Abstract

How does the monetary value of customer purchases vary by customer preference for purchase channels (e.g., traditional, electronic, multichannel) and product category? The authors develop a conceptual model and hypotheses on the moderating effects of two key product category characteristics—the utilitarian versus hedonic nature of the product category and perceived risk—on the channel preference–monetary value relationship. They test the hypotheses on a unique large-scale, empirically generalizable data set in the retailing context. Contrary to conventional wisdom that all multichannel customers are more valuable than single-channel customers, the results show that multichannel customers are the most valuable segment only for hedonic product categories. The findings reveal that traditional channel customers of low-risk categories provide higher monetary value than other customers. Moreover, for utilitarian product categories perceived as high (low) risk, web-only (catalog- or store-only) shoppers constitute the most valuable segment. The findings offer managers guidelines for targeting and migrating different types of customers for different product categories through different channels.

Conventional wisdom, shaped by anecdotal evidence and initial research studies, suggests that multichannel customers constitute the most valuable segment for marketers regardless of the product category. For example, the U.S.-based multichannel retailer Nordstrom finds that across categories, customers who use more than one channel spend four times as much as those who shop only through one channel (Clifford 2010). The limited relevant scholarly articles that typically analyze a single category demonstrate that multichannel customers purchase more often and spend a larger share of wallet than single-channel customers (Kumar and Venkatesan 2005; Venkatesan, Kumar, and Ravishanker 2007).

It is unclear, however, whether these results generalize to all product categories, which are typically classified along two key characteristics: utilitarian (e.g., office supplies, garden supplies) versus hedonic (e.g., apparel, cosmetics) and low perceived risk (e.g., books, home furnishings) versus high perceived risk (e.g., computers, jewelry). Are multichannel customers the most valuable for utilitarian, hedonic, high-risk, or low-risk categories? This issue is important because customer behavior fundamentally varies by these product category types (Ailawadi et al. 2006; Ailawadi, Lehmann, and Neslin 2003; Inman, Winer, and Ferraro 2009; Kamakura and Du 2012; Narasimhan, Neslin, and Sen 1996). For example, customers of a hedonic product category may seek variety and spend more on items in that category across different channels. In contrast, customers of utilitarian categories may want to shop efficiently in one channel and spend more in that channel. Similarly, low- (high-) risk product categories may attract customers of traditional (electronic) channels and induce them to spend more in those channels. However, because much research on multichannel customer behavior is based on data from a single product category or firm, it precludes the study of the product category's role in the monetary value of shoppers’ purchases by channel preference.

We define a multichannel customer of a broad product category as a customer who buys items in that category from more than one channel. 1 By viewing multichannel shopping from the customer angle, our approach provides a holistic view of a customer's behavior. We address two important research questions in the retailing context:

In our subsequent empirical analysis, we test for alternative definitions of multichannel customers and show that our results are robust to alternative definitions.

How does the monetary value of purchases by multichannel customers differ from that of single-channel customers?

How does the relationship between a customer's channel preference and monetary value vary by key product category characteristics (utilitarian vs. hedonic nature and perceived risk)?

The answers to these questions are critical from both theoretical and managerial standpoints. For example, if the monetary value of multichannel customers is higher than that of single-channel customers across all categories, marketers should reach customers of all categories through different channels. Similarly, if web-only shoppers are the most valuable channel segment for high-risk/utilitarian categories (e.g., computers, electronics), marketers should target these shoppers. Finally, if traditional channel shoppers of low-risk categories (e.g., office supplies, garden supplies) provide higher monetary value than multichannel or web-only shoppers, marketers should focus on these shoppers.

To address these research questions, we develop a conceptual framework and important hypotheses related to the moderating role of the two key product category characteristics—utilitarian versus hedonic nature and perceived risk—on the link between channel preference and customer monetary value. We test our hypotheses and obtain empirically generalizable insights by analyzing a unique large-scale, cross-sectional data set of 1 million customers randomly drawn from 96 million customers of 750 direct marketing retailers, spanning 22 product categories across the catalog and web channels over a four-year period. We generalize the results to the store channel with a longitudinal analysis of transaction data from a large multiproduct retailer with the store channel in addition to the catalog and web channels.

Our results show that contrary to conventional wisdom, multichannel customers form the most valuable segment only for hedonic product categories. We also find that traditional channel customers of low-risk product categories provide higher monetary value than other customers. Moreover, web-only (store- or catalog-only) customers of high-(low-) risk/utilitarian categories offer higher monetary value than other single-channel or multichannel customers. Our findings provide valuable managerial guidelines for shopping in different channels.

This article contributes to the literature in at least two key ways. First, it offers a theoretical understanding of the moderating effects of category characteristics on the channel preference–monetary value relationship. Second, it provides empirically generalizable counterintuitive findings about this relationship. Furthermore, as Table 1 shows, unlike related research (e.g., Ansari, Mela, and Neslin 2008; Kumar and Venkatesan 2005), the current research examines the moderating effects of the product category and analyzes data from multiple categories and firms in an integrated framework.

Contribution of Current Research to Relevant Research

Conceptual Development

We first develop a conceptual model of the relationships between channel preference, product category characteristics, and monetary value (see Figure 1). We focus on both traditional and electronic channels. We classify the store and catalog channels under the unifying banner of a traditional channel because they have a much longer history than electronic channels and are perceived as close substitutes (Avery et al. 2012). Any combination of these channels constitutes a multichannel. Among the outcomes, we focus on a key managerial variable—that is, the monetary value of customer purchases—measured as the dollar value of customer transactions.

A Conceptual Model of Relationships Between Channel Preference, Monetary Value, and Product Category Characteristics

Prior research has examined the role of the product category in influencing different facets of customer behavior in traditional and electronic channels (Yadav and Varadarajan 2005b). Consistent with this research, we examine the moderating role of two key product category characteristics (i.e., utilitarian vs. hedonic nature and perceived risk) in shaping the relationship between channel preference and customer monetary value.

We define a utilitarian category as a category dominant on attributes such as functionality, practicality, cognition, and instrumental orientation, consistent with Dhar and Wertenbroch (2000). Computing equipment, consumer electronics, office supplies, home appliances, and garden equipment are examples of utilitarian categories. We define a hedonic category as a category dominant on attributes such as experiential benefits, affect, enjoyment, enduring involvement, intrinsic motivation, and aesthetics (Dhar and Wertenbroch 2000). Examples of hedonic categories include CDs, DVDs, antiques, and apparel. Unlike hedonic products, utilitarian products can be easily compared and evaluated along different attributes.

We refer to perceived risk of a product category as the “customers’ (overall) perceptions of uncertainty and adverse consequences of buying a good (or service)” (Dowling and Staelin 1994, p. 119; see also Bart et al. 2005). Perceived risk of a product category is evaluated on five dimensions of uncertainty: functional (not performing to expectation), financial (losing money), safety (causing physical harm), psychological (tarnishing self-image), and social (lowering others’ perceptions of the user) (Jacoby and Kaplan 1972). Office supplies and books are examples of low-risk categories, while jewelry and computers are examples of high-risk categories.

