Abstract

Much research has focused on how consumers and competitors respond to short-term changes in advertising and promotion. In contrast, the authors use Procter & Gamble's (P&G's) value pricing strategy as an opportunity to study consumer and competitor response to a major, sustained change in marketing-mix strategy. They compile data across 24 categories in which P&G has a significant market share, covering the period from 1990 to 1996, during which P&G instituted major cuts in deals and coupons and substantial increases in advertising. The authors estimate an econometric model to trace how consumers and competitors react to such changes. For the average brand, the authors find that deals and coupons increase market penetration and surprisingly have little impact on customer retention as measured by share-of-category requirements and category usage. For the average brand, advertising works primarily by increasing penetration, but its effect is weaker than that of promotion. The authors find that competitor response is related to how strongly the competitor's market share is affected by the change in marketing mix and the competitor's own response and to structural factors such as market share position and multi-market contact. The net impact of these consumer and competitor responses is a decrease in market share for the company that institutes sustained decreases in promotion coupled with increases in advertising.

Although these studies have enhanced the understanding of how consumers and competitors respond to advertising and promotion, they typically focus on response to short-term changes in these marketing instruments. Rarely have researchers studied the effects of major policy changes. The purpose of this article is to examine market response to a major and sustained change in advertising and promotion policy. We use Procter and Gamble's (P&G's) value pricing strategy to examine consumer and competitive response and to trace how this response ultimately affects market share. Starting in 1991–92, P&G instituted major reductions in promotion and increases in advertising in an effort to reduce operating costs and strengthen brand loyalty (Shapiro 1992). This new policy ran counter to the general trend of promotion increases at the expense of advertising that prevailed in the packaged goods industry during the 1980s and early 1990s (Donnelley Marketing Inc. 1995).

Analysis of market response to such a major policy change offers several advantages. First, it provides substantial variation in marketing-mix variables instead of week-to-week movement around a fairly stable level. This provides better estimates of the impact of marketing-mix variables. For example, Deighton, Henderson, and Neslin (1994) find that advertising attracts consumers to the brand but does not increase purchase probabilities among current users. They note, however, that this finding may not be applicable beyond the range of their data.

Second, the sustained policy change enables us to evaluate the effectiveness of advertising and promotion in a long-term setting. Studies based on short-term changes in advertising and promotion often find that promotion has a much stronger effect on market share than advertising does (e.g., Deighton, Henderson, and Neslin 1994; Sethuraman and Tellis 1991; Tellis 1988). However, Farris and Quelch (1987, p. 91) note that the effects of relatively minor changes in advertising are hard to detect and recommend that advertising experiments should be long enough for measurable effects to occur.

Third, the policy change also enables us to study competitor response in a long-term setting. The reaction of competitors to marketing-mix changes by a market leader depends, at least to some extent, on consumer response elasticities (Gatignon, Anderson, and Helsen 1989; Leeflang and Wittink 1996). Thus, if consumer response to sustained marketing-mix changes differs from short-term response, competitor response is likely to be different.

Fourth, researchers have recently called for studying responses to fundamental policy changes that are of strategic importance to senior management, not just the tactical changes that are made in the short run (e.g., Abeele 1994).

Fifth, that P&G is the clear leader in this setting simplifies the analysis of competitive response in that we do not need to determine first who, if anyone, is the leader (see, e.g., Kadiyali, Vilcassim, and Chintagunta 1999; Leeflang and Wittink 1996).

Finally, P&G's policy change was broad based. Our data and analysis encompass 118 brands in 24 product categories in the packaged goods industry. This should make our results more generalizable than those of other market response studies that are based on one or two product-markets.

We use the sustained policy change enacted in P&G's value pricing move to investigate three major research questions:

What are the roles of advertising and promotion in attracting and retaining customers?

To what extent are competitor reactions determined by market share response elasticities and structural factors versus firm-specific strategy?

How do consumer and competitive responses combine to determine the overall effect of a sustained change in advertising and promotion on market share?

Our study is unique in integrating both consumer and competitor response to a substantial, sustained change in advertising and promotion and in doing so across a large number of brands and product categories.

The article is organized as follows: We first discuss previous work relevant to the central questions of this research and present our conceptual model for analyzing them. Next, we describe the data and provide an overview of P&G's value pricing strategy. In the following sections, we present results for consumer and competitor response and show how these responses combine to determine the overall impact on market share. Finally, we summarize our findings and discuss implications for researchers and managers.

Theoretical Background and Conceptual Model

Consumer Response

A firm's advertising and promotion policy influences its ability to attract and retain customers by inducing more of them to (1) switch to the firm's brand, (2) repeat-purchase it more often, or (3) consume larger quantities.

Brand switching

As described by Blattberg and Neslin (1990), promotions induce consumers to switch to a brand by improving short-term attitudes toward it, conditioning consumers to respond to promotions, simplifying the purchase decision, and reducing perceived risk. These theories are supported by several empirical studies showing that promotions result in a large brand-switching effect (e.g., Bell, Chiang, and Padmanabhan 1999; Gupta 1988).

Advertising can induce brand switching through either raising awareness or improving consumer attitudes (Vakratsas and Ambler 1999). Although there is ample evidence that advertising influences awareness and attitudes, there is less evidence that it exerts a significant effect on brand switching. Deighton, Henderson, and Neslin (1994) and Lodish and colleagues (1995a, b) find that advertising helps small or new brands, presumably by attracting new users.

Repeat purchasing

Three theories point to a negative relationship between promotion and repeat purchasing. First, self-perception and attribution theories suggest that steep price cuts encourage consumers to attribute their purchase of the brand to the promotion, not to underlying preferences (Dodson, Tybout, and Sternthal 1978). Second, behavioral learning theory indicates that promotions train the consumer to buy on deal rather than repeat-purchase the brand (Rothschild 1987). Third, promotion can reduce the consumer's reference price for the brand, causing “sticker shock” on the next purchase (Winer 1986).

Theoretical support also exists for a positive effect of promotions. Promotions can be used to shape brand loyalty, thus increasing repeat rates (Rothschild and Gaidis 1981). Promotions can increase repeat rates in a competitive environment, because they preempt current users from taking advantage of other brands' promotions and therefore increase purchase probabilities not only among new triers but among current users as well.

Empirical research on promotion and repeat purchasing has produced a range of findings, including a negative association (Dodson, Tybout, and Sternthal 1978), no association (Ehrenberg, Hammond, and Goodhardt 1994), and both positive and negative associations (Gedenk and Neslin 1999).

