Abstract

Brand equity is a valuable yet fragile asset. The mounting frequency of product-harm crises and ill-prepared corporate responses to such crises can have profound consequences for brand equity. Yet there is little research on the marketing impact of crises. The authors employ the expectations–evidence framework to understand the impact of firms' responses to crises on customer-based brand equity. The results of a field survey and two laboratory experiments indicate that consumers interpret firm response on the basis of their prior expectations about the firm. The interaction of expectations and firm response is shown to affect postcrisis brand equity. The authors draw implications for the expectations–evidence framework and for the outcomes of different types of firm response (i.e., unambiguous support, ambiguous response, and unambiguous stonewalling) on brand equity.

For most firms, the equity vested in their brands is an invaluable yet fragile asset. The value of brand equity has been the subject of much recent research in marketing (Aaker 1996; Keller 1993; Shocker, Srivastava, and Ruekert 1994). The fragility of brand equity is less well understood. Brand equity is fragile because it is founded in consumers' beliefs and can be prone to large and sudden shifts outside of management's control because of consumers' exposure to new information, among other factors. For example, the recent consumer outrage at contaminated Coca-Cola cans in Belgium and France and the subsequent ineffective corporate response may have damaged the brand's equity in Europe (The Economist 1999).

Product-harm crises are discrete, well-publicized occurrences wherein products are found to be defective or dangerous (Siomkos and Kurzbard 1994). The increasing complexity of products, more stringent product-safety legislation, and more demanding customers have combined to make product-harm crises ever more frequent occurrences (Birch 1994; Patterson 1993). Despite the potentially devastating effects of crises, however, firms appear ill-prepared to handle them, and most firms faced with a crisis respond, at best, ambivalently (Mitroff and Pauchant 1990; Pearson and Clair 1998). In addition, crisis research that addresses marketing issues is scant, and little is known about the effects of different corporate responses on critical marketing variables such as brand equity (Dawar 1998a, b). Nevertheless, anecdotal evidence suggests that crises such as the Perrier incident need not inevitably be detrimental to the firm. For example, Tylenol emerged stronger from a terrorist capsule poisoning incident in the early 1980s by responding quickly and effectively to maintain consumer confidence in the brand (Murray and Shohen 1992). A recent study of 2645 consumers by the advertising agency DDB Needham showed that a company's handling of a crisis ranked as the third most important purchase influence (after product quality and handling of complaints) and was mentioned by 73% of consumers (Marketing News 1995). Corporate response to a crisis appears to be a critical determinant of the impact of the crisis on consumer beliefs that constitute brand equity (Aaker 1991; Keller 1993).

However, on the basis of previous research that demonstrates consumers' tendency to interpret information in the context of prior expectations, we suggest that the impact of firm response alone is likely to be insufficient to predict effects on brand equity (e.g., Smith and Swinyard 1982). Rather, we propose that objectively identical firm responses may have substantially different impacts on customer-based brand equity depending on consumers' prior expectations about the firm. For the purposes of this study, we define consumers' expectations about a firm as their beliefs about the behavior of a firm in a given situation based on their experience and knowledge of the past behavior of the firm.

Previous research on the interaction of consumers' prior expectations and new evidence has shown that consumers' interpretation of evidence is affected by their prior expectations but that some of the predicted interactions are elusive (Deighton 1984; Ha and Hoch 1989; Smith 1993). Specifically, findings are mixed for the hypothesis that evidence consistent with prior positive evaluations leads to more positive evaluations than positive evidence alone (e.g., Deighton 1984; Smith 1993). Researchers suggest that prior positive expectations create a ceiling effect in the sense that new positive information cannot improve an already high positive evaluation. A crisis setting, which provides negative information, overcomes this methodological limitation in detecting this interaction. Furthermore, brand equity research has tended to examine the construct as an independent rather than a dependent variable. As a result, little is known about the impact of corporate actions on brand equity (Aaker 1996). Corporate actions such as a firm's response to a crisis can have a rapid and profound impact on customer-based brand equity.

The present research has two objectives: (1) to develop a preliminary understanding of the impact of crisis response on customer-based brand equity by examining the phenomenon through the theoretical lens of the expectations– evidence framework and (2) to study expectations–evidence interactions in a novel setting (that of product-harm crises) that alleviates methodological problems that prevent detection of some of the key effects hypothesized by theory. In the following sections, we review relevant research, develop hypotheses, and present results from a field survey and two experiments designed to test these hypotheses. We discuss implications of the results, the study's limitations, and directions for further research.

Background

People are constantly exposed to vast amounts of information in the environment. Because of cognitive processing constraints, they adopt means of filtering, selectively attending to, and processing bits of relevant information. Research on the expectations–evidence framework—under a variety of labels, including “confirmatory-bias,” “labeling effects,” and the broader rubric of “framing”—examines how such information-selection heuristics may result in biased judgments (Darley and Gross 1983). We focus on how the nature of prior expectations affects the interpretation of evidence. In the following subsections, we describe the key constructs and the predicted effects.

Brand Equity

Brand equity has been variously conceptualized as a financial measure, a measure of consumers' behavior (e.g., willingness to pay a premium, brand loyalty), or a measure of consumers' beliefs (Aaker 1991; Keller 1998). Most authors agree that brand equity is the differential contribution of the brand name on the value of the branded product. Our focus is customer-based brand equity, which is defined as “the differential effect that brand knowledge has on consumer response to the marketing of that brand” (Keller 1993, p. 45). Differential consumer response (e.g., intention to purchase) is based on consumers' knowledge of the brand (e.g., perceptions of quality and trust) as well as the favorability of associations (e.g., brand attitudes and brand desirability). For the purposes of this study, we treat brand equity as a composite of brand-related beliefs, including brand attitudes, brand desirability, perceptions of quality, brand trust (reliability, dependability, trustworthiness), and brand purchase likelihood (Aaker 1991; Agarwal and Rao 1996; Keller 1993).

