Abstract

This article examines the implications of interfirm cooperation for a firm's level of customer orientation. Drawing on research in marketing, organizational theory, and economics, the authors suggest that firms engaged in cooperative alliances with competitors will become less customer oriented over time. Using longitudinal survey data, the authors find that firms in alliances dominated by competitors experience a significant decrease in their level of customer orientation. In contrast, the authors do not observe this type of decrease for firms in alliances dominated by channel members. Moreover, the authors find that both behavioral and structural mechanisms influence the relationship between alliance type and customer orientation. Behaviorally, firms in competitor-dominated alliances with weak relational ties with their collaborators exhibit a greater decrease in customer orientation compared with firms with strong ties with their collaborators. Structurally, firms that collaborate with competitors in alliances with a third-party monitor, such as a government agency, experience a smaller decrease in customer orientation than firms in alliances without such a monitor.

Over the past two decades, interfirm cooperation has emerged as a significant area of managerial practice and academic inquiry. In the realm of practice, cooperative inter-firm relations have been successfully employed in both vertical relations (between channel members) and horizontal relations (between competitors) as a means of gaining access to new knowledge and of reducing the costs and risks associated with developing new products and processes (Brandenburger and Nalebuff 1996; Millson, Raj, and Wilemon 1996). In the realm of inquiry, marketing scholars have investigated several aspects of these cooperative relations, including their antecedents (e.g., Anderson and Weitz 1989; Heide and Miner 1992), key success factors (e.g., Bucklin and Sengupta 1993; Morgan and Hunt 1994), resource-commitment decisions (Amaldoss et al. 2000), and new product-related outcomes (e.g., Rindfleisch and Moorman 2001; Sivadas and Dwyer 2000).

Although this literature has produced a considerable amount of knowledge about the precursors, facilitators, and outcomes of cooperative interfirm relations, the knowledge is largely centered on outcomes tied directly to either the relationship itself or the firms within it. Thus, relatively little is known about the effect of these relations on the broader marketing environment, including their impact on a firm's customers. This is a notable issue because scholars and public policy officials posit that though cooperative interfirm relations may be beneficial to participating firms, they may be harmful to their customers (e.g., Sakakibara 1997; Wright 1986).

Concerns about the possible anticompetitive effect of interfirm cooperation have been voiced for well over a century, as historical incidents have shown that collaboration can readily lead to anticompetitive practices. For example, Lamoreaux (1985) documents how collaboration in the copper, whiskey, rubber, oatmeal, cotton, and sugar industries led to wide-ranging collusion and harm to customers in the form of restricted production and high prices during much of the nineteenth century. As Adam Smith (1930, p. 130) noted more than two centuries ago, “People of the same trade seldom meet together, even for merriment and diversion, but the conversation ends in a conspiracy against the public.”

Although this type of blatant collusive activity has been constrained by modern antitrust regulation since the early twentieth century, the risks associated with collaboration have risen sharply over the past 20 years after the passage of the National Cooperative Research Act of 1984 (NCRA) and the National Cooperative Research and Production Act of 1993 (NCRPA; codified together at 15 U.S.C. §§ 4301– 4306). These acts opened the door for increased interfirm cooperation by reducing the threat of antitrust prosecution. In response, economists and legal scholars have taken renewed interest in the possible anticompetitive effects of interfirm cooperation (e.g., Petit and Tolwinski 1999; Wright 1986). Despite this interest, empirical research on the impact of collaborative activities on customers is scant at best (for exceptions, see Scott 1988; Vontoras 1997).

In this article, we attempt to address this gap by examining the effect of interfirm cooperation on a firm's level of customer orientation. Our definition of customer orientation bridges the two views offered in the literature. Specifically, we define customer orientation as the set of behaviors and beliefs that places a priority on customers' interests and continuously creates superior customer value (Deshpandé, Farley, and Webster 1993, p. 27; Narver and Slater 1990, p. 21). Thus, interfirm cooperation may directly affect firm behaviors, such as the extent to which marketing practices (e.g., price) reflect market-based considerations. In addition, interfirm cooperation may have more subtle effects on a firm's culture or belief systems, such as the degree to which the firm prioritizes customers in its decision making. The latter effects are longer term and may be more difficult to detect, but they have been found to be crucial to a firm's customer orientation (Deshpandé, Farley, and Webster 1993).

Although alliances can be formed for many purposes, our study focuses on alliances formed to conduct joint research and development (R&D) and/or to commercialize new products and processes. Thus, following previous research (Rindfleisch and Moorman 2001), we adopt the term new product alliances, which we define as formal collaborative arrangements among two or more firms to conduct these activities.

We offer a longitudinal examination of the effect of vertical (i.e., channel dominated) and horizontal (i.e., competitor dominated) new product alliances on changes in a firm's level of customer orientation over time. 1 We hypothesize that firms in competitor-dominated alliances have greater difficulty maintaining a strong customer orientation than firms in channel-dominated alliances because of overlapping knowledge, low levels of mutual trust, and a tendency to collude. In addition, we investigate two mechanisms for minimizing this deleterious effect of competitor-dominated alliances on customer orientation. Specifically, we suggest that firms in competitor-dominated alliances can maintain a strong customer orientation by altering either the structure of their alliance or their behavior with their collaborators. Thus, our research provides not only an examination of the relationship between interfirm cooperation and customer orientation but also an investigation of potential remedies for maintaining a strong customer orientation for firms that cooperate with competitors.

In contrast to dyadic alliances (i.e., buyer–seller partnerships), the alliances in our study typically include more than two members. Thus, we employ the terms “competitor-dominated” for alliances mainly populated by competitors and “channel-dominated” for alliances mainly populated by channel members.

From our review of the literature, we believe this study represents the first longitudinal investigation of how inter-firm cooperation affects changes in a firm's level of customer orientation over time. Thus, this research provides a first exploration of the determinants of the evolution of a firm's customer orientation, and it offers insights for marketing scholars and practitioners interested in interorganizational relations or customer orientation.

An Overview of the Effect of Interfirm Cooperation on Customers

Traditional marketing strategy depicts firms as engaged in a zero-sum game in which cooperation is both infrequent and undesirable (Arndt 1979). Over the past two decades, this traditional economic-based view has given way to a relational perspective that suggests that interfirm cooperation is both frequent and desirable (Dwyer, Schurr, and Oh 1987). However, even relational marketing scholars seem to operate under a metabelief that interfirm cooperation may lead to negative consequences. For example, although Hunt and Morgan (1995, p. 2) recognize the benefits of interfirm cooperation, they also acknowledge that “[e]conomies premised on competing firms are far superior to economies premised on cooperating firms.” This acknowledgment is based on a fundamental premise of neoclassical economic theory: Cooperation interferes with efficient market processes.

This neoclassical view of the perils of interfirm cooperation has played a major role in the development of U.S. antitrust policy. For example, based on the premise that information sharing among current or potential rivals leads to anticompetitive collusive behavior, U.S. antitrust policy historically has tried to limit this type of collective behavior (Best 1990; Mowery 1998). Because of this stance, new product alliances are a recent phenomenon, following a relaxation in the U.S. Department of Justice's position on interfirm cooperation (Wright 1986). Given its phenomenological recency, the effect of new product alliances on customer-related outcomes has not received attention from either relationship marketing scholars or market orientation researchers.

Although the effect of interfirm cooperation on customers has received little attention in the marketing literature, economists and legal scholars have debated the issue for some time. Essentially, two divergent schools of thought frame these debates. 2 On the one side, advocates of interfirm cooperation argue that alliances, joint ventures, and other forms of collaboration are largely procompetitive because they help firms reduce risk, lower costs, and provide the opportunity for organizational learning through knowledge sharing (Best 1990; Teece 1992; Telser 1985). For example, Teece (1992) suggests that cooperation is necessary to promote competition because it helps firms gain access to important industry information. Similarly, other advocates suggest that interfirm cooperation enhances welfare by promoting collective innovation (e.g., Clarke 1983; Telser 1985).