Theory regarding the role of advertising in repeat purchasing centers on attitudes and framing. Advertising enhances beliefs, thereby improving attitudes and encouraging higher repeat rates. Framing theory suggests that advertising does not immediately persuade consumers but does predispose them toward a favorable consumption experience.

Empirical evidence on the role of advertising in repeat purchasing is mixed. Deighton (1984) provides evidence for framing, and Tellis (1988) finds that advertising increases repeat purchasing. Conversely, Deighton, Henderson, and Neslin (1994) find that advertising serves more to induce brand switching than to reinforce repeat purchasing. Lodish and colleagues' (1995a, b) findings also suggest that advertising primarily influences brand switching rather than repeat purchasing (small and new brands have more customers to attract and fewer to retain).

Consumption

Promotion can increase the consumption rate among a brand's users by inducing them to load up on the brand and then consume it faster (Ailawadi and Neslin 1998; Folkes, Martin, and Gupta 1993; Wansink and Deshpande 1994). However, promotion may also decrease consumption among a brand's users, because many of these users have bought only because of the promotion and may buy smaller sizes because of perceived risk (Blattberg and Neslin 1990, p. 49). Wansink (1994) and Wansink and Ray (1996) provide theoretical and experimental evidence that advertising can induce higher category consumption by suggesting new usage situations.

Moderators of consumer response

Researchers have found that advertising and promotion elasticities differ by brand as well as by product category. Probably the most important brand characteristic found to influence market share elasticities is brand market share: High-share brands have weaker elasticities than low-share brands (Bolton 1989; Danaher and Brodie 1999; Ghosh, Neslin, and Shoemaker 1983). Additional characteristics that have been found to influence elasticities include promotional and advertising activity, stockpilability, average purchase cycle, sales force, distribution, and advertising copy (Bell, Chiang, and Padmanabhan 1999; Bolton 1989; Gatignon 1993; Ghosh, Neslin, and Shoemaker 1983; Kaul and Wittink 1995; Litvack, Calantone, and Warshaw 1985; Narasimhan, Neslin, and Sen 1996).

Competitor Response

There are two streams of competitor response research. The micro approach studies the nature of competitive interactions in established markets using weekly or monthly data (e.g., Kadiyali, Vilcassim, and Chintagunta 1999; Leeflang and Wittink 1996; Putsis and Dhar 1998). The macro approach focuses on the response of incumbent firms to new entrants in the market (e.g., Gatignon, Anderson, and Helsen 1989; Ramaswamy, Gatignon, and Reibstein 1994; Robinson 1988; Shankar 1999). Both streams draw on the economics, industrial organization, and/or strategy literature to identify three sets of factors that influence competitor response: (1) market share elasticities, (2) structural factors, and (3) firm-specific effects.

Market share response elasticities

Economic theory posits that competitor response to a firm's change in advertising and promotion is governed by cross-elasticities (how strongly the competitor's share is affected by the firm's move) and self-elasticities (how easily the competitor can recover lost share). For example, Leeflang and Wittink (1996) show that competitors should react more strongly to preserve their market shares if their cross-elasticities are high. Although self- and cross-elasticities should determine whether a competitor reacts, the empirical literature shows that it is more difficult to predict their effect on how the competitor will react. For example, Gatignon, Anderson, and Helsen (1989), Putsis and Dhar (1998), and Shankar (1999) show that firms compete more strongly with effective weapons, that is, with variables for which they have strong self-elasticities. However, Brodie, Bonfrer, and Cutler (1996) and Leeflang and Wittink (1996) find that competitors often either overreact or underreact; Bell and Carpenter (1992) show that competitor response is different depending on the objectives sought; and Putsis and Dhar (1998) note that responses to cooperative versus competitive moves can be very different.

Structural factors

Industrial organization theory suggests that market structure influences competitive interaction (Scherer and Ross 1990). Concentration of the market, market share position, and multimarket contact of competitors with the initiating firm have been identified as key structural determinants of competitor response. As with elasticities, however, it is difficult to predict the direction of their influence. For example, some researchers believe that multimarket contact increases competitive rivalry (Porter 1980), whereas others argue that it leads to mutual forbearance and dampens rivalry because the competing firms have a high stake in many shared markets (Bernheim and Whinston 1990; Shankar 1999). Dominant competitors are expected to react differently from fringe firms, though it is not clear what the differences are (e.g., Putsis and Dhar 1998; Shankar 1999; Spiller and Favaro 1984). Market concentration is expected to increase cooperative behavior, because monitoring is easier, signaling is more likely to be perceived, and firms are less likely to compete away high margins (e.g., Qualls 1974; Ramaswamy, Gatignon, and Reibstein 1994; Scherer and Ross 1990).

Firm-specific effects

The resource-based view conceptualizes the firm as a unique entity with specific core competencies, leadership, culture, and resources that determine its actions (Barney 1991; Chen 1996; Collis 1991; Wernerfelt 1984). Not surprisingly, the marketing literature focuses on identifying and measuring the marketing resources of firms, such as brand equity, sales force, advertising and general marketing expertise, and market orientation (e.g., Capron and Hulland 1999). Although market share position and marketing-mix elasticities may be imperfect surrogates for resources such as brand equity and marketing expertise, other resources and competencies are unobserved or difficult to measure and are accounted for through a firm-specific effect (e.g., Boulding and Staelin 1993).

Conceptual Framework

On the basis of this literature, we have developed the framework in Figure 1 to answer our research questions. The consumer response portion of this framework decomposes market share into three components and considers the effects of own and competitive marketing mix on these components. These effects are moderated by brand and category characteristics. The competitive response portion posits that market share elasticities, structural factors, and firm-specific effects determine competitor reaction. Finally, the net impact of a policy change by a brand comes both directly, from consumer response to the brand's own policy change, and indirectly, through competitors' reactions to the policy change and consumers' response to the competitors' reactions.

Conceptual Framework

Decomposition of market share

Market share, the central focus of our study, is the product of three components: penetration (PEN), share-of-category-requirements (SOR), and category usage (USE). These three components correspond to brand switching, repeat purchasing, and consumption effects, respectively, as the means by which advertising and promotion attract and retain customers. We define PEN as the proportion of category users who purchase the brand at least once, SOR as the proportion of the brand's customers' category purchases accounted for by the brand, and USE as the average category purchase volume of the brand's customers compared with the average category purchases of all households buying the category. Market share equals PEN x SOR x USE. 1 For example, assume that P&G is purchased by 55% of all bar soap buyers. Buyers of P&G are somewhat heavier users of bar soap. Their use of the category is 1.30 times that of the average category user. Only 49% of their bar soap purchases are accounted for by P&G, so they are not very loyal to P&G. Therefore, P&G's share in the bar soap category is .55 (PEN) x 1.30 (USE) x .49 (SOR), which is .3504, or 35.04% market share.

