Abstract

Firms allocate their limited resources between two fundamental processes of creating value (i.e., innovating, producing, and delivering products to the market) and appropriating value (i.e., extracting profits in the marketplace). Although both value creation and value appropriation are required for achieving sustained competitive advantage, a firm has significant latitude in deciding the extent to which it emphasizes one over the other. What effect does strategic emphasis (i.e., emphasis on value creation versus value appropriation) have on firm's financial performance? The authors address this issue by examining the effect that shifts in strategic emphasis have on stock return. They find that the stock market reacts favorably when a firm increases its emphasis on value appropriation relative to value creation. This effect, however, is moderated by firm and industry characteristics, in particular, financial performance, the past level of strategic emphasis of the firm, and the technological environment in which the firm operates. These results do not negate the importance of value creation capabilities, but rather highlight the importance of isolating mechanisms that enable the firm to appropriate some of the value it has created.

Value creation alone, however, is insufficient to achieve financial success. A second necessary process involves a firm's ability to restrict competitive forces (e.g., erect barriers to imitation) so as to be able to appropriate some of the value that it has created in the form of profit. Indeed, firms have little incentive to engage in value creation in the absence of “isolating mechanisms” that prevent the immediate dissipation of profits associated with a value creating initiative (e.g., an innovation). Firms that do not have the capabilities to restrict competitive forces are unable to appropriate the value they have created. Instead, competitors and customers will claim it (Ghemawat 1991). Factors as varied as reputation and brand effects, customer switching costs, advertising, and network externalities, for example, are isolating mechanisms that are central considerations to marketing managers.

Firms are faced with the strategic task of balancing the two processes in their marketing strategies and determining an adequate amount of support for each. Firms need to simultaneously develop or acquire value creation capabilities and capabilities that facilitate value appropriation. These two sets of capabilities require substantial resource commitments and management attention. The task of allocating limited organizational resources between value creation and value appropriation capabilities necessitates strategic prioritizations and trade-offs. As such, we define strategic emphasis as the relative emphasis a firm places on value appropriation relative to value creation. A fundamental issue facing managers is deciding how a firm chooses to compete (Day 1994). Strategic emphasis is a central aspect of this choice.

Research in marketing has extensively explored how acquiring resources and skills and developing different capabilities affects financial performance (see, e.g., the meta-analysis by Capon, Farley, and Hoenig [1990]). Although less study has been directed toward assessing the relative benefits of emphasizing one capability over another, prior research has highlighted various types of strategic and tactical trade-offs that firms make. For example, Porter (1996) considers the trade-offs involved in positioning strategies, Miles and Snow (1978) propose alternative strategic archetypes, Boulding and Lee (1992) address the issue of marketing mix specialization versus diversity, and Ettlie and Johnson (1994) note the trade-off between focusing on customers and processes. Although the inherent trade-off between value appropriation and value creation capabilities has been acknowledged (e.g., March 1991), research to date has not explored what effect strategic emphasis has on financial performance. Our study addresses this issue by examining the effect shifts in strategic emphasis (i.e., the emphasis on value appropriation versus value creation capabilities) have on stock return.

Our analysis makes use of movements in the {[advertising expenditures – research and development (R&D) expenditures]/assets} ratio as an indicator of shifts in strategic emphasis. Although other factors also influence value appropriation and value creation, movements in this measure can be expected to provide information about shifts in strategic emphasis related to value appropriation versus value creation. That is, increases in the ratio will tend to be associated with increased emphasis on value appropriation, and decreases in the ratio will tend to be associated with increased emphasis on value creation. Empirically, we find that the stock market reacts favorably when a firm increases its emphasis on value appropriation rather than on value creation. However, this effect is moderated by firm and industry characteristics, in particular, financial performance, the past level of strategic emphasis of the firm, and the technological environment in which the firm operates. These results do not negate the importance of value creation capabilities, but rather highlight the importance of isolating mechanisms that enable the firm to appropriate some of the value it has created.

Value Creation and Value Appropriation

Firms engage in innovative activities that lead to creation of societal value, that is, the total social surplus arising from the difference between the utility that consumers derive from the product and the costs of producing it. The societal value will end up being captured by three major players in the market: The innovating firm will appropriate some of the societal value it has created in the form of economic profit, the customers will claim a portion of it in the form of consumer surplus, and other firms (competitors and noncompetitors) will get a portion of it through profits stemming from imitation and development cost savings (Mansfield et al. 1977).

Considerable variation exists across innovations as to the proportion of the surplus captured by each of the major players. The polio vaccine is perhaps the most extreme example of an innovation that created tremendous societal value, but where the innovator did not appropriate any surplus. Jonas Salk did not patent the vaccine (stating a desire not to personally profit from it) but rather wished the vaccine to be disseminated as widely as possible. As such, consumers claimed the entire surplus from the innovation.

Even firms with a desire for profit often do not profit from their innovations. For example, the CT scanner was invented by EMI Ltd., but the firm's inability to profit from the innovation led to its takeover around the same time the inventors were receiving the Nobel Prize in Medicine. Competitors and consumers claimed the surplus generated by the innovation. However, it is the hope of realizing profits that motivates firms to innovate. Indeed, countless examples exist in which a firm captured considerable surplus from its innovation. Dupont with Teflon, G.D. Searle with NutraSweet, Microsoft with Windows, and Pfizer with Viagra, for example, were all able to appropriate a substantial proportion of the societal value created by their innovations.