We chose these two product category characteristics as potential moderators from two main theoretical considerations. First, both category characteristics are grounded in regulatory focus theory (RFT), the basis for our hypotheses development. Prior research in marketing (see Chernev 2004; Yeo and Park 2006) treats hedonic (utilitarian) and high (low) perceived risk attributes as consistent with a promotion (prevention) focus in goal orientation, the key ingredients of RFT.

Second, utilitarian versus hedonic nature and perceived risk constitute fundamental bases for consumer purchase and consumption. Batra and Ahotla (1990, p. 159) state that “consumers purchase goods and services and perform consumption behaviors for two reasons: (1) consummatory affective (hedonic) gratification (from sensory attributes) and (2) instrumental (utilitarian) reasons.” Likewise, the study of perceived risk as an inherent product category characteristic behind purchase and consumption behavior has a long tradition in the marketing literature (e.g., Cox and Rich 1964; Sheth and Venkatesan 1968).

Our conceptual model includes the direct/main effect of channel preference and the interaction effects of channel preference and product category characteristics on monetary value. We develop hypotheses pertaining to these effects. Our overarching argument is that different shoppers have different foci based on RFT, and if shoppers’ focus fits with their channel preference based on the product category characteristics, they will experience greater regulatory fit. In turn, stronger regulatory fit will lead to higher spending in their preferred channel on the product categories that exhibit those characteristics.

Main Effect

We first develop our hypothesis about the main effect of customer channel preference on the monetary value of purchases across categories. An entity (e.g., customer) evaluates the outcome of an exchange process with another entity (e.g., firm) by comparing the perceived benefits with the perceived costs related to the exchange, consistent with the quid pro quo notion (Bagozzi 1975). In addition to economic aspects, social and psychological aspects (e.g., mutual respect, commitment, trust) play an important role in determining the entities’ perceived overall benefits, costs, and value in an exchange (Frazier 1999).

Depending on their perceived value of an exchange through a channel, customers prefer to use different channels and spend different amounts in different channels. Customers who perceive exchanges in a channel as being of high value become frequent customers with a high degree of trust and commitment to purchase through that channel. Customers with a stronger commitment spend more on their purchases than other customers (Venkatesan, Kumar, and Ravishanker 2007).

The use of multiple channels is associated with a high level of monetary value for customers across all product categories for several reasons. First, additional channels provide greater convenience value for customers, increasing their purchase frequency and accelerating purchases across multiple items and categories. Second, the wide assortment of products across different channels offers multiple opportunities for customers to buy and increase their spending. Third, customers can combine the benefits from different channels, realize greater value, and increase their spending (Frazier 1999). The web and traditional channels are complementary rather than cannibalistic with regard to the money spent on shopping (Deleersnyder et al. 2002). Thus, channel segment membership (single-channel or multichannel) is a proxy for customers’ perceived value of and commitment to that channel. This commitment is positively related to customers’ spending in that channel across products. Therefore:

H1: Across all product categories, multichannel customers have a higher monetary value of purchases than single-channel customers.

Moderating Impact of Product Category Characteristics

We now develop hypotheses on how the hedonic versus utilitarian nature and perceived risk moderate the strength of the relationship between channel preference and monetary value. We present a summary of the hypotheses together with the associated rationale in Table 2.

Summary of Moderating Effects Hypotheses

Notes: M = multichannel, T = traditional channel (store/catalog), and E = electronic; superscripts: H = hedonic, U = utilitarian, HR = high-risk, and LR = low-risk.

We adopt RFT to motivate our hypotheses. According to RFT, people can be classified into two types on the basis of their regulatory orientation in pursuing a goal: prevention focused and promotion focused (Avnet and Higgins 2006). A prevention focus stresses safety, security, and responsibility, whereas a promotion focus emphasizes hope, advancement, and achievement. Thus, a promotion focus involves maximizing positive outcomes, whereas a prevention focus means minimizing negative outcomes. As RFT postulates, people make choices that are consistent with their regulatory orientation (promotion or prevention focus) in goal pursuit (Avnet and Higgins 2006). When such choices sustain their regulatory orientation, people experience a regulatory fit, leading them to continue their pursuits (Aaker and Lee 2006). Thus, a customer is likely to engage repeatedly in his or her preferred buying process (channel) if doing so is consistent with his or her regulatory orientation (Avnet and Higgins 2006). Regulatory fit leads to greater customer engagement through two well-documented processes (Cesario, Higgins, and Scholer 2008): (1) feeling right about the task and (2) increased information processing. These engaged customers tend to value and pay more for products than customers lacking in regulatory fit (Avnet and Higgins 2006). Therefore, promotion- and prevention-focused customers will tend to spend more on their purchases in their preferred channel.

Some channels are closely associated with a prevention focus, whereas others are aligned with a promotion focus. Because of their long history, traditional channels (i.e., catalog and store) offer high levels of familiarity, safety, confidence, and trust. In the case of physical stores, customers can browse, touch, and feel products before purchase. Furthermore, many catalog companies and physical stores have had a long-standing practice of accepting returns from customers without asking questions. Therefore, traditional channels offer customers high confidence and trust in their purchases. Thus, catalog- and store-only customers are likely to have a high prevention focus as they repeatedly patronize traditional channels that offer high levels of safety, minimizing negative outcomes.

In contrast, the relatively newer electronic channels (e.g., the web) evoke high behavioral and environmental uncertainty (Schlosser et al. 2006; Van Noort, Kerkhof, and Fennis 2008). A large-scale survey by the Pew Internet Project (2008) shows that the web is perceived as highly uncertain such that approximately three-quarters of participants were unwilling to provide personal and credit card information over the Internet. Furthermore, the web entails the risk of identity theft, a significant deterrent to online channel adoption (Garver 2012). Despite more than a decade since the advent of electronic commerce, the adoption of the web as a transaction channel is still limited because of a high level of perceived risk. Therefore, web-only customers who repeatedly patronize the electronic channel are likely to be driven by adventure and the need to signal advancement—that is, by focusing on positive outcomes. Moreover, web-only shoppers tend to be younger, better educated, and more prone to search on the web than other shoppers. Thus, these customers are likely to have a greater promotion focus.

Customers who adopt multiple channels seek greater convenience and display boldness associated with the adoption of the electronic channel. They seek greater enjoyment and adventure through the use of different channels. Therefore, multichannel customers are also likely to have a greater promotion focus.

In summary, customers patronizing traditional modes of transaction (catalog and store) are likely to have a greater prevention focus. In contrast, customers adopting nontraditional modes (web and multiple channels) are likely to have a greater promotion focus. However, product category characteristics moderate the monetary values of customers by channel preference.

