Abstract

Recent export studies have focused on the internal/controllable determinants of export performance. The external/uncontrollable determinants of export performance have received scant research attention. In this study, the authors examine two key external/uncontrollable factors, namely, industry concentration and firm location, in the context of Chinese manufacturing firms. In addition, the authors include several frequently studied factors such as firm size, capital intensity, technology innovation, and industry in the analysis as covariates. On the basis of logistical regression and multiple regression analysis, the authors find that both domestic market concentration and firm location are potent predictors of Chinese firms’ export propensity and export intensity. The authors discuss implications of the findings to expose the reason behind the success of Chinese exporters in international markets.

Exporting represents a viable strategic option for firms to internationalize and has remained the most frequently used foreign market entry mode chosen by companies. This has caused the research interest in the determinants of export performance to remain strong over the past two decades (Zou and Stan 1998). Although significant progress has been made in understanding the effect of a firm's internal controllable factors on export performance (Cavusgil and Nevin 1981), knowledge regarding the external uncontrollable determinants of export performance is limited and warrants further research (Zou and Stan 1998). In particular, the relationships of export performance with domestic industry concentration and the location of firms have gone largely unattended by researchers. As a consequence, the knowledge of the determinants of export performance remains incomplete.

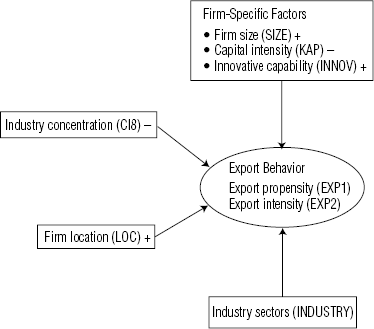

While embracing the general model that export behavior is driven by external and internal factors, we focus our analysis specifically on the effects of two external factors, namely, industry concentration and location of the firm. This research is aimed at complementing previous studies on the determinants of export behaviors by shedding some light on the relevance of external determinants of export performance. The specific objective of this study is to examine empirically the influence of industry concentration and firm location, in addition to several frequently analyzed determinants, on the firm's exporting propensity and intensity, using a data set of 1049 manufacturing firms across 37 industrial sectors in China.

This analysis reflects Chinese firms’ exporting experience. Understanding the export behavior of Chinese firms contributes to the current body of export literature in several ways. First, the Chinese economy has been transformed from a centrally planned system to a socialist market system in which the private sector and public sector coexist. The unique market environment in China is an ideal context for this study because the industry structure varies significantly from one industry to another. In some Chinese industries, competition is fragmented and intense, with large numbers of small and medium-sized firms. In other industries, a few large state-owned firms dominate the market.

Second, China has evolved into one of the major trading economies. Ranked eleventh in the world, the value of China's exports has increased dramatically from U.S. $18.1 billion in 1980 to more than U.S. $250 billion in 2000 (Statistical Bureau of China 2001). An empirical examination of factors that have contributed to the fast growth of exports by Chinese firms would enrich the export-based literature. In addition, the findings could offer international firms practical insights to the business operating background and the nature of the Chinese competitors. This knowledge could be used by foreign firms operating in China.

Third, given the lack of empirical studies that have investigated the effect of industry concentration on export behavior and the inconclusive findings (Schmalensee 1987), a study of the effect of industry concentration on the export activities of a large developing country could make a significant contribution to the literature. A review of the export performance literature shows that, except for a limited number of studies, the majority of previous studies have been conducted in the context of developed economies (Leonidou 1998).

This article is organized as follows: In the section that follows, we briefly review the relevant literature. Next, we develop the research hypotheses with regard to the relationship of two major dimensions of export behavior with industry concentration and firm location, along with other control variables (Calof 1994). Then, we describe the data and method employed in this study. Finally, we present and discuss the results and their implications.

Overview of the Literature

Research on the determinants of export performance has proliferated in the past two decades. More than 100 empirical studies have been published on the topic (for reviews, see Aaby and Slater 1989; Zou and Stan 1998). The early literature focuses on identifying factors that are linked to export performance. Among the factors that have been identified are firm characteristics, management characteristics, product characteristics, export market characteristics, and export marketing policy/strategy. Although the previous studies contribute to the understanding of success factors of exporting, they lack a sound theoretical basis and treat all factors indiscriminately (Cavusgil and Zou 1994).

