Abstract

Life insurance settlement (LIS) is a US$15 billion global industry and is expected to grow tenfold or more by 2040. It involves the controversial practice of investors acquiring the life insurance policies of living people and then receiving the proceeds of the policy after the death of the insured. This article examines LIS exchange and consumption from a consumer-focused public policy and marketing perspective. The authors find that the vast potential of LIS to meaningfully expand consumer choice has yet to be fully realized as a result of (1) LIS consumers often being inherently at a high risk of experiencing vulnerability, (2) inconsistent and inadequate industry regulation, and (3) ethically or legally questionable industry marketing practices. Public policy recommendations are formulated with a view toward facilitating regulatory reform that benefits both LIS consumers and ethical LIS marketers.

Keywords

It's as macabre an investing concept as Wall Street has ever cooked up. … For the investors it's a ghoulish actuarial gamble: The quicker the death, the more profit is reaped. (Goldstein 2007, pp. 44, 46)

Despite this apparently rosy scenario, the potential of LIS to expand consumer choice remains far from being fully realized. This appears to be ultimately due to regulatory inadequacies that have created opportunities to take advantage of a particularly vulnerable group of consumers. Although only a minority of LIS marketers have capitalized on these opportunities, industry marketing practices have been featured in a leading investor watchdog group's annual list of “top investments scams” six of the last eight years (Consumers’ Research 2002; North American Securities Administrators Association 1999, 2001, 2004, 2005, 2007).

Public policy and marketing (PPM) scholars have yet to examine LIS. The primary purpose of this article is to stimulate discussion among PPM scholars on LIS marketing practices and regulation. We also hope to indirectly facilitate regulatory reform that both better protects LIS consumers and levels the playing field for ethical LIS marketers. With respect to LIS consumers, although the welfare of both life insurance policyholders and small, noninstitutional investors is worthy of attention, our focus is on the former.

We begin with a discussion of LIS products and exchange. This is followed by a brief history of the industry. We then address consumer vulnerability in the context of LIS exchange. Finally, we provide suggestions for regulatory reform.

LIS Products and Exchange

The two key LIS products differ mainly with regard to target market. “Viatical settlements” are targeted at terminally ill life insurance policyholders (i.e., people with a certified life expectancy of fewer than 24 months [Kohli 2006]). This product provides access to funds that can be used to pay for drugs and medical and dependent care services or to prepare for imminent death. “Life settlements” are targeted at insured people who are not terminally ill. Events or factors driving need, priority, or lifestyle change that could potentially make a life settlement attractive include (1) the death of designated beneficiaries to the life insurance policy (e.g., a spouse, children), (2) the financial independence of beneficiaries (e.g., grown children with less of a need for financial support), (3) the onset of a chronic but nonterminal illness or disability, (4) a sudden, sharp decline in economic condition, (5) divorce, (6) perceptions that life insurance premiums have become unaffordable, (7) changes in estate tax laws making LIS proceeds exempt from taxable income (Jensen and Leimberg 2007), (8) perceptions that life insurance had been purchased as a result of ethically questionable marketing practices, and (9) the pursuit of better investment opportunities (i.e., the certainty of a large payment now coupled with the opportunity to invest the proceeds in higher-yielding alternatives).

The prototypical LIS exchange involves a consumer in possession of a universal life, whole life, or convertible term life insurance policy. Depending on state law, life insurance policies can be sold to third parties after either a two- or a five-year waiting period. The exchange itself is typically initiated when the insured, sometimes acting on the referral of an insurance consultant or financial advisor, contacts a broker (see http://www.settlementsforlife.com/). The broker collects health and policy-specific financial information from the insured and then solicits settlement offers from multiple life settlement providers (LSPs). The broker transmits an offer to the insured, and when the insured accepts, an exchange occurs in which the insured receives immediate cash compensation. The amount of the insured's compensation, known as the “settlement amount,” varies widely and is primarily a function of the life expectancy of the insured; the shorter the life expectancy, the higher is the payout. Brokers are compensated in the form of a commission, typically either 6%–10% of the transacted policy's total death benefit or up to 30% of the gross amount offered by the LSP to buy the policy (Lavine 2008; Leimberg et al. 2008). The LSP takes possession of the policy, assumes responsibility for all future premiums, and possesses full rights to the policy's total death benefit after the death of the insured.

The appeal of LIS for the consumer is that it represents a relatively unique opportunity to dispose of an otherwise illiquid asset that has become unwanted or unneeded. Perhaps most important, LIS provides significantly more money for this asset than the other primary disposal alternative—namely, selling the policy back to the insurance company that issued it for a “surrender value” stipulated at the time of initial acquisition. Analysis of 12 exemplary “case studies” provided by the Life Insurance Settlement Association (LISA; 2008a) indicates that settlement amounts range from 3.9% to 53% of policy total death benefits, with an average of 28.41%. In the 8 cases that disclose surrender values, these range from .48% to 16.21% of total death benefits and average 4.57% percent. Applying these averages to a US$1 million life insurance policy yields a settlement amount of $284,100 and a surrender value of $45,700.

Finally, an alternative and highly controversial form of LIS transaction warrants consideration: “stranger-owned life insurance” (STOLI). With STOLI, unlike traditional life insurance purchases, policy acquisition is not motivated by a desire to protect family members against the risk of loss of income or to create an estate for dependents. Instead, the policy is purchased solely to gain access to the settlement amount through “a prior agreement to cede control to an investor (the stranger) … at issuance” (LISA 2008c, ¶ 1). In STOLI transactions, it is commonplace for LIS marketers (i.e., brokers or investors) to (1) recruit potential consumers and make them aware of the opportunity to engage in LIS exchange, (2) be present during the acquisition of the policy, and (3) loan consumers money to pay insurance premiums during the waiting period before actual policy transference (Kiplinger's Personal Finance 2008; LISA 2008c, d). In addition, STOLI transactions are typically at least twice as large as other LIS exchanges, involving life insurance policies valued at US$1 million or more (Lysiak 2008).

