Abstract

Firms are increasingly outsourcing new product development (NPD), yet little is known about the financial performance implications of this decision. An empirical test shows that there is considerable variation in the performance implications of NPD outsourcing. The authors develop a contingency framework to explain when taking a minority equity participation in the outsourcing provider versus selecting a provider to whom the outsourcing firm has outsourced NPD in the past (i.e., prior tie selection) may increase the outsourcing firm's performance. They find that the superior governance mechanism depends on two forms of uncertainty: technological uncertainty and cultural uncertainty.

Keywords

Firms have long outsourced some of the activities previously performed in-house to independent, outside firms. What began as the outsourcing of peripheral functions, such as data entry or payroll processing, has evolved into the outsourcing of more strategic activities, such as new product development (NPD). Interest in outsourcing NPD activities is growing among firms in industries as diverse as automotive, electronics, pharmaceuticals, and consumer packaged goods, to name just a few (Carson 2007).

Despite the increased popularity of NPD outsourcing, many NPD outsourcing arrangements may not deliver the expected benefits. Barragan et al. (2003) describe a multinational computer manufacturer whose management worried that the high rate of technological change could reduce its provider's ability to deliver an innovative solution. Siemens faced problems of a different nature, with some of its NPD outsourcing providers being stubborn and unwilling to adjust technical specifications and others acting against Siemens' strategic interests by leaking knowledge (Cui et al. 2009).

As alluded to in the preceding examples, the disappointing results of outsourcing NPD may have their roots in the outsourcing provider's low ability to perform (adverse selection problem) and/or low motivation to perform (moral hazard problem). With regard to ability, outsourcing providers in an NPD context must be able to bring a creative solution to the table (Carson 2007). In addition, they must be able to transfer the developed knowledge back to the outsourcing firm. Without knowledge transfer from the provider to the outsourcing firm, outsourcing firms lose touch, erode critical knowledge-based capabilities, and jeopardize their potential for organizational learning (Mohr and Sengupta 2002), which may place their future performance on the line (Gilley and Rasheed 2000).

Even highly capable outsourcing providers may fail to make a sufficient effort. That is, the outsourcing of NPD may also create concerns regarding the outsourcing provider's motivation to develop and transfer knowledge. The costs of safeguarding against the outsourcing provider's potentially opportunistic behavior are often overlooked or underestimated at the time outsourcing contracts are signed (Williamson 2008). A Deloitte Consulting (2005, p. 17) survey of the world's largest organizations reports that nearly half these firms identified hidden costs as a serious problem when managing outsourcing relationships.

In light of the aforementioned ability and motivation concerns, a critical question is how firms can design their NPD outsourcing deals to alleviate these concerns and to reap the benefits of NPD outsourcing. We contribute to answering this question in three ways. First, we study two governance mechanisms—one formal and one informal—that firms can use to reduce ability and motivation concerns when outsourcing NPD. An important formal governance mechanism is taking a minority equity stake in the outsourcing provider (Kale and Puranam 2004). An important informal governance mechanism is selecting a provider to whom the outsourcing firm has outsourced NPD in the past—that is, prior tie selection (Parkhe 1993). Although prior tie selection has been studied previously, the research focus has been on peripheral outsourcing contexts in which knowledge plays a moderate role, if any (Stremersch et al. 2003, p. 347). The literature on minority equity participation is scant in general, despite its increasing use in interfirm collaborations (Folta and Miller 2002, p. 77).

Second, we study the performance implications for the outsourcing firm of using a prior tie or a minority equity stake to govern the outsourcing relationship. The (descriptive) literature has been mainly concerned with describing firms' choices to deploy these mechanisms and has focused much less on their (normative) performance consequences. According to evolutionary economics, descriptive studies have normative value because firms imitate successful firms such that, after some time, all firms converge toward optimal behavior (Anderson 1988). However, the extant literature on the drivers of these mechanisms reports conflicting results, indicating a lack of convergence in behavior. As a consequence, investigations into the determinants of these governance choices may reveal little about their actual influence on performance. Against this backdrop, we link NPD outsourcing to a financial metric of performance that is highly relevant to managers today: the stock market reaction around the outsourcing announcement date (Srinivasan and Hanssens 2009). This is a forward-looking measure that reflects investors' consensus forecast of the change in the long-term value of the firm attributable to the event (Gielens et al. 2008).

Third, we study when one governance mechanism is superior to the other. We theorize and test whether the performance implications of minority equity participation and prior tie selection in an NPD outsourcing arrangement depend on the technological and cultural uncertainties the outsourcing firm faces. We argue that the two types of uncertainty create different ability and motivation concerns and that minority equity participation and prior tie selection differ in their capacity to alleviate these concerns. Our analysis of these two governance mechanisms and their performance consequences under two types of uncertainty may help resolve some of the confusion in the literature regarding the relationship between uncertainty and governance.

Uncertainty, Governance, and Performance

A distinctive characteristic of all interfirm relationships is that partners must not only deal with external uncertainty in their environment but also deal with uncertainty internal to the exchange. External uncertainty is the volatility or unpredictability of the environment in which firms operate. In the context of NPD outsourcing, an important form of external uncertainty is technological uncertainty (Stremersch et al. 2003), the uncertainty arising from rapid and unpredictable changes in technology due to new inventions or discoveries. Internal uncertainty is the equivocality in understanding the exchange partner. In an international setting, a particularly potent form of internal uncertainty is cultural uncertainty. We define cultural uncertainty as the uncertainty extending from cultural differences between the partners. Although coping with cultural uncertainty has been recognized as complicated and costly, it is important to outsourcing success (Deloitte Consulting 2005).