More recently, significant progress has been made in developing a more comprehensive theory and increasing knowledge of the export performance of firms. For example, on the basis of industrial organization theory, Cavusgil and Zou (1994) develop a theoretical framework of export marketing strategy and performance that, for the first time, focuses on the dynamic role of export marketing strategy in determining export performance. In their recent review of the empirical export studies, Zou and Stan (1998) use a 2 × 2 framework to organize the determinants of export performance. Specifically, they argue that the determinants of export performance should be classified into internal versus external factors and controllable versus uncontrollable factors. After reviewing and synthesizing the empirical export literature from 1987 to 1997, Zou and Stan (1998) conclude that, among other things, the external/uncontrollable factors have received the least research attention in the past. To advance the knowledge of the determinants of export performance, they suggest, there is an urgent need for studies to investigate the external/uncontrollable determinants of export performance. Moreover, they suggest that future studies need to extend to developing countries and to use multivariate analyses that incorporate key covariates.

Two key external, and arguably uncontrollable, factors that potentially determine export performance are industry concentration and firm location. Although the impact of industry concentration on firm performance has long been a part of industrial analysis, it has received little attention as a factor in the theory of export marketing. The study of the relationship between export behavior and industry concentration is primarily the result of an increasing convergence of international trade and industrial organization theories. Recognizing the existence of various types of imperfect competition, researchers from the two disciplines have attempted to integrate the analysis of exporting with the analysis of industry concentration (Das 1982). One of the early theoretical studies linking trade and industry concentration proposes a useful theoretical framework to analyze the relationship between the domestic market structure and export/import (White 1974). Although these theoretical works have laid a foundation for studying the effect of domestic market structure on trade, little empirical work has linked industry concentration to export behavior.

In contrast to the industrial organization theory that emphasizes the importance of industry characteristics, the location theory places emphasis on firm location as an important variable in explaining a firm's export behavior. However, empirical analysis of the relationship between firm location and exporting is scarce in the literature. A recent comprehensive review of 70 empirical studies on the determinants of export behavior identifies only six studies that have attempted to relate location to export behavior (Leonidou 1998). Of these, two studies specifically examine the effects of firm location on export propensity but find no significant association. Nevertheless, on the basis of an analysis of 1446 European firms, Glejser, Jacquemin, and Petit (1980) find that location characteristics are related to export performance. Companies located close to transportation centers are more prone to export than those located in other areas.

To enrich the knowledge of the export behavior of firms, we investigate the effect of industry concentration and firm location on Chinese firms’ export propensity and intensity. In addition, we include several frequently analyzed covariates, such as firm size, capital intensity, innovativeness, and industry effects, in the analysis. In the following section, we develop hypotheses related to domestic industry concentration, firm location, and the covariates.

Research Hypotheses

In this study, we consider the export behavior of firms to be composed of two discrete decisions: whether to export (export propensity) and, if a decision is made to export, what proportion of production output to export (export intensity). The decision to commence exporting is an important commitment for firms with a domestic focus and is an important step toward internationalization (Cavugsil 1984). Firms that successfully generate revenues from exporting are in a better position to earn higher profits and enjoy the advantage of reinvesting the export-generated profits to enhance their competitive positions in the domestic market.

Extensive studies have been undertaken to examine the determinants of the export behavior of firms, as discussed in the previous section. For the purpose of this study, we focus on the two least investigated external factors, industry concentration and firm location, controlling other firm-specific variables in the analysis. Building on Zou and Stan's (1998) organizing framework, we outline the research hypotheses developed in this study in the framework given in Figure 1.

Summary of Hypothesized Relationships of Export Behavior with Industry Concentration and Firm Location

Export and Industry Concentration

The notion of industry concentration refers to the extent to which a few large firms dominate sales of a given industry. It represents an important characteristic of the nature of competition in an industry. A highly concentrated industry connotes the presence of high market power enjoyed by only a handful of firms with a large percentage of market share and the ability to exercise price discrimination.