Both schools of thought focus mainly on other forms of cooperation among horizontally related firms. However, these arguments also seem at least partially applicable to channel-dominated alliances, because vertically related firms may also engage in both anticompetitive activities, such as channel price fixing (e.g., Heil and Langvardt 1994), and procompetitive activities, such as developing innovative products and services (e.g., Sivadas and Dwyer 2000).

On the other side, detractors of interfirm cooperation argue that these collaborative activities may be anticompetitive because of the risks that the cooperation may lead to outcomes harmful to consumer welfare (Clarke 1983; Petit and Tolwinski 1999; Wright 1986). For example, Wright (1986) suggests that alliances among competitors may suffer from “overinclusiveness.” This argument asserts that a new product alliance of several competitors may use its collective research endeavor as a substitute for firm-level inhouse R&D and that this substitution will result in a net reduction in overall R&D and weakened incentives for independent innovative activity.

Although both viewpoints appear to have theoretical merit, neither side has much empirical evidence. The scant research conducted in this area only indirectly tackles the issue of how interfirm cooperation affects customers, because it is largely derived from econometric models that are based on macromarket indicants, such as industry price movements (e.g., Clarke 1983; Telser 1985). Thus, economic and legal research on the effects of interfirm cooperation on customers is thin in terms of empirical verification. To our knowledge, there are no longitudinal studies of this issue at the level of changes in individual firm behavior that use primary data sources. Our research attempts to address this limitation.

Conceptual Framework

Alliances and Customer Orientation

Our conceptualization of the effect of new product alliances on customer orientation draws insights from the market orientation literature and recent research on interfirm alliances in marketing, organizational theory, and economics. Collectively, the literature suggests that firms engaged in competitor-dominated alliances differ from firms in channel-dominated alliances in several notable ways. Specifically, firms in competitor-dominated alliances display higher levels of overlapping knowledge (e.g., McEvily and Zaheer 1999), lower levels of mutual trust (e.g., Rindfleisch 2000), and a stronger tendency for collusion (e.g., Petit and Tolwinski 1999) than do firms in channel-dominated alliances. We believe these differences have implications for an alliance member's ability and motivation to develop and maintain a strong customer orientation. In the aggregate, these differential profiles suggest that firms engaged in competitor-dominated alliances should experience a decrease in customer orientation over time, and firms engaged in channel-dominated alliances should not.

Degree of overlapping knowledge

Because of their shared location at a similar point in the value chain and membership in a common industry, firms in competitor-dominated alliances share a much higher level of overlapping knowledge about products and customers than do firms in channel-dominated alliances (McEvily and Zaheer 1999; Rindfleisch and Moorman 2001). There is good reason to believe that this high level of knowledge overlap may hamper firms' ability and motivation to acquire valuable information. Overlapping knowledge has been negatively related to a firm's ability to develop innovative solutions to customer needs. In the parlance of organizational learning scholars, exposure to redundant knowledge creates a bias in favor of knowledge exploitation by encouraging the use of existing skills and capabilities at the expense of knowledge exploration, which entails the development of novel skills and abilities (March 1991).

Organizational learning theorists argue that the inputs essential for knowledge exploration often lie outside a firm's industry (Garud 1994; Nonaka and Takeuchi 1995). For example, Garud (1994) suggests that firms that collaborate with organizations that have similar capabilities want to protect the status quo, and firms that collaborate with organizations that have dissimilar capabilities want to destroy existing know-how. Similarly, Scott (1988) and Vontoras (1997) suggest that participation in horizontal alliances has only a marginal impact on knowledge exploration, because these alliance participants tend to invest in existing lines of product development.

As a result of these influences, the infusion of novel information that is essential for developing and sustaining a strong customer orientation (Deshpandé, Farley, and Webster 1993; Kohli and Jaworksi 1990) is likely to attenuate among firms participating in competitor-dominated alliances. Over time, this attenuation is likely to hamper the ability of these firms to sustain a strong absorptive capacity (Cohen and Levinthal 1990), which is considered a critical aspect of a firm's ability to develop innovative customer solutions in the form of new product development. Specifically, lack of exposure to new information may atrophy a firm's capabilities to sense and respond to emerging customer needs. Without such a capability, firms will display a reduction in customer orientation.

In contrast, channel-dominated alliances tend to comprise firms from different industries and different points in the value chain and therefore have lower levels of knowledge overlap. Thus, firms in channel-dominated alliances are more likely to be exposed to new information that is essential for generating customer-focused innovation. Moreover, firms in channel alliances should also have greater access and understanding of the entire value chain, which is considered a critical input for developing and sustaining a customer orientation (Day and Wensley 1988; Narver and Slater 1990). Notably, channel alliances typically involve partners that are closer to the customer, thereby increasing the opportunity to access customer information. This proximity may also increase the benefit of using customer information, because it should improve relationships with channel members interacting more directly with customers.

Amount of mutual trust

Trust is widely regarded as an essential component for a firm's ability to succeed in interorganizational relationships (Moorman, Zaltman, and Deshpandé 1992; Morgan and Hunt 1994). Prior alliance research suggests that firms in competitor-dominated alliances display lower levels of mutual trust than firms in channel-dominated alliances (Bucklin and Sengupta 1993; Rindfleisch 2000). This weakened level of trust arises from firms in competitor-dominated alliances facing higher levels of opportunism (see Williamson 1985) and being fearful that their self-interested alliance partners will shirk their alliance investments and exploit the products of their collective endeavors. As Park and Russo (1996, p. 887) note, “cooperating with competitors is risky business … [because] the incentives to act opportunistically appear to motivate actions that threaten and frequently undermine joint ventures with them.” Likewise, Bucklin and Sengupta (1993, p. 33) warn that in horizontal alliances, “[t]he potential for opportunism is high as partners may use the alliance only as a means to gain market position at the expense of a partner.” Opportunism and mistrust have been shown to have a negative impact on the acquisition and utilization of information among exchange partners (Vontoras 1992). Consequently, mistrust's negative influence on the willingness of alliance participants to share and use information should diminish the ability of firms engaged in competitor-dominated alliances to sustain a strong customer orientation.

In addition to hampering the free flow of information, the fear of opportunism also increases the amount of resources firms need to expend in monitoring the behavior of their exchange partners (Williamson 1985). Faced with the reality of limited resources (Pfeffer and Salancik 1978), participants in these alliances may not be able to monitor customers sufficiently. Thus, because of mistrust in their alliance partners, firms in competitor-dominated alliances may find it difficult to make sufficient investments in the monitoring functions essential for sustaining a customer orientation over time. This view is supported by research indicating that trust reduces the need to monitor (Heide 1994; Heide and Miner 1992) and encourages risk-taking behavior among exchange partners (Moorman, Zaltman, and Deshpandé 1992; Morgan and Hunt 1994). In the absence of trust, partners are likely to be more conservative in making specific investments in an exchange relationship (Anderson and Weitz 1992). Following this logic, in contrast to competitor-dominated alliances, the higher levels of trust that characterize channel-dominated alliances should enhance a firm's willingness and ability to invest in and maintain a focus on customer needs.

Tendency for collusion

As is widely noted by neoclassical economists, firms that cooperate with competitors have strong motives to engage in collusive practices (Clarke 1983; Katz 1986; Petit and Tolwinski 1999). The dangers to consumer welfare from the collective setting of high prices or agreements to restrain production are the most widely acknowledged forms of collusive activity (Clarke 1983). As Katz (1986, p. 541) suggests, “a cooperative R&D arrangement might serve as a chance for [firms] to get together to discuss means of colluding in the product market.” The fear of price and production collusion in horizontal cooperation is a clear and present concern among critics of the NCRA (Petit and Tolwinski 1999; Scott 1991; Wright 1986). Thus, it is conceivable that firms in competitor-dominated alliances will exhibit a reduction in their focus on customers by substituting market-focused pricing strategies for collectively determined ones and/or by replacing demand-forecasted production for output established by collective agreement. This reduced customer focus is unlikely to occur for firms in channel-dominated alliances, because the members of the alliances occupy different points in the value chain and compete in different markets (Katz 1986). Thus, external competitive pressures should decrease the likelihood that firms in channel-dominated alliances engage in such practices.

