Abstract

Although retail price wars have received much business press and some research attention, it is unclear how they affect consumer purchase behavior. This article studies an unprecedented price war in Dutch grocery retailing that started in fall 2003, initiated by the market leader to halt its sliding market share. The authors investigate the short- and long-term effects of the price war on store visits, on spending, and on the sensitivity of these decisions to weekly prices and price image. They use a unique data set with consumer hand-scan and perceptual data for a national panel of 1821 households, covering two years before and two years after the price war started. Although the price war initially entailed more shopping around and increased spending, spending per visit ultimately dropped because consumers redistributed their purchases across stores. The price war made consumers more sensitive to weekly prices and price image, which helped both the chain that showed an improvement in price image (the price war initiator) and the chains that already had a favorable price image (hard discounters). The price war initiator managed to halt the slide in its market share, and its stock price improved. The losers were the rival mid-level and high-end chains. Unlike the initiator, their price image did not improve, and they suffered from increased price image sensitivity. The authors provide managerial implications for firms that are (or about to be) involved in a price war.

A price battle between large retailers is not uncommon. But the price war that rages now is entirely different. The price cuts encompass a much larger assortment, and the percentage price reductions are spectacular. More is going on here. (Schöndorff 2003, p. 1)

In the early 2000s, the leading Dutch supermarket chain Albert Heijn suffered from an unfavorable and deteriorating price image, which was especially troublesome in light of the rise of hard discounters (Aldi and Lidl) and worsening economic conditions. Despite their continued belief in the retailer's quality and service, fewer and fewer shoppers could justify paying such high prices. After several years of a sliding market share, on October 20, 2003, Albert Heijn decided to slash its prices for more than 1000 products. Using the headline “From now on, your daily groceries are much less expensive,” its double-page color advertisements in all national and local newspapers made clear that the chain was committed to decrease its prices systematically and permanently. 1

Additional factors may have contributed to Albert Heijn's decision to initiate a major policy change. Its holding company, Ahold, was involved in a major accounting scandal in 2002, which seriously affected its reputation as a reliable firm. Furthermore, in the weeks preceding the price war, the media and the general public had been stirred up by a payment bonus for Albert Heijn's chief executive officer, which many considered excessive in a time of economic decline. Several customers even decided to participate in a boycott of Albert Heijn to express their disagreement.

The price reduction applied to many national brands from a wide variety of categories. For example, Figure 1 shows how the regular price for a 1.5-liter bottle of Coca-Cola went down from €1.23 to €1.12 (–9%). Although Albert Heijn's operation to decrease prices was undertaken in complete secrecy, within two days all major competitors carrying this (Coca-Cola) stockkeeping unit (SKU) (C1000, Edah, and Super de Boer) matched or even exceeded the price reductions.

Prices of a 1.5-Liter Bottle of Coca-Cola at Four Leading Chains Over Time

A week later, Albert Heijn decreased prices for another 550 products. The price war that followed is unprecedented in Dutch retailing. As Table 1 shows, many more price-cutting rounds occurred over the next years and lasted until October 31, 2005. These subsequent rounds involved different brands (national versus private label) and categories, resulting in negative retail margins for hundreds of products (Holla and Koreman 2006; Van Aalst et al. 2005). As for scope and depth, this national price war dwarfs both documented incidents in the grocery industry that Heil and Helsen (2001) mention: the price cuts on private labels among the U.K. retailers Tesco and Asda and the 2% price drop in the Houston retailing market. In our case, the price war was nationwide, entailing an 8.2% reduction in food prices (Baltesen 2006a) and resulting in the lowest inflation level in 15 years (Consumer Reports 2004). The loss in added value for the Dutch retailing industry is estimated to be €900 million in one year, and more than 30,000 employees in the grocery industry lost their jobs (Van Aalst et al. 2005).

Overview of Price War Rounds

Sources: Van Aalst et al. (2005); Holla and Koreman (2006).

This Dutch supermarket price war fits in with the trend that retail price competition has become increasingly vivid in recent years, reducing retailer profitability (Ailawadi 2001). Discounters such as Wal-Mart, Aldi, and Lidl are challenging traditional retail formats on both sides of the Atlantic (BusinessWeek 2003). In almost all Western markets, grocery discounters have captured market share from traditional supermarkets and now occupy a prominent position (Cleeren et al. 2007). In the United States, Wal-Mart controls a large part of the retail market and is driving down prices at other retailers (Singh, Hansen, and Blattberg 2006). In the Netherlands, more than 52% of households frequently shopped at hard discounters Aldi or Lidl in fall 2003, up from 30% in 2001 (GfK 2003). The reaction of traditional retailers has varied from focusing on quality and service to engaging the challengers with substantial price reductions (Rogers 2001). However, these price reductions may trigger price wars, as in the case of Dutch supermarkets, which can last for a long time and strongly affect all market players (Rao, Bergen, and Davis 2000).

The literature is inconclusive about the consequences of price wars. Although, in general, price wars are believed to hurt revenues and long-term prospects for the market players (Brandenburger and Nalebuff 1996), other studies suggest that the impact depends on each player's price position and role in the price war (Busse 2002; Elzinga and Mills 1999; Rao, Bergen, and Davis 2000). Although the antecedents of price wars have been well documented (see our subsequent literature review), empirical research on their consequences is sparse. As a recent review concludes, “It is unclear what the overall effects of price wars are. Price wars are often assumed to lead to losses for the firms involved in the battle. … It is, therefore, important to research how price wars affect firms in the industry, whether these effects are uniformly distributed, and how such effects persist in the long run through lower reference prices” (Heil and Helsen 2001, p. 96).

To fill this gap in the literature, we study the consequences of the Dutch supermarket price war on consumer purchase behavior. We analyze how the price war affected two major components of purchase behavior (Singh, Hansen, and Blattberg 2006): store visits and spending (money spent per store per week). In particular, we investigate whether the price war led to more shopping around in the short run and to decreased spending in the long run. Furthermore, we test the hypothesis that the price war made store visit and spending decisions more sensitive to weekly prices and price image. To examine these issues, we use a unique data set that combines consumer hand-scan and perceptual data for a national panel of 1821 households, covering a period of 90 weeks before and 114 weeks after the price war started. For the six-largest national chains, we estimate a multivariate heterogeneous Tobit II model that includes the short- and long-term effects of the price war on store visits, spending, and the sensitivity of these decisions to weekly prices and price image. To complement our analyses, we not only estimate competitive reaction functions but also assess the effects of the price war on stock prices.

Although the price war initially entailed more shopping around and increased spending, spending per visit ultimately dropped because consumers redistributed their purchases across stores. The price war made consumers more sensitive to weekly prices and price image, which helped both the player that showed an improvement in price image (the price war initiator) and the players that already had a favorable price image (hard discounters). The price war initiator managed to halt the slide in its market share, and its stock price improved. The losers are the rival mid- and high-end chains: Unlike the initiator, their price image did not improve, and they suffered from the increased price image sensitivity. We expect these results to be generalizable because the Dutch grocery retail industry is representative of many Western markets on several key indicators (Steenkamp et al. 2005, p. 40). Moreover, a recent metaanalysis has concluded that price elasticities do not differ significantly among developed countries (Bijmolt, Van Heerde, and Pieters 2005). Thus, the consequences of the Dutch price war may hold lessons for retailers in other countries facing a similar situation.

We organize the remainder of this article as follows: In the next section, we discuss the price war literature, focusing on the gaps we aim to address. Then, we discuss the model used to quantify the price war effects on store visits and spending. The subsequent section describes the empirical setting and details our data sets. We then present the estimation outcomes and conclude by providing a discussion and limitations.