The relationship between domestic industry concentration and firms’ export behavior is complicated. Various arguments support either a positive or a negative relationship on the basis of the industrial organization theory. First, a concentrated domestic industry may create a captive domestic market for the few dominant firms in the industry such that the firms may have little pressure to explore export market opportunities. Second, export markets are generally perceived as more risky than the domestic market. Oligopolists are in a better position to bear the risks than smaller competitive firms are. Therefore, the dominant firms in a concentrated industry may be more able to absorb risks associated with exporting.

Third, to export successfully to worldwide markets, firms need to develop a repertoire of nonprice competitive assets, such as extensive marketing networks, workforce skills, and the ability to provide credits to buyers (Nolle 1991). The dominant firms in concentrated industries generally possess more of such nonprice competitive assets and thus are more suitable to exporting. Therefore, “a country will export the product of its relatively more concentrated sector” (Das 1982, p. 691).

Empirical evidence about the relationship between industry concentration and export behavior is also mixed. Some studies have found that a few dominant firms in an industry possess the ability to sell abroad, and therefore industry concentration has a positive effect on both import and export share (Geroski 1982; Glejser, Jacquemin, and Petit 1980). However, other studies suggest an inverse relationship between domestic market structure and exporting, arguing that, insofar as seller concentration denotes monopoly power, dominant firms in a sector can exploit the negatively sloped demand curve and avoid the necessity of exporting (Koo and Martin 1984).

In the absence of consistent arguments and conclusive findings in this area of research, we examine the unique market environment in China to determine which arguments are more likely to be valid in the Chinese context. In the past, Chinese industries were protected by the government through high tariff and nontariff barriers. Although China has initiated ambitious economic reforms during the past two decades, many inefficient state-owned enterprises still remain that rely heavily on government subsidies and protection to survive the increasing competition in China (Chao and Chou 2001). The result of government intervention is that Chinese state-owned enterprises face little pressure to become innovative, efficient, and risk-taking. Compared with Western competitors, therefore, many Chinese state-owned enterprises are more risk averse in export markets, possess limited skills to be successful in export markets, and have little pressure to export. Therefore, we contend that, in the Chinese context, firms tend to exhibit low export propensity and intensity. The preceding reasoning leads us to propose the following about the relationships between export behavior and industry concentration:

The export propensity of Chinese manufacturing firms is inversely associated with the industry concentration.

The export intensity of Chinese exporters is inversely associated with the industry concentration.

Export and Location Effects

Early studies of the export behavior of firms found that the geographic proximity of firms to transportation centers facilitates the export development and the performance of firms because of cost effectiveness (Wiedersheim-Paul, Olson, and Welch 1978). Given China's vast land mass and varying degrees of economic and infrastructure development, it is conceivable that the location of Chinese firms also has a bearing on the export behavior of firms. Although the export behavior of a firm can be understood basically in terms of the firm's internal factors, such as marketing skills and production and technology capabilities, the location of the firm tends to play a significant role when the domestic economy of the firm is less advanced.

In China, significant geographic variations and wide discrepancies in infrastructure and economic development exist between coastal areas and inland provinces. Because of government policy, coastal areas raced forward in the past two decades to develop the infrastructure and the economy. Today, the Chinese coastal areas are much more advanced than the inland areas in terms of economic output and availability of modern infrastructure. Not only do the coastal areas afford firms the advantage in economical transportation costs, but they also are at the center of the economic growth, having large pools of skilled labor that contribute to high product quality. Therefore, Chinese firms in the coastal areas should be able to sell their products more easily to the foreign markets than are the firms located in the inland provinces. Another reason for the linkage between firm location and export behavior is the exposure effect. Firms located near information centers or close to national borders are more likely to export because of greater exposure to various export stimuli. Finally, location matters because of the spillover from a geographic concentration of exporters. The cluster of exporters in a location manifests access to specialized transportation infrastructure, such as storage facilities, ports, or railroads, and to information on demand in foreign markets. These economic externalities certainly benefit the export activities of firms located in the area. Following this reasoning, we advance the following hypotheses:

The export propensity is higher for Chinese manufacturing firms located in the coastal areas than for firms located inland.