To examine this algebraically, let

unit brand sales, unit category sales, market share of the brand, number of households that buy the category, number of households that buy the brand, average category unit sales per household that buys the category, and average category unit sales per household that buys the brand.

Then,

NC x CC, SB/SC, NB/NC, SB/(NB x CB), CB/CC, and (NB/NC) x [SB/(NB x CB)] x (CB/CC) = [SB/(NC x CC)] = (SB/SC) = MS.

The component PEN is a measure of customer attraction, because it reflects what proportion of category users are attracted to the brand at least once; SOR is a measure of customer retention, because it reflects how much of the brand consumers buy after they have purchased it an initial time. Practitioners use SOR as a measure of brand health, even loyalty (Bhattacharya et al. 1996; Hume 1992; Kristofferson and Lal 1996a, b). This measure reflects how well the brand retains its customers and is particularly relevant in the context of P&G's value pricing strategy, because one of the stated goals of the strategy is to improve customer loyalty.

Effect of advertising and promotion

Our theoretical discussion suggests that both advertising and promotion should increase PEN by encouraging more consumers to switch to the brand, though previous empirical research suggests that the advertising effect is much weaker than the promotion effect. Advertising should have a positive effect on SOR, because it should enhance repeat purchasing. Promotion could have a negative or a positive effect on SOR. Advertising should have a positive effect on USE to the extent that it suggests new product uses. Promotion could have a negative or positive effect, depending on whether it creates new usage occasions and increases the consumption rate or brings in consumers who purchase smaller quantities to mitigate perceived risk.

Moderators of advertising and promotion effects

Consumer response elasticities differ systematically from category to category and brand to brand. These cross-sectional differences are not of direct interest for our research, but we must control for them to obtain valid estimates on average. We allow market share position, stockpilability, purchase cycle, deal intensity, and advertising intensity to moderate self- and cross-elasticities in the consumer response model. Although we do not have data on all possible moderators (e.g., advertising copy), the consumer response research cited previously suggests that the factors we include explain a significant portion of cross-sectional variation in elasticities.

Competitor response

Competitor response also differs from category to category and brand to brand. It is moderated by market share elasticities and the structural and firm-specific factors suggested in the literature. Because market share elasticities are estimated in the consumer response model, there is an important link between consumer response and competitor response. The structural factors are market concentration, market share position, and multimarket contact. Firm-specific factors over and above these are represented by dummy variables. 2

We do not include structural or firm-specific variables other than market share position as moderators in the consumer response model because they are not relevant to consumers. For example, consumers would not be expected to react differently to a given brand's advertising because that brand competes with another brand in multiple markets.

Method

Data

We study changes in the market between 1990 and 1996. In 1991, P&G introduced its value pricing program and implemented it over multiple years (Kristofferson and Lal 1996a, b; Shapiro 1992), and we look at the market before, during, and after implementation of the strategy. Our data are primarily from Information Resources Inc.'s (IRI's) annual Marketing Fact Book. We select 24 product categories in which P&G participates and compile data on price, promotion frequency and depth, market share, PEN, SOR, and USE for several brands in each category. Whenever possible, we include P&G, three of its largest competitors, and at least one small competitor. The analysis is at the level of a manufacturer within a product category. That is, for a manufacturer with more than one brand within a product category, we combine the brands into one umbrella brand. 3 This results in data on 118 brands across the 24 product categories, though data for some brands are missing for one or more of the seven years. The advertising data are compiled from the Leading National Advertisers publication of annual media advertising. All the moderators in the consumer and competitor response models are derived from these data, with the exception of category stockpilability, which we obtain from Narasimhan, Neslin, and Sen (1996). In Appendix A, we define all the variables, and in Appendix B, we list the 24 product categories.

This is consistent with the emphasis of packaged goods manufacturers on category management and with the strategic emphasis of our research. It enables us to assess a firm's category performance as a function of its advertising and promotion policy in that category.

We note that our data reflect changes observed at the retail level, so we cannot separately measure the change in P&G's strategy toward the trade and the consequent change in strategy of the trade. Also, these data represent activity only in U.S. grocery stores and therefore do not speak to changes in other countries or in other channels such as mass merchandisers. However, the Marketing Fact Book covers a large number of packaged goods product categories and markets and has been used to gain important insights by researchers such as Fader and Lodish (1990) and Lal and Padmanabhan (1995). Our compilation is particularly valuable because we cover a period of seven years, include most of the product categories in which P&G plays a role, and augment the Marketing Fact Book data with media advertising data.

These data enable us to undertake a broad-based pooled time series, cross-sectional analysis. This is a well-established approach in the econometric literature (Hsiao 1986) that has produced several important articles in the marketing literature (e.g., Boulding, Lee, and Staelin 1994; Boulding and Staelin 1990, 1993; Hagerty, Carman, and Russell 1988; Jacobson 1990; Jacobson and Aaker 1985). The advantage of this approach is that it enables broad and generalizable analyses that span several brands, categories, or industries. The challenge is to control for cross-sectional differences so that they are not confounded with longitudinal effects. We model changes over time to control for cross-sectional main effects, and we incorporate moderators of both consumer and competitor response to control for cross-sectional interaction effects.

Value Pricing: An Overview

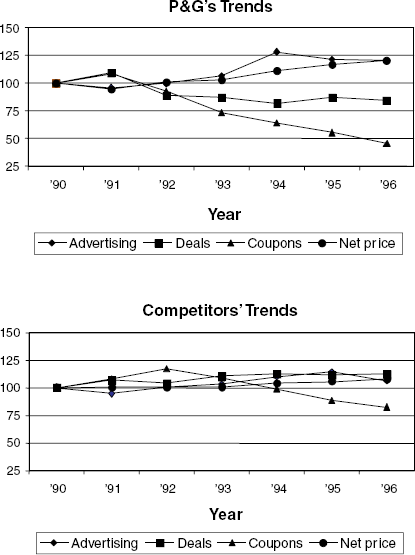

In Table 1, we present the average percent changes in price, advertising, and promotion made by P&G and its competitors between 1990 and 1996 across the 24 product categories. In Figure 2, we depict percent changes each year indexed to their values in 1990, which serves as the base year.

