Abstract

Do acquisitions increase, decrease, or have no effect on innovation? The empirical research on this question suggests that acquisitions may hurt innovation; that is, they may be a “poison pill” for innovation. The authors present an alternative view. For firms that first engage in internal knowledge development, the knowledge-based view the authors present suggests that acquisitions can help innovation; that is, they can be a tonic for innovation. Analysis of cross-sectional, time-series data on a sample of pharmaceutical firms during 1988–97 provides evidence to support the thesis.

Given the importance of the topic, many studies have explored the link between acquisitions and innovation. The empirical evidence so far is not encouraging. Research suggests that acquisitions tend to hurt, not help, innovation (Ernst and Vitt 2000; Hitt et al. 1991a; Miller 1990; for a recent exception, see Ahuja and Katila 2001). The bulk of the research implies that firms in search of innovation may do well to steer clear of acquisitions. Some researchers argue that the many activities involved in trying to consummate and integrate acquisitions can distract managers from the task of innovation (Hitt, Hoskisson, and Ireland 1990). Others note that key employees, including scientists and champions of innovation, may leave the firm after acquisition (Ernst and Vitt 2000). Researchers also point out that firms may take on considerable debt to finance acquisitions; the interest expenses and repayments associated with this debt may choke off much-needed funds for innovation (Hitt et al. 1991b). For these reasons, acquisitions have been referred to as a “poison pill” for innovation (Hitt et al. 1991b, p. 22). At best, acquisitions are simply considered to be a placebo, having no effect on innovation (see Jensen 1988).

However, the research on acquisition and innovation has focused on firms in the aggregate, without further exploring differences among firms. Most studies have sought to answer the general question, Are acquisitions good or bad for innovation? However, firms vary widely in their ability to convert external knowledge into innovation outcomes. For example, some observers attribute Johnson & Johnson's strong innovation record to its ability to spot good targets and manage them better than other firms do (Barrett 2002). Therefore, a different and potentially more useful question is, Why are some firms better at generating innovations from acquisitions than others? This is the question we address in this research.

In this article, we aim to make three main contributions to the literature. First, we present a knowledge-based view of the firm that highlights reasons some firms are better than others at innovation through acquisition. We argue that firms that are rich in internal knowledge to begin with are likely to achieve significantly greater innovation from their acquisitions than are other firms. By doing so, we show that prior research, in failing to employ such a knowledge-based view, has arrived at premature and overly pessimistic conclusions about the impact of acquisitions on innovation. Instead of acquisitions being a poison pill or placebo, as prior research has concluded, we show how acquisitions might work as a tonic for innovation.

Second, we complement the growing literature in marketing on the development of internally built knowledge by highlighting a hitherto overlooked benefit of such knowledge. We show that a sustained process of internal knowledge building in particular technological areas can pay off by enabling firms to better identify and assimilate knowledge bought from other firms. In doing so, we show the synergies to be gained by a program that combines internal with external knowledge. Indeed, our results show that examination of internal and external knowledge in isolation leads to an underestimation of the influence of either form of knowledge on innovation.

Third, we aim to make an important methodological contribution. We believe that limitations in the data and methods used in the existing empirical research cause the research results to be less than conclusive. For example, studies thus far tend to ignore a key metric of innovation: new products. This is the innovation output that is of most relevance to marketing scholars. Existing studies examine innovation input (e.g., research and development [R&D] expenditures) or intermediate output (e.g., patents). Ours is the first study (to our knowledge) to address the impact of acquisitions on product innovation.

Conceptual Framework and Hypotheses

The concept of knowledge is central to our thesis. We argue that a firm's internal knowledge is a key predictor of its ability to use external knowledge to create innovations. We use arguments from organizational theory on absorptive capacity (Cohen and Levinthal 1990; Kogut and Zander 1992) and the knowledge-based view of the firm (Bierly and Chakrabarti 1996; Grant 1996; Nonaka 1994; Spender 1996; Winter 1987) as well as recent work in marketing (especially John, Weiss, and Dutta 1999) to develop our arguments on the role of knowledge in postacquisition innovation. These arguments highlight why innovation from acquisitions is challenging yet ultimately feasible.

In this article, we focus on a particular type of knowledge: technical knowledge. We define technical knowledge as scientific knowledge applied to useful purposes. In prior research, this construct has sometimes been called technical know-how (John, Weiss, and Dutta 1999).

Technical knowledge is not easily transferred across different fields (Henderson and Cockburn 1994; John, Weiss, and Dutta 1999; Pisano 1994). Technical knowledge across different fields is, however, potentially combinable (Kogut and Zander 1992; Reed and DeFillipi 1990). The field-specific nature of technical knowledge underscores the need to study, in the acquisitions context, the depth (within fields), the breadth (across fields), and the similarity of the acquirer's knowledge with the fields in which the target has knowledge. For the sake of simplicity in exposition, we henceforth use the term knowledge to refer to technical knowledge.

Dimensions of Knowledge: Depth, Breadth, and Similarity

We define knowledge depth, breadth, and similarity as follows. Depth refers to the amount of within-field knowledge possessed by the acquiring firm. Breadth is the range of fields over which the firm has knowledge. Similarity is the extent of overlap in the fields of knowledge of the acquirer and target firms. Prior discussions of knowledge have implicitly focused on depth of knowledge (e.g., John, Weiss, and Dutta 1999), though even this variable has not been examined in the acquisitions context. However, the difficulty of transferring knowledge across fields implies that breadth and similarity of knowledge are also critical in the acquisitions context.

Sources of Knowledge: Internal versus External Knowledge

Knowledge differs not only in the dimensions discussed previously but also in its sources. Internal knowledge is based on learning by members of the firm; it results from the creation and distribution of knowledge within the boundaries of the firm (Chesbrough and Teece 1996). External knowledge, in contrast, originates from outside the firm. We use the terms internal and external knowledge in the spirit of Friedman, Berg, and Duncan (1979, p. 103); Bierly and Chakrabarti (1996, p. 127); Van den Bosch, Volberda, and de Boer (1999, p. 566); and Madhok and Osegowitsch (2000, p. 329) and differently from internalization as used by Nonaka (1994).

Acquisitions provide an important means to bring external knowledge into the firm (Bierly and Chakrabarti 1996). The emphasis in prior research on these two sources of knowledge has typically been on examining the trade-off between the two in a static sense. Thus, internal knowledge has been shown to enable firms to develop core competencies, especially in domains that are complex and deeply integrated with other domains of knowledge (Chesbrough and Teece 1996). In contrast, external knowledge is more likely to enable firms to keep abreast of new technical developments, thus increasing the flexibility of the firm in dynamic environments (Grant 1996).

By maintaining and replenishing their stock of knowledge on a continuous basis, firms that combine internal and external knowledge can reduce the chances of being locked out of areas of future technological and commercial importance (Cohen and Levinthal 1989; Schilling 1998). Much of the literature on combining internal with external knowledge is conceptual (see Cohen and Levinthal 1989; Zahra and George 2002). Only recently have researchers begun to test some of these ideas empirically (e.g., Cockburn and Henderson 1998; Lane and Lubatkin 1998; Moorman and Slotegraaf 1999). We are aware of no study that has applied these ideas in the area of acquisitions in general or acquisitions and innovation in particular. This is the focus of our research. A recent study (Wuyts, Dutta, and Stremersch 2004) examines the role of alliances in product innovation. However, (1) that study examines alliances, whereas ours examines acquisitions, and (2) that study examines technological diversity, whereas ours examines the depth, breadth, and similarity of technical knowledge. We next present hypotheses on the main effect of internal knowledge and then the interaction effect of internal and external knowledge in the context of acquisitions and innovation.