As such, both value creation and value appropriation capabilities are required for achieving sustained competitive advantage (Figure 1). A firm, however, has significant latitude in deciding the extent to which it emphasizes one set of capabilities as opposed to the other. They both shape the firm's competitive advantage (Ghemawat 1991; Rumelt 1987). Value creation influences the potential magnitude of the advantage; value appropriation influences the amount of the advantage the firm is able to capture and the length of time the advantage persists. Because firm value depends on both the magnitude and the persistence of advantage, both processes influence financial performance. As such, they both complement and serve as imperfect substitutes for each other.

Marketing Strategy and the Sustainable Competitive Advantage Framework

Strategic Emphasis: Trading off between Value Creation and Value Appropriation Capabilities

Firms divide their limited resources and attention between the two fundamental processes of creating and appropriating value. As a result, trade-offs occur between developing customer-value creation capabilities and developing value appropriation capabilities. A firm is forced to prioritize its resources between these alternative uses according to the way it has chosen to compete.

At one end of the spectrum, a firm may choose to compete primarily on the basis of value creation. It constantly moves ahead and innovates as competition erodes the profits from its previous initiatives. Alternatively, a firm can choose to fiercely defend its position in the market against competition by erecting barriers to imitation through, for example, brand-based advertising. In this case, a firm attempts to lengthen the time its advantage persists.

Most companies avoid the extremes and strive to choose a strategy that balances sufficient support for value creation efforts with adequate investments in capabilities that facilitate the appropriation of value. Yet differences in strategic emphasis exist among firms. Although industry characteristics shape the options available to the firm, even within the same industry, firms will take different courses of action reflected in different levels of strategic emphasis.

Consider, for example, ethical drug companies. Value creation, such as the development of new drugs, is central to success for firms in the industry. However, companies vary in the degree to which they emphasize value creation relative to value appropriation. For example, as the patent protection for a drug ends and generic clones enter the market, many firms discontinue support for the drug and focus on new innovation and the remaining patent-protected products. Alternatively, other drug companies place more emphasis on value appropriation. For example, Johnson & Johnson uses an umbrella brand for its products and successfully competes with generic drug manufacturers on the basis of superior brand image after the patent protection expires.

Operationalizing Strategic Emphasis

Various organizational resources and capabilities (i.e., technological, financial, physical, legal, human, organizational, informational, and relational) influence value creation and value appropriation. Most resources cannot be exclusively classified as pertaining just to value creation or to value appropriation: They influence both.

Yet two elements have been consistently highlighted in prior research as central to the value creation and value appropriation processes. That is, a firm's technology capabilities driven by R&D expenditures have been linked to value creation, whereas a firm's ability to differentiate its offering through advertising has been linked to value appropriation.

Technology in the Value Creation Process

Schumpeter (1942, p. 132) discusses value creation activities as “to reform or revolutionize the pattern of production by exploiting an invention, or more generally, an untried technological possibility for producing a new commodity or producing an old one in a new way, by opening up a new source of supply of materials or a new outlet for products, by reorganizing an industry.” As such, value creation uses various organizational resources and encompasses a wide range of activities. Yet it is the innovations resulting from R&D that have received the most attention as a cornerstone of value creation. Firms engage in R&D and build technological capabilities to generate superior products and improvements in the production and distribution processes. A firm uses its technological capability to build a new solution and to answer and meet new needs of the users (Gatignon and Xuereb 1997).

Value is created both through product innovations used by firms and/or households and through process innovation (Mansfield et al. 1977). An extensive literature in economics, stimulated by the work of Solow (1957), has documented a significant positive effect of R&D on economic growth and productivity. Some of the estimates from initial research in the area serve as useful benchmarks. For example, Denison (1962) reports that approximately 40% of the total increase in per capita national income was attributable to technological change and conjectures that about one-fifth of this amount stemmed from “organized R&D.” Mansfield and colleagues (1977) estimate the median social return to R&D at 56%. Although estimates vary, Griliches (1995) notes that all recent studies of R&D continue to report significant social returns from it.

A great deal of interest has been devoted to the gap between the societal value created and the profits appropriated by the innovating firm. At issue is that the returns realized by the innovating firm may bear little relation to the commercial success of the product or process it introduces. In theory, patents provide a solution to the problem of imperfect appropriability. However, in practice, patent protection has proved to offer only limited effectiveness. Competitors can “invent around” the patent. Levin and colleagues (1987) report that managers view other mechanisms as much more effective than patents in appropriating the returns from innovation (e.g., in only 4% of the industries surveyed did managers view patent protection as highly effective). In particular, marketing activities, such as advertising, were viewed as central isolating mechanisms and far more effective than patents in capturing advantages generated by R&D activities.

Advertising in the Value Appropriation Process

Just as there does not exist a single organizational factor that uniquely defines value creation, no single capability or activity determines a firm's ability to appropriate value. Several different capabilities give rise to isolating mechanisms and influence the length of time a firm is able to earn economic profits. Accumulated assets, as varied as a loyal customer base and network externalities, serve as isolating mechanisms and influence the ability of competitors to dissipate a firm's advantage. One key component of value appropriation capability that is of particular concern to marketing managers relates to the effects of advertising.