Research Background and Hypotheses

Price War: Definition and Importance

Price wars are characterized by competing firms struggling to undercut one another's prices (Assael 1990). Urbany and Dickson (1991) refer to a “price-cutting momentum,” or the downward price pressure that drives other competitors to follow the initial move. Price is a logical weapon of choice because it is easy to change fast (Kalra, Raju, and Srinivasan 1998). Unlike typical, intense price competition, price wars lead to prices that are not sustainable in the long run (Schunk 1999). After an extensive review of business press articles and academic literature, Heil and Helsen (2001) define a price war as requiring one or more of the following conditions: (1) There is a strong focus on competitors rather than on consumers, (2) the pricing interaction as a whole is undesirable to firms, (3) the competitors neither intend nor expect to ignite a price war, (4) the competitive interaction violates industry norms, (5) the pricing interaction occurs at a much faster rate than normal, (6) the direction of pricing is downward, and (7) the pricing interplay is not sustainable. Subsequently, we verify that the Dutch price war meets most (if not all) of these conditions.

Price wars have become a part of life in a wide range of industries (Rao, Bergen, and Davis 2000). Business press and academic research have reported on price wars in industries including electricity (Fabra and Toro 2005), oil (Slade 1992), telecommunications (Young 2004), automobiles (Breshnahan 1987), airlines (Busse 2002), fast food (Gayatri 2004), and groceries (Barnes 2004). Price wars erupt at various levels in the distribution channel and with growing frequency and intensity (Heil and Helsen 2001). As Rao, Bergen, and Davis (2000, p. 116) conclude, “If you're not in a battle currently, you probably will be fairly soon.”

Literature on Price Wars

Academic literature on price wars can be classified into three research streams. A first stream comprises game-theoretic contributions, with a strong focus on price war antecedents. An important price war trigger revealed in this steam is competitive entry (Elzinga and Mills 1999; Milgrom and Roberts 1982). Other factors deemed to be inductive to price wars are declining economic conditions (Eilon 1993; Slade 1990) and, often related to this, consumers' low (and/or declining) brand loyalty and high (and/or increasing) price sensitivity (Klemperer 1989; Sairamesh and Kephart 2000).

A second stream includes more managerial research. This work reflects on the link between price wars and firm strategies and characteristics. Companies with high exit barriers (Heil and Helsen 2001) and high stakes in the market or a worsened financial situation (Busse 2002) are more inclined to initiate a price war or to enter an ongoing battle. In doing so, these firms hope to bring about a market clear-out and to increase their profit from reduced competition in the long run (Fudenberg and Tirole 1986; Klemperer 1989), or at least to halt the loss of customers and maybe even reattract clientele (Elzinga and Mills 1999; Klemperer 1989). A widely advertised price cut may also establish a more favorable price image (Busse 2002; Rao, Bergen, and Davis 2000).

The third stream consists of empirical research documenting price war consequences. Unfortunately, despite the importance of price wars, such empirical contributions are extremely scarce and suffer from some limitations. Although the studies by Green and Porter (1984), Breshnahan (1987), Rotemberg and Saloner (1986) and Levenstein (1997) provide a glimpse of the nature and impact of price wars, the data set limitations of these studies do not allow the research to go beyond a rough empirical assessment. On the basis of 15 case studies in a diverse range of industries, Heil and Helsen (2001) provide some preliminary evidence on overall price war effects, including dwindling prices, declining image and revenues, and profit erosion for the parties involved. They also provide initial indications of increased shelf price elasticities for incumbent brands of a personal care product following a price war. They conclude (p. 86) that though their “descriptive statistics illustrate the importance and scope of price war phenomena, … more rigorous empirical research is needed.” We help fill in this gap by testing hypotheses on price war consequences with an empirical model, which we estimate using a unique and rich data set.

Price War Effects on Store Visits, Spending, and Price Sensitivity: Hypotheses

Henderson (1997) suggests that in the absence of a strong and sustainable cost advantage, price wars are “good for absolutely nothing” and may lead to dramatic losses for the market players involved. In this section, we develop a more refined picture of how price wars affect consumer spending, leading to a negative impact of the price war on some market players and a positive impact for others.

Given our focus on a retail setting, we decompose this spending effect into its two major components: store visits and spending, after a consumer decides to buy in the store. Moreover, we distinguish between the price war's main effect on these performance measures and its moderating impact on consumers' sensitivity to weekly store prices and to overall store price image. Finally, we expect substantial differences in the price war's performance effects in the short run versus the long run. The latter is important from a managerial perspective because great initial results may encourage retailers to cut prices further, even when the long-term effects of competitive escalation are disastrous (Dekimpe and Hanssens 1999; Ghemawat 1991). Figure 2 displays our conceptual framework and hypotheses.

The Effects of a Price War on (1) Store Visit and Spending and (2) Sensitivities to Weekly Price and Price Image

Main Effects of the Price War on Store Visits and Spending

Short-term Effects

By definition, price wars constitute market disruptions. Market players announce major strategy changes and formulate unprecedented claims on reduced prices. For example, the two major high-service/high-price Dutch retailers stated that shopping in their chain allows for “dramatic savings” on grocery spending (Albert Heijn) and that “gigantic” benefits are to be reaped from permanent price reductions (Super de Boer). Such widely publicized claims may shake up consumers' former beliefs about the market and lead them to reconsider their established purchase patterns, in terms of both store visits and spending.

In the short run (i.e., right after the start of a price war), consumers face increased uncertainty about which stores offer the best value for the money. As a result, they are likely to adopt risk-reducing strategies (Blattberg and Neslin 1989), engaging in comparison shopping to update previous information (Mick and Fournier 1998). In other words, they visit more chains, at least to check out the (new) prices in these stores. Thus:

H1: The price war leads to an overall increase in store visits in the short run.

At the same time, the price war's influence on spending is subject to three forces. First, the price war leads to lower prices, and as a result, spending is reduced even when quantities remain the same. In our approach, we focus on the impact of the price war on spending and control for these price-driven changes. This impact may be negative because of the second force; consistent with the argument on uncertainty, consumers may redistribute their purchases across stores, thus reducing the probability of systematically getting the worst deal (Fox and Hoch 2005). Conversely, the short-term impact of a price war on spending may be positive because of the third force; the sudden and heavily publicized price drop may create an unexpected “psychological income” or “windfall” effect. For example, a field experiment found that when given a monetary reward before entering a store, shoppers spent more in the store, in excess of the monetary reward (Heilman, Nakamoto, and Rao 2002). In a similar vein, the price war's sudden promise of “dramatic savings” may induce consumers to “burn a hole in their pockets”—that is, to increase their spending disproportionally—because the savings enable them to afford better-quality brands and to enjoy the transactional utility of getting a great deal (Chandon, Wansink, and Laurent 2000). Given these opposing forces, we investigate the price war's short-term effects on spending in an exploratory way.

Long-term Effects

Compared with the short run, there is little reason for the price war to increase store visits in the long run. Indeed, consumers in mature markets tend to develop stable purchase patterns, which are only temporarily disrupted by marketing activities (Ehrenberg 1988). Although specific stores may benefit from increased visits in the long run, consumers are unlikely to increase the overall frequency of store visits permanently.

In contrast, the price war is likely to decrease spending in the long run, even after we control for the changes driven by price reductions. Analogous to our argument for the short-term effect, we expect that a shopping environment characterized by an escalating price war induces consumers to redistribute their total grocery spending across the stores they visit. In contrast, the opposing force of a windfall effect is most likely only short lived because families are unlikely to consume much more food overall, even when prices drop substantially. An analogous result holds at the category level; that is, although weekly price promotions may expand the category substantially, they do so only temporarily (Pauwels, Hanssens, and Siddarth 2002; Van Heerde, Leeflang, and Wittink 2004). Because we believe that the negative force is present (splitting the grocery bill across stores) and that the positive (windfall) effect is absent in the long run, we expect that the price war will reduce spending.

H2: The price war leads to an overall decrease in spending in the long run.

Moderating Effects of a Price War: Consumer Sensitivity to Weekly Prices and Price Image

A unique feature of a price war is that pricing interactions occur at a much faster rate than previously (Heil and Helsen 2001). Intensive price interactions make price a more easily accessible attribute, which, as a result, increases its importance as a purchase criterion (Wänke, Bohner, and Jurkowitsch 1997). Lab experiments by Wathieu, Muthukrshnan, and Bronnenberg (2004) show strong evidence for this effect in a brand setting; specifically, offering and retracting discounts decreases the subsequent choice share for high-priced brands but increases the choice share of low-priced brands.

