Abstract

Even though the transaction costs framework has evolved considerably in the past decade, there is still only modest empirical knowledge about the governance performance implications of the theory. This article focuses on the governance performance of vertical coordination in relationships between manufacturing firms. On the basis of transaction cost analysis and related works in international marketing, the authors examine the impact of asset specificity and vertical coordination on ex post transaction costs in domestic and international buyer–seller relationships. In accordance with current literature in international marketing, performance measurement problems are expected to be more evident in international business trade than in domestic business-to-business relationships. The empirical findings show that under conditions with substantial asset specificity, vertical coordination reduces ex post transaction significantly more in international buyer–seller relationships than in domestic channel dyads.

In the absence of effective performance measurement, the high-powered incentives of market governance are expected to fail (Williamson 1991). Performance measurement difficulties are strongly associated with the degree to which the value of a trade partner's contribution is difficult to verify by ex post inspection of output (Ghosh and John 1999). In accordance with transaction cost analysis (TCA), performance measurement problems are expected to enforce the need for supportive governance arrangements to maintain productive value-adding opportunities and verify the benefits and costs associated with the trading parties’ contributions. In interorganizational research and strategic marketing management, such supportive governance arrangements have been conceptualized as “intermediate” or hybrid modes of governance, distinct from the traditional modes of market and hierarchy (Williamson 1985).

Research on intermediate governance modes has significant implications for strategic management, because it explores critical choices related to the scope and boundaries of the firm. The business press regularly reports dramatic changes in economic institutions that involve substantial reorganizations of buyer–seller relationships. These include, for example, new forms of research and development collaboration and cooperative arrangements to facilitate new product development and effective value adding.

Intermediate modes of governance take several forms, such as joint ventures (e.g., Harrigan 1988), strategic partnerships or alliances (e.g., Heide and John 1990), relational contracting (e.g., Heide and John 1992), joint action (e.g., Heide and John 1990), and vertical coordination (e.g., Andersen and Buvik 2001; Stern and Reve 1980). Vertical coordination implies organization of the flow of activities, resources, and information between supplier and buyer that extends well beyond the normal, legally enforceable interactions associated with an arm's-length exchange of price and quantity information.

According to TCA, specific assets and the uncertainty surrounding the exchange between the buyer and the seller represent the core dimensions of the transaction. The composition of these dimensions is supposed to be decisive for the way cost-efficient governance modes should be assigned to the transaction (Williamson 1981). When bilateral trade takes place under uncertain trade conditions, the combined presence of substantial asset specificity and performance measurement problems is assumed to create bilateral dependence and trading hazards that enhance the need for stronger vertical coordination.

So far, relatively few empirical studies have addressed governance performance problems in business-to-business relationships. Significant contributions include Buvik and John (2000), Dahlstrom and Nygaard (1999), and Noordewier, John, and Nevin (1990). We follow this research agenda and in particular examine the impact of vertical coordination on ex post transaction costs. The performance of interfirm governance is dependent on both the present level of performance measurement problems and employment of assets at risk (Williamson 1985), and this research investigates whether increased vertical coordination lowers transaction costs when asset specificity becomes substantial (Williamson 1991). Furthermore, we compare this performance pattern across domestic and international settings of interfirm trade. Ongoing relationships between independent buyers and sellers (no cross-holdings) in domestic and international marketing relationships constitute the unit of analysis, and a specific construct of ex post transaction costs is the dependent variable in the research.

Conceptual Framework

Background

The TCA perspective states that specific assets and the uncertainty surrounding interfirm exchange are the basic factors that evoke shifts in the mode of governance from conventional markets toward bilateral governance or vertical integration (Williamson 1981). The uncertainty surrounding interfirm trade arises from the difficulties in predicting and evaluating the behaviors and actions of trade partners (Williamson 1985). Such performance measurement problems have been employed as determinants of interfirm organization in the current literature. Notwithstanding, little empirical evidence has verified the impact of performance measurement problems on the performance of interfirm governance (Rindfleisch and Heide 1997).

The TCA framework states that bounded rationality combined with performance measurement difficulties creates substantial verification problems (Heide and John 1990; Rindfleisch and Heide 1997; Williamson 1985). To explore the possible effects of such performance measurement problems, we compare two sets of relationships that are expected to deviate with respect to this dimension. The international business literature asserts that international interfirm trade is surrounded by higher performance measurement difficulties than is the case in domestic business relationships (Anderson and Gatignon 1986). The higher measurement complexity in international settings has been explained by the lack of international experience or experiential knowledge and by sociocultural differences between home and host cultures (Anderson and Gatignon 1986).

In domestic buyer–seller relationships, the transacting parties are expected to be more familiar with current standards of trade, which provides better judgment of the performance of interfirm transactions. Furthermore, the specification and evaluation of trade performance and fulfillment of contract terms are expected to be far more difficult in international settings (Harrigan 1988). Even firms with extensive overseas experience perceive difficulties in understanding the practices of foreign business partners, evaluating complex product standards, and obtaining reliable market information in foreign markets. Accordingly, all other things being equal, we expect that the performance measurement problems surrounding interfirm trade will be higher in international buyer–seller relationships than in domestic ones.