A Brief History of LIS

The first LIS transaction is believed to have resulted from a conversation between a group of AIDS patients and the then president of Prudential Insurance's Canadian operations in 1988 (Kindleberger 1991). The exchanges that soon followed in both Canada and the United States similarly involved viatical settlements between terminally ill AIDS patients and insurance companies. By 1993, the target market for viatical settlements had expanded to include terminally ill cancer patients. The then-US$250 million industry included not only insurance companies but also approximately 50 specialized viatical settlement firms (i.e., LSPs) (Flaherty 1993). It was also at about this time that criticisms of LIS marketers in the United States began to surface (Pilgrim 1993). This was due, in large part, to the industry being regulated at that time in only a single U.S. state (Flaherty 1993; Pilgrim 1993).

The industry continued to expand rapidly throughout the mid-1990s. However, the late 1990s witnessed the bursting of the “viatical settlement bubble.” What had for investors been a safe, rapid return on investment—founded on the certainty of the short life expectancies of AIDS patients—was rendered far less attractive by the advent of “drug cocktails” and other advances in AIDS treatment. In addition, there were growing concerns about ethically questionable marketing activity and inadequate industry regulation (Consumer Reports 2001; Goldstein 2007).

The LIS industry quickly recovered, due mainly to marketplace innovation. Most notable was the introduction of the life settlement product, which expanded the market for LIS beyond the terminally ill to include tens of millions of middle-aged and older life insurance policyholders (e.g., older U.S. baby boomers). The market for LIS products was then further enlarged, this time beyond those presently in possession of life insurance policies, through the advent of the aforementioned STOLI transaction.

Another factor leading to the resurrection of LIS was widespread consumer dissatisfaction with “whole” life insurance. With whole life insurance, the insurer pays the policy's total death benefit to beneficiaries at the time of the insured's death, whenever it occurs. With the primary alternative, known as “term” insurance, benefits are paid only if the insured dies within the specified term of the policy (e.g., 5, 10, or 20 years). Protection ceases at the end of the policy period, and no cash value is built up (Vaughn 1982). Thus, although term insurance functions purely as a means of protecting against the risk of unexpected death, whole life is best understood as part of an investment and estate-planning package (Vaughan 1982). Note also that whole life costs much more than term life and that insurance agents are typically compensated far more heavily for whole life sales (e.g., commissions for whole life are roughly five times higher than for term [Updegrave 1992]).

High interest rates in the late 1970s and early 1980s caused investors largely to abandon whole life in favor of more attractive investment alternatives. The insurance industry's response was to develop “universal” life insurance, a form of whole life in which the eventual payout is sensitive to prevailing investment return rates throughout the duration of the policy. During the early 1980s alone, market share for universal life and related, newer forms of life insurance skyrocketed from 3% to 42% (Fischel and Stillman 1997). The sales pitch for universal life policies typically focused on optimistic “illustrations” laying out the required premium payments given certain sets of marketplace assumptions, many of which depicted scenarios in which the policy would be completely paid off in a relatively short time. When the assumptions behind these scenarios did not hold true, a wave of class-action suits against life insurance firms began (Consumer Reports 1998b; Fischel and Stillman 1997). Life settlement may be viewed as a less litigious response to many consumers’ disappointing experience with universal life policies (i.e., the seeking of a solution not in the court house but rather in the “auction house” of LIS). To the present day, the majority of life settlements involve universal life policies (Gardner, Welch, and Colvert 2009).

The most recent major development in the LIS marketplace is securitization. It is now commonplace for LSPs to resell life insurance policies to institutional investors (e.g., global hedge fund operators, investment banks [Goldstein 2007]). These investors amass large numbers of policies and convert them into asset-backed securities that are sold in fractional shares to further-downstream investors (Goldstein 2007). Exemplary of such LIS-backed securities is the Assured Fund, an Isle of Man–domiciled fund based solely on settled life insurance policies issued in the United States. This fund, targeted exclusively at independent financial advisors and institutional investors in the United Kingdom, comprises 261 policies with an average total death benefit of US$2.95 million and an average policyholder life expectancy of just under five years (Hedgeweek.com 2008; Policy Selection 2008).

Securitized LIS funds are positioned on the basis of (1) producing steady returns (of approximately 8%); (2) their safety as “portfolio diversifiers” not directly correlated with stocks, bonds, and other investment products; and (3) the certainty of eventual payout relative to securities based on mortgages and credit card receivables (Goldstein 2007; Lankford 2008). This “safe and certain” positioning has become particularly prevalent in the midst of the global economic crisis beginning in 2008 (see Business Wire 2008; FINalternatives 2008; PR Newswire Europe 2008).

Today, fueled by ongoing disposal of universal life policies and securitization, LIS is a US$15 billion global industry, with forecasts of more than tenfold growth by 2040 (Goldstein 2007; Lavine 2008; PR Newswire Europe 2008). The industry's growth, as well as projections for future expansion, is testament to LIS's vast potential to meaningfully expand consumer choice. However, viewed from a consumer-focused PPM perspective, this potential remains far from being fully realized. This is attributable, in part, to the macabre buyer–seller relationship that is frequently the central focus of mass-media coverage of LIS. In addition, LIS consumers are often at high risk to experience vulnerability. Our attention now shifts to consumer vulnerability and its incidence in the LIS marketplace.

Consumer Vulnerability and LIS

Baker, Gentry, and Rittenburg (2005, p. 134) define consumer vulnerability as “a state of powerlessness that arises from an imbalance in marketplace interactions or from the consumption of marketing messages and products.” Vulnerability is a matter not of who experiences it (e.g., a particular group of consumers) but rather the situations in which it is likely to be experienced (Baker, Gentry, and Rittenburg 2005, p. 136). Life insurance settlement exchange is a vulnerability-inducing situation because of (1) the high level of financial risk involved, (2) the high level of product complexity, and (3) information asymmetry favoring LIS marketers.

Subsequently, we discuss the factors rendering many LIS consumers inherently at high risk to experience vulnerability. We then examine more controllable factors (i.e., LIS industry regulations, marketing practices, and conditions of exchange) that significantly affect the probability that consumer vulnerability will be experienced.