A price war between stores may enhance a consumer's reliance on two types of price information. First, a consumer is confronted with the actual, objective prices the stores charge, which may vary weekly as a result of regular price changes or promotional deals. These weekly prices determine how much the consumer actually pays for a specific product basket in a specific store and week. We define the store visit sensitivity to price as the response parameter of weekly store price in the model for store visit probability and the spending sensitivity to price as the response parameter of weekly store price in the model for spending (for more details, see the “Model” section). Consistent with a preference for lower prices, we expect that store visit sensitivity to price is negative and that spending sensitivity to price is positive in the case of price-inelastic demand and negative in the case of price-elastic demand (see Figure 2).

Second, consumers also hold subjective summary views of the stores' overall price appeal. As Mägi and Yulander (2005) show, these subjective price images constitute a separate price dimension that, at best, is moderately associated with actual objective prices and is more stable over time. Price image differentiates stores on the basis of their perceived price positioning. This perceived price positioning has been found to exert an important influence on store selection (Arnold, Oum, and Tigert 1983; Severin, Louvière, and Finn 2001), beyond objective weekly store prices. We define the store visit sensitivity to price image (spending sensitivity to price image) as the response parameter of price image in the model for store visit probability (spending probability), and we expect both sensitivities to be positive (see Figure 2).

Consistent with this dual retail price construct, increased sensitivity to weekly prices and price image triggered by a price war may materialize in two ways (Bell and Lattin 1998; Galata, Bucklin, and Hanssens 1999; Lal and Rao 1997). First, the price war may stimulate more opportunistic buying behavior, with consumers shopping around more to benefit from weekly deals on prices (Bell and Lattin 1998; Fox and Hoch 2005). Thus, consumers will be more responsive to stores' actual weekly prices (Drèze, Nisol, and Vilcassim 2004; Fox and Hoch 2005):

H3: The price war increases (a) the sensitivity of store visits to weekly prices and (b) the sensitivity of spending to weekly prices (i.e., the price war makes the corresponding response parameter more negative).

Second, responding more strongly to weekly prices requires increased effort from consumers. They may also engage in other, more general impression-based forms of price-oriented shopping. A consumer's enhanced focus on price then translates into systematically seeking out stores with a favorable overall price image (Bell, Ho, and Tang 1998; Galata, Bucklin, and Hanssens 1999; Rhee and Bell 2002) and allocating larger shares of wallet to these stores. This leads to additional moderating price war influences:

H4: The price war increases (a) the sensitivity of store visits to price image and (b) the sensitivity of spending to price image (i.e., the price war makes the corresponding response parameter more positive).

Because it is an empirical question whether H3 and H4 imply sensitivity changes in the short run and/or long run, our tests allow for both possibilities. Note that the hypothesized increase in price image sensitivity would entail a differential impact of the price war on different market players. This would be especially troublesome for high-end chains, but it might actually help low-end competitors in the long run (Boulding, Lee, and Staelin 1994). As such, the price war may make the price differences between stores more salient, causing stores with worse price images to suffer.

Because price wars are different from a period of intense price promotions (Heil and Helsen 2001), we test the price war hypotheses and control for price promotion–intensive weeks (we provide more details in the subsection “Independent Variables”). To the best of our knowledge, no empirical study has systematically distinguished the impact of a price war on consumers' store visits, spending, and weekly price and price image sensitivity. This is an important gap because the net outcome for firms involved in a price war hinges on these (possibly countervailing) effects. Researchers used to lack the necessary data on consumer perceptions and behavior before and during the price war. Our data set on the recent Dutch retailing price war enables us to overcome this hurdle. Before we provide details on the data set, however, we outline the model.

Model

To study the consequences of the price war for national retail chains, we model the purchase behavior of a national panel of Dutch households before and after the price war started. A household faces choices along two dimensions: which of the stores to visit (possibly more than one in a given week) and how much to spend at each store. We develop a model for the store visit decision and ln spending level of every household h (h = 1, …, H), for every chain i (i = 1, …, S), and in every week t (t = 1, …, T). Given that a household may visit multiple stores in one week and given the left-censored nature of household spending, we specify a multivariate Tobit II model (e.g., Fox, Montgomery, and Lodish 2004; Singh, Hansen, and Blattberg 2006). A store visit of household h for store i in week t (zhit) is described by a multivariate probit model:

In a given week t, household h may visit multiple stores. Thus, zhit equals 1 for those stores. The latent variable, z*hit, is modeled through a linear model:

Conditional on a store visit (zhit = 1), we model yhit, the ln of spending (in euro cents) by household h in store i in week t as follows:

Consistent with the extant literature that uses Tobit models for store visits and spending (Fox, Montgomery, and Lodish 2004; Singh, Hansen, and Blattberg 2006), we model the logarithm of spending (conditional on a store visit) because its distribution is closer to normal than the distribution of spending. The independent variables in the store visit equations (xhit) and spending equations (vhit) need not be the same. We specify the independent variables after we give more details about the data. The intercepts in Equations 2 and 3 capture individual-specific store preferences. We assume that these intercepts are randomly distributed around store means:

The stores visited and the amounts spent depend on consumers' time and budget constraints and are interdependent between stores. Our model allows for this by embedding Equations 2 and 3 in a multivariate framework. More specifically, we assume that the error vectors uht = (uh1t, …, uhSt)′ and ∊ht = (∊h1t, …, ∊hSt)′ follow a joint multivariate normal distribution, with a full variance-covariance matrix: (∊′ht, u′ht) ∼ MVN(0, Σ). Intrinsic store preferences for visits and spending may also be correlated, leading to a joint multivariate normal distribution for the error terms in Equations 4 and 5 as well: (ξ′h, τ′h)′ ∼ MVN(0, V). We also allow for unobserved heterogeneity in response coefficients. Specifically, we assume that the coefficients from the store visit and spending equations are jointly distributed multivariate normal:

The Dutch Price War in Grocery Retailing: Setting and Data

Empirical Setting

Previously, we described the Dutch supermarket price war in detail. How does it compare with the definitional conditions of a price war in Heil and Helsen's (2001) study? First, as for the strong focus on competitors rather than on consumers, the rival chains Super de Boer, Edah, and C1000 reacted within two days to Albert Heijn's initial move, which does not allow enough time to assess consumer responses fully. This fast competitive reaction might have been provoked by the goal Albert Heijn began at the start of the price war: “to become less expensive than the market average” (Baltesen 2006b, p. 1). To verify that competitive interactions intensified because of the price war, we estimate competitive reaction functions (Leeflang and Wittink 1996) before and after the price war started. The results reveal more (significant) reactions after the start of the price war for every retailer than before (for details, see the Web Appendix, Part B, at http://www.marketingpower.com/jmroct08).

Second, pricing interaction as a whole is undesirable to firms because it places a lot of pressure on already tight margins (Van Aalst et al. 2005). Third, although we cannot peer into managers' minds to assess whether the competitors neither intended nor expected to ignite a price war, there is no evidence of such intent (Baarsma and De Nooij 2005). Fourth, the claim that the competitive interaction violates industry norms is evident from lawsuits brought by large national brand suppliers against the price war initiator for selling far below the recommended price. In addition, smaller suppliers and grocery stores are facing bankruptcy (Van Aalst et al. 2005). As a result, the Dutch Ministry of Commerce opened an investigation to consider outlawing below-cost pricing (Baarsma and De Nooij 2005). 2 Fifth, the pricing interaction occurs at a much faster rate than normal (i.e., days instead of weeks/months) and the direction of pricing is downward, as Figure 1 illustrates. Finally, the pricing interplay is not sustainable because hundreds of items are now sold below cost in Dutch supermarkets (Van Aalst et al. 2005).