We distinguish two intermediate governance mechanisms that firms can use to manage these two types of uncertainty when outsourcing NPD. Although a multitude of organizational forms fall within the broad rubric of “intermediate forms, ” we focus on one formal and one informal governance mechanism—namely, minority equity participation and prior tie selection. 1 Minority equity participation is a formal, authority-based control mechanism and refers to a “direct minority investment, where one party takes an equity position of less than 50 percent of its partner” (Folta 1998, pp. 1007–1008). An important informal governance mechanism is prior tie selection, the selection of a provider with whom the outsourcing firm shares a prior tie (Parkhe 1993). Informal or relational governance modes are typically open-ended relationships with no predetermined termination points. The means through which informal governance mitigates uncertainty hazards are both economic and sociological (Poppo and Zenger 2002). Economists emphasize expectations of payoffs from future cooperative behavior that prompt cooperation in the present (Axelrod 1984). In their view, if trust develops, it is carefully calculated. Sociologists emphasize shared values that emerge from a history of repeated exchanges embedded in social relationships (Uzzi 1997). Despite differences, both economists and sociologists argue that “repeated exchange provides information about the cooperative behavior of exchange partners that may allow for informed choices of who to ‘trust’ and who not to trust” (Poppo and Zenger 2002, p. 710).

Following Carson (2007), we exclude equity joint ventures and arrangements in which the outsourcing firm takes a majority equity position in the provider. Because equity joint ventures involve the creation of new entities, they “should not be seen as hybrids of market and hierarchy but instead as joint hierarchy” (Hennart 2010, p. 263; see also Gulati and Singh 1998). Majority equity stakes convert an external partner into a legal subsidiary, which reflects a step from hybrid to hierarchy (Folta 1998, p. 1015). This is also borne out by our data: None of the outsourcing announcements that we retrieved mentioned joint ventures or majority equity stakes.

On the normative side, we were unable to find studies that test the performance implications of minority equity participation or prior tie selection under technological and cultural uncertainty. On the descriptive side, the literature that describes firms' choices to deploy these mechanisms lacks convergence. First, with regard to technological uncertainty, Folta (1998) shows that firms are more likely to take a minority equity stake in their partner than to acquire the partner when technological uncertainty increases, while Steensma et al. (2000, p. 963) do not find an effect of technological uncertainty on firms' propensity to use equity ties in alliances. Heide and Weiss (1995) report that technological uncertainty stimulates the selection of a familiar partner firm. Similarly, Poppo and Zenger (2002) find that technological uncertainty encourages relational governance. In sharp contrast, Heide and John (1990) find that technological uncertainty decreases expectations of continuity.

With regard to cultural uncertainty, Pan (1996) finds that firms that enter China are less likely to opt for a minority equity stake, compared with equal or majority equity ownership, as cultural distance increases. Gatignon and Anderson (1988) report a similar preference for majority equity participation or full ownership over minority equity participation for U.S. firms that enter culturally distant geographical markets. In contrast, Hennart and Larimo (1998) and Pak and Park (2004) find that cultural distance increases firms' preference for partial rather than full equity. 2 Zhang, Cavusgil, and Roath (2003) hypothesize but do not find that cultural differences between the parties foster relational governance.

Many empirical studies on minority equity participation should be interpreted with care, for the following reasons: (1) They do not compare minority equity participation with nonequity arrangements but with full equity arrangements, and/or (2) they do not distinguish minority equity participation from other forms of partial equity participation (e.g., majority equity participation, joint ventures). For example, both Hennart and Larimo (1998) and Pak and Park (2004) compare partial equity with full equity, with partial equity ranging from 10% to 95% in the former study and from 0% to 95% in the latter.

The lack of normative studies on the performance implications of prior tie selection and minority equity participation under technological and cultural uncertainty is surprising given that explaining firm performance represents one of the fundamental questions in the marketing strategy field. Descriptive research in this area cannot be used to infer normatively “correct” decisions. Indeed, the limited evidence regarding the effects of technological and cultural uncertainty on the minority equity participation and prior tie selection decisions is inconsistent, which suggests that the market has not yet adapted to optimal practice and that organizational decision makers are still ill-informed.

Hypotheses

We examine how the performance consequences of minority equity participation and prior tie selection in an NPD outsourcing arrangement depend on the technological and cultural uncertainties the outsourcing firm faces. 3 We develop our predictions in line with the arguments that technological uncertainty and cultural uncertainty present different ability and motivation concerns and that minority equity participation and prior tie selection differ in their capacity to alleviate these concerns. Table 1, which we use as a guiding tool for developing our hypotheses, highlights the different ability and motivation concerns created by technological uncertainty and cultural uncertainty when outsourcing NPD. To arrive at our hypotheses, we adopt an insight from expectancy theory that was originally developed in the organizational behavior literature (Vroom 1964) and that has subsequently been corroborated in marketing (Oliver 1974): When either ability or motivation is low, performance is low. Put differently, for a governance mechanism to increase performance, it must address both ability and motivation concerns.

We define “prior tie selection” as the selection of a prior tie that is of the same type (i.e., a prior NPD outsourcing tie). Hereinafter, we refer to “prior NPD outsourcing tie” as “prior tie.”

MOTIVATION AND ABILITY CONCERNS UNDER TECHNOLOGICAL UNCERTAINTY AND CULTURAL UNCERTAINTY

Managing Technological Uncertainty When Outsourcing NPD

Technological uncertainty makes it difficult to accurately forecast future technical requirements. It creates ability concerns because the outsourcing firm may not be sure about the true value-creating potential of the outsourcing provider's technology (Kale and Puranam 2004, p. 89). Technological uncertainty also creates motivation concerns because the uncertainty with regard to the direction of technological change may reduce the provider's loyalty (Heide and John 1990).

Minority equity participation and technological uncertainty

Minority equity participation may alleviate the ability concerns that result from technological uncertainty in two ways. First, in technologically uncertain environments, the outsourcing provider may have difficulty securing external financing at reasonable terms (Fee, Hadlock, and Thomas 2006, p. 1222). Minority equity participation provides a direct infusion of cash to the outsourcing provider. As such, it serves as a financial stimulus that increases the outsourcing provider's ability to develop innovative solutions that advance the technological frontier (Folta and Miller 2002, p. 79). For example, in their drug development outsourcing arrangements, pharmaceutical firms such as Eli Lilly make small investments to enable their outsourcing providers to make technological progress in a technologically turbulent field (Ernst & Young 2010).