Dependent and Independent Variables

Ex Post Transaction Costs

Ex post transaction costs represent the dependent variable in this research. The TCA framework states that substantial asset specificity increases the costs of safeguarding interfirm agreements because of the prospects of opportunistic behavior of the trading partners (Pilling, Crosby, and Jackson 1994; Williamson 1985). Such costs are associated with haggling, verification problems, and other bargaining difficulties that may arise because of inappropriate or ambiguous performance measures, hidden information, or moral hazards. The lack of appropriate performance measures may lead to productivity losses due to free-riding or performance relaxation (Ghosh and John 1999). Transaction costs can be separated into ex ante costs and ex post costs. Ex ante costs represent direct opportunity costs (Ghosh and John 1999), which imply productivity losses resulting from the lack of appropriate employment of specific assets or from lost trade opportunities (Ghosh and John 1999; Rindfleisch and Heide 1997). This research focuses on ex post costs that are associated with the problems of performance evaluation, such as measurement costs (e.g., verification of production costs), performance evaluation costs (e.g., product quality assessment), adjustment cost (e.g., due to changed orders), and bargaining costs (e.g., due to hidden information in negotiations of prices).

Vertical Coordination

The TCA framework argues that interfirm exchanges fraught with unforeseen contingencies cannot be governed with complete contracts. The parties can resort to incomplete contracts that enable them to adapt better to changing circumstances by aligning supportive governance arrangements. One such supportive mechanism is vertical coordination (Stern and Reve 1980). This implies routinization of information exchanges and joint planning in ways that extend beyond an arm's-length exchange of information about product design specifications, verification of production costs, and production planning. In this research, we conceptualize vertical coordination as the interactions that organize the flow of activities, resources, and information between supplier and buyer to improve value-adding and marketing performance (Dahlstrom and Nygaard 1999). Specifically, vertical coordination is important to improve the handling of ex post matters such as cost documentation, product design changes, production planning, and quality control. We find that vertical coordination of these issues reflects significant aspects of the coordinated adaptation, which takes place to support trade between manufacturing firms.

Asset Specificity

Asset specificity has been extensively employed in empirical research as an antecedent to vertical integration and vertical coordination (e.g., Buvik and Reve 2001; Heide and John 1990). Asset specificity refers to physical and immaterial assets tailored to a specific relationship that cannot be redeployed for other purposes without the sacrifice of productive value. This research focuses on asset specificity on the buyer side (Heide and John 1988, 1992), which refers to adaptations and resources the buying firm deploys to tailor own skills, product design, production processes, or logistics to the relationship with a specific supplier.

Research Hypotheses

Several studies assert that the costs of acquiring information that is needed to measure and evaluate the performance of an exchange partner are higher in international business trade than in domestic business-to-business relationships (Eriksson et al. 1997).

The availability of accurate and reliable information about trade partners is restricted in foreign markets for several reasons and incurs trading hazard problems (Barney 1997). Both cultural and geographic distances between trade partners restrict the use of extensive personal information exchange that allows for immediate feedback and observation of multiple cues, such as body language and facial expression (Daft and Lengel 1990). Furthermore, third-party information from competitors, customers, or suppliers for the purpose of validating and complementing information about trade partners is less available in foreign markets because of restricted knowledge about business actors in international settings (Daft and Lengel 1990).

Transaction cost analysis asserts that performance measurement difficulties will increase the costs of evaluating the performance of exchange partners and thus incur ex post transaction costs (Buvik and John 2000; Ghosh and John 1999; Rindfleisch and Heide 1997). Accordingly, we state the following hypothesis:

Ex post transaction costs are higher in international buyer–seller relationships than in domestic channel dyads.

In accordance with TCA reasoning, we argue that the governance performance of vertical coordination is contingent on both the present levels of asset specificity and measurement difficulties surrounding interfirm trade (Williamson 1985). One fundamental assumption underlying the TCA perspective is that the assignment of governance forms serves governance performance and economizes on transaction costs (Williamson 1985, 1991). Figure 1 depicts this reasoning in more detail. We illustrate the relationship between ex post transaction costs and asset specificity for two different modes of governance (market governance, Line A, and vertical coordination, Line B).

Governance Mode, Asset Specificity, and Ex Post Transaction Costs

Transaction cost analysis predicts that market governance is cost efficient when the level of asset specificity is modest. When asset specificity remains low—for example, in the trade of standardized products—interfirm ties are still modest, and market governance will be the frame for deciding terms of trade (e.g., prices, service level, product quality). Basic TCA reasoning assumes that as long as competition and conventional market conditions prevail, exposure to opportunism is expected to be of less concern because of reputation effects. Under such conditions, the whole market or market segment is expected to provide collective insurance against moral hazard (e.g., unfair prices, quality decreases), and conventional verification efforts can still be enforced (Buvik and Reve 2001; Heide and John 1990). This is illustrated in Figure 1, in which the governance costs associated with market governance (Line A) are lower (i.e., higher governance performance) than the governance costs associated with vertical coordination (Line B) when asset specificity is low or modest (below the level of ASPEC 1).

Vertical coordination will be more advantageous (higher governance performance) when asset specificity becomes substantial. Under such circumstances, vertical coordination arrangements are warranted for the purpose of enhancing the utility of specific productive resources (Williamson 1991). Substantial asset specificity is expected to enforce interfirm dependence, small number conditions, and subsequent exposure to opportunism. Accordingly, when asset specificity becomes substantial, enforced vertical coordination is warranted for the purpose of handling the trading hazards that small number conditions foster (Williamson 1985). Figure 1 illustrates this reasoning and demonstrates that the ex post transaction costs associated with vertical coordination (Line B) are lower (high governance performance) than the governance costs associated with market governance (Line A) when asset specificity becomes substantial (i.e., exceeds the level of ASPEC 1).

