Abstract

Lateral exchange markets (LEMs) are sites of technologically intermediated exchange between actors occupying equivalent network positions. To develop an enriched understanding of these markets, the authors develop a more broad-based and differentiated understanding of peer-to-peer, sharing, and access-based markets. They focus on two key axes: the extent of (1) consociality and (2) platform intermediation. Drawing on these attributes, the authors theoretically deduce four ideal types—Forums, Enablers, Matchmakers, and Hubs. Each type provides value in a different way: Forums connect actors, Enablers equip actors, Matchmakers pair actors, and Hubs centralize exchange. Twenty organizational cases reveal insights into the failure, adaptation, and success of LEMs. Lateral exchange markets shift responsibility for personal and exchange security to relevant personal actors, to institutions, or to the governing algorithms of technology platforms. Extending the general proposition that sociality increasingly infuses market logics, the findings suggest a new frontier in which social resources and software platform algorithms interact as operand resources whose negative consequences (e.g., opportunism) require careful management through assurances and institutional arrangements matched to the type of LEM operation.

Keywords

The rapid growth of peer-to-peer markets is inescapable. Indeed, a sizeable majority of U.S. adults have already used them (Smith 2016). However, there are many gaps in our understanding of these markets. First, we have no general agreement about what to call them. Belk (2014, p. 1595), mentioning companies such as Airbnb, Zipcar, and Freecycle, groups these and other “related business and consumption practices” under the umbrella term “the sharing economy”; yet Arnould and Rose (2016, p. 80) argue that the use of the term “sharing” obscures the economic status of the markets. Second, research thus far has investigated only particular kinds of peer-to-peer markets. For example, in their study of Zipcar consumers, Bardhi and Eckhardt (2012, p. 881) focus only on “access-based consumption,” defining it as “transactions that may be market mediated in which no transfer of ownership takes place.” Another study, Benoit et al. (2017, 219), focuses only on “collaborative consumption” and concludes that platform providers’ “main role is matchmaking.” Because only particular manifestations of these markets, such as those involving access-based consumption or collaborative consumption, have been studied, we still know very little about the breadth and diversity of the general phenomenon or about how generalizable conclusions gained studying one type of consumption might apply to other types. Third, because prior studies have been limited in scope, they have been unable to compare different types of markets. Thus, we have very limited understanding about the underlying characteristics and relative effectiveness of different forms of peer-to-peer markets.

To address these research gaps, our article offers an improved conceptualization of the phenomenon, develops an empirically based typology, and explains how understanding the differences between types of peer-to-peer markets can lead to better marketing theory and managerial practice. Our core research questions aim to clarify the conceptualization and definition of these markets and to specify their general principles. How can we best understand these new markets and the various forms in which they manifest? What are some of their most important underlying characteristics? How do the different types compare in effectiveness? How do these aspects affect our theorizing and management? We answer these questions by first defining and differentiating our core conceptual contribution, lateral exchange markets (LEMs), and providing a typology. We subsequently map configurations of successful and unsuccessful peer-to-peer businesses onto the typology. Finally, we discuss how our findings alter, guide, and extend extant understanding and managerial practice.

Theory

Defining and Differentiating LEMs

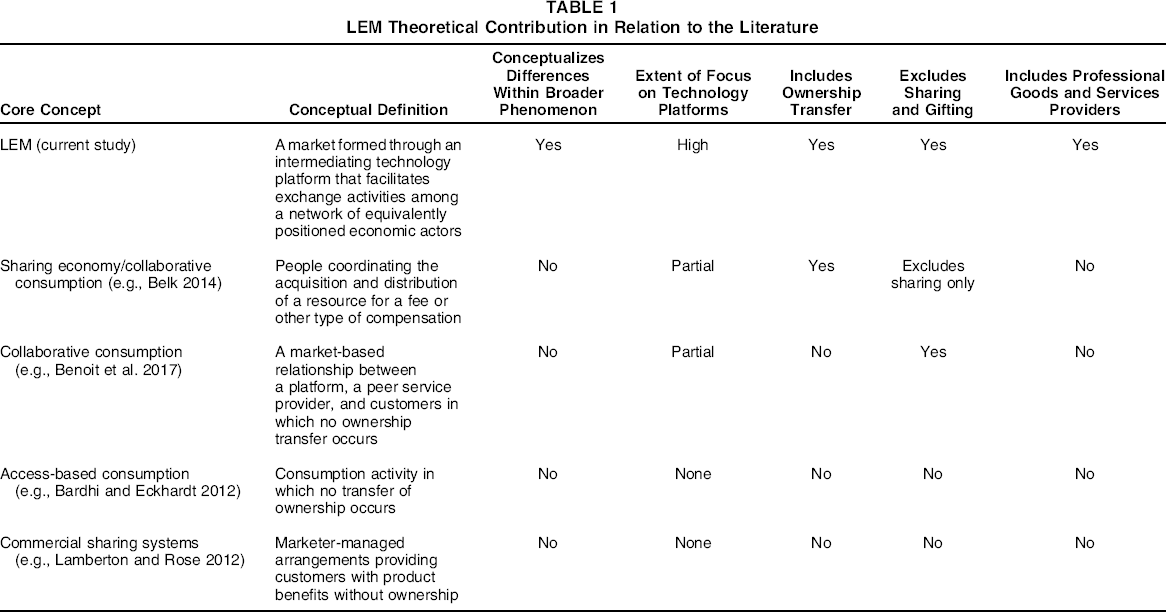

To make a coherent contribution to our understanding of these markets, we must first clearly differentiate, specify, and define our focal concept, which is the use of a technology platform to connect a network of economic and social actors. This phenomenon, or aspects of it, has been given many different names, including “the sharing economy” (Belk 2014), “collaborative consumption” (Benoit et al. 2017), “commercial sharing systems” (Lamberton and Rose 2012), and “access-based consumption” (Bardhi and Eckhardt 2012). Table 1 specifies the definitions of these concepts and distinguishes them from our article's core concept of LEMs.

LEM Theoretical Contribution in Relation to the Literature

Our comparison is intended to advance more coherent conceptual thinking. Although prior studies have attempted to understand a fairly broad phenomenon, they have failed to distinguish and conceptualize important differences within it. Furthermore, the emphasis on technology platforms is limited. Belk (2014, p. 1595) calls the sharing economy a phenomenon “born of the Internet age” and refers to such companies as founded on “disruptive technologies” (p. 1599), and Benoit et al. (2017) develop platform providers as a medium of connection; however, neither of these articles makes technology platforms, or their social affordances, central to their conceptualization. Belk (2014) includes transfers of ownership, such as the sale of property, in the sharing economy, but all the other concepts exclude them. However, we see no reason to exclude markets that facilitate sales between peers (e.g., eBay) from a more general conception of the sharing economy. In addition, some of these concepts include sharing and gift giving, which take place outside conventional financial markets, whereas others exclude them.

We question the use of the term “peer” to refer to these market types, because they often include professional sellers and buyers. For example, a 2014 report based on New York City records revealed that professional property owners and managers made 37% of all revenue on Airbnb (New York State Office of the Attorney General 2014). In a study of its drivers, Uber found that 18% of them were professionals who previously or concurrently drove taxis or limousines (Uber Newsroom 2015). Given the importance of professionals to these networks and the lack of recognition in prior conceptualizations, we believe it is advisable to avoid the implication of amateur status accompanying the use of the term “peer.” Instead, we use the term “lateral exchange” to signify exchanges occurring between actors at equivalent levels. Even though some of the actors in a given network might be professionals, whereas others might be amateurs, their participation through the exchange platform renders the two groups roughly equivalent. For example, one specific Uber driver can play the same role on the company's platform as any other. A driver can also be a customer of Uber, and vice versa.

