Abstract

The emergence of the Internet has pushed many established companies to explore this radically new distribution channel. Like all market discontinuities, the Internet creates opportunities as well as threats—it can be performance-enhancing as readily as it can be performance-destroying. Making use of event-study methodology, the authors assess the net impact of adding an Internet channel on a firm's stock market return, a measure of the change in expected future cash flows. The authors find that, on average, Internet channel investments are positive net-present-value investments. The authors then identify firm, introduction strategy, and marketplace characteristics that influence the direction and magnitude of the stock market reaction. The results indicate that powerful firms with a few direct channels are expected to achieve greater gains in financial performance than are less powerful firms with a broader direct channel offering. In terms of order of entry, early followers have a competitive advantage over both innovators and later followers, even when time of entry is controlled for. The authors also find that Internet channel additions that are supported by more publicity are perceived as having a higher performance potential.

One aspect of e-commerce that has yet to be addressed in detail is the … performance of the new medium…. The expectations of profitability of Internet trading vary greatly, from it being perceived as a more profitable medium to the converse. (Booth 2000, p. 21)

It is difficult for executives at most companies … to estimate accurately the returns on any Internet investment they may make. (Ghosh 1998, p. 126)

Despite the uncertainty surrounding the performance implications of adding an Internet channel to their channel portfolio, many firms, attracted by the potential access to millions of customers and the relatively low costs of setting up the channel, have rushed to establish an Internet channel. Others, daunted by the fear of a continuing price squeeze and/or an alienation of their entrenched channels, wait for more evidence to accumulate.

In this context, one of the main conclusions of the eBusiness workshop organized by Penn State's eBusiness Research Center is that academic contributions on the subject are needed, because “without sound research, eBusiness managers are sailing rudderless” (Donath 1999, p. 2). A similar call for more scholarly research is raised by Hoffman (2000), who deplores the lack of a solid base on which to make Internet-related investment decisions. We address these calls in three ways. First, we develop a conceptual framework for the various performance-enhancing and performance-destroying forces at work when a company adds an Internet channel. As is apparent from the literature we review, academic research has been characterized by a focus on a single, conventional channel, and the combined use of multiple channels, including the use of an Internet channel, has not yet received its due attention. Second, we quantify the performance potential of an extra Internet channel through its impact on the firm's stock return, that is, investors' expectations of the change in future cash flows. We thus assess whether stock market participants recognize predominantly opportunities or threats from incumbent firms' expansion into Internet channels. Third, building on our conceptual framework, we examine several firm, introduction strategy, and marketplace characteristics that may influence the direction and magnitude of the change in performance potential associated with an Internet channel addition. We test our hypotheses on a data set of Internet channel entries in the newspaper industry. Not only are several of the performance-enhancing and performance-destroying forces present in this industry, but also electronic publishing is expected to act as “a pacesetter for the Information Society” (European Commission 1996, p. 1) and to foreshadow trends that may occur more slowly in other industries.

Literature Review

Channel research has long emphasized the importance of recognizing the performance implications of channel decisions. This has fueled a significant, multifaceted literature. An important stream of literature, starting with Jeuland and Shugan (1983) and McGuire and Staelin (1983) and including the more recent contributions of Gerstner and Hess (1995) and Lal, Little, and Villas-Boas (1996), has extensively analyzed the performance implications of a wide variety of channel decisions (e.g., coordination of channel efforts, use of exclusive resellers) game theoretically. These studies focus on the performance implications of a supplier's channel decisions in terms of their effect on a single channel only, abstracting from their potential effect on other channels. More recently, several game-theoretical studies have started to examine the performance implications of a firm's channel decisions, taking into account their effect on the firm's entire channel system (e.g., Purohit 1997; Purohit and Staelin 1994). Of particular interest is Zettelmeyer's (2000) work, in which the profit implications of the decision to add an Internet channel to a conventional channel are analytically derived.

In addition to the extensive game-theoretical literature, many studies have tested the performance implications of channel decisions empirically. These studies can be described along two dimensions: (1) the nature of the performance measure being used (perceived versus factual) and (2) the scope of the study (single-channel versus multiple-channel). Most studies have used perceptual (e.g., Jap 1999; Kumar, Stern, and Achrol 1992) as opposed to factual (e.g., Ambler, Styles, and Xiucun 1999; Buchanan 1992) performance measures. Although it would seem that factual measures such as sales (growth) or gross margins are the preferred way to measure channel performance, several studies have questioned their use (e.g., Siguaw, Simpson, and Baker 1998). These studies argue that often respondents are unwilling to provide factual performance data, or they provide it in a way that is either not representative of true performance or not consistent with that provided by other firms. In this article, we propose an alternative factual measure that is less susceptible to these problems, stock-price returns. In terms of the scope of the study, an extensive literature review of International Journal of Research in Marketing, Journal of Marketing, Journal of Marketing Research, and Marketing Science identified only one empirical study on the performance implications of a firm's channel decisions that takes into account the decisions' effect on the firm's entire channel system. Lehmann and Weinberg (2000) focus on product sales across channels that are added sequentially. The presence of just one empirical multichannel performance study demonstrates the room for more research in this area. The current study develops a framework for conceptualizing the performance effects on the entire channel system of adding an Internet channel and provides empirical tests on the impact of a variety of moderating factors.

The Performance-Enhancing versus Performance-Destroying Capacity of Internet Channel Additions

The addition of an Internet channel poses opportunities as well as threats—it can be performance-enhancing as readily as it can be performance-destroying. Supplementing existing channels with an Internet channel can enhance a firm's expected performance when demand- and/or supply-side advantages are bestowed on the firm. A demand-side advantage enables firms to charge a higher price at a given level of demand or generate a higher demand at a given price. Supply-side advantages occur when a lower cost structure is incurred. Adding an Internet channel can also harm expected performance, however, through demand- (reduced revenues) and/or supply-side (increased costs) disadvantages. We elaborate on each of these factors.

Demand-Side Advantages

Demand expansion

The Internet can increase sales in three ways: market expansion, brand switching, and relationship deepening. Market expansion occurs when new (segments of) customers are reached who did not yet buy in the category. Estee Lauder, for example, hopes that Clinique.com will attract customers who avoid buying at a cosmetics counter because they find the experience intimidating. Demand may also expand through brand switching, that is, by winning customers from competitors. One specific way in which new segments can be tapped or customers won from competitors is through expansion of the current market to the global market (Quelch and Klein 1996). Finally, demand may expand through relationship deepening, that is, selling more to existing customers. Barnes and Noble, for example, experienced record sales in its real-world stores upon launching its online store, because this increased its customers' interest in books.

Higher prices

Lal and Sarvary (1999) show that when the proportion of Internet shoppers is sufficiently high and the product's nondigital attributes (i.e., attributes for which a physical inspection of the product is necessary) are not overwhelming, the Internet may represent an opportunity for firms to increase their prices. Also, because the Internet enables consumers to save shopping time and effort, it makes it costly for them to try new products for which sensory attributes need to be physically evaluated. Instead of going to the store, consumers may decide to infer the missing attributes on the basis of their overall evaluation of the brand. Consequently, in some cases, consumers may become more brand loyal when purchasing through the Internet. Because loyal customers are less price sensitive, firms may be able to raise their prices and enjoy higher revenues. Finally, during the emerging stages of the Internet market, consumers tend to be more affluent and therefore less price sensitive (Degeratu, Rangaswamy, and Wu 2000).