Depth of Knowledge and Innovation

A firm's ability to create knowledge is a key driver of its ability to innovate (see Griliches 1984). New knowledge does not arise in a vacuum; rather, it is a path-dependent outcome of building on prior knowledge. However, as noted previously, knowledge is field specific in nature. Firms are therefore likely to vary in the depth of knowledge they have in a particular field.

The effects of depth of knowledge on innovation are not straightforward. Some researchers have argued that greater depth in knowledge could, ceteris paribus, lead to the setting in of core rigidities, which in turn could decrease innovation (Leonard-Barton 1992). However, a larger and more recent stream of research indicates that inadequate knowledge in a particular field can result in firms being locked out of developing or assimilating new knowledge in that area (Zahra and George 2002). Specifically, to be able to develop new knowledge in a field, firms must already possess some knowledge in that field. Developing depth in key fields enables firms to produce new knowledge in those fields, gain competency in core product areas, and thus innovate (Bierly and Chakrabarti 1996; Hamel and Prahalad 1994). As a result, there is likely to be a main effect of depth of knowledge on the innovation activity of firms: The deeper a firm's knowledge in certain fields, the greater is its ability to create innovations in these and related fields.

In addition to this main effect, there is likely to be an interaction effect of depth of internal knowledge and external knowledge from acquisitions. Successful innovation from acquisition involves the ability to choose the target with the most promising knowledge, absorb the knowledge made available by the target, and exploit it to create new knowledge. Firms that differ in depth vary in their ability to evaluate, absorb, and build on external knowledge and therefore derive different levels of innovation from such knowledge. Firms with low depth are likely to fall prey to technological lockout (Cohen and Levinthal 1989). Such firms may not be able to assess accurately the innovation potential of targets. Compared with firms with high depth, these firms may acquire targets with less innovation potential. Furthermore, given their lack of experience in creating knowledge, they are likely to manage acquisitions (even those with high innovation potential) poorly. Key technical personnel from the target firm may leave the combined firm because of a perceived lack of prestige or appreciation for their activities.

Firms with high depth, in contrast, are better able to evaluate and manage new knowledge and use it to innovate (Cohen and Levinthal 1990). They are therefore best positioned to leverage acquisitions to create innovations. For all these reasons, we expect that

Firms with high depth of knowledge produce more innovations than do firms with low depth of knowledge.

Firms with high depth of knowledge produce more innovations from acquisitions than do firms with low depth of knowledge.

Breadth of Knowledge and Innovation

Just as they vary in depth, firms also vary in the breadth of knowledge they possess. Again, the effects of breadth on innovation are not obvious. Some researchers have noted that greater breadth in knowledge could, ceteris paribus, cause the firm to spread resources too thinly (e.g., Werner-felt and Montgomery 1988). Breadth can also cause distraction within the firm, thus lowering innovation.

However, the bulk of the knowledge-based literature suggests that breadth in knowledge is helpful for innovation (Bierly and Chakrabarti 1996; Cohen and Levinthal 1990; Henderson 1994; Henderson and Cockburn 1994). Several researchers have pointed out the importance of being able to integrate knowledge from across different fields, especially in technically complex industries (Henderson and Cockburn 1994; Pisano 1994; Volberda 1996). The broader a firm's existing knowledge, the greater is its ability to combine knowledge in related fields in a more complex and creative manner (Bierly and Chakrabarti 1996; Kogut and Zander 1992; Reed and DeFillipi 1990). In addition, the potential for “happy accidents,” whereby concepts from one field are applied to a different field in hitherto unexpected ways, increases with greater breadth of knowledge.

Moreover, firms with a broad base of knowledge are less likely to develop core rigidities and thus be locked out of emerging technical domains (Leonard-Barton 1995). With changes in market preferences and technological opportunities, knowledge that was once a source of competitive advantage may become irrelevant. Low breadth makes the firm especially vulnerable to such irrelevance. Broader knowledge, however, gives the firm greater flexibility and adaptability in responding to environmental change (Volberda 1996). Overall, these arguments suggest that the broader a firm's knowledge, the greater is its ability to create innovations.

As does depth, breadth is likely to have an interaction effect with acquisitions. Given the field-specific nature of knowledge, a firm with low breadth is perforce faced with a greater number of targets that lie outside its own field of knowledge. Therefore, the probability is higher that it will choose acquisition targets outside its own field, from fields that are unfamiliar to it (Chaudhuri and Tabrizi 1999; Hitt, Harrison, and Ireland 2001). When acquiring from outside its own field, a firm with narrow knowledge is likely to be handicapped by its lack of expertise in the other fields (see Cohen and Levinthal 1990; Rosenberg 1982; Zahra and George 2002). It may, for example, choose targets that others with more knowledge in the field may avoid (e.g., Morck, Shleifer, and Vishny 1988). More important, when it acquires such targets, it may be less able to manage and exploit, after the acquisition, the unfamiliar knowledge it has acquired through the target firm (Haspeslagh and Jemison 1991).

In the context of acquisitions, the successful exploitation of an acquired firm involves the ability to absorb the knowledge of the target firm and then use it to develop still newer knowledge (Jemison 1988). The greater the breadth of the acquirer's knowledge, the greater is its ability to absorb the knowledge of the target firm and the greater is its potential for discovery (and therefore innovation) after the acquisition, both by accident and through planning. Therefore,

Firms with high breadth of knowledge produce more innovations than do firms with low breadth of knowledge.

Firms with high breadth of knowledge produce more innovations from acquisitions than do firms with low breadth of knowledge.

Similarity of Knowledge and Innovation

The similarity of knowledge between the acquirer and the target is crucial to the acquirer's ability to absorb the target's knowledge and use it for innovation (Mowery, Oxley, and Silverman 1996). In general, prior research (though not directly focused on the acquisitions context) implies a linear relationship between similarity of knowledge among firms and innovation outcomes from joint activities (Henderson 1994; Henderson and Cockburn 1994). In an empirical study of strategic alliances, Lane and Lubatkin (1998) show that one firm's ability to exploit the knowledge of another depends on the similarity of both firms’ knowledge bases. Cohen and Levinthal (1990) state that for firms to facilitate absorption of new knowledge, the prior knowledge should be closely related to it.

In contrast to the linear effects implied by prior research, we argue that a nonlinear relationship between similarity of knowledge and innovation is more likely (see also Ahuja and Katila 2001). Greater similarity between the acquirer and the target will make it easier for the acquirer to absorb the knowledge of the target firm. Similarity may also lead to easier postacquisition integration, less turnover of key inventors, and therefore greater innovation. However, in the case of highly similar acquisitions, there will also be less new knowledge to absorb. Too much relatedness will result in overlapping and redundant research (e.g., Rindfleisch and Moorman 2001). There will also be fewer knowledge synergies and therefore fewer opportunities for combining different types of knowledge in creative ways.

