

Figure 1 shows the combined branching process for both variables for the first three stages. Starting from stage 1, four branches go out to stage 2, with four more branches going out from each node to stage 3. Even though the prices recombine, the scenarios must be distinguished because decisions made at earlier time periods influence subsequent decisions (e.g. the stockpile could be empty in one scenario but not in another). However later decisions do not affect earlier ones (non-anticipatory clause).

Diagram showing the branching process starting from the initial state (stage 0), with four branches going out to stage 1, and then four more branches going out from each node to stage 2. At the outset, the price was S, the mine was in full production and the stockpile contained SP(0). At stage 1, in the top scenario the price rose to Su, while the quantity produced remained high. The probability of reaching this node is puqu. Similarly for the other three nodes. Each node in stage 1 branches out to four more nodes. The price in the top one is Suu; the production Qu, is full. The probability of reaching this node is puqu×puqu = (puqu)2

Case studies

Three case studies were carried out for all the consortium members that sponsored this work in order to test the program under different circumstances, but because of the limited space available only the results of the first one are presented.

When the production would normally satisfy the contractual commitments except if major production incidents occur. This is, of course, the normal situation. The interaction between building up a stockpile, buying or selling on the spot market and leasing material is of interest. In the first case the stockpile is full (200 units) whereas in the second one it contains only 40 units.

When the contractual commitments are small compared to the production potential. In this case the excess production is sold on the spot market, or stockpiled. If there is still excess capacity, the production should be cut back (i.e. the first control variable will be less than its normal value of 100%).

When the contractual commitments are larger than the production potential. Under these circumstances, after having used up the stockpile and exhausted the possibilities of buying on the spot market or leasing material, the Company would be obliged to accept a shortfall (and the ensuing penalty). The penalty parameter has been set to a dissuasively high value to discourage this.

Parameter values

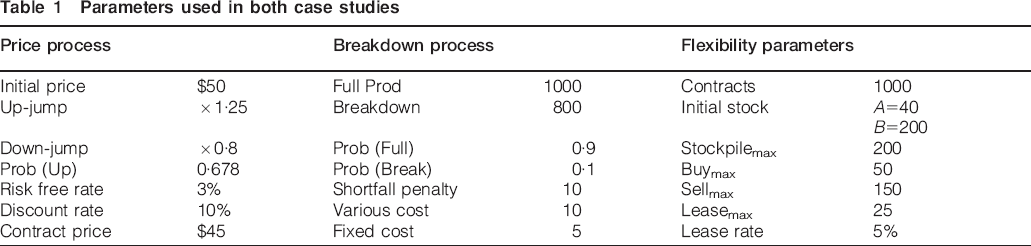

Table 1 presents the values of the parameters used for the first case. Throughout the case studies, it was assumed that the commodity prices follow a geometric Brownian motion. For confidentiality reasons we set the initial value S0 to $50, and the volatility to 22·3%. In fact these are the values used by Hull (2003) in his textbook example of a binomial tree. After one up-jump or a down-jump, the prices are $62·50 and $40 respectively. The contractual price was set to $45, that is, a little less than the initial spot price. For simplicity, the corporate discount rate, the risk-free rate and the lease rate were taken to be 10, 3 and 5% respectively.

Parameters used in both case studies

One of the key questions was to decide how serious the production incidents should be. As management are used to handling minor incidents, it was assumed that only being able to produce at 80% of full rate would constitute a major incident. For a company with five mines this corresponds to one mine being out of action for the full 12 months. In the example the production would drop to 800 instead of 1000 for full production. The Company's contractual commitments were set to 1000. In the event of an incident, the Company would be short 200 units. The probability of an incident occurring was set to 10%. In case 1A, the stockpile was assumed to be full initially (with 200 units of the commodity). In that case, the Company could take material to avoid a shortfall but could not stockpile any more under normal circumstances when there is some excess production. In case 1B, it was assumed to contain 40 units of material.

Project value and results

The project value was computed over a 5-year period, with a time step of 1 year. That is, a five-stage problem was considered. In that case the tree in last year contains 45 = 1024 terminal nodes, each with five control variables. In stage 2, there are 4×5 = 20 control variables and another 16×5 = 80 for the third stage and so on. This leads to a system with 6280 unknowns which can easily be solved using Matlab.

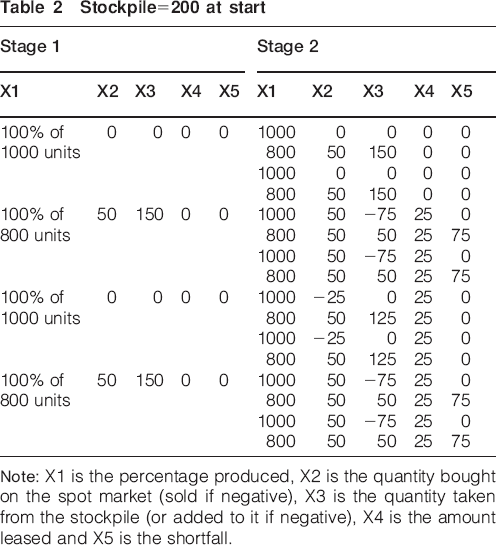

The real problem is to visualise and interpret the results. Tables 2 and 3 give the values of the control variables in the first two stages. In the first case where the stockpile is full initially, if an incident occurs, the mine makes up the 200 unit drop in production by buying 50 units on the spot market and taking 150 units from the stockpile, leaving 50 units in the stockpile. If another incident occurs the next year, it takes the remaining 50 units from the stockpile, buys 50 units on the spot market leases 25 units, leaving a shortfall of 75 units. However, if no incident occurs, no extra material can be stockpiled because the stockpile is already full.