Did P&G's publicized policy change affect retail activity? The answer to this is a clear yes. P&G increased advertising expenditures in the neighborhood of 20% over the seven years. It also reduced promotion activities: Deal frequency declined 15.7% and coupon frequency declined 54.3%. As a result of the cuts in P&G's promotion, the net price paid by consumers increased by approximately 20%. Figure 2 also shows that these changes occurred gradually over several years, though price and deals had stabilized by 1995–96.

Overview of Value Pricing

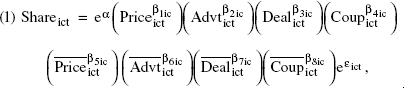

How did competitors respond? For advertising and coupons, they followed P&G directionally but not completely, and for deals, they did not follow P&G at all. Competitor advertising increased, but only by 6.2%; coupon frequency decreased, but only by 17.3%; and deal frequency increased by 12.6%. As a result, the net price paid by consumers for competitor brands increased, but only by 8.4%. Overall, then, competitors only partly went along with P&G's policy change. Table 1 shows the significant differences in the reactions of different companies. Colgate and Gillette were more competitive than Unilever. 4 Both companies strongly increased advertising and promotion. Unilever, in contrast, cut coupons while instituting small increases in advertising and deals. We examine subsequently how much of this difference in reaction across competitors is due to economic and structural factors and how much to firm-specific effects.

Value Pricing: An Overview

We refer to price decreases and advertising, deal, and coupon increases as competitive because these actions are intended to take share away from P&G. Analogously, we refer to price increases and advertising, deal, and coupon cuts as cooperative. This terminology takes into account the inherent asymmetry noted by Ramaswamy, Gatignon, and Reibstein (1994) and Putsis and Dhar (1998), who point out, for example, that following a price increase may be cooperative but following a price decrease is not.

What was the net consequence of the strategy change and competitive reaction for P&G's market share? Our data show that during this period, P&G lost approximately 18% of its share on average across these 24 categories (approximately five points per category). In line with changes in the marketing-mix variables, this share loss occurred gradually over several years and stabilized somewhat during 1995–96.

Although this overview provides a broad picture of P&G's initiative, our purpose is to gain an in-depth understanding of the market response to the policy change. In the next two sections, we estimate econometric models of consumer and competitor response that enable us to examine not just what happened but also why it happened. Specifically, we are able to (1) quantify the individual effects of advertising and promotion on penetration, share of requirements, and category usage; (2) account for differences across brands and categories; (3) determine the role of elasticities and structural and firm-specific factors in competitive response; and (4) attribute the total impact on P&G's market share to changes in each of its own marketing-mix variables and to competitors' reactions.

The Consumer Response Model

Model Specification

We model market share as a multiplicative function of marketing-mix variables, similar to Wittink and colleagues (1987) and Leeflang and Wittink (1996). Specifically,

market share of brand i in category c in year t relative to 1990, net price paid per unit volume for brand i in category c in year t relative to 1990, advertising (in tens of millions of dollars) for brand i in category c in year t relative to 1990, percentage of total sales of brand i in category c sold on deal in year t relative to 1990, percentage of total sales of brand i in category c sold with manufacturer's coupons in year t relative to 1990, average (volume-weighted) Price of brand i's competitors in category c in year t relative to 1990, average (volume-weighted) Advt of brand i's competitors in category c in year t relative to 1990, average (volume-weighted) Deal of brand i's competitors in category c in year t relative to 1990, and average (volume-weighted) Coup of brand i's competitors in category c in year t relative to 1990.

Note that the dependent and independent variables in the model are ratios with respect to the base year, 1990.

5

This indexing is similar in spirit to Wittink and colleagues' (1987) and controls for brand-specific main effects. As discussed previously, market share position and four category characteristics moderate consumer response elasticities, so different brands in different categories have their own elasticities, even though data for all categories and brands are pooled to estimate the model. This results in a process function for elasticities (Gatignon 1993):

elasticity for variable k in Equation 1 for brand i of category c; 1 if brand i in category c accounts for less than 5% of the sales of the top three brands in the category in 1990, 0 otherwise;

6

1 if brand i in category c accounts for 5% to 40% of the sales of the top three brands in the category in 1990, 0 otherwise; average percentage sold on deal in category c; average advertising expenditure in category c; average length of purchase cycle for category c; and Stockpilability of category c.

When data are missing for 1990, we use 1991 as the base year.

We use a three-part classification of market share position (small, middle, and high) to allow for nonlinear or nonmonotonic relationships between market share and consumer response. We include dummy variables for small and middle; high is the omitted category. In our sample, the lowest quartile of market share relative to the top three brands is approximately 7%, and the highest quartile is approximately 38%. We use slightly more extreme cutoffs of 5% and 40% to separate the really small/fringe and really big/powerful brands from the majority in the middle.

We take logarithms of both sides and estimate the following log-linear model using ordinary least squares (OLS):

7

We estimate this consumer response model using market share as well as the three components of market share, PEN, SOR, and USE, as dependent variables. Given the definitional identity relating market share to PEN, SOR, and USE, each coefficient estimate in the market share model equals the sum of the corresponding coefficient estimates from the models for the three components (see Farris, Parry, and Ailawadi 1992). As a result, the market share elasticity with respect to advertising equals the penetration elasticity with respect to advertising plus the SOR elasticity plus the USE elasticity.

We correct for serial correction that may be caused by indexing to a base year and find that the estimated elasticities are not substantively different from those obtained using OLS. We thank Vithala Rao for bringing the serial correlation issue to our attention. We also estimate the consumer response model using lagged values of the independent variables as instruments to control for possible simultaneity and again find few substantive differences in estimated elasticities. Therefore, we report the OLS results here for simplicity.

Results

In Table 2, we summarize the fit of the consumer response model for market share and its three components. Adjusted R2s are quite strong, showing that changes in the marketing mix are significantly related to changes in market share and its components. Furthermore, the F-tests show that both brand and category characteristics have a significant influence on consumer response. 8

Although the multiplicative model does not force market share predictions to lie between 0 and 100%, there are no instances in our sample either of negative predicted market share or of market shares within a category summing to more than 100%.

Consumer Response Model: Summary (569 observations)

p < .01.