The governance efficiency pattern described previously is, however, contingent on the present performance measurement problem (Williamson 1985). Information asymmetry and performance ambiguity are expected to enforce the exposure to opportunistic behavior and moral hazards, in particular when asset specificity is substantial. Under such circumstances, the firms employing specific assets will face both performance evaluation problems and a safeguarding problem, and it becomes urgent to align supportive governance arrangements to work things out and settle agreements (Williamson 1991).

As argued previously, performance measurement difficulties are expected to be more evident in international marketing relationships than in domestic channel dyads (Anderson and Gatignon 1986). On the basis of this reasoning, we propose the following refutable hypothesis:

When there are high levels of asset specificity, vertical coordination will be more effective in lowering ex post transaction costs in international buyer–seller relationships than in domestic buyer–seller relationships.

Control Variables

Purchasing Amount

The TCA framework assumes that parties to a high-stakes exchange will face higher exposure to opportunism and higher transaction costs when terms of trade are to be realigned. Furthermore, the purchasing amount might reflect the frequency of interfirm exchange and therefore be associated with the efficiency of specialized vertical coordination arrangements (Rindfleisch and Heide 1997; Williamson 1985). The buying center literature also suggests that greater stakes attract parties from multiple organization levels and across several departments within each firm and make the industrial purchasing process more complex (Johnston and Bonoma 1981). Most discussions of interfirm relations find that the amount of business-to-business trade reflects a significant stake and use the natural logarithm of the buyer's annual dollar purchases from the focal supplier to control for these effects.

Prior Length of Relationship

According to relational contracting theory, relational norms, trust, and personal relationships will be developed as firms’ relationships evolve over time. Relational norms are expected to diminish the hazards of opportunism over time (Bradach and Eccles 1989) and thereby attenuate ex post transaction costs. To account for this effect, we introduced the natural logarithm of the prior length of the relationship in our research model.

Customization

We incorporated the customization of the supplier's product in the research model to account for possible effects of the complexity of interfirm exchange. Product customization reflects technological factors, which represent important sources of interfirm dependence. Furthermore, product customization will reflect the supplier's employment of specific assets with subsequent need for supportive governance arrangements (Williamson 1985). Accordingly, we expect increased product customization to increase ex post transaction costs.

Research Setting and Data Collection

Research Context

The unit of analysis is the relationship between independent manufacturing firms with no ownership cross-holdings. The present study addresses how the buying firm perceives the level of its own specific assets, ex post transaction costs, and the extent of vertical coordination in a specific supplier relationship. Data were collected from manufacturing firms from different Standard Industrial Classification codes, and representation was highest among firms from chemical production (25%) and engineering production (45%). The average size of the purchasing firms was $112 million, and the annual purchasing amount delivered by the focal supplier to the purchasing firm was $1.63 million, on average, in the sample.

The empirical setting is composed of 177 relationships between manufacturing firms in Norway. Among these, 128 relationships represent interfirm trade between domestic buyers and sellers, and 49 relationships consist of Norwegian buying firms and foreign suppliers. A majority of firms (87%) was engaged in foreign trade, and the average share of these firms’ sales (export share) going to export markets was 61%. There was no significant difference across domestic and international channel dyads in our sample with respect to export sales and export share.

Pilot Studies

To capture the full domain of the constructs in the research model, we carried out an extensive literature search on the research issue (Churchill 1979). Then, we performed several exploratory studies. The first one was based on personal interviews among purchasing professionals in manufacturing firms; purchasing consultant firms; and academics doing research in procurement, logistics, and production planning.

In the next step, we undertook an archival study of purchasing agreements across four different industries to examine whether the interorganizational issues of the research corresponded to terms applied in industrial purchasing agreements. Two industry organizations and the Norwegian Association of Purchasing and Logistics provided specific contract schemes that are regularly used in four different industries for this purpose.

We then carried out a pilot study based on a semistructured questionnaire among 14 manufacturing firms to obtain preliminary tests of scales and capture relevant issues reflecting asset specificity, vertical coordination, and transaction costs. The data collection was administered at a national, annual conference in business logistics arranged by the Norwegian Association of Purchasing and Logistics for Norwegian industry firms. This research gave important guidelines for improvements of ambiguous questions, imprecise vocabulary, and scaling methods.

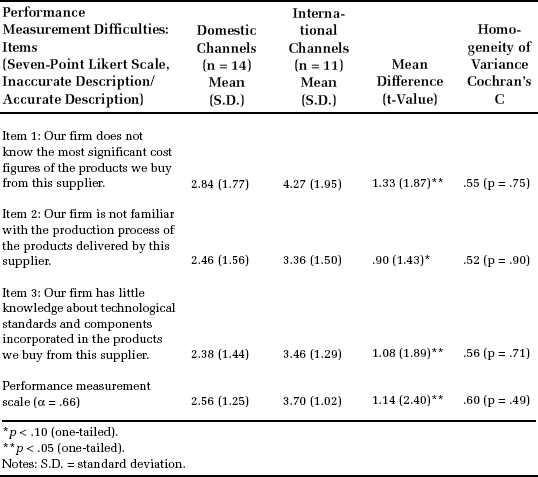

Before the full-scale data collection, we conducted a quasi-experimental design among 25 manufacturing firms outside our sampling frame to examine whether performance measurement problems varied across domestic and international buyer–seller relationships. Among these, 14 firms were instructed to report about their interactions with a focal domestic supplier, and 11 firms were instructed to report about their relationship with a specific foreign supplier on the basis of a three-item scale that captured performance measurement difficulties. The analysis of the pilot research data demonstrated significantly higher measurement difficulties (mean difference 1.14, p < .05) in international buyer–seller relationships than was observed in domestic relationships (Appendix 1). Finally, we carried out a pretest of the revised questionnaire based on personal interviews; the pretest revealed no significant problems with any of the measures or scaling formats.