Utilitarian versus hedonic nature and channel preference interaction

Because utilitarian products (e.g., computers, garden equipment, sports equipment) have clear and well-defined attributes, they are relatively easy to compare and evaluate. Thus, for utilitarian product categories, shopping tasks involve planned purchases, goal-directed choice, and cognitive involvement (Novak, Hoffman, and Duhacheck 2003). Goal-directed behavior can lead to habit formation and automatic behavior (Aarts and Dijksterhuis 2000). In addition, utilitarian categories are typically high on search-dominant attributes. People allocate time, a scarce resource, to different activities, including search (Becker 1965). Scarcity of time is negatively linked to search efforts (Beatty and Smith 1987). Therefore, consumers of utilitarian products value efficiency in shopping (Mathwick, Malhotra, and Rigdon 2002). In general, efficiency attributes are associated with a greater prevention focus (Chernev 2004). Goal-oriented shopping behavior associated with utilitarian product categories is efficient in time utilization when both search and purchase are done habitually and repeatedly in a single channel. Because efficiency is paramount, these customers prefer using a single channel to multiple channels.

Customers of traditional channels have a greater prevention focus, which maps with the prevention-focus attributes of utilitarian product categories, providing a strong channel–category fit. In contrast, because multichannel customers are promotion focused on utilitarian products, they experience a relatively weak regulatory fit. A stronger regulatory fit is associated with greater engagement and higher spending, and thus we expect traditional channel customers of utilitarian products to spend more than their multichannel counterparts.

Although web-only and multichannel customers are likely to have a greater promotion focus, which provides a weak regulatory fit with the utilitarian attributes, the greater efficiency of the web maps well with the shopping goals associated with utilitarian categories. Thus, web-only customers of utilitarian categories are also likely to have better goal–attribute fit than their multichannel counterparts. Taken together, we expect that single-channel customers of utilitarian product categories have higher monetary values than multichannel customers. Thus:

H2: The monetary value of purchases by single-channel customers of utilitarian product categories is higher than that by multichannel customers of these categories.

Hedonic categories, such as apparel, cosmetics, and DVDs, are conducive to unplanned or impulse buying and variety seeking (Novak, Hoffman, and Duhacek 2003). Impulse purchases are characterized by spontaneity, compulsion, excitement, and disregard for consequence (Koufaris 2002). Variety-seeking behavior is, in part, driven by factors such as product category–specific differences (Van Trijp, Hoyer, and Inman 1996). Customers of hedonic product categories likely have high goal ambiguity because of affect-dominant attributes and the salience of the experiential value of hedonic products. Such goal ambiguity leads customers of hedonic categories to include disparate products in their consideration set (Ratneshwar, Pechmann, and Shocker 1996) and seek variety. In addition, perceived uncertainty about future preferences is likely to be higher for hedonic products, leading to variety seeking as a choice heuristic (Simonson 1990). In general, hedonic attributes are associated with a greater promotion focus (Chernev 2004). Thus, customers are more likely to engage in variety-seeking behavior for hedonic categories and spend more (Garg, Inman, and Mittal 2005; Kurt, Inman, and Argo 2011; Ratner and Kahn 2002; Stilley, Inman, and Wakefield 2010a, b).

Multichannel customers are likely to have a greater promotion focus, which provides a strong regulatory fit with hedonic attributes. Multiple channels provide a greater assortment of products than a single channel. More hedonic products across multiple channels offer customers more opportunities to engage in impulse purchases, enhance customers’ consideration set, and promote greater variety seeking. In contrast, the prevention focus of traditional channel customers has a weak regulatory fit with hedonic attributes. Thus, multichannel customers are likely to be more strongly engaged and have a higher spending level than their counterparts from traditional channels.

Web-only customers are also likely to have a greater promotion focus, which provides a strong regulatory fit with hedonic attributes. However, the use of multiple channels offers greater convenience and variety, which are more satisfying for variety-seeking and impulse purchase behaviors commonly involved in hedonic categories. Thus, multichannel customers of hedonic categories are likely to have a better goal–attribute fit than their web-only counterparts.

In summary, we expect that multichannel customers of hedonic product categories have higher monetary value than their single-channel counterparts. These arguments lead to the following hypothesis:

H3: The monetary value of purchases by multichannel customers of hedonic product categories is higher than that by single-channel customers of these categories.

Perceived risk and channel preference interaction

For product categories with high perceived risk, such as electronics, telecommunications equipment, and musical instruments, customers face considerable uncertainty. Therefore, product categories with high perceived risk fit the goal orientation of promotion-focused customers (Yeo and Park 2006). A promotion focus is consistent with risk-seeking behavior (Avnet and Higgins 2006). Conversely, a prevention focus is synonymous with risk-averse behavior and fits with low-risk product categories, such as office supplies, books, and toys.

Because of the channel–category fit, low-risk categories likely attract prevention-focused customers who shop in traditional channels, whereas high-risk categories may draw promotion-focused customers, such as those shopping on the web or through multiple channels. Consistent with the notion that the perceived risk of the web is due to the relative newness and impersonal nature of the channel (Montoya-Weiss, Voss, and Grewal 2003), we expect that web-only customers have a greater promotion focus than a prevention focus. Similarly, because multichannel customers may seek greater enjoyment and adventure through different channels, they are likely to have a greater promotion focus. In contrast, because of the low-risk profiles of the store and catalog channels, single-channel customers are likely to have a greater prevention focus.

With the high degree of fit among prevention focus, low-risk categories, and traditional channels, traditional channel customers tend to spend more than web-only or multichannel customers in low-risk categories. In contrast, web-only and multichannel customers of high-risk categories likely spend more than customers of traditional channels because of the high degree of fit between these categories and channels. These arguments lead to following hypotheses:

H4: The monetary value of purchases by traditional channel customers of low-risk product categories is higher than that by electronic channel and multichannel customers of these categories.

H5: The monetary value of purchases by electronic channel and multichannel customers of high-risk product categories is higher than that by traditional channel customers of these categories.

Empirical Analyses

We examine an empirical context comprising a carefully compiled, unique, and large cross-sectional database of approximately 1 million U.S. customers who were randomly selected from a cooperative database of 96 million customers of 750 direct marketers covering 22 product categories and several subcategories during a four-year period (2001–2004). We obtained data from i-Behavior, a syndicated data aggregator firm. Firms in the cooperative database have only the web and catalog channels (no physical stores exist), so the catalog is their offline channel. The data contain customers’ demographic characteristics, shopping experiences, preferred purchase channels, order details, and product categories purchased. This period adequately captures the growth phase of the web as a distribution channel. Details on these 22 product categories appear in the Web Appendix (WA1; www.marketingpower.com/jm_webappendix).

Our data set is neither firm nor industry specific, and it captures customer purchases across a comprehensive set of product categories and competing firms. Such data are highly representative of the population and allow for empirical generalizability. Data sets from prior research are primarily from a single firm across one or a few product categories. Our database covers a wide range of product categories, such as apparel, accessories, gifts, hobby items, electronics, and musical instruments, for 750 multichannel direct marketers, which enables us to develop a richer understanding of a customer's channel preference and behavior than when analyzing data from a single firm or a few categories.

Operationalization of Variables

The operationalization of the variables in our data appears in Table 3. The exogenous classes of variables, such as demographic characteristics, shopping experience, high-end catalog usage, and the number of unique mailing lists that contain the customer's name, are based on the customers’ past transaction history.

