Abstract

As previously protected and emerging markets continue to open up for international trade, export firms often have a difficult time developing marketing strategies, particularly pricing strategies. However, few studies focus on the pricing practices of export firms, which makes it difficult to understand whether the same pricing strategies apply across markets, particularly in emerging markets. Using a framework of price complexity, the authors examine and compare the cost variables that are factored into price (price complexity) by export firms in the United States and Korea. The authors also investigate and compare some important noncost factors that influence pricing decisions for exporters in both their domestic and international markets. The results show that firms from the United States, a developed market, tend to factor more cost variables into price than do firms from an emerging market such as Korea. On the basis of the results of the study, the authors discuss implications for exporters and future research directions.

As previously protected and emerging markets continue to provide growth opportunities for exporters and multinational businesses, the development and implementation of marketing strategies, particularly pricing strategies, are critical managerial decisions for acceptance and success in new markets. East Asia, with more than three-fifths of the world's population, is an emerging market with tremendous potential for growth. Several countries, including South Korea (Korea), the People's Republic of China, and Taiwan have been identified by the U.S. Department of Commerce (2001a) as “big emerging markets” on the basis of the economic opportunities in the region. Because of the economic development, economic reforms, easier access, and the export drive policy for growth, many foreign companies are investing in, entering, and competing aggressively in previously protected markets such as Korea, the 8th largest trading partner with the United States and the 11th largest economy in the world. Korea is a heavily sought-after trade partner, and there is fierce competition among foreign companies that are trying to obtain a leadership position. However, it is described as one of the most difficult markets in the world for international trade, which makes pricing decisions even more arduous (Choe 1997; U.S. Department of Commerce 2001b; U.S. Department of State 2001).

Pricing in international markets is a complex decision because of the many influential variables that must be considered. Given the importance and problematic nature of international pricing decisions, it is ironic that price, the variable in the marketing mix that generates revenue and is easiest to manipulate, has received little attention.

The literature on international pricing tends to be general and conceptual in nature, focusing on issues such as pricing policies, processes, transfer pricing, cost-plus pricing, and factors that influence pricing decisions (Cateora and Graham 1999; Cavusgil 1988, 1996; Czinkota and Ronkainen 1996; Koh and Robicheaux 1988; Moustafa 1978; Myers 1997; Myers and Cavusgil 1996; Samiee 1987). Although factors influencing pricing decisions and the use of cost-plus strategies are discussed, little attention has focused on the specific costs that are factored into the pricing decisions of export firms. It is also unclear whether the same pricing decisions apply across all markets, particularly in emerging markets. The lack of literature on pricing in international markets, especially for emerging markets and exporters, may be due to the reluctance of managers to discuss pricing issues, the complexity and uncertainty of pricing decisions, the lack of a formal export pricing theory, and/or the idea that the process used for setting domestic prices can simply be applied to setting international prices. Although determining best pricing practices may be especially difficult, it is extremely important for exporters involved in international trade with emerging markets.

The purpose of this study is to examine the cost complexity and pricing decisions of export firms in the United States and Korea and investigate which factors are considered in determining firms’ pricing structures. We propose a framework to examine the factors that influence pricing decisions and the degree of complexity (from a cost perspective). Specifically, we investigate the cost complexity of pricing decisions and seek to determine what cost variables are factored into price for both U.S. and Korean firms and if these variables or prices change in domestic versus international markets. On the basis of the study's results, we discuss managerial implications, potential problems for exporters as well as multinational firms, and future research directions.

Background

Export pricing strategy has been identified as an important factor associated with export performance, profitability, and success (Bilkey 1982; Cateora and Graham 1999; Cavusgil 1988, 1996; Cavusgil and Zou 1994; Kirpalani and Macintosh 1980; Koh and Robicheaux 1988; Myers and Cavusgil 1996; Zou and Stan 1998). Although price has been identified as a key factor for success in international markets, the international pricing literature is sparse, and few studies use empirical data to support firms’ pricing decisions. Many of the studies focus primarily on multinational corporations (MNCs) or companies that have operations in more than one market rather than on firms that just export and do not have operations in different markets.