Supply-Side Advantages

The Internet can offer supply-side advantages through reduced production and transaction costs. In a distribution context, the former refer to the costs of completing the physical distribution activity (Klein, Frazier, and Roth 1990). Transaction costs are the costs incurred as a result of the firm's efforts to coordinate and control the entities performing the physical activities. They include such ex ante costs as drafting and negotiating agreements with these entities and such ex post costs as monitoring and enforcing agreements (Rindfleisch and Heide 1997).

Lower physical distribution costs

Internet distribution can help companies dramatically cut physical distribution costs. For intangible goods that can be delivered digitally, distribution costs are often reduced by 50% to 90%. For tangible goods, Internet channels are estimated to reduce distribution costs by more than 25% (Organisation for Economic Co-operation and Development 1999). These savings can be attributed to a variety of factors: Transaction processing is eased, thereby reducing paperwork, human errors, and customer disputes; inventory costs may be reduced as intermediaries are bypassed; and some marketing functions are shifted to the customer (Hoffman, Novak, and Chatterjee 1995).

Lower transaction costs

Organizational innovations often have the purpose of economizing on transaction costs. By setting up an Internet channel, companies can reduce ex ante transaction costs by bypassing intermediaries (thereby reducing commission costs) and dealing directly with their customers (Benjamin and Wigand 1995). Airlines, for example, are making headway selling tickets online because their direct sales model eliminates the commission paid to travel agents.

Demand-Side Disadvantages

Demand reduction

Adding an Internet channel to an entrenched channel system may involve channel “shift” (customers moving from one channel to another) without channel “lift” (new sales) (Alba et al. 1997). Adding an Internet channel may even lead to a decrease in total sales when consumers buy less through the new channel than through their old channel—for example, when there are fewer impulse purchases through the Internet or when disenchanted distributors offer less support to the firm's products, resulting in more brand switching toward the firm's competitors.

Lower prices

For many firms, a major threat posed by the Internet is that profits could be eroded through the intensified price competition that might ensue as consumers' search costs are lowered (Alba et al. 1997). The Internet can increase the power of the consumer, because price comparisons across suppliers can be performed quickly and easily. Therefore, prices and margins are expected to be pushed down (Degeratu, Rangaswamy, and Wu 2000).

Supply-Side Disadvantages

Higher physical distribution costs

The cost of an Internet channel has two components: fixed start-up costs, such as the purchase of computer hardware and software, and the costs of Internet hosting services. Also, higher advertising expenditures may be needed to create awareness for the new channel. Even though Internet channels can vary dramatically in cost, some incremental expenditures are always involved.

Higher transaction costs

Existing channels may view the new Internet channel as unwelcome competition. They may fear their sales will be reduced if firms reach out directly to their consumers. In addition, the low physical distribution costs and easily obtainable economies of scale of Internet channels may lead firms to reduce their prices and may put pressure on the existing channels' profit margins (Alba et al. 1997). When this happens, interchannel friction becomes likely. The firm's entrenched channels may lose motivation and reduce their support for the firm's products (a passive response), retaliate, or even discontinue their distribution (active responses) (Coughlan et al. 2001, p. 252). To prevent entrenched channels from shirking, firms need to monitor them more extensively to check whether they live up to their agreements and, if necessary, enforce these agreements. This is likely to increase ex post transaction costs (Stump and Heide 1996). In a recent survey of 50 consumer goods manufacturers by Forrester Research, 66% indicated that channel conflict, with its potentially costly result, was the biggest issue they faced in their online strategies (Gilbert and Bacheldor 2000).

Net Effect: Performance-Enhancing or Performance-Destroying?

Even though it would be of interest to quantify the impact of each of the preceding factors separately, it is first and foremost important to understand the overall net performance impact of establishing an Internet channel. Apart from quantifying this net effect, we use our conceptual framework as a guiding tool to develop hypotheses on the moderating impact of several firm, introduction strategy, and marketplace characteristics, as summarized in Table 1.

Framework for Developing Hypotheses

To be read as follows: When adding an Internet channel to their entrenched channel systems, more powerful firms are subject to more demand advantages and/or less demand disadvantages than less powerful firms.

This effect is put in parentheses because we expect it to be of marginal magnitude.

Notes: A “+” means a positive impact on the performance potential of a new Internet channel, implying more value-enhancing capacity (e.g., more demand, higher prices/margins) and/or less value destruction (e.g., lower costs). Similarly, a “-” means a negative impact on the performance potential. A “+/-” means that there are good arguments for both a positive and a negative relationship. A “∩” indicates an inverted-U relationship.

Hypotheses

The discussion to this point has focused on the performance-enhancing versus performance-destroying capacity of an Internet channel addition. The extent to which performance is enhanced or destroyed is likely to be contingent on several factors. The marketing strategy literature suggests that the performance of a new entry depends on firm characteristics, the introduction strategy, and the marketplace or environment (see Figure 1). 1

The Effect of Internet Channel Additions on Performance Potential Moderated by Firm, Introduction Strategy, and Marketplace Characteristics

In case conclusive prior research/evidence in a “new economy” setting is not yet available, we use “old economy” evidence as a logical and useful starting point when developing our hypotheses. This approach is in line with the parsimony principle in developing science and empirical generalizations.

Firm Characteristics

Firms are distinctive because they have accumulated different physical and intangible assets, such as financial reserves, equipment, brand equity, channel equity, employee skills, and marketing expertise. These firm-specific resources and capabilities may influence the effectiveness of the firm's new channel introduction. We consider three dimensions of a firm's resources and capabilities: its channel power, direct channel experience, and size.

Channel power

Power is a crucial concept in marketing channel research. Channel researchers have often derived their definitions of power from Emerson's (1962) power– dependence theory: A firm's power over a distributor is determined by the latter's motivational investment in the relationship and its availability of alternatives. Motivational investment refers to the value of the resources or outcomes mediated by the firm and has often been operationalized through the “sales and profits” approach: The greater the sales and profits a firm accounts for, the greater is its power (Frazier, Gill, and Kale 1989). The availability-of-alternatives component refers to the difficulty of replacing the outcomes mediated by the firm because of the lack of alternative partners: The lower the number of available alternatives, the more difficult it is to replace the sales and profits accounted for by the firm, and the greater is the firm's power over the distributor (Buchanan 1992).

When a firm establishes an Internet channel, this is likely to lead to a loss of goodwill on the part of the established channels, regardless of whether the firm is low or high in channel power. However, whether the entrenched channel will act on this loss of goodwill depends on channel power. When a firm has little channel power, opportunistic behavior may arise on the part of distributors; for example, distributors may provide less support for the firm's products while pushing competitors' products instead (Frazier 1999). This may cause some of the firm's customers to switch. To limit this unfavorable demand evolution, higher ex post transaction costs are required. In contrast, when a firm is powerful in its entrenched channels, the latter's continued cooperation is more easy to obtain because of the dormant potential to invoke sanctions. We therefore hypothesize the following:

The performance potential of an Internet channel addition is positively related to the firm's channel power.

Direct channel experience

According to Erramilli (1991), experience has two facets—intensity and scope—that may influence firms in two distinct and possibly opposing ways. In an Internet channel context, the intensity of a firm's experience is the time span the firm has already been engaged in direct channel operations before the current entry. The scope of a firm's experience is the number of direct channels established by the firm before the current Internet channel addition.