In addition to these more explicit forms of collusive activity (i.e., prices and production), economists note that collusion comes in many other forms, including a reduction in collective innovation (Telser 1985; Wright 1986). As we noted previously, these economists suggest that firms in competitor-dominated alliances use their collective R&D activities as a substitute for individual-level R&D, and this substitution results in a decline in the diversity of innovation to the detriment of customers. In the long run, this type of decrease in firm-level R&D investment weakens a firm's absorptive capacity, as Cohen and Levinthal (1990) show. This leaves firms with less ability to sense and respond to market developments. As Cohen and Levinthal also note, firms that skimp on R&D investments often find themselves “locked out” of perceiving emerging market trends. In contrast, because of their greater variance in terms of products and technology (Scott 2000), firms that participate in channel-dominated alliances should be less likely to use collective R&D as a substitute (intentionally or otherwise) for in-house R&D activities.

Finally, collusive-type outcomes may arise in competitor-dominated alliances as a result of weakened cultural foundations and belief systems that underlie a customer orientation. Specifically, the very act of interacting with competitors in an ongoing cooperative manner may lessen a firm's degree of competitiveness. As Mandell (1995) notes, opponents of horizontal R&D cooperation fear that this type of weakening of competitive spirit is an unintended byproduct of such alliances. Consistent with this viewpoint, Mariti and Smiley (1983, p. 449) warn that “the cordial linkages that prevails between partners may preclude vigorous competition.” As several market orientation scholars note, having a strong focus on competitive threats (i.e., competitor orientation) is strongly correlated with having a strong focus on customers (Gatignon and Xuereb 1997; Narver and Slater 1990). This cultural shift toward a weakened competitive spirit is unlikely for firms in channel-dominated alliances, because their competitors do not populate their alliance.

In the aggregate, the economics literature on alliances suggests that firms engaged in competitor-dominated alliances are more likely than firms in channel-dominated alliances to engage in collusive activity. This shift in behaviors and/or culture (whether in the form of increased prices, restricted production, diminished investment in R&D, lower absorptive capacity, or weakened competitive focus) is likely to amount to a reduction in a firm's customer orientation by deemphasizing the market-sensing and customer-linking activities that are crucial to a firm's ability to sustain a market orientation (Day 1994; Moorman 1995).

Counterarguments

Although we believe the preceding arguments provide good reason to suspect that firms participating in competitor-dominated alliances have difficulty sustaining a strong customer orientation, there is little empirical research to provide strong substantiation for these claims. Thus, each of the arguments can be countered.

First, although the overlapping knowledge associated with competitive alliances may hurt customer orientation by restricting knowledge exploration, it also may enhance customer orientation by increasing a firm's capacity to absorb and apply information from alliance members in the short run (Mowery, Oxley, and Silverman 1996; Saxton 1997; Teece 1977). For example, Mowery, Oxley, and Silverman (1996) find that shared technological experience enhances the transfer of complex capabilities among alliance members. Similarly, Rindfleisch and Moorman (2001) show that the overlapping knowledge structures that characterize competitor-dominated alliances have a positive influence on the acquisition and utilization of novel information from partners. As previous research has shown, redundancy may also enable firms to find innovative ways to combine their knowledge (Madhavan and Grover 1998). Therefore, depending on the level of shared knowledge, firms in competitor-dominated alliances might experience an increase in customer orientation in terms of both the acquisition and the utilization of information.

Second, although a low degree of trust is unlikely to have any positive direct effects on the customer orientation of firms in competitor-dominated alliances, a lack of trust could indirectly help the firms maintain a focus on their customers. This indirect effect may arise because the fear of opportunistic exploitation should serve as a stumbling block to the development of explicit collusive arrangements to restrict production or increase prices. In effect, this view suggests that the lack of mutual trust and threat of opportunism should encourage firms in competitor-dominated alliances to keep their focus on meeting customer needs, because the threat of competition remains high. 3

Although a lack of mutual trust should make explicit collusion more difficult to enact, prior research has shown that mutually beneficial arrangements, such as price collusion, are feasible even under conditions in which trust is absent (Axelrod 1984).

Third, although it is possible that firms in competitor-dominated alliances may still seek to collude even under low-trust conditions (Burns 1936), explicit collusion seems unlikely for alliances filed with the U.S. Department of Justice (as the NCRA requires). None of the 800-plus alliances filed to date under the NCRA have been accused of this type of collusive activity. Therefore, at least in terms of price or production control, there is little evidence of explicit collusion in these alliances.

Finally, a counter to the idea that competitor-dominated alliances result in a decrease in R&D activity comes from research in the Schumpeterian tradition (Schumpeter 1942). This view suggests that firms in concentrated markets can more easily appropriate the returns from innovative activity, which may create an incentive to increase investments in R&D. Translating to alliances, this view implies that cooperative relationships among competitors should actually stimulate, not decrease, R&D investments. However, as Cohen and Levin (1989) review, empirical support for the relationship between industry concentration and R&D investment is quite mixed. Thus, the implications of this Schumpeterian perspective for positive customer-related outcomes from competitive-dominated alliances are questionable.

Summary

Although the three characteristics provide mixed arguments about the relationship between alliance type and customer orientation, we believe the collective weight of these arguments suggests that competitor-dominated alliances should have a negative effect and that channel-dominated alliances should have little influence on customer orientation over time. Thus, we hypothesize the following:

H1: Firms that cooperate in competitor-dominated alliances experience a reduction in their level of customer orientation over time, and firms that cooperate in channel-dominated alliances experience a stable level of customer orientation over time.

Mechanisms Influencing the Negative Impact of Competitor-Dominated Alliances

Although we predict that competitor-dominated alliances will have a detrimental effect on a firm's customer focus, this relationship may be influenced by various mechanisms. We examine two. First, competitor-dominated alliances may erect structural mechanisms, such as the involvement of a neutral third party, to monitor their behavior and mediate disagreements (Scott 2000). Second, competitor-dominated alliances may provide additional behavioral mechanisms in the form of higher levels of relational ties, which may influence the outcomes of the alliances (e.g., Axelrod 1984; Heide and Miner 1992; Rindfleisch and Moorman 2001). Our focus on structural and behavioral mechanisms is congruent with prior research on interfirm cooperation that suggests that cooperation is a by-product of both mechanisms (e.g., Gulati 1998; Smith, Carroll, and Ashford 1995). We offer hypotheses about the expected effects of each mechanism. Note that because we expect that channel-dominated alliances will not reduce a firm's level of customer orientation, we examine these mechanisms for only competitor-dominated alliances.

Third-party monitor

As we noted previously, competitor-dominated alliances are generally believed to have a strong tendency to engage in explicit or tacit collusion (see Ouchi and Bolton 1988; Teece 1992; Telser 1985). This is essentially a governance problem in that the alliances lack the structural mechanisms of monitoring and enforcement that competitive market forces provide. As Williamson (1985, p. 90) notes, marketplace competition “promotes high-powered incentives” that deter opportunistic behavior and encourage innovative activity. If competitor-dominated alliances weaken the competitive incentives, monitoring activities, and enforcement structures, the result should be a reduction in the customer orientation of alliance members.