Myers and Cavusgil (1996) develop a conceptual framework that illustrates relationships of pricing strategies and decisions with export performance and that outlines the determinants of these two constructs. The proposed determinants of these two constructs are firm management; the product, including product costs; industry conditions; and export market conditions. The conceptualization illustrates that though the selection of some pricing strategies for international customers may be influenced by external factors such as government regulations and political issues, other pricing strategies are chosen by management, which has a proactive role. Under pricing strategies and decisions, Myers and Cavusgil (1996) discuss competitive posture, price-setting philosophy, the pricing process, and pricing practices. The competitive posture suggests the importance of price as a competitive tool, and Myers and Cavusgil note that firms emphasizing nonprice benefits might not view price as a competitive tool. This view may be based on the firm's international experience. The pricing philosophy includes objectives, drivers (costs, competition), full versus marginal costs, and centralization of decisions. Myers and Cavusgil note that a cost-centered pricing strategy is used by most exporting firms. The pricing process refers to how often pricing is reviewed and adjusted and the use of flexible versus rigid export pricing. The firm's pricing practices include the effect of channels of distribution on pricing, the choice of which currency to use in pricing, the decision whether to have uniform pricing for all markets, and the adaptation of the product to the individual market. Myers and Cavusgil conclude that characteristics of the international market must be taken into consideration when a firm develops export pricing strategies.

In another study, Cavusgil (1996) examines global pricing, the factors influencing international pricing, and the different options for export pricing, but he focuses on MNCs. Cavusgil notes that pricing in international markets is difficult because of the number of influential factors. He identifies the nature of the product or industry, the location of the production facility, the distribution system, the location and environment of the foreign market, and foreign currency differentials as the five most important factors influencing pricing for international markets. In a previous article, Cavusgil (1988) discusses six factors that influenced global pricing decisions. Although he includes the first four factors listed previously in the latter study, he does not mention management's attitudes and government regulations. However, Cavusgil (1996) notes that for international customers, MNCs also need to consider duties and external costs such as documentation, insurance, and freight in addition to production costs, demand, and competition.

In one study of exporters from an emerging market, Raymond, Kim, and Shao (2001) examine factors influencing international strategies and the difficulty of various strategic decisions. The findings show that exporters from emerging markets have difficulty setting price, estimating fixed and variable costs, and adjusting to exchange rate fluctuations. Forman and Lancioni (1999) identify the variables of concern for international pricing managers as currency fluctuations, government interventions, tariffs on international prices, and inflation in the foreign country; they believe the last is the most influential factor. The authors state that many pricing managers use the same pricing processes in both domestic and international markets but that cost-plus pricing is too simplistic for foreign markets. They point out that transfer pricing, second-market pricing, countertrade, and standardized versus adaptive pricing are strategies only for international markets (Forman and Lancioni 1999), but they do not link the strategies to the variables of concern for pricing in international markets.

In addition to identifying factors that influence international pricing decisions, Cavusgil (1988, 1996) notes that companies tend to use one of three pricing approaches for exports: rigid cost-plus pricing, flexible cost-plus pricing, or dynamic incremental pricing. However, he does not discuss the specific cost components of these three approaches. Czinkota and Ronkainen (1996) discuss three comparable pricing strategies for export markets: the cost-plus method, the marginal-cost method, and market-differentiated pricing. Rigid cost-plus pricing involves adding a gross margin and international customer costs to domestic manufacturing costs. Profit margins for the intermediaries, overhead costs, transportation, and customs charges are also included, which often makes the final price too high to be competitive in most markets. Flexible cost-plus pricing, or the marginal-cost method, is similar except that price variations, such as discounts for large orders, are allowed under certain circumstances. Both of the cost-plus pricing approaches focus on maintaining profit margins and are considered to be static because price cannot be changed in any significant manner (Cavusgil 1996).

Dynamic incremental pricing assumes that fixed costs are always incurred. Only part of the overhead is added to the price, and firms only try to recover international customer costs and variable costs in export prices, which enables the company to be more competitive. However, companies that use dynamic incremental pricing do so only in certain situations (Cavusgil 1996). The dynamic incremental pricing approach is similar to market-differentiated pricing (Czinkota and Ronkainen 1996) and to what Moustafa (1978) describes as a direct-cost approach.