Intensity of experience

Firms with longer experience have more and better information, face less uncertainty, and can more easily transfer technology and managerial resources (Ansoff 1965), which leads us to propose that firms with longer experience have a significant advantage in physical distribution costs. In contrast, some authors (e.g., Singh and Lumsden 1990) claim that firms may get stuck in routines that are no longer appropriate in the current environment and that bureaucratic inertia may set in. Therefore, inexperienced firms can be argued to be less committed to old (outdated) routines, which may provide them with a differential advantage when technological change is rapid (Grant 1991), as is the case in the rapidly changing Internet environment. On balance, however, the empirical evidence appears to support a positive effect for intensity of experience. We therefore hypothesize the following:

The performance potential of an Internet channel addition is positively related to the intensity of direct channel experience.

Scope of experience

The scope of direct channel experience, or the number of direct channels a firm already operates when it sets up the Internet channel, is expected to have negative demand effects. The more direct channels a firm already offers, the lower is the probability that the new Internet channel will be viewed as significantly different from existing channels. A new channel that is perceived as only marginally different is less likely to attract new category demand and more likely to cause channel shift or cannibalization (Friedman and Furey 1999).

As for the supply-side effects, the learnings achieved in one channel can be translated to the other, thereby reducing the inherent risk of new ventures and allowing the firm to exploit potential economies of scope. However, adopting the Internet as an additional distribution channel may place considerable stress on the existing distribution network. The more direct channels a company establishes, the more wary the incumbent distribution network becomes: It may increasingly view this as the prelude to a conversion to direct channels only (Dutta et al. 1995). In response, distributors may provide lower levels of support for the firm's products, pushing competitors' products instead (Frazier 1999). This may cause some of the firm's customers to switch to one of these competitors. To limit this unfavorable demand evolution, higher transaction costs are required. When we total up these effects, our net prediction is as follows:

The performance potential of an Internet channel addition is negatively related to the scope of direct channel experience.

Firm size

On the demand side, small firms typically have more to gain from an Internet channel addition than large firms do (Alba et al. 1997). Because the Internet greatly extends the geographic reach of small companies, it enables them to secure new customers from around the world in ways formerly restricted to much larger firms (Organisation for Economic Co-operation and Development 1999). Therefore, the smaller the firm, the more it can benefit from the geographic market-expansion and brand-switching opportunities offered by the addition of an Internet channel. In contrast, large firms may be better able to command a higher price/margin. To feel more secure when dealing over the Internet, consumers may be willing to pay a price premium to purchase a product from a large, well-known firm, because its reputation may signal reliability of delivery, security of information, dependability of return policy, and so forth (Smith, Bailey, and Brynjolfsson 2001).

On the supply side, it could be argued that large firms can enjoy economies of scale. The larger the firm, the more efficiently it can fulfill marketing functions in general and distribution functions in particular, and therefore the lower are its physical distribution costs (Anderson 1985). However, in the context of market discontinuities such as the introduction of Internet channels, costly investments and general marketing expertise built up over the years may become useless, and new skills and assets need to be acquired (Mitchell 1989). As a result, the superior resources and capabilities of larger organizations may no longer give them the same cost advantages as in the “old economy.” Because good arguments are available to support higher performance potential for larger (price premium potential) and smaller (demand expansion potential) firms, we do not advance a hypothesis for the relationship between firm size and performance potential.

Introduction Strategy

The introduction strategy for a new channel sets the platform from which competitive advantages can be gained. We consider two introduction decisions: the order of entry and the level of publicity surrounding (media attention given to) the introduction.

Order of entry

On the demand side, order of entry may influence the Internet channel's impact on market expansion, brand switching, relationship deepening, and price. First, the opportunity to benefit from market-expansion effects declines as firms fall further behind in entering the market (Kalyanaram, Robinson, and Urban 1995). Changes in the environment, such as changes in technology, create windows of opportunity. Firms that enter soon after this window has opened are able to “skim off” new category demand, leaving fewer opportunities for firms that enter later (Kerin, Varadarajan, and Peterson 1992). Second, brand-switching advantages are also believed to accrue to early entrants. Early entrants may be able to attract customers from competitors that do not yet have an Internet offering and to avoid some of their own customers switching away to more proactive competitors. Moreover, early movers may shape customer preferences, in that customers come to view the pioneering Internet channel as a prototype against which later entries are judged (Carpenter and Nakamoto 1989). Given a favorable experience, consumers may be reluctant to switch upon later entry of other Internet channels to minimize the risks involved. Third, postponing the introduction of an Internet channel may project an image of not being a dynamic, up-to-date company. This may cause a loss of goodwill among current customers and affect their decisions to buy other products from the firm, that is, the relationship-deepening opportunities (Hendricks and Singhal 1997). Finally, early movers may be able to earn a higher price/ margin if switching costs to competing products and channels are sufficiently high (Lieberman and Montgomery 1988).

On the supply side, early entry may have positive effects on distribution costs. In addition to experience curve effects, marketing cost advantages may accrue to early movers. Later entrants may require more marketing support to overcome the barriers of entry erected by earlier firms in terms of consumer awareness and preference (Kerin, Varadarajan, and Peterson 1992).

Other researchers have advocated early imitation as a profitable alternative (Lee et al. 2000; Teece 1986). Specifically, technological discontinuities may create advantages in physical distribution costs to later entrants. When superior technologies are expected to become available, it may be beneficial to postpone the Internet channel introduction and to immediately incorporate the new technologies when they become available. This may enable later entrants to leapfrog early movers if these stay committed to older technologies (Dos Santos and Peffers 1995). Also, early firms may make costly mistakes, because there is little precedent from which to learn about the idiosyncrasies of the new channel. In contrast, firms that wait until some competitors have made the move can learn from the latter's experience and do better at a lower cost.

In conclusion, the previous argumentation suggests that it may be beneficial to wait and learn from the first mover's experience but still be fast enough to exploit the various demand advantages related to early entry. As such, early followers may reap the greatest benefits and outperform both pioneers and late movers. We therefore propose the following:

The relationship between the performance potential of an Internet channel addition and order of entry takes the form of an inverted U.

This hypothesis focuses on the mere order of entry and abstracts from the time lag among the respective entrants (for an extensive discussion on this issue, see Brown and Lattin 1994). However, the longer the time in market, the longer consumer learning may take place, and therefore the more consumer preferences may be shaped. To account for this consumer learning, we follow the recommendation of Brown and Lattin (1994) and Huff and Robinson (1994) and test the order-of-entry hypothesis while controlling for the time of entry.

Publicity

A second aspect of the introduction strategy involves the level of publicity surrounding (or media attention given to) the introduction, which may have positive demand effects through its impact on market expansion, brand switching, and pricing. Publicity may assist in building awareness and lead to customer trial. It may serve as a credible source of information that helps reduce consumers' insecurities toward the new channel and thus build primary demand (Assael 1998). Publicity can also help a company build selective demand by encouraging brand switching toward its own channel. Moreover, publicity may affect price sensitivity. The “market-power” school of thought contends that publicity may increase brand loyalty and thus reduce price elasticity (Comanor and Wilson 1979). As such, more publicity may enable a firm to charge higher prices for the products/services offered through its Internet channel. On the supply side, publicity is inexpensive or even free of charge—there are few costs other than maintaining a public relations department (Assael 1998). We therefore hypothesize the following:

The performance potential of an Internet channel addition is positively related to the level of publicity.