In Belgium, France, Greece, Ireland, Italy, Luxemburg, Portugal, and Spain, law prohibits retailers from selling at a price below cost. Other European countries, such as Denmark, Germany, Finland, Austria, Sweden, and the United Kingdom, are similar to the Netherlands in that they do not explicitly impose that selling prices must exceed costs (Baarsma and De Nooij 2005).

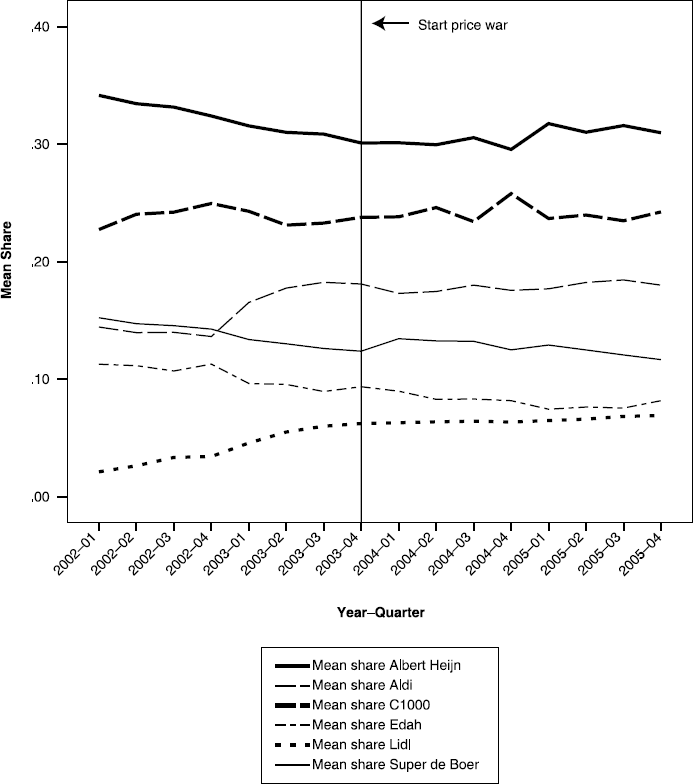

Although most sources agree that the price war appears detrimental to grocery retailers on average, there are mixed signals when it comes to individual players, especially by the time the price war seems to have taken its full effect. By the end of 2005, after more than two years of price warfare, Laurus (the holding company of Edah and Super de Boer) was on the edge of bankruptcy, but Albert Heijn claims to have achieved its goals, reporting a revival of revenues and profit (Baltesen 2006a). In a similar vein, Figure 3, which displays market share for the six leading supermarkets in the 2002–2005 period, indicates a strong post–price war decline for Edah, whereas the slide in Albert Heijn's market share before the price war is halted. A key question remains: What explains the difference in price war consequences for these key market players? By disentangling the price war impact from that of other drivers of chain revenue and by unraveling its effect on separate revenue components, our model and empirical results shed light on these issues.

Quarterly Market Shares of the Six National Chains (Within The Submarket of the Six Chains)

Data Sources

Our data set combines several sources. First, we use purchase records from the Dutch GfK consumer hand-scan panel across a period of four and a half years (July 1, 2001–December 31, 2005). Panel members scan at home all their purchases at all Dutch grocery retailers, and the data are sent electronically to GfK Benelux. This GfK panel consists of 4400 households, which represent a stratified national sample. We use this source to operationalize our dependent variables (store visits and spending) and the household- and store-specific weekly prices. A unique advantage of consumer hand-scan data (over in-store scanned data obtained through household identification cards) is that the market research agency does not need the permission for data collection from the retail chains. Such permission is increasingly problematic in both Europe (especially for the hard discounters) and the United States (Wal-Mart).

GfK also provided household perceptions of grocery retailing chains. Every six months, some of the panelists are surveyed on their perceptions of price image and produce quality. On the basis of these surveys, GfK prepares Christmas and summer reports for the Dutch grocery industry. In addition to these biyearly reports, GfK conducted a survey a few weeks after the price war started. We obtained the store image data at the individual household level for the same period, and for each week t, we assigned the perceptions from the measurement moment that is closest to week t. For the households that were not surveyed for a specific Christmas or summer report, we imputed image data using a two-way linear model—a typical and commonly used best-fit imputation approach (see Little and Rubin 1987, Chap. 2).

We obtained data from Information Resources Inc. and Publi Info (both in the Netherlands) on weekly feature and display for all items sold in Dutch grocery retailing chains across the same period. We used these variables to operationalize household- and store-specific feature and display variables. Finally, Reed Business provided the sizes (in square meters) and the locations (zip codes) for all Dutch grocery stores and each year in our data set. The store size data are a useful proxy for assortment size of each chain's store nearest to the household. We combined the store zip codes with the GfK household panelists' zip codes to compute the Euclidean distance between a household and the closest store from each chain.

Data Selection

Because the panel composition changes over time, we decided to select the 1821 households that remained in the panel across the four-and-a-half-year period. We use the first 30 weeks (Week 27 of 2001–Week 4 of 2002) as the initialization period for determining households' spending across categories and for the lagged store visit and spending variables. We used the remaining 204 weeks (Week 5 of 2002–Week 52 of 2005) for model calibration. The price war started in Week 43 of 2003, and thus we have 90 weeks before the start of the price war and 114 weeks afterward. This seems sufficient to measure long-term effects because by the end of 2005, the price war was in its aftermath (Van Aalst 2006). The full data set consists of 2,228,904 observations: purchases of 1821 households at six retail chains over 204 weeks.

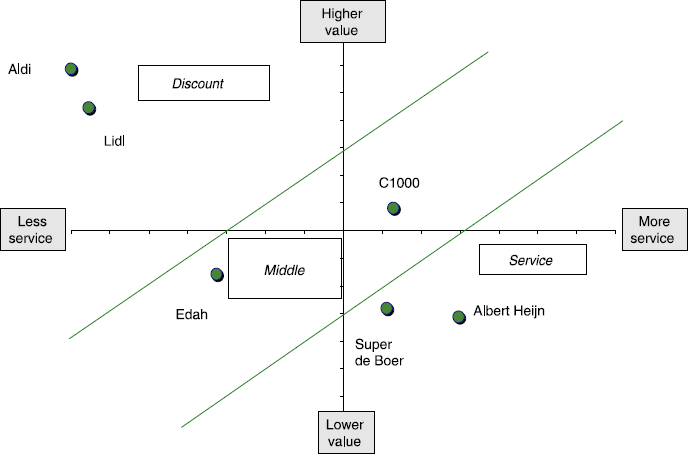

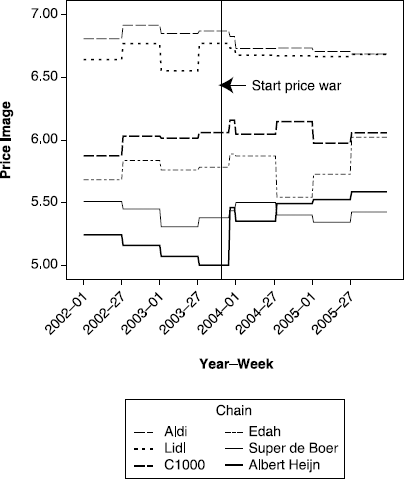

We model store visit and spending at the six largest chains with national coverage, which jointly comprise 70% share of the 2002 market. To illustrate the positioning of these chains before the price war, Figure 4 summarizes the store perception data in two main dimensions (according to GfK): service and value for the money. Albert Heijn is the market leader that initiated the price war. As illustrated by its scores on price image and produce quality (see Table 2), Albert Heijn is a high-price, high-service chain, which also applies to Super de Boer. The middle segment comprises two chains: C1000, with good scores for service and value, and Edah, with low ratings on both dimensions. The two hard discounters (low price, low service) are Aldi and Lidl. Notably, the price war led to a strongly improved price image for Albert Heijn, as Figure 5 shows.