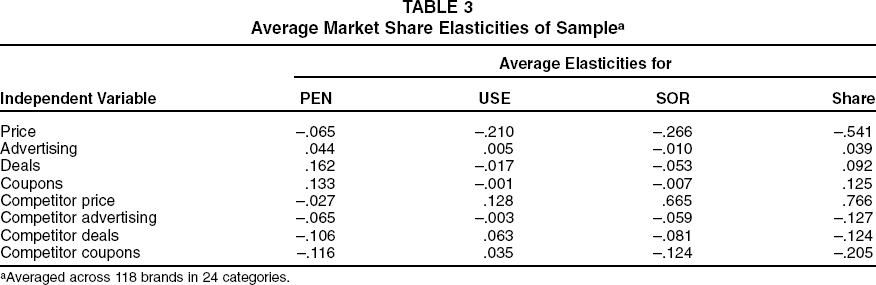

In Table 3, we present estimated elasticities for the average brand, which suggest that

Price paid is negatively associated with market share, primarily through SOR and USE. That is, lower prices enhance SOR and USE. Because our price variable is net price paid, this effect includes the impact of promotional price cuts.

Deals and coupons have similar share elasticities, exerted mostly through PEN. Both elasticities are fairly strong even though they represent just the signaling aspect of promotions (the impact of price cuts themselves is included in the price variable). 9

The overall effect of promotion includes the signaling effect captured by the deal and coupon variables, plus the price effect captured by the price variable. Examining how these effects combine, we conclude that promotion clearly increases PEN, because the signs of the deal and coupon variables are positive and the sign of the price variable is negative (meaning that price cuts increase penetration). For SOR and USE, the signs of the deal and coupon variables are negative, but the signs of the price variable are also negative (meaning that the price cuts associated with deals would increase SOR and USE). Even though the price coefficients are much larger than the deal coefficients, these balance out to mean that promotion has little effect on SOR and USE. This is because a fairly large percentage increase in deal frequency decreases net price paid by only a small percentage. 10

Advertising has a relatively weak relationship with market share. Its biggest association is with PEN, but it has little association with SOR. 11

We also estimate the model using regular price, calculated as shown in Appendix A. As might be expected, price elasticities are weaker and deal and coupon elasticities are stronger in that model. We report the results on the basis of net price to be consistent with most other scanner data–based studies (e.g., Bucklin and Lattin 1991; Chintagunta 1992, 1993; Fader and Lodish 1990; Mela, Gupta, and Lehmann 1997); also, overall model fit is better with net price.

For example, consider a brand with a regular price of $2 and a promotion price of $1.40. Currently, 70% of purchases are at regular price, and 30% are at the deal price. This yields a current net price paid of $1.82. Consider an increase in deal frequency, so that now 40% of purchases will be at the deal price. This is a 33.3% increase in the deal variable. The average price paid will then be $1.76, a 3.3% decrease in the price variable. Assuming the average elasticities as in Table 3, the new SOR compared with the current SOR will be (.967)−.266 x (1.333)−.053 = .9937, a marginal .63% decrease in SOR.

We estimate a model with current as well as lagged effects of all advertising variables (main and interaction effects) to test for carryover effects of advertising and cannot reject the null hypothesis that all lagged coefficients are zero. These results are consistent with those of Lodish and colleagues (1995a), who find that if advertising does not have an effect in the first year, it does not have any effect in subsequent years either.

Average Market Share Elasticities of Sample a

Averaged across 118 brands in 24 categories.

Competitive price cuts lead to lower share, mostly through a negative impact on SOR.

Competitive advertising is associated with lower market share through PEN and SOR. In other words, competitive advertising makes it more difficult to attract and retain customers.

Competitive deals and coupons are also associated with lower market share, largely through PEN and SOR.

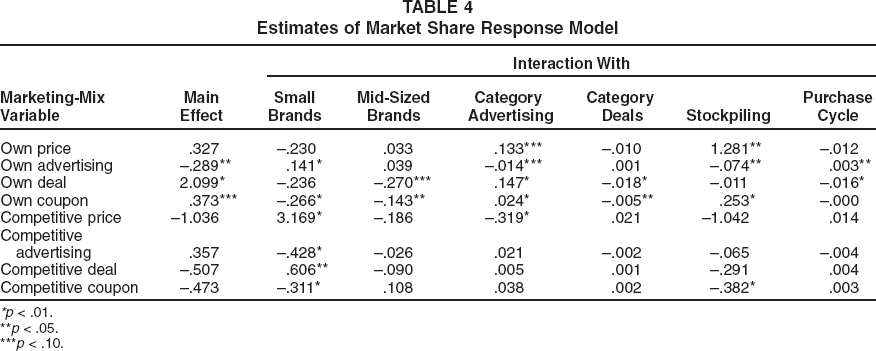

Elasticities vary for different brands in different product categories, as would be expected from the significant impact of brand and category characteristics shown in Table 2. For example, the market share model estimates in Table 4 show that heavily advertised categories are less price elastic, consistent with the role of advertising in product differentiation (e.g., Ghosh, Neslin, and Shoemaker 1983; Kaul and Wittink 1995). They are also less advertising elastic, consistent with a saturation effect (e.g., Bolton 1989). Similarly, heavily promoted categories are less deal and coupon elastic, also consistent with a saturation effect. And categories with long purchase cycles are less deal elastic, consistent with the findings of Narasimhan, Neslin, and Sen (1996), but more advertising elastic. In terms of brand differences, small brands have the strongest advertising elasticities, consistent with prior work by Deighton, Henderson, and Neslin (1994), Lodish and colleagues (1995a), and Batra and colleagues (1995). They are also the most vulnerable to competitive price cuts and advertising, consistent with the literature on asymmetric effects (e.g., Blattberg and Wisniewski 1989). Large brands have the strongest promotion (both deal and coupon) elasticities. Table 5 provides mean elasticities for small, mid-sized, and large brands in our sample.

Estimates of Market Share Response Model

p < .01.

p < .05.

p < .10.

Average Market Share Elasticities by Size of Brand

Validation with Disaggregate Data

Although these findings are consistent with the theoretical and empirical literature, they are based on aggregate data. To ensure that our results are not an artifact of category or temporal aggregation, we validate our market share model with more disaggregate data. Specifically, we compile quarterly market share, price, and promotion data over the 1990–96 period for 26 brands in six product categories from a data set on the Chicago stores of the Dominick's grocery chain. The product categories are automatic dishwasher detergent, dishwashing liquid, laundry detergent (powder and liquid combined), toilet tissue, toothpaste, and toothbrushes. We obtain quarterly advertising data from Leading National Advertisers. Although the advertising data are national, there is no reason to believe that changes in the Chicago market would be systematically different from nationwide changes.