Consumer Vulnerability and Inherent LIS Consumer Vulnerability

According to Baker, Gentry, and Rittenburg (2005), further compounding the notion that certain situations are likely to lead to vulnerability being experienced is the presence of a wide range of personal characteristics, individual states, and external factors. Personal characteristics increasing the probability that vulnerability will be experienced in the context of LIS exchange include (1) advanced chronological age, (2) limited resource assets, and (3) the lack of self-efficacy in negotiating complex exchanges with far more knowledgeable marketers. Individual states motivating consumers to engage in LIS exchange that are also likely to incite vulnerability include (1) being diagnosed with a terminal or potentially terminal illness, (2) poor health or perceptions of declining health, (3) death-related grief, (4) disability-related grief, (5) a sudden and sharp decline in economic welfare, and (6) role transition due to death or divorce. Finally, an external factor motivating LIS exchange that is of particular current relevance is ongoing economic upheaval. Emerging from consideration of the role of these factors in rendering LIS consumers inherently at high risk to experience vulnerability are three factors of particular salience. We discuss each in turn.

Advanced Age and Poor Health

The typical LIS consumer is age 65 or older (Goldstein 2007; Lankford 2008). In addition, LIS consumers are often in poor health (Consumer Reports 2001). Although this is particularly the case in exchanges involving viatical settlements, it also frequently applies to life settlements. Indeed, it is the onset of old age and, most profoundly, poor health that both leads to changes in needs and priorities that motivate consideration of a life settlement and makes a given consumer an attractive prospect for LIS marketers and investors. Given that the approximately 80 million “aging baby boomers” in the United States are prime targets of financial scams and investment fraud (Chu 2006; North American Securities Administrators Association 2006), the incidence of age- and health-induced vulnerability is likely to escalate significantly in coming years.

Death- and Disability-Related Grief

Life insurance settlement consumers sometimes find themselves “desperate … [and] at the mercy” of industry marketers (Consumer Reports 2001, ¶ 11). A factor that possibly leads to a desperation-driven vulnerable state is grief associated with the death of life insurance beneficiaries (e.g., a spouse, children). As Gentry and colleagues (1994, p. 129) describe, death-related grief is a particularly strong vulnerability-inducing factor for consumers:

Grief restricts a person's ability to note when he or she is being mischarged or overcharged … as well as limits his or her ability and desire to share such information when practices are noted. … Medical, insurance, and funeral decisions would, on the surface, appear to require high-involvement decisions. People in grief, however, may not use decision making strategies typical of high-involvement purchases; … their vulnerability is due to a transformation of the self that forces them to face new consumer roles when they are least prepared to do so because of the associated stresses.

When the death of a beneficiary occurs, the grieving policyholder faces the task of deciding what to do with what may now be a useless policy. Although LIS is likely to be superior to other disposal options in this situation, grief renders the consumer at high risk to experience vulnerability. Compounding the matter, the grieving consumer may also be dealing with other complex death-related issues (e.g., estate administration, funeral arrangements, the deceased's health and life insurance).

Another source of vulnerability-inducing grief is being diagnosed with a chronic illness or traumatic disability. Dealing with the new state as a disabled person can involve grieving in much the same manner as dealing with the death of a loved one. According to Schlesinger (1965, pp. 92–93),

The disabled stroke patient is faced with a number of problems in dealing with himself. … One of the most common reactions to the vascular accident is mourning—grieving over the lost abilities. The loss of function … is like any other kind of serious loss of life, including the loss of someone who is very dear.

A person trying to come to grips with disability may view LIS as perhaps the most expedient means of obtaining the financial resources needed to pay forthcoming medical or dependent care expenses. Unfortunately, grief may lead to vulnerability and less-than-optimal exchange outcomes for consumers.

Economic Upheaval and Sudden Decline in Economic Welfare

Given current economic conditions, increasingly large numbers of consumers are likely to experience vulnerability as a result of considering LIS in response to a sharp, sudden downturn in economic standing. Such people in possession of life insurance may view LIS as a means of quickly compensating for losses or maintaining their standard of living. Exemplary of this, many once-comfortably wealthy people who lost money in the Madoff investment fraud scandal are considering LIS (Ostrowski 2008). However, the current economic crisis and the Madoff scandal are but two of the latest in a long series of events helping create a sizable segment of “newly poor” prospects for LIS. The recent surge in white-collar layoffs, coupled with similar layoffs in the past 10–15 years (Downs 1995; Ehrenreich and Draut 2006), has likely left many people with a relatively high propensity to own life insurance in a desperate financial state.

Controllable LIS Consumer Vulnerability

The preceding sections collectively demonstrate that many LIS consumers are at high risk to experience vulnerability because of factors largely beyond their control. This section considers “the more controllable side” of LIS consumer vulnerability. Our focus is on marketing practices and conditions of exchange, enabled or at least not prohibited by existing industry regulation, that are most likely to lead to consumer vulnerability. After first providing a brief background on the current LIS regulatory environment, we discuss three vulnerability-inducing practices and conditions of exchange: information disclosure, privacy, and STOLI transactions.

LIS Industry Regulatory Environment

In the United States, LIS marketplace activity is regulated at the state level. This is because LIS products are classified as “insurance” products rather than “investment” products, the latter being regulated at the federal level. As is common in specialized areas of the law, many states base their regulations on a “model act” (i.e., a proposed statute drafted by industry trade associations or other interested parties). Model acts are rarely adopted wholesale. Instead, each state legislature tailors the model to fit the needs and precedents of that given state.

The LIS industry in the United States is regulated on the basis of two model acts that have been adopted, in some form, in just over 30 states. One of the acts was drafted by the National Association of Insurance Commissioners (NAIC), and the other was drafted by the National Conference of Insurance Legislators (NCOIL). As of late July 2008, some form of the NCOIL model had been adopted in 10 states, and the NAIC model served as the basis for regulation in at least 23 states (Estey 2008; Tyrrell 2008 [see also LISA 2008b]). 1 In regulated states, both brokers and LSPs must be licensed (NAIC 2007, § 3; NCOIL 2007, § 3). The approximately 17 states that have adopted either of the models remain totally unregulated or have sparse statutory treatment of the topic pending further action by their respective state houses (LISA 2008e). In these states, “anyone can hang a shingle” and market LIS products (Goldstein 2007, p. 47). Although both the NCOIL and the NAIC model acts have been recently updated to better address STOLI transactions, as of October 2008, 12 states have also enacted specific legislation to restrict this type of LIS exchange (Lysiak 2008).