Therefore, in contradistinction to prior conceptualizations, we aim to build a general understanding about these markets that conceptualizes them as (1) a broad marketplace phenomenon with internal differences, (2) a manifestation of technology platforms linking actors, (3) including the possibility for exchange of ownership and not merely access, (4) excluding sharing and gifts, and (5) including both amateur (“peer”) and professional actors. We define a lateral exchange market (LEM) as a market that is formed through an intermediating technology platform that facilitates exchange activities among a network of equivalently positioned economic actors. Our conception emphasizes the important role of both platform and network actor; spotlights commercial exchange; and includes buying, selling, renting, trading, bartering, and swapping. However, as we explain in the following subsection, although we exclude gifting and sharing from LEMs, this does not mean that we neglect the social nature of these exchanges.

LEMs Are Technological, Economic, and Social Exchange Systems

Contemporary markets such as LEMs are “social arenas where firms, their suppliers, customers, workers, and government interact” (Fligstein and Dauter 2007, p. 107), influencing the creation, distribution, and consumption of goods and services by human, material, and technological actors. Lateral exchange markets are a new form born of the potential of contemporary digital technology to coordinate and monetize networks. Because their technology platforms combine social actors into various exchange-related configurations, LEMs do not fall neatly into existing categories but create new legal categories and institutional practices. As such, the nature and governance of their “hybrid and ambiguous status” (Arsel and Dobscha 2011, p. 66) is unclear.

Our approach builds on Adler's (2001) important insight that the increasingly knowledge-based economy is leading to hybrid market forms that differ in fundamental ways from market forms of the past. Adler (p. 218) proposes that many of these “knowledge economy” hybrids use methods of “community-based governance,” conceptualized as “a third coordination mechanism that can be combined in varying degrees with price and authority.” Although not an explicit focus of this article, we are cognizant of the manner in which the introduction of new forms of business creates crises in moral, cognitive, and pragmatic legitimacy (Coskuner-Balli and Ertimur 2017) that are often settled with changes to the regulative legal system (Denegri-Knott and Tadajewski 2017). In the following two subsections, we explore two elements of these changes in the way markets coordinate buyer and seller behavior.

Managing Sociality in LEMs

Complex social relationships embed value creation in any market (Lusch and Vargo 2014; Vargo, Wieland, and Akaka 2015). Arnould, Price, and Malshe (2006, p. 94) include “networks of relationships” that encompass traditional relationships such as families and ethnic groups as well as emergent ones such as consumer tribes and brand communities as “social operant resources.” The purpose of this subsection is to clarify how recognizing different forms of social operant resources can enhance our understanding of LEMs. We do this by defining sociality and consociality and explaining how they are relevant to LEMs.

Sociality is a term used to refer to people's universal tendency to associate in groups and to form cooperative relationships with other people (Wittel 2001). Sociality can be distinguished from Schutz's (1962) notion of “consociality,” which refers to a state in which two or more people are copresent in space and time. Hannerz (2016, p. 151) extends this notion to a contemporary frame in which “consociality is defined by co-presence of both—or either— physical and virtual [interaction].” We thus define consociality as the physical and/or virtual copresence of social actors in a network, which provides an opportunity for social interaction between them. We recognize that the rules governing social interaction are institutional—that is, governed by procedures and norms such as current cultural practices, public opinion, legal systems, and certification and accreditation bodies (Scott 1995).

The technological elements of LEMs, which bring people together to create value, also create new forms of social connection and experience and, thus, new types of social operant resources. Wittel (2001, pp. 71–72) terms this new, network-based form of social connection “network sociality,” describing it as “deeply embedded in technology; it is informational, ephemeral but intense.” Rainie and Wellman (2012) also find “networked individualism” to be more individualistic and opportunistic than traditional sociality. Miller (2008, p. 390) suggests that this type of sociality is “an instrumental or commodified form of social bonding based on the continual construction and reconstruction of personal networks or contacts” (Arvidsson and Calliandro 2015; Cova and Pace 2006, p. 1101).

Lateral exchange markets facilitate different kinds of social relationships. Network actors sometimes participate in novel social situations, such as sleeping in someone's spare bedroom through Airbnb, or using SnapGoods to lend their power tools to a stranger for a fee. These novel situations are social, but they are also instrumental, commodified, opportunistic, intermediated, and ephemeral. There are situations in which the closeness of sharing a room, a ride, or a set of messages can also inspire communal feelings of affability, friendliness, and social satisfaction (Dyck 2002). In related studies of online businesses, trust is sometimes linked to sociality. Examining the successful provision of services online, Gefen and Straub (2003, p. 8) find that providing “socially rich exchanges” has a positive effect “on consumers’ trust and on their subsequent intentions to purchase services.” These findings lend support to the notion that LEMs might employ these new and different forms of sociality as a form of what Adler (2001) terms “community-based governance.” In this article, we distinguish between types of LEM on the basis of the ways that their varying combinations of virtual and in-person social interactions influence trust and govern exchanges. In the following subsection, we highlight another important source of difference, the technological intermediation of the platform.

Managing Exchanges in LEMs

In addition to influencing trust using sociality, LEM companies have added opportunities to manage exchanges using technology platforms. Trust in a technology platform assumes many forms, including (1) trust in the platform itself, as with Lu, Wang, and Hayes's (2012) study of a consumer-to-consumer e-commerce site; (2) trust in reputation-based algorithms, as Aberer and Despotovic (2001) theorize in their research about managing trust in peer-to-peer environments; and (3) trust in the objectivity of computer algorithms, which, as O'Neil (2016) demonstrates, can be blind to faults in these heuristics. Lateral exchange market buyers and sellers usually have no prior experience with one another and occupy roughly equivalent positions in the network. Platform intermediation therefore plays an important role in mitigating duplicity, incentivizing trustworthy behavior, and inspiring trust in the exchange. We term this element “platform intermediation” and define it as the deployment of a software platform and its various digital tools as an intermediary that manages and coordinates the exchange between network actors. In our “Lateral Exchange Markets” section, we investigate the extent to which software platform and consociality effectively intermediate lateral exchanges and influence market outcomes. Next, we describe the method we employed for our study.

Method

Data Collection

This article was the result of a six-year-long multisite “market-oriented” ethnographic investigation (Arnould and Wallendorf 1994). The ethnography included participant observation, interviews, and netnography. Online netnographic activities followed the guidelines of Kozinets (2015) and were interrelated with the ethnography. We collected screenshots, news articles, press releases, and other data from 193 LEM platforms, resulting in 2,168 pages of collected data. To be included in our data set, the platform or site needed to use networked technology to organize exchanges and serve as an intermediary between actors at equivalent network positions. Accordingly, we excluded firms that did not use networked technologies (e.g., a local flea market) or that served as an online intermediary between traditional business enterprises and individuals (e.g., listings for local businesses such as Angie's List). We provide a list of the original 193 cases in the Web Appendix. The Web Appendix also highlights the 31 LEMs within which we engaged in ethnographic participant observation.

Over a six-year period from 2010 to 2016, the first author ethnographically engaged with 31 LEM platforms and generated 650 pages of field notes about the accompanying experiences. Lateral exchange market participation included buying and selling merchandise, hiring labor, renting vehicles, using ride-share services, staying in homes, trading electronics, and swapping household items. In situ interviews, included in the field notes, were supplemented with an additional 31 interviews with university students who actively participated in LEMs. Interviews were relatively short and focused by consumer research standards, lasting from 10 to 40 minutes in duration. They were recorded and subsequently transcribed, resulting in an additional 228 pages of data.