Data Collection

The final questionnaires were in Norwegian and were mailed to a census of 684 industrial purchasing professionals with memberships in the Norwegian Association of Purchasing and Logistics. Appendix 2 provides a sample of the items translated into English.

This design corresponds to a key informant approach (Campbell 1955), in which the selection of informants in the buying firms is based on informants with particular knowledge about the core issues of the research. The informants were asked to select a specific (focal) supplier firm that they considered important for the purchasing firm's value-adding and procurement strategy, and they were instructed to relate all the questions and subsequent information to the relationship with this supplier. No instructions were given to the informants with respect to the nationality of the selected firms. Greater familiarity with and knowledge about domestic supplier firms might explain why most of the informants (72%) selected Norwegian firms as their focal supplier in this research.

Among the informants, 114 reported that they fell outside the scope of the study because their firm had gone out of business or was no longer engaged in manufacturing. Among the remaining 570 informants, 182 (32%) responded to the questionnaire after two callbacks. In the group of nonresponders, 67% reported busy work schedules or lack of time as the main reasons for not participating in our research.

We measured nonresponse bias by comparing early and late responders (Armstrong and Overton 1977). Most of the questionnaires (64%) were returned within a month, and two callbacks captured the last 36% of the sample. There were no significant differences with respect to prior length of relationship, firm size, annual purchasing amount, or key informants’ knowledge of and involvement with the selected informants between the two groups. Among the responding firms, 177 (97%) responded completely to all 30 items incorporated in the constructs that represented our research model.

Measure Development and Validity Assessments

Construct Validity

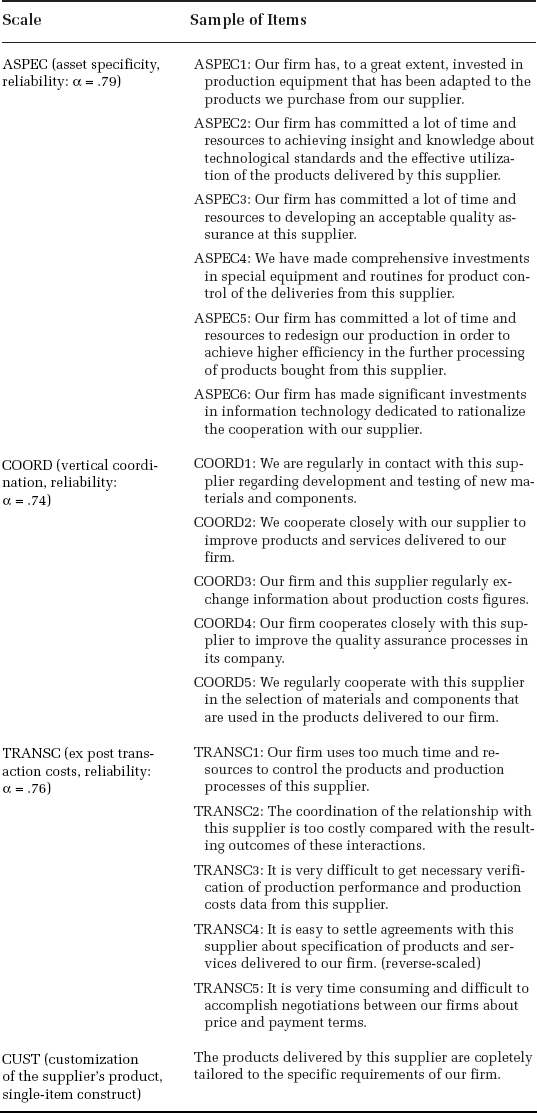

We used Likert-type items on a 1 to 7 scale with endpoints “inaccurate description” and “accurate description” to measure asset specificity, vertical coordination, and ex post transaction costs (see Appendix 2). We estimated the correlation matrix for each multi-item construct and inspected item–total correlations to detect possible ill-fitting items. We factor analyzed each set of items to verify a single factor structure. We calculated the internal consistency of the scales by Cronbach's α.

Transaction Costs (TRANSC)

Consistent with Williamson (1985, 1991), transaction costs were defined as ex post costs connected to the problem of performance evaluation and monitoring. This research focuses on measurement costs (verification of production costs), performance evaluation costs (assessment of product and production process quality), adjustment costs (coordination efforts and product specifications), and bargaining costs (hidden information in price negotiations). Empirical work by Dahlstrom and Nygaard (1999) provided a useful suggestion for measuring these dimensions of transaction costs. Principal axis factor analysis of the five items that reflect transaction costs assigned all of them to one single-construct factor, and the item–total correlation among the items showed satisfactory internal consistency with a Cronbach's α of .76.