To ensure that competitor firms maintain a strong customer orientation, traditional theory (from neoclassical economists) and practice (by the U.S. Department of Justice) have focused on the role of preventing the breakdown of marketplace incentives by making most forms of horizontal cooperation either illegal or subject to a high degree of scrutiny (Teece 1992; Telser 1985). These scholars suggest that competitor-dominated alliances will not harm customers if they are governed by a system that provides adequate monitoring of their activities and enforcement against anticompetitive practices. A means of providing this form of governance is the inclusion of a neutral third party, such as a government agency or university (Williamson 1985). Theoretically, these third parties have no profit motive and serve a watchdog function by ensuring that participants do not engage in anticompetitive practices.

In addition to serving as a watchdog against collusion, a third-party monitor can also infuse fresh ideas, which may minimize the dangers of overlapping knowledge. As cluster theorists hypothesize, neutral third parties, such as research universities, are critical sources of knowledge exploration for firms that cooperate with fellow industry members (Rosenfeld 1997; Saxenian 1994). Finally, a third-party monitor can also serve as a neutral judge and group facilitator to help resolve disagreements and build trust among alliance participants (Ouchi and Bolton 1988; Scott 2000). In summary, competitor-dominated alliances that have a third-party monitor should be more likely to maintain a stronger customer orientation over time than are competitor-dominated alliances without such a monitor. This leads to our second hypothesis:

H2: The presence of a third-party monitor attenuates the reduction in customer orientation experienced by firms cooperating in competitor-dominated alliances.

Relational ties

In addition to the structural mechanism of a third-party monitor, firms in competitor-dominated alliances may employ the behavioral mechanism of relational ties to influence alliance outcomes. Specifically, relational ties may serve as a governance mechanism by developing norms of reciprocity and perceptions of inter-connectedness among alliance participants (Rindfleisch and Moorman 2001). Although these norms and perceptions may evolve into trust in the long run (Axelrod 1984; Gulati 1998), relational ties rely more on mutual past debts and prospects of future interactions (e.g., Heide and Miner 1992) than on explicit trust in exchange partners.

Critics of interfirm cooperation have expressed considerable concern about the development of relational ties among competing firms because of the fear that these ties may lead to implicit collusion and a decreased customer focus (e.g., Clarke 1983; Mariti and Smiley 1983; Petit and Tolwinski 1999). Related cross-disciplinary research focuses on how the subtle pattern of ties and informal interconnections among executives of rival firms, through such mechanisms as common social backgrounds (Chandler 1977; Sabel 1993) and interlocking corporate directorates (Scott 1991; Westphal and Zajac 1997), influence firm behavior. In the aggregate, these studies imply that the development of close, relational ties among competing firms is detrimental to customers, because these links subvert marketplace incentives by promoting perceptions of goodwill and the development of norms of reciprocity among competitors.

This traditional view of the dangers of relational ties stands in stark contrast to the manner in which relational marketing scholars view such ties. Over the past decade, these scholars have established that the presence of relational ties (e.g., reciprocity, embeddedness) enhances the performance and satisfaction of firms engaged in alliances and other forms of long-term relations (Heide and John 1992; Lusch and Brown 1996; Morgan and Hunt 1994). For example, Lusch and Brown (1996) find that relational behavior between distributors and suppliers is positively related to distributor performance. As Heide (1994) specifies, relational ties provide an effective form of governance that reduces the hazards of opportunism and other forms of exploitation among exchange partners. Similarly, Gulati (1998, p. 296) suggests that relationalism “diminishes uncertainty and promotes trust between actors.” Thus, relational ties should enhance the ability of firms in competitor-dominated alliances to focus on customer needs by reducing the amount of time and attention they need to devote to monitoring the actions of their fellow alliance participants.

Although the relational marketing literature's findings about the benefits of relational ties are impressive, this research is largely focused on vertical relations and has not yet examined the relationship between interfirm relations and customer orientation. Thus, the extent to which these findings are relevant for customer-related outcomes among participants in competitor-dominated alliances remains an open empirical question. However, recent research in both marketing and related fields lends suggestive evidence that relational ties may also provide enhanced outcomes for firms that participate in horizontal relationships. For example, research on geographic clusters indicates that relational ties among competitors enhance information acquisition and organizational learning (Porter 1998; Rosenfeld 1997). In a marketing context, Rindfleisch and Moorman (2001) show that relational ties enhance information acquisition and utilization among firms in both vertical and horizontal alliances. This increased information should provide firms with an increased ability to respond to customer needs.

Given the two divergent perspectives on relational ties, it is possible, depending on the focus of the norms that are developed among alliance participants, that strong relational ties could either strengthen (as neoclassical economists suggest) or weaken (as marketing relationship scholars suggest) the reduction in customer orientation among participants in competitor-dominated alliances. Specifically, on the one hand, from the viewpoint of neoclassical economists, if alliance participants develop relational ties centered on norms of collusive activity, a dropoff in customer orientation should be observed. On the other hand, from the viewpoint of relational marketers, if alliance participants develop relational ties centered on norms of innovation or any other area of competition, a decrease in customer orientation should not be observed. As a result of this conceptual controversy and lack of prior empirical support for either direction, our third and final hypothesis explores the moderating role of relational ties in general without detailing a specific direction. We hypothesize the following:

H3: The presence of strong relational ties moderates the reduction in customer orientation experienced by firms cooperating in competitor-dominated alliances.

Method

Sample and Procedures

The sample frame for this longitudinal study is firms that have recently participated in new product alliances. As a sampling base, we examined the 242 alliances filed in the Federal Register from January 1, 1989 to March 15, 1995. In accordance with the NCRA and NCRPA, participants can file written notification of their alliance with the U.S. Department of Justice to protect alliance members from the threat of antitrust prosecution. The filings are published in the Federal Register and provide information about the formation date, identity, and location of each participant as well as the basic objective of each alliance. The NCRA filings provide one of the few freely available systematic data sources that document interfirm cooperative activity (Hemphill 1997). As the NCRA specifies, all the alliances were formed for the purposes of R&D but can legally encompass a broad swath of activities, including prototype development and model testing. In addition, although joint commercial production was beyond the scope of protection afforded by the original NCRA (though not illegal), the expanded NCRPA explicitly included joint commercialization activities under its purview.

Using these 242 filed alliances as a starting point, we selected 153 alliances (which contained 719 participants in total, for an average of 4.7 participants per alliance) for sampling. The 89 alliances that we omitted were deemed either too large for a firm to report on reasonably (i.e., more than 12 participants) or had no new firms to sample (i.e., all the participants were members of one or more of the other alliances in our data set). We limited the number of firms selected in each alliance to no more than six to increase the diversity of alliances in our sample. Within each alliance, we selected each firm (up to six), unless that firm had already been included in another alliance. Thus, firms that participated in more than one alliance were mailed only one survey about one specific alliance. We adopted this approach to increase the diversity of our data and the generalizability of our results. Because prior research indicates that international alliances systematically differ from domestic alliances (Harrigan 1985; Kogut and Singh 1988), we only included firms that were U.S. companies or domestic divisions of multinational corporations. These procedures resulted in 380 firms for inclusion in our study. 4 For each firm, we targeted the vice president of R&D (or an occupant of a similar position) as our key informant (Campbell 1955).

Of the 339 entities omitted from our sampling frame (719 – 380 = 339), 136 were duplicate firms, 51 were nonfirm entities (e.g., universities), 42 were foreign firms, and 110 were firms from alliances in which six members had already been selected.

Time 1 survey

Before mailing our first survey, we attempted to contact key informants by telephone. This process eliminated 39 firms (among six alliances) that we could not reach or for which we could not identify a knowledgeable informant. Thus, the population for our final sampling frame consisted of 341 firms. Each informant was mailed a cover letter, a summary describing the alliance in question, and a postage-paid reply envelope. Three weeks after the mailing, we telephoned nonrespondents as a reminder. One week later, we sent each nonrespondent a handwritten reminder postcard. Informants who did not reply within six weeks were mailed a second set of survey materials.

