Abstract

To manage marketing channels, subsidiaries of multinational corporations (MNCs) must balance mandates from headquarters (HQ) with the local realities of the foreign markets. The performance implications of subsidiary–distributor relationship efforts thus are contingent on the HQ–subsidiary relationship. Drawing on marketing channels, economics, and organization theory literature streams, the authors (1) describe the complex performance properties of output and process control mechanisms that MNC subsidiaries deploy to manage foreign distributors and (2) conceptualize the HQ–subsidiary nexus along three attributes that should moderate the performance effects of control mechanisms: task coordination, or HQ's central coordination of processes across subsidiaries; subsidiary decision involvement, or two-way communications and consensual decision making between HQ and the subsidiary; and relational disharmony, or the extent of the HQ–subsidiary conflict. The authors test the hypotheses using field data from German and Japanese MNCs in the United States and Bayesian models that account for measurement error, endogeneity in the control mechanisms, heterogeneity in country of origin, and nonlinear and interactive terms for the latent constructs. The results demonstrate the importance of the HQ–subsidiary relationship for managing the subsidiary–distributor relationship.

Keywords

Multinational corporations (MNCs), which include household names such as Coca-Cola, Siemens, and Toyota, are significant features of modern markets (Bartlett and Beamish 2008; Feinberg and Gupta 2009). An MNC typically comprises the headquarters (HQ) and one or more geographically dispersed subsidiaries,1 which in turn depend on local channel partners (i.e., distributors) to serve their respective foreign markets. As such, not only must the subsidiary craft appropriate strategies for managing distributor performance, but it must do so in consultation with HQ (Andersson, Forsgren, and Holm 2007; O'Donnell 2000). The MNC subsidiary's ability to manage foreign distributors thus relies on its linkage with HQ. The trade-offs and challenges that subsidiaries face in managing foreign distributor performance and the interplay between subsidiary–distributor and HQ–subsidiary relationships raise important questions for both marketing channels and MNC literature streams. This represents the primary focus of our research.

Subsidiaries are not franchised units but are internalized (Feinberg and Gupta 2009, p. 283) by the MNC through ownership and/or similar integrative linkages.

In Figure 1, we depict the trade-offs a subsidiary faces in managing distributors in foreign markets. The MNC marketing channel consists of the HQ located in a home country (area on the left in Figure 1) and subsidiaries located in foreign markets or host countries (area on the right in Figure 1) together with foreign distributors. These three entities (HQ, subsidiary, and distributor) interact such that HQ has an intrafirm relationship with the subsidiary (arrow A in Figure 1; Doz and Prahalad 1991) and the subsidiary in turn manages the foreign distributor (arrow B in Figure 1; Palmatier, Scheer, and Steenkamp 2007). In an MNC context, attributes internal to the HQ–subsidiary dyad (“internal relationship,” hereinafter) influence relationships external to it, namely, the subsidiary–distributor dyad (“external relationship,” hereinafter) (arrow C in Figure 1); thus, performance outcomes in the subsidiary–distributor relationship depend partly on the HQ–subsidiary relationship. Such contingencies between connected MNC relationships have both theoretical and managerial relevance, and yet they have received little scrutiny in marketing (e.g., Bello, Katsikeas, and Robson 2010) or MNC (e.g., Bartlett and Ghoshal 2004) research. Our goals are to investigate (1) how firms can organize subsidiary–distributor relationships to motivate foreign distributor performance and (2) how the MNC HQ–subsidiary relationship influences these performance outcomes.

MNC Channel Setup

We draw on agency theory (Eisenhardt 1989; Jensen and Meckling 1976), the measurement branch of transaction cost theory (Alchian and Demsetz 1972; Ouchi 1979), and the interfirm literature in marketing (Antia and Frazier 2001; Bergen, Dutta, and Walker 1992) to conceptualize the subsidiary–distributor relationship according to its emphasis on formal controls. Formal control mechanisms take two prototypical forms: output control, which involves the evaluation of distributor performance against predefined goals, and process or behavior control, which involves influencing and guiding distributor behaviors through suggestions (Bello and Gilliland 1997; O'Donnell 2000). We articulate two conflicting perspectives for the efficacy of control mechanisms for the subsidiary–distributor relationship: On the one hand, formal control can support distributor performance by fostering distributor goal clarity and accountability (Kashyap, Antia, and Frazier 2011). On the other hand, control may also have the unintended effect of compromising performance by triggering psychological reactance and dysfunctional behaviors (Heide, Wathne, and Rokkan 2007). We integrate these disparate theoretical positions into a unified framework by positing that although both scenarios can arise in principle, only one will dominate at a given time, contingent on the strength of the focal control mechanism. We thus propose and empirically test a curvilinear effect of subsidiary control mechanisms on distributor performance.

We also examine the way the MNC organizational context influences the efficacy of the focal mechanisms (Figure 1, arrow C). Governance of a foreign distributor involves interactions within the MNC HQ–subsidiary relationship as well; for example, a subsidiary's ability to implement output control with foreign distributors is facilitated to the degree that the HQ and subsidiary are in agreement about focal output goals. However, the geographic and institutional separation between HQ and subsidiaries implies that the MNC cannot always be assumed to act as a unified entity (Bartlett and Beamish 2008; Birkinshaw and Hood 1998). As such, we posit that the performance implications of control mechanisms in the subsidiary–distributor relationship are contingent on the HQ–subsidiary attributes (Ghosh and John 2009; Wuyts et al. 2004).

We draw on the economics (e.g., Williamson 2010), organization theory (e.g., Roberts 2004), and MNC (e.g., Almeida and Phene 2004) literature streams to conceptualize the HQ–subsidiary nexus along three attributes: task coordination, or the nature of task and resource flows across MNC subsidiaries; subsidiary decision involvement, or the nature of HQ–subsidiary communication; and relational disharmony, or the extent of HQ–subsidiary conflict. As Figure 2 depicts, we advance a series of novel, refutable arguments regarding the contingency roles these attributes serve in relation to output and process controls. Notably, scholars (e.g., Ghosh, Dutta, and Stremersch 2006) have posited the existence of such interplays across connected exchange relationships, and yet empirical evidence in this regard is surprisingly scarce (Granovetter 2005). As part of our broader agenda to understand the influence of the MNC context on the efficacy of control mechanisms, we also consider the role of MNC country of origin (e.g., Steenkamp and Geyskens 2012).

Conceptual Framework

To test our hypotheses, we use a field study of German and Japanese MNCs in the United States and develop a Bayesian model that corrects for measurement error, accounts for endogeneity in the control mechanisms, includes heterogeneity emanating from the MNC country of origin, and incorporates nonlinear and interactive terms for latent constructs. The results provide support for the moderating role of the HQ–subsidiary nexus on the efficacy of formal control mechanisms.

We contribute to research on marketing channels and MNCs. First, although researchers frequently assume that control mechanisms yield performance benefits throughout their entire continuum, we argue that this perspective is overly restrictive, because control generates not only performance payoffs but also psychological reactance. We reconcile these opposing perspectives by articulating and demonstrating the curvilinear performance effects of control mechanisms. Second, we answer recent calls to generate insights into the question of “governance spillovers” or interplays across “connected” marketing relationships (Palmatier, Scheer, and Steenkamp 2007) by demonstrating that the effects of control mechanisms in the subsidiary–distributor relationship are contingent on HQ–subsidiary attributes. Our results imply that the exchange properties of control mechanisms are not fully revealed in analyses of individual relationships but instead require consideration of the larger constellations of exchange relationships. Third, we advance the MNC literature by shedding light on the relationship strategies of complex organizations such as MNCs, a topic on which “little research” exists (Griffith, Harmancioglu, and Droge 2009, p. 218); in doing so, we also document how an MNC's country of origin influences its governance of foreign channel partners.