Two Stages of Data Analysis: Typology Development and Principle Observation

Our intention in this article is (1) to advance understanding by providing an organized typology of contemporary LEMs and (2) to explain, using data, how different structuring elements work in practice to provide different LEM outcomes. Our research protocol had two corresponding stages. In the first stage, we examined a large number of LEMs and began coding them and discussing their common elements and differences. We used numerous different descriptors and ideas to help explain the patterns we began to observe across different LEMs. As we collected more data and held more discussions, we dropped initial ideas (such as peers, collaborative consumption, ecosystems, extent of interaction, sociopetal systems, and social commerce) in favor of other ones (such as lateral exchange, sociality, and consociality). We sought negative cases and revised or abandoned theoretical notions on the basis of whether they fit. We subsequently used those dimensions to construct an ideal type classification. The purpose of an ideal type is to provide an abstract ideal or typology against which actual occurrences of a phenomenon can be compared (Blalock 1969). Thus, in our second stage, we collected additional data from 20 LEM cases and then examined, classified, and organized them into findings. Table 2 provides a description of the selected 20 firms along with information on industry, scope, founding year, and similarity to ideal type. This type of systematic comparison of actual cases to ideal types is commonly used across the social sciences (e.g., Kvist 2007).

Reduced Set of 20 Cases Selected for Ideal Type Interpretive Data Analysis

Platform failures: no longer operational as of October 2016.

To analyze this more detailed data about a smaller number of cases, we followed the comparative process described by Stake (2006). Throughout, we followed a process of induction, developing “a causal model built by someone like a forensic pathologist, a detective or an historian, using a progression of inferential analyses to run an evidential trace out to its end point” (Miles and Huberman 1984, p. 329). We systematically compared case data and emergent framework until our theoretical position was both internally consistent and externally able to accommodate both new entries to the industry and novel events occurring in a constantly changing empirical field. During the multiple rounds of combined ethnographic data collection and analysis over the six years of the project, we returned to our field sites to investigate, gather additional details, seek nuance, and find disconfirming evidence. Throughout, our research focus was “informed by a variety of shared communications, observations, and formal or informal hypotheses and generalizations” (Belk, Fischer, and Kozinets 2013, p. 168). Our procedure is in keeping with accepted principles of mainstream qualitative data analysis and interpretation. We next turn to our findings, which explore the underlying structure of LEMs.

Lateral Exchange Markets

The Underlying Structure of LEMs

Results of the Analysis

Our analysis of 193 LEM companies reveals two structural patterns. First, LEMs are distinguished by the implementation of platform intermediation. Second, the form of the LEM has the effect—intended or not—of variously constricting or facilitating consociality between network actors. These two dimensions serve to effectively classify and explain the general principles behind LEMs. We devote the remainder of this section to explaining and illustrating these principles.

Extent of platform intermediation

All LEM companies intermediate exchanges using a software-based technology platform. There are, however, differences in the extent to which the technology platform, rather than the exchange partners, is involved in the exchange process. Our typology's first organizing dimension, platform intermediation, surfaces from observations regarding the varying extent to which the software platform and its attendant algorithms and tools manage and coordinate exchanges. Freecycle is an example of an LEM in which the extent of platform intermediation is low. Freecycle provides a basic central website connecting those who wish to give away various sorts of used goods (such as old televisions or furniture) with those willing to pick up these goods. Freecycle provides a message board platform and a set of guiding rules but offers little else to manage the exchange. Under the supervision of local board moderators, human actors communicate, negotiate, organize, complete, and oversee their exchanges, relying on the board's rule set as well as their own guiding norms.

At the other end of the platform intermediation spectrum are companies whose platforms coordinate, monitor, and regulate almost every element of their network's exchanges. The car rental LEM Turo has high platform intermediation. It has a very strict screening process for car renters. Furthermore, it offers these renters several structural reassurances, such as high-quality service and product standards, extensive reviews, customer service (including 24/7 roadside support), and $1 million in included liability insurance. Some of these elements can be conceived as legitimate forms of technical rationality that network actors perceive or assume to be “desirable, proper, or appropriate” (Suchman 1995) within the LEM system.

Extent of consociality

Across LEMs, there are important differences in the extent to which they allow or constrain consociality. Some LEMs permit relatively free-flowing interactions as actors communicate, negotiate, and coordinate, resulting in (perhaps unintended) social benefits. For example, the ride-sharing service, Lyft, exhibits high consociality. A passenger booking a ride in on the Lyft app sees a photograph of their driver and learns about his or her hometown and musical tastes. On entering the vehicle, the passenger is greeted by a glowing electronic mustache displaying a greeting featuring the passenger's name. The Lyft driver often offers bottled water and chewing gum and asks about the rider's day, reciprocally inviting conversation. At the end of the ride, payment occurs automatically and invisibly. Afterward, the app prompts the rider for a quality rating and offers several options to tip the driver. On its website, Lyft (2012) claims to have “produced thousands of friendships and even one marriage.”

Occupying the low-consociality end of the spectrum are LEMs that minimize or even eliminate social interaction between network actors. Lending Club allows actors to invest in the loans of other network actors, but it anonymizes lenders and borrowers, providing no opportunities for communication or social interaction. Interestingly, some LEM loan companies offer higher consociality formats. Prosper.com provides borrowers with “a voluntary open-text area” that network actors can use to communicate an “identity narrative” that has positive effects on loan funding; however, this can also lead to deception (Herzenstein, Sonenshein, and Dholakia 2011, p. 139). Whatever the format, it is noteworthy that although the LEM provides opportunities for social behaviors, the enactment of those behaviors is optional and may not occur.

Crossing the two dimensions

Crossing extent of platform intermediation with extent of consociality yields four distinct market configurations for lateral exchange: Forums, Enablers, Matchmakers, and Hubs. Managing software interface and copresence enables LEM companies to transform equivalently placed network actors’ “microspecialized competences” (Lusch and Vargo 2006, p. 415) into legitimate service exchanges. Figure 1 illustrates these four types.

Lateral Exchange Market Types

Four Types of LEMs

Distinct value propositions of LEM types

Each LEM type represents a specific configuration of a service ecosystem (Vargo, Wieland, and Akaka 2015). Forums, Enablers, Matchmakers, and Hubs act as intermediaries that contribute to between-actor value creation by offering distinct value propositions through sociality and technology deployment. As intermediaries, LEM firms offer two potential benefits: they create the market and lower transaction costs. In this section, we detail the structure and process that each LEM type uses to offer these benefits to network actors.

Forums connect actors

Forums are LEM configurations that facilitate the flow of services directly between actors (actor ↔ actor), providing low platform intermediation and high consociality. Carpool World, a company that provides drivers and passengers with carpool matching software, is a good example. Carpool World's software platform performs one basic task: enabling interested individuals to contact and meet new people who may have matching transportation needs or abilities. Carpool World's platform creates the market. Everything else—the communication and coordination involved in making the actual carpool happen—is left up to the network's actors. Of course, because passengers and drivers share time and space together during carpool rides, copresence and consociality is high. Service provision at Carpool World flows directly between actors as they coordinate and negotiate schedules, locations, and payment terms. This example shows that forums lower the search costs that actors incur when trying to find each other in a broad and disorganized market. Consequently, the core value proposition of a Forum LEM is to connect actors.