Operationalization of Variables in the Data

Data aggregators in the direct marketing industry classify catalogs into five categories on a continuum from “low-scale” to “high-scale” catalogs. The number of times a customer orders from the highest category of the “high-scale” catalogs is the operationalization of the variable.

MasterCard and Visa issued by major banks, American Express, and Discover are classified as major credit cards.

Table 4 provides summary statistics for the key variables in our model. Of the usable sample (customers with data on every variable in the database), 71.8% purchased only through the catalog channel, 5.3% purchased only through the web, and the remaining 22.9% purchased through both channels. 2 Although the number of purchases of web-only shoppers is much smaller than that of catalog-only and multichannel shoppers, web-only retail sales grew by approximately 12% during the 2006–2010 period (Jupiter Research 2011). The summary snapshot suggests that multichannel customers spend approximately one and a half times more than catalog-only customers and approximately five and a half times more than web-only customers. Similarly, multichannel customers buy more often (higher frequency) than single-channel customers. However, are these initial summary observations true for all product categories? We address this question in our empirical analysis.

We compared the usable sample (n = 412,424) with the unusable sample on each of the five dependent variables analyzed in the subsequent sections. The means of the key dependent variables of the usable and unusable samples are similar.

Summary Statistics of Key Variables in the Data

The reported summary statistics are before performing an Anscombe transformation.

Measurement of Product Category Characteristics

We use data from exogenous sources to measure the two key category characteristics of the 22 product categories. We classify product categories with a higher utilitarian score than hedonic score as utilitarian, and vice versa for the purchased product category basket. We classify the categories as high or low risk on the basis of a median split along these dimensions for the purchased product category basket. We dummy-code consumer shopping baskets on four variables: hedonic dummy, utilitarian dummy, high-risk dummy, and low-risk dummy. The mixed shopping basket, containing both hedonic and utilitarian and high-risk and low-risk products, serves as the base case scenario.

Measurement scale

Consistent with prior research, we operationalize the hedonic versus utilitarian nature of a product category using the hedonic utility (HEDUT) scale (Voss, Spangenberg, and Grohmann 2003). The scale measures the strength of a product category on utilitarian and hedonic aspects using an equal number of items. The details of the scale items and anchors used for measuring each of these two aspects appear in the Web Appendix (WA2; www.marketingpower.com/jm_webappendix). We operationalize perceived risk using the scale developed by Jacoby and Kaplan (1972) and used by others (e.g., Chaudhuri 1998). Product category risk has five components: functional (not performing to expectation), financial (losing money), safety (causing physical harm), psychological (tarnishing self-image), and social (lowering others’ perceptions of the user). Figure 2 depicts the relative positions of categories on these two dimensions. We calibrate the axes in the map on deviations from the median score. Details of the scale items appear in WA2.

Relative Positions of Product Categories Along Key Category Characteristics

Data collection

We collected data on these measures from students in a nationally ranked business program of a large well-known university in the eastern United States. To reduce cognitive fatigue associated with long questionnaires, we used a split sample approach in which each respondent evaluated only 11 product categories. We randomly assigned the product categories to the two types of questionnaires and randomly distributed the questionnaires to the respondents. Of the 78 questionnaires, we received 67 usable responses.

Scale properties

Both the HEDUT and Perceived Risk scales possess excellent convergent validity, divergent validity, and reliability. All five items from the Perceived Risk scale load on one factor, measuring the underlying concept of perceived risk. Details on the scale properties and computation of the composite measures of HEDUT and Perceived Risk appear in the Web Appendix (WA2; www.marketingpower.com/jm_webappendix). Table 5 reports the mean composite scores for each product category on each of these three underlying dimensions across our sample.

Summary Scores of Product Categories on HEDUT and Perceived Risk Scales

Notes: The scores are based on a seven-point scale in which higher numbers indicate greater strength of the measured attribute.

Measurement validation

The measures have considerable face validity. The categories with higher technological complexity and higher prices or those used more in social settings scored higher on perceived risk (e.g., electronics, photography and video equipment, jewelry, apparel and accessories). Similarly, the respondents perceived the beauty and cosmetics, wines, and home furnishing categories as largely hedonic and the computing, telecommunications, and office supplies categories as mainly utilitarian. We cross-validated these findings through the ratings of five experts who classified all 22 categories into this 2 × 2 matrix. The interrater reliability was .93, suggesting high external validity of our survey results.

Model Formulation

Monetary value

We model the key dependent variable of interest, monetary value (DLLRi) of a customer i, as a function of his or her channel preference, purchase frequency (ORDRi), and number of marketing mailers received (MAILi), as follows:

where CTLG (catalog only) and WEB (web only) are dummy variables for the use of the catalog and web channel, respectively, with multichannel as the base channel. In addition, UTL (utilitarian categories only), HED (hedonic categories only), LR (low-risk categories only), and HR (high-risk categories only) are dummy variables representing category characteristics with all categories as the base. Finally,

For example, a customer may prefer to use multiple channels because he or she has a larger shopping basket or purchases more expensive items. Similarly, a customer may have a high monetary value because he or she receives many marketing mailers or has a high purchase frequency. We model and account for such simultaneity and endogeneity.

Channel preference

A customer is likely to prefer a channel (or combination of channels) that provides the highest utility. Let the utility U of customer i's preference of channel j be given by (2)

where

where Φ is the probability density function of normal distribution and V is the deterministic component of utility.

Purchase frequency

The purchase frequency of a customer is given by

where γ is a parameter vector,

Mailers

The number of marketing mailers a customer receives is given by

where

Identification and Instrumental Variables

To identify the four equations, each with three endogenous variables, we require at least three excluded exogenous variables or instruments for each one. Theoretically, a good instrument should be correlated with the left-hand-side endogenous variable but uncorrelated with the independent variables. 4 We propose nine excluded exogenous variables for each equation that constitute appropriate instruments according to theoretical considerations examined in the marketing literature.

We subsequently test for the quality of instruments in the “Robustness Checks” section.

Customer-ordering characteristics (ID)

Three customer-ordering characteristics—namely, the number of high-end catalogs used, the value of the highest basket, and the relative use of a credit card—may influence the monetary value of purchases for the following reasons. Customers who browse high-end products (HIGH) are likely to spend more because the average unit price of such items is higher than that for other items. Similarly, the dollar value of the customer's largest order (HISPEND) will be strongly correlated with the monetary value of customers but only weakly related to the other endogenous variables such as purchase frequency. Finally, consistent with previous research that shows that customers who purchase with a credit card are likely to spend more than those who use other payment modes (Soman and Cheema 2002), we use relative credit card usage (RCCU) as an instrument for monetary value.