The surveys for 8 firms were undeliverable, and 33 firms replied that they lacked sufficient information about the alliance in question to provide useful information. This left an effective sampling frame of 300 firms across 147 alliances. From this base, 106 surveys were returned (across 70 alliances), for a 35% response rate. This response rate compares favorably with those of previous studies of alliance activity (e.g., Littler, Leverick, and Bruce 1995; Sivadas and Dwyer 2000). As Armstrong and Overton (1977) recommend, we assessed potential nonresponse bias using an extrapolation method in which we compared early (first two-thirds) and late (last one-third) respondents. These tests showed no significant differences between the two groups (alliance type: F(1, 104) = 1.18, not significant [n.s.]; customer orientation: F(1, 96) = .36, n.s.; relational ties: F(1, 103) = .08, n.s.; presence of a third-party monitor: F(1, 99) = .001, n.s.; number of alliance partners: F(1, 104) = 1.42, n.s.; alliance duration: F(1, 104) = .14, n.s.). This suggests that our data are unlikely to be tainted by nonresponse bias.

As an informant validity check, respondents provided information about their position, the number of years they had worked for the focal firm, and their degree of familiarity with the alliance in question. This information revealed that respondents were highly knowledgeable about the alliance (5.8 on a seven-point scale) and had substantial experience with their firm (14.8 years on average). Of the respondents, 66% were presidents or vice presidents of their firms. Thus, our sampling approach appears to have been quite successful in identifying knowledgeable and experienced key informants.

Although the NCRPA includes commercialization in its purview, we took steps to ensure that the alliances in our sampling frame engaged in customer-related activities. We analyzed content of the Federal Register filings for the 147 alliances in our sample and coded each alliance's stated objectives for research, development, and/or commercialization. On the basis of the assumption that product development and commercialization are activities that are closer to the market (and thus, the customer), we attempted to discern the frequency of these activities in our alliances. Results indicate that 97% of the sample had a research objective, 82% had a development objective, and 38% had a commercialization objective. The results show that most alliances had multiple objectives and that a large percentage were connected to the market through either product development or commercialization. We found no significant difference in the overall distribution of these objectives among firms in competitor-dominated (research = 98%, development = 83%, commercialization = 45%) and channel-dominated (research = 97%, development = 81%, commercialization = 36%) alliances.

As an additional means of evaluating the appropriateness of our sampling frame, the Time 1 survey included questions that provided information about the underlying motives that drive alliance formation. Specifically, we asked informants to rate the importance of a series of motives behind their firms' decision to enter the alliance using a seven-point scale (1 = “not at all important,” 7 = “very important”). These factors (and reported means) were changing customer needs (M = 4.80), increased threat of foreign competition (M = 3.15), increased threat of domestic competition (M = 3.93), and increased government legislation or regulatory requirements (M = 3.58). Analysis of mean differences reveals that changing customer needs is a significantly more compelling motive than the threats of foreign competition (t = 7.14, p < .001), domestic competition (t = 4.33, p < .001), or government requirements (t = 3.72, p < .001). The results indicate that customer-related concerns were the most important motive behind alliance formation, and they provide further support that the alliances formed under the NCRA have a substantial connection to customers.

Time 2 survey

Approximately three years after the mailing of our initial survey, we conducted a follow-up study. We mailed a cover letter, a survey, a description of the alliance in question, a postage-paid reply envelope, and a $10 bill as an incentive to the 106 respondents from our initial study. Three weeks after this initial mailing, nonrespondents were mailed a remainder letter. Three weeks later, the remaining nonrespondents were mailed a second complete set of survey materials. Twenty of our surveys were nondeliverable as a result of participants' relocation. This left an effective population of 86 respondents, from which 60 surveys were returned, for a 70% response rate. This response rate compares favorably with that found in prior longitudinal surveys (e.g., Jap 1999; Moorman and Rust 1999; Wotruba and Tyagi 1991). After eliminating five surveys that contained a severe amount of missing data, we were left with 55 longitudinal responses (from 39 alliances) for analysis.

To ensure that the respondents to our Time 2 survey were representative of both our Time 1 respondents and our sampling frame in general, we conducted several checks. First, we compared the means for our key measures among the 55 respondents of our Time 2 survey with the 51 nonrespondents and partial respondents. The tests showed no significant differences between the two groups (alliance type: F(1, 104) = .001, n.s.; customer orientation: F(1, 96) = 1.15, n.s.; relational ties: F(1,104) = .54, n.s.; presence of a third-party monitor: F(1, 99) = .26, n.s.; number of alliance partners: F(1, 104) = .912, n.s.). 5 Thus, it appears that the respondents to our Time 2 survey are representative of the firms that replied to our Time 1 survey.

It was not possible to calculate differences in alliance duration, because we do not have information on the duration of Time 1 alliances that did not participate in Time 2.

As a second means of safeguarding against selection bias, we compared our Time 2 respondents to the last third of our Time 1 respondents (see Armstrong and Overton 1977). Based on the assumption that the last third of the Time 1 respondents are similar to nonrespondents, similarity in response profiles between these two groups lends confidence that our Time 2 sample is not different from the original sample. An analysis of responses to our key measures indicates no significant difference between these two groups: (alliance type: F(1, 70) = .04, n.s.; customer orientation: F(1, 64) = .28, n.s.; relational ties: F(1, 70) = .31, n.s.; presence of a third-party monitor: F(1, 68) = .02, n.s.; and number of alliance partners: F(1, 71) = .07, n.s.).

As a third test of nonresponse bias, we examined the formation dates and number of alliance participants for the 39 alliances in our Time 2 sample against the remaining 108 (147 – 39) alliances in our original sampling frame. We computed the formation date of each alliance in terms of the number of months transpired since the beginning of our examination date (i.e., January 1989). Results indicate no difference in the alliance formation date between these two groups (MStudy 2 = 55, Msampling frame = 49, F(1, 145) = 2.01, n.s.); however, the results show a significant difference in the number of alliance participants between these two groups (MStudy 2 = 6.3, Msampling frame = 4.4, F(1, 145) = 14.03, p < .001). This difference arises from larger alliances having had more surveys mailed out to them than smaller alliances. Considering that collusion and interfirm cooperation is more difficult to establish in large alliances (e.g., Heil and Robertson 1991), this difference actually works against, not in favor of, our hypotheses.

Finally, based on the coding of alliance objectives, we used a repeated-measures test to compare the alliance objectives for our Time 2 alliances with both Time 1 alliances and the 147 alliances in our initial sampling frame. Results indicate no significant differences in the percentage of firms with research (sampling frame: 97%, Time 1: 95%, Time 2: 100%, F(2, 144) = 1.87, n.s.), development (sampling frame: 82%, Time 1: 90%, Time 2: 87%, F(2, 144) = .01, n.s.), or commercialization (sampling frame: 38%, Time 1: 45%, Time 2: 38%, F(2, 144) = .42, n.s.) objectives. In the aggregate, the four tests of nonresponse bias provide a reasonable degree of confidence that our final Time 2 sample is representative of both our Time 1 sample and our original sampling frame.

Measurement and Validation

Measure development began with interviews and a field test of our instrument among product development personnel at IBM to ensure that our measures were relevant and our language was appropriate for target respondents. Using the learning gained from this field test, we developed a pretest survey that we administered to 50 firms (23 responded) from an array of industries that had recently participated in new product alliances. We assessed psychometrics and adapted measures as needed. The final Time 1 survey contained measures of the key constructs and a set of control variables. We also assessed a subset of these key constructs in our Time 2 survey. These measures are detailed in the Appendix, and the intercorrelations, reliability, and descriptive statistics are provided in Table 1. With the exception of our Time 2 measure of customer orientation and our calculation of alliance duration, all the measures were collected in our initial survey, for which they served as our key predictor variables.

Key Measure Statistics

p < .01.

p < .05.