Enablers equip actors

Enablers are configured to help individual actors provide services to other actors (LEM firm → actor → actor). They have relatively low levels of platform intermediation (i.e., they minimize use of their technology platform to coordinate the transaction) and low levels of consociality. An example of this Enabler type is Poshmark, a company through which new and used fashion goods are sold and traded. Poshmark does not handle the exchange itself but instead equips actors for exchange using a smartphone-based software application. The app simplifies the act of photographing, describing, and listing items for sale. For example, the app offers different categories and shopping themes to organize the listing. The app also produces addressed, prepaid shipping labels to print and place on packages. Typical of the Enabler type, little or no direct interaction or communication occurs between Poshmark's buyers and sellers. Enablers such as Poshmark lower search costs as well as decision costs, such as resources expended evaluating terms and assessing expected performance. As a result, the core value proposition of an Enabler LEM is to equip actors for service provision.

Matchmakers pair actors

Matchmakers mediate the service flow between providers and beneficiary actors (actor ← LEM firm → actor) and are characterized by high platform intermediation as well as high levels of consociality. An example of a Matchmaker type is DogVacay, a company that matches pet owners with animal caregivers. DogVacay's platform employs a quality control process that includes interviews, training, and reference checks on potential caregivers. It also handles the payment and provides pet insurance, a money-back guarantee, and 24/7 customer support. Pet owners and caregivers are encouraged to learn about and communicate with each other, and the company requires active caregivers to provide daily photo updates featuring the pet. In addition to lowering search and decision costs, Matchmakers such as DogVacay lower the surveillance costs that usually result from monitoring other actors (e.g., by requiring daily photo updates). The core value proposition of a Matchmaker LEM comes from providing a pairing of exchange actors.

Hubs centralize and standardize service flows

Hubs act as the central point in the exchange, resulting in two discrete and bidirectional flows between platform provider and actors (actor ↔ LEM firm ↔ actor). Combining high platform intermediation with low consociality, this configuration hides the service flow between equivalent actors behind its own platform. Lending Club, introduced previously for its constrained consociality, is a strong example of a Hub type. Prospective borrowers apply for loans online, and Lending Club's technology leverages its own algorithms, along with available credit data, to assess their risk level and assign them corresponding interest rates. On the other side of the exchange, investors use Lending Club's platform to build diversified loan portfolios that earn monthly returns based on differential levels of borrower risk. The service flows directly between borrowers and Lending Club and investors and Lending Club, with borrowers and lenders never interacting directly. Hubs such as Lending Club lower search, decision, and surveillance costs as well as the enforcement costs that arise from ensuring that actors meet performance expectations. Thus, the core value proposition of a Hub LEM is to centralize and standardize service flows. With the different value propositions of the four types of LEM explained, we next turn to a detailed examination of the empirical enactment of their general principles.

Empirical Cases and General Principles

Cases Illustrating Complexity, Competence, and Collapse

Contemporary business is far more complex and dynamic than our models can accommodate. This fact explains why we need to empirically explore simplifications such as typologies to comprehend the current market landscape. In this section, we examine eight cases—two from each LEM type. Four of these LEMs are successful and four have either failed or been forced to change radically. As a starting point, we offer Figure 2, which categorizes each of our 20 detailed LEM cases within an ideal type classification and dimensionalizes them in terms of their consociality and platform intermediation. Our findings benefit from the contextual richness of our ethnographic method to demonstrate and organize the empirical complexity of LEMs. In the following four sections, we again visit each of the LEM types in turn, closely examining one successful case and one failure for insight into their general operating principles.

LEM Companies Categorized as Types

Forum Cases

Forums as social markets

The Forum LEM type is distinguished from the other types by having the most social user experience, wherein individual actors organize many aspects of their exchange. The social experiences in this platform type are often characterized by offline in-person meetings (e.g., picking up goods from someone's home, riding in someone's car). Because Forum exchanges are unmediated by the LEM company and its platform, trust is rooted in interpersonal social exchange, which includes virtual communication. We discuss these elements with two case study examples, Craigslist and Zimride. Craigslist is one of the longest-running LEMs, but it has been plagued by safety and trust concerns. Zimride, after limited initial success, revamped its platform and business model, providing a useful negative case example.

Craigslist

Craigslist is a well-known bulletin board site that typifies the Forum LEM configuration. Founded in 1995 as an email distribution list between friends, the platform currently has operations in 70 countries. Craigslist provides a central location for actors to connect in order to fill and find jobs and housing, sell and trade goods and services, look for romance and friendship, and much else. Employing a sparse, utilitarian design that relies on the individual content of its users, Craigslist is a decentralized system with minimal platform intermediation.

Craigslist relies on high levels of consociality to mitigate trust concerns and encourages network actors to “deal locally with folks you can meet in person—follow this one rule and avoid 99% of scam attempts” (http://www.craigslist.org/about/scams). However, personal meetings for the purpose of exchange entail heightened personal risk. Rules of conduct are mostly implicit. In recounting their exchange experiences on Craigslist, our interview informants related numerous uncertainties about the norms governing the exchange: “When should the money be exchanged? Should the item be inspected first? Is it okay to negotiate the price?” (personal interview, March 2013).

These uncertainties lead to continuing challenges for Craigslist users. However, this level of ambiguity is typical for the Forum configuration. Craigslist delegates exchange responsibility to individual actors and devotes a prominent section of its site to tips about avoiding scams and ensuring personal safety. Some Craigslist users also assume a role as the platform's watchdogs by monitoring posted content and flagging posts for positive reasons (i.e., “best of Craigslist”) or flagging for removal those that are prohibited or suspect. However, much of the controversy surrounding Craigslist comes from the unintended side effects of its consocial affordances, which actors have used to promote services such as prostitution and which have been linked to 101 murders (Dewey 2016).

Zimride

When it was founded in 2007, Zimride originally offered its ride-sharing service only to university students to share their rides back home with other students. Zimride's origins in university carpooling meant that a social experience was part of the service's appeal. Emphasizing consociality, the platform connected people who shared Facebook friends, worked at the same company, or attended the same school. The platform even aimed to match people with similar smoking preferences and musical tastes (Carpenter 2011).

Zimride expanded from a university market to serve business clients, and then the general public (Yu 2012), eventually launching the first public ride-sharing app called “Lyft” in May 2012. Desperately seeking profitability, the company began offering many different options. Payments could be processed directly by the Zimride platform or cash could be used. In either case, Zimride did not offer refunds or any other guarantees. The company claimed to provide driver and rider verification; however, this procedure did not include actual background screening but required only a working email account (Lobel 2016).

Zimride struggled for several years because it failed to operate coherently as an LEM Forum. It had created an LEM company that had both high intermediation (payment processing and oversight) as well as low intermediation (cash payments and minimal oversight). It fostered mistrust by offering the copresence of a shared ride to the general public, offering safety assurances and then failing to properly vet riders and drivers. As a result, the company could not sufficiently monetize the value-adding connections it enabled.

In 2013, the company sold most of its assets to Enterprise Rent-a-Car. Enterprise renamed the company “Zimride by Enterprise” and promptly addressed its security concerns by closing public access, offering stronger background checks, and centralizing reviews. The company clarified the payment situation with stronger platform intermediation—cash payments were no longer allowed. With stronger platform intermediation and better management of the risks of copresence, Zimride by Enterprise became a viable LEM business.

Enabler Cases

Equipping actors for trustworthy exchanges

Enablers provide a group of network actors with a marketplace, equip them in different ways, and set broad exchange rules. However, they do not enforce those rules, leaving execution to network actors. With low consociality and low platform intermediation, gaining actors’ trust can be problematic. Although many Enablers offer some way for actors to communicate with each other (e.g., comments section, direct message, user forums), most transactions are processed with limited communication. To illustrate and develop our understanding of this LEM type, we present findings from a successful example, Kickstarter, and thredUP, a firm that failed as an Enabler but later reinvented itself as a Hub.