These numbers are “best estimates” based on information obtained directly from the two drafting organizations. Imprecision is possible because states do not need to disclose whether their adopted legislation is based on one specific model act or on neither act or represents an amalgam of both.

As Table 1 summarizes, each of the two operative model acts deal with key LIS issues in a distinctive way. Our analysis of how the acts address these matters does not lead us to favor one, in total, over the other. Rather, each model act, relative to the other, contains elements that better protect the rights of consumers, as well as other elements that may heighten the probability that vulnerability will be experienced. Next, we examine how the two model acts address information disclosure, consumer privacy, and STOLI transactions.

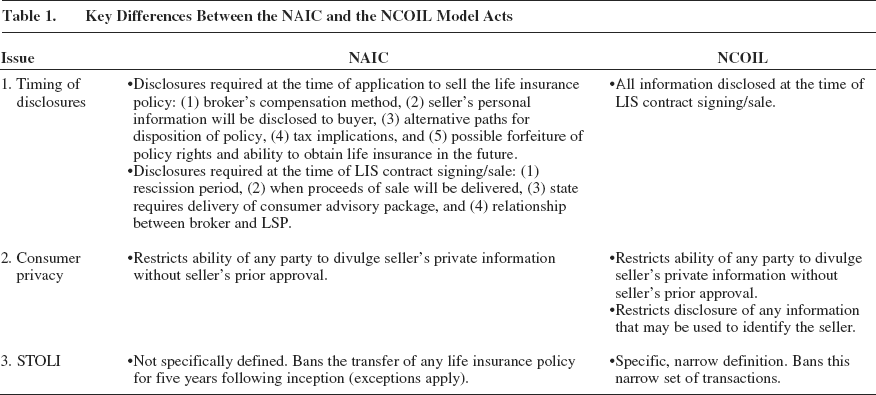

Key Differences Between the NAIC and the NCOIL Model Acts

Disclosure

Both model acts address disclosures to three distinct entities: (1) the consumer (i.e., the individual prepared to sell the life insurance policy), (2) the organization issuing the policy, and (3) the party prepared to acquire the policy or broker the exchange (NAIC 2007; NCOIL 2007). We focus on what the model acts require and do not require in terms of what must be disclosed to the consumer, as well as when required disclosures must be made.

Required content of disclosures

The two models closely parallel each other with respect to the content of what must be disclosed to consumers. The key disclosures fall into three categories: (1) potential disadvantageous outcomes experienced as a result of engaging in LIS exchange, (2) rights the seller retains, and (3) various transaction details.

With regard to the potential downside of LIS exchange, both model acts require that the consumer be informed (1) that alternatives to LIS exist; (2) of the various tax, creditor, and governmental assistance implications; (3) of the forfeiture of certain rights under the policy; (4) of the possibility of medical, personal, and financial information being furnished to the buyer (and subsequent/secondary market buyers) of the policy; (5) that the consumer may be contacted in the future to ascertain his or her current health status; and (6) of the possibility that the seller's ability to obtain additional life insurance in the future may be limited (NAIC 2007, § 8; NCOIL 2007, § 9).

With respect to rights retained by the seller, both model acts require disclosure (1) of the “cooling off” or rescission period, within which the customer may nullify the contract; (2) of when the proceeds of the sale will be delivered; (3) that the State Commissioner of Insurance requires delivery of a consumer advisory package; and (4) that LIS brokers owe consumers a legal obligation of loyalty and care.

Finally, both acts mandate that consumers be informed of the following transactional details: (1) the amount of the broker's compensation and the method employed to calculate the compensation, (2) the date on which settlement funds will be made available to the seller, and (3) the relationship, if any, between the LSP and the issuer of the life insurance policy (NAIC 2007, § 8; NCOIL 2007, § 9).

Timing of disclosures

While the two model acts are highly similar with respect to what must be disclosed to the consumer, they differ significantly on the timing of these disclosures (see Table 1). The NCOIL model act takes a straightforward approach, requiring all disclosures “no later than the date the [LIS] contract is signed by all parties” (NCOIL 2007, § 9A). Note that by the letter of the law, the disclosure could come after signing, as long as it occurs on the same date. The NAIC model act splits the disclosure items, with some disclosures required at the time of the submission of the application to sell the life insurance policy and others at the time of contract signing (NAIC 2007, §§ 8[A]–8[B]). Examples of items to be disclosed at the time of application submission include (1) the amount of the broker's compensation and its method of calculation; (2) the potential disclosure of the seller's identity and medical and financial information to the buyer (and subsequent buyers); (3) the existence of alternatives to the sale of the policy; (4) various tax, creditor, and governmental assistance implications; (5) the forfeiture of certain rights under the existing policy; and (6) the possibility that engaging in LIS exchange can limit the consumer's future ability to purchase life insurance (NAIC 2007, §§ 8[A]–8[B]; NCOIL 2007, § 9[A]).

Privacy

The two model acts use virtually identical language in addressing consumer privacy. Most notably, both restrict the ability of any entity involved in any aspect of a LIS transaction to divulge the life insurance policy seller's identity and financial or medical information without the seller's consent. In addition, the NCOIL model act restricts the disclosure of “information that there is a reasonable basis to believe could be used to identify the insured” (NAIC 2007, § 6[B]; NCOIL 2007, § 6[B]).