Two polar views exist with respect to the role of advertising as an isolating mechanism. One view argues that advertising is anticompetitive (i.e., erects barriers to imitation by differentiating the firm's offering). The opposing view regards advertising as procompetitive, in that it provides information that serves to dissipate competitors’ isolating mechanisms. Although the debate of the aggregate competitive effect of advertising is likely to be never-ending, both views suggest that a firm's advertising will improve its position by either lengthening its value appropriation opportunities or reducing the value appropriation opportunities of its competitors.

Of these two, the first—the ability of advertising to differentiate a firm's offering from that of competitors—has received the most attention (Chamberlin 1933). This ability is one of the central features governing brand strategy. For example, Aaker (1996) notes that a brand can serve as the foundation for meaningful differentiation, especially in contexts in which brands are similar with respect to product attributes. A brand can be a formidable barrier to imitation, making it difficult for competitors to copy and dissipate a firm's advantage. As such, brand-based differentiation serves to prolong a firm's advantage and is frequently used as an entry deterrence strategy (Bunch and Smiley 1992).

Indeed, the often-cited Advertising Age (1983) study reports that of 25 leading consumer brands of 1923, 19 still remained leaders 50 years later. Although the length of time this stability actually lasts is subject to question (Golder 2000), few question the durability of advantage enjoyed by well-established brands. This durability stems not from the product attributes, which are typically readily imitable, but from the differentiation sustained by advertising. Indeed, Golder (2000) highlights advertising as one of the key factors that separates market share leaders that maintain their advantage from those that do not. For example, in contrast to American Chicle, which attempted to maximize short-term profits by minimizing marketing expenditures, Wrigley invested in building its brand through a commitment to advertising. 1

Golder (2000) also notes Underwood's inability to sustain its place in the typewriter market as a result of a failure to innovate. Again, this highlights the need for firms to invest in both value creation and value appropriation capabilities.

Empirical evidence regarding the effect of advertising on value appropriation capabilities (e.g., the persistence of profits) is sparse but consistent. The empirical results suggest a significant positive effect of advertising on persistence of profits (e.g., Kessides 1990; Mueller 1990). These findings reinforce the view that excess returns erode more slowly for firms advertising heavily. Thus, firm advertising facilitates value appropriation because it extends the duration of competitive advantage.

This is not to suggest that no advertising creates value. Rather, our contention is that the association of advertising with value creation is substantially weaker than the association between R&D and value creation. Indeed, in contrast to the substantial empirical literature highlighting the effect of R&D on economic activity, advertising expenditures have not been systematically linked to value creation. For example, Ashley, Granger, and Schmalensee (1980) conclude that advertising does not lead to increased economic activity, but rather follows it. This lack of association is consistent with the premise that a substantial amount of advertising is not directed at creating value, but rather toward other goals, in particular, value appropriation.

An Indicator of Strategic Emphasis

Within organizations, different projects and applications compete for the same scarce resources. In this internal competition for resources, the most essential and strategically appropriate applications win. Resources end up concentrated in the areas of the greatest perceived importance. Consequently, the strategy of a company is revealed in the allocation choices and the trade-offs it makes between the different possible applications of its resources. Indeed, past research (e.g., Harrison et al. 1991, 1993; Ittner, Larcker, and Rajan 1997; Ramaswamy 1997) has used resource allocation patterns to depict the underlying strategies of the organization.

Because advertising tends to have a greater association with value appropriation efforts and R&D has greater association with value creation, we expect the following indicator of strategic emphasis, which we label

Positive scores represent companies that have relatively stronger commitment to value appropriation–based marketing strategies and negative scores represent companies that have relatively stronger commitment to value creation–based strategies. Intertemporal increases in the

We observe that the

However, even within a given industry, firms will choose different ways of competing, and this will manifest itself in a different level of strategic emphasis. For example, considerable variation in the

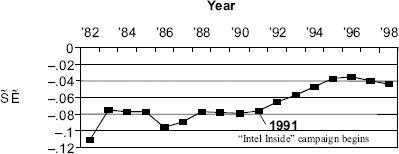

Strategic emphasis will also change for a given firm over time to reflect a change in strategy. Consider Figure 2, which plots the

Strategic Emphasis Indicator for the Intel Corporation 1982–98

The Financial Implications of the Trade-off between Value Creation and Value Appropriation

Our research goal is to assess the financial effect generated by shifts in emphasis between value creation and value appropriation and to address the conditions under which these shifts might have differential performance implications. To capture the long-term financial impact (i.e., the total expected value), our analysis focuses on the effect of strategic emphasis on the stock market valuation of the firm.

Stock Return as a Measure of the Long-Term Financial Performance

The economic return to a marketing strategy is not attained typically in a single reporting period, but rather is realized over a long-term time horizon. Yet most of the research in marketing assessing strategic decision has involved measures such as sales, accounting return on investment, or market share, whose current value provides, at best, an incomplete picture of the value of a strategy. An alternative is to make use of stock market data, which provide the financial markets’ estimate of the total expected value of the strategy.