Customer demographics (IC )

A customer's demographics may significantly influence his or her channel preference behavior. Different socioeconomic classes may have different predispositions to buy from different types of channels, and customer demographics play an important role in the choice of the information channel and the resulting share of volume for a channel (Inman, Shankar, and Ferraro 2004). Age, family size, and education are key demographic variables influencing channel preference. 5 The literature on store choice behavior (e.g., Popkowski Leszczyc, Sinha, and Timmermans 2000) and channel–category associations (Inman, Shankar, and Ferraro 2004) suggests that three customer demographic variables—age (LAGE), family size (FSIZE), and education (EDU)—most likely influence channel preference.

We do not include gender in our analysis because there are no strong theoretical reasons to expect differences in channel preference due to gender differences and because a subsequent empirical analysis involving gender showed that gender has a nonsignificant effect on channel preference (p > .10). This finding is consistent with the result that there are no significant differences between male and female web-only shoppers (Jupiter Research 2011). We also exclude income because it is highly correlated with education in the data we subsequently analyze.

Customer shopping experience (IO )

We expect that customer shopping experience, which includes years of shopping (EXP), number of product categories purchased (CAT), and number of items returned (RET), influences purchase frequency for the following reasons. Typically, customers who have shopped longer are more knowledgeable about selling practices and channels, have greater shopping involvement, and order more frequently (Bolton 1998). The number of categories and purchase frequency are positively related because a customer tends to buy associated categories on a given occasion (Kumar and Venkatesan 2005). 6 Customers with higher returns also likely have higher purchase frequencies (Kumar and Venkatesan 2005).

Although the number of categories may seem positively correlated with monetary value, there is no theoretical reason to believe this is so. A customer buying one low-value item each from several categories may have a lower monetary value than another customer buying several high-value items from a single category. Indeed, the correlation between these two variables is not high in our data (.39).

Customer marketing profile (IM )

Firms send marketing mailers to prospects according to their marketing profiles. Three key variables that constitute marketing profile are (1) the number of unique mailing lists containing the customer's name (UNQML), (2) the net worth of the target customer (NTWTH), and (3) the number of unique mailing lists to which the customer has responded (UNQRS). Direct marketers typically use these factors when selecting new customers to target in their direct mail campaigns (Direct Marketing Association 2005).

Estimation

The proposed simultaneous system comprises an observed endogenous discrete choice variable (channel preference), endogenous count variables (frequency and mailers), and an endogenous continuous variable (monetary value). Because we have a combination of discrete and continuous variables in the system, traditional two-stage or three-stage least squares estimation will lead to biased estimates. To estimate this system, we extend the generalized probit framework (Amemiya 1978), which assumes that the random error component in each equation is normally distributed. To make the joint estimation tractable, we transform the negative binomially distributed count variables (frequency and marketing mailers) into near-normal distributed variables, using Anscombe transformation (Anscombe 1948). This procedure ensures that our system has equations with only two types of dependent variables with normally distributed errors. We follow the two-step estimation approach detailed in the Web Appendix (WA3; www.marketingpower.com/jm_webappendix). In Step 1, we regress each endogenous variable on all the exogenous instruments. In Step 2, we regress monetary value on the included exogenous variables and predicted values of endogenous variables (from Step 1). We use the ordinary least squares estimation for the monetary value, purchase frequency, and marketing mailers models and the multinomial probit estimation for the channel preference model.

Results and Discussion

Main Effect

We present the results of the monetary value model in Table 6. 7 Consistent with H1, across all product categories, multichannel customers have a significantly higher monetary value than single-channel customers (p < .01). The average multichannel customer outspends the average catalog- and web-only customers by $60.13 (β1) and $108.92 (β2), respectively. In addition, the intercept is positive and significantly high ($436.76; β0), highlighting the expected high spending level of multicategory, multichannel shoppers.

The model results for the other endogenous variables not used for hypotheses testing appear in the Web Appendix (WA4; www.marketingpower.com/jm_webappendix).

Results of Monetary Value Model

Multichannel is the base case.

Notes: All boldfaced coefficients have ps < .05.

Hypothesized Interaction Effects

H2 suggests that single-channel customers of utilitarian product categories spend more than other customers. After we control for the effects of other variables, the average catalog-only, web-only, and multichannel customers of utilitarian product categories spend $438.70 (β0 + β1 + β3 + β7), $431.65 (β0 + β2 + β3 + β8), and $435.05 (β0 + β3), respectively. 8 However, the difference in spending among the average catalog-only, web-only, and multichannel customers is not significant (p > .10). Thus, we find that the monetary values of utilitarian category purchases do not significantly differ among traditional, electronic, and multiple channel customers.

We tested the differences between the effects by accounting for the standard errors and covariances of the parameter estimates.

H3 proposes that multichannel customers of hedonic product categories will outspend their single-channel counterparts. We find that the average catalog-only, web-only, and multichannel customers of hedonic product categories spend $187.43 (β0 + β1 + β4 + β9), $112.77 (β0 + β2 + β4 + β10), and $331.53 (β0 + β4), respectively. The difference in spending between the average multichannel and catalog-only customers ($144.09) and between the average multichannel and web-only customers ($218.76) is positive and significant (p < .01). These findings suggest that multichannel customers of hedonic product categories significantly outspend their single-channel counterparts, in support of H3.

H4 proposes that traditional channel customers of low-risk categories have higher monetary value than that of other customers. The average catalog-only, web-only, and multichannel customers of low-risk product categories spend $459.27 (β0 + β1 + β5 + β11), $350.70 (β0 + β2 + β5 + β12), and $411.87 (β0 + β5), respectively. The difference in spending between the average catalog- and web-only customers ($108.57, p < .01) and between the average catalog-only and multichannel customers ($47.41, p < .10) is positive and significant, suggesting that traditional customers of low-risk categories offer higher monetary value than other customers. These results are consistent with H4.

According to H5, multichannel and web-only customers of high-risk categories have higher monetary value than that of other customers. The average catalog-only, web-only, and multichannel customers of high-risk product categories spend $485.24 (β0 + β1 + β6 + β13), $501.30 (β0 + β2 + β6 + β14), and $496.10 (β0 + β6), respectively. The difference in spending among the average multichannel, catalog-only, and web-only customers is not significant (p > .10). Thus, these results do not support H5.

Other Interaction Effects

We did not have formal hypotheses for the effects of three-way interactions among channel preference, utilitarian versus hedonic nature, and perceived risk because we treat these effects as empirical issues. We now discuss the results of these interaction effects.

Low-risk/utilitarian

We find that the average catalog-only, web-only, and multichannel customers of low-risk/utilitarian product categories spend $585.57 (β0 + β1 + β3 + β5 + β7 + β11 + β15 + β19), $322.78 (β0 + β2 + β3 + β5 + β8 + β12 + β15 + β20), and $404.51 (β0 + β3 + β5 + β15), respectively. The average catalog-only customers of low-risk/ utilitarian product categories spend $262.79 (p < .01) and $181.05 (p < .01) more than their web-only and multichannel counterparts, respectively. Therefore, for low-risk/utilitarian categories, traditional channel customers outspend non-traditional channel customers. Although the interaction effects of channel preference and a utilitarian nature suggest no significant difference between the monetary values of single-channel and multichannel customers (lack of support for H2), the interaction effects of channel preference and the low-risk nature of the category indicate a higher spending level by customers of traditional channels (H4). Because traditional channel customers are a subset of single-channel customers, for low-risk/utilitarian categories, traditional channel customers (who tend to have a prevention focus) experience a stronger regulatory fit than their web-only and multichannel counterparts.