Asset Specificity (ASPEC)

Asset specificity describes the investments made by the buyer in physical assets, production facilities, tools, and knowledge that are tailored to a specific purchasing relationship. The construct is based on items developed by Heide and John (1990, 1992). Asset specificity is expected to reflect a broad scope of resources that are tailored to the relationship (Williamson 1991), and the measure construction is based on reflective scaling of six items. All items were factor analyzed and assigned to one single construct factor, and the scale showed satisfactory reliability, with a Cronbach's α of .79.

Vertical Coordination (COORD)

Vertical coordination describes the extent of interfirm flows of activities, resources, and information in order to coordinate productive values and deal with the realignment of terms of trade. Empirical studies from manufacturing settings by Heide and John (1990, 1992) and Noordewier, John, and Nevin (1990) gave constructive guidelines for determining issues and items reflecting this concept. Principal axis factor analysis assigned all five items reflected by this concept to one single-construct factor, and a Cronbach's α of .74 indicates satisfactory internal consistency for the scale.

Domestic versus International Buyer–Seller Relationships (INTNAT)

A dummy variable approach was applied in which 0 represents domestic buyer–seller relationships and 1.0 represents relationships in which the buyer firm and the supplier firm have different countries of origin.

The prior length of the relationship (LENGTH) and annual purchasing amount (PURCH) are both single-item measures based on metric scales (years and dollars). The customization of the supplier's product (CUST) is measured by a single item, which is described in Appendix 2.

Discriminant Validity

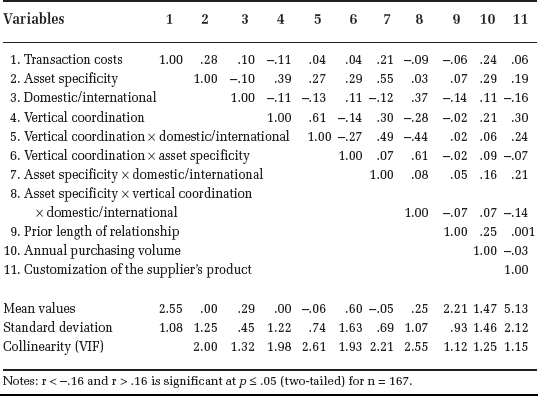

We assessed discriminant validity by confronting all of the 16 items that represent vertical coordination, asset specificity, and transaction costs in a maximum likelihood factor analysis (Table 1). All own-construct loadings are above .40, and all cross-construct loadings are smaller than the corresponding own-construct loadings. The analysis provided support for a three-factor model (χ2 = 89.30, d.f. = 75, p = .125) and indicates satisfactory discriminant validity for these constructs.

Assessment of Discriminant Validity of Specific Assets, Vertical Coordination, and Ex Post Transaction Costs (Maximum Likelihood Factor Analysis, Rotated Factor Matrix)

Notes: Fit of three-factor model: χ2 = 89.30 (d.f. = 75, p = .125). Complete descriptions of the items are given in Appendix 2.

On the basis of TCA reasoning, we expect vertical coordination to be positively associated with asset specificity, and our empirical findings confirm that this association is positive and significant (r = .39, p < .01; Table 2). To assess discriminant validity between asset specificity and vertical coordination further, we regressed these two constructs against ex post transaction costs, which are expected to be correlated with both of these constructs but in opposite directions, in accordance with TCA arguments (Williamson 1985, 1991). Such a pattern of association is logically impossible if asset specificity and vertical coordination reflect the same construct (Tesser and Krauss 1976).

Correlation Matrix

Notes: r < -.16 and r > .16 is significant at p ≤ .05 (two-tailed) for n = 167.

Consider the outcome of the regression analysis in Table 3. It shows that the association between vertical coordination and ex post transaction costs is negative (b2 = -.20, p < .01), in accordance with Dahlstrom and Nygaard's (1999) empirical findings. Furthermore, asset specificity is positively associated with ex post transaction costs (b1 = .32, p < .01), which replicates Pilling, Crosby, and Jackson's (1994) findings. Taken together, our findings satisfy one of Tesser and Krauss's criteria, which states that the discriminant validity of Variable A (vertical coordination), Variable B (asset specificity), and Variable C (ex post transaction costs) is established if the correlation between A and C (rAC) < 0 (b2 = -.20 in Table 3), the correlation between B and C (rBC) > 0 (b1 = .32 in Table 3), and the correlation between A and B (rAB) > 0. The correlation between A and B (rAB) is r = .39 and is significant at p < .01 (see Table 2). These validity assessments give strong support for satisfactory discriminant validity of the basic TCA constructs in our model and further provide support for nomological validity of the TCA constructs.

Regression Analysis: Assessment of Discriminant Validity (Dependent Variable: Ex Post Transaction Costs [C])

Notes: The correlation between asset specificity and vertical coordination (rAB) is r = .39 * (see Table 2).

Significant at p < .01.

Model Specification and Empirical Findings

Model Specification

The following ordinary least squares regression model was estimated to test the research hypotheses:

ex post transaction costs, asset specificity, international versus domestic relationships, vertical coordination, customization of the supplier's product, the natural logarithm of the prior length of the relationship, the natural logarithm of annual purchasing volume, intercept, and error term.

The estimated model includes all the main effects and the interaction effects and seems to be well fitted to our data set (R2Adj = .25, F(10,156) = 6.42, p < .01). When a large number of interaction terms is included in one model, the likelihood of serious multicollinearity problems exists. Except for the dummy variable, we centered the scales of the variables entering the interaction terms (Cronbach 1986) to cope with possible collinearity problems. Collinearity diagnostics revealed acceptable tolerance measures (variance inflation factor [VIF]) for all variables (Table 2). We then inspected residuals for heteroscedasticity, and no particular pattern appeared.