A firm's marketing strategy can be viewed as an intangible asset that influences future returns (Srivastava, Shervani, and Fahey 1998). The value of the strategy can be represented as the excess future returns generated by the firm when this particular strategy is employed. As such, the value of a marketing strategy to the firm can be depicted as a discounted present value of the future cash flows generated through the use of this marketing strategy:

In practice, it is virtually impossible to estimate the value of a marketing strategy with this formula. Although the measure of Vi is not available, under the efficient markets hypothesis, abnormal stock return (the difference between the actual and expected return, given the market and firm risk characteristics) will provide an unbiased estimate of the change in Vi. Given efficient markets, all available information about future cash flows is incorporated into the current stock price. When an unanticipated change in strategy occurs, the markets react, and the new stock price reflects the long-term implications such change is expected to have on future cash flows. As such, abnormal stock return provides an estimate of the difference in market value of the firm before and after the change in marketing strategy occurs. Therefore, it can be used as an estimate of the long-term financial value that results from a shift in marketing strategy. 2

Although market anomalies exist, they tend to be rare and short-lived. As such, particularly for analysis based on a large number of firms across a long time period, the efficient markets hypothesis appears to be a good approximation for the functioning of the financial markets. Even those who question the overreliance on the efficient markets hypothesis (e.g., De Bondt and Thaler 1985) agree that it is a good starting point.

Testing for the “Information Content” of Strategic Emphasis

We seek to assess the extent to which changes in strategic emphasis are associated with long-term financial performance. We do so by examining the information content of strategic emphasis (i.e., whether changes in the

Early work in the area of assessing information content, for example, in accounting, focuses on the role of changes in accounting variables such as size-adjusted earnings. More recent work (e.g., Aaker and Jacobson 1994, 2001; Barth et al. 1998) has begun to investigate the role of nonfinancial variables, such as brand attributes. These studies seek to test for incremental information content, that is, the degree to which a series provides added explanatory power to current earnings information in explaining stock price movements.

Assessing the incremental information content of strategic emphasis can take place by regressing stock returns on changes in accounting business performance and changes in strategic emphasis. That is, estimating the following model:

3

Differences in firm return stem not only from differential changes in expected cash flows but also from differences in risk. That is, riskier firms earn higher returns. Historically, differences in risk have been controlled by modeling the systematic risk of the firm, as reflected by its beta. More recent work (Fama and French 1992, 1996) has expanded on this single-factor capital asset pricing model by allowing risk to depend not only on beta but also on size and “book-to-market” factors. Fama and French (1992) find that after the role of size (as modeled by log[market value]) at the start of the period and book-to-market equity (as modeled by the log[book value/market value]) at the start of the period are accounted for, estimates of beta are unrelated to firm stock return. To control for these risk factors, our model also includes log(book valuet – 1/market valuet – 1) and log(market valuet – 1). Because the effect of these factors may vary depending on economic conditions, we allow their effect to differ over time (i.e., we allow for differential effects by year). By including these factors in the model, we control for the different types of risk, and as such, our analysis is based on abnormal (i.e., risk adjusted) return. The model also includes (1) annual dummy variables so as to capture the effects of economywide factors and (2) industry dummy variables to capture industry-specific effects.

Equation 2 reflects that accounting measures supply information about current and future-term financial performance. This effect is captured by α1 (commonly known as the “earnings response coefficient”), which depicts the stock market response to unanticipated changes in accounting information. However, accounting indicators are limited in their ability to capture completely the expected net cash flow from the future opportunities facing the firm. Do investors view shifts in a firm's strategic emphasis as providing additional information about these opportunities and their impact on the firm's future cash flows?

The null hypothesis is that α2 = 0, which would imply that the indicator of strategic emphasis has no incremental information content. That is, the financial markets perceive the measure to provide no information about future earnings beyond that reflected in current-term earnings. The alternate hypothesis is that α2 ≠ 0, which implies that stock market participants perceive the change in the strategic emphasis indicator to contain information (incremental to that reflected in current-term accounting business performance) about future cash flows.

In this study, we are particularly concerned with investigating the opposing elements of the alternative hypotheses of α2 > 0 and α2 < 0, that is, whether a shift in strategic emphasis toward value appropriation versus value creation has a positive or a negative effect on expectations of future cash flows. Although increasing either value creation or value appropriation capabilities should enhance firm performance, the effects of shifts in emphasis between the two have not been examined previously. 4

Other studies (e.g., Erickson and Jacobson 1992) have examined the separate effects of advertising and R&D on stock return. Comparing response coefficients from this type of model would result in our testing different effects than what we are trying to assess in our analysis. In particular, this approach would not only capture shifts in emphasis (as does our

Differential Response to Shifts in Strategic Emphasis

The effect of strategic emphasis on market value may not be constant across firms. Rather, investors may have a differential response to shifts in strategic emphasis under different conditions. In particular, the response may vary systematically with (1) situational factors regarding the firm and (2) the type of environment in which the firm is operating.

The Situation of the Firm

Market response can vary depending on the situation of the firm. One key difference among firms is profitability. Competing hypotheses about the moderating effect of profitability exist. One view emphasizes exploiting opportunities when they arise. Under this view, firms with positive unexpected earnings should focus on locking in their advantage through a shift to greater emphasis on value appropriation. By the same logic, firms in a weaker than expected financial position would be better served by emphasizing value creation capabilities (i.e., they are not creating sufficient value to justify increased investments in value appropriation). However, an alternative view emphasizes the dissipation of profits. Under this view, firms cannot rest on their past success. Firms should not focus on sustaining existing advantages, which is often futile, but rather on creating new advantages at a faster rate than the old advantages are being eroded by competition (Grant 1991). As such, a firm in a superior financial position needs to prepare for the eventual dilution of its existing advantages by focusing more on value creation projects.