Marketplace Characteristics

We distinguish between two types of marketplace characteristics: the growth in demand for the product sold through the Internet channel and the growth in demand for the new channel per se.

Product-demand growth

The evolution in product demand may affect the performance potential of a new Internet channel through three demand-side mechanisms. First, a high product-demand growth rate implies a greater incentive for all firms to increase the breadth of their channel system to satisfy various growing consumer segments. This combined effort may cause further market expansion (cf. Bayus and Putsis 1999). Second, because of some untapped demand or need, growth markets provide both existing channels and the new Internet channel with sales opportunities (Dwyer and Oh 1987), making cannibalization less likely because firms do not need to engage in a zero-sum game. Third, in growth markets, consumers' price sensitivity tends to be lower (Aaker and Day 1986).

The supply-side mechanism for the effect of product-demand growth pivots on channel conflict and the corresponding transaction costs. Specifically, “channels in declining markets [are] often associated with intense inter-channel rivalry” (Dwyer and Oh 1987, p. 348). In contrast, in rapidly growing markets, the friction between the firm and its entrenched channels should decrease, because losses in share need not reduce the latter's absolute sales levels. Therefore, we hypothesize the following:

The performance potential of an Internet channel addition is positively related to product-demand growth.

Channel-demand growth

Many scholars have employed a demand-pull perspective toward innovation and change. In this view, the adoption of an important organizational innovation such as the addition of an Internet channel is driven by its revenue-generating potential, which is likely to increase as the Internet community grows (Peterson, Balasubramanian, and Bronnenberg 1997). This growth may come from new customers to the category or may involve a switching from traditional channels (company- or competitor-owned). As for the prices charged, Zettelmeyer (2000) has recently shown analytically that the prices firms set are linked to the reach of the Internet. Specifically, it is shown that as the Internet's reach increases, firms tend to refrain from competitive price discounting over the Internet. Therefore, as the Internet grows, average prices on the Internet increase and need no longer be lower than prices in conventional channels. Still, it has also been argued (e.g., Erevelles, Rolland, and Srinivasan 2000) that current cases in which Internet prices are higher than prices in conventional channels are due to initial market imperfections that will disappear as the market grows and matures. Moreover, as the Internet market grows, the dominance of affluent, time-constrained customers, who are known to be less price sensitive (Degeratu, Rangaswamy, and Wu 2000), is likely to be attenuated.

On the supply side, distributors face higher competition for ownership of customers when channel-demand growth is high as opposed to low (Moriarty and Moran 1990), in which case they become more likely to neglect the firm's products in favor of its competitors' products. This may result in increased switching toward competitors unless the firm takes measures to monitor its distributors, which results in higher transaction costs. Because it is not clear how the opposite effects of the demand and supply forces total up, we do not advance a hypothesis for how channel-demand growth affects the performance potential of an Internet channel addition.

Performance Appraisal of Internet Investments

Evaluating Internet Investments

Performance appraisal of Internet-related investments is quite difficult. Commonly used performance measures such as return on sales, return on assets, and return on equity are found to be less appropriate indicators of an Internet channel's value, because (1) they have a historical orientation as opposed to a forward-looking focus and (2) their temporal aggregation level makes the link to specific events questionable. To deal with these issues, we quantify the performance potential of an Internet channel addition through its impact on the firm's stock return, that is, investors' expectations on the change in future cash flows.

First, Internet channels operate in a setting in which current accounting results are almost bound to suggest poor performance. Indeed, accounting numbers immediately reflect the costs of the investments made, but revenues are only recognized (i.e., put on the books) in the periods they materialize. Because accounting measures only evaluate “historical” performance indicators, they are not well suited to capture anticipated future revenue streams (Kalyanaram, Robinson, and Urban 1995). This is unfortunate, because Internet investments are known to take several years before they fully translate into bottom-line performance effects (Bharadwaj, Bharadwaj, and Konsynski 1999). The stock market reaction, in contrast, compares investment costs with the expected revenues. Although we do not refute the notion that, at some later point in time, realized cash flow data will eventually become available (and that these data are likely to be better than any expectation at the time of the event), we argue that the market expectations as reflected in the stock market reactions are the best option currently available to assess the performance potential of a given Internet investment.

Second, end-of-the-year accounting numbers may be influenced by various factors that took place during the year, of which the Internet channel introduction is just one. The event study methodology advocated in this study (see infra) has the advantage that it enables us to measure the impact of a specific event on daily (i.e., temporally disaggregated) stock returns. For an extensive discussion of these critiques, see Bharadwaj, Bharadwaj, and Konsynski (1999), and for a recent translation to a marketing context, see Doyle (2000, Ch. 1).

Event-Study Methodology

Cash flows are increasingly viewed as less susceptible to the two problems mentioned in the preceding section (Srivastava, Shervani, and Fahey 1998). According to financial theory, a company's stock price reflects the market's expectations of the discounted value of all future cash flows expected to accrue to the firm (Rappaport 1987). Market efficiency implies that the stock price accurately reflects all available information (including information on future expected outcomes) related to the performance of the firm. As new information becomes public, investors update their expectations about long-term future cash flows, reacting immediately by buying or selling stock. As such, information resulting in a positive (negative) change in expected future cash flows will have a positive (negative) effect on stock price. The release of information, or event, we investigate in this study is the announcement of an Internet channel addition.

The percentage change in the stock price is the stock return:

We make the link between the event and the firm's stock returns using the well-established event-study methodology.

2

We compare the stock return Rit at the event day with E(Rit), that is, the return that would be expected if the event had not taken place. Following Brown and Warner (1985), we make use of the market model to obtain estimates of expected returns. According to the market model, the expected return E(Rit) to asset i at time t can be expressed as a linear function of the returns from a benchmark portfolio of marketable assets Rmt:

Event-study methodology, which has been developed and is most popular in the finance literature, has also been applied to assess the impact on a firm's value of marketing-related events such as new product introductions (Chaney, Devinney, and Winer 1991), company name changes (Horsky and Swyngedouw 1987), celebrity endorsements (Agrawal and Kamakura 1995), and brand extensions (Lane and Jacobson 1995).

This abnormal return, or prediction error, is the unexpected change in the stock price, which is then attributed to the event that took place at time t. Because of market efficiency, the abnormal return eit provides an unbiased estimate of the future earnings generated by the event and is a random variable with mean equal to 0.

We conducted an event study across several firms for which the event of interest could have taken place on different calendar dates. We tested the average effect of a particular type of event by first computing the average of the abnormal returns over all announcements:

Thus far, we considered the ideal situation that there is no information leakage prior to the event day and that all information is completely disseminated during the event day. In practice, these assumptions may be violated (McWilliams and Siegel 1997). As soon as information leaks (e.g., a newspaper article speculating about a potential Internet channel introduction prior to the official announcement), the event period should include one or more days prior to the announcement of the event so that abnormal returns associated with the leakage are also captured. In a similar vein, when information becomes only gradually available to the broad public, an allowance should be made for dissemination effects on the days following the announcement. When leakage (for t1 time periods before the event) and/or dissemination over time (for t2 time periods after the event) occur, we can use a similar test statistic as in Equation 5 to compute the significance of the average abnormal return on these days. We can also aggregate the abnormal returns over the event period [-t1, t2] into a cumulative abnormal return (CAR) to draw overall inferences for the event of interest:

Because the event study is conducted over multiple events, this CAR can be averaged across events into a cumulative average abnormal return (CAAR):

We used the t-statistic described by Brown and Warner (1985) for testing the significance of the CAARs for various event windows. Note that the event window should be long enough to capture the significant effect of the event but short enough to exclude confounding effects.