The export intensity is higher for Chinese exporters located in the coastal areas than for firms located inland.

Research Methodology

Data

We drew the data used in this analysis from three sources: China's Leading Companies (China Statistical Information and Consultancy Service Center and Hualin International Inc., USA 1994), China Statistical Yearbook on Science and Technology (State Science and Technology Commission 1992), and China Industrial Economic Statistical Yearbook (State Economic Planning Commission 1992). Company data were collected from China's Leading Companies. The publisher of China's Leading Companies collected the data through a national survey using the standard survey questionnaires of the State Statistical Bureau of China. The primary objective of the survey was to provide foreign investors and the public with basic information on major Chinese firms. The survey covered 3900 firms (1743 are in the manufacturing sector and 2157 are in service industries). There are no foreign-invested companies in the sample. Sixty-four firms had missing values and were excluded from the analysis. This leaves a total of 1649 manufacturing firms in our first-step analysis on export propensity. Of the 1649 sample firms, 999 firms reported exports. We used these in the second-step analysis on export intensity. We used a dummy variable, EXP1, to capture the two types of firms: exporting firms and nonexporting firms. In addition, we collected industry research and development (R&D) and sales data from China Statistical Yearbook on Science and Technology and China Industrial Economic Statistical Yearbook, respectively, to calculate the variables included in the current study. We believe that quality of data used in this study is good. Although they may not be as reliable as those collected in developed countries, studies of Chinese data collection by well-known statisticians conclude that data from China are “by and large honest” (Chow 1986, p. 193). Moreover, secondary data from these sources also have been widely used in strategic management and international business studies.

The Covariates

Examination of the relationships of export behavior with industry concentration and firm location is the focus of the present research. However, we do not mean to suggest that the nature of industry concentration and firm location solely determine the export behavior. To control the potential effects of other factors, we also include in the analysis three firm-specific factors and industry sectors as covariates (see Figure 1).

Firm size (SIZE) is one of the most widely analyzed factors pertaining to export performance (Calof 1994). Size is measured by the total sales of the firms. Although little consensus exists in the extant literature about the direction of the effect of firm size on export performance (Zou and Stan 1998), empirical studies document the significant impacts of firm size on exporting (Meredith and Maki 1992). Exporting is a costly and risky business activity. Smaller firms on their own may be at a disadvantage in collecting foreign marketing information, launching overseas sale-promotion campaigns, and adapting their products to foreign demands (Kau and Tan 1987).

Capital intensity (KAP) is another important covariate included in this study. It represents the capital input of production of a firm and has been found to be associated with exporting. We measure KAP by the depreciated stock value of fixed assets divided by the total number of employees.

Technology innovation (INNOV) is the third firm-specific covariate. It connotes technological activities, such as R&D undertaken by firms. Innovative ability enables a firm to improve existing products and develop new products and processes. It enables the firm to produce internationally competitive products and gives it at least a temporary monopoly on its production and sales. Previous studies reveal a positive relationship between export performance and technology factors (Gomez-Mejia 1988). We measure INNOV by a dummy variable that equals 1 for firms that undertake R&D activities and 0 for firms that undertake no R&D activities. Using this dummy as a measure is justified because the underlying ability to innovate depends greatly on R&D activities carried out and is widely conceived as a critical factor in exporting.

In addition, we control for the possible export variations associated with specific industries (INDUSTRY) by including an industry dummy variable in the statistical tests. The covariate INDUSTRY is a vector of ten dummy industry variables to control for the variances due to the potential differential effects of industry. Specifically, we consolidate firms into 11 related industrial groups according to their primary production activities. We then use a vector of ten dummy variables (1–10) to capture these industries. The statistical models and measurements of research variables are described subsequently.