Although little research directly examines the impact of crises on brand equity, some financial studies show that firms suffer large drops in stock price (averaging 7% of net worth) because of product recalls, which reflects not only the direct costs of the recall but also the indirect costs, including damage to brand equity (Davidson and Worrell 1992; Pruitt and Peterson 1986). From the available research, we expect that publicity about dangerous or defective products, considered independently, will have a negative impact on brand equity. In particular, using Keller's (1993) terminology, the knowledge and favorability of brand associations components of brand equity will decline in a product-harm crisis. Although firm response to crises may differentially affect the various components of brand equity, our hypotheses focus on the moderating effects of consumers' prior expectations on the composite construct.

Firm Response

In practice, firm response to crises varies from stonewalling, as evidenced by Exxon's reaction in the wake of the Valdez oil spill in 1989 (Williams and Olaniran 1994), to the assumption of responsibility and unconditional product recall and communication exemplified by Johnson & Johnson's handling of the Tylenol poisoning crisis (Murray and Shohen 1992). 1 Most instances of firm response, however, can be placed between these two extremes. For example, as the Perrier product-harm crisis unfolded, the New York and Paris offices were issuing inconsistent statements as to the cause of the benzene contamination and the remedial measures undertaken, which led to the perception of an ambivalent and confused corporate response (Kurzbard and Siomkos 1992).

Sometimes stonewalling may be legitimate in that the firm may accurately deny responsibility for a crisis it did not cause. Similarly, a firm may assume responsibility for a crisis it did not cause. In either case, we believe that the effects on brand equity will depend on consumers' perceptions of firm responsibility and firm response. These perceptions may or may not coincide with the actual cause of the crisis.

Conceptually, firm response can be considered along a continuum from unambiguous support to unambiguous stonewalling. Unambiguous support consists of assumption of responsibility, an apology to consumers or other affected constituencies, and some form of remedy, such as a voluntary product recall and free replacement (Hearit 1994). Stonewalling consists of a denial of responsibility and absence of remedial measures or no communication at all. Between these two extremes lie ambiguous responses, some dimensions of which suggest support and others that do not. For example, a firm may suggest through advertisements that remedial action is being taken but fall short of assuming responsibility, extending an apology, or instituting a product recall (Heinzl 1993).

Interaction of Expectations and Evidence

The primary consequence of including expectations in a model of belief updating is that objective evidence may be interpreted very differently depending on these expectations (Oliver and Winer 1987). Consumers tend to selectively seek and assign greater weight to evidence that is consistent with their expectations (Darley and Gross 1983). In the marketing literature, studies typically manipulate prior expectations by exposing subjects to advertising, followed by independent confirmatory or disconfirmatory evidence (Deighton 1984; Hoch and Ha 1986; Kopalle and Lehmann 1995; Olson and Dover 1979; Smith 1993; Snyder and Swann 1978). As pointed out previously, these studies find support for the interaction between expectation and evidence consistently when the evidence is either disconfirming or ambiguous.

We organize our review of the literature on the interaction of expectations and evidence according to the strength of prior expectations and the degree of consistency of evidence with these expectations. Prior expectations are examined at two levels (strong positive and weak positive), and consistency of evidence with these expectations at three levels (consistent, ambiguous, and inconsistent). Figure 1, based on a framework initially proposed in the context of attribution theory (Metalsky and Abramson 1981), provides a summary of the theoretical predictions. In a product-harm crisis context, we expect that selective information processing driven by confirmatory biases affects consumers' brand-related beliefs and behavioral outcomes such as purchase intentions. As stated previously, we conceptualize consumers' expectations about a firm as their beliefs about the behavior of a firm in a given situation based on their experience and knowledge of the past behavior of the firm. In the case we examine here, these expectations refer to how the firm is expected to respond to a crisis. These expectations may themselves be embedded in corporate associations, which Brown and Dacin (1997) define as a generic label for all the information about a company that a person holds. These associations differ from brand equity in that they relate to the firm rather than to specific products or services (Brown and Dacin 1997; also, Keller [1993] distinguishes between brand knowledge and secondary associations, and Aaker [1996] distinguishes between organizational associations and brand associations). Because expectations about firm behavior form secondary associations for the brand and may be embedded in the brand schema, we recognize that it may be difficult to separate expectations from brand equity. Nevertheless, conceptually we treat expectations independently here, with the objective of assessing the impact of their interaction with situational evidence on brand equity. Note that we are predicting effects of the interaction of expectations and evidence on the brand schema rather than on consumers' judgments of the firm's response. Because the expectations–evidence framework has never been examined in the crisis context, we first propose to test its relevance in a field setting. Subsequently, we explore interactions predicted by the framework under controlled laboratory conditions.

THEORETICAL PREDICTIONS ON THE INTERACTION OF EXPECTATIONS AND EVIDENCE

Research Hypotheses

Selective Attention and Weighting

Selective information processing is expected to occur in crisis settings for two reasons. First, the general observation that consumers attempt to confirm prior expectations selectively should also apply in a crisis setting. Second, consumers who buy a product may seek to minimize cognitive dissonance in a crisis by selectively processing information that is consistent with their prior purchase of the brand (see Kiesler, Nisbett, and Zanna 1969). Specifically, we expect that consumers with strong prior expectations about the firm (e.g., those who purchase the firm's brand) are more likely to attend to information about the crisis than are consumers who have weak prior expectations (e.g., those who purchase other firms' brands). At a more detailed level, we expect that consumers differentially weight aspects of the crisis information, such as the dangers of the product and the firm's responsiveness, depending on their prior expectations. These differences in cognitive processing are expected to affect behavioral outcomes such as intentions to purchase, which as we mentioned previously, is the consumer response component of brand equity. We propose that

H1: Consumers with strong prior expectations about a firm affected by a product-harm crisis will be more likely to be aware of the crisis than consumers who have weak prior expectations about the firm.