Cross-Sectional Variation in Stock-Price Reactions

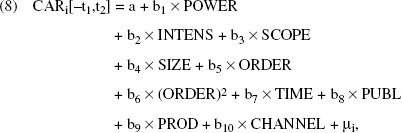

When the event period and the CARs over that period have been established, we examine the cross-sectional variation in the stock-price reactions in more detail. Specifically, we quantify the moderating impact of firm-specific [channel POWER, INTENSity and SCOPE of direct channel experience, and firm SIZE], introduction strategy [ORDER of entry, TIME of entry, and PUBLicity], and marketplace characteristics [PRODuct-demand growth and CHANNEL-demand growth] by regressing the (standardized) cumulative abnormal return against the different covariates:

The standardized CARi are used as dependent variables to reduce heteroskedasticity problems that might arise when the estimated variances of the market model residuals vary across firms and/or events. For a formal motivation, see Jain (1982), and for a similar practice, see Agrawal and Kamakura (1995) and Horsky and Swyngedouw (1987).

Assumptions Underlying Event-Study Methodology

As with any methodology, event studies rely on some key assumptions. Specifically, we assume that (1) shareholders are the only relevant group of stakeholders, (2) researchers can isolate the stock-price reaction of the event of interest, (3) an appropriate benchmark is used to compute the (ab)normal returns, and most critically, (4) the financial markets are efficient (Bromiley, Govekar, and Marcus 1988; McWilliams and Siegel 1997). We discuss Assumption 1 in more detail in the “Discussion” section. To avoid confounding effects (Assumption 2), we must explicitly check whether no other events are announced at or around the time of the Internet channel introduction (for details, see the “Data” section). We extensively test the robustness of our findings to the specific choice of performance benchmark (Assumption 3) in the “Robustness Checks” section.

As for key Assumption 4, researchers must always keep in mind that event studies test a joint hypothesis: whether the event has an impact and the efficiency of the market. In this respect, the issue is to what extent individual investors can integrate all information that becomes publicly available on the different components of our conceptual framework. 5 Friedman (1953) eloquently argues that even when people do not make all the necessary calculations reflected in an economic model, they may still act as if they could do so. Moreover, even if people make mistakes and occasionally act irrational, this still is no problem in explaining aggregate behavior, as long as these mistakes tend to cancel out. In that case, the trading of the irrational investors would not affect market prices, which would be left in the hands of the more rational investors (Rubinstein 2001). Such (often larger) investors, as well as stock analysts, tend to be well informed and indeed use valuation methods based on discounted cash flows, as discussed by Fabozzi (1995), among others. In addition, even if these more informed individual investors do not have all the relevant information, markets tend to exert an information aggregation function, through which they become more rational than the individual investors that constitute them (see Ball 1995; Hayek 1945).

It is worth noting that field interviews were conducted with fund managers from three different banks in both Luxembourg and Belgium to validate the general structure of our developed conceptual framework, which is shown in Equation 8 and Figure 1. All three fund managers reported that the suggested model of moderator effects “is plausible and covers most of the factors that [they] would take into account.”

These arguments all rely on the assumption of either rational or nonsystematic irrational behavior. Systematic irrational behavior, in contrast, would cause the errors to go in the same direction (in which case there would be no cancellation at the aggregate level) and result in certain anomalies. This is especially important in our context, as the recent market interest in buying and selling high-tech and e-stocks has led some authors (e.g., Higson and Briginshaw 2000) to argue that financial markets are no longer efficient. Recent evidence, however, suggests that extremely high share prices are mostly paid for “pure” e-firms (which do not have a bricks-and-mortar counterpart), whereas firms that complement their traditional business with Web-based operations are still judged by normal earnings criteria (The Economist 2000). We nevertheless conduct extensive checks on the robustness and validity of our substantive findings.

Data

Sample and Data-Collection Procedure

Our empirical application is situated in the newspaper industry, which offers an interesting setting in which to apply our framework. First, it represents a mature, old-economy industry that faces rising costs, falling revenues, and increasing retail power (Nicholas et al. 1996). As a result, many publishers have examined more closely the opportunities offered by direct distribution and have wondered whether the Internet may become a profitable option. Although they share these characteristics with many other industries, newspapers have the natural advantage that they can be “delivered” online fairly easily. As a consequence, publishers have taken the lead in exploiting the Internet as a new distribution channel. By the end of 1999, more than 2700 newspapers around the world had online businesses (U.S. Department of Commerce 1998). As such, the publishing industry tends to “act as the pacesetter for the Information Society” (European Commission 1996, p. 1) and is expected to foreshadow trends that will occur more slowly in other industries.

In addition, newspaper executives are confronted with many of the performance-enhancing and performance-destroying forces identified previously, leading them to call the Internet both their prime concern and their most promising source of new revenues (Casale 2000). On the demand side, most online newspapers do not yet generate adequate revenues. Newspaper revenues come from two sources: circulation and advertising. In terms of circulation, most publishers are still reluctant to charge for their online editions. It is unclear, however, whether this situation will persist in the future, and some publishers already experiment with subscription schemes (The Economist 1998). Second, it is unclear to what extent cannibalization threats will materialize. Many Internet newsreaders still consume both mainstream and online news sources (www.poynter.org/eye-track2000). In addition, online newspapers may be able to attract readers who live abroad and/or to gain access to segments (e.g., young, with average to high social standing) in which traditional readership is declining (Picard and Brody 1997). Traditionally, advertising and circulation revenue streams are positively related. In the new economy, advertisers may well decide, even if the newspaper's total audience stays the same, to shift advertising spending from the print to the Internet edition (cannibalization) or other Internet hosts (brand switching) if they believe that this provides a more effective means to reach their audience. Other analysts expect advertising revenues through the Internet editions “to become an important driver of revenue growth” (as stated by the 1998 Newsquest Annual Report). On the supply side, newspaper executives do not yet have enough experience to draw firm conclusions on cost implications. On the one hand, online editions require a lower capital investment, and the marginal cost of distributing extra copies is negligible. On the other hand, costs may simply shift from physical printing and distribution to acquiring and maintaining technology while incurring higher marketing costs (U.S. Department of Commerce 1998). There is also uncertainty about the transaction costs involved. Some experts argue that online newspapers will not replace the print versions. Others fear that their distributors may interpret online editions as a declaration of war (Noack 1993). In summary, considerable uncertainty prevails on both the demand and the supply side, making the newspaper industry a good test case.

We identified all daily newspapers from four European countries (France, Germany, the Netherlands, and the United Kingdom) that have ventured on the Internet. Our search led to the identification of 7 French, 5 German, 23 Dutch, and 63 English newspapers that have embraced the Internet as an additional channel of distribution and whose parent firms are listed on the stock exchange. These 98 newspapers represent 22 different firms. We considered the event date to be the day the announcement was mentioned in the media. 6 We gathered information on the announcement date by contacting each newspaper, and we extensively validated it through both newspaper archive searches and the Dow Jones Interactive Publication Library. According to the theory of efficient markets, all new information is incorporated in the stock price as soon as the information becomes available. Therefore, to assess the impact of an event, we examined the change in stock price on and surrounding the date of the announcement. 7

To avoid confounding effects, we checked whether no other events were announced at or around the time of the Internet channel introduction. To this extent, we systematically searched the Dow Jones Interactive Publication Library, Wright Investors' Service, Hoover's Online, and the major financial newspapers of the countries included in our sample. As a result, we deleted two events from our sample, because we found that company results were announced simultaneously. In addition, two newspapers that had followed a strategy of gradual turnover and one outlier (with a standardized residual greater than 3) were removed from the sample. Our final sample therefore consists of 93 announcements.