Because many firms in developing markets lack experience and often have higher costs, Moustafa (1978) states that the direct-cost (contribution margin) method appears to be more practical than the full-cost method of pricing. In the direct-cost method, the maximum price is a function of competition, not cost, and the minimum price is determined by the total variable costs. Specific variable cost dimensions are not examined; however, Moustafa finds that various versions of the full-cost method, in which a markup covering a share of the overhead costs is added to the manufacturer's product cost, are the most commonly used methods among exporters in developing nations. The reason for the acceptance of the full-cost method in developing nations is its simplicity and its tendency to provide stable and safe prices. Kublin (1990) finds that cost-plus pricing approaches are the most popular for pricing environments that are ambiguous, though cost-plus pricing is actually very complex.

The cost-based approach to pricing, which Moustafa (1978) states that firms in developing markets use, appears to be different from a market-based strategy used by firms that emphasize nonprice elements of the marketing mix as the selling points of a competitive strategy. Samiee (1987) examines the role of pricing in U.S. and foreign-based firms that operate in the United States and finds that U.S. firms emphasize price to a much greater extent than foreign-based firms do. Almost two-thirds of the 104 U.S. firms and only half of the 88 foreign firms Samiee studies rank price as one of the top three marketing decisions. Foreign firms tend to focus on nonprice elements of marketing to obtain a competitive advantage, whereas U.S. firms tend to focus on price as a selling point (Samiee 1987). In his study of British industrial exporters, Piercy (1981) finds that a market-based pricing approach rather than a cost-based pricing strategy is used by almost two-thirds of industrial exporters. Kublin (1990), however, finds that U.S. firms have recently focused more attention on pricing, though exporters are slow to use price as a competitive tool. Myers (1997) explores pricing policies of eight U.S. exporters and eight Mexican exporters of manufactured goods and finds that some firms use cost-plus pricing, some use competitive-based approaches, and others have no observable pricing process. Most of the managers believe that they do not have enough control over price and that a preset cost-oriented pricing model is emphasized.

Although cost-plus pricing appears to be a simple, useful pricing procedure with a “target” return, it may not lead to desired financial performance (Nagle and Holden 1995).

Cost-plus pricing may lead to pricing too high in weak markets and pricing too low in strong markets, not reflecting market conditions and therefore causing problems for sellers and exporters. Therefore, the number of cost variables factored into price (the cost complexity) is a critical issue in both domestic and international markets.

In summary, pricing has been found to be an important element in determining financial and export performance. How prices are determined has been observed to differ between firms from developed versus emerging countries. Given that countries in the two stages of economic development appear to use and emphasize different pricing strategies, it is important to understand the basis and cost complexity of pricing decisions.

The United States, a world leader in most areas of business and industry, is an industrialized, developed market, whereas Korea is a rapidly emerging market with many opportunities for trade with other markets. Several of the biggest emerging markets, and therefore many opportunities in the world, are in East Asia. However, as emerging and previously protected markets open up to international trade, export firms often have a difficult time developing marketing strategies, particularly pricing strategies. Underlying government regulations, cultural and social values, economic issues, and strong relationships, as well as other environmental factors, affect the difficulty of business operations in emerging markets such as Korea.

Pricing strategies often influence Koreans’ perceptions of foreign products and play a critical role in the poor brand image of many Korean products. Korean exporters have experienced major obstacles that may affect their pricing decisions and international trade activities. These include problems dealing with exchange rate fluctuations, foreign marketing activities, inactive new product development departments, weak marketing research skills, ineffective advertising, passive distribution channel management, and poor after-sales service (Korea Economic Daily 1995a, b; Maeil Business Newspaper 1995).

Pricing in international markets is a complex decision because of the number of factors influencing pricing decisions (Cavusgil 1988, 1996). Although many factors influence pricing as well as other strategic decisions, they are not all cost variables. Among the many critical and complex issues that remain to be explored in both domestic and international markets are the specific cost variables factored into price, or the cost complexity of pricing decisions.

A Framework for Pricing Complexity

As Cavusgil (1988, 1996) notes, pricing is a complex process because of the number of influential variables, and it is generally subjective in domestic markets. He conjectures that pricing is even more difficult in international markets because of multiple currencies, trade barriers, additional cost considerations, and longer distribution channels. Raymond, Kim, and Shao (2001) examine factors that influence strategic marketing decisions in international markets and note the difficulty that exporters from emerging markets have in setting price, estimating fixed and variable costs, and adjusting to exchange rates. Myers and Cavusgil (1996) develop a conceptual framework that can perhaps be described as strategic in nature, in that it identifies the factors that influence the choice of a pricing strategy and performance in international markets. Similarly, other studies point out various factors that are or should be considered in international pricing.