Second, if an outsourcing firm does not know which provider is technologically superior due to technological uncertainty, it may be beneficial to remain flexible (Heide and John 1990). At the same time, when the technology in question is potentially critical to its business goals, the outsourcing firm may need to prevent rivals from gaining access to it (Kale and Puranam 2004). Minority equity participation can provide this balance. By taking a minority equity position in the outsourcing provider, “the sourcing firm [obtains] a certain degree of … exclusivity over the technology” (Kale and Puranam 2004, p. 90). Even at low levels of equity participation, the outsourcing firm's rivals are discouraged from creating relationships with the same provider because the outsourcing firm may use its minority equity position to further its own interests at their expense (Kale and Puranam 2004, p. 80). A minority equity position also provides the outsourcing firm with enough flexibility to move quickly to a majority or full equity position as technological uncertainty is resolved (Folta and Miller 2002). This “real option” becomes more valuable as uncertainty about the value of the technology increases (Kale and Puranam 2004, p. 89).

Minority equity participation can also address the motivation concerns created by technological uncertainty. Minority equity participation provides firm-level control, when the outsourcing firm gains a seat on the board of directors, or project-level control, through the creation of oversight committees that periodically meet to monitor the progress of the NPD activity being outsourced (Robinson and Stuart 2007). Through these rights of control, minority equity participation enables the outsourcing firm to manage unexpected technological contingencies that cannot be fully programmed in advance because of their unfolding nature (Pisano 1989). The likelihood of adverse partner behavior (e.g., the provider reneging on its agreements to improve the terms of trade at the outsourcing firm's expense) is correspondingly lower (Kale and Puranam 2004, p. 82). Because minority equity participation helps address the ability and motivation concerns associated with technological uncertainty, we hypothesize the following:

When technological uncertainty is higher (lower), minority equity participation leads to more (less) favorable performance consequences of outsourcing NPD.

Prior tie selection and technological uncertainty

An important concern of working with a familiar as opposed to a new NPD provider in a technologically uncertain environment is that a familiar provider is less likely to be able to generate creative and novel NPD solutions (Grayson and Ambler 1999; Moorman, Zaltman, and Deshpandé 1992). It has long been argued that for accessing creative and novel ideas, firms should look not only beyond the boundaries of their firm but also beyond their existing partners (Heide and Weiss 1995). Similarly, Wuyts, Verhoef, and Prins (2009) find that customer firms in information service markets prefer not to work with prior partners for services when creativity is key. They attribute this finding to cognitive biases associated with working with known partners (selective perception, confirmation bias): Their panel discussion with 70 industry experts underscores that prior partners are less likely to provide surprising, novel solutions. The lower creativity of a familiar outsourcing provider is a hindrance when facing technological change.

The literature is divided as to whether prior tie selection can alleviate the motivational problems associated with technological uncertainty. On the one hand, researchers have found that social norms foster mutually agreeable outcomes in the face of renegotiations due to highly consequential disturbances, such as high levels of technological change (Poppo and Zenger 2002, p. 722). On the other hand, the shared history between the outsourcing firm and its provider may reduce the provider's incentives to put much thought in the development project beyond previous ideas and insights (Baiman and Rajan 2002). This lack of motivation may cause the provider to opportunistically evade necessary adaptations to a changing environment (Wathne and Heide 2000; Wuyts and Geyskens 2005).

In summary, whereas prior partners are less able to provide creative, novel NPD solutions in the face of technological uncertainty, the literature is inconclusive with regard to the effectiveness of prior tie selection in alleviating motivation concerns associated with technological uncertainty. Because both ability and motivation are necessary conditions for performance, we hypothesize the following:

When technological uncertainty is higher (lower), prior tie selection leads to less (more) favorable performance consequences of outsourcing NPD.

Managing Cultural Uncertainty When Outsourcing NPD

When cultural uncertainty is high, the companies may be “too far apart in their ways of doing things to understand each other and connect to each other effectively” (Doz 1996, p. 66). This may lead to two adverse consequences, as summarized in Table 1. First, on the ability side, cultural uncertainty may cause honest (rather than deceitful) misunderstandings, which may hamper interfirm knowledge transfer (Simonin 1999). Second, on the motivation side, the increased difficulty of interpreting the outsourcing provider's actions (Gong 2003, p. 729) creates a situation in which the outsourcing provider has an information advantage over the outsourcing firm. Such information asymmetry enables the outsourcing provider to act opportunistically without easily being detected (Wathne and Heide 2000).

Minority equity participation and cultural uncertainty

We argue that minority equity participation cannot solve the ability and motivation concerns that arise when cultural uncertainty is high. With regard to the outsourcing provider's ability, cultural uncertainty may lead to misunderstandings, which can turn into key obstacles to interfirm knowledge transfer (Simonin 1999). Extant research has argued that the mutual understanding required for effective knowledge transfer should be achieved at the lower echelons of the firms (e.g., engineers, scientists), where daily interaction takes place (Bierly and Coombs 2004, p. 196). Equity participation, in contrast, concentrates interfirm communication at high strategic levels, such as directory boards or management committees (Gulati and Singh 1998; Kale and Puranam 2004). This is also reflected in Moorman's (1995, p. 322) observation that formal structures “are less likely to develop the person-to-person systems crucial to information processes.” Because minority equity participation does not resolve the misunderstandings that are caused by cultural uncertainty, it would be redundant and therefore inefficient.

Minority equity participation cannot alleviate the motivational problems associated with cultural uncertainty. As cultural uncertainty increases, it becomes more difficult for the outsourcing firm to interpret the outsourcing provider's actions (Gong 2003), which creates information asymmetry in that the outsourcing provider has better insight into its own actions and performance than the outsourcing firm has. When it is difficult to accurately interpret and assess the partner's actions, opportunism is difficult to detect (Wathne and Heide 2000, p. 42), making it difficult and inefficient to use authority as a mechanism to control an opportunistically inclined partner's behavior. The difficulty of detecting opportunism as a result of information asymmetry further heightens the risk of using the authority mechanism inappropriately (i.e., to control an outsourcing provider who is not inclined to behave opportunistically). The outsourcing provider may interpret this as a signal of distrust, which may paradoxically increase rather than decrease opportunistic behavior because distrust begets distrust (Bradach and Eccles 1989). Therefore, we propose the following:

When cultural uncertainty is higher (lower), minority equity participation leads to less (more) favorable performance consequences of outsourcing NPD.