H2: In a product-harm crisis, consumers will differentially attend to and weight aspects of information in their intentions to purchase, depending on their prior expectations.

Theoretically, expectations are said to generate hypotheses, which are subsequently tested against evidence (such as product trial, objective product test reports, expert referrals, and so on). However, these tests are inherently biased because of consumers' tendency to selectively seek and process confirmatory rather than disconfirmatory evidence (Klayman and Ha 1987). Hypothesis confirmation results in a cumulative interactive effect of expectations and evidence on judgments of, say, product quality (Deighton 1984; Smith 1993), whereas initial exposure alone only serves to generate expectations.

Unambiguous Confirmation

Deighton (1984) shows that consumers' judgments of the reliability of Ford cars based on objective product test data in Consumer Reports are positively affected by preexposure to Ford advertisements. In his study, consumers interpreted the objective evidence from Consumer Reports much more positively when they had been exposed to the advertisement previously than when they had not. The advertisement alone and the evidence alone had little effect on consumers' judgments. Although later studies have shown that evidence alone may have an effect on judgments (e.g., Smith 1993), it is the interaction of expectations and confirmatory evidence that creates a strong cumulative effect (e.g., Levin and Gaeth 1988). However, advertising and evidence interactions are not universally found. Smith (1993) shows that the weight of product trial evidence dominated the weight of advertising in consumers' judgments when the two pieces of information were consistently favorable, resulting in no difference between an advertisement + trial condition and a trial-only condition. However, in the same experiment, advertising did moderate a negative (disconfirmatory) product experience.

Hoch and Ha (1986) and Ha and Hoch (1989) demonstrate interactions of advertisement-generated expectations with product trial evidence, but only when the evidence was ambiguous and open to multiple interpretations and not when the evidence was unambiguously consistent with expectations. Ha and Hoch (1989, p. 354) argue that expectation–evidence interactions “are limited to cases in which the objective evidence was ambiguous.” They (p. 357) suggest that Deighton's (1984) finding of an interaction using unambiguous evidence may have been the result of providing subjects with “an enormous amount of data, effectively forcing subjects to engage in selective processing.” A shortcoming of this explanation is that it does not explain how advertising can moderate the effects of unambiguous disconfirmation (Olson and Dover 1979; Smith 1993).

Smith (1993) offers a methodological explanation for the lack of a significant interaction for confirmatory evidence. He suggests that advertising information is dominated by the more compelling evidence from product trial, which creates a ceiling effect. This explanation is supported by a study using panel data by Deighton, Henderson, and Neslin (1994), who find that the evidence from product usage so dominates expectations created by advertising that the predicted interaction is swamped. This methodological explanation suggests that the interaction occurs but is not detected because of calibration or measurement lacunae. Thus, theory suggests that expectations coupled with confirmatory evidence should lead to a cumulative effect on judgments (Cell 1, Figure 1), but in practice the effect has been elusive.

If the methodological explanation holds, removing the ceiling effect should enable detection of the interaction. In contrast, if the theoretical explanation is accurate, no interaction should be detected even if the ceiling effect is removed. In a crisis situation, the baseline impact (that of a product-harm crisis) on beliefs is inherently negative, counteracting the ceiling effect. Consistent with the theoretical framework, firm response to the crisis is considered at three levels, including unambiguous support, ambiguous support, and unambiguous stonewalling. When prior expectations are weak, belief change is based primarily on the evidence (Cell 4, Figure 1). Consumers' strong positive prior expectations about a firm should combine with unambiguous support during the crisis to counter the negative effect of the crisis. As a result, with respect to an expectations-only control situation in which no crisis occurs, we predict the following effect:

H3: Unambiguous support following a product-harm crisis will lead to a smaller loss of brand equity when consumers' positive prior expectations are strong rather than weak.

Ambiguity

Confirmatory biases are particularly pronounced when the evidence against which consumers test their hypotheses is inherently ambiguous (Darley and Gross 1983; Ha and Hoch 1989; Hoch and Deighton 1989; Hoch and Ha 1986). Ambiguity of firm response is high if the various dimensions of firm response suggest different levels of apology and/or remedy (Ha and Hoch 1989). This often occurs when a firm reacts to a crisis without a prior coordinated plan (Pearson and Mitroff 1993). Ambiguous evidence allows for multiple interpretations, whereas with unambiguous evidence, a unique consensus interpretation of the evidence is likely (Ha and Hoch 1989). When expectations are strong, ambiguous evidence is interpreted in a manner consistent with expectations (Cell 2, Figure 1), which leads to a cumulative effect of expectation and evidence similar to Cell 1 in Figure 1.

In contrast, when prior expectations are weak, belief change is driven primarily by evidence (Cell 5, Figure 1). Research in public relations as well as marketing suggests that consumers' baseline expectations of firm behavior in crises are stringent and that anything short of unambiguous support (complete apology and remedy) is considered inadequate (Hearit 1994; Susskind and Field 1996). Thus, an ambiguous response evaluated under weak prior expectations is expected to affect brand equity negatively. Combined with the effect predicted under strong expectations, an interaction of expectations and ambiguous firm response is expected relative to a no-crisis (expectations-only) situation.

H4: An ambiguous response following a product-harm crisis will lead to a smaller loss of brand equity when consumers' positive prior expectations are strong rather than weak.