Stoli

As we discussed previously, STOLI refers to a distinct and highly controversial type of LIS transaction. Virtually all parties voicing interest in STOLI firmly oppose it. Even LISA, an advocacy group for the life settlement industry, states a definitive opposition to STOLI (LISA 2008e). However, there is little consensus as to what constitutes a STOLI transaction. Some define it broadly, holding that a STOLI exchange has occurred if a person initiates a policy on him- or herself and then simply contemplates selling it to another party at some point in the future (Bozanic 2008, p. 242). Others narrow the scope of STOLI with a focus on the issue of ownership rights. From this perspective, a STOLI transaction has transpired only if the insured has been denied (1) rights to the death benefit during the contestability period, (2) the right to retain the policy (should the insured choose to do so), and (3) the right to assign the policy back to the investor in satisfaction of debt accrued for premiums paid (Jensen and Leimberg 2007, p. 121).

When state legislators look to the NAIC and NCOIL model acts for regulatory guidance on STOLI, a key difference between the two models is the definition, and resultant treatment, of this form of LIS transaction. The NCOIL model act specifically defines STOLI, defines it relatively narrowly, and bans that fairly narrow set of transactions. The NAIC model act takes a more blunt-instrument approach and is even more restrictive. Rather than attempting to define STOLI, it bans the transfer of any life insurance policy for a full five years following inception (versus two years in the NCOIL model), with exceptions for major life changes, such as catastrophic illness (NAIC 2007, § 11; NCOIL 2007, § 2[Y]).

Summary

Current regulatory inconsistencies and inadequacies pertaining to information disclosure, consumer privacy, and STOLI transactions represent market failures that heighten the probability that marketers might take advantage of previously discussed inherent LIS consumer vulnerability. Our attention now turns to regulatory reform aimed at lessening the incidence and severity of LIS consumer vulnerability.

LIS Public Policy Issues and Recommendations for Regulatory Reform

It has been more than 20 years since the first LIS exchange. Yet strong concern lingers over the way LIS is regulated. As Table 2 indicates, arguably most problematic is that more than 15 U.S. states have yet to adopt either the NAIC or the NCOIL model act as the basis for LIS regulation. This lack of regulation, in the context of the sale of complex products targeted at consumers often inherently at high risk to experience vulnerability, significantly increases the probability that consumer abuse will occur. State legislators in unregulated states should enact legislation based on either the NCOIL or the NAIC model act or, most optimally, a combination of their most consumer-friendly elements.

Key LIS Public Policy Issues and Recommendations for Regulatory Reform

Beyond the urgent, basal need for regulation in unregulated states, information disclosure, consumer privacy, and STOLI merit the bulk of PPM scholar and policy maker concern. Public policy recommendations in each area follow.

Information Disclosure

Disclosure requirements in the two model acts are thorough. However, consumer protection is significantly compromised because of the required timing of disclosure in the ten states regulated on the basis of the NCOIL model. This model act does not require the disclosure of potentially critical, deal-breaking information until the time of contract signing. Many consumers might be inclined to follow through with the proposed sale without asking questions that, if asked earlier, would motivate them to terminate the exchange. This situation represents a significant market failure, leading to information asymmetry that is disadvantageous to consumers.

A prominent example of NCOIL disclosure not required until the date of contract signing involves broker compensation, which is often at least equal to the amount of money received by consumers in exchange for their life insurance policies. The NCOIL approach to this key issue seems more a fig leaf than an actual attempt at consumer fairness. A possible alternative would be an industrywide standard compensation approach, as is the norm for real estate brokers. Regardless of the specific approach taken, consumers should be clearly informed of the amount of broker compensation, as well as how it is calculated, well in advance of contract signing.

Other problematic NCOIL late disclosures include both broker–buyer affiliations in the secondary market for life insurance and estimates of policy market value. Although the NCOIL model requires the broker to disclose all offers, counteroffers, acceptances, and rejections of proposed sales to third parties, disclosure is not required until the signing date. This problem is compounded because, here, the free market may not be counted on to adequately protect the consumer and deliver a fair price. Consider a scenario in which the consumer allows several brokers the opportunity to sell the policy. Prospective buyers may now bid on the identical policy from multiple brokers. In this scenario, competing brokers have an incentive to lower their asking price to win. Copying the seller on all price-setting correspondence as the broker–potential buyer negotiation process transpires would do much to help level the informational playing field. Under NCOIL rules, therefore, consumers must negotiate a deal with no objective estimate of the value of their policy, plus no idea of how much the broker is taking off the top. This information vacuum should be reduced or eliminated because it both raises the probability that consumer vulnerability will be experienced and places brokers and LSPs at a significant informational advantage. Requiring this information to be disclosed as soon as it is available, coupled with a mandatory waiting period of 30 days between the dates of application and contract signing (during which the consumer has the absolute right to void the proposed sale), should lead to more informed, intelligent consumer decisions. Consumer knowledge could be further enhanced by also requiring brokers to obtain, document, and disclose a minimum of at least three bids for each policy before the date of contract signing. These bids should come from firms that have no association with the broker.

Finally, although timing is the main area of current disclosure inadequacy, we suggest that an additional disclosure be made to consumers—one not involving brokers or other LIS marketers. We recommend that life insurance firms and sales agents be required to clearly disclose to all prospective policy buyers that LIS exists as a legal disposal alternative, along with letting the policy lapse or surrendering it to the insurer. This disclosure should include realistic examples of the financial consequences of engaging in each of the three disposal options. Furthermore, with respect to timing, we suggest that this disclosure be made as soon as practically possible after interest in policy acquisition is demonstrated and that it must be made before the signing of the contract to purchase life insurance.

As of early May 2009, only two states—Maine and Washington—required any disclosure of life insurance policy disposal options. In both states, the superintendent of insurance is required to “develop a brochure, which can mention settlements as an alternative” (Life Settlement Report 2009, ¶ 4). Insurance firms then distribute the brochures to (1) “seniors who are considering lapsing or surrendering their policies or seeking accelerated death benefits” and (2) “people who are 60 or older or who are terminally or chronically ill” (Life Settlement Report 2009, ¶ 5). Our suggested disclosure approach would complement and expand existing disclosure practices in an effort to ensure that the people most interested in purchasing life insurance are better aware of all policy disposal alternatives early in the consumer decision-making process.