Test of the Research Hypotheses

H1 involves the difference in ex post transaction costs between domestic and international buyer–seller relationships. This should be positive and significant, and our empirical findings support this prediction and show that ex post transaction costs are significantly higher in international buyer–seller relationships than in domestic business-to-business relationships (b2 = .45, t = 2.46; p < .05, see Table 4).

Regression Analysis: Entire Sample, Domestic and International Buyer–Seller Relationships (Dependent Variable: Ex Post Transaction Costs)

Notes: S.D. = standard deviation; n.s. = not significant.

H2 involves the interaction term of the three-way interaction (ASPEC x COORD x INTNAT). According to the hypothesis, we expect that there will be a more negatively shaped relationship between vertical coordination and transaction costs in international buyer–seller relations than in domestic buyer–seller relations when asset specificity is substantial. If this is the case, the interaction term (b7) should be negative. Furthermore, when deducing separate regression analysis for domestic and international buyer–seller relationships, we expect the interaction effect of specific assets and vertical coordination on ex post transaction costs (ASPEC x COORD) to be significant and negative in international buyer–seller relationships and less negative (less governance performance) in domestic buyer–seller relationships.

Moderated regression analysis was used to test the hypothesis. This method is generally regarded as a conservative method for identifying interaction effects, because the interaction terms are not tested for significance until the main effects of the independent variables are estimated in the regression equation. Therefore, the interaction effects are significant only if they add explanatory power to the regression model (Jaccard, Turrisi, and Wan 1990).

We first compared a model consisting of the three two-way interactions with a model with no interaction terms by testing the incremental R2. The observed F-value was 2.20 (d.f. = 3,163), indicating the presence of significant two-way interaction effects (p = .07). Then, we compared the complete model that included the three-way interaction term (ASPEC x COORD x INTNAT) with the restricted model that included the three two-way interaction terms. In this case, the observed F-value was 9.72 (d.f. = 1,165), implying the presence of a statistically significant three-way interaction (p < .01), as anticipated in H2. We measured the strength of the three-way interaction effect by the difference in R2 between the complete model with the three two-way interaction term and the restricted model (Jaccard, Turrisi, and Wan 1990). This turned out to be .05, which means that the three-way interaction effect accounts for 5.0% of the explained variance in ex post transaction costs.

To elaborate this further, we examined two separate regressions models (Models 1a and 1b) deduced from the complete model (Table 4). Goodness-of-fit measures (F and R2Adj) show that Model 1b (international buyer–seller relationships) fits the data set better than Model 1a (domestic relationships). In the domestic setting, the interaction effect of vertical coordination and asset specificity on transaction costs was absent (b6 = .04, t = .60). In international buyer–seller relationships, the governance efficiency of vertical coordination was significantly improved as asset specificity increased (b6 = -.31, t = −3.91; p < .01 for the interaction term ASPEC x COORD), corresponding to the prediction in H2.

In summary, the regression analysis (Table 4) shows that b7 is significantly less than zero (b7 = -.36, t = −3.35; p < .01), which demonstrates that when asset specificity becomes substantial, vertical coordination reduces ex post transaction costs more in international buyer–seller relationships than in the domestic dyads.

We can more precisely conduct this analysis by making a statistical test comparing the interaction effect of vertical coordination and specific assets on ex post transaction costs in international buyer–seller relationships (estimated coefficient is -.31) with that in domestic buyer–seller relationships (estimated coefficient is .04). We tested the difference in the regression coefficient across the two subgroups (Δb = -.35) by conducting a Chow test (Chow 1960), which confirmed a significant difference across these two subgroups (t = 3.51; p < .01). Accordingly, our hypothesis (H2) stating that that high vertical coordination combined with substantial asset specificity reduces ex post transaction costs more evidently in international buyer–seller relationships than in domestic relationships received strong support.

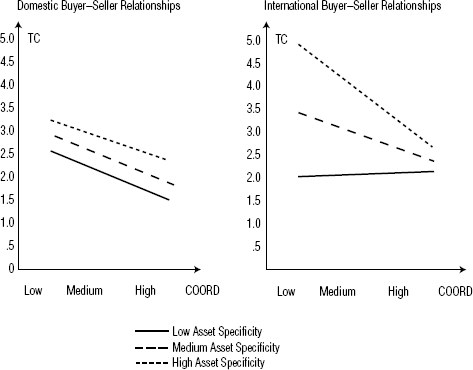

To obtain further insight into the nature of this interaction, we estimated ex post transaction costs for low, medium, and high levels of asset specificity and vertical coordination for each of the two models. Following Jaccard, Turrisi, and Wan (1990), we defined low as one standard deviation below the mean, medium as the mean, and high as one standard deviation above the mean. We held the effects of the control variables constant at their average levels. Note that these three-level scales (value) for specific assets and vertical coordination were restricted to the analysis in Figure 2.

Estimated Transaction Costs (TC) for Domestic and International Buyer–Seller Relationships for Different Levels of Vertical Coordination and Asset Specificity

The plotted lines in Figure 2 show the association between vertical coordination and ex post transaction costs. A downward sloping line indicates that ex post transaction costs decrease as vertical coordination increases. The figure demonstrates that for all levels of vertical coordination, ex post transaction costs are higher when asset specificity increases.