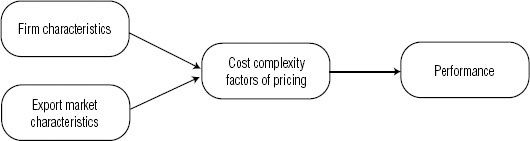

Although research has shown that many factors influence pricing decisions in international markets, understanding the cost complexity of the pricing decision and determining whether firms factor in different variables for domestic and international prices is important. As such, we develop a framework that describes pricing activities. Thus, we examine pricing decisions by understanding first the practice of pricing in terms of the complexity of the pricing decision. The complexity of pricing involves determining the number of cost variables that are factored into price. This requires examining factors that influence pricing decisions, including firm characteristics (and objectives) and export market characteristics, as well as examining specific cost variables. By determining the cost complexity of pricing decisions, firms have a better understanding of strategies, including the use of competitive (market-based) or cost-based strategies.

Consider a continuum that ranges from purely market-based pricing to cost-plus pricing. Market-based pricing requires understanding a firm's relative value in comparison with competitive offerings and pricing accordingly. For cost-plus pricing, a firm must add all costs together, which requires an effective cost-allocation process for fixed costs, and then add a desired margin to arrive at the final price. Reality is often somewhere in between, with a floor (bottom line) that is the price set to break even (cover cost of goods sold [COGS]) and a ceiling that represents the maximum price or the market's perception of the product's value. Furthermore, as the implications are considered more fully, it is clear that not one but two separate dimensions can operate. For example, in a truly one-dimensional decision, the more the various cost elements are considered in creating price, the more a cost-plus pricing system is used; the less the various cost elements are considered, the more a market-based pricing system is used.

The argument, though, can be raised that the use of more or fewer cost elements in pricing does not determine the number or influence of the market elements used in pricing. Nor does a single-dimension approach recognize the use of market pricing to determine product design and other practices that are also influenced by costing practices. Thus, two dimensions are present—each representing the degree to which elements, both cost and market, are used in determining price.

This study and the framework we present focus strictly on the cost dimension. Using the previous literature on export pricing, we propose a framework that shows internal (firm characteristics) and external (export market characteristics) factors that may influence pricing strategy, costs that are factored into price, and the degree of complexity (from a cost perspective) involved. We examine some of the same factors identified by Cavusgil (1988, 1996) and conceptualized in Myers and Cavusgil's (1996) framework, which we adapt to reflect the notion of cost-based pricing complexity. Myers and Cavusgil include government regulations and political issues under both industry and export market characteristics, though these factors are often addressed in the literature in discussions of tariffs and taxes. These tariffs and taxes are cost components that vary because of export market conditions. Therefore, these are part of the pricing complexity index we employ to determine the degree to which cost-plus pricing is used. However, foreign exchange fluctuations, which may influence pricing decisions, affect entry and exit into a market as well as transfer pricing, and the currency used for payment (Cavusgil 1988, 1996; Czinkota and Ronkainen 1996; Forman and Lancioni 1999) are not necessarily cost components that are factored into pricing complexity. Therefore, as illustrated in Figure 1, two factors, firm characteristics and export market characteristics, are proposed to influence pricing complexity. The cost complexity factors of pricing include costs that exporters factor into domestic and international prices.

Framework for Pricing Complexity

First, though, one critical assumption must be discussed to fully understand the proposed relationships. That assumption is that pricing complexity differs for export markets compared with domestic markets. That is, because of several uncontrollable factors, different considerations may be made. Therefore, our first research question is whether there is a difference in pricing complexity between domestic and export markets. We expect greater complexity in export pricing in part because there are more elements in determining cost. Transportation costs, for example, may include more or different modes of transportation. Tariffs are not present when domestic prices are calculated. Firms may change other elements, such as packaging, to export the product, so export pricing may require greater complexity than domestic pricing.

Research Question 1: Is export pricing more complex than domestic pricing?

Supposing that the first relationship holds, there may still be differences in pricing complexity because of the stage of economic development and related firm characteristics. Given the trade opportunities with emerging markets such as Korea, one of these characteristics could be the status of the home country, whether developed or emerging. Companies in developed countries may have more advanced costing systems and therefore may be more likely to use more cost elements. Therefore, in the context of this study's comparison of U.S. and Korean firms, we ask the following:

Research Question 2: Will U.S. firms exhibit greater pricing complexity than Korean firms?