Unambiguous Disconfirmation

Consumers' confirmatory tendencies are thwarted when the evidence unambiguously disconfirms expectations. The inconsistency of strong prior expectations and evidence creates a dilemma. Ultimately, this dilemma tends to be resolved by discounting the evidence rather than updating expectations (Olson and Dover 1979; Ross and Lepper 1980; Smith 1993). Olson and Dover (1979) reported a study in which subjects were preexposed to advertising claiming a coffee was not bitter and were then asked to taste and rate a (very bitter) coffee that was brewed with 50% more coffee than usual. Experimental subjects rated the bitter coffee as marginally less bitter than control subjects who had not been exposed to advertising. Smith (1993) reported similar results on the discounting of disconfirmatory evidence based on advertising-induced expectations. In contrast, when prior expectations are weak, the updating of beliefs is based primarily on the evidence rather than expectations, as in Cell 6 in Figure 1. Consequently, we expect that

H5: An unambiguous stonewalling response following a product-harm crisis will lead to a smaller loss of brand equity when consumers' positive prior expectations are strong rather than weak.

Data from a field survey undertaken during a product-harm crisis and two laboratory experiments provide the basis for testing these hypotheses. We use the field survey (Study 1) to address H1 and H2, and we use the laboratory experiments (Studies 2 and 3) to test H3 through H5. Study 2 provides evidence of the predicted interactions using fictitious brands, and Study 3 generalizes these findings using real brands and addresses follow-up issues raised by Study 2.

Study 1

The objective of Study 1 is to establish whether and how selective information processing operates in a crisis context. The occurrence of selective processing would provide a rationale for applying the theoretical framework and testing the specific interactions of expectations and evidence. In this study, we focus on understanding effects on postcrisis purchase intentions, and in subsequent studies, we examine the broader construct of brand equity.

Data

Data were collected from a national probability sample (screened for recent coffee purchase) through telephone interviews by a market research firm during a product-harm crisis (i.e., during the week in which news of the product-harm crisis and firm response unfolded in the media). The trigger event for the product-harm crisis was the discovery of fragments of glass in canisters of instant coffee of one of the dominant brands in a large European market. The sample consisted of 218 instant coffee buyers who had purchased one of the two brands during the previous two months. We use previous purchase as a proxy for the nature of consumers' expectations of a brand. There were 178 usable responses, composed of 49% regular Brand A purchasers (including 31 consumers who also purchased Brand B). Almost half the sample (48.2%) was more than 54 years of age, 16% between 45 and 54 years of age, 19.7% between 35 and 44 years of age, 10.6% between 25 and 34 years of age, and 5.5% below the age of 25. The sample was 42.6% male.

After identification of the respondents as instant coffee purchasers and determination of the brand they purchased regularly, respondents were asked if they had recently seen or heard anything about instant coffee in the newspapers, on television, or on the radio. If they had, they were asked to identify the brand and what they had heard. If they correctly identified the brand and the issue, they were classified as being spontaneously aware of the product-harm crisis. All respondents were then informed of the crisis event and were asked about their perception of the risk from the affected product (1 = no risk at all, 5 = extremely serious risk). Respondents were then informed of the firm's response to the crisis (recall of all canisters of the product followed by reintroduction in a newly labeled package). They were then asked whether, in their opinion, the firm acted responsibly in dealing with the situation (1 = not at all responsibly, 5 = very responsibly). Finally, intentions to purchase the brand in the future were measured (1 = definitely will not buy, 5 = definitely will buy).

Analysis and Results

To preserve confidentiality, the firm whose brand was the subject of the crisis is referred to as Firm A and its brand as Brand A, and the other large brand in the market is referred to as Brand B. H1 predicts that purchasers of Brand A, who presumably had stronger positive expectations of Firm A than did purchasers of competing brands, would be more likely to be aware of the crisis event than purchasers of Brand B. As expected, a larger proportion of purchasers of Brand A than of Brand B were spontaneously aware of the crisis event (39% versus 16%; χ2 = 14.5, p < .001).

H2 predicts that purchasers of Brand A and purchasers of Brand B would be influenced by different types of information in the formation of their postcrisis intentions to purchase Brand A. Two regressions, one for purchasers of Brand A and one for purchasers of Brand B, were run to analyze the influence of risk perceptions and perception of firm response in predicting postcrisis intentions to purchase. The results show that for purchasers of Brand A, perceptions of responsible firm behavior predict postcrisis intentions to purchase (β = .41, t87 = 13.81, p < .001), whereas perceptions of risk do not (β = −.08, t87 = −1.99, p > .16). In contrast, for purchasers of Brand B, perceptions of risk are related to future intentions to purchase (β = −.28, t91 = −9.15, p < .01), whereas perceptions of responsible firm behavior appear unimportant (β = .11, t91 = .41, p > .52). For the regression using data from Brand A purchasers, model R2 is .16, whereas for Brand B purchasers, the model R2 is .10. Purchasers of the two brands did not differ significantly on the absolute level of perceptions of responsibility (means: 4.15 versus 4.21 for Brand A and Brand B, respectively; Z = .42, p > .34) and perceptions of risk (means: 2.51 versus 2.32 for Brand A and Brand B, respectively; Z = 1.13, p > .12), whereas they did differ in their intention to purchase (means: 4.47 versus 3.28 for Brand A and Brand B, respectively; Z = 8.15, p < .01).

Discussion

The field survey results provide support for H1 and H2, corroborating the occurrence of selective attention and differential weighting of crisis-related information by segments of consumers with differing prior expectations. This selective processing appears to affect intentions to purchase. The study suggests that purchasers of a crisis brand are more likely to be aware of the crisis than are purchasers of other brands and that these two groups of consumers place different weights on aspects of information in their intentions to purchase the affected brand. Specifically, purchasers of the crisis brand are more sensitive to firm response than to the risk inherent in the defective product. Purchasers of other brands appear to focus on product risk perceptions more than on firm response to the crisis.