Kickstarter

Kickstarter is a crowdfunding platform for creative projects such as films, art and performances, books, music, video games, and gadgets (Mitra and Gilbert 2014). This firm has been successful and influential, funding over 100,000 projects with more than $2 billion pledged (Kickstarter 2017). The system is decentralized, with minimal involvement in and coordination of the transaction. However, Kickstarter's platform provides a template for project creations that standardizes the creative project's promotion. Creators use the provided templates to build their project pages, shoot videos, brainstorm rewards for financial backers, set funding goals, and choose deadlines. When completed, the crowdfunding page can be shared and promoted to financial backers both on the platform and through other social media.

Just as Craigslist manages the risks of its low platform intermediation by educating actors, so, too, does Kickstarter. Kickstarter offers a “Creative Handbook” as a guide to educate creators about the best practices to produce videos and create sponsor rewards as well as how to design, manage, and advertise their projects. The Kickstarter website boasts that each project is independently created and explains that actors have “complete control over and responsibility for their projects”; the firm further clarifies its role as “a platform and a resource” and advises that it is not involved in the development of the projects themselves (Kickstarter 2017). The lack of direct involvement in project development, promotion, and management, as well as dispute resolution, is relevant to our classification and understanding of the firm as an Enabler type.

Consociality is constrained on Kickstarter. However, social presence remains salient. Rather than permitting interaction between creators and financial supporters, potential backers are directed to provide creators’ profiles, which include records of prior project funding. Although avenues for more extensive interaction between actors are available, a type of “para-social interaction” (Horton and Wohl 1956) develops, similar to the one-sided attachment felt between fans and celebrities. For example, our netnography studied several Kickstarter campaigns, including “Lucky Girl,” a popular indie pop-folk artist who had already had several small hits. She was appealing to the Kickstarter community to help fund her new solo record. “Backed by a very friendly video where she shares her life struggles with motherhood and surviving cancer, she explains that, now that her kids are out of babyhood, she is ready to ‘reclaim something, some sense of myself as my own person.’” (Author fieldnotes, May 2016). Although there was very little communication between other network actors and Lucky Girl, she exceeded her funding goals, raising over $53,000 in near-record time.

The Lucky Girl campaign illustrates how network actors take full advantage of the platform's interface to create a social identification within the Enabler's less interactive format. Those asking for creative funding will use their personal values and identity cues (such as being a talented artist and struggling mother) to create a sense of identification and spur alternative forms of connection. Project backers on Kickstarter learn about creators’ backgrounds by reading their bios and project narratives, visiting their websites, and examining whether their previous projects have been backed. Although Kickstarter may be low in copresence, Mitra and Gilbert's (2014) research suggests that skillful use of language is an important element, with the use of socially charged phrases predicting significantly greater funding success.

thredUP

Founded in 2009, thredUP was originally set up as an online swapping platform for men's shirts. However, this turned out to be a limited market. Beginning a long line of pivots, the company moved toward a focus on men and women's shirts, and then settled on children's clothing. In a 2010 press release, the company described its offering in this way: “thredUP kids combines the best features of some of the most popular sites on the web: Like Netflix, parents can queue up a box of gently used clothes to receive. Then, similar to eBay, members build virtual boxes of clothing to exchange…. The marketplace facilitates exact matches, ensures quality and remedies the lack of coordination that plagues offline clothing swaps. The service is a complete end-to-end solution for busy parents” (PR Newswire 2010).

As an Enabler, the company created a marketplace for people to trade boxes of used children's clothing. It offered tools for reporting and rating the clothing's quality, style, size, and gender, equipping parents with what it termed a “best-in-class interface” (PR Newswire 2010). However, after two years in business, three major problems were evident. First, the site needed additional monitoring—leaving quality and value assessments in the hands of sellers led to a very uneven offering. Second, the requirement of trading entire boxes of used clothing was unwieldy. Finally, the commission structure was proving to be unprofitable.

Increasing the extent of its platform intermediation, thredUP introduced a new offering, which they termed “Concierge.” Company communications described it this way: “Customers request a pre-paid, ready-to-ship recycling bag. They then fill the bag with their children's outgrown items, put the bag on their doorstep, and thredUP handles the rest. At thredUP's processing facility, expert consignors inspect items and reward senders based on the quality and quantity of clothes returned. Similar to consignment, the amount paid to the sender varies by item type, brand, size and season—up to $5 per piece. All items that meet quality standards are then resold via thredUP's online secondhand marketplace” (BusinessWire 2012).

Our fieldnote excerpts reveal delight with the end product of the sales process, facilitating trust in the exchange: “I ordered all the clothes for my daughter this Christmas in one shot. I browsed and searched thredUP's site by brand, size, style, age, gender, and curated seasonal selections. All the items I ordered came carefully folded, wrapped in tissue paper, attached with tags that read ‘Renewed with love,’ packed into a signature polka-dot box, and sealed by a sticker with the message ‘Enjoy!’” (author's field notes, December 2011). Note that thredUP's new interface, repackaging, and tagging now emulate the norms of other large online retailers.

Storytelling and other interactions between people exchanging their children's secondhand clothes proved to be unnecessary. In addition, thredUP's “best-in-class interface” was not enough to create profitability, because the market required more monitoring and enforcement of the exchange. Its “Concierge” service transformed the firm into a Hub configuration whose institutional norms were isomorphic (Scott 1995) with other large online clothing retailers. News reports show that thredUP is hiring and recently expanded into its fourth distribution center (BusinessWire 2016); Forbes estimated its market value at $400 million (Mac 2015).

Matchmaker Cases

Lowering transaction costs for exchange

Matchmakers combine technology and sociality in sophisticated ways. Their systems decrease search costs, simplify decisions, and locate matches that are superior to the ones actors could achieve on their own. In addition, Matchmaker LEMs deploy platforms alongside institutional arrangements to intermediate exchanges. Those platforms are tasked with managing the unpredictabilities of consociality, monitoring the equitability and safety of the exchange, and ensuring that the transaction proceeds as desired. The multibarreled approach to trust is crucial because, although network actors connect through the matchmaker's platform, most exchanges are finalized offline. We illustrate a successful Matchmaker configuration with TaskRabbit and use Skillshare as negative case.

TaskRabbit

Founded in Boston in 2008, TaskRabbit connects vetted skilled freelance labor (or “taskers”) with actors in their neighborhood seeking services such as cleaning, shopping, delivery, moving assistance, or home repair. Task posters review tasker profiles and ratings before accepting quotes for the job posting, which is often completed on the same day. TaskRabbit facilitates the service search, conducts background checks on its taskers, processes service purchaser payment, handles payment to the service provider after the work has been completed satisfactorily, provides customer support, supplies liability insurance, and guarantees satisfaction. Background checks, customer service desks, insurance, and guarantees are institutional supports and arrangements that legitimate the business (Scott 1995; Suchman 1995).

Although exhibiting a high degree of platform intermediation and deploying institutional assurances, Matchmakers such as TaskRabbit pair actors in a situation of copresence. On its app, the company frames the social aspect of its platforms as “neighbors helping neighbors, re-imagined for today” and assures potential customers of a “safe” and “reliable” experience (TaskRabbit 2016). TaskRabbit emphasizes recruiting responsible actors who will earn good reviews. In communications targeted at professionals, they emphasize their empowerment of taskers, claiming to be creating “a network of micro-entrepreneurs” (Dinges 2012).