Other firm characteristics include size, export experience, export intensity, export motives, and other such characteristics. Although we can make a case that greater size or experience should enable greater use of cost components and has an effect on performance, this study focuses on the cost dimension rather than performance. Therefore, we simply ask the following:

Research Question 3: Do firm characteristics, such as size and export experience, influence pricing complexity?

Finally, we consider the impact of export market characteristics, including political regulations, which have been discussed as influential factors in several studies (Cavusgil 1988, 1996; Myers and Cavusgil 1996). Although much can be made of factors such as climate and other differences that can influence product design, packaging, and other cost elements (e.g. Cavusgil 1996), we consider instead a broader range of issues and do so from the perspective of the ease with which firms can adapt. Thus, we examine cultural differences, economic conditions, political and legal issues in terms of how difficult it is to adapt to local conditions, rather than the actual differences in market conditions that may exist. As such, we consider influential factors such as adjusting to exchange rates.

Research Question 4: Does the degree of difficulty in adapting to local conditions influence the complexity of pricing?

Research Design

By means of a two-dimensional framework and a complexity index, the current study examines factors used in making pricing decisions for both U.S. and Korean exporters and focuses on the cost complexity of pricing decisions. We investigate research questions related to the dimensions and differences firms use in pricing in both international and domestic markets by surveying small and medium-sized exporters based in the United States and Korea. We discuss the sample, survey instrument, and preliminary data analysis and then provide the results of the study, a discussion of implications, future research directions, and the conclusion.

Sample and Response Rate

To determine pricing complexity and compare cost factors used in pricing decisions, we use the size of a firm as a sample parameter. To compare the cost variables of export firms in both the United States and Korea, we used two sources for the sampling frame. Controlling for company size and type, we obtained a random list of 557 U.S. exporters, ranging in sales from $500,000 to $100 million, from the Kentucky World Trade Center. The exporting companies selected were primarily single-line consumer goods companies. After confirming that the companies exported, met the sampling parameters, and were still in business, we used 406 companies in the study. Ninety-five export marketing managers responded, for a response rate of 23.4%.

Using the same parameters, we obtained the sampling frame of Korean exporters from the Directory of International Trading Companies published by the Korea International Trade Association (1994). We randomly selected 350 companies and contacted them to ask if they would be willing to participate in the study. One company was no longer exporting, which made the effective sample 349. A total of 74 export marketing managers completed the survey, for a response rate of 21.2%.

Nonresponse bias was examined by an early versus late response comparison. No differences were identified in early versus late responders. The mean annual sales for the Korean firms were $23.6 million, whereas the mean annual sales for the U.S. firms were $21.7 million (z = .26, p = .794); the majority of companies in both countries experienced sales of less than $50 million. The mean number of employees for each country was also comparable: 205 in Korea and 178 in the United States (z = .57, p = .568).

Survey Instrument

We developed a structured questionnaire using the literature on pricing and other international literature. To establish translation equivalence, we translated the original questionnaire that was administered in the United States into Korean and then back-translated it into English to ensure that comparable data were obtained in each market (Mullen 1995). We divided the questionnaire into sections to identify cost variables in domestic and international markets and differences in pricing that may exist in domestic versus international markets. Respondents were asked whether they had difficulty with other factors that may influence pricing decisions. We obtained classification data from each respondent to ensure that each firm met the sample parameters and determine if pricing complexity varied depending on firm characteristics.

Analysis of Data

Because this study involves an international data set, it is important to determine whether the differences are real and if the results are expected (Mullen 1995). Initially, we performed factor analysis to ensure that factor structures were comparable across cultures and provide support for previous research. Because factor analysis identifies underlying dimensions and reduces the set of variables into smaller sets of composite variables, it is useful in simplifying the data. The factor analysis was first run separately on exporters from the United States and Korea. The data were aggregated and the factor analysis was done on the entire data set, because the underlying structures were found to be the same for exporters in both countries. The items loaded on the factors as expected, the reliability scores (using Cronbach's alpha) were in the acceptable range, and the results were expected, showing equivalence (Mullen 1995).

The results of the factor analysis provided some of the independent variables that were used in the regression analysis to explain complexity. In addition to regression analysis, chi-square tests were used. Z-tests were used to test the significance of the difference in pricing complexity between domestic and international pricing and between the United States and Korea.