In contrast, if the two firms’ knowledge is very dissimilar, the external knowledge will be difficult for the acquirer to absorb in the first place. In the context of acquisitions, because absorbing the knowledge of the target is a prerequisite for using it to create new knowledge, very dissimilar knowledge will make it difficult to generate innovations after the acquisition. Therefore, we hypothesize an inverted U-shaped relationship between the similarity and innovation:

Firms with moderate similarity of knowledge produce more innovations from acquisitions than do firms with very high or very low similarity of knowledge.

Method

Through our methodological approach, we attempt to avoid several pitfalls that are evident in research on acquisition and innovation. Data limitations have constrained the focus of much prior research to acquisitions in which the targets are large, publicly held companies. The Federal Trade Commission's Large Merger Series is a commonly used source of data on acquisitions, but this database includes only data on acquisitions of the largest target firms. It is possible that the distraction and debt arguments noted in the literature are particularly severe for acquisitions involving large targets. A vast majority of acquisitions involve small and privately held targets (see U.S. Small Business Administration 1998). The debt and distraction problems may be less acute for such targets. In this research, we study not only large acquisitions but also those involving small and medium-sized targets. We control for heterogeneity due to firm-specific effects by employing a unique panel data set that we specifically construct for this study.

In addition, research thus far has generally focused on the immediate effects of acquisitions on innovation (see Hitt et al. 1991a). However, there could be many lags involved in assimilating acquisitions and generating innovations from them. The true effects of acquisitions may become evident only over a longer term, perhaps over multiple years. To assess more completely the impact of acquisitions on innovation, we apply distributed-lag models to measure not only the current effects of acquisitions but also their future effects. This section describes the empirical context, data, and analysis used in this research.

Empirical Context

Knowledge manifests itself in different ways in different industries. The metrics used to measure knowledge therefore need to vary from industry to industry. The measurement of knowledge across multiple industries is likely to be prone to substantial errors because any uniform metric for knowledge may understate the true knowledge in some contexts while overstating it in others. For this reason, we focus on a single industry to test our hypotheses.

The empirical context for this study is the pharmaceutical industry. This context is especially suitable for our purpose. First, innovation is a particularly critical activity in the pharmaceutical industry (Graves and Langowitz 1993; Jensen 1987; Koberstein 2000; Scherer 1993). Innovative firms in this industry benefit from large and persistent competitive advantage (Comanor 1986; Cool and Dierickx 1993; Henderson and Cockburn 1994).

Second, this industry is characterized by a heavy reliance on knowledge that is codified in the form of patents (Cohen, Nelson, and Walsh 2000; Levin et al. 1987; Mansfield 1986). Both product and process innovations are patented at high rates in this industry, and pharmaceutical firms view patenting as an effective means to prevent competitors from copying innovations (Cohen, Nelson, and Walsh 2000; Klevorick et al. 1995). This reliance on patents allows for a relatively clean yet comprehensive metric for knowledge.

Third, the pharmaceutical industry is an important and widely studied context. A considerable volume of academic research has focused on this industry (e.g., Bierly and Chakrabarti 1996; Cockburn, Henderson, and Stern 1999; Lichtenberg 1998; Yeoh and Roth 1999; for reviews, see Comanor 1986; Scherer 1993). Although acquisitions are a salient issue in the industry, their impact on innovation has not received much academic attention.

Sampling Procedure

To identify our sample group, we randomly selected 47 companies from a population of 185 pharmaceutical companies in the Financial Times Sequencer, an international database of share price data, financial news articles, key financial ratios, and balance sheet and profit and loss data. To assess list validity, we compared a random sample of 40 companies from the Sequencer list with a similar list from the Datastream International database. This comparison indicated a high degree of overlap between the samples in the two lists.

Of the 47 companies in our Sequencer list, we filtered 12 out so that the final sample included only firms that were U.S. based, existed as independent entities during the period from 1988 through 1997, and had pharmaceuticals as the primary line of business. We collected information on the group of 35 acquirers over a ten-year sample period from 1988 through 1997. The firms in the acquirer data set collectively acquired 157 targets during the sample period. Recall that much of the existing research on acquisition and innovation uses the Federal Trade Commission's Large Merger Series database. Our data are more representative of the population of pharmaceutical firms than the Large Merger Series data for two reasons. First, our data consist of all acquisitions by a random sample of (public) firms. We therefore include all acquisitions by the firms in our sample, whereas the Large Merger Series includes only the largest acquisitions. Second, several firms in our randomly selected sample of acquirers are small, whereas the Large Merger Series data include only the largest acquirers.

Measures and Data Sources

We use archival time-series data to measure our conceptual variables. We do so because a proper accounting of the future effects of acquisitions requires data over time. Survey data on a long enough time series are difficult to obtain. Furthermore, survey data on knowledge and innovation are prone to self-report and memory biases.

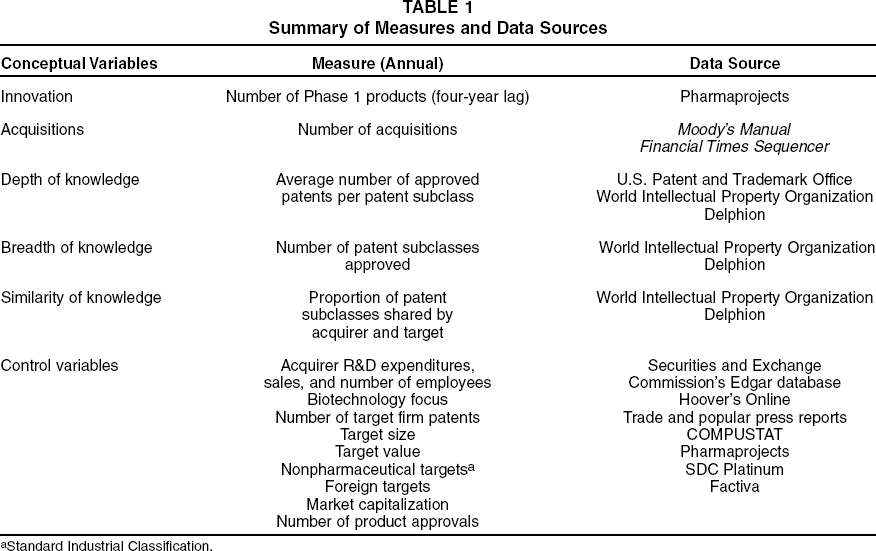

We were unable to find a single database that contains cross-sectional, time-series data on all our variables of interest. We therefore put together our database on a firm-by-firm and year-by-year basis, using different sources for different variables. Table 1 provides a summary of the measures and data sources. We provide information on each of the key measures next.

Summary of Measures and Data Sources

Standard Industrial Classification.

Innovation

Innovation occurs at many stages in the pharmaceutical industry: from the discovery of new molecules to the introduction of drugs based on these molecules into the marketplace. In general, prior research has used patent counts as a measure of innovation (Ahuja and Katila 2001; Jensen 1987; Narin, Noma, and Perry 1987). Although patent counts provide a measure of technical knowledge, patents are at best an incomplete measure of innovation, because patents may or may not translate into actual drugs. It might therefore be more appropriate to consider more product-based measures of innovation.