By providing a commercial service with strong social interaction whose exchange elements are technologically intermediated, TaskRabbit ameliorates some of the drawbacks of social exchanges, such as the burdensome norms of reciprocation (Marcoux 2009). The LEM's hybrid commercial-communal and social-technological structure is at its most sophisticated in the Matchmaker type. TaskRabbit warns actors against violating the “spirit of payment” by circumventing the payment system, because doing so will leave them “personally liable for any damages or injuries arising from the task” (TaskRabbit 2016). TaskRabbit combines these normative enforcement mechanisms with its strong platform intermediation in order to manage actors’ ability to negotiate side deals in person or plan future transactions that would sidestep the platform altogether. TaskRabbit's social, institutional, and technological management of the transactional consequences of sociality demonstrate the delicate balance that successful Matchmakers achieve. Developing and maintaining such a system requires significant investment. TaskRabbit has raised $38 million in venture financing, employs 60 people, is available in 24 markets, and “is not yet profitable” (Stangel 2017).

Skillshare

Skillshare was a Matchmaker that aimed to connect amateur teachers with students in local markets. Once connected, teachers and students would arrange to meet in person for classes or tutoring. Skillshare's classrooms provided a social experience similar to that provided by traditional teaching and tutoring. Platform intermediation handled payment and centralized the financial exchange but left service delivery in the hands of network actors. Although the company's idea was supported by venture capital, it failed in the market.

There are three important reasons for Skillshare's failure. First, the high consociality of the offering was not accompanied by corresponding safeguards. Customers faced with the prospect of amateur, lower-priced teachers were rightly concerned about safety. Second, the logistics required to arrange face-to-face classes and teaching were difficult and expensive. Finally, Skillshare's market competitors, such as Udemy, were effectively replacing in-person classes with distance learning video technology.

Shedding its Matchmaker skin and adopting the form of an Enabler, Skillshare transitioned to an online-only platform and began successfully delivering online and video courses. In its first year online, the company attracted 75,000 new students, who provided $1.5 million in compensation to its online teachers (Griffith 2013). Three years later, the company had 40 full-time employees and boasted 3 million enrollments from over 180 countries (Noto 2016).

Hub Cases

Building on talent and developing standards

The Hub is characterized by a uniform service experience similar to that found in a conventional marketplace. As with retail consignment, Hubs integrate resources from different actors and serve as a central place to enact exchanges. Hubs provide network actors with many assurances against risk: they create a marketplace, lower search costs, offer product guarantees, monitor actors, and ensure that the exchange transpires as planned. Yet, for some companies, these elements are insufficient for success. In this subsection, we illustrate the empirical manifestation of the Hub form with two cases. The first, Quirky, has struggled to be a financially viable company. The second, Homejoy, shut down after five years in business.

Quirky

Founded in 2009, Quirky is a platform that brings crowdsourced inventions to market. The centralized platform enables inventors to propose and refine their ideas for a fee. Then, from an online community of thousands of interested participants, network actors judge the ideas and offer suggestions. With input from members of the community, the company chooses the best ideas, manufactures the products, and commercializes the innovations. Platform intermediation is high, with the flow of innovative ideas moving from the actors to the platform to the public. Quirky also apportions benefits from the sales. Not only does the inventor of the product receive a commission from Quirky, so too do the members of the community who provided helpful suggestions. Typical for the Hub configuration, Quirky remains in full control of the exchange process, providing privacy while ensuring quality and a consistent user experience.

The company grew quickly, with over a million network members, $100 million in revenue, and 400 products developed by 2014 (Lohr 2015). It attracted $185 million in capital and signed development deals with companies such as General Electric (Lohr 2015). According to Walker (2009), “Part of what its customers are buying isn't just a doodad but also the crowd-pleasing notion of tapping into the creativity of the many: a nonexpert with an interesting concept that is sharpened to perfection by the input of an engaged, online peanut gallery.”

The financial commitments required by Quirky's high platform intermediation strategy caused the company to struggle with production and retail distribution costs (Martin 2015). The company also failed to properly attract high-quality inventors who were looking for a stable system on which to develop and profit from their new product ideas. In favoring the tight controls of low consociality, the company had neglected two important considerations. First, many types of invention require coordination between several people with different skills. By minimizing sociality, Quirky limited participants’ abilities to collaborate. Second, social and nonfinancial rewards play an important role in motivating high-quality inventions and evaluations. Anonymizing participation constrained the site's ability to attract talented inventors.

Attempting to address these concerns, Quirky added increased collaboration functions to its system. It gradually provided more places for inventors to communicate publicly and privately. In addition, the website began featuring personal “meet the community” profiles of members and activities featuring individual inventors discussing what drives them. However, these social elements were added too late. The company filed for Chapter 11 bankruptcy in September 2015. It returned in February 2016 with new owners and financing.

Homejoy

Homejoy was formed in 2010 to connect customers with home service providers, especially house cleaners. With Homejoy, “cleanings were fully bonded, and cleaners contracting on the platform had to go through a screening process which involved third-party background checks…. The platform charged a uniform rate of $25 an hour for service” (Huet 2015). Although they were lateral network actors, Homejoy's cleaners were treated like employees; the platform charged customers for their services just as if it were any other cleaning service. This new labor formula worked well, and the company grew rapidly. Eventually, it operated in 31 cities across the United States, Canada, and the United Kingdom.

However, by 2015 the company was teetering on the edge of bankruptcy. Homejoy faced three major challenges common to the Hub form. The first was quality control. Service provided by the often-unskilled network actors was uneven. The firm tried to standardize the home cleaning service by training and certifying its house cleaners. However, training actors to provide a uniform service (e.g., leaving a Homejoy-branded fold on the bed) led to the second challenge: legal disputes that questioned the ostensibly independent status of its independent contractors. As Denegri-Knott and Tadajewski (2017, p. 234) explain in the context of another “peer-to-peer” market, “Only certain practices are rendered legitimate methods for facilitating the co-creation of value and here the role of the legal system is paramount.” Lateral exchange markets are new forms of exchange and are still in the turbulent process of gaining legitimacy and institutional (including regulatory) support. At a purely pragmatic level, even after training, Homejoy's work was still plagued with “run-of-the-mill execution problems” (Farr 2015). The final challenge for Homejoy was a retention problem resulting from the opportunism of copresence. “Cleaners who excelled would sometimes strike independent relationships with clients who wanted to see them again” (Farr 2015). By industry standards, Homejoy's cleaners were underpaid. Working independently “often resulted in a pay increase, and some cleaners even attracted enough new clients to start their own small cleaning businesses. Homejoy's only recourse against this threat, known as disintermediation, was to stop working with cleaners who attempted to recruit customers” (Farr 2015). When disintermediation occurred, Homejoy lost a service provider as well as a customer. Homejoy's quality control, legal, and opportunism challenges sunk the company. It ceased operations in July 2015.

These eight empirical examples—Homejoy, Quirky, Skillshare, TaskRabbit, thredUP, Kickstarter, Zimride, and Craigslist—illustrate the diversity of LEMs. They also demonstrate how the underlying dimensions of sociality and platform intermediation work in concert with institutional attempts to legitimate the company to provide either effective or ineffective solutions to governance and trust issues. In the next section, we explore the implications of these findings for marketing theory and managerial practice.