The firm's existing strategic emphasis may also moderate the stock market response to shifts in strategic emphasis. The concept of path dependency advanced in evolutionary economics postulates that the strategic choices a firm made in the past shape its current strategic position and, as such, the viability of future choices. That is, the stock market response to an unanticipated strategy change (ΔSEit) may be moderated by the past strategic choice (SEit – 1). However, the theory is not clear regarding the direction of the effect. Diminishing marginal returns hypothesis suggests that firms with high levels of value creation capability would receive less gain from expanding their value creation capabilities and firms with high levels of value appropriation capability would receive less gain from expanding their value appropriation capabilities. Conversely, Lei, Hitt, and Bettis (1996) argue that as a firm's skills become more specialized, they may produce expertise that is difficult for the competitors to imitate and, therefore, may become a source of competitive advantage. Thus, firms with high levels of value creation emphasis should further enhance their value creation capabilities, and firms with high levels of value appropriation emphasis should continue to enhance their value appropriation capabilities.

Allowing for this type of differential response can be achieved by modifying Equation 2 to allow for systematic variation in α2 depending on unanticipated ROA and the past level of strategic emphasis. That is, estimating a model of the form

The coefficient α21 depicts the extent to which unanticipated ROA moderates the effect of strategic emphasis on stock return. A value of α21 > 0 would indicate that firms in a weak (strong) financial position are better suited by emphasizing value creation (value appropriation). A value of α21 < 0 would indicate that firms in a weak (strong) financial position are better served by emphasizing value appropriation (value creation). The coefficient α22 depicts the moderating effect of past strategic emphasis on the stock market response to an unanticipated shift in strategic emphasis. Values of α22 < 0 would support the diminishing marginal returns hypothesis; values of α22 > 0 would support the specialization hypothesis.

The Role of the Technological Environment

Differences in market response can be posited to stem not only from firm-specific factors but also from industrywide characteristics. Chandler (1994) highlights the role of technology as a key characteristic differentiating industries. He defines high-technology industries as those in which new product development is the critical element of interfirm competition. These industries tend to be characterized by high R&D intensity, changing products, and long-term horizons for achieving a payback. He contrasts this with stableand low-technology industries in which the final product has historically remained much the same. Competition is more functional and strategic than in high-technology industries. That is, firm performance, for example, is based more on the improvement of the existing product and processes and on enhanced marketing efforts. Research and development is still important, but it is likely to be less intensive and focuses more on product improvement and cost reductions than on new product development.

One hypothesis is that value creation capability is more important in environments in which technology is changing (i.e., in high-technology industries). A firm cannot stem the tide of innovation and constantly must adopt new technologies and create new products to be successful. Conversely, value appropriation capability is more important in stable-and low-technology industries. Here, there is less opportunity for value creation, and firms must work to sustain their advantages. This suggests that increasing emphasis on value creation capability is more important in high-technology markets than in stable- and low-technology markets. This suggests differences in magnitude (or even in sign) for the estimates of α20 among the technology environments.

An alternative view stemming from the literature on imitation suggests that, even for the high-technology firms, the ability to capitalize on innovations is at least as important as the ability to create new value. Levin and colleagues (1987) find that it is relatively easy and at least 35% cheaper for competitors to replicate an innovation than to develop it. The majority of typical unpatented innovations can be imitated within a year, and major patented innovations within three years. However, it is not easy and cheaper to imitate superior reputation or brand image. Because patents do not provide adequate protection in many high-technology industries, firms are forced to seek other ways to restrict competitors from dissipating their profits. Thus, even in high-technology industries, firms should engage in development of value appropriation capabilities. Testing for differential effects of technological environment can be achieved by estimating separate regressions for the different technological environments and then testing whether the coefficients differ among them.

Data Source

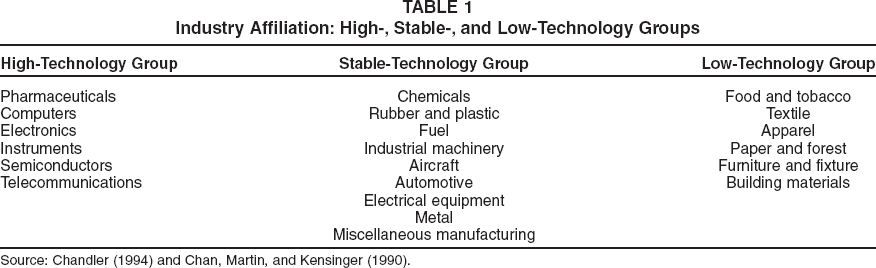

The data set used in our analysis comes from the Standard & Poor's 1999 COMPUSTAT database. This database provides annual accounting and stock market information for publicly traded firms on the New York, American, and Nasdaq stock exchanges. The sample of companies used in the analysis is restricted to manufacturing companies reporting their market value, R&D expenditures, advertising expenditures, assets, and net income. Table 1 provides a list of the industries included in our study and classifies them into the high-, stable-, and low-technology subsamples. To ensure correspondence between the stock price and accounting information, an additional requirement that companies have a December fiscal year is used. Our data sample consists of observations from 566 different firms reporting for all or some of the period 1980–98. We have a total of 3480 observations available for analysis. In Table 2, we provide descriptive statistics for and the definitions of the variables that form the basis of our analysis.