Measurement of Research Variables and Method

Following Calof (1994), we define the export behavior of firms as consisting of two major dimensions: export propensity and export intensity. To test the hypotheses related to these two dimensions, we have chosen to divide the analysis into two steps. First, we examine the export propensity measured by a dichotomous variable using the logistic regression model. We assume that firms’ propensity to export occurs such that export decisions are derived in discrete steps from no exporting to committed exporting. The effects of industry concentration and firm location may systematically influence the process, along with other firm-specific covariates that are discussed in the previous section. Given this dichotomous nature of export propensity, logistic regression analysis that relates the likelihood of an export decision to industry concentration, firm location, and other observable factors suits the test at hand well. The logistic probability function takes the following basic form:

The measurements of the variables used in both logistic and multiple regression models are as follows:

EXP1 is a binary dependent variable taking a value of 1 if a firm exports and 0 otherwise.

EXP2 is a dependent variable representing the export intensity. This variable is reported in the data source as a firm's export value divided by its production output value. The production output value, a unique measure of output used by the Chinese government, measuring the total market value of products before they are introduced to market for sale is similar to sales (Statistical Bureau of China 2001). The data source reports no separate export values, and therefore we are unable to calculate export intensity by dividing export values by total sales. Because the measure of industry concentration is calculated on the basis of sales values (described subsequently), a strength of this definition is that it avoids the potential confounding effect associated with the customary measure of export intensity that uses sales as a denominator.

CI8 and LOC are the measures of industry concentration and firm location, respectively. Most of the previous studies operationalized industry concentration by using measures such as four- or eight-firm seller concentration or the entropy. These measures, which have their strengths and limitations,1 are commonly used to indicate the degree of competition. The industry concentration ratio is obtained from Ma (1991), who calculated the eight-firm concentration (CI8) index for 39 Chinese industries on the basis of data collected from the 500 largest Chinese firms in 1990 by the Chinese Economic Research Center (1995). The industries are classified according to the three-digit industrial classification system, as are our sampled firms. The higher the value of CI8, the more highly concentrated the industry is, with a small number of firms.

LOC is an index variable. Unlike in previous studies that have used dummy variables to indicate the location differentials (Zhao and Zhu 1998), in this study we constructed a composite index using the prime infrastructure data. The sample firms are located across 24 provinces and cities in China, ranging from most inland areas to coastal areas that include the special economic zones and open cities. A noticeable difference between the coastal areas and inland areas is the presence of an adequate communication infrastructure. Because the lack of an adequate infrastructure essentially hampers the exporting ability of firms, firms located in an area with easy access to infrastructure are more favorably positioned to conduct exporting than are those located in the areas with poor access to infrastructure. To capture the heterogeneous location characteristics, we constructed a location index defined as LOC = ∑3j=1(Rji/Ai/3) x Ti, where R refers to total freight volume, j connotes three modes of transportation (1 = road, 2 = railroad, 3 = waterway), i represents 24 locales, A is total square kilometers, and T is telephones per capita. The data used to construct this index are collected from The Urban Statistical Yearbook of China (Chinese Ministry of Urban and Rural Construction 1990).

Results

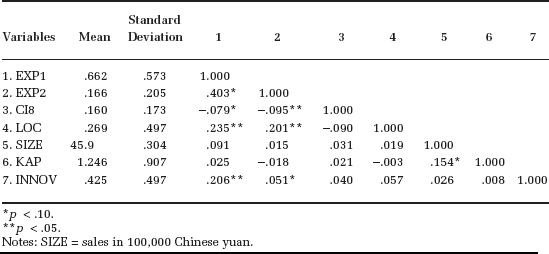

Table 1 presents the mean and standard deviation of the included variables and their correlations. As shown, with the exception of SIZE and KAP, which are moderately correlated, the variables showed no significant correlation. To test the severity of possible multicollinearity that might lead to inflated coefficients of independent variables, we also examined the variance inflation factors. The variance inflation factor tests indicate that these moderate correlations do not pose a serious problem in the model.

Descriptive Statistics

p < .10.

p < .05.

Notes: SIZE = sales in 100,000 Chinese yuan.