Our research holds implications for MNCs such as Siemens and Toyota, which rely on foreign channel partners to drive sales and profitability. A McKinsey industry report (Donoghoe et al. 2012) notes that well-managed foreign partners are crucial for MNCs to understand their customers and markets. We offer guidelines for effective foreign channel partner management and highlight firm-specific considerations that impinge on the manager's ability to leverage control mechanisms.

We present our theoretical framework and hypotheses next and then our methodology and results. We conclude by elaborating on the implications of our research for theory and practice.

Conceptual Framework

Output Control

Output control “approximates a market contracting arrangement” (Anderson and Oliver 1987, p. 76) that firms use to assess the observable consequences of an exchange partner's actions against predetermined standards (Heide et al. 2007). To implement output control, subsidiaries offer explicit goals to foreign distributors (e.g., desired sales) against which they evaluate the distributors’ outcomes.2 These output goals, designed by the MNC's HQ in consultation with the subsidiary, are implemented in the distributor relationship by the subsidiary (Almeida and Phene 2004).

For example, as ChannelWorld.in (October 29, 2009) reports, Hewlett-Packard intensively monitors its Indian distributors’ market share, reach (penetration), and profitability.

In theory, two opposing effects are associated with output control. On the one hand, by specifying explicit or measurable outcomes, the subsidiary offers goal clarity to the distributor (Stouthuysen, Slabbinck, and Roodhooft 2012). Tracking achieved outcomes against clearly stated benchmarks also enables the subsidiary to hold the distributor accountable for nonperformance (e.g., Ambos and Schlegelmilch 2007). We refer to this ability of output control to establish concrete goals and foster distributor accountability as the “goal clarity effect.” The motivational effects of well-specified goals are salient in an MNC context, because the institutional and cultural distance between parties often creates misunderstandings about relationship goals. On the other hand, output control can also trigger a “reactance effect.” Output control by the MNC subsidiary can limit a distributor's discretion and autonomy, which can potentially elicit distributor psychological reactance (Brehm 1966) and precipitate dysfunctional behaviors (Celly and Frazier 1996). The resulting “dark-side” behaviors, such as gaming the system and reporting invalid numbers, undermine distributor performance. Reactance is particularly likely given the cultural and institutional differences between the MNC and the foreign distributor, because dissimilarity between actors is known to enhance the adverse consequences of autonomy loss (Chadee 2011).

In summary, output control can create both a beneficial goal clarity effect and an adverse reactance effect. In line with the foregoing reasons, we argue that a subsidiary's emphasis on output control should have an inverted U-shaped effect on distributor performance. That is, an initial emphasis on output control should motivate distributor performance by enhancing distributor goal clarity and accountability. In such instances, reactance is unlikely because distributors that view output control as enhancing their goal clarity are unlikely to frame it as a threat to their autonomy (Fuegen and Brehm 2004). Beyond a point, however, increasing emphasis on output control ceases to provide any incremental goal clarity and instead is likely to be viewed as severely limiting distributor discretion. Then, the reactance effect should dominate and reduce distributor performance.

H1: The MNC subsidiary's emphasis on output control has an inverted U-shaped effect on distributor performance.

Process Control

Process control entails offering helpful suggestions or “guidance” (Bello and Gilliland 1997, p. 25) to influence a partner's marketing activities, such as selling procedures, promotional practices, and product management, to achieve desired outcomes (Celly and Frazier 1996).3 The HQ typically crafts these relevant suggestions in consultation with the subsidiary, which then communicates them to the distributor (Gupta, Govindarajan, and Malhotra 1999).

Some scholars focus on “harsh” process monitoring, which is deployed ex post to assess compliance with preestablished procedures (e.g., Eisenhardt 1989). Our focus is on ex ante suggestions that an MNC offers to facilitate distributor performance. Considerable research suggests the suitability of this conceptualization for both marketing organizations in general (e.g., Anderson and Oliver 1987) and MNCs in particular (e.g., Bello and Gilliland 1997).

Process control by an MNC subsidiary can create two contrasting effects. On the one hand, process controls influence the daily operations of the foreign distributor and could be viewed as intrusive interferences (Heide, Wathne, and Rokkan 2007). Consequently, they could be perceived as autonomy-depriving, unwarranted interventions that will engender distributor reactance and inhibit its motivation to perform; we label this effect the “reactance effect” of process control. Specifically, distributors whose reactance is aroused will reassert their threatened freedom by purposely refusing to comply with process guidance (Brehm 1966). On the other hand, MNC process control could signal the MNC's commitment to the foreign distributor, that is, the commitment effect of process control. Processes consist of multiple interlinked activities that take effect holistically; for example, an MNC subsidiary's suggestions to distributors regarding sales procedures might encompass customer qualification, product customization, and service execution activities, all of which combine to make an effective sales process. Process suggestions also involve some adaptation to the distributor's local market. 4 Generating suggestions about multiple interlinked activities and adapting them to the distributor's context requires the MNC subsidiary to invest time and effort idiosyncratic to the focal distributor's market. As such, process suggestions could be viewed as a signal of MNC commitment (Frazier et al. 2009) and thus a “cognitive foundation” (Heide, Wathne, and Rokkan 2007, p. 425) regarding the legitimacy of MNC subsidiary interventions in the distributor activities is fostered between the parties.

For example, Ford's service suggestions to international distributors explicitly recognize the local market context, such as the availability of spare parts (see Ford 2007).

Thus, process control can create both a harmful reactance effect and a beneficial commitment effect. Integrating these two effects, we propose that process control should have a U-shaped effect on distributor performance. Because multiple interlinked activities constitute a process, initial emphases on process control that fail to address these activities holistically or to their fullest extent should not enable the distributor to achieve process effectiveness. For example, effective sales management demands both product customization and service execution activities; subsidiary process suggestions that address only one aspect cannot yield satisfactory improvements, and the foreign distributor is unlikely to appreciate the value of process guidance (Narayanan and Raman 2000) but instead view the MNC subsidiary's process inputs as ineffectual and unwarranted interventions. As a result, with initially increasing emphases on process control, the reactance effect should dominate and compromise distributor performance.

However, we argue that an increasing emphasis on process control beyond the initial levels should lead to the dominance of the commitment effect. When the MNC subsidiary offers extensive guidance for a range of interlinked activities with a holistic view, the distributor can better discern the benefits that follow from the relevant suggestions and should view the MNC's willingness to offer extensive guidance as a signal of commitment. This perception should be further strengthened to the degree that the MNC subsidiary adapts its suggestions to the distributor's local market (Anderson and Weitz 1992). When the distributor views process control as a legitimate and beneficial intervention, process control should motivate distributor performance.

In summary (within the ranges of control observed in the marketplace), we expect a U-shaped effect of process control on distributor performance: initial emphases on process control undermine performance (creating a negative slope of process control on performance; i.e., the reactance effect dominates), but subsequent emphases beyond the initial levels support performance (creating a positive slope of process control on performance; i.e., the commitment effect dominates).

H2: The MNC subsidiary's emphasis on process control has a U-shaped effect on distributor performance.

Interaction of Output and Process Control

Firms often emphasize both output and process control in the same relationship, as revealed by a positive correlation between the two control mechanisms (.20 at the low end [Challagalla and Shervani 1996] and .72 at the high end [Bello and Gilliland 1997]). We contend that this practice reflects a synergistic relationship between mechanisms whose effects are mutually contingent.