Study 1 helps establish the basis for expecting interactions between prior expectations and different types of firm response. It also validates the link between firm response and intention to purchase, a key component of brand equity. However, a limitation of the study is that prior expectations were measured using a proxy rather than manipulated, and firm response was constant rather than varied. The use of previous purchase as a proxy potentially confounds different antecedents of selective information processing, which makes it impossible to determine whether it is expectations- or dissonance-driven. Although the study establishes the relevance of selective information processing to the product-harm crisis phenomenon, a more controlled research setting is necessary to test the complex predictions about the interaction of expectations and firm response. Two laboratory experiments were conducted to test H3 through H5.

Study 2

In Study 2, both consumers' expectations and firm response are experimentally manipulated. The stimuli— including the use of fictitious brand names—ensure that, unlike in Study 1, prior purchase and therefore cognitive dissonance cannot account for the results. A cognitive dissonance explanation would suggest that subjects attempt to render their cognitions consistent with their own previous behavior. Although both the cognitive dissonance–based and expectations-based explanations imply selective information processing, the expectations–evidence framework does not require prior brand purchase. The use of a fictitious brand in Study 2 enables us to test whether the expectations-based explanation holds.

Independent Variables

A 2 (consumer expectations) × 3 (firm response) factorial between-subjects design, with control conditions, was used to test the hypotheses. Prior expectations were manipulated by informing subjects in cover story instructions as well as in an excerpt from a newspaper article that the firm (1) was “highly reputable and successful” in its home market, with a “spotless record of excellent products for over 30 years,” and had “won an award from consumers the previous year” (strong positive expectations condition) or (2) had “sold products in its home market for over 30 years” (weak expectations condition).

The three levels of firm response were (1) unambiguous support, which consisted of an apology, product recall, and restitution announced in a full-page newspaper advertisement; (2) ambiguous response, which consisted of a notice from the firm to consumers announcing the product defect but not offering an apology, product recall, or restitution, also in the form of a full-page advertisement; or (3) unambiguous stonewalling, operationalized by providing a second newspaper article (in lieu of the advertisement in the other two conditions), which described the absence of any form of response or remedial measures from the firm “despite repeated attempts” by the newspaper to elicit comment. In the control conditions, subjects read the same description of the firm used to generate expectations and a neutral newspaper article.

In prior marketing studies of the expectations–evidence framework, advertising may have been dominated by evidence for two reasons: (1) Product trial usually involves many more senses and is more compelling than advertising, and (2) information from advertisements is discounted because advertising is perceived to be a partisan source (Smith 1993). The use of a crisis setting and the stimuli described here alleviate these problems.

Dependent Variables

The dependent measures consist of multiple-item scales tapping dimensions of brand equity, which have been used in previous research (Aaker 1991; Agarwal and Rao 1996; Keller 1993). Brand attitude was measured on three seven-point scales (unfavorable–favorable, bad–good, and negative–positive), brand trust on three seven-point scales (not at all trustworthy–very trustworthy, not at all dependable–very dependable, and not at all reliable–very reliable), perceived quality on two seven-point scales tapping overall quality of the brand and overall quality of the product (low quality–high quality), and purchase likelihood and brand desirability on seven-point scales (not at all likely–very likely, not at all desirable–very desirable). In addition to the dependent measures, subjects in the experimental conditions responded to questions to ensure that experimental manipulations were effective.

Stimulus Materials, Subjects, and Procedure

A fictitious soft drink, Vesuvio, was used as the stimulus brand in all conditions. The trigger event for the product-harm crisis consisted of newspaper reports of cans of Vesuvio that were rusted on the inside. Subsequent information identified the cause of the problem as external—some retailers were selling old stocks of the product. The reported setting of the crisis was a different city than the one in which the study was conducted (to ensure plausibility of the fictitious brand name and crisis story), and subjects were instructed as part of the cover story for the experiment that the brand would soon be introduced in their city.

Subjects were 195 undergraduate students enrolled in business courses, who participated in the study for course credit. Participants were asked to read the stimulus material carefully (newspaper articles and advertisement) and respond to the questions in the booklet. They were then debriefed and excused. Questionnaires were administered in classroom sessions, all experimental and control conditions were run in each session, and subjects were assigned randomly to a condition.

Analysis and Results

Manipulation checks

Subjects who incorrectly identified the source of the problem on a multiple-choice question were omitted from the analysis, which left an effective sample of 171. Subjects in all six experimental (excluding control) conditions did not differ in their assessment of the seriousness of the problem (means from 5.32 to 5.95 on a seven-point scale, where 7 = very serious; F5, 134 = 1.02, p > .40), which suggests that the crisis event was successfully manipulated. A check for the manipulation of expectations was not included in the experimental questionnaire for two reasons: (1) It would be reactive, and (2) it could be contaminated by the firm response manipulation. Instead, a pretest of the expectations manipulation on 29 subjects from the same pool indicated significant differences in perceptions of how concerned about customers the firm was (means: 3.47 for the weak expectations manipulation versus 4.54 for the strong expectations on a seven-point scale, where 7 = very concerned about customers; F1, 28 = 10.02, p < .01). As discussed previously, ambiguous information allows for multiple interpretations, whereas unambiguous information yields a consensus interpretation. As a check on the firm response manipulation, subjects were asked whether, in their opinion, the firm had apologized. In the unambiguous support conditions, 49 of 54 (91%) subjects indicated that, in their opinion, the firm had apologized. In the ambiguous response conditions, opinion was divided: 29 of 51 (57%) subjects indicated that, in their opinion, the firm had apologized. In the stonewalling conditions, 8 of 36 subjects believed the firm had apologized (22%).