Results

Tables 1 and 2 present the results of chi-square comparisons for cost factors used in setting domestic and international prices. Overall, U.S. firms tend to factor different cost components into both domestic and international prices to a larger extent. Although the picture may be somewhat distorted because COGS should be considered at least as a floor factor in setting price, many firms, especially those from emerging markets such as Korea, may be more interested in establishing competitive position. In addition, these subjects may have considered such an element so basic that it did not warrant separate identification. An alternative explanation is that market conditions make COGS irrelevant. Another possible explanation is that firms from cultures high in collectivism, such as those in East Asia, may set prices at least above COGS as part of informal collaborative trade agreements. Yet if that were the case, cost factors in general would be irrelevant, and there are very few markets with that luxury.

Cost Components Factored into Domestic Prices

Percentage of firms that factor the cost component into their domestic prices.

Adjusted for continuity correction.

Cost Components Factored into International Prices

Percentage of firms that factor the cost component into their international prices.

Adjusted for continuity correction.

Research Question 1 asked whether export pricing is more complex than domestic pricing. Firms in the United States tend to factor fewer components into export pricing than domestic pricing, whereas Korean firms seem to consider only added transportation costs into export pricing (Tables 1 and 2). Therefore, with the exception of costs that are directly affected by exporting (e.g., transit insurance), fewer costs are considered when determining export price. What this suggests is that firms should use domestic price as a guide and then add the incremental costs of exporting.

To examine further the complexity of export pricing compared with domestic pricing and determine whether there is a significant difference in pricing in export and domestic markets, we conducted a test of means. The results indicated that there are no significant differences in the complexity of pricing in export and domestic markets for either U.S. or Korean firms. The cost components may be different, as indicated in Tables 1 and 2, and the number of variables influencing pricing decisions may be greater for international pricing, making it a complex decision (Cavusgil 1988, 1996), but the cost complexity is not significantly different.

Research Question 2 considered whether U.S. firms use more cost components than Korean firms. An examination of means indicates that there is a significant difference in the number of cost components used by U.S. and Korean firms. When comparing U.S. and Korean firms with regard to their domestic pricing, the z-value is 2.71, indicating a significant difference at the .01 level. Similarly, when comparing the cost factors that U.S. and Korean firms factor into their international prices, the z-value is 2.95, also indicating a significant difference at the .01 level. When we examine the specific components, we find that U.S. firms tend to factor in advertising, commissions, transportation costs, and net profits to a greater extent into domestic prices. Korean firms take value-added taxes and specific duties into account more when setting domestic prices. When setting international prices, U.S. firms are more likely to factor in administrative overhead and fixed plant costs, whereas Korean firms do not factor any particular costs into international prices at a greater rate than U.S. firms.

To examine pricing complexity differences further, in Tables 3 and 4 we compare firms on the basis of setting an international price lower than, equal to, or greater than the domestic price by country of origin. In general, companies that charge more internationally do so because of transportation costs—they appear to use a cost-plus model of setting price. For example, 83% of U.S. firms and 70% of Korean firms setting a higher price report that transportation costs are used to set price; 69% and 55%, respectively, cite transit insurance; and 54% and 55%, respectively, cite packaging. These frequencies are significantly greater than for firms whose prices are equal to or less than domestic prices. Korean firms also consider marketing costs such as rebates and allowances, promotional materials, and marketing research more frequently. Thus, the findings pertaining to the first two research questions are not as clear when we consider whether the export price is higher, the same, or lower than domestic prices.

Comparison of the International Price with the Domestic Price

Notes: χ2 = 31.78, p = .000.

Comparison of International Cost Factors with Their Domestic Counterparts

Notes: LT = less than the domestic cost, EQ = equal to the domestic cost, GT = greater than the domestic cost.

Firm characteristics and their influence on pricing complexity were the focus of Research Question 3, and export market characteristics were the focus of Research Question 4 (see Figure 1). To examine whether other factors that are influential in pricing decisions are also influential in pricing complexity, we regressed different variables against pricing complexity. Specifically, the independent variables included various firm characteristics and export motives, such as productivity and growth, the difficulty of adapting to export marketing conditions, and price and nonprice considerations (Raymond, Kim, and Shao 2001). Adjusting to exchange rates and estimating fixed and variable costs are considered under a variable called marketing costs accounting. For a list of the independent variables regressed against the dependent variable, complexity, see the Appendix. In Table 5 we present results for the entire sample.