This announcement may occur before the date of the actual Internet channel introduction. For the majority of newspapers, they turned out to be the same, and in our subsequent analyses, we found no significant impact when we controlled for this joint occurrence.

Operationalization of Measures

Financial measures

We obtained daily stock prices of the firms included in our sample and daily market indices of the Amsterdam, Frankfurt, London, and Paris Stock Exchanges (i.e., AEX-24, DAX-30, FTSE-100, and CAC-40) from the Datastream database. We used these data to calculate the firms' daily returns, Rit, and the market returns, Rmt.

Channel power

Following Emerson (1962), we included a measure for both motivational investment and availability of alternatives to capture channel power. We measured the former as the percentage of sales the newspaper accounts for in the total sales of an average distributor in the sales region in which the newspaper is being sold (median = 4.6%, range = .1%–55%). 8 We measured availability of alternatives through the number of titles distributors in a sales region can use to replace the sales accounted for by the focal newspaper (median = 3, range = 1–19). We measured both motivational investment and availability of alternatives on a per–sales-region basis, because distributors in the same region are highly similar in terms of these two constructs— distributors in the same region can use the same number of titles to replace the focal newspaper and derive roughly the same proportion of sales from these newspapers. 9 Because the power of a supplier over a distributor is (1) directly proportional to the supplier's contribution to the distributor's sales and (2) inversely proportional to the number of alternatives available to the distributor, we measured channel power by the ratio of contribution-to-sales to number-of-alternatives, after standardization of both measures. We obtained all relevant data from the International Federation of Audit Bureaux of Circulations (IFABC). 10

Marketing channel studies have often combined a contribution-to-sales measure with a contribution-to-profits measure to construct an index of motivational investment. Unfortunately, we were not able to include contribution to profits because of data limitations. However, we can expect a high correlation between contribution to profits and contribution to sales in our specific newspaper setting. Indeed, prices of different newspapers show little variation, agency commissions barely vary, and we were informed by the IFABC that there is no reason to assume that a distributor's cost structure would be different for different newspapers. Therefore, restricting the measurement of motivational investment to contribution to sales is not likely to affect our substantive results.

Note that a manufacturer's channel power is distributor specific; that is, it can vary across its distributors. Because our study takes the firm as the unit of analysis (and not the individual manufacturer–distributor relationship), we were unable to take into account these differences across distributors. We addressed this issue by measuring motivational investment and availability of alternatives per sales region, because distributors in the same sales region are highly similar in terms of these two constructs. More specifically, sales regions are regions where the same set of newspapers is being sold. As a consequence, the number of titles distributors in a specific sales region can use to replace the focal newspaper (i.e., availability of alternatives) is the same across all distributors within the same sales region. The percentage of sales the newspaper accounts for in the total sales of a distributor (i.e., motivational investment) by definition is not equal across all distributors within a specific sales region. However, we were informed by the IFABC that, because of the idiosyncrasies of the newspaper industry, the percentage of sales that distributors within a region derive from various newspapers is approximately the same (even though they can vary widely in terms of sales levels).

Regional newspapers are typically sold in a single sales region (personal communication with IFABC). National newspapers, by definition, are available in multiple regions. To make the measures comparable across both types of newspapers, we computed a population-weighted average across regions for the national newspapers.

Intensity and scope of experience

Following Erramilli (1991), we operationalized intensity of direct channel experience as the number of days the firm was engaged in direct channel operations prior to the current Internet channel addition (median = 342, range = 0–1710). We operationalized scope of direct channel experience as the number of direct channels established by the firm before the current Internet channel addition (median = 3, range = 1–18). 11 We obtained data on intensity and scope of experience by contacting each newspaper, and we extensively validated these data by searching annual reports and newspaper archives.

Given that each firm, through the nature of its business, tends to have a nonvirtual direct channel, the variation in this figure captures the number of virtual channels established by the firm before the current Internet channel.

Firm size

We compiled three measures of firm size from Wright Investors' Service: number of employees (median = 6477, range = 400–49,285), sales (median = €700 million, range = €56 million–€12,284 million), and the market value of the firm (median = €2,307 million, range = €76 million– €38,550 million). After standardization, we averaged the three items into a single scale of firm size. We log-transformed firm size to account for potential diminishing returns to scale. 12 Through this transformation, we also reduced the skewness in this variable, thereby avoiding having a few extreme observations drive our results (see, e.g., Dekimpe et al. 1997).

Because the three items were standardized before being averaged, negative values for firm size may result. A small, positive value was therefore added to ensure the nonnegativity before taking the logarithm.

Order and time of entry

Order of entry is the temporal rank order position, compared with other Internet entries in a given country (median = 28, range = 1–87). It is important to realize that in operationalizing this variable, we also account for entries made by firms not listed on the stock exchange. Time of entry is measured as the number of days the newspaper went online after the first release of Netscape Navigator on December 15, 1994 (median = 1060, range = 16–2204).

Publicity

Publicity measures whether media attention was given in the printed press to the Internet channel addition. It is a binary variable coded 1 if the Internet channel was announced in other newspapers than in the own newspaper (15% of the cases) and 0 otherwise (85% of the cases). We compiled our measure of publicity on the basis of searches of newspaper archives and the Dow Jones Interactive Publication Library.

Product- and channel-demand growth

Product-demand growth is the percent change in the industry's sales from the previous month's sales for each month of the analysis (median = 0%, range = −3.6%–3.4%). To reflect that newspapers may be competing internationally, sales include domestic and foreign sales. To measure channel-demand growth, we used the monthly growth rate in the total number of Internet users per language (median = 3.5%, range = 2.3%–18.5%). We obtained product-demand growth and channel-demand growth data from the IFABC and Global Reach (www.glreach.com), respectively.13,14

In approximately 30% of the cases, monthly data were not available. In these cases, we intrapolated using the estimates obtained through an auxiliary regression model. For example, in case of the Netherlands, where no annual circulation data are collected, we fitted a quadratic model (several specifications were tested, and the best fitting alternative was retained) with an R2 amounting to .91.

Because events are recorded daily whereas firm and market data are available only on a yearly and monthly basis, respectively, and to avoid endogeneity problems, we consistently use the values for the firm and market variables in the year and month, respectively, prior to the event. In addition, we deflated all monetary values.