To allay concerns about aggregation over time, brands, and categories, we estimate our multiplicative market share model separately for each brand in each category instead of pooling data across brands and categories and using moderators. Thus, we obtain 26 sets of elasticity estimates. As Table 6 shows, the pattern of elasticities from this disaggregate analysis is consistent with those obtained from the aggregate analysis. Overall, price elasticities are the strongest, followed by promotion elasticities, whereas advertising elasticities are quite weak. A comparison of Table 6 with Table 5 shows that differences in elasticities among small, mid-sized, and large brands are also similar to the aggregate results. Small brands have the strongest advertising elasticities and are the most vulnerable to competitive price cuts and advertising. 12 In summary, this disaggregate analysis corroborates the findings from our aggregate data, suggesting that the latter are not an artifact of aggregation.

Market Share Elasticities: Disaggregate Data

We also estimate the basic multiplicative competitive interaction attraction model (Cooper and Nakanishi 1988) for each category and find that the estimated elasticities are generally consistent with those from the multiplicative model.

Competitive Reactions

Model Specification

The competitive response model consists of four equations, one for each of the four marketing-mix variables. The dependent variable in each equation is the change in the marketing-mix variable of a given P&G competitor from the base year to the current period.

13

As discussed previously, competitor response should depend on how strongly P&G's strategy change affects the market share of the competitor. Therefore, we model competitive marketing-mix reaction, Mmixchg, as a function of Shreff, the predicted effect that P&G's strategy change would have on the competitor's market share if the competitor does not change its strategy:

14

We model predicted share change on the basis of the four marketing-mix variables:

change in marketing-mix variable k for brand i in category c in year t relative to 1990; predicted number of share points by which the market share of brand i in category c would change in year t relative to 1990 as a result of P&G's strategy change if there is no reaction; market share of brand i in category c in the base year 1990; cross-elasticity of brand i in category c with respect to variable k estimated in the market share response model; and percent change in the average (volume-weighted) Price of brand i's competitors in category c from 1990 to year t, assuming P&G's actual change in price from year 1990 to year t and no change for other competitors. Analogous definitions are used for the other marketing-mix variables.

We index competitive reaction to the base year (1990) for the same reason as in the consumer response model. Furthermore, we consider magnitude changes in a linear model rather than percent changes in a log-linear model because the fit of the former is significantly better for the advertising and coupon equations.

Shreff combines the impact of all four of P&G's marketing-mix variables. We do not model reaction to each of P&G's marketing-mix variables separately because there is strong multi-collinearity among them. One option is to follow other researchers and model reactions only in kind (e.g., model competitive price changes as a function of P&G's price alone, not its other marketing-mix variables). We believe that combining the impact of all P&G's mix variables into a single Shreff variable is a better alternative, because reactions may not occur only in kind (e.g., Leeflang and Wittink 1992, 1996).

In addition, αk represents the change in competition's marketing-mix variable k even if Shreff is zero, which reflects general trends in the market and/or an overall cooperative or competitive stance by competitors; βk indicates how competitors change variable k in response to Shreff. A positive sign for k = Price means that competitors increase their prices as P&G's move increases their share. A negative sign means that competitors decrease their prices as P&G's move increases their share.

Because competitor response is moderated by market share elasticities, structural factors, and firm-specific effects, we allow for both intercept and slope shifts by these factors.

15

To control for other category characteristics that may moderate competitive response, we also group the categories into five broad classes—health remedies, cleaners, personal care products, paper products, and food products— and include intercept and slope dummies for them:

16

self-elasticity of firm i in category c with respect to marketing-mix variable k, estimated from the market share response model; concentration of category c, equal to market share of top three firms; number of product categories in which firm i competes with P&G; 1 if firm i in category c is Colgate Palmolive, 0 otherwise; 1 if firm i in category c is Unilever, 0 otherwise; 1 if firm i in category c is Gillette, 0 otherwise; 1 if category c is a health remedy, 0 otherwise; 1 if category c is a cleaning product, 0 otherwise; 1 if category c is a personal care product, 0 otherwise; and 1 if category c is a paper product, 0 otherwise.

To ensure that we have enough observations to estimate a company effect reliably, we include dummy variables only for companies that participate in at least five of the product categories in our study.

We thank an anonymous reviewer for suggesting that we add these dummy variables.

Results

The system of four competitive reaction equations is estimated from observations on P&G's competitors in all the product categories. We use seemingly unrelated regression, because the error terms across the four equations may be correlated (Johnston and DiNardo 1997). The system-weighted R 2 for the four equations is .23. 17 In Table 7, we summarize the results of tests to determine whether market share elasticities and structural, firm-specific, and category class–specific factors have significant explanatory power. Each of these groups of factors is significant in all four competitive reaction equations, with the exception of the firm-specific effect in the advertising reaction equation. Thus, although a significant portion of competitor response is due to self- and cross-elasticities and structural factors, a significant portion is also firm-specific.

Competitive Reaction Model: Summary (376 observations)

p < .05.

p < .10.

p < .15.

We also estimate the competitive reaction model using one-year lags. There is no improvement in overall model fit, and none of the coefficient estimates changes significantly.

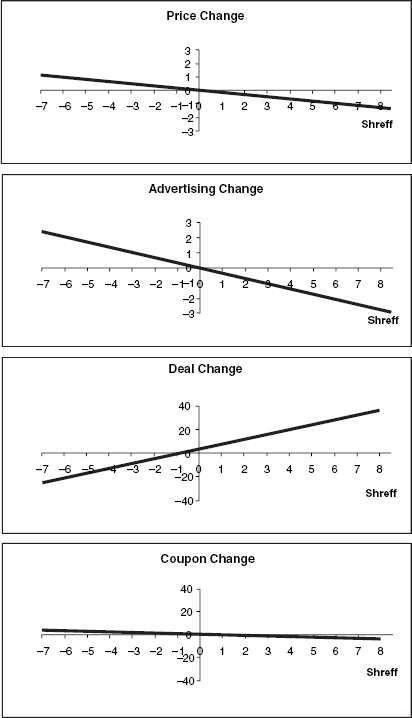

Figure 3 shows the response of the average competitor as a function of Shreff. The length of the line represents the range of Shreff in the sample. The price, advertising, and coupon intercepts being close to zero shows that competitors did not change these variables much during the period of study if they were unaffected by P&G's policy change.

Average Competitive Reactions

The deal intercept, however, is strongly positive, showing that competitors generally increased deals during this period even if they were unaffected by P&G.