High-risk/utilitarian

We find that the average catalog-only, web-only, and multichannel customers of high-risk/ utilitarian product categories spend $454.88 (β0 + β1 + β3 + β6 + β7 + β13 + β16 + β21), $554.16 (β0 + β2 + β3 + β6 + β8 + β14 + β16 + β22), and $395.88 (β0 + β3 + β6 + β16), respectively. The average web-only customers of high-risk/utilitarian product categories spend $99.28 (p < .05) and $158.27 (p < .01) more than their catalog-only and multichannel counterparts, respectively. In addition, we find that the difference between the monetary values of the average multichannel and catalog-only customers is not statistically significant (p > .10). These results suggest that for high-risk/ utilitarian product categories, web-only customers provide the highest monetary value, but the monetary values of catalog-only and multichannel customers do not differ.

This result is consistent with the arguments used for theorizing two-way interaction effects. Promotion-focused web-only customers are often comfortable buying high-value items from high-risk/utilitarian categories (e.g., consumer electronics, computing equipment) (Van Noort, Kerkhof, and Fennis 2008). Furthermore, utilitarian categories typically require a high degree of information search. For such categories, the web is conducive for information gathering and offers a high level of convenience for shopping and ordering items (Yadav and Varadarajan 2005a). Moreover, as we suggested previously, web-only shoppers tend to be younger, better educated, more risk taking, and more prone to obtaining information on utilitarian products on the web than other shoppers. Satisfaction and enjoyable experience with the information search through an online channel can lead to positive outcomes (Mathwick and Rig-don 2004). Consequently, web-only customers of high-risk/utilitarian categories buy more often and spend more than other single-channel customers. Because the utilitarian nature of the categories leads to efficient shopping through a single channel, web-only customers also outspend multichannel shoppers.

Low-risk/hedonic

We now turn to the effects of the interactions of perceived risk with the hedonic nature of the product category. For low-risk/hedonic product categories, the average catalog-only, web-only, and multichannel customers spend $231.72 (β0 + β1 + β4 + β5 + β9 + β11 + β17 + β23), $180.46 (β0 + β2 + β4 + β5 + β10 + β12 + β17 + β24), and $419.13 (β0 + β4 + β5 + β17), respectively. The average multichannel customers of low-risk/hedonic product categories spend $187.41 (p < .01) and $238.68 (p < .01) more than their catalog- and web-only counterparts, respectively. The result of the test of H4 shows that traditional channel customers of low-risk product categories outspend other customers of these categories. The result of the test of H3 shows that multichannel customers of hedonic categories spend more than other customers. However, for both the low-risk and the hedonic nature categories, multichannel customers have higher monetary value than other customers. This finding suggests that the hedonic nature has a stronger effect than low risk on monetary value.

High-risk/hedonic

The average catalog-only, web-only, and multichannel customers of high-risk/hedonic product categories spend $192.73 (β0 + β1 + β4 + β6 + β9 + β13 + β18 + β25), $144.64 (β0 + β2 + β4 + β6 + β10 + β14 + β18 + β26), and $353.19 (β0 + β4 + β6 + β18), respectively. The average multichannel customers of high-risk/hedonic product categories spend $160.47 (p < .01) and $208.55 (p < .01) more than their catalog- and web-only counterparts, respectively. The two-way interaction effects of channel preference and hedonic nature (H3) and of channel preference and high-risk nature (H5) indicate a higher spending level by multichannel customers than other customers. Consequently, the interaction of the hedonic nature with high risk has a more positive effect on the spending of multichannel customers than that of single-channel customers. Taken together, the results show that for hedonic categories, multichannel customers provide the highest monetary value regardless of the risk level of the category.

Extension and Generalization of Results to the Store Channel

The large data set in our study helps uncover empirically generalizable findings across multiple product categories and direct marketers with catalog, web, and multiple channels. To generalize these findings to the store channel, we extend this study with an analysis of a U.S. multiproduct retailer's data set that includes (1) time-series data and (2) data from physical stores. Time-series data facilitate the study of the potentially causal relationship between channel preference and monetary value. Because store purchases constitute a majority of transactions for many multichannel retailers, analysis of physical store data enables us to generalize our results.

The details of this analysis appear in the Web Appendix (WA5; www.marketingpower.com/jm_webappendix). The findings from this analysis are consistent with those from the larger cross-sectional data set and reinforce our conclusions. In addition, the findings bolster the temporal links among the variables in our model and extend the generalizability of our results for the catalog-only channel segment to all traditional channel segments, including the store-only channel segment.

Robustness Checks

Out-of-sample predictions

We validate our findings with an out-of-sample prediction on a randomly selected holdout sample of 50,000 customers. Using the parameter estimates from our estimated model on a sample of the remaining 362,424 customers, we predict the monetary value of customers in the holdout sample. The mean absolute deviation (MAD) is 250.14, the mean monetary value of the holdout sample is $1,254, and the MAD is approximately 19.95% of the sample mean. These values are reasonable for cross-sectional out-of-sample validation. 9

These MAD percentage values are comparable to those Jen, Chou, and Allenby (2009) report in a similar direct marketing context for predicting monetary value using linear regression.

Quality of instruments

We test the validity and strength of our instruments in multiple ways. In the “Identification and Instrumental Variables” subsection, we argue that our choice of instrumental variables is based on theory. We test for the strength of the instrumental variables using Staiger and Stock's (1997) approach. In this approach, we test the first-stage F-statistic for each equation with the instrumental variables. The bias introduced by the weak instruments is of the order of the inverse of the F-statistic. We follow Stock and Watson's (2003) rule of thumb; that is, an F-statistic greater than 10 is acceptable because it corresponds to a bias of less than 10% in the estimates. Staiger and Stock's (1997) test for the first-stage regression in our data does not indicate the presence of poor instruments. The F-statistics of the monetary value, frequency, and mailers equations are 26,747, 28,033, and 31,058, respectively. Thus, any weak instrument introduces, at worst, a less than .0001% bias. The adjusted R-square for these regression equations is also healthy (at least 60%), and the instrumental variables used in each equation are significant (p < .001), suggesting that the instruments are strong.

We also perform two formal tests to evaluate the validity of our instruments. First, consistent with Bound, Jaeger, and Baker (1995), we examine the validity of our instruments by using the correlation test. The correlation matrix reported in the Web Appendix (WA6; www.marketingpower.com/jm_webappendix) suggests that the correlations of instrumental variables with the associated endogenous variables are high, whereas those with other endogenous variables are moderate to low. Second, to ensure that our choice of instruments does not drive the directions of our results, we compare the observed average values of monetary value across the different baskets. The directions of these observed differences are similar to those from the results estimated through our simultaneous system. However, by accounting for endogeneity and simultaneity in our model, we can determine the correct magnitudes of the differences in monetary values across the baskets. Together with the theoretical arguments, these tests support the appropriateness of our instruments.