Notes: The coefficient alpha for each measure is on the diagonal, and the intercorrelations among the measures are on the off-diagonal. The coefficients for third-party monitor and alliance type represent point-biserial correlations (rpb). For alliance type: 0 = channel-dominated alliances and 1 = competitor-dominated alliances. N.A. = not applicable.

Customer orientation

We assessed customer orientation by means of five items from Narver and Slater's (1990) customer orientation dimension of their market orientation scale. These items are conceptually similar to the items in Deshpandé, Farley, and Webster's (1993) customer orientation scale and thus tap both the behavioral and the cultural foundations of customer orientation. We assessed all items on a seven-point Likert scale in which 1 = “strongly disagree” and 7 = “strongly agree.” This scale was included in both the Time 1 and Time 2 surveys and demonstrated good reliability in both applications (Time 1: α = .81; Time 2: α = .83).

Alliance type

This measure is designed to capture the horizontal versus vertical nature of the relationship among new product alliance participants. We asked respondents to classify each organization participating in the alliance as a customer, supplier, competitor, or other (adapted from Littler, Leverick, and Bruce 1995). On the basis of these classifications, we calculated the percentage of competitors in each alliance. The mean percentage of competitors across all alliances was 37%. Approximately 40% of the firms participated in an alliance in which half or more of the participants were competitors. The incidence of competitor-dominated alliances found in our sample is similar to that reported in prior studies (e.g., Robertson and Gatignon 1998; Vontoras 1997).

To reflect our theoretical interest in the distinction between horizontal and vertical alliances, we classified alliances into channel-dominated alliances (alliances composed of 0%–49% competitors) and competitor-dominated alliances (alliances composed of 50% or more competitors). Similar types of categorizations of alliance type have been successfully employed in prior research (Rindfleisch and Moorman 2001). As a means of assessing the validity of this categorization, we conducted a two-group k-means cluster analysis for alliance composition. This analysis revealed that our grouping displays a high degree of correlation (r = .96) with this cluster-group membership. Thus, it appears that our categorization closely fits the pattern of responses in our data, which is the essential concern when conducting categorical splits of continuous data (Tybout 2001).

As a means of assessing the equivalence of firms involved in competitor- and channel-dominated alliances, we examined the size of the firms (i.e., sales and employees) in the two types of alliances. We measured firm sales by the overall firm revenue as reported in Compustat for 1997 (the year the Time 1 survey was fielded). Using 1997 information collected from OneSource, we measured the number of firm employees. Results indicate that firm sales (Mcompetitor dominated) = $17.07 million, Mchannel dominated = $23.68 million, t = –.51, n.s.) and number of employees (Mcompetitor dominated = 780 employees, Mchannel dominated = 667 employees, t = .31, n.s.) do not differ between firms across these two types of alliances.

Third-party monitor

Recall that our conceptualization of a third-party monitor focuses on the effects that a neutral third party has on the interaction among alliance participants. We believed that respondents might have limited knowledge or difficulty reporting the specific activities of a third-party monitor. Therefore, instead of introducing error due to reporting problems, we simply asked respondents whether a neutral third party, such as a government agency, played a role in monitoring or enforcing the behavior of alliance participants. Of the firms, 49% in our Time 1 sample and 52% in our Time 2 sample reported participating in an alliance with this type of third-party monitor. 6 In 86% of the cases, the monitor was not a formal participant in the alliance, which we verified in the Federal Register filings.

Firms in alliances with a third-party monitor are statistically similar to firms without a third-party monitor in terms of both number of alliance participants (Meanmonitor = 6.92, Meanno monitor = 6.10, t = −1.55, n.s.) and alliance duration (Meanmonitor = 84.6, Meanno monitor = 70.6, t = −1.58, n.s.).

Relational ties

In accordance with research in the relational exchange literature (e.g., Dwyer, Schurr, and Oh 1987; Heide and John 1992; Lusch and Brown 1996), we view relational ties as evolving over time and as focused on interconnectedness and reciprocal exchange. In contrast to trust, these norms do not assess the degree to which respondents place confidence in the integrity and reliability of alliance partners (see Moorman, Zaltman, and Deshpandé 1992; Morgan and Hunt 1994). To capture this construct, we employed a four-item Likert scale, developed by Rindfleisch and Moorman (2001), that asks respondents to assess their firm's level of reciprocity and closeness with their alliance partners in general. This measure displayed adequate reliability (α = .83).

Dimensionality and discriminant validity

Using a confirmatory factor analysis, based on the data from our Time 1 sample, with LISREL 8.3 (Jöreskog and Sörbom 1993), we assessed the unidimensionality and discriminant validity of our two multi-item measures (i.e., customer orientation and relational ties). This model assessed the fit of these latent indicants by specifying the observed items for each measure as loading on their hypothesized latent construct and had strong fit indexes (χ2(36) = 349, goodness-of-fit index = .93, comparative fit index = .95, Tucker-Lewis index = .95, root mean square error of approximation = .06), suggesting that our multi-item measures display adequate dimensionality.

To assess the discriminant validity between our two latent constructs, we reran the initial model (in which the correlation between the latent constructs was freely estimated) and used a model in which the correlation between the latent constructs was constrained to unity (Anderson and Gerbing 1988). We found that the chi-square values for the unconstrained model were significantly lower than the chi-square values for the constrained model (Δχ2(1) = 134, p < .001), which provides evidence of the discriminant validity of these measures. As a more stringent test of discriminant validity, we employed Fornell and Larcker's (1981) test of shared variance between our two latent constructs. The results of this test reveal that the squared correlations between these constructs do not exceed average variance extracted for each single latent construct (p < .001), indicating discriminant validity.

Control variables

In addition to these key measures, we also collected data on two control variables. Specifically, we assessed the number of alliance partners and the duration of the alliance to ensure that these alliance characteristics did not confound the relationships among our key predictor variables and customer orientation. Prior research suggests that these two variables play an important role in influencing the outcomes of alliance activity (e.g., Heil and Robertson 1991; Link and Bauer 1989; Morgan and Hunt 1994). The number of participants is important because it should be easier to conduct anticompetitive collusive activities in small groups than in large ones. The duration of the alliance is important because a long history of interaction should enable firms to develop relational ties that may influence the outcomes of interfirm cooperation.

We observed the number of alliance partners by counting the number of alliance members listed in the Federal Register. The mean number of alliance partners was 5.42 (range: 1–11) for the 106 firms at Time 1 and 5.57 (range: 1–11) for the remaining 55 firms at Time 2. We controlled for the duration of the alliance by asking respondents (at Time 2) if and when they stopped participating in the focal alliance. Using the filing date in the Federal Register as a starting point, we calculated the number of months each firm had spent in the alliance. For firms that were still participating in their focal alliance at the time of the follow-up survey, we used September 2000 (the date the survey was closed) as the end point to calculate alliance duration. The mean duration was approximately 79 months (range: 17–132 months).

Results

Overview of Analysis Approach

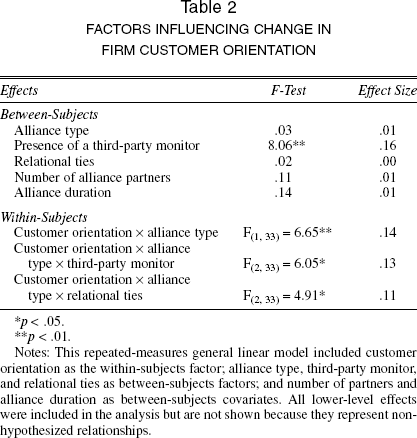

We tested our hypotheses using a general linear model with a repeated-measures design. The model included (1) customer orientation (Time 1 and Time 2) as a within-subjects factor; (2) alliance type, third-party monitor, and relational ties as between-subjects factors; and (3) number of partners and alliance duration as between-subjects covariates. In addition to providing a longitudinal perspective, a repeated-measures analysis also controls for subject variability. As Keppel (1991, p. 334) notes, “The error component … should be smaller in the case of repeated measures…. This reduction in error variance represents a direct increase in economy and statistical power.” This increase in statistical power reduces the likelihood of Type II errors and helps compensate for the smaller sample sizes typically associated with longitudinal surveys. The key results from our general linear model analysis are presented in Table 2.