Insurers may oppose this recommended disclosure on grounds that it forces them to take actions detrimental to themselves (e.g., by decreasing policy lapse rates and increasing total death benefit payouts). However, this disclosure can potentially be beneficial to insurers in that consumer knowledge of the presence of LIS as a means of disposal could “save sales” that might otherwise be lost because of a lack of acceptable disposal options—particularly with prospects concerned that they may not be able to afford policy premiums. Making this disclosure can also be considered a way for life insurers to help better position their products as “safe and sound investments” to consumers.

Consumer Privacy

The key privacy principle operating in both model acts requires that no substantive information may be released to third parties to the initial sale of the life insurance policy without consent of both the insured and the policy owner; they need not necessarily be one in the same, but they usually are. Although this may sound like a strong statement of consumer protection, in practice it simply means that unless a person provides consent, he or she is effectively precluded from selling a policy.

Rather than requiring identity disclosure, regulations should bar disclosure of consumer identity information to anyone other than reputable, licensed brokers, who in turn may be suspended from practice for not properly safeguarding this information. This should eliminate the safety concerns of those opposed not only to STOLI but also to the sale of life insurance policies in secondary markets in general. However, this approach comes with problems of its own. It would not be a simple matter of enacting a one-time sale from the policyholder to an LSP by using only objective data free of identity information. Rather, should the LIS marketer want to resell the policy, the consumer must be recontacted for a health information update to make an accurate, current value assessment. There should be some mechanism in place for making a postsale contact and confirmation while still guaranteeing consumer privacy.

Furthermore, greater protection of consumer identity information should help lessen perceived physical risk that goes along with LIS “gambling on death.” Many questions are raised, both moral and practical, by person A receiving a reward for the death of person B. These questions are at least significantly muted if the party in possession of the life insurance policy does not know the identity of the insured person and cannot easily determine it.

Stoli Transactions

Stranger-owned life insurance remains the most controversial aspect of the LIS industry. The first matter of concern should be the aforementioned definitional debate. Currently, consensus on what constitutes a STOLI transaction does not exist. The probability of meaningful regulatory reform significantly increases when there is formal agreement about the exact nature of the focal phenomenon.

Parties to both sides of the ongoing definitional debate appear to place inadequate emphasis on a consumer's right to determine appropriate product usage. From the consumer's perspective, there is nothing inherently wrong with STOLI as long as the exchange was entered into with adequate and timely disclosure of key information and predatory or other unethical sales practices were not employed. The NAIC model act bans the sale of any life insurance policy for a full five years following inception, with no further attempt to define STOLI. This blanket ban unnecessarily limits consumer choice and value. The NCOIL approach of more specifically defining what constitutes a STOLI transaction preserves consumer rights and freedom while still prohibiting the small number of truly egregious transactions.

When the STOLI definitional debate is sufficiently resolved, attention should turn to specific legal and moral issues. Meaningful consideration of these issues from a consumer-oriented PPM perspective requires additional background on STOLI and opposition to it. Toward this end, we briefly discuss two exemplary STOLI cases. We then both examine common criticisms of STOLI and assess their validity. Finally, based on consideration of the background information provided, we offer general suggestions for regulatory reform.

Exemplary STOLI Cases

An exemplary STOLI transaction is described in the case of Life Product Clearing v. Angel (2008). This case involves an LIS exchange transacted in November 2005, in which Joel Miller, an insurance agent, made Leon Lobel, a 77-year-old retired butcher, “aware of a financial opportunity whereby (Lobel) could receive an immediate, substantial cash payment by taking out a life insurance policy on himself for the benefit of an investor who was a stranger to him” (Life Product Clearing v. Angel 2008, p. 648). Before being made aware of this opportunity, Lobel “had no personal desire to obtain a life insurance policy … and … could not afford one even if he so desired” (Life Product Clearing v. Angel 2008, p. 649). After being made aware of this opportunity, Lobel applied for a US$10 million life insurance policy on himself. Lobel's signature on the application was witnessed by Joel Miller, the very agent who sold the policy. The application for the purchase of the policy included the question, “Does the client intend to use the policy for any type of viatical settlement, senior settlement, life settlement or for any other secondary market?” This question was left unanswered. Despite this conspicuous omission, the policy was issued within a month (Life Product Clearing v. Angel 2008, pp. 648–50).

Lobel sold the policy to Life Product Clearing, an LSP, for $300,000. Joel Miller acted as the broker for this exchange. Lobel never made a payment; indeed, court documents indicate that he would not have been able to pay even the first year's premium of $570,000. All payments were made by Life Product Clearing in anticipation of receiving the policy's $10 million total death benefit when Lobel died. Life Product Clearing did not have to wait long. Lobel died just six days after receiving the $300,000 (Life Product Clearing v. Angel 2008, pp. 650–51).

This case, involving a STOLI transaction brokered by the very person who both made the consumer aware of the opportunity to engage in the exchange and then sold him the life insurance policy, exemplifies the macabre, “gambling on death” nature of STOLI that is commonly at the heart of its harshest criticism. Typically viewed as problematic here is (1) the aggressive—some may say “predatory”—manner in which the transaction is initiated by the investor, (2) the life insurance policy being purchased with the sole intent of selling it to an investor (which runs counter to the basic purpose of life insurance), (3) the notion that the eventual owner of the policy has a vested interest in the expedient death of the insured party, and (4) the large and sometimes rapid profits realized by LIS marketers and investors (Huslin 2007; Kiplinger's Personal Finance 2008).

Another STOLI case often referenced by critics involves talk-show host Larry King (see Huslin 2007; Insure.com 2007; Kiplinger's Personal Finance 2008). According to allegations contained in an October 2007 breach of fiduciary duty lawsuit filed by King against LIS broker The Metzler Group, King was approached by the broker and persuaded both to purchase one $10 million life insurance policy (to be ceded to Metzler) and to sell an existing $5 million policy to Metzler. The transactions took place in 2004 and yielded King a total settlement amount of $1.4 million, or 9.33% of the total death benefits of the two policies. King, 73 years old with a long history of serious health problems at the time, alleges in his lawsuit that he was not informed that the commissions received by the broker would nearly equal King's compensation. The lawsuit also contends that (1) Metzler did not disclose to King that engaging in the transaction could make it difficult for him to acquire additional life insurance coverage in the future; (2) Metzler did not adequately solicit bids from prospective policy buyers that, if done, could have significantly increased King's compensation; and (3) the eventual owner of one of the policies was a company of questionable repute that was, at the time of the lawsuit's filing, under investigation for unethical and illegal conduct.