An obvious metric at first glance would be the number of new drugs that firms in our sample introduce into the marketplace over time. On closer examination, however, this metric is not well suited for our purposes because of the large time lags involved in developing and testing new pharmaceutical products. To solve this problem, we use a measure of innovation that is intermediate between patents and actual drug introductions: the number of products in Phase 1 trials by each firm in each year. (For additional details on this measure of innovation, see Appendix A.)

We obtain product information (Phase 1 drugs) from the Pharmaprojects database, which identifies and monitors the progress of all significant new drug candidates as they enter pharmaceutical R&D programs around the world (www.pharmaprojects.co.uk; Snow 1993). New drug candidates are tracked through the various phases of pharmaceutical product development, up to market launch or discontinuation. All records are retained in the database, regardless of the fate of the drug. The cumulative nature of the database provides a comprehensive history of global drug R&D. We were unable to obtain information on product innovation for eight firms, because these firms were themselves acquired by other firms between 1997 and 2003. As such, we dropped them from the analyses.

Acquisitions

We measure the number of acquisitions in each year for each firm in the sample. We obtain this information from FIS Online, the electronic version of the Moody's Manual, and cross-check it with information from Financial Times Sequencer. Prior research has often relied on a dichotomous measure of acquisition, whereby a firm is judged to have either acquired one or more firms or not acquired at all (e.g., Hitt et al. 1991a). By measuring the actual number of acquisitions in each year, we obtain a more refined measure of the impact that knowledge obtained through acquisition has on innovation. 1

We also tested an alternative metric of knowledge obtained through acquisition by measuring the number of patents granted to each target in the three years leading up to the year of acquisition. Our results are robust to this metric.

Knowledge

The field-specific nature of knowledge implies that any measure should address knowledge both within and across fields. Therefore, to measure knowledge for a firm properly, we need to identify the specific fields in which the firm possesses knowledge. In the pharmaceutical industry, as noted previously, patents are an excellent indicator of firms’ technical knowledge. Patents have the added advantage that they are classified by the Patent Office as belonging to specific classes that relate to their field of use. Therefore, it is possible to identify the technical fields in which a firm has knowledge by studying the classes in which it holds patents.

Information on the nature of each patent class is available from the World Intellectual Property Organization. The number of approved patents in each patent class for each firm in each year is available from the Delphion database. Patent classifications vary in their level of specificity, and the World Intellectual Property Organization uses the following hierarchy of classifications: section (most general) → class → subclass → group → subgroup (most specific). An examination of patenting activity within each patent category indicates that the subclass level provides the appropriate level of specificity for our purposes, as there are more than 10,000 subclasses in which firms may have patents. Our sample of acquiring firms patented in more than 750 subclasses during the study period, and the targets that these firms acquired patented in 258 subclasses.

Depth of knowledge is measured as the average number of approved patents per patent subclass for each firm in each year. Breadth of knowledge is measured as the number of patent subclasses covered by each firm's approved patents in each year. 2 Similarity in knowledge is measured as the number of patent subclasses shared by the acquirer and target firm, divided by the total number of patent classes owned by the acquirer and target combined. 3

We also tested two alternative measures of breadth: entropy [E = Σnj=1pjln(1/pj)] and the Herfindahl–Hirschman concentration index (HH = Σnj = 1pj2), where pj = Pj/P is the fraction of the firm's patents in patent subclass j relative to its overall patent portfolio. The results using these measures are consistent with those from the simpler and more intuitive measure of breadth we use in the article.

We also tested an alternative measure of similarity that does not divide by the total number of patent classes owned by the acquirer and target. The results using this measure are consistent with those from the percentage measure of similarity we use in the article.

To calculate similarity, we therefore need to identify all the unique patent classes in which both acquirers and targets have approved patents. The problem of dealing with a large number of patent subclasses is intensified because many firms acquire more than one target a year, and each of these targets potentially has patents approved in one or more of the full set of patent subclasses. We first collect the number of unique patent subclasses for each target for each year across the entire period of our sample. We then compute the total number of patent subclasses that each acquirer has in common with each of its targets for three years leading up to the year of acquisition. We divide each number by the total number of patent subclasses owned during this period by the parent and each target combined. Next, we average across all targets acquired by a firm in a particular year to arrive at a measure of similarity between an acquirer and its targets in each year of the data set.

Conceptually, a proper measure of similarity should account for overlap in knowledge not just in the current year but also in previous years. One option is to sum data on all patent subclasses for all years for all acquirers and targets before acquisition. However, given the potential for knowledge to decay in high-technology industries, similarity in most recent knowledge is likely to be more relevant than knowledge from the distant past. To balance practical constraints with conceptual completeness, we chose a three-year window before acquisition to measure similarity.

Control variables

To control for the effects of factors beyond those described previously, we include data on additional variables related to both the acquirer and the target. Success or failure of acquisitions is often deemed to be a function of the culture of the firms involved. But culture, like love, is a many-splendored thing. Dimensions of culture could include (1) national culture, (2) organizational culture, (3) market culture, and (4) scientific culture. To control for these dimensions of culture, we include the following variables:

National culture: We measure whether the target firms have different countries of origin from the acquiring firm, and we sum across all targets in each year for each acquirer.

Organizational culture: We measure the acquirer's size (measured as the number of persons employed by the firm) and the target's size (measured using the price at which it was acquired). 4

Market culture: We measure whether the primary Standard Industrial Classification codes of the target firms are different from that of the parent, and we sum across all targets in each year for each acquirer.

Scientific culture: We measure the acquirer's biotechnology focus (coded as biotechnology-only or general pharmaceutical).

We also measured target size using number of employees, sales, net income, and assets. Data on these measures were more difficult to find for our entire sample. For the subsample for which we have data on these measures, we find that acquisition price correlates highly with each of the other measures of target size (all correlations > .78, p < .001).

In addition to these variables, we also include the acquirer's R&D intensity (R&D expenditures divided by sales) and the target's level of technical knowledge before the acquisition (measured as the number of patents received by the target in the preceding three years). We convert the dollar expenditures and sales figures for each year into constant 1982–1984 dollars by multiplying them by the appropriate inflation indices.

Model Specification

We seek to fulfill multiple objectives in our model specification. First, the model should enable us to estimate not only the current effects of internal and external knowledge on innovation but also their future effects in the years following the acquisition. This requirement allows for a more complete assessment of the true impact of acquisitions on innovation, because the effects of current knowledge (whether internal or external) on future innovation could last for many years.

Second, the model should account for heterogeneity due to firm-specific effects. Unobserved factors other than those explicitly addressed in our conceptual framework can also have an impact on innovation. For example, it could be that some firms tend to view innovation as the overriding goal of acquisitions, whereas innovation may be just one of many goals of other firms. Such goals are difficult to assess and are unobserved by the econometrician. Other examples of unobserved firm-specific variables include alliance-proneness, licensing arrangements, and quality of management. To parcel out the true effects of our hypothesized variables properly, we need to control for these unobserved effects.