Prior tie selection and cultural uncertainty

The ability problem created by cultural uncertainty pertains to honest (undeceitful) misunderstandings that make knowledge transfer difficult. Differences in organizational NPD routines between culturally distant companies complicate information sharing. Repeated interaction with the same provider establishes modes of communication (Zollo, Reuer, and Singh 2002) and creates a common language for discussion (Hoetker and Mellewigt 2009). A common language is more comprehensible when it is function specific (i.e., when it results from repeated interaction in the same functional domain; Moenaert and Souder 1996, p. 1593). In the context of outsourcing NPD, a prior NPD tie thus facilitates NPD-related communication. As partners learn through prior interaction how their cultural differences may be overcome or even constructively combined, knowledge sharing becomes more efficient (Gulati, Lavie, and Singh 2009).

Cultural uncertainty also creates motivation concerns. As we explained previously, the outsourcing firm faces difficulties in accurately interpreting and assessing the outsourcing provider's actions when cultural uncertainty is high (Gong 2003), which may stimulate the outsourcing provider to act opportunistically (Wathne and Heide 2000). Prior tie selection reduces the risk of deceitful communication in case of cultural uncertainty. By sharing a prior tie, the outsourcing firm and its provider have tacitly developed an understanding of norms about appropriate behavior (Doz 1996; Dyer and Singh 1998). The social norms that result from a prior tie enhance social identification and, in turn, reduce deceitful communication by the outsourcing provider (Dyer and Singh 1998; Puranam and Vanneste 2009). In contrast, when there is no history of prior ties between the outsourcing firm and its provider, each firm may project onto the other a set of interpretations borrowed from its own cultural context, often incorrect, resulting in greater information asymmetry and more motivational concerns (Doz 1996). Because prior tie selection addresses both the ability and motivation concerns that arise from cultural uncertainty, we hypothesize the following:

When cultural uncertainty is higher (lower), prior tie selection leads to more (less) favorable performance consequences of outsourcing NPD.

Methodology

Event Study Methodology

Our performance metric is shareholder value. We examine the effect of outsourcing NPD on shareholder value using the event study methodology. A company's stock price reflects the discounted value of all future cash flows that are expected to accrue to the firm. According to the semistrong version of the efficient market hypothesis, all publicly available information about a firm is reflected completely in its stock price. When new information becomes available, investors update their expectations and react immediately by buying or selling stock, thereby bidding the stock price up or down. Thus, if investors expect that NPD outsourcing will affect firm performance by increasing (decreasing) future cash flows, they react to the announcement by buying (selling) stocks, which positively (negatively) affects the firm's stock price.

Stock price reactions are of interest not only because they guide the decisions of top managers but also because they allow for an inference of cause and effect in a quasi-experimental setting (Srinivasan and Hanssens 2009). Specifically, the event-study approach enables us to isolate individual outsourcing events—for which different governance mechanisms may have been chosen—and study their impact on stock prices, while the effects of other events that may have affected stock prices are randomized (because the NPD outsourcing events are announced on different dates). In contrast to accounting measures, which evaluate “historical” performance indicators, the stock market reaction is forward looking; it reflects the stock market's best estimate of the change in the long-term value of the firm (Gielens et al. 2008). This is especially important in our context because the loss of critical knowledge-based capabilities that may result from NPD outsourcing may take several years before fully translating into bottom-line performance.

The percentage change in the stock price of firm i between day t − 1 and day t is the daily stock return Rit. Here, Rit reflects investors' expectations of the performance impact of the information that became available between t − 1 and t. The event study methodology compares the observed stock return Rit on the event day with E(Rit), the return that would be expected if the event had not taken place. To estimate E(Rit), we use the market model. According to this model,

where Rmt is the market index return in the home country of the outsourcing firm on day t and

Because the event day differs for each firm in our sample, error terms across market model equations are unlikely to be correlated (Jain 1982, p. 219). A Breusch-Pagan test for the null hypothesis that errors across equations are not correlated confirms that there is no loss of information when we use ordinary least squares equation by equation.

where ARit provides an unbiased estimate of the future earnings generated by the event.

Thus far, we have considered the situation that there is no information leakage before the event day and that all information is completely disseminated during the event day. In practice, these assumptions may be violated (Gielens et al. 2008). To account for leakage (for t1 time periods before the event) and dissemination over time (for t2 time periods after the event), we aggregate firm i's abnormal returns over the event period [–t1, t2] into a cumulative abnormal return (CARi) to draw overall inferences for the event of interest:

Because the event study is conducted over N events, this CAR can be averaged into a cumulative average abnormal return (CAAR):

The extent of information leakage and dissemination, and thus the length of the event window [-t1, t2], is an empirical issue and is determined by selecting the most significant CAAR from several calculated CAARs for different event windows (see Swaminathan and Moorman 2009). To test the significance of the CAARs, we use the Patell (1976) statistic.

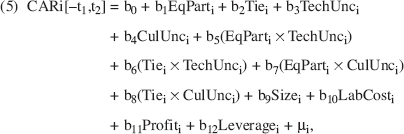

We test our hypotheses on the performance differences between outsourcing firms through a regression analysis on the (standardized) CARs 5 :

We use the standardized CARs as dependent variable to reduce hetero - skedasticity problems that may arise when the estimated variances of the market model residuals vary across events (Jain 1982; for similar practice, see Geyskens, Gielens, and Dekimpe 2002; Gielens et al. 2008). The standardized CARi is the CARi divided by the standard deviation of the estimation-period abnormal returns.

where EqPart is minority equity participation, Tie refers to prior tie selection, TechUnc is technological uncertainty, and CulUnc refers to cultural uncertainty. We include Size, LabCost, Profit, and Leverage to control for the outsourcing firm's size, for labor-cost differences between the country of the outsourcing firm and the country of the outsourcing provider (the primary rationale for most firms to engage in outsourcing), and for the outsourcing firm's profitability and leverage (financial information that may influence stock returns; Luo 2007). We use mean-centering before forming the interactions to ease interpretation. To control for unobserved heterogeneity between countries, industries, and calendar years, we add dummy variables for each country, industry, and announcement year to Equation 5. Because the number of observations in our sample is too low to include all dummy variables, we tested each dummy separately and retained only the significant ones. In the interest of brevity, we do not report the dummies in the model or the tables. Eleven firms made multiple outsourcing announcements, which may give rise to correlated errors. Therefore, we estimate Equation 5 with GEEs (generalized estimating equations).