Regression Analysis for the Determinants of Pricing Complexity

p < .05.

p < .005.

p < .0005.

As shown in Table 5, different factors explain pricing complexity for U.S. and Korean firms and for domestic and international pricing circumstances. Productivity and growth is positively related to pricing complexity for domestic pricing but is negatively related for Korean international pricing. Thus, for Korean firms, as productivity and growth increases in importance, fewer cost factors are used in setting price.

To measure price differential, we asked, “What is the relationship between your price to your largest international distributor and your lowest domestic price?” and regressed the same variables against those responses. The significant results are shown in Table 6. The results are somewhat different than for pricing complexity. Productivity and growth is negatively related to price differential for U.S. firms, as are setting price and economic uncertainty, whereas number of employees for exports is positively related to price differential (the greater differential, the greater is the price charged to the largest international distributor compared with the lowest domestic price). For Korean firms, adapting marketing strategy to the environment is the only significant variable. The negative relationship indicates that as the importance of adapting increases, the more likely it is that the international price is less than the lowest domestic price.

Regression for the Relationship Between Domestic and International Price

p < .10.

p < .05.

Research Question 3 pondered the effects of firm characteristics such as size, export intensity, export experience, and the like. The effects of these variables are different depending on the home country of the exporter. For example, size (number of employees) is positively related to the price differential for U.S. firms but is not related for Korean firms. Furthermore, differences are observed, by country, for the effects of firm characteristics on different cost areas.

When specifically examining Research Question 4, whether the degree of difficulty in adapting to local conditions influences pricing complexity, we again find differences between U.S. and Korean firms. Although there are country differences, adapting marketing strategy to the local market is a common adaptability issue influencing pricing complexity. In addition, the variable is related to the difference between domestic and international marketing costs.

Discussion

The results of this study provide a wealth of insight, in particular because the variance between Korean firms and U.S. firms appears to be great. In general, Korean firms seem to price more competitively in international markets than in domestic markets, whereas U.S. firms seem to consider more cost and profit factors when setting price. However, the number of factors (complexity) used in determining price does not imply either cost-plus or market (competitive)-based pricing. Firms may use market-based pricing to get a foothold when they enter a new market, though it may appear that various cost factors are ignored. Local market conditions where firms do business must be considered in pricing decisions. Therefore, any general model must take into account whatever factors are driving the differences that were observed.

For example, we investigated a research question that was based on differences expected in developed versus emerging economies. Future research should examine the issue of the home economy further, particularly as to whether developed or emerging home economies lead to different marketing goals, which then lead to different pricing strategies, or whether differences are due to cultural factors. For example, it has been considered that cultural factors in Japan led the Japanese to use warfare strategies in marketing (Ford, Tanner, and French 1989). These strategies led to penetration pricing, as Japanese companies were willing to forgo some short-term profit to gain market share. Our findings indicate that Korean firms that price exports lower than domestic prices (an indication of a penetration pricing strategy) are also more likely to consider marketing costs, an indication of a strategy similar to that of the Japanese. Firms in the United States that price exports equal to or lower than domestic prices tend to focus more on packaging and transport costs. This strategy indicates a focus on contribution margin rather than market share.

Similarly, productivity and growth is positively related to domestic pricing complexity but negatively related to international pricing complexity for Korean firms. This finding could support a market penetration strategy for exports, because fewer cost elements used in pricing may indicate greater reliance on market factors when pricing. The issue of whether pricing is two-dimensional (cost and market dimensions) should be explored in the context of models of strategy (e.g., Mintzberg 1994; Porter 1985). Furthermore, such an exploration should consider the perspective of strategy as emerging from experimentation and market feedback (e.g., Moorman and Miner 1998) versus a strategic perspective of planning (e.g., Thorelli 1977) to explore the potential existence of a two-stage strategy and other derivations of pricing processes.

Thus, on the basis of the findings of this study, further research should consider whether some companies use a two-stage pricing process: (1) set a cost-plus price and (2) adjust for market feedback. However, further research should also explore what is the most effective method of pricing for entering new markets. A price set too high when a firm enters a market may create perceptions about the company's image that cannot be changed without significant marketing costs. A price set too low may cause customers to question the company's quality, even after price adjustments. As Nagle and Holden (1995) point out, cost-plus pricing does not reflect market conditions and may cause poor performance because of over- or underpricing in different types of markets.