Positioning of the Six Major Dutch Retail Chains in Summer 2002

Price Image for The Six Chains Over Time

Descriptive Statistics of the Six Chains Before (Pre) and After (Post) The Start of the Price War

The pre–price war period runs from January 2002 to October 19, 2003; the post–price war period runs from October 20, 2003, to the end of 2005.

This variable is the product of the percentage of stores that carry the promotion times the percentage of products that are promoted. It varies from 0 (no activity whatsoever) to 10,000 (100% of the products in 100% of the stores are promoted).

Actual weekly prices hardly decreased across the four and a half years of data (Table 2), which may be surprising given the magnitude of the price war. Two comments are relevant here. First, the prices we report in Table 2 are nominal price indexes. As Baltesen (2006a) points out, the corresponding decline in real prices was much stronger: In the absence of the price war, Dutch food prices would have been 8.2% higher than they actually were. Second, although many items were reduced in price, the majority of the stores' SKUs were not (and some prices of heavily featured SKUs increased again after an initial advertised price drop), implying that price drops for the entire basket remained modest.

Independent Variables

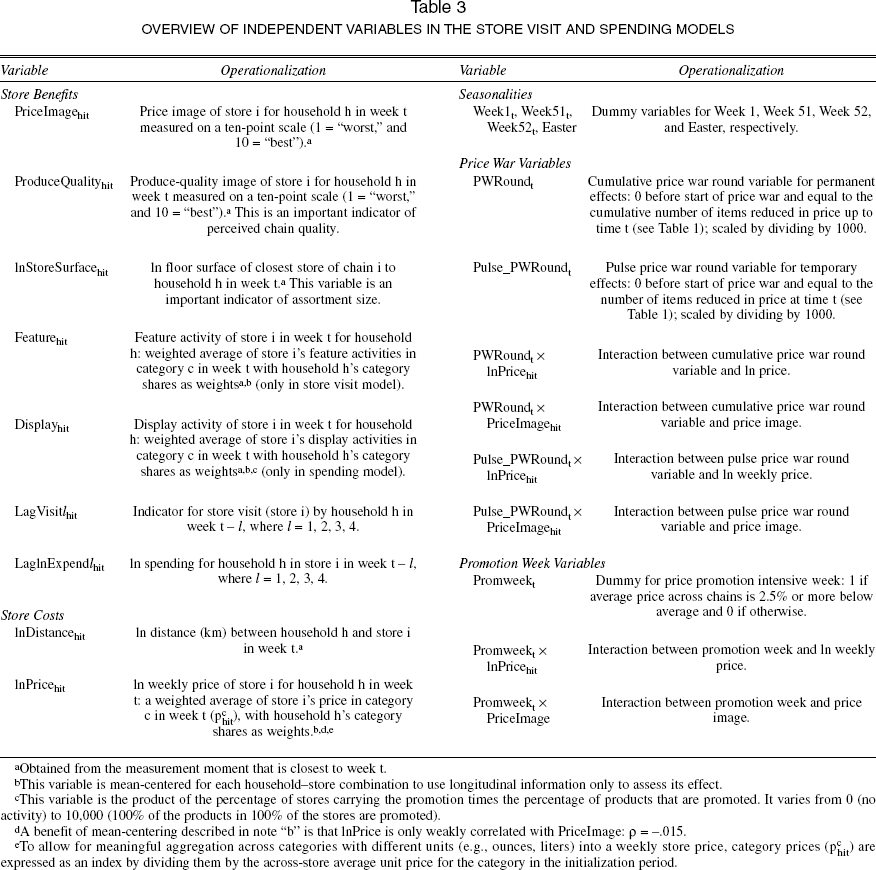

Store selection and spending depend on a trade-off between shopping benefits and costs (Bell, Ho, and Tang 1998; Tang, Bell, and Ho 2001), and Table 3 summarizes the corresponding independent variables. As store benefits variables, we include store price image, produce quality (an indicator of general quality), store surface (an indicator of assortment size), and feature and display variables (Bell, Ho, and Tang 1998; Fox, Montgomery, and Lodish 2004; Sirohi, McLaughlin, and Wittink 1998; Tang, Bell, and Ho 2001).3 Store familiarity or spending habits affect store visits and spending as well (Bell, Ho, and Tang 1998; Rhee and Bell 2002). Such state dependence can be captured with lagged purchase indicators (Ailawadi, Gedenk, and Neslin 1999; Seetharaman 2003). To capture a variety of shopping visit and spending patterns, we use four lagged variables that represent prior store visits and spending, one for each of the four preceding weeks.

We include feature in the store visit model but omit it from the spending equation because feature promotions represent out-of-store communication intended to enhance store visits. Similarly, we include display in the spending model but exclude it from the store visit model because this marketing instrument is observed only by shoppers inside the store. We verified both restrictions and found that posterior interval for the display parameter includes zero in the store visit model, and the same applies for the feature parameter in the spending model.

Overview of Independent Variables in the Store Visit and Spending Models

Obtained from the measurement moment that is closest to week t.

This variable is mean-centered for each household–store combination to use longitudinal information only to assess its effect.

This variable is the product of the percentage of stores carrying the promotion times the percentage of products that are promoted. It varies from 0 (no activity) to 10,000 (100% of the products in 100% of the stores are promoted).

A benefit of mean-centering described in note “b” is that lnPrice is only weakly correlated with PriceImage: ρ = –.015.

To allow for meaningful aggregation across categories with different units (e.g., ounces, liters) into a weekly store price, category prices (pchit) are expressed as an index by dividing them by the across-store average unit price for the category in the initialization period.

We include two independent variables for store costs: (1) store distance, representing fixed costs, and (2) weekly prices paid to acquire a basket of products, representing variable costs (Bawa and Ghosh 1999; Bell, Ho, and Tang 1998; Popkowski-Leszczyc, Sinha, and Sahgal 2004). 4 Importantly, because we mean-center weekly prices for each store–household combination, they capture longitudinal variation only, whereas the (untransformed) price image variable captures both cross-sectional and longitudinal variation. Furthermore, we include seasonal dummies (Weeks 1, 51, 52, and Easter).

As we discussed in the “Research Background and Hypotheses” section, we need to include weekly price as an independent variable in the models for store incidence and spending. This enables the price war variable (which we discuss subsequently) to capture the impact of the price war while controlling for mere price reductions. To avoid endogeneity issues, we use purchases from the initialization sample to define each household's basket of products rather than the current week's basket.

To test the hypotheses, we include price war variables, based on the price war rounds outlined in Table 1. We define the step variable PWRound as the cumulative number of items that were reduced in price since the start of the price war. Its coefficient in the model for store visit and spending represents the price war's long-term (permanent) effect. We also use its first difference, the pulse variable Pulse_PWRound, which represents the extra number of items reduced in price in a particular week. Its response coefficient represents the short-term effect of the price war on store visits and incidence. The use of step and pulse variables, combined with lagged endogenous variables, captures a wide variety of dynamic effects (Hanssens, Parsons, and Schultz 2001, pp. 295–96); at the same time, this specification is still parsimonious and tractable.5 In both the store visit and the spending equations, we also test whether the price war affects consumers' sensitivity to weekly prices and price image, in both the short and the long run. To that end, we use the interactions between these variables and the pulse and step price war variables: Pulse_PWRound × lnPrice, Pulse_PWRound × PriceImage, PWRound × lnPrice, and PWRound × PriceImage.

It is unlikely that retailers set basket prices or decide on the number of items to reduce in price as a function of same-week spending levels of individual households, especially in a competitor-centered price war setting. This justifies our choice of treating weekly price and price war variables as exogenous.

Finally, consumers may become more price and price image sensitive not only in the course of the price war but also in other periods of intensified price promotions in which supermarkets tend to engage. To identify these periods, we define a new dummy, Promweek, which is 1 in promotion intensive weeks (average price index across stores is 2.5% or more below the yearly average) and 0 otherwise. This operationalization identifies promotion-intensive periods that make intuitive sense because they largely correspond to the periods when households are on tighter budgets (beginning of the year and end of summer). We include the main effect of promotion week and its interaction with weekly prices (Promweek × lnPrice) and price image (Promweek × PriceImage) in the models for store visits and spending. Our results are robust to alternative definitions of Promweek (based on a price that is 2% or 3% lower than average).