Because output control can clarify goals and enforce distributor accountability but also arouse reactance in the distributor, who may feel deprived of autonomy, we propose that to the extent that the subsidiary can specify certain underlying processes that support the accomplishment of desired outputs, the foreign distributor should be motivated to achieve those outputs. When the subsidiary offers elaborate process guidance in relation to focal output goals, the distributor, instead of perceiving loss of autonomy, should regard the MNC as committed to the relationship (commitment effect) and feel empowered to achieve the outputs. Thus, with increasing process control, the reactance potential of output control diminishes, and distributor performance improves. 5

Honda offers substantial process inputs to its international dealers to facilitate output goals, such as reducing customer wait times for service. The MNC visits partner premises to identify service bottlenecks (e.g., dealer knowledge, service area layout). Then it institutes appropriate diagnostic procedures and continuous quality improvement processes to cut down customer wait times (see Honda 2012).

H3: As the MNC subsidiary's emphasis on process control increases, a greater emphasis on subsidiary output control enhances distributor performance.

MNC HQ–Subsidiary Relationship

Multinational corporation channels represent multilevel agency arrangements (Gibbons 2010), which involve a subsidiary–distributor relationship “connected” to an HQ–subsidiary relationship. As a result, the focal control mechanisms offer only partial insights into distributor performance, because the output and process decisions implemented in the subsidiary–distributor dyad also involve interactions within the HQ–subsidiary dyad (Figure 1). For example, the MNC's ability to leverage control mechanisms with foreign distributors for value-creation purposes relies partly on information flows within the HQ–subsidiary dyad, which could affect the way relationship objectives are set and communicated to distributors. Thus, the efficacy of control mechanisms deployed in a subsidiary–distributor relationship should be contingent on the elements of the HQ–subsidiary relationship. To investigate this contingency, consistent with Roberts (2004, p. 17), we recognize that the HQ–subsidiary relationship has multiple facets that can be classified along three core dimensions: operational coordination, information flow, and sentiments. We choose one key representative for each of these aspects of HQ–subsidiary relationship, as we describe subsequently.

A salient and unique feature of MNCs is that the various subsidiaries and HQ are disaggregated globally and possess specific constraints and interests, so the HQ must align operations across subsidiaries for optimal MNC outcomes (Andersson, Forsgren, and Holm 2007). We capture such operational alignment across subsidiaries through the construct of task coordination (Tsai 2002). The second aspect of HQ–subsidiary relationships, information flow, is also both critical and distinctive in MNC contexts, because HQ makes product-brand decisions that affect the subsidiary, whereas the subsidiary possesses superior information about its local markets but lacks the HQ's global view. As such, effective decision making requires bilateral communication and consensus building in the HQ–subsidiary relationships, which we capture as subsidiary decision involvement (Kim and Mauborgne 2003). Finally, for sentiments, an extensive body of research has highlighted dissension as a common sentiment in MNC organizations (Schotter and Beamish 2011). Disagreements are particularly salient in HQ–subsidiary relationships given the parties’ unique perspectives on relationship goals, which are fostered by the geographic and institutional separation between them. For example, subsidiaries sometimes view HQ-mandated goals as lacking legitimacy due to the HQ's sparse knowledge of the local issues, while the HQ might ride roughshod over subsidiary perspectives. We use the relational disharmony variable to capture such sentiments of conflict in HQ–subsidiary relationships.

The aforementioned HQ–subsidiary features are particularly compelling in our study because they can be expected, on theoretical grounds, to alter the effects of control mechanisms, and indeed, these contingency roles might differ across mechanisms (O'Donnell 2000). For example, task coordination across subsidiaries is expected to support the efficacy of output control by cross-channeling complex resources (e.g., personnel, competencies, equipment) to distributors in local markets, which can enable the distributors to achieve the focal output goals (Kim, Park, and Prescott 2003). However, global task coordination, to the degree that it overlooks the fit of the relevant processes to a focal subsidiary's local market idiosyncrasies in favor of global considerations, can undermine the performance benefits of process control.

Task Coordination across Subsidiaries

Task coordination is the extent to which operations such as manufacturing, product design, and marketing are coordinated in an integrated fashion across the global system of MNC subsidiaries (O'Donnell 2000). It represents a continuum: At one end is domestic coordination, in which individual subsidiaries handle subsidiary-level tasks with minimal cross-subsidiary integration; the intermediate level implies a multidomestic setup such that subsidiary tasks are integrated nationally or regionally (Kim, Park, and Prescott 2003); and the highest level involves the global integration of operations for various subsidiaries.

We use cross-subsidiary task coordination to characterize the MNC organization because it is central to current conceptions of the firm. In the resource-based view, a firm's core purpose is the “optimal deployment” (Grant 1996, p. 110) of tasks and resources across the hierarchy; economists have formalized this idea by conceptualizing the firm as a vehicle to coordinate team inputs (e.g., Alchian and Demsetz 1972). Indeed, the firm emerges when exchange actors resolve their mutual dependency by assigning task-coordination authority to a hierarchy (Williamson 2010). Task coordination is relevant to our study particularly because MNCs represent intraorganizational systems composed of HQ and various foreign subsidiaries across which resources and expertise are distributed (Bartlett and Ghoshal 2004). Activities and resource flows therefore must be integrated across subsidiaries to attain efficient operations, and task coordination represents both a “parsimonious operationalization” (Ghoshal, Korine, and Szulanski 1994, p. 100) and a “fundamental dimension” (Tsai 2002, p. 180) of such integration across subsidiaries. Finally, we use task coordination because scholars have hinted that the benefits of control mechanisms could vary with the level of task integration, though empirical evidence remains scarce (e.g., O'Donnell 2000).

Output control and task coordination

As we noted previously, both goal clarity and reactance effects are associated with output controls. We propose that as task coordination across subsidiaries increases, the reactance effect should diminish such that the goal clarity effect will dominate. Achievement of distributor outputs is supported by the availability of appropriate local resources (e.g., adequate product inventory, competitively priced offerings), which are facilitated by increasing integration of tasks across subsidiaries. In particular, resources not specialized to one country, such as finished goods, raw materials, and production equipment, can be shared across subsidiaries; the resulting scale and scope economies enable the MNC to provide cost-effective offerings in a timely and adequate manner to distributors to achieve focal goals (e.g., sales). In turn, to the degree that cross-subsidiary task coordination facilitates the availability of appropriate resources to foreign distributors to accomplish outputs, the distributor, rather than perceiving a loss in autonomy due to increasing output control, should be empowered to achieve the focal outputs such that the reactance effect of output control should dissipate. The subsidiary is also in a superior position to hold the distributor accountable for the subsidiary's output goals, because distributor nonperformance cannot be ascribed to the lack of supportive resources from the subsidiary. The goal clarity effect then should dominate and enhance distributor performance.

H4a: As task coordination across subsidiaries increases, an increase in a focal subsidiary's emphasis on output control enhances distributor performance.

Process control and task coordination

Process control can create both a reactance effect and a commitment effect. We argue that the reactance effect dominates with greater task coordination across subsidiaries because, to be effective, the firm must adapt process suggestions to the distributor's local market (Ouchi 1979). For example, process guidance for product promotions should reflect local consumer preferences. However, global coordination of foreign subsidiaries’ operations overlooks such idiosyncratic local market conditions; therefore, with increasing integration of subsidiary operations, the fit of the MNC process inputs with the local market decreases, and distributors should view process suggestions as unwarranted interventions. Ultimately, such developments should trigger distributor reactance and undermine the effectiveness of process control. 6

Global task coordination, in theory, can facilitate the movement of generalized resources across subsidiaries, but generalized resources may not be relevant to process control, which involves context specificity.

H4b: As task coordination across subsidiaries increases, an increase in a focal subsidiary's emphasis on process control diminishes distributor performance.