Factors Influencing Change In Firm Customer Orientation

p < .05.

p < .01.

Notes: This repeated-measures general linear model included customer orientation as the within-subjects factor; alliance type, third-party monitor, and relational ties as between-subjects factors; and number of partners and alliance duration as between-subjects covariates. All lower-level effects were included in the analysis but are not shown because they represent non-hypothesized relationships.

Tests of Hypotheses

As we predicted in H1, our results indicate that alliance type has an important influence on customer orientation, because the two-way interaction between customer orientation and alliance type is significant (F(1, 33) = 6.65, p < .01) and has a medium effect size (partial ω 2 = .14). A plot of this interaction, which is shown in Figure 1, indicates that whereas firms in channel-dominated alliances experience essentially no change in their level of customer orientation over time (Time 1 = 5.95, Time 2 = 5.99), firms in competitor-dominated alliances experience a significant drop in their level of customer orientation over time (Time 1 = 6.22; Time 2 = 5.70). This pattern of results provides strong support for H1.

Change In Firm Customer Orientation By Alliance Type

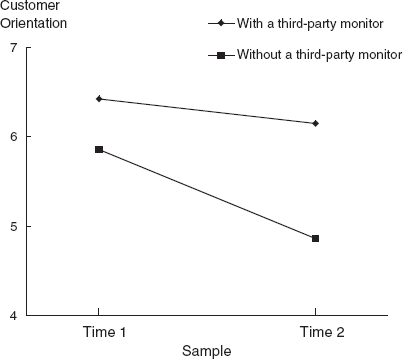

H2 predicted that firms in competitor-dominated alliances with a third-party monitor should experience a smaller decrease in customer orientation than firms in competitor-dominated alliances without such a monitor. We tested this hypothesis by examining the three-way interaction of customer orientation, alliance type, and third-party monitor. As shown in Table 2, this three-way interaction is significant (F(2, 33) = 6.05, p < .02) and has a medium effect size (partial ω 2 = .13). A plot of this interaction is shown in Figure 2 and reveals that firms in alliances with competitors without a third-party monitor experience a sharp drop in customer orientation (Time 1 = 5.86, Time 2 = 4.86), but firms in competitor-dominated alliances with a third-party monitor experience only a slight decrease in customer orientation (Time 1 = 6.42, Time 2 = 6.15). This finding provides strong support for H2.

The Effect Of A Third-Party Monitor On Change In Firm Customer Orientation In Competitor-Dominated Alliances

In contrast to the significant influence of the presence of a third-party monitor for competitor-dominated alliances, the presence of a third-party monitor had no effect on customer orientation for firms in channel-dominated alliances (third party absent: Time 1 = 5.91, Time 2 = 5.94; third party present: Time 1 = 6.00, Time 2 = 6.04). Notably, firms in competitor-dominated alliances with a third-party monitor also appear to possess a higher level of initial customer orientation (M = 6.42) than firms in such alliances without a monitor (M = 5.86). This difference is reflected in the third party's significant (F = 8.06, p < .01) and medium between-subjects effect size (partial ω 2 = .16), which is shown in Table 2.

H3 predicted that firms in competitor-dominated alliances that have strong relational ties with their collaborators should experience either an increase or a decrease in customer orientation compared with firms in competitor-dominated alliances that have weak ties. We tested this hypothesis by examining the three-way interaction among customer orientation, alliance type, and relational ties. As shown in Table 2, the three-way interaction is significant (F(2, 33) = 4.91, p < .03) and has a medium effect size (partial ω 2 = .11). Thus, H3 is supported. The plot of this interaction is shown in Figure 3 and reveals that firms in competitor-dominated alliances that have a low degree of relational ties with their collaborators actually experience a much greater decrease in their level of customer orientation (Time 1 = 6.13, Time 2 = 5.42) than firms in such alliances that have a high degree of relational ties (Time 1 = 6.31, Time 2 = 6.00).

The Effect Of Relational Ties On Change In Firm Customer Orientation In Competitor-Dominated Alliances

Although relational-tie strength has a strong influence on customer orientation for firms in competitor-dominated alliances, it has little effect on customer orientation for firms in channel-dominated alliances (strong relational ties: Time 1 = 6.12, Time 2 = 5.94; weak relational ties: Time 1 = 5.77, Time 2 = 6.18). Unlike the presence of a third-party monitor, relational ties do not have a significant between-subjects effect (F = .02, n.s.) on customer orientation.

Discussion

Understanding the consequences of interfirm relations is a central issue in contemporary marketing strategy research. Although considerable work has been conducted about the consequences of these relationships for participating firms or the alliance overall, relatively little is known about how such relationships affect these firms' constituencies, including their customers. As research on interfirm relations matures, an increasing number of scholars have begun to raise concerns about the broader consequences of these relations. As Smith, Carroll, and Ashford (1995, p. 17) note, “Cooperation among individuals, groups, and organizations can have harmful consequences for others…. [A]dditional research is needed on the potential drawbacks of cooperation and the conditions under which a very high degree of cooperation is not desirable.” Likewise, Ingram and Roberts (2000, p. 420) suggest that understanding the impact of cooperation among competitors “presents a very challenging but useful goal for future researchers.” Our longitudinal research directly addresses such concerns by finding that a key drawback to cooperation among competitors is a decrease in customer orientation. Moreover, we identify the conditions under which this drawback may be alleviated. In this final section, we review these findings, discuss their implications, identify the limitations of our work, and highlight further research opportunities.

Review and Implications of Our Findings

Using a longitudinal study among alliance participants over a three-year time frame, our study reveals three notable findings about the relationship between interfirm cooperation and customer orientation: (1) Cooperation among competitors appears to have a negative impact on a firm's level of customer orientation over time, (2) this negative impact may be attenuated among competing firms in alliances with a neutral third-party monitor, and (3) the presence of a high degree of relational ties among competing firms helps maintain a strong customer orientation. Collectively, these findings advance knowledge on the effects of interfirm cooperation on customers and hold important implications for both managerial practice and public policy.

Reflecting the new realities of the globalized, information-based, and time-dependent economy, interfirm cooperation has been heralded as the form of economic organization best suited to the environmental threats and customer demands of the twenty-first century (e.g., Best 1990; Brandenburger and Nalebuff 1996; Teece 1992). Our findings imply that though cooperation may be beneficial for certain firm- or alliance-level outcomes, it may also harbor a hidden danger by making some firms less sensitive to the needs of their customers. This danger appears to be greatest for firms involved in competitor-dominated alliances rather than channel-dominated alliances. Given marketing's traditional focus on channel-dominated alliances (Sheth and Sisodia 1999), decrements in customer orientation and other negative byproducts associated with horizontally based cooperation have received little attention in the relational marketing literature. Our findings imply that these potential hazards deserve further consideration from both marketing scholars and public policy officials.

A means of minimizing the hazards of competitor-dominated alliances appears to be the inclusion of a neutral third-party monitor, such as a government agency or a university. As our findings show, firms that participate in competitor-dominated alliances in which this type of third-party monitor is present exhibited no decrease in customer orientation over time. In contrast, firms in alliances that lack a third-party monitor experienced a sharp decrease in customer orientation during the three-year study period.

Transaction cost theorists (e.g., Williamson 1985) have noted that a neutral third party can provide an effective monitoring mechanism to ensure that exchange parties act in a forthright manner and resist opportunistic exploitation. However, the focus of these theorists has been on deceptive and opportunistic behavior among the exchange parties themselves. We believe our research enriches this theory by showing that this type of monitoring mechanism may also extend protection to the customers of the exchange parties. As shown in Table 1, third-party actors appear to be quite common in alliances; nearly half the R&D alliances in our sample had a third-party monitor. To date, the roles of these actors remain largely hidden, given that the vast majority of alliance-based research focuses on the main players (i.e., profit-based firms). Our research suggests that these hidden actors deserve more scholarly attention.