To fulfill these objectives, our analysis combines an error-component regression model with a Koyck distributed-lag specification. As such, we assume that the effect of knowledge decays exponentially (Pakes and Schankerman 1984; Schott 1976, 1978; for an alternative viewpoint, see Madhavan and Grover 1998). The panel structure of our data enables us to use an error-component model that controls for unobserved firm-specific heterogeneity (Baltagi 2001). Our distributed-lag specification enables us to represent parsimoniously the effects of prior internal and external knowledge on innovation.

To obtain efficient and unbiased estimates of the future effects of current knowledge without a distributed-lag specification, we would need an infinite (or at least a very large) number of lags of data on the independent variables (Intriligator, Bodkin, and Hsiao 1996). Practically, such an estimation procedure creates severe problems with multicollinearity among the lagged knowledge terms. Our modeling challenge is similar to that faced by researchers attempting to model the effect of advertising on sales. There too, the key independent variables (advertising in that case, and knowledge in ours) could have effects not only in the current period but also in future periods. (For a classic exposition of this issue in marketing, see Clarke 1976; for a recent application, see Tellis, Chandy, and Thaivanich 2000.) The problem of multicollinearity is especially severe when key hypotheses revolve around the interaction effects, as is the case here.

A distributed-lag model, however, alleviates the need for and the problems caused by numerous lags on knowledge. Moreover, this specification provides an intuitive metric of the rate of decay of knowledge, thus enabling a calculation of the impact of current internal and external knowledge on innovation in future periods. An analysis of various lag specifications using our data indicates that a simple Koyck model (with its associated exponential decay pattern for knowledge) fits the data best. This specification is consistent with a long tradition of research in the advertising and investments areas (see Clarke 1976; Koyck 1954) and with other recent studies of innovation and knowledge (e.g., Dutta, Narasimhan, and Rajiv 1999).

We use the following model specification to test our hypotheses (for the model derivation, see Appendix B):

The element Iit* refers to the innovation output of firm i in year t*, where t* = t + n (n ≥ 0), and Acquisition, Depth, Breadth, and Similarity are defined in Table 1. For the reasons noted in Appendix A, we set n = 4 when estimating Equation 1. Controli,t is a matrix of control variables, μi and γt are the firm-specific and time-specific effects, and vi,tis the remaining error term.

Our dependent variable, innovation, is a count variable, and therefore it might be argued that it is appropriate to use a nonlinear (Poisson or negative binomial) specification to test our hypotheses. However, such an approach is not straightforward in our context. Estimation techniques that simultaneously account for (1) count data, (2) a lagged dependent variable, and (3) panel data are still in their infancy (see Windmeijer 2002). Recently, some of the pioneers in this area of econometrics (see Blundell, Griffith, and Windmeijer 2002; Windmeijer 2002) have developed a generalized method of moments (GMM) estimator that meets all three requirements.

Accordingly, we employed a GMM, quasi-differenced, linear feedback model to estimate the effects of the variables in Equation 1. The model diagnostics indicate that our specification is appropriate; that is, the hypothesis that our instrument set is valid cannot be rejected at the p < .10 level (Sargan statistic: χ2(13) = 11.89, p = .53). In addition, the pattern of serial correlation in the first-differenced residuals is consistent with the assumption of these models that the uit disturbances are serially uncorrelated; that is, the Δuits have a significant and negative first-order correlation (M1 = −2.01, p < .10) and no significant second-order correlation (M2 = 1.23, p < .10) (Bond 2002). Thus, overall, the null hypothesis that our moment conditions are valid cannot be rejected at the p < .10 level (Blundell, Bond, and Windmeijer 2000). Finally, the results from the GMM estimation are similar to the more standard generalized least squares estimation results we report subsequently. However, the interpretation of interaction effects is difficult in nonlinear GMM models because marginal effects are a function of all independent variables, not just the variables in the interaction term (see Ai and Norton 2001, 2003). This problem of interpretation is compounded by the presence of a large number of independent variables. Moreover, the error distribution associated with the interaction parameters in the nonlinear specification is unknown (see Ai and Norton 2001, 2003); thus, the standard errors and significance levels of the interaction parameters are not available. Therefore, we report results from the more traditional random-effects generalized least squares estimator (Baltagi 2001) in the next section.

Results

Table 2 presents the descriptive statistics for the variables of interest. Table 3 presents the estimation results with the number of Phase 1 products developed by the acquirer as the dependent variable. We test three models: Model 1 tests the effect of external knowledge only, Model 2 tests the effect of internal knowledge only, and Model 3 tests the effect of both internal and external knowledge. Model 3 therefore presents the estimates for our model in Equation 1.

Descriptive Statistics by Firm

We run three models to show the importance, as we argued previously, of examining the effect of internal and external knowledge acting together as opposed to separately. As the results show, our hypothesized model (Model 3) outperforms Models 1 and 2. The R2 increases from .46 (Model 1) and .49 (Model 2) to .56 (Model 3), an increase of 22% and 14%, respectively (see Table 3). These increases are all statistically significant at the p < .001 level.

Effect of Internal and External Knowledge on Product Innovation by Acquirer

p < .10.

p < .05.

p < .01.

Notes: Standard errors are in parentheses. Dependent variable = number of drugs in Phase 1 trials per firm per year. Number of observations = 162.

The λ coefficient is positive and significantly different from zero in all models, indicating that the effect of knowledge on innovation continues into future periods. The estimate of this decay parameter in the fully specified models (λ= .19, p < .01) can be used to compute the long-term impact of each component of knowledge using the following formula:

We next describe the results for each of our hypotheses and focus only on the results of the estimation of our hypothesized model (Model 3).

Depth of Knowledge and Innovation

H1 argues that firms with high depth of knowledge produce more innovations than do firms with low depth of knowledge. The coefficient of depth of knowledge is significant and positive in Model 3 (β = .11, p < .05) (see Table 3). Therefore, in support of H1 the greater the acquirer's depth of knowledge, the greater is its innovation output.

H2 suggests that firms with high depth of knowledge derive more innovations from acquisitions than do firms with low depth of knowledge. In other words, the hypothesis predicts a positive interaction effect of number of acquisitions and depth of knowledge. Our results support this hypothesis.

For the sake of exposition, we next present some simple results from a bivariate categorical analysis of the interaction effect of depth of knowledge and acquisitions on innovation. Table 4 reports the results using median splits of acquirers based on their number of acquisitions and depth of knowledge. Firms that are high in both depth of knowledge and the number of acquisitions appear to produce the most innovations. The formal analysis in Table 3 confirms this result. The coefficient of the interaction term of depth and acquisitions in Table 3 is significant and positive in Model 3 (β = .12, p < .01). This result suggests that the marginal impact of acquisitions on innovation is greater for firms with high depth of knowledge than for other firms.

Breadth of Knowledge and Innovation

H3 argues that high breadth of knowledge leads to greater innovation than low breadth of knowledge. The coefficient of breadth of knowledge is significant and positive in Model 3 (β = .09, p < .01) (see Table 3). Thus, in strong support of H3, the greater the acquirer's breadth of knowledge, the greater is its innovation output.