Subsidiary Decision Involvement

Subsidiary decision involvement captures the nature of communication between HQ and subsidiary, such as mutual information flows and consensus building for decision making. Greater subsidiary decision involvement manifests in the form of HQ's emphasis on two-way communications with the subsidiary rather than a unilateral approach that allows for minimal inputs from and to the subsidiary. 7

Task coordination and subsidiary decision involvement differ in their level of analysis and substantive content. Subsidiary decision involvement pertains to the HQ–subsidiary relationship level; task coordination is a system-level construct. In terms of content, task coordination refers to operational coupling among various subsidiaries; subsidiary decision involvement refers to information flows in HQ–subsidiary interactions. Tightly integrated operations across subsidiaries can exist with or without subsidiary consensus.

We investigate decision involvement because it constitutes an “indispensable function” (Barnard 1938, p. 122) of the firm. Indeed, a principal advantage of the hierarchy is the ease of communication among internal units, a notion that has prompted scholars to describe the firm as “an information processing and decision rendering system” (Cyert and March 1963, p. 21). However, agency theorists (e.g., Gibbons 2010) have also noted the possibility that intrafirm communication can be unilateral, incomplete, or restricted. The quality of communication is not assured in complex organizations such as MNCs because the local information possessed by subsidiaries situated in foreign markets may be at odds with the global perspective of the HQ, with which superordinate decision rights traditionally have been vested (Kim and Mauborgne 2003). In particular, HQ–subsidiary communication could affect the efficacy of different control mechanisms that vary in terms of communication intensity (Bello and Gilliland 1997).

Output control and subsidiary decision involvement

Goal clarity and reactance effect are both associated with output control, but depending on the context, one dominates the other. We propose that information exchange and consensus building in the HQ–subsidiary relationship (i.e., decision involvement) will offer clarity to the subsidiary regarding focal goals and will lead to dominance of the goal clarity effect (Bartlett and Ghoshal 2004). Even when output goals are modified, such as in response to emergent market conditions, ongoing HQ–subsidiary communication should promote goal clarity; consequently, the subsidiary, which serves as the intermediary between HQ and distributor, is able to convey and justify a set of clear output goals to the distributor. Goal justification should dissipate the reactance potential of output control by fostering the belief that illegitimate interference with autonomy is unlikely (Brehm 1966). Furthermore, incorporating inputs from the subsidiary in the goal-setting process should also facilitate HQ's ability to articulate output goals that foreign distributors view as legitimate. Therefore, with increasing subsidiary decision involvement, we expect the reactance effect to diminish and the performance augmenting goal clarity effect to dominate.

H5a: As subsidiary decision involvement increases, an increase in a focal subsidiary's emphasis on output control enhances distributor performance.

Process control and subsidiary decision involvement

With regard to process control, we argue that the commitment effect should dominate when subsidiary decision involvement increases. First, bilateral communication acquaints the subsidiary with the HQ's perspective underlying the focal process suggestions, so the subsidiary can elaborate and justify these suggestions to the distributor. The distributor is then able to benefit from the focal process suggestions and to discern the MNC's supportive intentions behind the suggestions. Second, bilateral communication acquaints HQ with the subsidiary's local perspective, which helps infuse the MNC's process inputs with context-specific considerations and promotes fit with the distributor's situation. 8 With increasing subsidiary decision involvement, the distributor is likely to view process control not as unwarranted interventions but as a signal of MNC commitment, and thus, the distributor should be better motivated to perform.

That is, the quality of process control should improve due to context specificity, which affects how increasing the level (strength) of process control affects performance. Our measure of process control captures the level of process control and is conceptually distinct from its context specificity.

H5b: As subsidiary decision involvement increases, an increase in a focal subsidiary's emphasis on process control enhances distributor performance.

Relational Disharmony

Relational disharmony captures disagreements between the subsidiary and HQ with regard to relationship goals and priorities (Schotter and Beamish 2011). Disharmony is especially relevant to MNCs, because it highlights the MNC as a goal-disparate organization (Bartlett and Ghoshal 2004) that must balance the global perspective of HQ and the local viewpoint of the subsidiary (Feinberg and Gupta 2009). Consistent with this view, agency theory (Eisenhardt 1989) and organization theory (Cyert and March 1963) both characterize intrafirm interactions as principal–agent exchanges, in which the units “share only partially congruent objectives” (Ouchi 1979, p. 833). Our focus on disharmony also derives from our interest in control mechanisms, because even though HQ–subsidiary disharmony is common in practice (Hofstede 2005), its influence on mechanisms’ exchange properties remains unclear.

Specifically, as we detail next, the efficacy of control mechanisms might be undermined by HQ–subsidiary dis-agreements (Ouchi 1979), although disharmony could also serve productive purposes in some conditions (Schotter and Beamish 2011). Importantly, prior research (e.g., Hofstede 2005) has suggested that MNC country of origin crucially affects the implications of disharmony within the organization. As such, we first outline our baseline expectations regarding the role of relational disharmony in the context of control mechanisms and subsequently advance formal hypotheses that also take account of the MNC country of origin.

In terms of output control, we expect the reactance effect to dominate the goal clarity effect with greater HQ–subsidiary disharmony. The goal clarity effect emerges because output control, which approximates a “market contracting arrangement” (Oliver and Anderson 1994, p. 76), motivates performance by providing explicit goals for which the distributor is accountable (Kashyap, Antia, and Frazier 2011). Disharmony, which reflects disagreements within the HQ–subsidiary dyad, implies that the distributor receives conflicting messages from the MNC subsidiary regarding output standards, which should compromise distributor goal clarity and weaken its motivation to perform. Thus, our baseline expectation is that as HQ–subsidiary relational disharmony increases, an increase in a focal subsidiary's emphasis on output control decreases distributor performance.

Unlike output control, whose effectiveness rests on explicitness (i.e., preset and fixed definition of the focal outputs), processes have an implicit or tacit quality such that to be effective, the firm must adapt processes continually to fit the evolving context in which they are implemented. We argue that HQ–subsidiary disharmony could support such ongoing process adaptations. Typically, the HQ has superior information about the MNC's product strategy, whereas the subsidiary has more direct insights about the distributor's local market where the focal process suggestions are implemented (Bartlett and Ghoshal 2004). Disharmony (i.e., HQ–subsidiary disagreements) acquaints these parties with each other's perspectives on the processes; thus, HQ's rich product and brand insights and the subsidiary's foreign market expertise can both be incorporated into the processes. The resulting adaptation of the processes to the MNC's focal product and the distributor's local market context should support process efficacy (Siggelkow 2002). 9 In this scenario, the distributor should view subsidiary process control not as unwarranted interventions but as a signal of commitment, and it should be motivated to perform. Thus, our baseline expectation is that as HQ–subsidiary relational disharmony increases, an increase in a focal subsidiary's emphasis on process control increases distributor performance.

Distributors’ motivation to perform can be augmented if they are aware of the subsidiary's efforts to infuse context sensitivity in process inputs, especially if it involves opposing HQ's one-sided suggestions. Dörrenbächer and Gammelgaard (2006, p. 28) describe the case of Siemens, whose subsidiary co-opted foreign channel partners as allies in its conflict with HQ, suggesting that foreign partners are often aware of subsidiary opposition to HQ.

Relational disharmony and MNC country of origin

Our aforementioned baseline expectations reflect unique contingencies between relational disharmony and control mechanisms. However, the practices of MNCs are rooted in their domestic cultural influences (Tihanyi, Griffith, and Russell 2005), which reflect the taken-for-granted beliefs of decision makers—that is, beliefs that are not subject to deliberate consideration but that influence the efficacy of chosen strategies (e.g., Scheer, Kumar, and Steenkamp 2003). Thus, the implications of relational disharmony with regard to control mechanisms likely depend on the MNC's country of origin.