Most STOLI transactions are somewhat more nuanced and less egregious than the case of Leon Lobel and involve smaller sums of money than the cases of both Lobel and Larry King. However, as we discuss subsequently, many of the same ethically or legally questionable marketing practices alleged in these two cases are at the heart of common opposition to STOLI exchange.

Opposition to STOLI

The strongest opposition to STOLI comes from the life insurance industry. Life insurers’ foremost criticism is the alleged violation of the “insurable interest” laws active in all 50 states (Bozanic 2008, pp. 249–50). Under these laws, the person initiating a life insurance policy must have an insurable interest in the life of the insured (e.g., a blood or marriage relation, or such a substantial business relationship that the person has an interest in the continued health of the insured). The purpose of these laws is to eliminate “wager” policies (i.e., policies that have no purpose other than to bet on the life expectancy of another person). Justice Oliver Wendell Holmes explains the Court's distain for such policies:

A contract of insurance upon a life in which the [policy owner] has no interest is a pure wager that gives the [policy owner] a sinister counter interest in having the life come to an end. And although that counter interest always exists, … the chance that in some cases it may prove a sufficient motive for crime is greatly enhanced if the whole world of the unscrupulous are free to bet on what life they choose. (Grigsby v. Russell 1911, pp. 154–55)

Lack of insurable interest has been the central allegation in a recent surge of lawsuits filed by life insurance companies against STOLI practitioners (Lysiak 2008). Life insurers assert that policies enacted through STOLI exchange should be voided because there is no insurable interest at the time the policy was issued (i.e., that the “stranger” in STOLI clearly has no insurable interest in the insured's life). Therefore, life insurers further argue that insurers should recover commissions paid to STOLI brokers (Lysiak 2008). The primary obstacle for life insurance firms has been proving the seldom formally stated intent of the insured to sell the policy at the moment of its acquisition, intent that must be proved to demonstrate a lack of insurable interest.

Another legal criticism often levied against STOLI by life insurers is that turning life insurance into a wager or investment vehicle is not among its legitimate uses (e.g., to allow estate planning, to protect families against the potential catastrophe of the death of the primary earner, to allow a business to continue after the death of a principle [Consumer Reports 1998a; Vaughan 1982]). Because of the clear social benefits, the U.S. Congress has afforded special, favorable tax treatment to life insurance benefits. This favorable tax treatment does not extend to investors purchasing policies from third parties (Gardner, Welch, and Colvert 2009).

In addition to objections to STOLI on legal grounds, many moral concerns exist. Some opponents hold that the inherent vested interest in the expedient demise of the insured may motivate investors to murder the insured parties or have them killed by a third party. Others hold that STOLI epitomizes the notion that it is patently immoral and offensive for one person to profit from the death of another in a speculative way, effectively reducing human life to the level of an economic commodity (Jensen and Leimberg 2007, p. 119). This concern is not without precedent. For example, the British Gambling Act of 1774 (12 Geo. III, c. 48, 1 [Eng.]) was enacted in response to the then-common practice of wagering on the life expectancies of people accused of capital crimes (Bozanic 2008, p. 248).

Several recent STOLI cases have been cited as justification for moral “gambling on death” concerns. One such case involves Michael Lee Davis, the accused ringleader behind a $10 million scheme in which he allegedly recruited HIV-positive people to purchase life insurance policies and then had a corrupt insurance agent help these terminally ill people falsify policy applications (Lankford 2000). Perhaps most worrisome here is that Davis was on parole from a murder-for-hire-plot conviction when he first got into the LIS business in 1996 (Lankford 2000). Another case involves two brokers accused of fraudulently misrepresenting the profit potential of their proposed deal to investors, such that the brokers allegedly (1) planned to take out life insurance policies on the entire congregation of an African American church in South Central Los Angeles and (2) promised potential investors 25% annual returns on the basis of African Americans having shorter life expectancies than other racial groups (Goldstein 2007). Particularly troublesome here is the mere possibility that investors might be motivated to expedite their return on investment by, for example, setting fire to the focal church during services.

Are the Opposition Arguments Valid?

Critics of STOLI more often than not present a one-sided argument, largely ignoring benefits to the consumer. It is difficult to deny, even in a case such as that of Leon Lobel, who died just six days after receiving his $300,000 settlement, that the consumer did not benefit significantly as a result of engaging in STOLI exchange.

From a legal perspective, at the heart of STOLI criticism is the alleged creation of “wager” life insurance policies. The prohibition against wager policies is rooted in the previously alluded to British Gambling Act of 1774. Before passage of the act, British citizens were free to place a bet on the life of a complete stranger, sometimes a member of the Royal Family (The Economist 2003; Jenkins 2006; Nevill 1909). The original reason for prohibition of this practice might have had more to do with the large number of British monarchs whose reign ended by assassination than with any thinking about how insurance should operate in a more general sense (Richardson 2001, pp. 267–69). Although insurance firm advocates are fond of quoting Justice Oliver Wendell Holmes on the alleged dangers of STOLI, they regularly omit his further explanation regarding why, when a person sells a policy of his or her own creation, the wager policy dangers no longer exist. Holmes goes on to state the consumer advantages of allowing such sales: He would

allow the holder of a valid insurance upon his own life to transfer it to one whom he, the party most concerned, is not afraid to trust. The law has no universal cynic fear of the temptation opened by a pecuniary benefit accruing upon a death. … So far as reasonable safety permits, it is desirable to give to life policies the ordinary characteristics of property. … To deny the right to sell except to persons having [an insurable] interest is to diminish appreciably the value of the contract in the owner's hands. (Grigsbsy v. Russell 1911, pp. 155–56)

Holmes makes clear that as long as the insured is comfortable with the transaction, he would allow it to go forward, thus creating value for policyholders. The danger lies when someone can take out a policy without the insured's knowledge or consent, creating a straight wager on a life. Typically, STOLI does not involve such an arrangement. Although a “stranger” is involved in the initiation of the exchange, the insured must also be involved every step of the way leading up to and including the sale of the policy.