Dependent variable

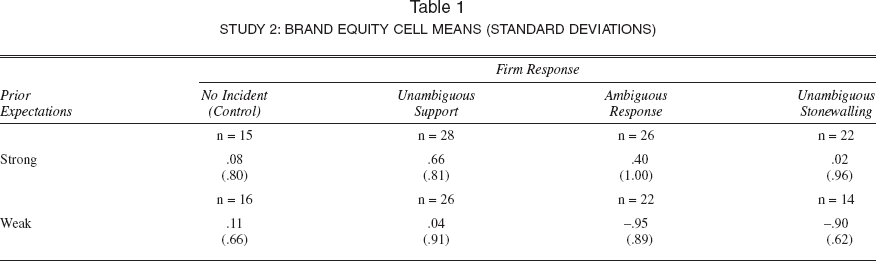

A reliability analysis on the ten items of the brand equity scale indicated that Cronbach's α = .94. A factor analysis on the ten measures yielded a single factor, which accounted for 69% of the variance. The linear combination represented by this factor was used as the dependent measure representing brand equity in hypothesis tests. 2 Data were analyzed in a between-subjects analysis of variance (ANOVA) with planned contrasts applied to test specific hypotheses. We present the results in Table 1.

Factor scores rather than a simple average were used to extract common variance due to the underlying brand equity construct and to eliminate the redundancy created by multiple measures of the same component of brand equity by weighting variables in proportion to their correlation to the overall factor.

STUDY 2: BRAND EQUITY CELL MEANS (STANDARD DEVIATIONS)

Hypothesis tests

H3 predicts that the loss of brand equity relative to a no-crisis control will be smaller with an unambiguous support response when expectations are strong than when they are weak. The predicted interaction is marginally significant (F1, 81 = 3.09, p < .09). Planned contrasts reveal a significant positive main effect of unambiguous support under strong expectations relative to a no-crisis control (means .66 versus .08; F1, 41 = 4.96, p < .03) and no main effect when expectations are weak (means .04 versus .11; F1, 40 = .08, p > .70). Furthermore, a comparison of the mean brand equity under the strong and weak expectations conditions with identical unambiguous support responses reveals a significant main effect (means .04 versus .66; F1, 52 = 6.94, p < .01), which shows that strong positive expectations lead to higher brand equity. Overall, we find moderate support for H3.

H4 predicts that prior expectations moderate an ambiguous response. The predicted interaction is significant (F1, 75 = 11.8, p < .01). Likewise, the main effect of expectations is significant (means .28 versus −.50; F1, 75 = 10.8, p < .01), and the main effect of firm response is marginally significant (means .09 versus −.22; F1, 75 = 3.35, p < .08). Planned contrasts comparing ambiguous response with the no-crisis control show that an ambiguous response under weak expectations has a significantly negative effect on brand equity (means .11 versus −.95; F1, 36 = 16.15, p < .001). Furthermore, it was suggested that the effects of an ambiguous response and an unambiguous response would be similar under strong positive expectations. Contrasts reveal that brand equity is no different in the two response conditions (means .40 versus .66, F1, 52 = 1.06, p > .30). H4 is supported.

H5 suggests that the negative effect of stonewalling on brand equity is less pronounced for consumers with strong positive prior expectations than for those with weak prior expectations. The predicted interaction is significant (F1, 63 = 5.88, p < .02). The main effects of firm response and consumer expectations are also significant (means .09 versus −.38; F1, 63 = 7.35, p < .01; and means .04 versus −.36; F1, 63 = 5.15, p < .03, respectively). H5 is supported.

Discussion

Broadly, these results show that consumer expectations moderate the impact of firm response on brand equity, regardless of the type of firm response. The details of the results reveal interesting patterns. The weak expectations conditions provide an indication of the baseline impact of the product-harm crisis. This impact is severely negative in both the stonewalling and ambiguous response cases. In contrast, under unambiguous support with equally weak expectations, there is no decline in brand equity.

A surprising result was that strong expectations combined with unambiguous support to increase brand equity relative to a no-crisis control situation. This effect is likely due to a calibration of the stimuli. Expectations were based on information provided in the experimental setting and may therefore have been more malleable than for existing brands. In addition, by accepting responsibility for something that was not directly its fault, the firm may have been seen as acting altruistically. Yet the result is interesting for two reasons. First, it provides evidence that, at least conceptually, precrisis levels are not an upper limit for changes in brand equity in a crisis situation. Second, the effect is part of an interaction of expectations and unambiguous evidence, which has previously been difficult to establish in marketing settings.

In the ambiguous response case, the interaction of prior expectations and firm response is strongest. When expectations are strong, the effect on brand equity resembles the unambiguous support case. When expectations are weak, it is indistinguishable from the stonewalling case. It is this interaction that has most often been reported in prior advertising evidence studies. Its occurrence in the crisis setting suggests that the theory is valid in other domains. Finally, in the stonewalling condition, the dilemma arising from a disconfirmation of expectations appears to have been resolved by the use of a combination of the two sources of information (expectations and evidence). This suggests that as predicted, even unambiguous stonewalling was somewhat discounted under favorable prior expectations.

In this study, the use of fictitious stimuli allowed a level of control that would have been impossible had we used real brands. For example, as is evident from the lack of difference between the brand equity measures for the two expectations control conditions, we were able to manipulate expectations independently of prior brand equity. Furthermore, because the study was concerned with changes in brand equity rather than absolute levels of brand equity, the absence of prior brand equity enables us to ascribe any changes more confidently to the effects of our manipulations rather than to the interactions of our manipulations with previous knowledge. In addition, on the basis of these results, we can claim more confidently that the selective information processing effects observed in Study 1 were driven by expectations rather than dissonance.

Nevertheless, the control achieved in Study 2 has a cost. Experimentally manipulated expectations are unlikely to have the depth or strength of expectations of real brand schemas, and the notion of brand equity for a brand that subjects encounter for the first time in the laboratory setting may be limited. Furthermore, Study 2 used a different format of information presentation (a newspaper article) in the stonewalling condition versus the other two conditions (advertisements). Although no comparisons were made between the stonewalling condition and other response conditions, the potential confounding could be removed and external validity enhanced by employing comparable information presentation formats. To overcome these limitations and examine the robustness of the findings, we conducted Study 3 using real brand names, a different product category, a different crisis event, and a uniform set of information presentation formats.