Discussion

Understanding LEMs

Lateral exchange markets are not limited to the consumption of access-based, sharing-based exchange or the amateur-based activities of peers; nor are they characterized by a monadic approach to exchange. These widespread and influential activities are technologically intermediated exchanges between the members of a network of buyers and sellers. After examining a large set of LEMs and analyzing how they function, we develop four LEM types. The types have two underlying trust-related dimensions: the extent of consociality between actors and the extent of intermediation of the platform. We then closely examined 20 cases of variously successful and unsuccessful LEMs to gain additional insight into their general organizing principles. Our work contributes two sets of novel insights to theory construction. First, our quadripartite typology reveals limitations in prior research that generalized findings from just one LEM type, such as access-based consumption (Bardhi and Eckahrdt 2012) or collaborative consumption (Benoit et al. 2017), to all types. Relatedly, our model explains why these types tend to exhibit particular characteristics. Second, it reveals how platform intermediation and extent of consociality are applied in discernible patterns across and within LEM types to create value and solve trust-related problems such as opportunism. In the following subsections, we discuss these contributions and their managerial implications.

Revealing the Different Types of LEMs

Our findings consolidate, organize, and provide novel conceptual underpinnings for previous research on peer-to-peer marketing, collaborative consumption, and the sharing economy. Although we avoid the misnomer “sharing economy,” this article informs Belk's (2014, p. 1597) observation that many of these contemporary companies rely “on the Internet, and especially Web 2.0.” Our analysis of processes of sociality management and exchange mediation explains, in a general sense, how and why these companies rely on networking technology. Unlike Belk's (2014, p. 1596) conception of the sharing economy, in which technology is used to “facilitate older forms of sharing,” our conception views the technology platform as an inextricable element of the LEM phenomenon—one that actuates certain elements of the exchange and interaction, but does not completely determine them—and is situated within a complex and dynamic institutional environment.

Our platform focus explains Arsel and Dobscha's (2011, p. 67) notable observation that Freecycle platform users defy rules, tell stories that are squelched by the organization's platform, and feel conflicted about the firm's ostensibly nonprofit nature. Our model views Freecycle as a manifestation of the Forum ideal type and explains why we would expect to find minimal platform intermediation and high consociality in it. Forums are social, even festal, markets, where we would expect to see rule breaking and storytelling. These characteristics also make the Forum one of the most difficult types to manage and monetize.

Similarly, we should not expect to find that all LEMs have the sociality of Muniz and O'Guinn's (2001) brand communities. Bardhi and Eckhardt (2012) find a communal ethos absent from the access-based consumers of Zipcar, a for-profit car-sharing platform. They attribute the “deterrence” of a communal ethos to the company's “big brother model” of “governance” (Bardhi and Eckhardt 2012, p. 888). Our model indicates that Zipcar is a Hub type, an LEM that deliberately inhibits consociality among actors and instead confers trust through strong platform intermediation. Although Zipcar's efforts to foster a brand community are noteworthy, its failure is relevant because it highlights the incompatibility of a centralized exchange platform with a highly social and communal experience. Our findings demonstrate how Bardhi and Eckhardt's (2012) important conclusions about Zipcar should not be applied generally to all types of “access-based consumption” or to all varieties of LEMs, but only to Hubs.

Similarly, Benoit et al. (2017) use Uber as an exemplar to develop their conceptualization of “collaborative consumption.” They classify Uber as a “matchmaker,” a platform provider that “uses sophisticated algorithms” to “match drivers with customers while at the same time optimizing a number of different, sometimes competing, objectives” (Benoit et al. 2017, p. 224). Their classification accords perfectly with our typing of Uber as a Matchmaker. However, they proceed to suggest that the value for all platforms in all forms of collaborative consumption—which they link to a wide variety of related access-based, peer, and sharing exchange markets—lies solely in matchmaking. Our findings contradict their generalization. For example, although it is true that all LEMs create value by bringing actors together, not all of them must use platforms with sophisticated algorithms, or perform complex optimization tasks. Craigslist, Freecycle, and other Forum types rely on social connection between actors for these coordination and optimization tasks, whereas Enabler LEMs such as Yerdle and 99Dresses perform them by equipping actors to sell to one another. In all, our model and its findings extend current thinking about these types of markets by providing a more comprehensive and more nuanced classification scheme.

Patterns of Assurance in Trusted Platforms

Our investigation of contemporary LEMs develops Adler's (2001) contentions about the effective management of information-based companies flowing mainly from a communal form of governance. It also reveals the importance of technology platforms as well as institutional arrangements such as third-part verification, liability insurance, and money-back guarantees to the creation of the trust required for this new form of exchange to gain social acceptance. Across all of our empirical LEM cases, the need to instill and manage trust was strongly evident. For some LEMs, such as TaskRabbit, the uncertainties of matching task service providers with buyers necessitated that they expand their business into verifying identities, supplying liability insurance, guaranteeing satisfaction, providing customer support, and managing the ratings of both sellers and buyers. For Homejoy, it meant training the people who were going to provide the home cleaning services so that the company could offer a more standardized experience. thredUP found that depending on buyers’ abilities to price, photograph, list, and package their own products was insufficient, so the company took over this aspect of the transaction for these lateral actors to create a more legitimate purchase experience isomorphic with existing online retail practices. On Craigslist, we see the results of failing to identify scams, suspicious posts, and potentially dangerous social interactions. This lack of control is not due to some failing of Craigslist itself but, as our model suggests, an unfortunate side effect of the type of LEM they represent. To manage this unintended consequence, Craigslist added watchdogs to its forums.

Our findings illustrate how the LEM form inspires different governance mechanisms that use training, verification, ratings, watchdogs, insurance, and legal mechanisms such as guarantees and warranties to manage transaction trust. Institutional norms are still in flux regarding this new form of business, necessitating governance with additional assurances such as insurance and guarantees. Governance is anchored by the interpersonal confidence conferred by consociality on one end, and the technological assurances of platform intermediation on the other. Either type of governance can be managed successfully, and our analysis of a variety of examples suggests not only that institutional and legal arrangements play supporting roles but also that there are many profitable ways to combine them.

For example, successful LEMs with low platform intermediation, such as Craigslist, shift the responsibility for personal and exchange security to lateral actors. The combination of virtual and physical copresence, along with its possibilities for communication and negotiation, allow transaction actors to establish trust and to work out a successful exchange.

Other forms of LEM find market success with a different combination of platform and social assurance. With an enabler LEM such as Kickstarter, a predetermined format for the online exchange provides a degree of consistency but also allows actors to improvise and display their individuality. Lending Club's fiscal responsibilities and high need for exchange assurance enable it to provide a platform that handles every element of the exchange, renders personal identities invisible, and severely limits consociality. Lending Club's use of software algorithms to assess lender and borrower worthiness is built into its platform. Those algorithms, along with the Lending Club brand and platform, serve as the basis for lenders’ trust. Actors’ trust in LEMs’ technology platforms is often similarly based on a normative belief in the legitimacy of their algorithms—or perhaps faith in algorithms in a general sense (O'Neil 2016).

In summary, LEM platforms affect value creation by enabling, directing, and constraining social and economic interactions. Acting as an intermediary, the platform provider offers the two potential benefits of creating the marketplace and lowering various transaction costs. Acting as a social space, the platform offers the opportunity to communicate, personalize, and negotiate. When the need for trust is especially high (as with a personal meeting or a significant financial transaction), it is generally met with a higher level of platform intermediation (as with thredUP), with higher levels of sociality (as with Quirky), or with additional institutional attempts to build legitimacy (as with TaskRabbit). In multiple cases, including Craigslist and Skillshare, we observe how sociality and copresence introduce a degree of unpredictability that can have positive as well as negative outcomes (e.g., the marriages of people who met through Lyft, the murders of people who met their killer through Craigslist). The general principles of the quadripartite model of LEMs contribute a novel understanding about how technology successfully combines with exchange and social behaviors in our contemporary marketing landscape. It demonstrates how consociality interacts with and can be replaced or titrated by various forms of platform intermediation.