Table 2 reports the results of both logistic regression (Column 1) and multiple regression (Column 2) using the statistical procedures in SPSS (2000). The two models exhibit high explanatory powers. The logistic model shows that chi-square statistics and −2 log-likelihood statistics are significant at the p < .01 level. The model correctly classified approximately 74% of the sample firms into the export and nonexport categories. The multiple regression model explains approximately 52% of the variation in the export intensity of the sampled firms. The F-statistic is significant at the p < .01 level, indicating that the data fit the model well.

Results of Logistic and Multiple Regression Analyses

p < .10.

p < .05.

p < .01.

Judging by the levels of significance and the sign of the coefficients of CI8, we conclude that the statistical tests lend strong empirical support for H1 and H2. Specifically, CI8 is significantly associated with both dimensions of export behavior, export propensity (EXP1) and export intensity (EXP2), at the p < .01 level. As the sign of the coefficient of CI8 in the logistical regression model shows, the likelihood of Chinese firms to engage in export activity is significantly lower in a highly concentrated industry than in a less concentrated industry.

Similarly, the sign of the coefficient of CI8 in the multiple regression model suggests that firms in a highly concentrated industry also tend to have lower export intensity than do those in a less concentrated industry. This suggests that a handful of firms dominating an industry will likely stifle the export competitiveness of firms in that industry. The existence of these oligopolistic firms may substantially alter the circumstances of the remaining firms in the industry in ways that may cause their exporting to be less successful than under conditions of greater competition. In contrast, in a more fragmented industry, the absence of dominating firms enables more rigorous competition in the industry. The resulting high competition in the domestic market may lead to more efficient use of resources, which in turn may positively affect those firms’ competitive standing in export markets.

Variable LOC also appears to be an important factor in explaining the export propensity and export intensity of Chinese firms, in support of H3 and H4. The positive coefficients of LOC in the two models indicate that (1) firms located in coastal areas have higher odds of committing to exporting than do firms located inland (p < .01) and (2) exporters located in coastal areas have a higher export intensity than do those located in inland areas (p < .01).

Regarding the covariates included in the analysis, INNOV appears to be significantly associated with both EXP1 and EXP2 (p < .001 and p < .01, respectively), but it is inversely related to EXP2. This result may suggest that, though the export propensity of firms that undertake R&D activities is higher than that of firms that do not undertake R&D activities, exporters that undertake R&D activities do not export more intensely than those that do not undertake R&D activities. This finding appears to contradict some of the previous studies that find that firms’ R&D activities contribute positively to the export competitiveness of firms in international markets (Lee and Shim 1995). It casts a doubt on the generalizability of the R&D–export intensity linkage to the Chinese context. The negative influence of R&D could be plausibly interpreted as import-substitution practices used by Chinese manufacturing firms. Increases in R&D investment may be basically aimed at improving and upgrading the products for domestic market, because the Chinese manufacturers find that they are able to sell more successfully in the home market by substituting locally made products for costly imports. In adopting this import-substitute attitude, the Chinese firms may benefit from increased R&D by being able to compete on price against higher-priced imports. Therefore, it is likely that the effects of such R&D are not being passed to export sales but rather are limited to increases in domestic sales. Related to this import-substitution explanation is the nature of the competitive advantage of Chinese firms in the global market. Firms in developed countries compete in the technology-based product segments. They enhance their global competitiveness by offering technology-intensive and high value-added product lines. Thus, increases in R&D activities are likely to result in enhanced export intensity. Unlike these firms, the Chinese firms compete in the low-end product-markets. The competitive edge of the Chinese firms may still lie in the labor-intensive product segments in the global market. When R&D is more inward oriented, products for export sales are less likely to be affected.

The negative relationship between INNOV and EXP2 may also be attributed to two measurement issues. First, different types of R&D may have various impacts on export intensity. Product R&D that often embodies product alterations and adaptations can have a significant effect on product quality and export sales, whereas process R&D may not have a direct impact on export sales. However, our data set does not enable us to disaggregate R&D into different forms in order to analyze such effects further. Second, the failure of the R&D variable may indicate that export intensity is not as dependent on R&D spending as on whether prior research is successful. Measures of innovative output such as patents have been suggested as superior and found to be a significant key input in early work (Greenhalgh, Taylor, and Wilson 1994).