We focus on subsidiaries of German and Japanese MNCs in the United States because (1) these countries contribute among the highest proportions of U.S. foreign direct investment (FDI; Ibarra and Koncz 2008) and (2) firms in these two countries follow distinct organization or decision logics that are shaped by their country-specific cultures (Hofstede 2001). As Hofstede (2001, p. 377) describes, Japanese firms represent a so-called pyramid mode, whereas German firms represent a “work-flow bureaucracy” mode of organization. 10 The pyramid logic, which involves an authority figure at the top “and each successive level at its proper place below” (Hofstede 2005, p. 244), is partly a reflection of high power distance in Japan. In the pyramid mode, disagreements within the firm are resolved through appeals to the personal authority of a hierarchical superior (Hofstede 2001). In contrast to Japanese firms, the lower power distance in Germany is reflected in the functioning of German firms as “well-oiled” work-flow bureaucracies (Hofstede 2001, p. 377); here, the organizational units are treated on equal footing, and disagreements are resolved through explicit rules. Next, we consider how the MNC country of origin influences the joint effect of monitoring and disharmony hypothesized previously. 11

Hofstede (2005) categorizes firms into these organization modes on the basis of two elements of national culture: (1) uncertainty avoidance (the extent to which a culture programs its members to minimize uncertainty or disharmony in interactions) and (2) power distance (a society's willingness to accept unequal distribution of power among its members). Both the work-flow mode of German MNCs and the pyramid mode of Japanese MNCs emphasize avoidance of uncertainty, which HQ–subsidiary disharmony can trigger; however, given their distinct power-distance orientations, these modes differ sharply in the specific means they advocate to resolve disharmony. The work-flow bureaucracy mode relies on formally established dispute-resolution rules that supersede the authority of any hierarchical authority. Such disavowal of an individual-centric approach is partly a result of low power distance in Germany, where all parties are treated on equal footing. In contrast, the pyramid mode of Japanese MNCs relies on the individual authority of a hierarchical superior to resolve disharmony; this individual-centric approach is driven partly by high power distance in Japan, which tends to centralize authority in the hands of a hierarchical superior.

We do not expect differences in German and Japanese MNCs for formal operational arrangements such as task coordination, which remains a common economic denominator across all MNCs (Kim 2003). Decision involvement also can be beneficial, independent of country context (Ghoshal, Korine, and Szulanski 1994). Therefore, we do not offer formal hypotheses for country-specific differences in task coordination and subsidiary decision involvement, though we do test for such effects.

Output control, relational disharmony, and MNC country of origin

The baseline scenario we outlined previously regarding the joint effect of output control and relational disharmony suggests that disharmony limits the performance benefits of output control because explicit output goals cannot be specified, which triggers distributor confusion regarding these goals. We expect this baseline scenario to hold for Japanese MNCs, whose pyramid logic involves handling disharmony through personal authority of a superior, a process that “prevails over [explicit] rules” (Hofstede 2005, p. 252). Such an individual-centric approach has the advantage of bridging disagreements and facilitating quick adaptations to changing circumstances by reducing the need for explicit documentation (Uzzi 1997), but it also leaves aspects of decision making implicit and idiosyncratic (Williamson 2010). Thus, the deleterious effect of HQ–subsidiary disharmony on output control (per the baseline expectation) should hold for Japanese MNCs, whose pyramid logic runs counter to the explicitness required for effective output control. Output goals, which are already unclear due to HQ–subsidiary disharmony, are compromised further by the pyramid logic of Japanese MNCs, whose implicit and idiosyncratic approach can leave aspects of goal setting ambiguous. As a result, distributor confusion should increase and undermine its performance as HQ–subsidiary disharmony rises.

In contrast, the work-flow bureaucracy logic of German MNCs emphasizes explicitness in HQ–subsidiary dealings. Explicitness involves clear articulation and codification of the parties’ positions and decisions guided by a set of formal procedures (Uzzi 1997). Insistence on formal procedures and explicitness could delay the resolution of disagreements, but the resulting decisions and goals are likely to be unambiguous. Therefore, the deleterious effect of HQ–subsidiary disharmony on output control (per the baseline scenario) should not hold. Instead, in the face of disharmony, explicit interactions within the German context should limit foreign distributor confusion regarding output goals and support the effectiveness of output control; this beneficial effect of the German context should be particularly pronounced with increasing disharmony in the HQ–subsidiary relationship, which undermines output control initially.

H6a: As HQ–subsidiary relational disharmony increases, an increase in a focal subsidiary's emphasis on output control (i) decreases distributor performance for Japanese MNCs but (ii) increases distributor performance for German MNCs.

Process control, relational disharmony, and MNC country of origin

The baseline scenario we advanced previously regarding the joint effect of process control and relational disharmony suggests that disharmony supports the efficacy of process control by promoting the adaptive fit of the relevant processes to the distributor's foreign market. We expect this effect to hold for Japanese MNCs. The pyramid logic within Japanese HQ–subsidiary relationships facilitates the speedy adaptation of processes without the need for explicit codification and elaborate documentation. Thus, the beneficial baseline effect of disharmony in relation to process control should be complemented by the pyramid logic of Japanese MNCs, which can permit process adaptations “on the fly” (Uzzi 1997, p. 47).

In contrast, German MNCs’ focus on explicitness could impede adaptations to process inputs (Tinsley 1998). For example, a subsidiary might suggest a flexible pricing strategy in light of emerging local competition, but the HQ might request explicit documentation of the competition's moves before making pricing changes, which could delay the adaptation of MNC pricing processes. The beneficial baseline effect of HQ–subsidiary disharmony in relation to process control as we outlined previously thus should be undermined for German MNCs.

H6b: As HQ–subsidiary relational disharmony increases, an increase in a focal subsidiary's emphasis on process control (i) increases distributor performance for Japanese MNCs but (ii) reduces distributor performance for German MNCs.

Model Development

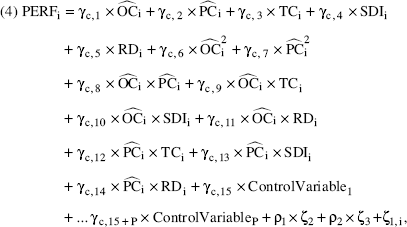

We used survey methodology to collect data from subsidiaries of German and Japanese MNCs in the United States. With this two-country cross-sectional survey data, we took several data structure issues into consideration for our model specification. First, primary data gave us multiple indicators to measure each (latent) construct, so we could correct for measurement error with structural equation modeling (SEM). Second, output and process control mechanisms are both endogenous because prior performance may determine emphases on the control mechanisms, so we must correct for potential endogeneity biases. Third, with our data from subsidiaries of German and Japanese MNCs, we aimed to estimate regression parameters that varied between countries and to capture potential heterogeneity in the effects emanating from the country of origin. Fourth, to test our hypotheses, we needed to model the quadratic effect of latent constructs and their interactions; modeling such nonlinearities is cumbersome and problematic in SEM models and often limited in the number of nonlinear effects that can be modeled. In summary, we needed to estimate a model that (1) corrected for measurement error, (2) accounted for the endogeneity of the control mechanisms, (3) accounted for heterogeneity emanating from the MNCs country of origin, and (4) modeled nonlinear and interactive effects of latent constructs. Thus, we developed a Bayesian SEM that corrects for measurement error and uses data augmentation to handle nonlinear effects (Lee 2007). We used shrinkage specification to account for heterogeneity and embedded a latent instrumental variable approach in the model to correct for endogeneity (Ebbes et al. 2005).

Measurement Error

We used the SEM framework to account explicitly for measurement error. By modeling the error component, we ensured that we were able to correct for any bias that measurement error induces.