In sharp contrast to the lack of attention paid to third-party actors, relationship marketing scholars have devoted considerable attention to the issue of relational ties among alliance participants (e.g., Heide and Miner 1992; Rindfleisch and Moorman 2001). The general consensus among these researchers is that stronger relational ties are a boon to performance, because alliances characterized by strong ties last longer and produce superior relationship outcomes. This viewpoint is so widely shared that the benefit of strong relational ties is rapidly emerging as an established paradigm in the literature.

Our findings lend additional credence to this paradigm by suggesting that the benefits of strong relational ties extend beyond the particular exchange partners themselves; firms engaged in competitor-dominated alliances exhibit a much weaker decline in customer orientation if they have high levels of relational ties with competitors. Specifically, by serving as the building blocks of mutual trust, these ties should lower opportunism among alliance partners. This should help alliance members reduce the time and effort needed to monitor one another, thus freeing up their scarce managerial resources for sensing and responding to changing customer needs. These findings provide a marked extension to the relational marketing literature, which has focused on the internal benefits of relational ties for firms engaged in dyadic vertical relationships.

Collectively, this pattern of results helps shed light on the reasons competitor-dominated alliances appear to be harmful for customer orientation. Recall that competitor-dominated alliances differ from their channel-dominated counterparts in terms of displaying (1) higher levels of overlapping knowledge, (2) lower levels of trust, and (3) stronger motives for collusion. Although our study was not designed to test the predictive power of each of these characteristics, our findings lend some preliminary insight into their relative efficacy. Specifically, our finding that customer orientation is higher among competitors that have strong relational ties with their alliance partner seems to discount the premise that competitor-dominated alliances are havens for collusive activity. In addition, the positive effect that the presence of a third-party monitor plays in terms of sustaining the customer orientation of firms in competitor-dominated alliances appears to have more to do with its role as a mediator of interfirm conflict than as a monitor of interfirm collusion. Combined, the findings suggest that the ability of competitor-dominated alliance participants to sustain a customer orientation is largely hampered by the devotion of scarce managerial resources needed to build trust, gain information, and establish cooperation with competitors. In support of this supposition, our Time 1 survey revealed that firms in competitor-dominated alliances report a significantly lower level of trust in their alliance partners than do firms in channel-dominated alliances (Mcompetitor dominated) = 4.39, Mchannel dominated = 4.86, p < .03; for details, see Rindfleisch 2000).

Our findings also have implications for the market orientation literature. Although there are exceptions, most of the market orientation literature has not paid explicit attention to the impact of the distinct components of a customer orientation and a competitor orientation. Narver and Slater (1990) measure these separate components but combine them to examine the overall effect of market orientation on return on assets. Likewise, Jaworski and Kohli (1993) have separate items associated with competitors versus customers, but fold them into their intelligence acquisition, dissemination, and response dimensions of market orientation. Only Deshpandé, Farley, and Webster (1993) examine customer orientation in isolation. Following their lead, our concentrated focus on customer orientation enables us to discern the effect of interfirm cooperation on this specific orientation. As we have shown, cooperative arrangements among competitors can reduce customer orientation, especially if the alliance does not have the structural (e.g., third-party monitor) or behavioral (e.g., strong relational ties) mechanisms in place to ensure customer-focused outcomes.

Although our findings suggest that cooperation among competitors may be harmful to a firm's customer orientation, it is also possible that this orientation suffers under conditions of intense competition. As several scholars across a broad range of disciplines have observed, competitive rivalry does not always maximize consumer welfare (for a review, see Kohn 1986). For example, both Moorman (1995) and Gatignon and Deshpandé (1994) argue that excess competition can result in a cultural shift in which firms focus so heavily on beating their competition that they lose sight of both their customers and innovating on the customers' behalf. Relatedly, Day and Nedungadi (1994) find that managers with a strong competitor orientation make relatively little use of customer-based information when making marketing-mix decisions. In summary, as Best (1990, p.17) suggests, “The task is to create the right mix of competition and cooperation, a mix that is continually shifting.”

Limitations and Research Directions

Perhaps the major limitation of our study is the restricted size of our sample. Although our follow-up study obtained only 55 usable responses, our response rate was extremely high (70%), and our effect sizes are substantial (see Cohen 1977). Moreover, this type of longitudinal inquiry is often called for by relational marketing scholars (e.g., Dwyer, Schurr, and Oh 1987; Heide and Miner 1992), but it is seldom conducted. Nevertheless, further research efforts that use alternative sampling frames would nicely complement our work.

Another limitation pertains to the breadth of our sample. Although our sample included a broad swath of industries (e.g., manufacturing, energy, chemicals, electronics, transportation, customer goods), it focuses solely on U.S. firms. Thus, additional research is needed to establish whether our patterns of effects are globally generalizable. In particular, it would be worthwhile to determine whether collaboration among competitors also weakens customer orientation in Japan and Western Europe, where governments view cooperation as a means of enhancing both allocative and productive efficiency (e.g., Best 1990; Cohen et al. 2002; Villas-Boas 1994).

Our findings are also limited by our focus on a single dependent variable (i.e., customer orientation). Interfirm cooperation is a complex phenomenon that has many effects on the broader environment. Some of these effects may be quite beneficial in terms of enhancing consumer welfare. For example, collaborative R&D alliances are widely regarded as beneficial in terms of eliminating wasteful duplication of research by firms engaged in similar activities (e.g., Katz 1986; Petit and Tolwinski 1999). Thus, further research efforts could provide a valuable contribution by exploring a broader scope of consequences of interfirm cooperation, such as R&D savings, standardization of formats, and enhanced new product development activities (see Ouchi and Bolton 1988; Teece 1992).

A related limitation involves the self-report nature of our study. It is possible that competitor-dominated alliances did not change a firm's actual customer orientation level but rather changed the manager's perception of the orientation. Specifically, as firms interact with competitors, they may learn more about how competitors handle customer-related issues. As a result of this learning (i.e., benchmarking), firms in competitor-dominated alliances may systematically report a reduction in customer orientation over time. However, self-report measures, if biased, should be biased in a direction that reflects favorably on informants; our results do not and thus work against potential bias.

Nevertheless, further research could enhance our efforts by examining more direct indicants of consumer welfare, such as average price levels, customer satisfaction, or customer perceptions of the innovativeness of a firm's new products. As a preliminary indicant of consumer welfare, our Time 2 survey asked respondents to report the number of patents applied for based on their firm's participation in the new product alliance. It is notable that firms in channel-dominated alliances applied for approximately four times more patents than did firms in competitor-dominated alliances (Mchannel dominated = 1.61, Mcompetitor dominated = .41, t = 1.84, p < .08). This finding is congruent with our results for customer orientation and suggests that though competitors' overlapping knowledge may enhance self-reported innovation (i.e., creativity and speed) compared with internal firm standards (Rindfleisch and Moorman 2001), this knowledge may not translate into customer benefits.

As a final limitation, our study's focus on the formal aspects of interfirm cooperation does not address the vast amount of informal cooperation that occurs among firms on a regular basis (Lee and Lee 1992). For example, several studies of interfirm R&D activity show that informal know-how trading is commonplace in many industries (Allen 1983; von Hippel 1987). In addition to this informal research activity, competitors often cooperate on many day-to-day activities. For example, major airlines often sell one another's tickets and typically provide advance notice of fare increases (Cooper 1993). Similar forms of cooperative activity are also commonplace among major U.S. oil companies (Renfrew 1993). Researchers may want to investigate the impact of these informal forms of cooperation on customer orientation and other aspects of a firm's broader environment.