Study 3

The objective of Study 3 is to extend Study 2 using previously known brands as stimuli and a uniform information presentation format across firm response conditions. In addition, whereas in Study 2 the crisis locus was external across conditions, in Study 3 it was internal. Attribution theory predicts that consumers' attitudes are more likely to be negatively affected when the crisis event is perceived to be internal and controllable by the firm than when it is external and uncontrollable (Weiner 1986).

Independent and Dependent Variables

The experimental design was identical to that of Study 2, except that prior expectations were manipulated by using different brands (of laptop computers), firm response was reported to subjects in the form of a newspaper article in all conditions, and in the control condition, subjects were simply asked to rate the brand on the dependent measures. The stimulus brands were selected on the basis of a pretest (n = 64 drawn from the same population as the main study) that measured the extent to which the brands were concerned about customers (this question was used as a check of the expectations manipulation in Study 2). An additional manipulation check measure indicated subjects' perceptions of the sufficiency of the firm's response, and a measure of subjects' familiarity with brands of laptop computers was obtained (1 = not at all familiar, 7 = very familiar) for use as a covariate.

Stimulus Materials, Subjects, and Procedure

Laptop computers were chosen as the product category because of the interest and familiarity of the subject population. A pretest showed that of 64 subjects from the same pool as the main study, 63 owned either a laptop or a desktop computer (99% computer ownership and 66% laptop ownership), their mean familiarity with computers was 5.37 (7 = very familiar), and all subjects rated their familiarity above 3. On the basis of this pretest, Compaq and Zeos were chosen to represent the strong and weak expectations brands, respectively (mean of 5.15 for Compaq versus 3.17 for Zeos on a seven-point scale, where 7 = very concerned about customers; t47 = 8.5, p < .001). The trigger event for the product-harm crisis consisted of newspaper reports of exploding laptops, which caused hand and face injuries. Subjects were 175 undergraduate business students, who participated voluntarily in the study. Procedures were identical to those used in Study 2. A one-to-one debriefing of a subsample of 20 subjects (drawn from different experimental conditions) showed that there was no evidence of demand effects.

Analysis and Results

Manipulation checks

Subjects who incorrectly identified the source of the crisis event or failed to respond to the dependent measures were omitted from the analysis, which left an effective sample of 164. Subjects in the experimental conditions did not differ in their assessment of the seriousness of the problem (means from 6.22 to 6.59 on a seven-point scale, where 7 = very serious; F5, 117 = .258, p > .93), which suggests that the crisis event was successfully manipulated. As a check on the firm response manipulation, subjects were asked whether, in their opinion, the firm had apologized. In the unambiguous support conditions, 37 of 42 (88%) subjects indicated that it had. In the ambiguous response conditions, the comparable number was 12 of 41 (29%), and in the stonewalling conditions, 39 of 40 subjects believed the firm had not apologized (98%). The continuous (seven-point) scale of perceptions of the sufficiency of the firm's response (not at all sufficient–quite sufficient) also indicated that the manipulation was successful: Means were 4.95, 3.09, and 1.79 in the unambiguous support, ambiguous, and stonewalling conditions, respectively. Paired t-tests are significant at p < .05.

Dependent variable

A reliability analysis on the ten items of the brand equity scale indicated that Cronbach's α = .98. A factor analysis on the ten brand equity measures yielded a single factor, which accounted for 88% of the variance and formed the dependent measure representing brand equity in hypothesis tests. We applied ANOVA with planned contrasts to test specific hypotheses. We present the results in Table 2.

STUDY 3: BRAND EQUITY CELL MEANS (STANDARD DEVIATIONS)

Hypothesis tests

H3 predicts that the loss of brand equity relative to a no-crisis control will be smaller with an unambiguous support response when expectations are strong than when they are weak. The predicted interaction is marginally significant (F1, 79 = 3.02, p < .09). There is no loss of brand equity when expectations are strong (means .85 versus .69; F1, 40 = .49, p > .45), and there is a strong negative effect when expectations are weak (means −.06 versus −.80; F1, 39 = 10.21, p < .01). Overall, as in Study 2, we find moderate support for H3.

H4 predicts that prior expectations moderate an ambiguous response. The predicted interaction is significant (F1, 78 = 4.02, p < .05), as are the main effects of expectations (means .74 versus −.49; F1, 78 = 55.4, p < .01) and firm response (means .40 versus −.09; F1, 78 10.62, p < .01). A planned contrast comparing ambiguous response with the no-crisis control shows a significantly negative effect on brand equity (means −.06 versus −.94; F1, 37 = 15.62, p < .01) under weak expectations. Finally, the effects of an ambiguous and unambiguous response on brand equity are similar under strong positive expectations (means .69 versus .64; F1, 41 = .09, p > .76). H4 is supported.

H5 suggests that the negative effect of stonewalling will be less pronounced under strong versus weak prior expectations. The interaction is significant (F1, 77 = 4.12, p < .05). Planned contrasts comparing a stonewalling response with the no-crisis control show a significantly negative effect on brand equity when expectations are weak (means −.06 versus −1.20; F1,35 = 26, p < .01) and no significant effect when expectations are strong (means .85 versus .43; F 1,42 = 2.65, p > .11). H5 is supported. 3

Subjects' familiarity with notebook computers was measured and used as a covariate. The results indicate that this covariate is significant only in the analysis associated with H5 (F1, 75 = 2.87, p < .10), and the remaining results are essentially similar to those reported in the text, except that the predicted interaction is significant at p < .07 rather than p < .05. Familiarity with notebook computers rather than familiarity with the two specific brands was used, because brand familiarity and expectations are likely to be correlated. Extracting variance due to brand familiarity could have attenuated expectation-based effects.