Endogeneity of Control Mechanisms

We first specified the theorized effects of control mechanisms on performance as follows:

The latent control constructs OC and PC are endogenous to the system, which leads to a potential endogeneity bias due to simultaneity. Following Ebbes et al. (2005), we first model the two latent constructs using a latent instrumental variable approach, in which we specified each latent construct as a function of P observed control variables (Control-Variable1 − ControlVariableP) and an unobserved latent instrumental variable with k categories, as follows:

To correct for endogeneity bias in Equation 1, we included the effects of the residual error terms ζ2 and ζ3 from Equations 2 and 3. Thus, the equation for firm performance is

Country-of-Origin Heterogeneity

We captured country-of-origin heterogeneity in the theorized effects by allowing all regression parameters to differ across German and Japanese MNCs. Specifically, we build on extant Bayesian models (Rossi and Allenby 2003) that shrink parameter estimates for various populations (in our study, German and Japanese MNCs) toward the mean of the superordinate population (all MNCs) using a hierarchical prior structure that we detail in the “Model Estimation” subsection.

Nonlinear and Interactive Effects of Latent Constructs

We theorized nonlinear and interactive effects of the latent constructs, as captured by the coefficients γc,6-γc,14 in Equation 4. The estimation of models that incorporate only linear effects of the latent constructs is easy with standard maximum-likelihood procedures, though nonlinear and interactive terms involving the latent constructs may demand new methods for estimation. We draw from Lee (2007) to develop a flexible model specification that includes nonlinear and interactive effects as part of the estimation.

Model Estimation

In the model, Y = (y1, …, yn) is the observed data matrix, and θ is the parameter vector that contains all the unknown parameters. Because we have nonlinear and interaction effects, estimating θ using standard maximum likelihood-based procedures would be tedious and cumbersome. Instead, using Bayesian estimation, we augmented the data vector Y with the matrix of latent variables Ω in the posterior analysis. With the Gibbs sampler (Geman and Geman 1984), we generated a sequence of observations from the posterior distribution [θ,Ω|Y]. Because Ω is given, Equations 1 and 2 reduce to simultaneous regression models, and we derived the full conditional distributions of the elements of the parameter vector θ. We used conjugate prior distributions for all parameters and assigned noninformative start values to the priors. We provide additional details about the derivation of the full conditional distributions and the priors in the Web Appendix (www.marketingpower.com/jmr_webappendix).

We used standard Markov chain Monte Carlo procedures, with two concurrent chains for estimation. The first 5,000 iterations per chain were burn-in values; the next 40,000 iterations per chain provided the samples for parameter estimation. The Gelman–Rubin statistics showed that the model converged. For model comparisons, we calculated the deviance information criterion (DIC), for which lower values signify better fit (Spiegelhalter et al. 2002).

Methodology

Research Context

To test our framework, we surveyed managers of German and Japanese MNC subsidiaries. These MNC subsidiary managers operate in foreign markets, so we aimed to identify a foreign market that (1) is economically and strategically important, such that the MNC HQs must pay attention to subsidiaries and their execution of global strategies in the foreign market; (2) is not overly regulated, such that regulations do not constrain the execution of global strategies; and (3) offers an existing open market, so that MNCs have the opportunity to establish subsidiaries and develop channel relationships. The United States satisfies these criteria: It is a key foreign market for European and Asian MNCs, it has low levels of market regulation, and it has historically been open to MNCs. For the U.S. market, we identified MNCs from countries with significant FDI, which signals the likely establishment of subsidiaries, as well as varying cultural distance from the United States. Germany and Japan satisfy these criteria. First, MNCs from these countries contribute the highest proportion of U.S. FDI (Germany = 11%, Japan = 9%; Ibarra and Koncz 2008). Second, Germany, Japan, and the United States represent three different cultural blocks: Germany belongs to the Germanic block, the United States to the Anglo block, and Japan constitutes its own cultural block (Barkema, Bell, and Pennings 1996). Thus, the two combinations of MNC HQs–host country (Germany-United States, Japan-United States) offer appropriate contexts for our study.

Data Collection

We collected data through a survey of top MNC subsidiary managers. Our initial objective was to identify key informants involved in strategic decision making at both the subsidiary and HQ levels. We undertook initial contacts by telephone to locate and qualify key informants who were knowledgeable about the phenomena of interest and willing to participate. To contact parties who could not be reached immediately, we made a second attempt within a week. We directed potential respondents to send us a questionnaire redirect form if, after examining the questionnaire, they believed that someone else in the organization would be better able to respond.

We assessed the scale items and general flow of the questionnaire by interviewing managers from two MNCs. A pilot survey packet was subsequently mailed to a random sample of 400 MNC subsidiaries in our sample (200 German and 200 Japanese), with the goal of assessing the psychometric properties of our scale items. This process ultimately yielded 76 usable returns. The item-to-total correlations did not indicate any serious concerns.

To collect the actual data for the hypothesis tests, we replicated the pilot test procedure and mailed 1,000 survey packets to 500 MNCs from Germany and 500 MNCs from Japan. We obtained the mailing list from a commercially available, comprehensive directory of U.S. subsidiaries of German and Japanese MNCs with a listed physical address in the United States. The survey packet consisted of an official cover letter that described the study and requested participation, the questionnaire, a self-addressed prepaid return envelope, a redirecting form, and a dollar bill as an incentive. Informants rated their subsidiaries’ relationships both with the HQ and with a typical U.S. distributor. We personalized the cover letter and redirecting form for each respondent. We obtained 175 complete and usable returns for an effective response rate of 17.5%. Mann–Whitney tests for comparison of early and late responders on the control variables (i.e., global sales, subsidiary sales, and number of employees) did not yield significant differences. We did not detect any differences after splitting the sample according to the MNCs country of origin, so response bias was not an issue.

Key Construct Operationalization and Measures

To develop our measures, we undertook an extensive literature review and in-depth interviews with several MNC managers. All measures appear in the Web Appendix (www.marketingpower.com/jmr_webappendix).

Foreign distributor performance (PERF)

Drawing from Bello and Gilliland (1997), we measured strategic, sales, and economic aspects of distributor performance. Strategic performance (STPER) captures distributor outcomes with respect to the MNC organization's marketing, distribution, and pricing goals. Sales performance (SLPER) captures aspects such as customer contact maintenance and after-sales service. Economic performance (EPER) captures the extent to which the distributor achieved the MNCs return on investment, profit, and growth goals.

Output control (OC)

The output control measure pertains to the MNC subsidiary's efforts to monitor the foreign distributor's performance with respect to (1) market penetration of new products, (2) expansion of the customer base, and (3) sales volume. We drew specific items from Bello and Gilliland (1997) and Celly and Frazier (1996).

Process control (PC)

We drew the process control measure from Bello and Gilliland (1997). We designated this measure to reflect the degree to which the MNC subsidiary influenced the distributor's (1) promotional activities, (2) product management efforts, and (3) selling policy and procedures for the MNC's offerings.

Task coordination (TC)

We created a new measure, task coordination, in line with Morrison and Roth (1992) and Kim, Park, and Prescott (2003). This measure refers to the extent to which operations (e.g., procurement, manufacturing, marketing) of various subsidiaries of an MNC were coordinated globally (vs. locally).

Subsidiary decision involvement (SDI)

We drew on extant research (e.g., Mohr, Fisher, and Nevin 1996) to create the subsidiary decision involvement measure. This measure describes the degree to which HQ involved the subsidiary in decisions about its markets and legitimized decisions to the focal subsidiary.

Relational disharmony (RD)

Relational disharmony captures disagreements between HQ and the subsidiary regarding the (1) goals of the MNC, (2) processes the subsidiary used to achieve the MNC's objectives, and (3) terms of their relationship. We created this measure in line with, for example, Birkinshaw and Hood (1998).