Sample

We composed a sample of NPD outsourcing announcements by searching the LexisNexis, SDC Platinum, and Factiva databases over a period of 15 years (1994–2008). This resulted in an initial sample of 159 announcements. We removed 36 announcements because the outsourcing firm was not listed on the stock market and another 7 announcements because stock price information was missing around the event day. In 16 cases, the announcement included information about other firm events (e.g., firm sales, earnings), or another announcement concerning the firm appeared within the three-day window around the announcement. We removed these 16 announcements to minimize the presence of confounding effects.

This resulted in a sample of 100 announcements that unequivocally reflect stand-alone NPD outsourcing decisions (i.e., none of the announcements pertain to the continuation of an arrangement after an initial trial period). The outsourcing firms in our sample span 15 countries and 17 industries. The majority of announcements were made by outsourcing firms from the United States (55%), followed by Japanese (7%) and Canadian (6%) firms. The outsourcing providers come from a wide variety of countries, including Australia, Belgium, Canada, China, Finland, France, Germany, Hungary, India, Italy, the Netherlands, South Africa, Taiwan, the United Kingdom, and the United States.

Measurement and Descriptives

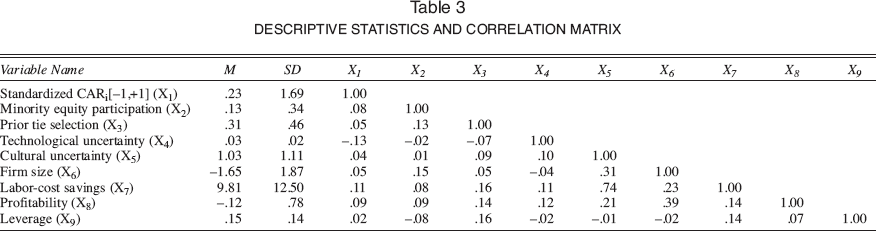

We collected information on stock prices and marketwide indexes from the Center for Research in Security Prices and Datastream databases. We use these data to calculate the daily returns of firm i, Rit, and the market returns, Rmt. Table 2 presents a summary description of all measures for the independent and control variables, and Table 3 provides descriptive statistics and correlations.

EXPLANATORY VARIABLES AND DATA SOURCES

Only two announcements indicated the percentage of minority equity participation. The equity participation taken by the outsourcing firm in the outsourcing provider in these two cases equaled 9% and 18%. In all other cases, the announcement referred to a minority equity position but did not disclose the percentage of equity participation, preventing us from using a continuous measure.

Because technological uncertainty arises from changes in technology due to new inventions and discoveries (Sutcliffe and Zaheer 1998) and because the latter are inherently difficult to predict, R&D investments in technologically uncertain environments are inherently less stable over time. Therefore, we measure technological uncertainty as “the magnitude of changes in research and development (R&D) activity” (Slater and Narver 1994, p. 51).

DESCRIPTIVE STATISTICS AND CORRELATION MATRIX

Results

On the announcement day, outsourcing firms experience on average a .20% increase in stock returns. Of all windows surrounding the event day, the one from −1 to +1 shows the most significant CAAR: CAAR[-1, +1] = .45% (p < .05). However, there is considerable variation in the performance implications of NPD outsourcing across firms. While 54% of the outsourcing firms show a positive abnormal return over the event window (average CAAR = 3.20%), investors negatively evaluated 46% (average CAAR = −2.79%). To understand this cross-sectional variation, we estimated Equation 5 with the individual firms' CAR[-1, +1] as dependent variable.

Because firms may choose governance mechanisms in response to the uncertainty they are facing, we first tested for potential endogeneity of minority equity participation and prior tie selection. 6 A Durbin-Wu-Hausman test indicates that endogeneity of the governance variables is not an issue in our context (χ2(6) = 3.65, p > .70). Notably, neither technological uncertainty nor cultural uncertainty significantly affected minority equity participation and prior tie selection (ps > .10).

In a first-stage probit model, we regress the potentially endogenous governance mechanisms (i.e., minority equity participation and prior tie selection, respectively) on the same variables that appear in Equation 5. As excluded instrumental variables, we use the outsourcing firm's research-and-development (R&D) intensity, intellectual property rights protection in the country of the outsourcing provider, and firm age. R&D intensity is indicative of exploration and may be a distinctive characteristic of firms that take options on external technologies through minority equity stakes. Intellectual property rights protection facilitates appropriating value from NPD investments, thus stimulating equity investments. We include firm size because older firms are more likely than younger firms to have accumulated a network of prior partners from which they can choose. A Sargan test confirms that our instruments are valid.

Table 4 presents the results. 7 To obtain more insight into the nature of the interaction effects, we performed a series of simple slope analyses (Aiken and West 1991), which Figure 1 depicts. The simple slope tests identify the direction and magnitude of the effects of minority equity participation and prior tie selection at specific levels of technological uncertainty and cultural uncertainty, namely, one standard deviation below the mean (low) and one standard deviation above the mean (high). 8

All variance inflation factors are well below 5 (maximum value = 3.20), indicating that multicollinearity is not likely to be a problem.

In the case of cultural uncertainty, the low level corresponds to no cultural uncertainty (i.e., when NPD is outsourced to a domestic partner). We held all continuous covariates constant at their mean value and set all dummy variable covariates to zero when deriving Figure 1.

DRIVERS OF THE STOCK MARKET REACTION TO OUTSOURCING NPD

p < .10.

p < .05.

p < .01.

We use one-sided tests for hypothesized effects, two-sided tests for non-hypothesized effects.

For simplicity of presentation, the results for the country, industry and year dummies are not reported in the table.

THE INTERACTIVE EFFECTS OF GOVERNANCE MECHANISMS AND UNCERTAINTY ON FIRM PERFORMANCE

As hypothesized (H1), we find a positive interaction effect between minority equity participation and technological uncertainty (b5 = 56.98, p < .05). Figure 1, Panel A1, illustrates that when technological uncertainty is low (i.e., one standard deviation below the mean), minority equity participation is not significantly related to the performance consequences of outsourcing NPD (blow = –.75, not significant [n.s.]). When technological uncertainty is high (i.e., one standard deviation above the mean), minority equity participation is positively associated with the performance consequences of outsourcing NPD (bhigh = 1.96, p < .01). Thus, H1 is partially supported. In sharp contrast, we find a negative interaction effect between prior tie selection and technological uncertainty (H2: b6 = −67.61, p < .01). Figure 1, Panel A2, shows that prior tie selection is positively related to the performance consequences of outsourcing NPD when technological uncertainty is low (blow = .88, p < .05), whereas prior tie selection is negatively related to performance when technological uncertainty is high (bhigh = −2.34, p < .01). Thus, we find support for H2.