Table 2 shows that the means of several store activities change between the periods before and after the price war started. For example, the average distance to a Lidl store decreases from 7.0 to 5.3 kilometers, reflecting Lidl's increase in the number of outlets. In addition, the average store surface areas tend to increase over time (because of either remodeling or new stores). Moreover, the feature and display activities increase for Aldi and Lidl and decrease for some other players. Our model includes control (independent) variables for each of these changes to obtain unbiased estimates for the price war effects.

Results

Store Visits

We present the store visit results in the left-hand part of Table 4. All benefit variables (PriceImage, ProduceQuality, StoreSurface, Feature, and LagVisit1–4) have positive effects on store visit probabilities (and their 95% posterior interval excludes zero). The positive impact of lnStoreSurface (.155) is consistent with store size being a proxy for assortment size. The coefficients of lagged visit (.235, .298, .283, and .264) indicate the expected positive state dependence. As for costs, we find that a greater distance between a household and a store (i.e., more travel time and costs) has the expected negative effect on store visit probability (–.502). In addition, the effect of price is negative (–.097), as we expected. The seasonal effect estimates indicate a decreased propensity to visit grocery stores in the Christmas week (Week 52: –.107) and in the first week of the year (Week 1: –.458), possibly because stores limit their opening hours (grocery stores are closed on December 25 and 26 and on January 1), and consumers prefer to stay at home with family and friends. On Easter, the store visit propensity goes up (.073), plausibly because consumers want to shop for holiday meals, and the longer opening hours (relative to Christmas) enable them to do so. We find that during promotion-intensive weeks, consumers go more often to stores (Promweek: .24). In addition, in these weeks, their store visit decision is more sensitive to weekly prices (Promweek × lnPrice: –.350). Both effects make intuitive sense.

Posterior Distributions of Response Parameters

The 95% posterior interval excludes 0.

Notes: To preserve space, we do not report store-specific moderators (intercepts) of the random household effects.

Focusing on the impact of the price war variables, we note several findings (see also Figure 2). Consistent with H1, the overall store visit propensity temporarily increases because of the price war; the coefficient for Pulse_PWRound is positive (.020). However, in line with expectations, this traffic increase does not persist. In the long run, the price war even reduces visits for the average store; the coefficient of PWRound is negative (–.011). This result must be interpreted against the finding that the price war makes the store visit decision more sensitive to weekly prices and price image, consistent with Heil and Helsen's (2001) prediction. Specifically, we find support for H3a in the short run (but not in the long run); the sensitivity of store visits to weekly prices increases temporarily at each new price war round (Pulse_PwRound × lnPrice: –.058). For H4a, we find support only in the long run (PWRound × PriceImage: .005), implying that price image becomes a more important criterion for store visit as the cumulative number of items reduced in price increases.

Spending

The estimates for the ln spending equation appear in the right-hand part of Table 4. All the benefit variables have the expected positive effects. Spending increases with PriceImage (.008), ProduceQuality (.010) and Display (.003). Moreover, it increases with lnStoreSurface (.098), consistent with the notion that larger assortments allow for the fulfillment of more consumer needs, and with lagged spending (.002, .009, .010, and .009), consistent with positive state dependence. On the cost side, a longer distance to the store leads to less spending (–.116). This may be true either because transportation from the store to home by foot or bike (which is common in the Netherlands) becomes increasingly difficult when there are more groceries to carry or because consumers visit these far-away stores for fill-in trips on their way home from work. The elasticity of spending to weekly prices is positive (.282) but lower than 1. This implies that before the price war, the elasticity of quantity to price was negative but inelastic. As for seasonalities, the effects of the pre-Christmas week (Week 51: .127), the Christmas week (Week 52: .025), and the Easter week (.128) on ln spending are positive, whereas the effect of the year's first week on spending is negative (Week 1: –.217), possibly because of consumers' use of excessive stocks from the preceding holiday week or their economizing or dieting. During promotion-intensive weeks, the reduced prices enable consumers to spend less (Promweek: –.07), and their store spending decisions are more sensitive to weekly prices (Promweek × lnPrice: –.026); these effects make intuitive sense.

Again, the price war variables reveal some notable results (see also Figure 2). Consistent with H2, the price war causes decreases in ln spending in the long run (PWRound: –.004). However, the coefficient of Pulse_PWRound indicates that after the start of the price war, consumers initially spend more per shopping trip (.008). This short-term phenomenon is consistent with a temporary income or windfall effect; that is, consumers initially perceive the announced price reductions as a gain that triggers them to buy more, but then they adjust spending downward again. Consistent with H3b, we find that the price war makes spending more sensitive to weekly prices both in the short run (Pulse_PwRound × lnPrice: –.084) and in the long run (PWRound × lnPrice: –.026). Similar to the store visit results, for H4b, we find support only in the long run (PWRound × PriceImage: .004), implying that price image becomes a more important criterion for spending as the cumulative number of items reduced in price increases.

Decomposing the Net Impact of Price War on Store Visits and Spending

The price war affects the models for store visit and spending in multiple ways. First, the price war has an impact on independent variables that capture price aspects (e.g., weekly price, price image). Second, there is a direct effect of the price war on intercepts and response coefficients for the store visit and spending models. The intercept effect is captured by the cumulative price war variable, PWRound, whereas the moderating effect of response coefficients is manifested in the terms PWRound × lnPrice and PWRound × PriceImage. Because we want to focus on long-term changes, we exclude the temporary change captured by the pulse variable Pulse_PWRound.

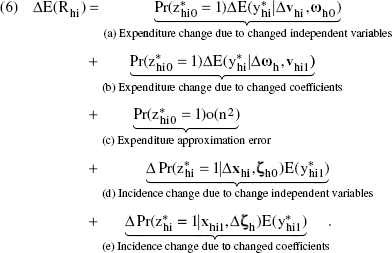

To decompose the effect of the price war on store visit and spending, we proceed as follows: Because we calculate a ceteris paribus effect, we vary only the price-related variables (price image, basket price, and the PWRound variables), keeping the other variables (e.g., distance to store, store surface, feature, display) constant. This avoids confounding these variables and the price war variables. Specifically, we consider the quarter before the price war started the pre-price war period (2003, Weeks 30–42). The vectors vhi0 (the expenditure equation) and xhi0 (the store visit equation) include the price and price image values in the pre-price war period for household h and store i. They also include other independent variables, such as distance to a store, which are kept at their means across the pre– and post–price war periods to isolate the price war effect. The corresponding response coefficients are ωh0 (the expenditure equation) and ζh0 (the store visit equation). For the post–price war period, we take the last quarter of the data (fourth quarter of 2005), and the variables and parameters are vhi and xhi1 (again, all non–price war variables are kept at their means across pre– and post–price war periods), ωh1, and ζh1. 6 The price war–induced change in a household's expenditure at a store, ΔE(Rhi) = E(Rhi1) – E(Rhi0), can be decomposed into five (a–c) components (see the Web Appendix, Part C, at http://www.marketingpower.com/jmroct08):

We also tested a few alternative post–price war periods and found that the substantive outcomes remain the same.

Because parts a and b capture expenditure changes multiplied by pre-price war store visit probabilities, these parts can be interpreted as changes in spending at the existing store visit propensity (which we interpret as “the existing customer base”). Conversely, because parts d and e capture store visit changes multiplied by post–price war spending, they represent the effect of the changed store visit propensity at the new expenditure level. Part c is an approximation term that is due to a Taylor series expansion (for details, see the Web Appendix, Part C, at http://www.marketingpower.com/jmroct08). We find this term to be negligible in all the subsequent calculations.