Control variables

We measured several control variables to account for alternative influences on distributor performance. First, following the power dependence paradigm (e.g., Kumar, Scheer, and Steenkamp 1995), we included the MNC's dependence (FDEP) on the focal distributor. Second, in line with prior research on the role of environment on organizations (Dwyer and Welsh 1985), we accounted for features of the MNC organization's environment, specifically, its munificence (MUN) and dynamism (DYN). The munificence measure assessed growth opportunities in the country in which the foreign distributor was located; the environmental dynamism scale gauged variability in customer needs as well as the product and pricing aspects of the MNC's offerings (Dwyer and Welsh 1985). Third, we controlled for the absolute size of the subsidiary (SSALES) and the MNC organization (GSALES) through their sales. Fourth, we included the number of subsidiary employees (NEMP).

Measure Validation and Measurement Invariance

The confirmatory factor analysis (CFA) model for the multi-item measures exhibited good psychometric properties (χ2701 = 1150.38, comparative fit index = .90, nonnormed fit index = .89; root mean square error of approximation = .06). Composite reliabilities were greater than .7, except for partner dependence and dynamism, which reached .68 and .67, respectively. The average variance extracted was also greater than .5 for all constructs except dynamism, which revealed a value of .41 and reasonable protection against the deleterious effects of multicollinearity (Grewal, Cote, and Baumgartner 2004). We established discriminant validity by showing that all ϕs (factor variance–covariances) were less than the average variance extracted and statistically different from 1. Because we are interested in estimating regression effects for German and Japanese MNCs separately, we first established measurement invariance across the two groups.

Following Steenkamp and Baumgartner (1998), we confirmed that the factor loadings were invariant so that we could compare the regression coefficients. We compared an aggregate CFA model with a two-country CFA model in which we allowed the factor loadings to vary between countries. A comparison of the DIC across the two models indicated that the pooled measurement model (DIC = 22,962) outperformed the country-specific model (DIC = 23,213), which verified model invariance.

To alleviate common methods concerns, per Lindell and Whitney (2001), we included informant risk propensity as a marker variable and compared the covariance matrix (ϕ) of the latent constructs before and after including the marker variable in a CFA model. The pattern and magnitude of ϕs did not change significantly. These analyses suggest that common method bias is not a major concern.

Results

Model Selection

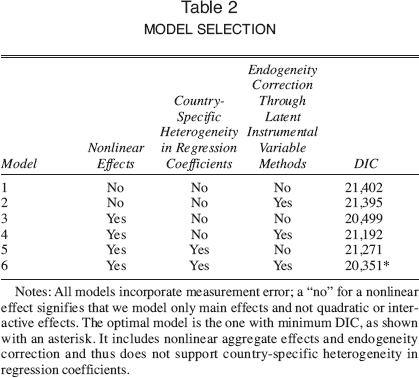

We present the descriptive statistics and bivariate correlation coefficients in Table 1. We believe that the three important characteristics of our estimation model are the correction for endogeneity bias, the presence of country-specific heterogeneity, and the presence of nonlinear effects. Therefore, to arrive at the appropriate model specification for testing the theorized effects, we estimated several models that we developed on the basis of the presence or absence of these three characteristics. The results from this model comparison analysis appear in Table 2 (we corrected for measurement error in all the estimated models). The optimal model, based on minimum DIC (Spiegelhalter et al. 2002), included nonlinear country-specific effects and the endogeneity correction; we illustrate this optimal model as M6 in Table 2 and use it for hypotheses testing.

Descriptive Statistics

p < .05 (one-tailed).

p < .01 (one-tailed).

Model Selection

Notes: All models incorporate measurement error; a “no” for a nonlinear effect signifies that we model only main effects and not quadratic or interactive effects. The optimal model is the one with minimum DIC, as shown with an asterisk. It includes nonlinear aggregate effects and endogeneity correction and thus does not support country-specific heterogeneity in regression coefficients.

Hypotheses Testing

In Table 3, we provide the unstandardized regression coefficients for both the Japanese (γj) and German (γg) MNCs. The coefficient for output control was positive (but not significant), and the squared term was negative and statistically significant (γj = −.22, p < .01; γg = −.27, p < .01), in support of H1. We also graph this effect in Figure 3, which shows that initial emphasis on output control increased but progressively greater emphases decreased distributor performance (inverted U-shaped effect; Figure 3). The positive squared term for process control (γ, = .12, p < .01; γg = .13, p < .01) supports H2, which hypothesized a U-shaped effect of process control on distributor performance (see Figure 3). Consistent with H3, the joint effect of output and process control was statistically significant and positive (γj = .14, p < .01; γg = .13, p < .05).

Plots Illustrating the Effects of Control Mechanisms on Performance

Results with Country-Specific Heterogeneity

Parameter is significant at the 90th percentile in a one-tailed test.

Parameter is significant at the 95th percentile in a one-tailed test.

Parameter is significant at the 99th percentile in a one-tailed test.

The “Difference” column shows the difference between parameter values in columns “A” and “B.” We created a parameter during the estimation that captured the difference between the values of the German and the Japanese effects for each iteration in the simulation. The values presented in the table are the posterior means of the difference parameter.

The “Pooled Effect” column includes the results from the model in which we constrained all the effects, except the interaction between the relational disharmony and control mechanisms, to be the same across German and Japanese firms. Therefore, there are two coefficients in the row listing the interaction effect for relational disharmony.

In H6a-b, we proposed the country-specific interaction effect between control mechanisms and relational disharmony. Specifically, in H6a we proposed that the effect would be negative for Japanese and positive for German MNCs. In H6b, we proposed that the effect would be positive for Japanese and negative for German MNCs. These country-specific effects appear in the “Pooled Effect” column. For both the H6a and H6b rows, the first cell in the “Pooled Effect” column shows the effect for Japanese MNCs, and the second cell shows the effect for the German MNCs. (As we noted previously, the pooled effect model constrained all effects to be the same across the two countries, except the focal interaction between control mechanisms and relational disharmony.)

Notes: The parentheses contain the 2.5th and the 97.5th percentiles.

With regard to the moderating role of the HQ–subsidiary relationship attributes, we found that, as we proposed in H4a, with greater task coordination, an increased emphasis on output control also enhanced distributor performance (γj = .56, p < .01; γg = .30, p < .05). The hypothesized negative interaction between process control and task coordination in H4b was supported, though only for German MNCs (γg = −.14, p < .10). Because task coordination interacts with both the control mechanisms, we used a three-dimensional plot (see Figure 4) to further visualize and explore these interactions. We show the two mechanisms along the x- and y-axes and plot the predicted performance on the z-axis at high (+2 SD) and low (−2 SD) levels of task coordination, which results in two response surfaces. As Figure 4 depicts, increasing output control weakens performance (reactance effect), but this is less so for high levels of task coordination, which is manifested as positive interaction between task coordination and output control, in support of H4a. Figure 4 also shows that process control enhances (reduces) performance at a high (low) level of task coordination, which is manifested as positive interaction between process control and task coordination, in line with H4b.

Impact of Control Mechanisms on Performance at Two Levels of Task Coordination (H4A AND H4B)

In line with H5a, among Japanese MNCs, increasing emphasis on output control supported distributor performance for greater subsidiary decision involvement (γj = .25, p < .10). However, we found no support for H5b, that is, for the positive interaction between process control and decision involvement.

Finally, consider H6a and H6b, which describe the contingency roles of both MNC country of origin and relational disharmony. To examine these hypotheses, we tested a series of three-way interactions such that we expected the joint effect of control mechanisms and relational disharmony to differ for German and Japanese MNCs. Specifically, we examined the difference between the two-way interaction effects of output control and relational disharmony for Japan and Germany: if the difference parameter was statistically different from 0, the country-specific effects differ from each other, and not otherwise. Table 3 presents the values of this parameter for all the pairs (Japanese-German) of coefficients.