Results

The Main Effect of an Internet Channel Addition

For each firm i, we estimated the parameters (αi and βi) of the market model in Equation 2 using an estimation period of 219 days (t = −250 to t = −30 relative to the event day, t = 0). We then used the estimated market model parameters to calculate the firms' abnormal returns (eit). Table 2 presents the average abnormal returns for the 93 announcements on the event day, as well as for a window of +5 days around the event day. Results show that, on average, firms establishing an Internet channel experienced .35% abnormal returns on t = 0 (p < .01) and .36% abnormal returns on t = +1 (p < .01). Of all windows surrounding the event day, the one from 0 to +1 shows the most significant CAAR, with a value of .71%. This positive value is driven by two factors: Positive evaluations occur more frequently (58% of the cases on the event day t = 0, and 64% of the cases on t = +1), and they are, on average, larger than the negative ones (the average positive CAAR over the event window [0,+1] is 1.83%, versus an average negative CAAR value of −1.36%). Our short event window of [0,+1] implies an almost instantaneous adjustment in stock prices to the arrival of the new Internet channel information, which is a necessary condition for market efficiency (McWilliams and Siegel 1997). Our estimate on the size of the stock market reaction to Internet channel announcements has the same order of magnitude as CAARs reported in other marketing-related event studies. Horsky and Swyngedouw (1987), for example, report a CAAR[0,0] of .61% for company name changes; Chaney, Devinney, and Winer (1991) find a CAAR[-1,+1] of .75% for new product announcements; and Agrawal and Kamakura (1995) report a CAAR[–1,0] of .54% in the context of celebrity endorsement contracts. Apart from the statistical significance of the CAAR values obtained, we consider their economic significance. To that extent, we calculated the average change in the market value of a median-sized firm in our sample. 15 A .71% cumulative abnormal return for such a company with a market value of €2,307 million results in an increase in market value (adjusted for overall market movements) of €16.38 million in two days.

Abnormal Returns for Internet Channel Additions

This column presents the percentage of the 93 abnormal returns that are positive for each day. For example, 58% of all cases had a positive abnormal return on the event day.

p < .01.

The market value of the firm on any trading day is the number of common shares outstanding times the share price at the end of that trading day.

Despite this statistical and economic significance, questions remain as to whether this positive evaluation is just a temporary reaction that is quickly corrected afterward. We found in this respect that the CAARs (see Figure 2) stayed at a higher level after the event, indicating that the positive evaluation is not just a short-term lift that evaporates in the days following the announcement. For newspapers that introduced their Internet version before November 8, 2000 (resulting in a sample size of 87), we subsequently computed the abnormal returns for up to 100 (trading) days after their announcement. Also, in this longer postannouncement period, no significant negative drift is observed, as is confirmed in a pooled regression of the CARs against the time since announcement (btime = .00, p > .10).

CAARs over Time

Identification of Successful Internet Channel Additions

The addition of an Internet channel to a firm's channel portfolio is, on average, evaluated positively by the financial markets. Still, we cannot ignore the finding that in more than 30% of the cases, negative stock returns are found (Table 2, last column), which indicates that the market at times expects the negative consequences to outweigh the positive ones. Therefore, a final aim of this article is to cross-sectionally explain the variation in observed stock-price reactions. For this purpose, we estimate Equation 8. 16 , 17 The results are presented in Table 3.

Moderator Analysis

p < .05 (one-sided).

p < .01 (one-sided).

p < .01 (two-sided).

It might be argued that the level of aggregation differs between dependent (corporate-level stock returns) and independent (information on a specific newspaper) variables. Ideally, we would want to run the regression SRNP = βX + μ, where SRNP is the stock returns associated exclusively with a particular newspaper. In reality, however, we ran the following regression: SR = bX + μ', where SR is the corporate stock return, which is composed of SRNP and SRnot-NP, the stock return of the publishing company not associated with the specific newspaper. Because SR = (SRNP + SRnot-NP), it can be shown that

To correct for a potential violation of the statistical-independence assumption (the 93 newspapers represent 22 different firms from four different countries), we implemented a fixed-effects correction for both dimensions in the regression equation. Two firm dummies turned out to be significant and were added to Equation 8. None of the country dummies was significant. White's test for heteroskedasticity turned out to be insignificant (p > .75), justifying the use of ordinary least squares as an estimation procedure.

Channel power has the anticipated positive effect (b = .650, p < .05). Therefore, H1 is supported. The effect of intensity of direct channel experience is positive, as expected, but not significant (H2; p > .05). Scope of direct channel experience has the hypothesized negative effect (b = -.938, p < .05). Therefore, H3 is supported. Firm size does not have a significant effect on the performance potential of an Internet channel addition (p > .05). The results for order of entry support H4. The positive linear (b = .133, p < .01) and negative quadratic (b = -.001, p < .05) effects imply more favorable stock market reactions for early followers than for both pioneers and later entrants. 18 As hypothesized (H5), additional publicity positively affects the stock market reaction (b = 1.175, p < .05). Finally, the performance potential of an Internet channel addition is not significantly affected by either product-demand growth (H6; p > .05) or channel-demand growth (p > .05). Therefore, powerful firms with fewer direct channels achieve greater gains in financial performance than do less powerful firms with a broader direct channel offering. Small firms should not recoil from adding an Internet channel to their entrenched channels; firms of any size can successfully play the game. Early followers have an advantage over both innovators and later followers, even when we control for time of entry. We also find that firms that provide additional publicity to their Internet channel introduction achieve greater gains.

We mean-centered the order-of-entry variable (before forming the quadratic term) to reduce multicollinearity (Jaccard, Turrisi, and Wan 1991).

Robustness Checks

We evaluate our results in four ways. We first calculate the CARs using three alternative stock portfolios. Next, we assess the stability of the results, the forecasting performance of the model, and the extent to which our data support some alternative (competing) explanations.

Alternative CARs

We use three alternative benchmark portfolios to determine the market and abnormal returns: (1) a market portfolio of stocks (used in Tables 2 and 3), which is the daily market index of the exchange the stock is trading on; (2) a broad portfolio of stocks; 19 and (3) a portfolio consisting only of printing and publishing companies that trade on the same exchange as the stock. Our results remain substantively the same, with CAARs[0,+1] of .71% (standard portfolio), .70% (broad portfolio), and .65% (publishing portfolio). We then reestimate Equation 8 using these alternative CARs as dependent variables. With one exception (the coefficient for publicity becomes insignificant when we use the portfolio of printing and publishing stocks), all results remain substantively the same. Therefore, our results are robust to the choice of market portfolio.

The broad portfolio of stocks, which was obtained from the Datastream database, includes the most important companies by market value. The precise number of constituents varies from market to market. The number of stocks included in the French, German, Dutch, and U.K. broad-based portfolios amounts to 200, 200, 130, and 550, respectively.

Stability of the Results

We use a jackknife procedure to test the stability of our parameter estimates. We calculate the jackknifed coefficients as described by Ang (1998). Our results are stable given that the t-values of the jackknifed coefficients for our significant coefficients range from 1.95 to 3.09.

Forecasting Performance

We assess the forecasting performance of our model using a procedure similar to the one by Dekimpe and colleagues (1997). Specifically, we omit the first 10% of the observations of the randomized sample and estimate the model on the basis of the remaining data points. We then use the resulting parameter estimates to forecast the omitted observations and compute the mean squared prediction error. Next, we repeat this procedure for the next 10%, until we have rotated the entire data set. Each time, we compute the mean squared prediction error, which is subsequently averaged across the different iterations. The resulting mean squared prediction error turns out to be only 8.6% higher than the mean squared estimation error, which is comparable to the results reported in previous studies. The average correlation between the holdout observations and their forecasts is .50 when calibrated on the subsamples, as opposed to .59 when these forecasts are derived from a full-sample estimation. Because the latter figure offers an upper bound (as it uses all information in the sample), the drop in correlation is limited.