Industry Affiliation: High-, Stable-, and Low-Technology Groups

Source: Chandler (1994) and Chan, Martin, and Kensinger (1990).

Estimation Results

We first estimate first-order autoregressive time series models for ROA and strategic emphasis. In Table 3, we present the estimated models. Following the convention (e.g., Kormendi and Lipe 1987), we use the residuals from these models as the measures of the unanticipated changes in ROA and strategic emphasis of a firm. 5 In Table 4, we present the results of estimating Equation 4 for our entire sample and for the high-, stable-, and low-technology subsamples. 6

Descriptive Statistics

Notes: S.D. = standard deviation.

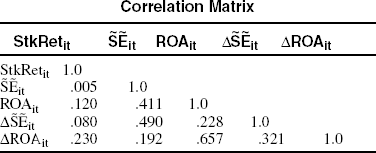

The use of a residual, as opposed to the series itself, in a stock return model follows directly from the efficient markets hypothesis. Stock return should exhibit a higher correlation with the residual series because the raw series includes an anticipated component that will be unrelated to stock return. As evidenced by the following correlation matrix, our results are consistent with this efficient markets implication:

Correlation Matrix

Although not reported in Table 4, consistent with previous research, we find significant coefficients for the yearly log(book valuet – 1/market valuet – 1) and log(market valuet – 1) measures. Controversy exists regarding how to interpret the coefficients. One view is that the estimated effects reflect the mispricing of stocks. An alternate view (e.g., that raised by Fama and French [1992]) is that the factors adjust for risk considerations. The overall negative effect of size reflects reduced risk associated with larger firms. The positive effect of book-to-market reflects risk associated with relative distress. The key for our analysis is not so much interpreting the rationale for the significance of the factors, which is an ongoing debate in finance, but rather controlling for these factors so that we are able to conclude that shifts in strategic emphasis are not associated with stock return merely through risk.

First-Order Time-Series Models for ROA and

t-statistics are in parentheses.

p < .001.

Notes: Each equation also includes (1) annual dummy variables to capture the effects of economywide factors and (2) industry dummy variables to capture industry-specific effects.

The Full Sample Results

In Table 4, the results for the full sample estimation indicate that unanticipated ROA has a positive (1.58) and significant effect on stock return. The coefficient estimate greater than 1.0 does not indicate that investors are short-term oriented in that they overvalue current-term results. Rather, consistent with the time series models showing that ROA exhibits persistence, a shock to ROA will not dissipate immediately but is likely to persist over several years. The greater the persistence of a ROA shock, the larger is the earnings response coefficient in the stock return equation (Miller and Rock 1985). As such, the market reaction to unanticipated ROA reflects that it provides information not only about the current-term results but also about the future-term profits.

Table 4 also shows that changes in strategic emphasis are significantly related to stock return. The positive coefficient (1.18) means that, on average, investors view increases in emphasis on value appropriation coming at the expense of value creation as being positively related to future-term performance. 7 Because the model accounts for the direct influence of unanticipated ROA, this effect is incremental to information contained in accounting returns. Investors perceive strategic emphasis as providing incremental information about the future-term prospects of the firm above and beyond that contained in current accounting returns.

An additional effect of Δ

However, the total effect of strategic emphasis is not constant, but rather is evidenced to vary systematically. Although the interactive effect with lagged strategic emphasis (i.e., -.61) is statistically insignificant, the interactive effect with unanticipated ROA is positive and highly significant. The positive interactive effect (3.73) indicates that investors view a shift toward value appropriation capability as amplifying firm value when a firm is experiencing a positive shock to ROA. 8 Conversely, when firms experience a negative shock to profits, investors view a shift toward value appropriation capabilities less positively. Indeed, depending on the magnitude of the earnings shock, conditions exist in which investors view a shift toward value creation capability as more preferable. This condition exists when unanticipated ROA is less than -.32 (i.e., 1.18/3.73).

Another interpretation of this interactive effect, which is observationally equivalent, is that Δ

Stock Market Reaction to Changes in Strategic Emphasis Dependent Variable: Stock Return *

t-statistics are in parentheses.

p < .01.

p < .001.

Notes: Each equation also includes (1) annual dummy variables to capture the effects of economywide factors, (2) industry dummy variables to capture industry-specific effects, and (3) annual effects for log(market valuet – 1) and log(book value/market value)t – 1 to capture firm-specific risk factors.

The Role of the Technological Environment

Analysis of the high-, stable-, and low-technology subsamples reveals both similarities and differences across the three environments. All three samples exhibit positive effects of unanticipated ROA on stock return. One difference to note among the samples relates to the magnitude of the earnings response coefficient estimates. The estimated effect is lowest for the high-technology sample (1.36), increases for the stable-technology sample (1.80), and is highest for the low-technology sample (3.09). Theoretical valuation models (e.g., Miller and Rock 1985) depict the magnitude of the earnings response coefficient to increase the greater the persistence of profits and decrease the larger the discount rate. The observed differential effect is consistent with differences across the three environments. Shocks to ROA are more likely to persist and future-period returns are discounted less, the less dynamic the environment is.