The results show that KAP is not a significant factor in explaining the export propensity (EXP1) of Chinese firms but exerts significant and negative impact on export intensity (EXP2). This finding suggests that increased capital intensity does not contribute positively to the export intensity of Chinese firms and supports the contention that export expansion by Chinese firms still, by and large, depends heavily on a comparative advantage in low-cost labor input (Zhao 1995). Moreover, SIZE turns out to be significantly and positively related to both dimensions of export behavior. This indicates that large firms are more likely than smaller firms to engage in exporting and achieve a higher export intensity. This is particularly true in the context of China. The government granted some large firms autonomy to export and even provided assistance through subsidies, but small and medium-sized firms have needed to depend on government trade corporations at the provincial level for exporting activities. Finally, the results for INDUSTRY point to the importance of including an industrial effect in explaining variations in export behavior. The results of the industry dummies provide insight into the export behavior of firms in different types of industries. Although 6 of 11 industries showed no significant relationships with export propensity (EXP1), 9 of 11 industries demonstrated significant linkages with export intensity (EXP2). One point worth noting is that the textile and apparel industry (IND3) is the only industry that is positively associated with both dimensions of the export behavior. This finding suggests that the exports from China were mainly from these industries in the 1980s, and it indirectly explains the negative impact of KAP on exporting.

Discussion

Knowledge of the determinants of export behavior has progressed after decades of research. However, there has been little research about the external/uncontrollable determinants of export performance (Zou and Stan 1998). In this study, the effects of two key external/uncontrollable factors (i.e., industry concentration and location of firm), in addition to some frequently studied internal factors, on export propensity and intensity are investigated in the context of Chinese manufacturing firms. On the basis of a large sample of Chinese firms, the current study has found support for the significance of industry concentration and firm location in determining export propensity and export intensity. Furthermore, we tested some existing findings in the literature regarding the effect of firms’ innovative activities, capital intensity, and size for their generalizability to the Chinese context. The study helps fill in the gaps in the export literature and contributes to the understanding of the determinants of export performance. Next, we discuss key findings of this study and their implications.

The evidence found in this study suggests that industry concentration exerts a negative influence on both export propensity and export intensity. This result runs counter to the customary contention that firms in highly concentrated markets are more likely to export and tend to export more than do firms in competitive industries. Instead, the findings suggest that when the market is dominated by a small number of firms, it may lead to complacency of home market position and reduce the desire to export. This is particularly true in the case of Chinese firms. Insofar as industry concentration means oligopolistic power, dominant Chinese firms are able to avoid the possibility of exporting by exploiting their favorable market positions in the home market. This finding may be unique to the Chinese case, because traditional state-owned enterprises dominate some key industries in China. Under government protection, these Chinese firms may develop a sense of complacency and have little incentive to expand through export sales. Nevertheless, the findings in this study indicate the significance of industry concentration in determining export propensity and intensity. Further research should assess the sign of the effect of industry concentration in other contexts.

Consistent with our expectation, firm location is found to be significantly related to both export propensity and export intensity. Firms in coastal areas not only may have the advantage in accessible port facilities that help reduce the cost of transportation but also may be more efficient and competitive for two other reasons. First, because the majority of foreign direct investment (FDI) in China is located in the coastal areas, it is conceivable that Chinese firms located in these areas enjoy a high symmetry of information through frequent interaction with foreign investors. Second, the availability of skilled labor and the high level of economic development in the coastal areas may afford firms the advantage of cost saving through high efficiency and productivity, which in turn makes their products more marketable in international markets. From a theoretical point of view, the result confirms the eclectic view that strategic locations enable firms to exploit advantages in marketing overseas.