The instruments are exogenous or predetermined with respect to the variables studied. Nevertheless, to ensure complete independence from the variables, we estimated the model with values of the instruments from a matched sample of customers in the database. We used the propensity score matching method to select the matched sample, consistent with Rosenbaum and Rubin (1983). The results of this analysis, reported in the Web Appendix (WA7; www.marketingpower.com/jm_webappendix), are consistent with those reported in Table 6.

Operationalization of category characteristics as continuous variables

We test the robustness of our findings to alternative (continuous) measures of category characteristics. We generate continuous measures for each of the utilitarian, hedonic, and perceived risk characteristics for a customer's basket by averaging the scores of each characteristic across the product categories bought. For example, if a customer purchased only apparel and accessories and beauty and cosmetics, his or her hedonic, utilitarian, and perceived risk scores would be 4.72, 5.88, and 4.38, respectively. The results of the monetary value model from this analysis appear in the Web Appendix (WA8; www.marketingpower.com/jm_webappendix) and are consistent with our main model results.

Alternative definitions of multichannel customer

We perform robustness checks for alternative definitions of a multichannel shopper. First, we define a multichannel shopper as someone who shops across channels but within one specific category (e.g., shoes) and across firms. The results are largely consistent with those reported in Table 6. Second, we define a multichannel shopper as someone who shops across channels and across categories but within a firm. We discuss this analysis in detail in the previous section on extension and generalization of results to the store channel (see WA5 in the Web Appendix; www.marketingpower.com/jm_webappendix). Finally, we define multichannel shoppers as those who shop across channels within a category and within a firm. We use the same data as those in the previous robustness check. However, we classify a customer as a multichannel shopper if he or she purchased across channels within a given product category of the multiproduct retailer. The results are largely consistent with those reported in Table 6.

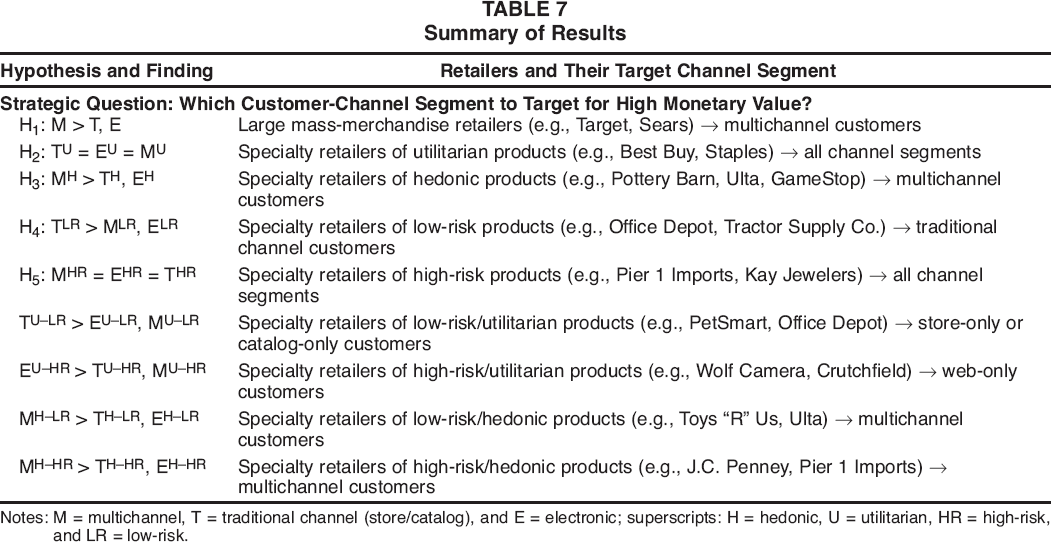

Implications

We summarize our findings in Table 7. Our main effect finding is that across product categories, an average multichannel customer provides higher monetary value than an average single-channel customer. As discussed in the “Conceptual Development” section, customers who prefer multiple channels may become more engaged in the purchase process as they shop across channels. Greater engagement may lead to more frequent purchases, a greater order quantity, greater spending, or a combination of all these outcomes.

Summary of Results

Notes: M = multichannel, T = traditional channel (store/catalog), and E = electronic; superscripts: H = hedonic, U = utilitarian, HR = high-risk, and LR = low-risk.

Importantly, our results show that product category characteristics moderate the relationship between channel preference and monetary value. The results of the two-way interactions show that the positive relationship between the preference for multiple channels and monetary value is stronger for hedonic product categories than for utilitarian categories. A plausible explanation is that hedonic product categories are likely to evoke impulse purchase and variety-seeking behaviors, and multiple channels provide greater opportunity and convenience to engage in those behaviors.

A key finding is that for low-risk categories, traditional channel customers have higher monetary value than other channel customers. This may be because low-risk product categories attract prevention-focused shoppers, who purchase mainly from traditional channels and spend more than their electronic and multichannel counterparts.

We also find that the perceived risk of a product category moderates the relationship between channel preference and monetary value for utilitarian product categories. A plausible rationale follows. According to RFT, for high-risk/utilitarian product categories, promotion-focused customers spend more in the web channel, whereas for low-risk/utilitarian product categories, prevention-focused customers spend more in the catalog or store channel. Because of the regulatory fit of their orientation with the product category and the channel, these customers spend more in the respective channels than their other single-channel or multichannel counterparts.

Theoretical Implications

We contribute to the literature in several ways. First, we extend prior research on the value of multichannel shoppers (e.g., Kumar and Venkatesan 2005) and offer new insights into the moderating effects of the product category on the channel preference–customer monetary value relationship. Contrary to conventional wisdom and prior research, we show that multichannel customers are not the most valuable segment for all product categories. Our results demonstrate that traditional channel customers of low-risk/utilitarian categories outspend multichannel customers and that web-only customers who buy only high-risk/utilitarian categories offer higher monetary value than multichannel customers.

Second, we extend prior research on the importance of product category characteristics on outcomes of managerial relevance. Prior research has examined the importance of category characteristics on variables such as unplanned purchases (Inman, Winer, and Ferraro 2009), category management (Dhar, Hoch, and Kumar 2001), sales promotion (Ailawadi et al. 2006; Narasimhan, Neslin, and Sen 1996), revenue premium (Ailawadi, Lehmann, and Neslin 2003), and spending during economically difficult times (Kamakura and Du 2012). We extend this research by showing the effects of product category characteristics on the relationship between channel preference and monetary value.

Third, we illustrate the importance of the utilitarian versus hedonic nature of a product category in determining the value of shopper channel segments. The finding that web-only (catalog- or store-only) customers spend more than multichannel customers on high-risk/(low-risk)/utilitarian categories suggests that the value of shopper channel segments depends on whether the category is utilitarian or hedonic. For utilitarian categories, it is highly efficient to shop in a single channel and realize the best value. However, for hedonic categories, customers shopping in multiple channels have multiple opportunities to spend, seek variety, or purchase on impulse. Our findings add to the literature on the importance of the utilitarian versus hedonic nature of product categories (Chitturi, Raghunathan, and Mahajan 2008; Dhar and Wertenbroch 2000; Inman, Winer, and Ferraro 2009).