We calculate decomposition (Equation 6) at the household level (using the households-specific parameters) and then take the average across households. 7 Table 5 shows the results for each of the six chains. For Albert Heijn, average spending decreases by €1.09, which is a reduction of 10.3%. However, because the six chains together also lose 10.3%, Albert Heijn's market share is preserved (consistent with Table 2 and Figure 3). Albert Heijn's spending loss is primarily due to a strong decrease in current customers' conditional spending (–.72), which is largely due to the effect of the price war rounds on the intercept (–.61). On the positive side, Albert Heijn, as the price war pioneer, enjoys an improvement in overall price image (see Figure 5), which somewhat enhances conditional spending (+.01). However, consumers' increased sensitivity to store price image, combined with the notion that Albert Heijn's relative price image in the market remains unfavorable, more than offsets this effect (–.16). 8 Albert Heijn also experiences a net decrease in store patronage (–.38), caused primarily by an intercept driven down by the price war rounds (–.41).

In these calculations, we use all parameters regardless of whether their posterior intervals exclude zero.

As price image enters the interaction term after mean centering, it reflects the chain's price position compared with the market average. Thus, it takes on negative values for stores with a worse-than-average price image. As a result, an increased price image coefficient leads to negative store visit and spending effects for such stores.

Decomposition of the Net Effect of the Price War on Store Visits and Spending

Notes: The table shows the decomposition of spending for each chain (in euros), averaged across all households on the basis of Equation 6. We use equilibrium estimates for conditional spending and store visit by repeated substitution. In particular, in the spending model, we use four lags of the predicted unconditional spending (product of store visit probability and conditional spending) on the right-hand side to predict for period t, t + 1, and so forth, until convergence. In the store visit probability model, we repeatedly use lagged predicted store visit probabilities as independent variables, until convergence. We contrast the quarter preceding the price war (2003, Weeks 30–42) with the final quarter in the data set (2005, Weeks 40–52). The approximation error (term c in Equation 6) is .06 for Albert Heijn but does not exceed .02 for the other chains, and therefore we omit it from the table.

Ironically, the two hard discounters, Aldi and Lidl, remain largely unaffected. Although the price war somewhat reduces the intercept part of store visit probability (–.23 and –.14 for Aldi and Lidl, respectively), consumers' increased sensitivity to their still-favorable price image (Figure 5) enhances store visits (+.25 and +.11, respectively). The other three chains (C1000, Edah, and Super de Boer) all experience net losses in average spending (–.85, –.32, and –.56, respectively). Table 5 shows that the increased sensitivity of spending and store visits to C1000's favorable price image (+.10 and +.09, respectively) is not enough to compensate for major intercept losses (–.51 for both store visits and spending). Edah faces an array of problems: Both spending (–.16) and visits (–.16) are down, in each case driven by price war–induced intercept losses and an increased sensitivity to an unfavorable price image. Finally, Super de Boer's loss in spending is driven by intercept reductions and reduced spending of the existing customer base due the chain's increased vulnerability to its weak price image (–.11).

The Impact of the Price War on Profitability and Share Values

Our core analysis pertains to changes in purchase behavior due to the price war. It might be argued that purchase behavior and the associated revenue implications are mediators for ultimate performance measures, such as profitability and stock market performance. Although detailed and reliable figures on national chain–specific margins are lacking (in particular, for Aldi and Lidl), the retailers' annual reports unveil some important insights. Ahold (2004, p. 64)—the holding company of Albert Heijn—indicates that “Albert Heijn's ongoing price repositioning strategy resulted in fierce price competition in the Dutch food retail market. This made it more difficult to maintain gross profit margins, and this pressure on gross profit margins is expected to continue in 2005. Albert Heijn was able to compensate for part of the impact of lower prices by reducing the cost of goods, largely as a result of negotiations with vendors as well as increased vendor allowances. The cost reduction program at Albert Heijn is focused on lowering logistic and distribution expenses.” Albert Heijn's dominant retail market position enabled it to recoup much of the price drop at the expense of manufacturers, whose profit margins, according to some industry sources, have decreased by 80% after three years of the Dutch price warfare (Baltesen 2006a). Together with a massive effort to improve the efficiency of its operations, this appears to have prevented huge downturns in Albert Heijn's profitability.

In contrast, for Laurus (which owns the chains Edah and Super de Boer), net sales (revenues times gross margin) decline sharply in three successive years (Laurus 2003, 2004, 2005) to −26% in 2002–2003, −14% in 2003–2004, and −10% in 2004–2005, leading to the following statement: “As a result of the price war, … hundreds of products are sold below cost. Combined with a lower sales volume, this has had a significant negative impact on our bottom line. Given the financial position of Laurus, there was no other option but to sell Edah” (Laurus 2005, p. 3). Lacking the deep pockets and market power of Albert Heijn/Ahold, the Edah chain is a primary casualty of the price war. For C1000, net sales initially keep increasing (+8.1% in 2002–2003; +3.2% in 2003–2004), but they begin to tumble as the price war lingers on (–1.6 % in 2004–2005) (Schuitema 2003–2005).

We observe similar patterns in the share values (see the Web Appendix, Part B, at http://www.marketingpower.com/jmroct08). Structural break analyses of the retail companies' weekly stock price indexes (own stock price divided by the total market price) on the Amsterdam Stock Exchange reveal that the price war, though not significantly altering the share notation of Schuitema (C1000), goes along with a downward slope shift for Laurus (Edah, Super de Boer, Konmar) but an upward slope shift for Ahold that almost nullifies the pre–price war downward trend. It appears that the improved price image of Albert Heijn, together with its no-longer-declining market share and pursuit of massive efficiency improvement operations, has outweighed the harmful store visit and spending implications of the price war, thus restoring shareholders' faith.

Discussion

Summary

This article examines the impact of a major price war on consumer purchase behavior. We find that the price war that has been raging among Dutch grocery retailers since October 2003 has affected both store visit probabilities and spending. On the basis of a national household panel that provides hand-scan data and perceptual measures of store image across a nearly four-year period, we estimate a multivariate Tobit II model for store visits and spending. The model allows for household heterogeneity and a full covariance structure (across store visits and spending) for the errors, for the random store intercepts, and for response coefficients. Decomposing the price war–induced changes in spending patterns, we show that these changes are induced not only by a shift in weekly prices and price image (independent variables in our model) but also by changes in household shopping behavior (model coefficients). As hypothesized, we find that the price war has induced consumers to shop around more, entailing a temporary increase in store visits across the board. Moreover, although the price war initially created a windfall effect that triggered temporarily increased spending, spending levels have shrunk in the long run as consumers have redistributed their purchases across the stores they visit. At the same time, the price war has enhanced consumers' sensitivity to both weekly store prices and chain price image, confirming predictions in the literature (Heil and Helsen 2001) and lab experiment findings (Wathieu, Muthukrshnan, and Bronnenberg 2004). Thus, consistent with the Lucas critique, we find that the initiator's major policy change affects response parameters (Van Heerde, Dekimpe, and Putsis 2005). Importantly, we distill these price war–based effects while controlling for price promotion–intensive weeks. Our decomposition of the spending change reveals differential consequences for key retail chains depending on (1) their overall (perceived) price position and (2) their ability to improve price image through the price war.

Price War, What is it Good For?

Our answer to the question “What is a price war good for?” has five aspects. First, the Dutch supermarket price war has been good for the price image of its initiator; that is, Albert Heijn succeeded in improving its price image without doing significant harm to its quality and service images. 9 However, other retailers, which followed Albert Heijn's move within days, did not obtain such price image gains. This first-mover advantage in a price war (Busse 2002; Elzinga and Mills 1999; Rao, Bergen, and Davis 2000) confirms several business anecdotes (Pauwels et al. 2004; Simon 1997). If the price war initiator specifically wants to improve its price image, the price war appears to be successful.

We fail to reject the null hypothesis of no change in these components after the start of the price war.