As expected (H3 and H4), we find a negative interaction effect between minority equity participation and cultural uncertainty (b7 = −.73, p < .05) and a positive interaction effect between prior tie selection and cultural uncertainty (b8 = .87, p < .01). According to Figure 1, Panel B1, minority equity participation is positively related to the performance consequences of outsourcing NPD when cultural uncertainty is low (blow = 1.36, p < .05) but does not affect performance when cultural uncertainty is high (bhigh = −.21, n.s.). In contrast, and as we show in Figure 1, Panel B2, prior tie selection negatively affects performance when cultural uncertainty is low (blow = −1.63, p < .01). At high cultural uncertainty (i.e., one standard deviation above the mean), the effect of prior tie selection is positive, as we expected, but not statistically significant (bhigh = .23, n.s.). The positive effect of prior tie selection under cultural uncertainty only becomes significant (p < .10) when cultural uncertainty exceeds a threshold of 1.56 times the standard deviation above the mean. This includes, among others, outsourcing relationships between U.S. outsourcing firms and Chinese providers and between Swedish outsourcing firms and Indian providers. Thus, H3 and H4 are partially supported.

Robustness Checks

Using a Different Model to Estimate Expected Returns

Our dependent measure is the difference between the actual return and the expected return, which we estimated using the market model. To assess the robustness of our findings to the type of model used to estimate the expected returns, we reestimated the expected returns using the world-market model, which adjusts not only for domestic market movements but also for global market movements and for changes in exchange rates (Park 2004). Our results are robust to this alternative specification.

Ruling Out Corrections in the Long Run

We eliminated the possibility that the initial stock market evaluation was just a short-term effect that was corrected in the long run. We calculated three-month, six-month, and one-year long-term effects using the buy-and-hold abnormal returns and Ibbotson's returns across time and securities models. We found no effect on long-term abnormal returns (ps > .10), suggesting that the stock market is reasonably efficient. Thus, the abnormal returns to NPD outsourcing accrue in the short-term window, and there are no corrections in the long run. 9

Our dependent variable is the short-term CAR accruing from the NPD outsourcing announcement to the outsourcing firm. Although this measure materializes in the short run (consistent with the efficient market hypothesis that a firm's stock price immediately reflects all new information), conceptually, this measure reflects the stock markets' best estimate of the change in the long-term value of the firm. Significant long-term abnormal returns, as computed by the buy-and-hold abnormal returns or Ibbotson's returns across time and securities methodology, reflect that the stock market was not efficient but rather over- or underreacted to the announcement. They do not connote long-term firm performance.

Removing Potential Outliers

We examined the effects of removing potential outliers (±5th, 10th, and 15th percentile of residuals). Our results are robust to these alternative specifications.

Including Additional Interaction Effects

Minority equity participation and prior tie selection are not necessarily mutually exclusive but can be used in combination, in which case they can reinforce or obstruct each other. 10 To explore this formally, we reestimated our model including an interaction effect between minority equity participation and prior tie selection. This interaction was not significant (p > .10), and it did not substantially change the significance of the hypothesized effects Table 4 reports. In a similar vein, we reestimated our model after including an interaction effect between technological uncertainty and cultural uncertainty. This interaction was also not significant (p > .10).

Only 6% of firms in our sample used both mechanisms simultaneously.

Removing Announcements from the Same Firm

There are 11 outsourcing firms in our sample with multiple NPD outsourcing announcements. Therefore, we performed an analysis on a sample in which each outsourcing firm appeared no more than once, by retaining only the first announcements from the repeating firms in our sample. The results remained substantively the same.

Removing Outsourcing Arrangements Subject to Government Restrictions on Foreign Equity Ownership

Our theorizing (H1) posits that a minority equity position may enable outsourcing firms to move to a majority position when uncertainty is resolved regarding the value of the provider's technology. However, the share of equity ownership may be restricted by government regulations and consequently not be left to the choice of the foreign outsourcing firm (Gomes-Casseres 1990, p. 4). Countries and industries differ widely in the extent to which they have restrictions on foreign equity ownership, with, for example, fewer restrictions in manufacturing than in services and fewer restrictions in Eastern Europe and Central Asia than in East Asia and the Pacific (World Bank 2010). To determine whether equity ownership was restricted for each of the countries and industries in our sample, we used the World Bank's foreign equity ownership (FEO) index, which measures the extent of overt statutory restrictions on foreign ownership of equity in new investment projects and on the acquisition of shares (0 = “foreign ownership is completely prohibited, ” and 100 = “full foreign ownership is allowed”). The average FEO score in our sample was a high 90.4, with a median of 100. We examined the effects of removing those observations for which country regulations were most restrictive, based on the 5th, 10th, and 15th percentile on the FEO index. The results remained substantively the same.

Unpacking the Cultural Uncertainty Measure

Our “composite” cultural uncertainty measure captures uncertainty arising from differences in individualism, power distance, uncertainty avoidance, and masculinity between the countries of the outsourcing firm and the outsourcing provider (see Table 2). To understand whether our results are driven by differences in some or all these cultural dimensions, we estimated four additional models in which we replaced our composite cultural uncertainty measure with a measure that was based on only one of the four cultural dimensions. We replicated the significant, negative interaction effect between minority equity participation and the composite cultural uncertainty measure for all but one cultural dimension. For cultural uncertainty arising from power distance differences (i.e., differences in the extent to which hierarchy is culturally accepted), we found an insignificant interaction effect with minority equity participation. Perhaps for power distance, the hypothesized negative effect is offset by a positive effect: Agreeing on a governance mechanism that offers some, but limited, authority—such as minority equity participation—may help reconcile the outsourcing firm and outsourcing provider's different views on authority.