The estimated direct effects of strategic emphasis are positive and significant for both high- and stable-technology markets. Although the estimated coefficients decrease in magnitude, moving from high- (2.01) to stable- (1.5) to low-(.91) technology markets, a Chow test is unable to reject the hypothesis that the direct effect of strategic emphasis is the same across technological environments. Thus, we find no evidence to suggest that value appropriation is any less important in high-technology markets than in stable-technology markets.

Moderating effects of profitability

The moderating effect of unanticipated ROA on strategic emphasis is positive for both the high-technology and stable-technology environments. This positive effect indicates that investors value a shift toward emphasizing value appropriation capability when earnings are greater than anticipated. In other words, when a firm is doing well, the market wants the firm to increase emphasis on value appropriation. The moderating effect is larger in stable-technology markets than in the high-technology sector (5.37 versus 2.79). This is consistent with the relative role that Chandler (1994) notes innovation plays in these two markets. In stable-technology markets, where innovation is less central, firms need to place greater emphasis on appropriation when the firm has an advantage. Locking in an advantage is still important in high-technology markets, but less important than in the stable-technology markets. The estimated effect is negative for the low-technology firms. However, the size of the standard error makes it difficult to isolate the effect or draw conclusions.

Moderating effects of the past strategy

The most dramatic difference among industry groupings is for the interactive effect of unanticipated strategic emphasis with the lagged level of strategic emphasis. The estimated effect is positive and significant for high-technology firms (6.00), negative and significant for stable-technology firms (-3.44), and negative (though insignificant) for low-technology firms (-5.80).

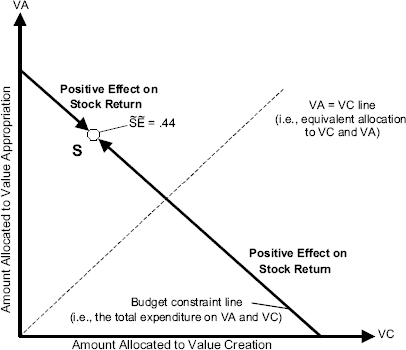

The negative effect is consistent with the proposition of diminishing marginal returns to a high value creation or value appropriation capability emphasis. This finding suggests that in the stable-technology sample, the higher the past level of strategic emphasis, the less positive the market reacts to increases in this emphasis. Indeed, for high levels of strategic emphasis, the effect turns negative. Figure 3 graphically depicts the estimated relation between stock return and strategic emphasis, depending on the previous level of strategic emphasis.

9

For the majority of the stable-technology firms, the market reacts positively to emphasizing value appropriation capability. However, there exists a threshold value S, such that for

The result follows directly from taking a first-order derivative of the estimated Equation 4. That is, we use the coefficient values from Table 4 as the estimated parameters in Equation 4 and take a partial derivative of the model with respect to Δ

Effects of the Directional Change in the Strategic Emphasis on Stock Return Given the Past Level of Strategic Emphasis: The Stable-Technology Sample

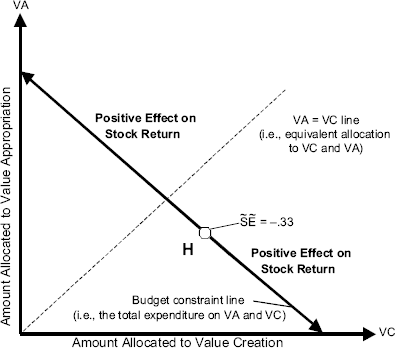

Conversely, for high-technology firms, the positive coefficient for the interactive effect of unanticipated strategic emphasis with the lagged strategic emphasis is reflective of positive reenforcing or specialization effects. Figure 4 graphically represents our findings for the high-technology sample. Here, a single optimum solution does not exist. Firms with high orientation on value creation are rewarded for further emphasis on value creation capabilities. All other firms are rewarded for further investments into their value appropriation capability. A separating point H is estimated at advertising intensity – R&D intensity = -.33 (i.e., −2.01/6.00). Movement toward H is viewed negatively by the market. Movement away from H to the extremes of value creation or value appropriation emphasis (represented by arrows in Figure 4) is rewarded by the stock market. This result suggests two possible sources of competitive advantage for the high-technology manufacturing firms: either a high value creation emphasis or a high value appropriation emphasis in their marketing strategy.

Effects of the Directional Change in the Strategic Emphasis on Stock Return Given the Past Level of Strategic Emphasis: The High-Technology Sample

Sensitivity Analysis

We undertook several tests to assess the sensitivity of our analysis. We found that alternative specifications and expanded models did not perform as well or added little to the analysis. We tested whether some alternative means of scaling the advertising–R&D differential for firm size, for example, dividing by the sum of advertising and R&D expenditures, sales, or lagged market capitalization, instead of assets, would enhance the information content of the

See, for example, Fisher (1984) for a discussion of issues relating to alternative size deflators.

We also assessed the presence of feedback effects from stock return to strategic emphasis. That is, our results could stem not from

Because the market response to shifts in strategic emphasis may also depend on factors other than those we modeled, we tested some additional possible moderating factors. For example, the anticipated component of ROAit (i.e., the predicted value from the univariate return on investment model), rather than just unanticipated ROA (i.e., ΔROAit), might moderate the effect of shifts in strategic emphasis on stock return. However, the tests revealed that only the unanticipated component of ROAit had a statistically significant moderating effect. In addition, we hypothesized that the market response might differ depending on the change in the intensity of combined R&D and advertising expenditures (i.e., the extent to which the firm is expanding or contracting its combined value creation and value appropriation activities). However, we found this moderating effect to be small and statistically insignificant, -.12 with a t-statistic of -.1. Similarly, we found no significant difference in response when we estimated separate effects for shifts in strategic emphasis for those firms increasing R&D and advertising expenditures versus those decreasing expenditures. The estimated effect of .127 for those increasing spending was not significantly different from the estimate of .097 for those decreasing spending (i.e., the t-statistic for the difference in effects was .5). We also tested whether the response to shifts in strategic emphasis varied by the size of the firm and the total amount spent on R&D and advertising. Here, we also found no significant differential.