Second, the price war has been good for the initiator's market share; specifically, the slide in its market share came to a screeching halt (Figure 3). However, our analysis shows that this holds because the price war decreased spending at Albert Heijn at the same rate as at the market average (–10.3%). In that sense, Albert Heijn's “price war victory,” as reported in the business press (Baltesen 2006a), is somewhat bittersweet. Still, investors have rewarded the price war initiator by neutralizing the downward trend in its stock price, consistent with the halt in its market share decline and its improved price image among consumers.

Third, with regard to competitors, the price war has been bad for the high-service follower (Super de Boer) and the middle-service followers (C1000 and Edah) because they were also affected by smaller spending. Moreover, they have not enjoyed an improved price image, as the pioneer has. Their lower prices appear simply to subsidize existing customers. Ironically, however, the price war has been good for the hard discounters. Although consumer spending has hardly been affected, these discounters' market shares have increased because their competitors' revenues have contracted. The hard discounters have benefited from an increase in store visit propensity triggered by consumers' enhanced sensitivity to price image.

Fourth, from a broader perspective, the upside of the price war for consumers is lower prices. Downsides are less obvious, but the lower manufacturer and retailer margins harm the industry as a whole. One likely consequence is a reduction in resources for research and development, which, in the long run, harms product quality and thus could hurt consumers. Another downside is that the price war may reduce the focus on important marketing variables, such as service and assortment.

Fifth, firms may go bankrupt, which reduces consumer choice. For example, the Dutch price war forced the Edah supermarket chain to go out of business.

External Validity

Although our findings are based on a unique data set and a new methodology, they are consistent with trends reported by external sources. The increased consumer sensitivity to weekly prices is reflected in the nationwide Consumer Trends survey by EFMI (2002, 2004, 2005), which reports that low prices became the major consumer decision criterion in store choice (46% of respondents named it within their top three criteria, up from 35%). This high sensitivity to price/promotions appears to be maintained in 2005.

Because our findings are related to the weekly household level for a representative sample, they must be projected to aggregate levels (whole population for a full year) to grasp their relevance to the retailer's overall performance. For example, the total per-household spending change of €–1.09 for Albert Heijn (Table 5) translates into an annual €369 million revenue loss across the 6.5 million Dutch households (www.cbs.nl [accessed November 7,2007]). Thus, the magnitude of the price war effects is managerially substantial compared with the €5.6 billion in revenue of Albert Heijn in 2003 (Ahold 2003, p. 61). Our estimated total loss among the six largest Dutch retailers amounts to €972 million, which is close to industry estimates that put the loss at €900 million (Van Aalst et al. 2005).

Managerial Implications

Although our findings are related to the specific consequences of this particular price war, we can speculate on recommendations for retail and brand managers who either intend to start a price war or perhaps are unintentionally involved in one. First, if the competitive situation is such that a price war is likely anyway (e.g., based on the early warning signals that Heil and Helsen [2001] identify), it is desirable to make the first strike because it may bring a first-mover advantage in price image improvement. This price war benefit is especially relevant for market players with a price image problem, as was the case for the Dutch price war initiator.

Second, we caution high-end market players about the risk of using price as a competitive weapon because it may increase price (image) sensitivity. This could backfire if the high-end player's price remains relatively high as a result of competitive reactions.

Third, discounters may actually benefit from a price war. They can advertise their low price levels, for which there may be increased consumer attention and sensitivity, leading to more store visits and expenditures. If there remains a substantial price gap with the middle- and high-end players (as was the case for Aldi and Lidl in the Dutch price war; see Table 2), low-end players seem to have little reason to reduce prices further during a price war.

Fourth, managers should not be too encouraged if a price war initially brings more visitors to their stores or buyers to their brands. A price move may reengage customers (Chen and McMillan 1992) to compare prices in the short run, but in the long run, they are expected to return to their usual shopping frequencies. In this study, we find that stores with an unfavorable price image tend to lose store visitors in the long run.

Fifth, to prevent a price war escalation, it may be a good idea first to analyze consumer responses when one market player begins to cut prices. If purchase behavior changes only modestly or temporarily, it may be better to focus on marketing-mix instruments other than price to win back customers. If the changes are strong, there is little resort other than to respond by offering price reductions as well, possibly spiraling down to a price war.

Sixth, channel power is a major asset when a retailer is involved in a price war. In the Dutch price war, Albert Heijn initiated the price war when it still had market leadership and was widely regarded as offering superior service and quality. As such, this situation is consistent with the power transition paradigm (Organski 1968); that is, the market leader launches a preemptive strike while it is still powerful (i.e., before most shoppers have lost interest). Because the chain had and has the highest market share, it represents a major outlet for many manufacturers, which they cannot afford to lose. As result, Albert Heijn could divert a major part of its loss in margin (due to reduced consumer prices) to its suppliers. Edah, a price war casualty, probably suffered from both low channel power and a lack of cost leadership (Rao, Bergen, and Davis 2000).

Seventh, it seems particularly unwise to provoke competitors with a competitor-focused goal, such as becoming less expensive than the market average, as Albert Heijn did at the start of the price war. Instead, it seems better to focus on the savings for consumers.

Finally, retailers should consider the market characteristics that may moderate the consequences of the supermarket price war we found in this study. The negative market-level consequences of the price war may be related to the grocery category, whose primary demand appeared to be price inelastic. Overall spending in the category may increase when the price war brings the product within reach of large new consumer segments (e.g., when air travel, then computers, and finally printers became inexpensive enough for most Westerners).

Policy Implications

The scope of price war consequences differentiates them from periods of intense price promotions (Heil and Helsen 2001). The Dutch supermarket price war has incited a nationwide discussion on setting minimum prices and competitive regulations, right up to the Dutch parliament (Baarsma and De Nooij 2005). Such a public debate is rather new to antitrust legislation, which has traditionally focused on a lack of competition and tends to ignore “too much competition” (e.g., in the form of price wars). For example, in defense of a laissez-faire approach, Baarsma and De Nooij (2005) argue that law enforcers cannot invoke Article 2 of the European Treaty, which prohibits the use of unreasonably low prices to drive out competition, because there is no evidence of intent to achieve this (though in reality, the Dutch supermarket price war drove out one chain, Edah). Such arguments reflect a strong belief in the economic rationality and foresight of managers, which may not be supported by the growing literature on managerial biases in pricing (e.g., Nijs, Srinivasan, and Pauwels 2007), competitive overreaction (Leeflang and Wittink 1996), and escalation of commitment (Ghemawat 1991). However, in the Dutch situation, there was no political majority to implement legislation to prevent price wars.

Limitations and Further Research

This study has several limitations, providing leads for further research. Our data come from one price war in one country; further studies are needed to establish whether our findings generalize to other price war situations. For example, how will consumer spending respond in a more price-elastic market? We model cross-chain effects with the correlated intercepts and error terms in the multivariate store visit and spending models. Although further research could analyze how each competitor's marketing-mix instrument price has a different impact, incorporating explicit cross-instrument effects would greatly complicate the already strenuous model estimation. In the computation of weekly prices, the household-specific basket weights are the same across stores. However, a household may buy a specific subset of the basket in one store and another subset in another store. Thus, there might be a temptation to use store-specific weights. The reason we chose not to follow this route is that it would lead to an endogeneity problem; the dependent variable (choice) is used to construct the independent variable. In relation to this point, another avenue for further research would be a detailed investigation of differences across households in terms of changes in basket content. Furthermore, we specify interactions for the moderating effects of the price war on price (image) sensitivity. An extension to stochastic time-varying parameters (e.g., Van Heerde, Mela, and Manchanda 2004) would be a worthwhile endeavor (though it would also severely stretch model estimation). Finally, we model prices as exogenous in relation to household decisions on store visits and spending because it seems much more likely that chains base their prices on competition than on unobserved individual-level demand shocks (for a similar argument, see Erdem, Imai, and Keane 2003). Incorporating endogenous prices and complicated feedback loops would allow for a quantitative analysis of the antecedents and momentum of a price war. Despite these limitations, our analysis of the Dutch supermarket price war generates valuable insights into an important and timely marketing phenomenon and points to exciting possibilities for further research.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.