H4 suggests that firms with high breadth of knowledge derive more innovations from acquisitions than do firms with low breadth of knowledge. In other words, the hypothesis predicts a positive interaction effect of number of acquisitions and breadth of knowledge. Table 5 reports the results using median splits of firms based on their number of acquisitions and breadth of knowledge. Firms that are high in both breadth of knowledge and the number of acquisitions appear to produce the most innovations. However, the formal results in Table 3 do not support this hypothesis. The coefficient of the interaction term of breadth and acquisitions is not significantly different from zero in Model 3 (β = -.02, p = .13).

Mean Number of Products in Phase 1 Trials for Firms with High Versus Low Acquisitions and High Versus Low Depth of Knowledge

Mean Number of Products in Phase 1 Trials for Firms with High Versus Low Acquisitions and High Versus Low Breadth of Knowledge

It is possible that the nonsignificant coefficient of the breadth x acquisitions interaction is due to multicollinearity among our breadth, acquisitions, and depth variables. To assess whether multicollinearity is the true cause of this result, we carry out five sets of analyses. First, we estimate the variance inflation factor for the breadth and depth variables and their interactions with acquisitions in our model. The variance inflation factor statistics for these variables are all well below the acceptable cutoff of 10. Second, using the condition index method (Belsley, Kuh, and Welsch 1980), we find the condition number to be 13.45, well below the cutoff of 30 (all singular values except one are below 10). Third, we reestimate Model 3 using Lance's (1988) method after we correct for multicollinearity due to interaction terms. The coefficient remains nonsignificant, indicating that multicollinearity between the main and interaction effects is not the cause of this result. Fourth, we test alternative functional specifications of breadth (e.g., by using a squared breadth term to test for curvilinear effects). The analyses do not provide support for such alternative specifications. Fifth, we check if the main and interaction effects of breadth hold when the main and interaction effects of depth are dropped, and vice versa. They do. In summary, these analyses indicate that multicollinearity does not drive our results.

Similarity of Knowledge and Innovation

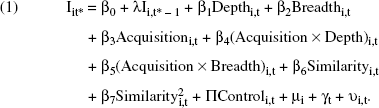

H5 suggests that acquirers with knowledge that is moderately similar to that of their targets produce more innovations after acquisitions than do acquirers with knowledge that is very similar to or very different from that of the targets. In Model 3, the coefficient of similarity is significant and positive (β = 40.41, p < .05), and the square of similarity is significant and negative (β = −263.07, p < .05) (see Table 3). The results provide support for H5 and, taken together, imply that the overall effect of similarity is curvilinear. Figure 1 depicts the predicted effect of similarity based on the model coefficients reported in Table 3. All our data points except one fall within the range of similarity values depicted in Figure 1. As the figure indicates, increasing similarity first increases and then decreases the innovation activity of the parent firm.

Predicted Effect of Similarity on Product Innovation

Additional Analyses

Relative importance of depth versus breadth

The results described previously indicate that depth and breadth of knowledge have significant effects on innovation. To identify the relative effects of depth and breadth on innovation, we also compute the standardized coefficients of these variables. A comparison of the standardized coefficients shows that breadth has a greater impact on innovation than depth does (βbreadth = .45 versus βdepth = .16). Furthermore, as Table 2 indicates, the effect size as captured by the Pearson correlation (see Fern and Monroe 1996; Sawyer and Ball 1981) between breadth and innovation is higher than that between depth and innovation (.57 versus .46). It appears that breadth, more than depth, promotes flexibility and adaptability (Volberda 1996), as well as the ability to combine diverse types of knowledge (see Henderson and Cockburn 1994; Pisano 1994), thus leading to greater innovation.

Process checks

An implicit argument in our hypotheses on the role of internal knowledge on innovation through acquisition is that firms with greater internal knowledge choose better targets. To test the validity of this claim, we conduct process checks on the relationship between acquirers’ knowledge and the quality of the targets they acquire. Specifically, we conduct additional analyses to address whether firms with greater depth and breadth of knowledge acquire targets that (1) have greater knowledge and (2) have more significant knowledge.

First, to assess whether firms with greater internal knowledge choose targets that have greater knowledge, we compare the average number of patents per target for acquirers with high versus low depth and breadth of knowledge (see Figures 2 and 3). We classify acquirers as low or high in depth and breadth of knowledge using a median split on the depth and breadth of patents granted to these firms over the sample period. Figures 2 and 3 show that acquirers with high levels of depth and breadth of knowledge acquire targets with higher patents on average than do acquirers with low depth and breadth, respectively (7.15 versus .87 and 7.32 versus .70, respectively; p < .05).

Average Patents per Target Acquired by Acquirers with High Versus Low Depth of Knowledge

Average Patents per Target Acquired by Acquirers with High Versus Low Breadth of Knowledge

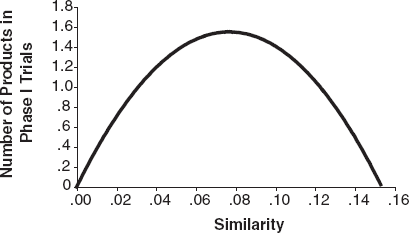

Second, to assess whether firms with greater internal knowledge choose targets that have more significant knowledge, we compare the average number of forward citations per patent per target acquired by firms with high versus low depth and breadth of knowledge. As in academic articles, forward citations provide a reasonable measure of the significance of a particular patent, because they indicate how many other patents cited this patent in their reference list. (For a similar use of this measure in the patents context, see Dutta, Narasimhan, and Rajiv 1999; Hall, Jaffee, and Trajtenberg 2000.) Figures 4 and 5 show that acquirers with high levels of depth and breadth of knowledge acquire targets with higher forward citations per patent per target than do acquirers with low depth and breadth, respectively (53.74 versus 12.96 and 54.09 versus 9.47, respectively; p < .05 for both).

Average Forward Citations per Patent per Target Acquired by Acquirers with High Versus Low Depth of Knowledge

Average Forward Citations per Patent per Target Acquired by Acquirers with High Versus Low Breadth of Knowledge

Endogeneity

It is possible that depth, breadth, and acquisitions are themselves endogenous with respect to acquirer variables such as R&D and size. Moreover, breadth of knowledge could itself be a function of depth, and vice versa. To check for potential effects of endogeneity, we test a three-stage least squares (3SLS) specification that treats depth, breadth, and acquisitions as endogenous, that is, dependent on one another as well as on various control variables such as R&D and firm size. The pattern of results is similar to those from the panel model we report in Table 3. More formally, the Hausman coefficient (m) for the comparison of the coefficients of the 3SLS model with the panel model is χ2(15) = 3.95 (p = .97); thus, the test fails to reject the null hypothesis that the difference in coefficients is not systematic. In other words, endogeneity does not cause problems with the consistency of our parameter estimates: The panel data model we use in the article is consistent and efficient, whereas the 3SLS model is consistent but inefficient (see Pindyck and Rubinfeld 1991).

Heterogeneity in slopes

The model in Equation 1 corrects for unobserved heterogeneity through error decomposition. It does not, however, correct for heterogeneity in slopes. If, for example, companies that acquire large targets are less capable of leveraging acquisitions into innovation than companies that acquire small targets, such heterogeneity could be problematic. To account for potential heterogeneity in our key variables, we run random coefficients models that allow the coefficients for our hypothesized variables to vary randomly. We find some evidence for heterogeneity in the effect of depth on innovation. This suggests that though the effects of depth are positive for the average firm, some firms may experience a negative effect of depth on innovation. In general, however, the results of this analysis are consistent with those for the error decomposition model we report in the article.