We also replicated the positive interaction effect between prior tie selection and cultural uncertainty for three of the four cultural dimensions, the exception being uncertainty avoidance, for which we found an insignificant interaction. The sentiment among firms that score high on uncertainty avoidance is that “what is different is dangerous, ” whereas the sentiment among firms that score low on uncertainty avoidance is “what is different is curious” (Hofstede 2001, pp. 160–61). Differences in uncertainty avoidance are likely to breed disagreement and dispute between firms (Barkema and Vermeulen 1997). A prior tie may not be effective to address such disputes because the two firms are likely to differ in their preference for a known, former partner (preferred by firms high on uncertainty avoidance) versus a new partner (preferred by firms low on uncertainty avoidance).

Discussion

Our finding that 54% of the NPD outsourcing announcements resulted in positive performance implications counters the still deep-rooted belief that firms should never outsource strategic activities. At the same time, the stock market evaluates 46% of the NPD outsourcing announcements negatively. Our focus is on what influences the expected performance implications of NPD outsourcing decisions.

Academic research in the burgeoning area of NPD outsourcing remains rare, despite Rindfleisch and Moorman (2001, p. 14) encouraging marketing scholars to adopt a broader perspective on NPD issues and examine interfirm cooperation as a source of new product innovations. A recent and notable exception is Carson (2007), who shows that contractual specifications may lead to higher task performance by the outsourcing provider. Carson (2007, p. 63) concludes that “a key area for further research is the detailed study of alternative methods or styles of control.” In particular, “incentives generated through property rights and relational governance forms could be promising methods of control for creative tasks” (p. 63). We address Carson's call for more research on alternative governance mechanisms and study whether and when minority equity participation and prior tie selection may increase firm performance when outsourcing NPD.

The rush toward outsourcing is often ascribed to labor-cost savings. Yet for the firms in our sample, labor-cost savings did not affect outsourcing performance. 11 Rather, we find that outsourcing firms can increase their performance by choosing an appropriate governance mechanism to manage two major types of uncertainty: technological uncertainty and cultural uncertainty. We find that no single governance mechanism is always superior. Instead, minority equity participation and prior tie selection can be double-edged swords, with a performance-enhancing potential that increases under certain conditions but decreases under others.

Our measure of labor-cost savings suffers from the limitation that it is calculated according to the average labor costs across all manufacturing industries in the countries of the outsourcing firm and its provider rather than on industry-specific labor costs. Unfortunately, we did not have access to the latter information.

Technological uncertainty creates ability concerns, in that the outsourcing firm may be unsure about the provider's ability to develop valuable technologies, and motivation concerns, in that the outsourcing provider may be less loyal to the outsourcing firm, thereby decreasing the outsourcing firm's performance. We find that outsourcing firms can hedge against technological uncertainty—and increase the performance consequences of outsourcing NPD—by taking a minority equity stake in the provider. We now return to the computer manufacturer example from the beginning of the article: The computer manufacturer's executives were worried that technological change would reduce the current provider's ability to deliver an innovative solution. Thus, they opted for a transactional, low-control NPD outsourcing arrangement with the firm's provider, so that the company could easily switch to an alternative provider if technological change would indeed reduce the current provider's ability to perform. Unfortunately, this resulted in loss of control over the developed technology and in a competitor appropriating the newly developed knowledge (Barragan et al. 2003). According to our findings, the computer manufacturer would have benefited from taking a minority equity stake in its provider, to balance its desire for flexibility with the need to discourage rivals from creating relationships with the same provider.

While the literature is inconclusive with regard to the effectiveness of prior tie selection under technological uncertainty, it seems to converge on the notion that prior tie selection reduces rather than increases access to valuable external technologies. In the extant marketing literature, several authors have pointed to problems associated with repeated partnering, such as decreased creativity and novelty (e.g., Grayson and Ambler 1999; Moorman, Zaltman, and Deshpandé 1992; Wuyts, Verhoef, and Prins 2009). Using secondary data, we corroborate these survey-based findings and show that the stock market punishes a firm for outsourcing NPD to a provider with which it shares a prior tie when technological uncertainty is high. Prior tie selection restricts the “freshness” of the solutions the outsourcing provider offers, which is worrisome when firms should be responding creatively to technological change.

Cultural uncertainty may complicate knowledge transfer between the outsourcing provider and the outsourcing firm: It may lead to ability concerns in the form of (honest) misunderstandings and to motivation concerns in the form of opportunistic miscommunication. We found support for our arguments that minority equity participation is inefficient in managing the knowledge transfer problems that are created by cultural uncertainty. In contrast, prior tie selection helps create a common language that alleviates the knowledge transfer problems that accompany cultural uncertainty. The simple slope analyses show that firms should select a new rather than a prior partner when outsourcing NPD in a low cultural uncertainty situation. When cultural uncertainty increases, the effect of prior tie selection becomes positive. It reaches significance at high levels of cultural uncertainty, arguably because a known provider is better able and more motivated to share knowledge with a culturally distant outsourcing firm. For example, in one of the less successful NPD outsourcing experiences of Siemens, which we referred to previously, the partner was located far away and had no previous collaboration with Siemens, leading to communication and trust problems. According to our findings, Siemens would have benefited from selecting a culturally distant provider with whom it shared a prior tie or, alternatively, from selecting a less culturally distant partner with whom it did not share a prior tie. In contrast, in one of Siemens' successful NPD outsourcing projects, Siemens has shared a history of collaboration since the 1960s (prior tie) with an outsourcing provider located in East Asia (high cultural uncertainty).

To illustrate the consequences of alternative managerial decisions, we calculate predicted CARs for different governance decisions under low and high levels of technological uncertainty and cultural uncertainty. Low and high levels are represented by one standard deviation below and above the mean (in the case of cultural uncertainty, the low level corresponds to no cultural uncertainty—i.e., when NPD is outsourced to a domestic partner). Table 5 reports the predicted CARs and can be used as a decision matrix for firms when outsourcing NPD.