If H2 is to be corroborated, the line connecting vertical coordination and ex post transaction costs should be steeper for the group of international buyer–seller relationships than for domestic buyer–seller relationships when asset specificity is high. As Jaccard, Turrisi, and Wan (1990) recommend, we conducted t-tests to test the differences in slopes. The slope of this line for the international relationships was significantly steeper than for domestic relationships in the case of high asset specificity (t = 2.22, p < .05; d.f. = 164). There were no significant differences in the slope of this line between international and domestic relationships for the medium or the low level of asset specificity. Taken together, the moderated regression results and the analysis in Figure 2 provide further support for H2.

Nonfocal Associations

The outcome of the regression analysis demonstrates that there is an overall positive association between asset specificity and transaction costs (b1 = .24, t = 2.92; p < .01), in accordance with basic TCA predictions (Willamson 1991), which replicates Pilling, Crosby, and Jackson's (1994) empirical finding.

In accordance with relational contract theory, the prior length of the relationship (LENGTH) is negatively associated with transaction costs (b9 = -.18, p < .05) and indicates that relational ties build up and attenuate conflicts and exchange difficulties as relationships evolve over time. Furthermore, the annual volume of trade (PURCH) shows the predicted positive effect on ex post transaction costs (b10 = .19, p < .01) and indicates that stakes and trading complexity enhance exchange difficulties.

The customization of the supplier's product (CUST) is expected to enhance interfirm dependence and ex post transaction costs because of trading hazards. The association between product customization and transaction costs was positive but not significant (b8 = .04, t = 1.16; p >.10).

Taken together, the analysis demonstrates that the TCA-based predictor variables maintain explanatory power when relevant control variables are implemented in the model and indicates a satisfactory robustness of the model.

Discussion and Implications

Research Findings and Implications

Even though TCA offers a compelling logic for evaluating the performance of alternative governance structures, there is still only modest empirical knowledge about the performance implications of the theory (Rindfleisch and Heide 1997). By measuring ex post transaction costs, we have investigated how the governance efficiency of vertical coordination is related to the present level of trading hazards. In particular, we have examined the prediction that increased vertical coordination reduces transaction costs when asset specificity and performance measurement difficulties become substantial.

The empirical findings indicate that this governance performance pattern varies across interfirm trade in domestic and international relationships. In international buyer–seller relationships facing substantial asset specificity, increased vertical coordination reduces ex post transaction costs significantly. This performance pattern is absent in domestic buyer–seller relationships, in which the problems of performance evaluation and less surveyable trade conditions are expected to be of less concern. However, performance measurement difficulties might vary strongly in international trade and be contingent on the actual differences in culture, language, and institutional frames across the home countries of the trading parties. Accordingly, differences in performance measurement across national and foreign business relationships are expected to have significant interest only when the cultures and institutions of trade in the home countries of the trading parties are different in nontrivial respects. Our empirical setting of domestic, business-to-business relationships within Norway is surrounded by relatively surveyable trade conditions in which reputation effects might attenuate trading hazards to some degree. In contrast, in trading relationships with firms within the Common Market, firms from nonmember countries such as Norway should face substantial changes in institutional frames, business practice, and availability of market information, which should enforce problems associated with performance evaluation and information asymmetry.

Several empirical studies have examined the association between performance measurement problems and governance structure in business-to-business relationships. Anderson (1985) demonstrates a positive association between performance evaluation problems and the use of in-house sales forces (hierarchical governance). Furthermore, Gatignon and Anderson (1988) provide evidence for a positive association between supplier performance evaluation difficulties and vertical integration. Finally, Heide and John (1990) give additional evidence for a positive relationship between performance measuring problems and supplier verification efforts. However, the association between performance measurement problems and governance performance is modestly examined in current interorganizational research, and further research about the antecedents to transaction cost is desirable to validate the TCA framework completely.

Managerial Implications

For the purpose of selecting efficient governance arrangements, an important managerial issue is to identify economic ties and prospective opportunism in buyer–seller relationships. The nature of bilateral dependence between the transacting parties is the most critical guideline for estimating the real costs and risks connected to interfirm business and detecting the need for specific governance arrangements. Alignment of comprehensive agreements, however, induces transaction costs on its own and should be restricted to situations in which it is advantageous and possible for trade partners to exercise opportunism. For the purchasing firm, for example, marketing intelligence conducted to examine and monitor the reputation and market conditions of both domestic and foreign suppliers might be appropriate for this purpose.

A buying firm employing substantial specific assets in a relationship may create offsetting effects by tying the supplier's trademark to the products entering the markets of end users so that several business actors can monitor the supplier's performance. In that situation, reputation effects would probably make some aspects of moral hazard less profitable.

The empirical findings of this research indicate that the validity of the standard TCA model might vary significantly across different research settings. A common system of legal regulations in a domestic buyer–seller relationship will have the potential to absorb risk and foster cooperation rather than disputes and conflicts. Similarly, a change in the institutional environment will induce shifts in the comparative costs of governance (Williamson 1991) as firms move from domestic to international trade partners. When trading partners are familiar with different institutional frames of business, this might induce higher costs of legal actions and make private ordering of business-to-business trade more advantageous. Accordingly, international contract law issues and other institutional factors establish an important frame for the organization of business-to-business trade in foreign trade.