Discussion

This article highlights two sources of knowledge: internal and external. Internal knowledge by itself can drive innovation in future periods, but internal knowledge also has another, more subtle benefit. Deep internal knowledge provides firms with a superior ability to generate innovations from external sources such as acquisitions.

The results support our central argument that the innovation outcomes of acquisitions are driven by the preacquisition knowledge of the acquirer and its similarity with the targets’ knowledge. We find a strong interaction effect of the depth of the acquirer's existing knowledge and that of its acquisitions on innovation output. We also find that moderate similarity leads to greater postacquisition innovation than does either low or a high similarity between the acquirer's and the target's preacquisition knowledge. Therefore, for firms with appropriate internal knowledge and fit, acquisitions can act as a tonic for innovation. However, when we control for firms’ internal knowledge, we find that acquisitions on their own act as a placebo; that is, they have no effect on firms’ postacquisition innovation output (βacquisition = -.02, p > .10; see Table 3).

Implications for Research

An important theoretical contribution of our article is that it sheds more light on the nature of knowledge and its role in innovation. We show how firms’ internal knowledge interacts with external knowledge gained through acquisitions to foster innovation. Thus, our theoretical perspective enables us to reexamine the impact of acquisitions on innovation; this in turn enables us to empirically extend, clarify, and correct some of the conclusions of prior research.

First, in general, prior research on innovation has focused on how internal knowledge influences innovation within the firm. In contrast we examine how, over time, both internal and external knowledge interact to influence innovation. Specifically, we observe whether acquisitions as a source of external knowledge lead to positive, negative, or no gains in innovation to acquiring firms. The limited research that has examined the influence of acquisitions on innovation has generally suggested and found that this influence is negative (Ernst and Vitt 2000; Hitt et al. 1991a; Miller 1990). We argue that the opposite is more likely, especially in industries in which firms undertake acquisitions with the express intention to boost innovation by gaining external knowledge. By including both large and small firms in our sample, examining lagged effects, and controlling for firm-specific effects, we show that acquisitions can increase innovation in such contexts.

Second, prior research on acquisitions and innovation tends to focus on postacquisition integration activities. In contrast, we control for such firm-specific effects and focus on the knowledge that acquiring firms bring to the acquisition. We then examine how the depth, breadth, and similarity of knowledge influence postacquisition innovation. Relatedly, prior research on knowledge has mainly speculated on the processes by which knowledge is created in firms. There has been much discussion of how firms learn, their absorptive capacity, and the factors influencing learning and absorption (see Cohen and Levinthal 1989; Zahra and George 2002). Limited empirical research has tested these ideas, and to our knowledge, none has examined them in the context of acquisitions. We contribute to this literature by showing that absorptive capacity is particularly critical to the successful acquisition and use of external knowledge. Firms that have greater absorptive capacity because of their existing internal knowledge are better at choosing and integrating external knowledge and using it to create still newer knowledge.

Third, prior research has argued for a positive linear effect of similarity between the knowledge of the acquirer and that of the target (see Singh and Montgomery 1987; for an exception, see Ahuja and Katila 2001). In contrast, we argue for and show a nonlinear effect of similarity in knowledge on postacquisition innovation. Specifically, firms that have a moderate amount of similarity with targets’ knowledge gain more from acquisitions than do firms whose knowledge is very similar to or very different from the knowledge of targets.

Implications for Firms

This article has several recommendations for firms involved in acquisition activity. First, the article suggests two independent routes to increased innovation: firms can either concentrate on building internal knowledge or buy it through acquisitions. Acquisitions offer acquiring firms access to knowledge that they may not otherwise have and that might combine with their internal knowledge to boost innovation. Independent of acquisition, however, building knowledge offers firms greater ability to use past knowledge to develop new knowledge and thus boost innovation. Moreover, it is not just the amount of internal knowledge that matters; rather, it is the type of knowledge. Firms with depth and breadth of internal knowledge are less likely to suffer from lockout (Leonard-Barton 1995), they have greater combinative capabilities (Kogut and Zander 1992), and they can use prior know-how to learn through both exploration and exploitation (Bierly and Chakrabarti 1996; March 1991). The article's results also suggest that breadth and depth have different magnitudes of impact on innovation: The impact of breadth is higher than that of depth. An excessive focus on deepening knowledge in an area could be counterproductive if it comes at the expense of breadth. Breadth of knowledge may promote flexibility, adaptability, and the ability to combine diverse types of knowledge (see Henderson and Cockburn 1994; Pisano 1994; Volberda 1996). Furthermore, the product scope that breadth provides also ensures the greater likelihood of serendipity and happy accidents, both of which are important drivers of product innovation (Helfat and Raubitschek 2000).

Second and more important, the article suggests that the two strategies of acquisitions and developing internal knowledge lead to even greater innovation when pursued in tandem. Despite the pessimism of many academics, some industry observers recognize the competitive advantages that can be derived from acquisitions. For example a Wall Street Journal article (O'Boyle 1988, p. 26) on the German chemical company Bayer's reluctance to engage in acquisitions quotes an industry expert, Michael Eckstut, as saying that though “Bayer has had a phenomenal record over the last few years, doing things internally can sometimes carry a higher risk than acquisitions.” Eckstut also warned that “companies that preclude acquisitions as a way of obtaining new skills and resources run the risk of losing leadership because they are too introverted.”

Firms that first develop deep internal knowledge have greater absorptive capacity; this enables them to choose and leverage external knowledge better. Indeed, successful firms appear to recognize this point. For example, in its annual report, Johnson & Johnson (1996, p. 4), one of the innovative firms in our sample, notes that “while internal development is our preferred source of growth, we view selective acquisitions as an appropriate mechanism for supplementing our efforts.”

Third, it is not merely the amount of knowledge that the acquirer brings to the acquisition that drives its postacquisition innovation: The similarity of its knowledge with that of the target is crucial too (Richardson 1972). Differences in the nature of firms’ knowledge can be considerable even within industries, and they can significantly affect the success of acquisitions. To gain the most from acquisitions, acquiring firms should ensure that their internal knowledge is neither too close nor too far removed from that of the target firm.

Finally, in contrast to prior research, which typically emphasizes the similarity between the markets in which parent and target operate (e.g., Singh and Montgomery 1987), the national origins of the two firms (e.g., Harzing 2002), and their relative size, we emphasize the importance to acquirers of assessing the fit in their knowledge with that of targets. We show that when similarity of knowledge is taken into account, other, more conventional measures of similarity have a less significant impact on postacquisition innovation. Of these, we find that only country of origin has a significant influence on innovation beyond the effects of similarity in knowledge we propose. The size of the target and its market similarity with the acquirer matter less. This suggests that in contexts in which innovation is an important strategic objective, acquiring firms should identify and choose targets on the basis of their fit in knowledge over other aspects of similarity.