Managerial Implications

Managing LEMs

Although the so-called sharing economy has grown rapidly and been the beneficiary of significant public attention over the past few years, its relative newness means that we know very little about how it actually operates. Marketing managers working in these disruptive new fields must make important decisions about their businesses without the tried-and-true guidelines bestowed to managers in established industries. In addition, many existing companies are entering LEMs as complementary businesses. For example, sustainability-minded outdoor clothing company Patagonia entered the LEM field with the “Common Threads Initiative,” an Enabler that connects customers who want to exchange their secondhand Patagonia clothing. Similar businesses might complement existing operations in a range of other industries, from musical instruments to art to electronics. As one of the first comprehensive investigations of LEMs, our article offers a comparative understanding of the structure and general organizing principles of these new forms of business that can be useful both to managers of pure play peer-based businesses and to established players extending their operations into these new forms. In this subsection, we explore the applications of our research findings by developing their strategic implications.

Awareness of LEM type is the first step to the effective management of LEMs. To effectively hone and market its value proposition, a marketer must understand the LEM type within which his or her company aims to operate. Forums, Matchmakers, Enablers, and Hubs each have particular forms of value creation that should focus managers’ business investment decisions and resource deployment. In addition, these types each face particular transaction risks that will require managers to balance network actors’ trust in the transaction with the risks that actors, once connected, will no longer need them. We offer guidance as we consider the strategic situation faced by the management of each of the four LEM types in turn.

Managing Forums

Forums reduce search costs and provide their greatest customer value by facilitating connections. Therefore, Forums need to invest in technologies and platforms that attract significant numbers of people to the network and then empower them to communicate with one another. Although it might be tempting to try to usurp control of between-actor communications or to filter them through the company, our model suggests that Forums are most effective when they facilitate a free flow of messages. The next major task of a Forum—to help manage actors’ transaction risks—flows directly from this high degree of freedom. To manage this risk, Forums should educate network actors about the unregulated nature of the market and inform them in no uncertain terms to be cautious about their exchange. Layers of volunteer moderators, reputation systems, and third-party verification may be helpful additions to the system that can verify actors and inspire trust. However, managers in Forum companies would be wise to realize that safety concerns are likely to be a fact of life and to adopt appropriate legal and fiscal safeguards, such as disclaimers and liability insurance.

Managing Enablers

Enablers provide value by lowering search costs and making it easier for actors to decide to transact. They should focus their investments and resources on equipping actors with tools sufficient to allow them to provide outstanding value to other actors. Enablers must find and build opportunities for network actors to engage in some of the value-creating practices described by Schau, Muniz, and Arnould (2009), which include customizing, badging, and milestoning. Tools for many of these practices can be programmed into the software interface of the platform. The platform would then simplify, standardize, and encourage actors to use these value-creating tools and practices. Enablers can minimize transaction risks by placing actors within a networking platform that allows them to broadcast a personal message that inspires interest and trust in other actors. However, the company is responsible for maintaining a minimally social environment in which actors can relate to one another's market offerings but conduct their transactions with a bare minimum of direct communication (if any).

Managing Matchmakers

Matchmakers lower monitoring costs, simplify search, and facilitate better decision making for actors. They provide their greatest source of value by appropriately pairing network actors. Matchmakers’ strategies must both embrace and manage the risks that accompany high consociality. First, a selection of third-party screening, identity verification, and reputation systems should be deployed and offered to network actors to mitigate safety concerns and help reduce the hazards that accompany the benefits of physical copresence. To ensure superior service, Matchmakers must also combine their high platform intermediation with a selection of actor training and certification, quality verification, and satisfaction guarantees. Furthermore, Matchmakers should emphasize consociality and its tendency to lead to social connection. Many companies assure actors that they will not be paired again with other actors to whom they have given a low rating. Forward-thinking companies might offer the opposite: the chance to be paired again with a familiar and liked service provider. To combat the danger that, once connected, network actors will engage in additional transactions outside the network, Matchmakers should combine the enticements of familiar network actors, a cutting-edge platform, high quality standards, and important exchange safeguards with moral persuasion and communal norms that discourage out-of-network exchange. Fostering the brand community engagement– and impression management–related practices of evangelizing, justifying, milestoning, badging, and documenting (Schau, Muniz, and Arnould 2009) may be effective ways to achieve this. These practices can also be programmed into the software interface of the company's platform.

Managing Hubs

Hubs lower the costs associated with search, decision making, monitoring, and exchange enforcement. Their core value proposition lies in the centralized exchanges they generate through their direct service interaction with network actors. Hubs must operate in an LEM business environment devoid of the attractive, humanizing, and trust-inspiring benefits of copresence. Depending on the industry, these elements may be important sources of value for actors. When they are less important (as in more quantitative, interchangeable markets such as finance), Hubs should invest strongly in their own platforms, related systems, and the promotion of the corporate brand. From a network actor's perspective, all other network actors are interchangeable, so it would therefore be sensible for Hub firms to invest in the cutting-edge abilities of the platform, its capacity to assess or mitigate risk, its ease of use and strong technical performance. Network actors will be particularly attracted to the Hub's platform. It is the platform itself that actors will trust, so the Hub would be wise to invest in its technology and branding. In some industries, the optimal performance of network actors may require collaboration or the acknowledgment of rare talent. In those cases, and only when necessary, the Hub should offer network actors minimal ability to personalize their experience and communicate with each other. When those abilities are provided, corresponding increases in platform intermediation should carefully monitor between-actor interaction to ensure that value-detracting social activities remain a negligible part of the Hub experience.

Conclusion

Emerging from a business format that extols “commons-based peer production” but does so within the “particular structural and ideological scaffolding” of Silicon Valley (Turner 2009, p. 76), LEMs are sites linked with a range of ideologies. The sharing economy literature (Belk 2014) connects peer exchange with utopian themes, casting its market forms in a generally positive, sometimes idyllic, light (Arnould and Rose 2016). Arnould and Rose (2016) reject the use of the term “sharing economy” in academia, given how promotionally freighted the term has become. We agree and offer our alternative: LEMs, a concept that, at its core, blends notions of the social and economic while also recognizing the complex institutional, legal, material, and representational worlds in which these markets are embedded—worlds whose practices will benefit from future research.

The legal, ethical, and moral problems of LEMs are challenges well worth exploring further. They are some of the most important and difficult issues that marketing practitioners working in a “post-trust age” currently face. Uber's scandals (Newcomer 2017) and Homejoy's problems are not atypical issues for LEMs, whose new forms are transforming the world of business but must build legitimacy and trust to achieve success. Although our research focused on the threat of opportunism from network actors who could meet and then transact outside the platform's ability to monetize the exchange, our findings reveal many opportunities for companies to use the power of their platform to be opportunistic. For example, Uber's ostensibly legitimate heuristics allegedly cheated its drivers of millions of dollars through system programming that rounded fees to the nearest dollar in the company's favor (Newcomer 2017).

Although we maintain an objective and supportive stance toward these still-emerging forms of exchange, we do not take lightly their power, their problems, and the intelligent legal and scholarly critiques leveled against them. We agree with Kreiss, Finn, and Turner's (2011, p. 256) assertion that, hidden below LEMs’ surface level of convenience, equity, and “peers” who “share equally in the spoils” is a technocracy that fails to “develop institutional mechanisms” for “values such as inclusion.” Our article can be read as a guide for management practice, as a sociological exploration, and as a critique. Finally, this research is intended as a contribution to the greater understanding of the transformational consequences of the ongoing intermingling of technologies, markets, institutions, and socialities.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.