The nonzero slopes show that competitors generally respond depending on how strongly they are affected by P&G. Competitors are competitive on deals, increasingly so when they benefit from P&G's policy change. This is also reflected in price response: Competitors' prices decrease as they benefit from P&G's policy change. Companies appear to use price and deals to take advantage of an opportunity for increasing market share. Response on advertising and coupons is quite different. Competitors cut advertising and coupons if they benefit from P&G's policy change, perhaps using the opportunity to save money.

Table 8 shows several interesting differences in competitive response due to structural and firm-specific factors. For example, competitors that have multimarket contact with P&G tend to follow P&G's lead on price and advertising more than others when they benefit from P&G's move. Small competitors react in the opposite way, however. They reduce price and advertising more than others if they are affected positively. 18 In addition, small brands are more likely than others to increase deals when they benefit from P&G's move. These findings suggest that small brands are less likely to follow P&G's move, whereas firms with multi-market contacts are more likely to follow. Over and above the differences in response that can be accounted for by market share elasticities and structural factors, response differs by company, which lends support to the resource-based view of the firm. For example, Gillette's reactions are less related to how much it is affected by P&G's policy change than Lever and Colgate's reactions, particularly on price and advertising.

This is partly attributable to a given share point change translating to a much larger percentage of a small brand's market share than a large brand's market share.

In summary, theory tells us that market share elasticities, structural factors, and firm-specific effects matter, and they do. Theory does not predict the direction of influence of these factors, and we find that there are several interesting differences in their influence across marketing-mix variables. These differences may be partly due to the initiating firm's move being cooperative on some variables (deals and coupons) and competitive on others (advertising). There may be other issues at play, however, such as the costs and profitability of various marketing-mix variables. Our research points to the need for further theory development to better understand how elasticities, structural factors, and firm-specific factors influence competitive response.

Net Impact of a Sustained Change in Advertising and Promotion Policy

Impact on Market Share

To understand the impact of the value pricing strategy on P&G's market share more fully, we use P&G's elasticities, obtained from the consumer response model, together with the changes made by P&G and the competition in each of the four marketing-mix variables, to trace formally the overall impact on the three components of P&G's market share— PEN, SOR, and USE. Table 9 suggests the following:

On average, P&G suffered a predicted 16% loss in market share across the 24 categories in our study. 19 The decrease in share is due mainly to a predicted 17% decrease in penetration. SOR and USE are virtually unchanged. The hoped-for increase in SOR to offset the loss in penetration did not materialize.

The loss in penetration is attributable to P&G's severe cuts in coupons and deals and the consequent increase in net price.

The increase in net price hurt SOR and USE. The deal and coupon cuts did not increase SOR as might have been expected if cutting promotions strengthened customer loyalty.

The actual loss was 18%, so the model represents share changes pretty well.

Standardized Coefficient Estimates of Competitive Reaction Model

Magnitude change in competitor's marketing-mix variable from 1990 to current year.

p < .05.

p < .10.

p < .15.

The Net Impact on P&G's Market Share

The increase in deals by competitors exacerbated P&G's loss in penetration and had a negative impact on SOR. This negative impact of competitor deal increases is just as strong as the negative impact of P&G's own deal cuts.

The competition's cuts in couponing and increases in net price helped P&G's SOR and offset the decrements in SOR resulting from P&G's increase in net price. But the competition's coupon cuts did not help enough, and P&G still lost penetration.

Neither P&G's own advertising spending increases nor the competition's smaller increases had much effect, because both self- and cross-advertising elasticities are quite weak.

Profit Implications

We use our findings, along with some assumptions, to examine the potential profit impact of value pricing. Our goal is not to evaluate P&G's strategy but to explore consequences other than market share that follow from a prolonged increase in advertising and decrease in promotion. We use a simple margin calculation as in Hoch, Drèze, and Purk's (1994) study:

First, the percent changes in price and market share in Table 1 and 9 show that total revenue should remain almost unchanged:

20

Second, under the conservative scenario that variable costs per unit do not change, the 18.2% reduction in total units sold leads to a corresponding reduction in total variable costs:

21

Total Variable Costs96 = (.818)(Variable Cost per Unit)(Sales90).

This assumes that total category sales in the market do not change (a reasonable assumption for mature categories) and the percentage change in retail selling price is equal to the percentage change in P&G's manufacturer selling price.

It is likely that variable costs per unit decreased because of operating efficiencies.

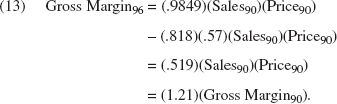

Thus, the gross margins in 1990 and 1996, respectively, would be

Equation 11 shows that gross margin in 1996 would be higher than in 1990, especially if variable costs are large.

One question is whether this increase in gross margin would be enough to cover the increased fixed costs of advertising. We obtained information about P&G's financials from COMPUSTAT's annual data file. In 1990, P&G's worldwide sales and advertising were about $24 billion and $2 billion, respectively, and the United States accounted for 62% of sales, that is, $15 billion. Furthermore, P&G's cost of goods sold as a percentage of revenue was approximately 57% in 1990. Thus, we can estimate variable cost per unit as .57 times the 1990 price, and gross margins in 1990 and 1996 can be written as

Thus, P&G's U.S. gross margin can be expected to have increased by about $1.35 billion as a result of value pricing (.21 x .43 x $15 billion). Assuming that the ratio of U.S. to worldwide advertising is the same as the ratio of sales, U.S. advertising in 1990 would be approximately $1.24 billion (.62 x $2 billion), and the increase in fixed costs due to a 21% increase in advertising would be $.26 billion (.21 x $1.24 billion). Thus, the increase in gross margin would be more than enough to cover the increase in fixed advertising costs. According to our calculations, net profit would increase by $1.09 billion ($1.35 billion - $.26 billion). 22 In short, it is plausible that P&G gave up share points in return for profits.

We do not compare these figures with P&G's reported earnings, because our data cover only U.S. grocery channel sales for these 24 categories and because we do not have information on cost cutting and other activities that P&G undertook during this period.

Conclusion

We have used P&G's value pricing strategy to study the impact of a major and sustained change in advertising and promotion policy. We focus on the role of advertising and promotion in attracting and retaining customers, the factors that influence competitive response, and the way these effects combine to determine overall market share impact. On the basis of previous theory and empirical work, we develop a framework for assessing this impact that integrates both consumer and competitive response. We test this framework using data on 118 brands in 24 categories in which P&G competed over a seven-year period.

Summary of Findings

Our first research question relates to how advertising and promotion work in attracting and retaining customers. We find the following:

Promotion increases penetration and has little impact on customer retention as measured by SOR and USE.