The negative effect of R&D activities on Chinese firms’ export intensity implies that the marketability of Chinese products may not depend on differentiation and new product features to meet the foreign market needs. Instead, the sampled Chinese exporters may compete on the basis of low prices in foreign markets. However, this explanation could be confounded by the limited number of firms in China that carry out R&D activities and by the nature of Chinese firms’ R&D, which is different from that of companies in developed countries (Lu 1993). In any case, it should be interesting to investigate the nature of R&D activities performed by Chinese firms so that the relationship between R&D and Chinese firms’ export intensity can be better understood.

The statistical significance of capital intensity in determining Chinese firms’ export intensity may help expose the secret behind China's success in developing exports or export markets. Indeed, the finding that less capital-intensive Chinese firms export more may suggest that successful Chinese exporters rely heavily on the labor-intensive products to open export markets. As a developing country, China is known to have a comparative advantage in low labor cost. Therefore, it appears that Chinese firms are successful in leveraging this comparative advantage.

Given the Chinese government's unique treatment of large Chinese exporters (e.g., granting them export autonomy), it is of no surprise that large Chinese firms are found to have higher export intensity. Although the current findings about the effect of firm size are consistent with the argument that firm size is indicative of resource availability and marketing skills, they should be interpreted with caution because of existing government policies unique to China.

Managerial Implications

The findings of the current study offer several implications for foreign firms that are interested in sourcing products from China. First, because Chinese firms in concentrated industries have a lower propensity to export, foreign firms could gain some bargaining power if they target Chinese firms in less concentrated industries. Having a higher propensity to export, Chinese firms in competitive industries may be more willing to compromise in negotiations with foreign customers. Second, because the location of Chinese firms affects their propensity to export, foreign firms can benefit if they target Chinese firms located in coastal areas. Because the transportation and communication infrastructure in the coastal areas of China is more developed, foreign firms will have more options when approaching Chinese suppliers in the coastal areas. Chinese exporters located in the coastal areas are more likely to offer timely delivery and to be able to respond to changing international market conditions quickly. Third, because the export intensity is relatively high for Chinese firms in competitive industries located in coastal areas, Chinese exporters in competitive industries and in coastal areas are more likely to understand and be responsive to foreign customers’ needs. Therefore, foreign firms should be more satisfied when dealing with Chinese exporters in competitive industries located in coastal areas.

Limitations of Current Research and Suggestions for Further Research

The present research has two main limitations that readers should keep in mind when they interpret the findings. First, although it is important to investigate the export behavior of firms from a major developing country, the single-country context of the study may limit the generalizability of its findings. Second, the study is based on secondary data. As in all studies using secondary data, some factors must be measured as dummy variables, such as EXP2, INNOV, and LOC. Although these variables help shed light on Chinese firms’ export behavior, they may not be the best measures. For example, we could not further classify INNOV into product and process R&D to examine other research questions.

From a future research perspective, several new directions seem especially promising. First, generalizations of this study can be improved if further research can extend the model to multiple countries. Enlarging the sample size with data from multiple countries will not only increase the level of confidence in the statistical modeling but also enable researchers to conduct meaningful comparisons across countries with different economic systems and market conditions, because the key determinants of exporting activities vary across countries. Second, a more refined measure should be constructed to capture the multifaceted nature of location effects. Although the composite location index used in this study offers a better approximation than the simple dummy measures frequently used in the previous studies, future studies may improve this measure by adding concrete indicators such as varying transportation costs and rental costs in different locations to the index or by adopting primary data.

Third, another fruitful future research direction is to simultaneously include internal/controllable and external/uncontrollable factors in the analysis. Such comprehensive research has the potential to significantly advance the literature. To accomplish this, primary data must be collected in addition to external variables. Finally, a corollary of the current findings indicates that the export performance of host country firms would be better explained if some account of FDI-induced exporting and measures of host government strategic trade policy can be constructed. Integrating these two factors in future studies would be meaningful because the presence of FDI attracted to spatial stimuli (Woodward and Rolfe 1993) and to export promotion policies of host governments may positively influence the export performance of local firms. Inclusion of these factors in future studies should certainly help build a more robust model for a clearer understanding of the determinants of the export performance of local firms.

Footnotes

1.

Readers are referred to a detailed discussion of this issue in a study by Caves, Khalizadeh, and Porter (1975).