Fourth, our findings highlight the role of perceived risk of a product category in determining the value of shoppers by their channel preference. The amount of money shoppers spend on a product category in their preferred channel depends on their perceptions of the risks associated with the category. These findings supplement prior conceptual and empirical research on consumer behavior in different channels (Balasubramanian, Raghunathan, and Mahajan 2005; Van Noort, Kerkhof, and Fennis 2008; Yadav and Varadarajan 2005b).

Fifth, our results suggest important implications for the interaction of perceived risk with the utilitarian nature of the category. The finding that a single-channel segment offers higher monetary value than the multichannel segment and the result that different single-channel segments provide higher monetary values of utilitarian categories for different levels of risk suggest that there are some commonalities but important differences in the underlying mechanism that may induce high spending. Because utilitarian categories are typically associated with a prevention focus, consumers may be emphasizing purchasing efficiency, which is better realized in a single channel than in multiple channels. Consequently, single-channel customers of utilitarian categories may be buying more items at higher spending levels. However, at the same time, if the risk levels are high, promotion-focused consumers using the web can obtain more information and buy utilitarian items more often with higher spending levels than those using other channels. In contrast, if the risk levels are low, prevention-focused consumers can routinize their shopping and spend more on traditional channels (e.g., catalog, store) than on other channels.

Managerial Implications

The results offer several actionable managerial implications. First, managers can use the finding about the direct effect of channel preference on monetary value to make channel-specific investments. Our finding reveals that in general, multichannel customers who buy in multiple categories are most valuable, so retail firms that sell multiple product categories (e.g., mass merchandisers such as Target and Sears) should induce multichannel customers to buy more by investing in all the channels.

Second, specialty retailers of hedonic products, such as Pottery Barn, Ulta, GameStop, and J.C. Penney could incentivize their single-channel customers to shop in other channels, because our findings show that multichannel shoppers provide the highest monetary value for such products. Shopping in multiple channels provides shoppers with more opportunities to indulge in favorable experiences offered by hedonic products, increasing their spending on those products. For example, when a web-only shopper purchases a fashion clothing item on the web, a retailer such as J.C. Penney could invite that shopper to visit its brick-and-mortar store by offering a gift or a preferred item at a discount that can be collected only at the store. When the shopper visits the store to pick up the item, he or she might try more hedonic products, perhaps prompting the purchase of more items.

Third, our results show that traditional channel customers of low-risk categories provide high monetary value due to a strong channel–category fit in prevention focus. Specialty retailers of low-risk products (e.g., Office Depot, Tractor Supply Co.) could induce traditional channel customers to spend more at their physical stores or through their catalogs by emphasizing items that are consistent with prevention focus. They could group similar products (e.g., surge protectors with cables and batteries, livestock feed with dog food and dog collar) through displays at the physical stores or in catalogs to remind prevention-focused customers to buy more items on each purchase occasion.

Fourth, our findings demonstrate that traditional channel customers of low-risk/utilitarian products spend more than other customers. Specialty retailers of low-risk/utilitarian products (e.g., Office Depot, PetSmart) could help traditional channel customers routinize their shopping and purchase more efficiently and repeatedly at their stores or through their catalogs. They could track the purchase histories of these customers and prompt them to buy more of the same items on a periodic basis.

Fifth, our findings reveal that electronic channel customers of high-risk/utilitarian products tend to outspend other customers. Specialty retailers of high-risk/utilitarian products (e.g., Wolf Camera, Crutchfield) could make their websites “sticky” through features such as single-click ordering, product reviews, and new item recommendations. In this way, these retailers could make it convenient for promotion-focused customers who typically prefer the electronic channel to continue shopping and spend more in their preferred channel.

Sixth, specialty retailers of high-risk/utilitarian products could also educate their prevention-focused customers who prefer to shop through catalogs or at physical stores about the high trust levels at their websites. In this way, marketers can help such customers reduce their risk perceptions and buy more from the web channel. For example, the staff at a Best Buy store could provide reassurance to prevention-focused store customers by demonstrating the ease and trustworthiness of ordering online through computers at the store and by enabling them to purchase online. Customers who become accustomed to the online channel might shop for more high-risk/utilitarian items online, leading them to provide a higher monetary value in the future.

Seventh, retailers could use the insights from our research to make more effective targeting decisions. Our findings imply that retailers of hedonic product categories (e.g., J.C. Penney, Pottery Barn, Pier 1 Imports) should target multichannel customers. The results also suggest that retailers of low-risk/utilitarian products (e.g., Office Depot, Tractor Supply Co., PetSmart) should target customers who prefer traditional channels. Similarly, retailers of high-risk/utilitarian products (e.g., Best Buy, Wolf Camera, Crutchfield) should target competitors’ web-only customers for switching and offer incentives to their own web-only customers to enhance retention.

Limitations, Further Research, and Conclusion

This study has limitations that further research could address. First, we examined observed purchase behavior. We do not have data on how customers use the channels for information search. Although such data are difficult to collect, analyzing them together with transaction data could shed additional light on single- versus multiple-channel shopping, extending the work of Verhoef, Neslin, and Vroomen (2007).

Second, if data on customer referrals are available, our model of customer value could be expanded to include referral value, extending Kumar, Petersen, and Leone's (2010) study to the multichannel context. Such an analysis could provide a richer understanding of customer value.

Third, if data on price promotions are available, an investigation of the differences in the effectiveness of price promotions across different channel shoppers would be a fruitful research avenue. Such an investigation would provide a deeper understanding of the role of discounts in creating differences in monetary values by channel preference.

Fourth, if longitudinal customer purchase data on a broad array of categories across firms are available, a deeper analysis of channel switching across product categories could be undertaken to obtain greater insights into multichannel shopping. Such an analysis would offer a nuanced understanding of changes in monetary values due to channel switching.

Fifth, although our conceptual arguments are rooted in individual motivation, we use behavioral outcome data (spending)—not data at the decision process level. Supplementing our study with behavioral experiments at the individual level would bolster the validity of the findings.

Finally, with the surge in the sales of mobile devices, such as smartphones and tablets, customer use of the mobile channel is growing rapidly. As data on mobile channel become available, it would be useful to extend our study to the mobile channel.

In conclusion, contrary to conventional wisdom that all multichannel customers are valuable, our results show that multichannel customers are the most valuable segment only for hedonic product categories; single-channel customers of utilitarian categories and traditional channel customers of low-risk categories provide higher monetary value than other customers. The results reveal that for utilitarian product categories involving high (low) risk, electronic (traditional) channel shoppers constitute the most valuable segment. Our findings offer managers guidelines for targeting and migrating different types of customers for different product categories through different channels. They also serve as an impetus for further research on the growing phenomenon of multichannel marketing.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.