Directions for Further Research

Although these sensitivity tests did not uncover results that challenged our findings, this is not to suggest that further work is not needed. Indeed, many directions for additional research are warranted. One would be to improve the measure of strategic emphasis. For example, we used resource allocation patterns to discern firm strategic emphasis. An alternative would be to survey experts or use statements in the annual reports to operationalize strategy. In addition, because our study examined firms across different industries, the

Another avenue might focus not on trying to measure the extent of shifts in emphasis, but rather on isolating events when a shift occurred and determining whether the event reflected increased emphasis on value appropriation or on value creation. An event study (i.e., assessing how the stock market reacted to these shifts) could then be undertaken.

Future work in the area could also explore the potential role of other moderating factors (e.g., economic conditions, cross-cultural differences, stage of the company life cycle, the effectiveness of patent protection). Indeed, a host of factors other than those included in our model can generate a nonlinear or even nonmonotonic stock market response to shifts in strategic emphasis. One approach would be to undertake threshold analysis to isolate different regimes in which the effect of strategic emphasis on financial performance differs.

Further research aimed at better understanding strategic emphasis is also in order. A potential research avenue would be to investigate the factors that influence strategic emphasis and that motivate a firm to shift its emphasis.

Implications

Our study shows that the relative emphasis that firms place on value appropriation relative to value creation contains information relevant to investors in the valuation of the firm. In general, we find that increases in emphasis toward value appropriation capability and away from value creation capability are associated with increases in stock return. This result serves to reinforce the view of Teece (1987) and others who note that many firms, particularly in the high-technology sector, labor under the illusion that developing new, superior products ensures success not only for the product but also for the firm. These firms do not pay sufficient attention to restricting competition from imitating innovation and dissipating a firm's returns from it. Our results show that even in the high-technology markets, where innovation and R&D are central to firm success, investors view favorably a shift toward value appropriation capability.

The positive response to enhancing value appropriation is particularly strong when a firm has better than expected earnings. In other words, when a firm is doing well, the market wants it to increase emphasis on value appropriation. When a positive shock to earnings occurs, this provides a signal to existing and potential competitors as to the direction resources should flow. The inflow of resources into areas with positive shocks will tend to bring returns back toward the competitive rate of return. If management wants to insulate itself from this process, it needs to place greater emphasis on value appropriation and restricting imitation.

However, conditions exist in which the financial markets view increases in value appropriation capability negatively. For example, for firms experiencing a negative shock to ROA, increased focus on value appropriation capability would in some cases lead to a drop in market value. If a firm is not doing well financially, the financial markets respond positively to efforts designed to generate value creation capabilities. The same is true for firms operating in stable-technology markets that are already highly emphasizing their value appropriation capability. For these firms, further increases in the value appropriation capability can decrease market value. If a firm already has placed considerable focus on value appropriation, the markets realize that there may be limits to the firm's ability to extract surplus. In this case, efforts to expand surplus through enhanced emphasis on value creation are rewarded.

Nonetheless, our results serve to highlight the importance stock market participants place on value appropriation. Why is this so, and why have firms not already acted on this information? Should firms shift their emphasis toward value appropriation? Two phenomena that are not mutually exclusive, namely, signaling and managerial inefficiency, provide some answers to these questions. First, changes in strategic emphasis may provide a signal to the marketplace. Firms shifting to strategy with greater emphasis on value appropriation may be signaling that they now possess sufficient value creation capability and are seeking to lock in their value creation advantage. Indeed, this can describe the Intel experience in which Intel possessed great value creation capabilities and sought to exploit this advantage by creating brand loyalty with the “Intel Inside” campaign. This reasoning indicates that not all firms should shift to value appropriation. Rather, it suggests that our results are driven by those firms having the necessary value creation capabilities that decided to shift their strategic emphasis.

Second, our results may be indicating that firms are inefficient in allocating resources in that they may be consistently underinvesting in value appropriation (e.g., marketing) relative to value creation (e.g., R&D) activities. This can be explained by the difficulty managers have in justifying marketing expenditures. Many commentators have noted that because of a lack of reliable measures in documenting the effect of marketing, fewer resources than should be are devoted to marketing. The Marketing Science Institute, for example, has noted this problem and has recently called for proposals to help address this issue.

Value creation investment decisions cannot be divorced from issues of appropriability. Countless examples exist of innovations that created enormous value, but where the innovating firm was unable to capture the surplus. For example, although exceptions exist, Xerox's Palo Alto Research Center is best known as a breeding ground for innovations from which Xerox was unable to achieve strategic or commercial success (e.g., the personal computer, Ethernet, graphical user interface, page-description language). Firms that fail to pay sufficient attention to value appropriation cannot be expected to achieve sustained competitive advantage and reap the rewards from their value creation capabilities.