Transportation is the one common cost factor of importance in exporting. Although the finding that transportation is a common cost consideration may seem obvious, what is interesting is that it seems to be the only common consideration. Otherwise, different factors and objectives play a greater role depending on the country of origin and the needs of companies in that country. Further research should examine the country of origin and the relative size of companies in a particular market.

In addition to contributing to the understanding of differences in pricing for domestic and international markets for both Korean and U.S. firms, this study also adds to the understanding of pricing in general. Pricing complexity and measures pertaining to international pricing comparisons appear to have worked well. These measures can be applied to other international settings but can also be applied to market segments within a trading area to understand the nature of pricing decisions.

One interesting question for future study is why COGS appears to be irrelevant for many firms, especially those based in Korea. Perhaps for these firms, market opportunities make COGS irrelevant. Another option is that the firms simply take domestic price and add transit costs to arrive at an export price; therefore, COGS is irrelevant. A third alternative is that in Eastern cultures such as Korea, which are high in collectivism and belonging, firms may set prices at least at a level to include COGS as part of informal collaborative trade agreements between firms. From a different perspective, the question in international pricing decisions may be to determine why most U.S. firms use COGS rather than why some Korean firms do not use COGS.

Multinational corporations have used transfer pricing (prices charged among subsidiaries) as a tool for avoiding taxes (Fraedrich and Bateman 1996). By adjusting the prices within firms for the transfer of products, firms can minimize their effective tax rate. According to Fraedrich and Bateman (1996), the Internal Revenue Service is aware of this tactic and has tightened the pricing methods allowed to firms in setting transfer prices. Only three pricing methods are allowed in the Internal Revenue Service Code, and the cost-plus method is the easiest to calculate. Therefore, another possible explanation for the difference between the importance U.S. and Korean exporters place on COGS is a difference in taxing regulations. In any event, the lack of or inclusion of COGS as an important cost element should be explored. Future studies on export pricing in other emerging markets will further add to the understanding of pricing complexity.

Furthermore, because price and other strategic marketing decisions (Cavusgil and Zou 1994; Myers and Cavusgil 1996; Raymond, Kim, and Shao 2001; Zou and Stan 1998) affect export performance, future studies should examine the relationship between cost complexity of pricing decisions and export performance. The use of more complex pricing components may reflect greater knowledge of the costs associated with exporting. As such, more complex pricing should result in perceptions of better performance. Therefore, the importance and use of market-based versus cost-based pricing and the resulting impact on performance should be examined.

Conclusion

Determining pricing strategies in international markets will continue to be critical and challenging decisions for both exporters and MNCs. As organizations continue to expand internationally, especially into previously protected markets with unique environmental conditions, pricing decisions will remain complex. Although there is no single pricing alternative that is best for all markets, this study examines cost factors across markets. As such, a cost complexity index is suggested as a useful tool for making pricing decisions. Market conditions and the competitive nature of pricing are also critical components of pricing decisions, which will continue to be difficult aspects for export managers.

We propose a model that indicates that two types of factors, firm characteristics and export market characteristics, influence export pricing decisions. These factors appear to influence export pricing complexity from a cost perspective. Furthermore, although the home country can be considered a characteristic of the firm, there are such significant differences between U.S. and Korean firms that we suggest exploring the nature of potential causes of those differences. As one of the few empirical studies of export pricing, this article both offers a mechanism for further study and identifies many important elements for such study.

Footnotes

Pricing Complexity (Dependent Variable) and other Influential Factors (Independent Variables) 1

The independent variables were the result of factor analysis done for export motives, export market characteristics, and strategic marketing decisions. The independent variables also included firm characteristics (Raymond, Kim, and Shao 2001).

This Appendix describes the dependent variable, pricing complexity, and the independent variables, which were regressed against complexity. To determine pricing complexity, we summed the number of items that respondents checked when asked to indicate items that were factored into their domestic and international prices. Domestic and international were summed separately.

Acknowledgments

The authors gratefully acknowledge the assistance of Robert Dahlstrom at University of Kentucky for collection of data from some of the U.S. exporters. They also thank John Mittelstaedt, Michael Dorsch, and the three anonymous JIM reviewers for their helpful comments on a previous version of this article.