Limitations and Further Research

Acquisitions are a complex phenomenon, and ours is by no means the last word on the topic. Our research has several limitations, some of which offer possibilities for further research. First, as in any early empirical endeavor, we have had to maneuver carefully between the Scylla of model misspecification and the Charybdis of model overparameterization. We cannot, within one study, exhaustively examine the many types of internal and external knowledge.

When studying internal knowledge, we examine the knowledge contained in patents. Patents are a widely used measure of knowledge in research across a range of high-tech industries: pharmaceuticals (Cockburn, Henderson, and Stern 1999), semiconductors (Dutta, Narasimhan, and Rajiv 1999), chemicals (Ahuja and Katila 2001), robotics (Katila and Ahuja 2002), and the industrial machinery industry in general (Arundel and Kabla 1998; Cockburn and Griliches 1988). Nevertheless, in some industries, important sources of knowledge may be difficult to codify, and future researchers on these industries may wish to employ other measures of such knowledge. Acquiring firms may also sometimes gain patents but not necessarily additional knowledge from their targets. Some patents may eventually manifest themselves as product innovations and thus artificially inflate the correlations between our dependent variable (innovation) and our independent variables (which are patent based). Fortunately, in the pharmaceutical industry, few patents end up becoming product innovations (DiMasi, Hansen, and Grabowski 2003); as such, this inflation is likely to be very small. Similarly, when studying external knowledge, we examine the knowledge obtained through acquisitions. Again, although acquisitions are an important source of external knowledge, other sources of such knowledge, such as alliances and interfirm cooperation, exist and are worthy of attention (see, e.g., Rindfleisch and Moorman 2001).

Second, we examine only one, albeit important, type of knowledge, namely, technical knowledge. The role of other types of knowledge—for example, knowledge related to consumers and competitors—also merits study (see Capron and Hulland 1999; Li and Calantone 1998; Moorman and Rust 1999). In this article, we attempt to capture the effects due to other sources of internal and external knowledge by accounting for firm-specific heterogeneity, as well as by using important control variables. Nevertheless, this remains an empirical solution. To gain a more complete theoretical picture, future researchers may wish to employ more explicit and fine-grained measures of other sources of internal and external knowledge than the ones we use here. Third, we use data that are at the yearly level of aggregation. As such, our model may overestimate the decay parameter (λ) in Equation 1 (Clarke 1976). More disaggregate data will allow for a more accurate assessment of the decay parameter. Fourth, our model assumes that the effect of knowledge decays exponentially. Although this assumption is in line with the bulk of the literature (Dutta, Narasimhan, and Rajiv 1999; Pakes and Schankerman 1984; Schott 1976, 1978), other researchers posit that knowledge can appreciate over time (see Madhavan and Grover 1998). More disaggregate data would enable the application of other, more flexible functional forms of the lag specification.

Finally, we study only one, albeit important, industry: pharmaceuticals. The choice of a single industry is critical in ensuring internal validity because the appropriate measures of knowledge can be quite different across industries. The pharmaceutical industry is especially suited to our use of patents as a measure of knowledge. Choosing one industry, however, also raises the issue of generalizability. The pharmaceutical industry is unique in many ways, but it is possible to make at least some tentative generalizations from pharmaceuticals to other high-tech industries. Indeed, we are not alone in this belief (see also Bierly and Chakrabarti 1996; Cockburn, Henderson, and Stern 1999; Shankar, Carpenter, and Krishnamurthi 1998). Nevertheless, other industries in which patenting is less common might require other measures of knowledge, and further research would benefit from an exploration of such empirical contexts.

Conclusion

A successful innovation strategy requires a judicious combination of internal and external sources of knowledge. Acquisitions provide a means to access external knowledge that can be difficult or even impossible to create through internal sources. For this reason, firms may not want to rely solely on internal sources of knowledge, but they may not want to rely solely on external sources either. We show that in the context of acquisitions, the two sources of knowledge—internal and external—interact in a dynamic fashion to produce innovations.

Acquisitions need not be a poison pill or even merely a placebo for innovation. For firms that first engage in internal knowledge development, the knowledge-based view of innovation we present in this article suggests just the opposite. Acquisitions can be a tonic for innovation.

Footnotes

Measuring Innovation

Though conceptually ideal, the number of new drugs that firms introduce into the marketplace over time is not empirically well suited for our purposes, mainly because of the large time lags involved in developing and testing new pharmaceutical products. After their synthesis and extraction, new drugs must go through preclinical and clinical trials and a process of Food and Drug Administration (FDA) approval before they are introduced into the market (Mathieu 2000). The average time in the 1990s for preclinical trials alone was 6 years (FDA 1999). The three phases of the clinical trials that follow took, on average, up to several months for Phase 1, several months to 2 years for Phase 2, and between 1 and 4 years for Phase 3. Finally, the process of FDA approval took, on average, another 1.5 years. As a consequence, the time from conception to product introduction in the pharmaceutical industry in the 1990s was frequently more than a decade. Given these large lags and the many intervening factors that come into play during this time, it is extraordinarily difficult to tie empirically the knowledge generated from individual acquisitions to all the future drug introductions that result from this knowledge.

To solve this problem, we use the number of products in Phase 1 trials by each firm in each year as our measure of innovation. This measure has several strengths. First, we cannot use approved products because of the time lags involved, so this is the next-best choice of a measure that goes beyond patents in being product based but nevertheless involves manageable lags. On the basis of information (FDA 1999; Mathieu 2000) on the average time from idea development to Phase 1 trials, we examine Phase 1 products four years after the year of acquisition.

Second, the measure correlates well with actual drug introductions. To confirm the link between Phase 1 trials and actual product approvals empirically, we calculated the correlation between the number of Phase 1 drugs of firms in our sample in 1996, 1997, and 1998 and the number of approved products in 2001. The correlations were all significant and positive (γ1996 = .76, p < .0000; γ1997 = .40, p < .05; and γ1998 = .51, p < .01, respectively).

Third, the measure is financially important because it is likely to correspond strongly with the stock market performance of the firm. Again, this is not surprising, given the relationship between drugs in Phase 1 and actual introductions. To confirm this intuition empirically, we collected data on the market valuation of the firm in each year in our sample. We find that the correlation between the number of Phase 1 drugs of firms in our sample in a particular year and market capitalization of the firms in that year is positive and significant (γ = .45, p < .0000).

Derivation of Empirical Model

Here, we derive our model specification. Let the relationship between knowledge and innovation for firm i at time t be represented as follows:

where I = innovation, and K = knowledge. Assume that (1) the effect of current knowledge on future innovation declines exponentially and (2) a real number λ measures the decay (or appreciation) of knowledge from year to year. Then, Equation B1 reduces to

A Koyck transformation on Equation B2, which involves lagging Equation B2 by one period, multiplying by X, and subtracting from the original Equation B2, results in

Next, we model the components of knowledge as follows:

where

Internal = f(Depth, Breadth),

External = f(Acquisition), and

Synergy = f(Depth x Acquisition, Breadth x Acquisition, Similarity).

Thus, Equation B4 reduces to

Substituting a linear specification of Equation B5 in Equation B3 and allowing for firm-specific and time-specific heterogeneity and an n-year lag between innovation and knowledge, we obtain Equation 1 (specified in the method section), which we use to test our hypotheses.