Stockpile = 200 at start

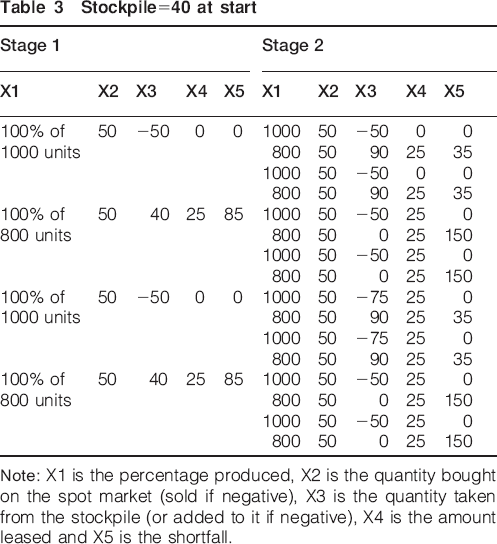

Stockpile = 40 at start

In the second case where the stockpile only contains 40 units, the optimal strategy if a production incident occurs, is to buy as much as possible on the spot market (50 units), lease as much as possible (25 units) and then take all the material in the stockpile (40 units), leaving a shortfall of 85 units. This would be the natural thing to do. But the results are counter-intuitive if no incident occurs in the first stage. The optimisation over a 5-year period shows that the mine should buy 50 units on the spot market (X2 = 50) and add this to the stockpile (X3 = −50). Most managers would not consider doing this unless an optimisation of this type had shown that it was better in the long run to do this.

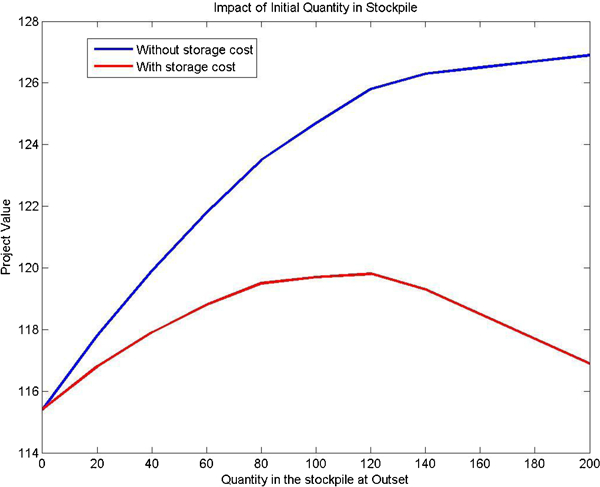

Next, we show how multistage programming with recourse can be used for strategic decision making. The impact of the quantity of material initially in the stockpile on the value of the project was studied. Figure 2 gives the project value computed when the cost of the material is taken into account (red) and when it is not (blue), depending on whether it is considered as a sunk cost or not. If the cost is considered, the maximum value occurs when the stockpile is about half full initially. Intuitively this allows management the flexibility to stockpile excess production if the spot price is low and the mine is in full production, and yet provides material to reduce the shortfall in case of a production incident.

Impact of the initial quantity in the stockpile on the project value when the storage cost is taken into account (red, below) and when it is not (blue, above)

Discussion and conclusions

The Company that commissioned this study wanted to determine the optimal strategy if confronted by a major production incident that would prevent or seriously reduce production for several months or more. The courses of action that are open to management vary from one operation to another. In this case, the following options were identified: buying on the spot market, taking material from a strategic stockpile or leasing material. A methodology based on multistage programming with recourse was developed to estimate the dollar value of the project with and without these types of flexibility. One advantage of this approach is that it provides decision makers with a ‘road map’ of how much to produce, how much to buy or sell, how much to take from the stockpile or add to it, or how much to lease as a function of the spot commodity price relative to the long-term contract price and whether the mine is in full production or has suffering from a major production incident.

If other companies want to develop a similar strategy, the first step would be to determine what financial and operating options are effectively open to them in the event of a production incident, and then to set up an objective function that reflects their revenue and cost structure. Once that has been done the same approach could be applied. As the trees representing the commodity prices and the state of production have been discretised, the system to be solved merely involves linear programming and most mining companies can handle this.

In the case-study presented to show how the procedure works, we evaluated the impact of the amount of material initially in the stockpile on the project's value, and hence to determine the optimum stockpile size. Preliminary results suggest that the value of the stockpile depends on how ‘tight’ the market is. If there is excess capacity on the market, it would be easier to make up a potential shortfall by buying on the market than by having recourse to a stockpile. However if there is little or no surplus on the market, then a stockpile could prove to be a valuable asset.

One point in the work that requires further work is how to choose the probability of a production incident and its severity. Here, we set the loss of production at 20%, which initially seemed rather severe. Having said that, ERA lost between 25 and 35% of sales revenues due to the heavy rainfall at the Ranger mine, even though production only stopped for 2–3 weeks. In-depth studies of the frequency and severity of major production incidents need to be carried out in the future. These empirical studies should also determine what links exist between production incidents and the commodity price. In this paper we have made the simplifying assumption that incidents have no impact on prices. We think that this is true for companies that are minor suppliers in the market or when the market is in oversupply. However a production incident at times of strong demand or involving a major supplier, would probably lead to a price increase. Further work is required to assess the impact of structural links between these incidents and prices in these two cases. On the theoretical side it would be interesting would be to extend the model to cases where production incidents affect the commodity price.

Footnotes

Acknowledgements

This research was carried out as part of a Consortium on the Application of Real Options in Mining. We would like to thank the sponsors, Codelco (Chile) and two multinational mining groups, for their support and encouragement during the consortium, and the reviewers for their constructive comments.

1

In mathematics inf is the abbreviation for infimum. The infimum of a subset S of a partially ordered set T is the greatest element of T that is less than or equal to all elements of S. See Wikipedia for some examples.