Limitations and Further Research

Applications of the TCA framework have become common in foreign entry mode investigations (Anderson and Gatignon 1986; Gatignon and Anderson 1988). Most of the current studies in the international marketing field use the selling (exporting) firm as the unit of analysis. However, this may cause problems in separating the impact of performance evaluation problems from the effects of asset specificity, because these issues involve interfirm relationships and should be studied with business relationships as the unit of analysis (Aulakh and Kotabe 1997).

One limitation of our research involves the focus of unilateral employment of specific assets made by the purchasing firm. Mutual employment of specific assets is expected to have a strong effect on the commitment of both parties in business relationships. When both parties in a relationship employ specific investments, reciprocity is maintained by a hostage exposure (Williamson 1983), which should enforce compliance to the relationship and thereby attenuate opportunistic behavior and subsequent transaction costs. This research has not made a complete control for the possible effect of reciprocal investments, though the customization of the supplier's product incorporated in the research model to some degree reflects supplier-specific investments and thus makes some control of the effect of this variable.

One significant research issue is the context of the transaction. The environment of international trade, such as contract law, custody of trade, the financial system, business culture, and the role of the state in industry, may deviate from the domestic frame and thus make conditions of trade difficult to survey (Lane and Bachmann 1996). As previously argued, the lack of opportunities for disclosure of information and the options for strategic misrepresentation may be more evident in an international setting because of higher costs of monitoring international trade partners’ performance and of using international courts or other third-party appeal. To disentangle the effect of such trading difficulties, we have compared domestic and international buyer–seller relationships. It would be desirable to elaborate this analysis further—for example, by developing a continuous variable reflecting contextual differences between the seller's and the buyer's domestic markets (see O'Grady and Lane 1996).

Business-to-business relationships are embedded in a context that represents individual attitudes reflected in the atmosphere of the transactions and institutional factors (Williamson 1993). Both these factors might affect the governance performance of vertical coordination. A further examination of the interaction between contextual factors and the pattern of governance would improve the validity of research within the field of economics of organization. Research focusing on cross-cultural interfirm settings is desirable to explore this issue further.

Footnotes

Performance Measurement Difficulties in Domestic and International Channel Dyads: Findings from Pilot Study

| Performance Measurement Difficulties: Items (Seven-Point Likert Scale, Inaccurate Description/Accurate Description) | Domestic Channels (n = 14) Mean (S.D.) | International Channels (n = 11) Mean (S.D.) | Mean Difference (t-Value) | Homogeneity of Variance Cochran's C |

|---|---|---|---|---|

| Item 1: Our firm does not know the most significant cost figures of the products we buy from this supplier. | 2.84 (1.77) | 4.27 (1.95) | 1.33 (1.87) ** | .55 (p = .75) |

| Item 2: Our firm is not familiar with the production process of the products delivered by this supplier. | 2.46 (1.56) | 3.36 (1.50) | .90 (1.43) * | .52 (p = .90) |

| Item 3: Our firm has little knowledge about technological standards and components incorporated in the products we buy from this supplier. | 2.38 (1.44) | 3.46 (1.29) | 1.08 (1.89) ** | .56 (p = .71) |

| Performance measurement scale (α = .66) | 2.56 (1.25) | 3.70 (1.02) | 1.14 (2.40) ** | .60 (p = .49) |

p < .10 (one-tailed).

p < .05 (one-tailed).

Notes: S.D. = standard deviation.

Description of Items

| Scale | Sample of Items |

|---|---|

| ASPEC (asset specificity, reliability: α = .79) | |

| ASPEC1: Our firm has, to a great extent, invested in production equipment that has been adapted to the products we purchase from our supplier. | |

| ASPEC2: Our firm has committed a lot of time and resources to achieving insight and knowledge about technological standards and the effective utilization of the products delivered by this supplier. | |

| ASPEC3: Our firm has committed a lot of time and resources to developing an acceptable quality assurance at this supplier. | |

| ASPEC4: We have made comprehensive investments in special equipment and routines for product control of the deliveries from this supplier. | |

| ASPEC5: Our firm has committed a lot of time and resources to redesign our production in order to achieve higher efficiency in the further processing of products bought from this supplier. | |

| ASPEC6: Our firm has made significant investments in information technology dedicated to rationalize the cooperation with our supplier. | |

| COORD (vertical coordination, reliability: α = .74) | |

| COORD1: We are regularly in contact with this supplier regarding development and testing of new materials and components. | |

| COORD2: We cooperate closely with our supplier to improve products and services delivered to our firm. | |

| COORD3: Our firm and this supplier regularly exchange information about production costs figures. | |

| COORD4: Our firm cooperates closely with this supplier to improve the quality assurance processes in its company. | |

| COORD5: We regularly cooperate with this supplier in the selection of materials and components that are used in the products delivered to our firm. | |

| TRANSC (ex post transaction costs, reliability: α = .76) | |

| TRANSC1: Our firm uses too much time and resources to control the products and production processes of this supplier. | |

| TRANSC2: The coordination of the relationship with this supplier is too costly compared with the resulting outcomes of these interactions. | |

| TRANSC3: It is very difficult to get necessary verification of production performance and production costs data from this supplier. | |

| TRANSC4: It is easy to settle agreements with this supplier about specification of products and services delivered to our firm. (reverse-scaled) | |

| TRANSC5: It is very time consuming and difficult to accomplish negotiations between our firms about price and payment terms. | |

| CUST (customization of the supplier's product, single-item construct) | The products delivered by this supplier are copletely tailored to the specific requirements of our firm. |