Discussion

Study 3 provides strong support for H3 through H5. As in Study 2, we find that prior expectations and new evidence interact in all conditions, and the effect is stronger in the case of unambiguous disconfirming and ambiguous evidence than with unambiguous confirming evidence. Unlike in Study 2, unambiguous support following the crisis did not lead to higher brand equity than the control conditions for brands when there were strong prior expectations, perhaps because of the different locus of responsibility for the crisis or the use of real versus fictitious brands.

General Discussion

The results from the comprehensive set of expectations and firm response conditions examined here resolve the disparity in the previous literature on the interaction of expectations with unambiguous evidence and provide theoretical and managerial implications related to the impact of corporate actions on brand equity. Simultaneously, the studies illustrate the generalizability of the expectations–evidence framework and illuminate the previously underresearched areas of the marketing impact of crises and the impact of corporate actions on brand equity.

From the perspective of the expectations–evidence literature, the findings lend weight to the methodological explanation for the previously inconclusive results on the interaction of expectations and confirmatory evidence. By removing the ceiling effect, the interaction is detected in both Studies 2 and 3. Furthermore, interactions from previous research are replicated in the ambiguous response and disconfirmation (stonewalling) cases. In summary, there appears to be no theoretical reason to limit the prediction of an interaction to ambiguous evidence conditions.

From a managerial perspective, the result that consumers' interpretation of the evidence of firm response is moderated by their prior expectations about the firm indicates that an identical response can have dramatically different effects on brand equity, depending on consumers' prior expectations about the firm. In other words, in developing an understanding of the impact of corporate actions on brand equity, firm actions alone are unlikely to be sufficient to predict the effects of product-harm crises on brand equity; consumers' prior expectations are a key moderator. The selective processing results also indicate that different consumer segments (e.g., loyal customers versus potential customers) may attend to different types of information in a product-harm crisis. This implies benefits from tailoring crisis communications to different audiences. For example, Study 1 results indicate that existing customers need reassurance about the firm's responsiveness, whereas potential future consumers of the crisis brand need to be reassured about the absence of risk in consuming the product. Tracking studies that monitor consumers' evolving perceptions in a crisis may provide valuable data in tailoring communications. From the perspective of protecting brand equity, it is important to remember that a crisis, by definition, generates substantial brand awareness. Therefore, it may be judicious to focus on limiting damage to brand associations (Smith, Thomas, and Quelch 1996).

Consumers' existing positive expectations may provide firms with a form of insurance against the potentially devastating impact of crises. For these firms, brand equity appears to be remarkably resilient to different types of firm response and less fragile than initially expected. Conversely, firms with weak consumer expectations may have to undertake aggressive support for their brands simply to preserve brand equity. Indeed, any ambivalence in their response is likely to be devastating.

Limitations and Further Research

It is important to note that Study 2 and Study 3 provide complementary tests of H3–H5. Study 2 provides a controlled setting in which expectations were manipulated independently of brand equity but at the cost of external validity. Study 3 solves this problem, but taken alone, its results can be attributed to the interaction of prior brand knowledge and the experimental manipulations. Together, however, the two studies provide internally and externally valid evidence. Yet other limitations remain. For example, a product-harm crisis is a phenomenon that involves marketplace dynamics such as word of mouth and rumors, which are difficult to replicate in a laboratory setting, though care was taken to make the stimuli as realistic as was feasible. Marketplace dynamics, such as spontaneous information sharing among consumers and competitive activity, could magnify or attenuate the individual-level effects reported here.

A complementary approach to understanding the results of this study is to model consumers as Bayesian decision makers who update their beliefs about brand equity in the context of their prior beliefs and new evidence of firm behavior in a crisis context. 4 When people are uncertain about some characteristics—for example, brand equity—we may represent their beliefs with a distribution of values representing the belief. The greater the uncertainty about the characteristics, the greater is the variance of the distribution. People use evidence from their environment to update their prior beliefs, and a new, posterior distribution replaces the prior. According to Bayesian updating models, the posterior distribution will resemble the new evidence more when the variance is high (i.e., a person's prior beliefs are weakly held) than when it is low (Lee 1989). Unfortunately, we did not measure the degree of confidence with which people hold beliefs (i.e., brand equity) and are therefore unable to make clear inferences about the distribution of individual perceptions of brand equity. However, insofar as the mean of that distribution is sufficient to describe the prior, our results are consistent with the Bayesian explanation. Specifically, they show that when expectations are strong, the posterior distribution (or more accurately, the mean) reflects the prior more closely than when expectations are weak. Further research would benefit from integrating measures such as belief certainty to examine the Bayesian updating predictions as a complement to the more cognitive process–oriented selective information weighting explanation.

We thank an anonymous reviewer for this insight.

The locus of control for the crisis event was external to the firm in Study 2 and internal to the firm in Study 3. Nevertheless, the key interactions in the two studies are similar. A post hoc analysis of the different components of brand equity indicates that purchase intentions are less sensitive to the interactions predicted here than to the knowledge and favorability components. These findings suggest the need for further research, beginning with the search for a background factor that may moderate the effects.

This research has examined firm response and its interaction with prior expectations. Several other factors that may affect brand equity were kept constant and require further investigation. These include the timing of the response (immediate versus delayed), the locus of fault (internal versus external), the nature of the crisis (acute versus chronic), the forced nature of the firm's response (voluntary versus legislated), and the impact of third-party interventions (e.g., independent expert testimonials during a crisis), as well as the differential effects of the components of firm response (e.g., product recall versus free replacement). Furthermore, given our interest in brand equity, our research examined only the impact on consumers' perceptions. Other stakeholders may also be affected and may directly or indirectly affect brand equity. For example, perceptions of the victims, the media, the trade, suppliers, investors, and regulatory authorities are likely to be vital in determining the overall impact of a product-harm crisis on brand equity. This phenomenon deserves further research attention in marketing.