PREDICTED CARS FOR DIFFERENT GOVERNANCE DECISIONS UNDER TECHNOLOGICAL AND CULTURAL UNCERTAINTY

When both technological uncertainty and cultural uncertainty are low, the choice of minority equity participation and prior tie selection is irrelevant because it does not affect performance. When technological uncertainty is low and cultural uncertainty is high, selecting a familiar provider is the preferred governance approach (CAR = 1.31%). When the outsourcing firm faces a technologically turbulent environment, it can increase its CAR from –.35% to 2.37% by taking a minority equity participation in a domestic outsourcing provider. If this same firm were to offshore to a culturally distant provider, its CAR would reduce from 2.37% to .50%, a 79% drop. Thus, when technological uncertainty is high, selecting a domestic outsourcing provider is preferable to outsourcing to culturally distant providers. Prior tie selection, in contrast, should be avoided at all times when technological uncertainty is high because CARs become as low as −2.03% (when cultural uncertainty is high) and −3.58% (when there is no cultural uncertainty).

A notable observation that stems from our endogeneity analyses is that the selection of governance mechanisms is not influenced by the degree of technological uncertainty and cultural uncertainty. Thus, firms do not behave optimally. We offer two possible explanations. First, for more recent phenomena, such as outsourcing NPD, it takes time before the market adapts to optimal practice (Nelson and Winter 1982). Because NPD outsourcing has only recently become popular, most firms have little or no own prior experiences on which to rely (Deloitte Consulting 2005). In addition, the secrecy surrounding NPD outsourcing deals results in a lack of clear market oversight and further leaves organizational decision makers ill informed. Second, Heide and Weiss (1995, p. 32) suggest that in contexts in which firms cannot rely on a standard set of decision criteria to select a partner, they tend to process limited information and rely on familiarity as a decision heuristic. This insight may explain why one-third of the firms in our sample selected familiar partners, even though prior tie selection negatively affects performance in three of the four conditions depicted in Table 5.

Limitations and Suggestions for Further Research

This study has several limitations, some of which provide worthwhile avenues for further research. First, we were unable to retrieve information on the percentage of minority equity participation. Even though our dummy variable measure is in line with Pan's (1996) observation that the equity participation decision is primarily a categorical rather than a continuous one, it would be useful to replicate our findings for a continuous measure of minority equity participation.

Second, equity arrangements often do not only include “rights of residual claimancy, ” such as the right to buy and sell equity (Folta 1998, p. 1013), but contractual constraints at the time of the initial investment may place an upper limit on the total size of an equity stake that the outsourcing firm can own in its partner (Robinson and Stuart 2007). In the current study, we argue that a minority equity position may alleviate the ability concerns that result from technological uncertainty in multiple ways: (1) by providing a direct infusion of cash to the outsourcing provider, (2) by ensuring more exclusive access to the technology (because rivals will be discouraged from creating relationships with the same provider; Kale and Puranam 2004), and (3) by providing the outsourcing firm with an option to move to majority or full equity ownership as technological uncertainty is resolved (Folta and Miller 2002). Although an upper-limit constraint on the total size of the equity stake is unlikely to affect the first two advantages, it may reduce the option value of the minority equity position. Further research might investigate the extent to which contractual constraints limit the effectiveness of minority equity participation in managing technological uncertainty.

Third, we examined prior tie selection. Because our study is based on secondary data, we were unable to test or control for other types of informal governance. Other informal governance mechanisms, such as trust-based governance or routines-based governance, may have similar contingent effects on performance because researchers have argued that they result from a history of prior ties (for trust-based governance, see Gulati and Singh 1998, p. 791; for routines-based governance, Zollo, Reuer, and Singh 2002, p. 704). Further research exploring the effectiveness of alternative informal governance mechanisms and their role alongside prior ties is warranted.

Fourth, we encourage scholars to investigate the relationship between prior tie selection and minority equity participation. In particular, outsourcing firms that share a prior tie with their outsourcing providers may be more likely to take a minority equity stake in their providers at a later stage. Although we did not find evidence for this in our cross-sectional sample (the correlation between minority equity participation and prior tie selection was insignificant), further research could explore the relationship between prior tie selection and minority equity participation through a longitudinal study that tracks outsourcing relationships from initial relationship formation to dissolution.

Fifth, we examined a prior tie of the same nature (i.e. a prior NPD outsourcing tie). Our findings do not necessarily generalize to prior ties of a different nature. For example, whereas a prior NPD tie is performance-diminishing under high technological uncertainty because of reduced creativity of the outsourcing provider, a prior tie of a different nature (e.g., a prior outsourcing tie in data entry, customer support) may help the firms acquaint themselves with each other better and may actually be performance-enhancing. Further research could contrast the effectiveness of prior ties of the same nature with those of a different nature.

In addition, because the outsourcing providers were often located in countries in which firm-specific information is poorly documented, we were unable to control for characteristics of the outsourcing providers, such as firm size, reputation, or nationality of the chief executive officer. Because it is common for outsourcing providers to be managed by professionals who worked in a U.S. business environment before migrating back to their home countries to start outsourcing provider firms, it would be worthwhile to establish whether the nationality of the outsourcing provider's chief executive officer matters. We were also unable to obtain data on the outsourcing provider's organizational culture. Future survey research might address how organizational and national cultural differences interact to affect outsourcing performance. We further encourage scholars to use Mohr and Sengupta's (2002) research as a starting point to investigate how characteristics of the outsourcing firm, such as the outsourcing firm's learning intent (e.g., merely accessing knowledge to substitute for its lack of skills vs. actually internalizing the knowledge and skills of the partner), may affect the selection and effectiveness of various governance mechanisms.

Furthermore, although we searched for NPD outsourcing announcements in three different databases (covering more than 100 newspapers and business/trade magazines) to increase the likelihood of obtaining a more representative data set, we may have failed to uncover announcements from firms that do not report in the public records covered by these databases. In addition, our study examined stock market reactions to announcements of NPD decisions, not the actual implementation of these decisions. Announcements are intended strategies that may be modified during implementation. Further research could study the effectiveness of strategy implementation.

Finally, while our focus was on outsourcing an activity that was previously performed by the outsourcing firm, a relatively new phenomenon is “backsourcing”: bringing an outsourced activity back in-house. Backsourcing is costly: A company must in effect reorganize twice (first transitioning to outsourcing, and then transitioning to insourcing), employee morale may be shaken, and customers may become dissatisfied. What factors drive firms to back-source? In addition, when is reorganizing outsourcing arrangements preferable to backsourcing? We hope that the results presented here encourage other scholars to pursue these possibilities in further research.