In addition, while some critics hold that STOLI involves an illegitimate use of the life insurance product, others find the very concept of “legitimate uses” for life insurance—or for any product—to be distinctly condescending to the consumer. In certain cases, using a product in ways not anticipated by the producer may limit the producer's liability. However, dictating to a customer how he or she may or may not use a product does not seem to comport with the free enterprise approach. Consumers, it may be said, determine the best use for a product, not the marketer.

Finally, contrary to commonly voiced concerns, there are no documented cases of STOLI-motivated murder. As exemplified in the case of Leon Lobel, it is likely that the practical extent to which the vested interest of investors will go involves locating people with short life expectancies and then persuading them to engage in the exchange. Thus, although we by no means condone marketing practices such as those involved in the Lobel case, moral criticisms of STOLI on the basis of it being “likely to incite murder” appear to be exaggerated.

More broadly, each individual is free to come to his or her own conclusion regarding the moral righteousness of STOLI. Furthermore, moral assessments of marketing practices take place within the cultural contexts in which they transpire (Thompson 1995). In the United States, both the privatization of death and the profiting from death, mainly by marketers of funerary goods and services, have long been widely accepted, despite a long history of consumer vulnerability and abuse (Gabel, Mansfield, and Westbrook 1996; Mitford 1963; Walter 2005). The U.S. society is also comfortable with defined-benefit pension plans, in which the employer gains if former employees have shorter-than-expected life spans. In addition, annuity contracts are permitted, in which the paying entity profits from the early deaths of consumers.

Perhaps most to the point, few investors in life insurance policies today buy and hold policies on a single life. Instead, they typically purchase fractional shares in a portfolio of policies representing hundreds of people. There is scant chance that an investor will be concerned with—let alone take actions to hasten—one particular person's demise. Given reasonable consumer privacy protections, the investor would have no pathway to discover who is in the pool of people in the investment portfolio (Blake and Harrison 2008, p. 19).

Note also that some question the apparently moralistic motives of STOLI's harshest critic: the life insurance industry. For example, consider that the portfolio value of a life insurer is influenced by many factors, including longevity of the client pool, improvements in health care, and the quality of the initial actuarial work. An additional factor is the percentage of life insurance policies that lapse as a result of the nonpayment of premiums, with the result being that the total death benefit is not paid out. By some estimates, approximately 90% of all life insurance policies lapse (Duhigg 2006). For insurers, the cost of a lapsed policy is essentially zero. Before the advent of LIS, surrendering the policy to the insurer was the insured's best option when premiums could no longer be paid. Because of the insurer's monopsony pricing advantage, such payouts are very low relative to true market value (Doherty and Singer 2003, pp. 450–51). The emergence of STOLI has helped reduce the life insurance industry's portfolio value by lowering the overall percentage of policies that lapse. Thus, insurance industry opposition to STOLI may be at least partially explained in terms of its adverse impact on insurance pricing and industry sales and profitability.

In summary, many criticisms of STOLI appear to be at least somewhat overstated. However, there remains much about STOLI to be concerned about, including inadequate and inconsistent regulatory treatment of this type of LIS transaction. Thus, there is great need for theoretical and practical contributions from both PPM scholars and public policy makers.

General Guidelines for Regulatory Reform

On a most basic level, straight wager policies are, and should remain, illegal. For example, allowing people to wager on the death of a president must be viewed as contrary to any sound vision of social policy. When such a bar is in place, a marketer's major concern becomes the fair treatment of, and full disclosure to, consumers, who are better protected by being afforded the opportunity to comprehend marketplace choices than by having these choices limited. Furthermore, no life insurance policy should be issued without the knowledge, consent, and active involvement of the insured. However, when a bona fide policy issues, people should be free to do with their property as they please, regardless of policy genesis.

This same freedom and enhancement of consumer value is compromised by NAIC's five-year waiting period. The NCOIL model is more customer friendly in that it specifically defines banned STOLI transactions. It is also the more logical approach because it focuses on the elimination of the relatively small number of bogus policies at their moment of origination rather than compromise property rights and market value for all policies and all consumers holding the vast number of legitimate policies.

Although specifying the exact nature of future STOLI regulatory reform is beyond the scope of this inquiry, the focus should be on enhancing consumer choice and value. Toward this end, reform based mainly on the NCOIL model act is necessary. However, as we previously alluded to, an important first step is agreement on a definition of what constitutes a STOLI transaction.

Recommendations for Further Research

Although the primary goal of this article is to stimulate discussion on LIS marketing practices and regulation among PPM scholars, we also hope to indirectly facilitate regulatory reform that both benefits consumers and levels the playing field for ethical marketers. With these objectives in mind, we suggest that further PPM research be focused on any of several topics we discussed (e.g., specific means of enhancing consumer protection in the areas of information disclosure and privacy; a more precise, standardized definition of STOLI; more in-depth analysis of the ethicality and legality of STOLI; the impact of LIS on the life insurance industry). More generally, in-depth empirical examination of actual LIS consumer experience is necessary. Methodologically, ethnographic and other qualitative analyses of lived consumer experience, similar to Hill and Kozup's (2007) examination of how consumers perceive and experience predatory lending, are most appropriate. Such inquiry may be instrumental in advancing knowledge of (1) why consumers consider LIS exchange, (2) the nature of the LIS consumer decision-making process, (3) levels and sources of LIS customer satisfaction and dissatisfaction, and (4) the prevalence and nature of unethical LIS marketing practices.

Finally, further research should not focus exclusively on finding regulation-based answers to LIS marketplace problems. Equally important is the development of possible market-based solutions. Inquiry should also not be confined to helping LIS marketers (i.e., brokers and LSPs) both better serve consumers and ethically profit from their efforts. Research should also be undertaken with a view toward understanding what life insurance companies can best do to creatively and ethically offset the apparent inevitability that their industry has been forever altered by the secondary market for their products manifest in LIS.