Ruling Out Alternative Explanations

It could be argued that our results are consistent with two alternative explanations. First, there is the possibility that the addition of an Internet channel does not offer real value to the firm but merely acts as a signal that the firm is innovative and responsive to changes in the marketplace and in technology. Second, questions remain as to what extent our findings are merely an artifact of the general hype surrounding high-tech and e-related stocks.

A signal of innovativeness

We followed the approach advocated by Horsky and Swyngedouw (1987) to empirically rule out the signaling hypothesis. Specifically, two of our hypotheses predict a particular directional effect that would not be found under the signaling hypothesis. First, our framework predicts a positive effect of channel power, whereas no link with channel power would be expected if Internet additions merely acted as a signal of innovativeness (i.e., distributors would prefer all their channel partners to be innovative, regardless of whether they are low or high in channel power). Second, our framework predicts a nonmonotonic relationship for order of entry, whereas a monotonically decreasing effect would be expected under the signaling hypothesis (i.e., the innovativeness content of the signal decreases as a firm lags other players in the market). Our empirical results, with a positive effect for channel power and a nonmonotonic effect for order of entry, enable us to reject the signaling hypothesis in both cases. 20

It is interesting to note that not every moderating factor allows for a formal test against the signaling hypothesis. For example, following Horsky and Swyngedouw (1987, p. 329) and according to the signaling hypothesis, we would expect a larger impact for Internet additions of smaller firms, because organizational inertia hampering innovative change will be lower for smaller than for larger firms. Our framework does not predict a directional effect for firm size, however. As such, our empirical result with a positive nonsignificant effect for firm size does not allow discriminating among both theories.

The hype surrounding Internet stocks

It could be argued that the positive stock market evaluation we observed reflects a general hype surrounding all technology-related stocks. We therefore added four tests of this alternative explanation on the basis of an approach recently advocated by Cooper, Dimitrov, and Rau (2001). First, we used the Datastream European Internet index as benchmark to calculate abnormal returns, in which case the benchmark would already capture the hype effect. Even when we corrected for the general overvaluation that might affect Internet-related investments (through the use of an Internet portfolio), the market, on average, still reacted positively to companies announcing that they are expanding into Internet channels, as was evidenced by a CAAR[0,+1] of .67%. We also estimated Equation 8 using the Datastream European Internet index as benchmark. All results remained substantively the same. Second, we compared the size of the announcement effect in the sample across up and down periods by calculating the monthly index return for the Datastream European Internet index for each of the 74 months from December 1994 to January 2001 and ranked the months according to the average return on the index. We subsequently computed CARs for all firms with announcement dates in the top 37 months (for which the index returns ranged from 0% to 137.5%). We repeated this for firms with announcement dates in the bottom 37 months (for which the index returns ranged from −55.5% to −5%). Forty-two firms announced Internet channel additions in up markets, and 51 firms announced Internet channel additions in down months. A t-test fails to reject the hypothesis that the CARs are significantly different across up and down months (p = .90). Third, we distinguished between periods with much versus little Internet activity in the industry we study. If firms attempt to take advantage of a hype effect, Internet channel launches would be clustered in “hot” market periods. To test this, we computed the number of launches per quarter. We then computed average abnormal returns earned by firms that launched an Internet channel in quarters with six or more launches (N = 55) and compared these with the returns earned by firms in nonclustering quarters (N = 38). Again, the difference was not significant (p = .55). Fourth, we examined returns both before and after March 27, 2000, which is often referred to as the date the presumed high-tech bubble burst. Eighty-seven firms announced Internet channel launches before the “plunge” in e-commerce stocks on March 27, 2000. Again, CAARs were not significantly different (p = .19). Finally, we included three dummies in Equation 8 to control simultaneously for the three previous effects. All effects were nonsignificant (p = .15, .86, and .18), and results remained substantively the same. In summary, no empirical evidence was found that our results are driven by an assumed hype effect.

Discussion

Adding an Internet channel to an entrenched channel system is a double-edged strategy: Although it costs money in the short run, it is as yet unclear whether the optimistic foresights about the long-term profit and growth potential will ever materialize. Yet managers of established firms feel pressured to decide now how to best respond to this market discontinuity. We show that, on average, stock market investors perceive that the expected gains of adding an Internet channel outweigh the present and expected costs. As such, managers and shareholders of established companies need not worry unduly about the stock market reaction as investments into Internet channels are announced. However, they cannot take for granted that the stock market will always react positively either; the market recognizes not only the potential gains but also the possible deleterious effects of adding an Internet channel, as is reflected by more than 30% of the cases resulting in negative stock returns. Therefore, it is imperative for managers to know what drives the success of an Internet channel addition strategy.

Substantive Implications

Major managerial guidelines emerging from our study are as follows:

Do powerful firms fare better when adding an Internet channel? Powerful firms can get away with far more when supplementing their entrenched channel system with an Internet channel. Although any firm that sets up an Internet channel should expect to lose at least some of the goodwill of its entrenched channels, powerful firms can use their market clout to ensure that these distributors continue to live up to their agreements.

Does more direct channel experience offer an advantage? Marketers generally view prior experience as an important driver for the success of new entries. We find that established firms that already have many other direct channels are financially hurt when adding a new Internet channel to their entrenched channel system. This supports our contention that adding an Internet channel is not likely to bring along substantial new category demand but instead may cause cannibalization and/or brand-damaging interchannel conflict.

Is size an important driver of Internet channel success? Small firms should not recoil from adding an Internet channel to their entrenched channel system: Firms of any size can successfully enter the playing field. Apparently, the geographic demand expansion opportunities flowing disproportionately to smaller firms compensate for the price premiums larger firms may enjoy. In addition, the superior resources and management skills of large firms no longer appear to give them the same physical distribution cost advantages as in the old economy.

Should firms strive to be first when adopting an Internet channel? Our results indicate that firms should indeed be fast. However, we also find that it may be beneficial to let a few other players enter first. Although firms should be fast enough to exploit various demand-side advantages, there is value in letting others experiment with different technical approaches and designs, thereby improving the new channel. We therefore recommend firms to be early followers rather than pioneers with respect to Internet channels.

Does publicity help make an Internet channel addition successful? Publicity substantially contributes to the success of an Internet channel addition. This result suggests strong, positive effects of publicity on market expansion, brand switching, and/or profit margins.

Does Internet channel success hinge on marketplace characteristics? Companies in declining product markets should not worry more than companies in growth markets about tarnishing channel equity when adding an Internet channel to their entrenched channel system. Also, growth in channel demand does not affect Internet channel success. Apparently, the possibility that new customers may be drawn to the category through the new channel does not outweigh concerns about potential losses of revenue due to competition for the “ownership” of customers.

One question is to what extent these findings are merely of historical interest, as the extent of press coverage on Internet introductions may well create the impression that all firms have already implemented the decision to add an Internet channel to their channel portfolios. Although this may be the case in some industries, note that many firms have not yet established an Internet presence and many others use their Web sites only for promotional purposes and not yet as distribution channels. In a recent large-scale survey of Belgian firms, Konings and Roodhooft (2000) find that of all firms that have access to the Internet, only 57% have their own Web sites, and an even smaller fraction (15%) uses those sites as additional channels to sell products online. In the United States, recent estimates indicate that more than 40% of all businesses do not yet sell online (www.nua.com/surveys; www.ecommercecommission.org), a number that increases to more than 70% when the largest businesses are excluded (The Washington Post 2001).

Limitations and Further Research