Advertising appears to work primarily by increasing penetration, but the effect is weaker than that of promotion. We find little evidence that advertising increases SOR or USE among the average brand's existing users.

Promotion has a stronger direct impact on share than advertising for the average packaged goods brand. This is a common finding in both micro and macro short-term studies (e.g., Boulding, Lee, and Staelin 1994; Tellis 1988) that has not been demonstrated previously in the case of a major and sustained policy change.

Our second research question pertains to the relative roles of market share response, structural factors, and firm-specific effects in determining competitor response. We find that

Competitors' reactions to a sustained change in advertising and promotion policy by a market leader vary with the degree to which their market share is affected. Reactions also vary by structural factors, such as the market share position of the competitor and the number of markets in which it competes with the initiator of the policy change.

Even after accounting for market share response elasticities and structural factors, there are still firm-specific effects in competitor reactions.

Competitors do not react the same way on all marketing instruments. In this case, competitors tended to decrease advertising and coupons but used deals to gain market share even when they were benefiting from P&G's policy change.

Our third question is how consumer and competitor response combine to determine overall market share impact. We find that the net impact is a decrease in market share for the initiating company, though it is plausible that its profits increased. The loss in penetration resulting from promotion cuts is not offset by increases in SOR or by competitive reactions. The effect of promotion on share is greater than that of advertising for established brands, though the reverse is true for small brands. The implication is that cuts in promotion, even if coupled with increases in advertising, will not grow market share for the average established brand in mature consumer goods categories.

Limitations and Further Research

Although these findings are both important and stimulating, our study has some limitations. First, we focus on a policy change that involves significant changes in advertising and promotion. We do not have data on any changes P&G may have made in variables such as product assortment or new product development, so we cannot speak to their impact. Similarly, data limitations preclude the use of moderators such as sales force, distribution, and advertising copy in our consumer response model (see Gatignon 1993). Although our purpose is not to study these moderators per se, including them might have generated additional insights. Nor do we have measures of firm-specific factors such as culture and management skill, though the statistical significance of the dummy variable surrogates we use for these factors should encourage further research in this area.

Second, we cannot make conclusive statements about the impact of the strategy change on profitability in the absence of data on P&G's manufacturer price and cost data. This would be an important area for further research if relevant data become available. Still, sales are a key objective for most companies, including P&G (see Brooker 1999; Fairclough 1999; Kristofferson and Lal 1996a, b), so we believe that our analysis of market share is important.

Third, as noted previously, our analysis pertains to sales made through the U.S. grocery channel, and alternative channels such as mass and discount merchandisers have become more important in recent years. We note, however, that the shift to alternative channels is occurring for other large competitors as well.

Fourth, we assume that P&G's adoption and consistent application of value pricing is exogenous; that is, P&G did not react to competition. With only seven time series data points, we cannot investigate this issue. Trends in P&G's marketing mix over the seven-year period, however, do not reveal any major pattern shifts or reversals. If a reversal in strategy occurs in the future, it would provide another valuable opportunity to examine market response.

Finally, our analysis is based on aggregate data. There is a trade-off between the micro approach to examining individual brands, categories, or markets and the broad-based, strategic view provided by our analysis and others like it. We believe that both approaches contribute to understanding market response and should be viewed as complementing each other. More important, many of our results are consistent with micro studies, and the product categories in which we are able to replicate our analysis with disaggregate quarterly data also corroborate our findings. Still, it would be valuable to examine differences between our conclusions and those based on more disaggregate data, should those data be available. Such data would also enable researchers to study brand and category differences in market response in more detail and to study interactions between marketing-mix variables—for example, the effect of a brand's advertising and promotion on its price elasticity (e.g., Gatignon 1993; Jedidi, Mela, and Gupta 1999).

Implications for Researchers and Managers

While acknowledging these limitations, we believe that our results are provocative and raise several important questions and implications for researchers and managers:

What is the correspondence between SOR and brand loyalty?

A sustained decrease in promotion and increase in advertising should have enhanced P&G's SOR through increased brand loyalty. However, advertising did not improve SOR. Furthermore, the net impact of cutting deals and coupons and of the increase in net price paid was to decrease SOR. We believe this is due to the retention role of price promotions: In a competitive environment, an existing user is more likely to repurchase the brand when it is on promotion than when it is not. But, even if promotions do not hurt SOR, underlying attitudinal loyalty could be diminishing. It is important for researchers to investigate this further (e.g., Kopalle, Mela, and Marsh 1999), because SOR is a commonly used indicator of brand loyalty (e.g., Bhattacharya 1997; Bhattacharya et al. 1996).

What does advertising do?

We find that the direct effect of advertising on the components of market share is weak for all but small brands. This lack of effectiveness could be attributable to execution (e.g., Lodish et al. 1995a) or to the way advertising works for established brands in mature markets. It is important to have a base level of advertising, but even substantial increases over that base level may not generate dramatic gains in market share for established brands. Our results are consistent with those of Tellis (1988), Deighton, Henderson, and Neslin (1994), and Batra and colleagues (1995), even though we were working with a substantial increase in advertising. In any event, more research is needed on how and in what circumstances advertising works.

Market share elasticities and structural and firm-specific factors play a role in competitor response

Managers who try to anticipate competitor response must not only know how their policy change will affect competitors' market share but also consider structural issues such as the market share position of their competitors and in how many markets they compete. Furthermore, competitor-specific resources, capabilities, and culture also determine the response. Our findings strongly suggest the need for theory that can predict not only the factors that determine competitive response but also the direction of their influence.

Competitors' response to policy changes is not uniform across marketing instruments

The reasons for this need to be sorted out. An obvious potential explanation would be differences in profitability across marketing instruments, but there may also be some organizational factors at work. For example, it may be easier for managers to reallocate their total marketing budgets than to change them drastically.

Researchers should make use of major policy changes

Dekimpe and Hanssens (1995) note that most markets are stationary, which precludes the finding of persistent effects of marketing-mix variables. The substantial changes in marketing-mix variables as well as market share that accompany a major policy change provide a valuable opportunity to test for persistence. Jedidi, Mela, and Gupta (1999) do not find significant long-term effects of advertising on price or promotion sensitivity. Perhaps such effects can be detected with more substantial variation in advertising. The P&G value pricing policy is one example of a policy change, as are the Post cereal price rollback of 1998 and Marlboro's earlier price cutback. We conclude with a call for making use of these strategic policy changes to better understand the impact of marketing strategy.