In H6a, we hypothesized that as relational disharmony increases, a subsidiary's emphasis on output control would hinder distributor performance for Japanese MNCs but increase it among German MNCs. Our results supported this hypothesis; the effect was negative for Japanese MNCs (γj = −.38, p < .01) and positive for German MNCs (γg = .24, p < .01), and the two effects differed significantly from each other (γ − γg = −.46, p < .01). In support of H6b, as relational disharmony increased, subsidiary emphasis on process control increased distributor performance for Japanese MNCs (γj = .41, p < .01) but decreased it for German MNCs (γg = −.13, p < .05), and the two effects again were significantly different (γj − γg = .43, p < .01).

Following the procedure described previously, we used three-dimensional plots (see Figure 5) to depict these interactions for further exploration. We show the two control mechanisms along the x- and y-axes and plot predicted performance on the z-axis at high (+2 SD) and low (−2 SD) levels of relational disharmony, which generates two response surfaces. Given the country-specific predictions in H6a and H6b, we show the effects for Japan (Panel A) and Germany (Panel B) separately. As we portray and explain in Figure 5, the plots offer further support for H6a and H6b.

Impact of Control Mechanisms on Performance at Two Levels of Relational Disharmony (H6a and H6b)

As a further robustness test for H6, we constrained all effects, except the interaction effects hypothesized in H6, to be the same across the two countries and reestimated the empirical model. Table 3 presents the results from this analysis in the column labeled “Pooled Effect.” As the column indicates, the interaction effects that were allowed to be different across German and Japanese firms were statistically significant and different in direction from each other, further suggesting country-specific heterogeneity in this effect across the firms in the sample.

Discussion

Recognizing the unique challenges that MNCs face in managing foreign channels, we have theorized that the efficacy of the control mechanisms subsidiaries use to manage foreign distributors depends on both the HQ–subsidiary relationship and the MNC's country of origin. We detail the theoretical and managerial implications of our research subsequently.

Theoretical Implications

Our research contributes to the marketing channels and MNC governance literature streams. Foremost, we elucidate two opposing influences of output and process control (e.g., goal clarity vs. reactance effects) and integrate the conflicting perspectives by proposing a curvilinear effect of the control mechanisms on performance. In contrast with established perspectives (e.g., Eisenhardt 1989) that view control mechanisms as goal-alignment devices that yield favorable performance payoffs, we demonstrate that they can both motivate performance (goal clarity effect) and become unique sources of agency costs in themselves due to the psychological reactance that they are capable of arousing. Emerging research (e.g., Carson 2007) has begun to acknowledge these issues, but empirical evidence regarding the curvilinear effects of mechanisms remains scarce. We also establish that the direction of the curvilinear effect differs for output (inverted U-shaped) and process (U-shaped) controls, which implies that overarching prescriptions advocating less or more control in general are unlikely to bear fruit; such recommendations instead must be tied to the specific mechanisms. Finally, we uncover a positive joint effect of output and process mechanisms; an intriguing question is whether these mechanisms can also serve as functional substitutes (e.g., Puranam and Vanneste 2009). Overall, by highlighting the complex trade-offs inherent in managing MNC marketing channels, our research tells a cautionary tale about referring to distinct control mechanisms collectively as “market mechanisms” (Williamson 1991, p. 277).

We also describe the boundary role of the characteristics of HQ–subsidiary relationship with respect to the control mechanisms the firm deploys with foreign distributors. We demonstrate that certain aspects of HQ–subsidiary relationships, such as decision involvement, which are ordinarily expected to facilitate performance, might bestow no such benefits when used in conjunction with control mechanisms. In contrast, seemingly dysfunctional aspects, such as relational disharmony, might even complement the favorable performance effects of control mechanisms. Thus, our analyses suggest that selective alignments between control mechanisms and firm characteristics translate into distinct economic consequences (Ghosh and John 2009). However, such discriminating alignment patterns cannot be revealed without including firm-specific considerations in analyses of exchange relationships. More generally, following the ideal-typical portrayal of hierarchy (e.g., Williamson 2010), marketing and MNC literature streams have largely viewed the firm as a unitary actor that experiences unproblematic goal alignment and decision making. Consequently, limited research has addressed the complexities that characterize the “black box” of the internal organization or their implications for the management of exchange relationships (Gibbons 2010). We show not only that a unitary actor perspective is untenable for complex organizations such as MNCs but also that understanding the organizational context of the relationship mechanisms may indeed be key to generating insights into the performance properties of these mechanisms.

In particular, we uncover complex interplays across the boundaries of connected MNC relationships, which suggest that the efficacy of control mechanisms deployed in subsidiary–distributor relationships can be supported and undermined by HQ–subsidiary relationships. Our perspective represents a departure from the orthodoxy that views individual exchange relationships in isolation (Granovetter 2005); instead, we emphasize the “connectedness” between these relationships. In so doing, we advance extant MNC literature that has “consistently underplayed” the role of such governance spillovers for MNC organizations (Birkinshaw et al. 2006, p. 697).

Finally, we uncover the role of country of origin in relation to the joint effects of control mechanisms and disharmony. The country context is a key parameter in exchange, but its complex interactions with a firm's existing configuration of ties and effects on organizational choice and performance are not well established (Mantzavinos, North, and Shariq 2003). Our study is a step in this direction. Admittedly, our arguments are only ceteris paribus, because factors other than country of origin can also contribute to differences between German versus Japanese MNCs. Moreover, as we have argued, country-of-origin influences can shape a firm's functioning, but they need not be completely deterministic. Further research is required to characterize these influences fully.

Methodologically, we extend the latent instrumental variable approach (Ebbes et al. 2005) to the SEM context and incorporate it within a Bayesian framework. We employ a cross-sectional survey design so the relevant limitations still apply, but by using this method, we control for endogeneity that might arise due to the simultaneous measurement of control mechanisms and distributor performance. The choice of control mechanisms has long-term ramifications for channel partners, so longitudinal studies, particularly those that examine both linear and more complex, curvilinear, time-dependent effects, can qualify the implications of our research.

Managerial Implications

Our findings offer several guidelines to MNC subsidiary managers. First, they should deploy output controls with caution, because they can trigger reactance and should be scaled back if distributors perceive a threat to their autonomy. In contrast, managers can benefit from the commitment effect of process control by offering extensive process guidance to distributors.

Second, subsidiary managers should consider the characteristics of their relationship with the HQ before determining which control mechanism to use for managing distributors. As we illustrate in Figure 6, depending on the levels of task coordination, subsidiary decision involvement, and relational disharmony between the HQ and subsidiary, subsidiary managers can choose to emphasize (or de-emphasize) output versus process control.

Control Mechanisms and HQ–Subsidiary Relationship

Third, the moderating effects of task coordination and subsidiary decision involvement merit consideration, because they are common economic denominators for all MNCs. When task coordination is high (two standard deviations above mean) and subsidiary operations are globally coordinated, an emphasis on output control benefits distributor performance, irrespective of the MNC's country of origin. Relational disharmony between the HQ and subsidiary suggests an emphasis on process (and de-emphasis on output) control for Japanese firms but an emphasis on output (and de-emphasis on process) control for German firms.

Conclusion

Our research highlights systematic patterns of interaction between control mechanisms and their specific contexts. Consistent with the governance value analysis framework (Ghosh and John 2009) and other emergent paradigms (e.g., Nickerson and Silverman 2009), our findings suggest a need to move beyond an exclusive focus on generic governance forms for organizing a particular transaction to consider what is the “best way for a specific firm” (Madhok 2002, p. 542), in light of its specific organizational context. Such efforts, though challenging, will advance emergent knowledge of complex marketing organizations and their effective management.