Abstract

A portfolio selection model with return as triangular intuitionistic fuzzy number is developed in this study to assess and select portfolios on China Stock Exchange. Although the portfolio selection has been widely investigated, and most studies have regarded return and risk as the main decisive criteria, there are many uncertainties in the financial market, such as social, political and human psychological factors, which makes it difficult for us to describe the risks in line with empirical evidence. To fill this gap, first, a literature review was conducted to clarify the current situation and shortcomings of portfolio selection. Second, the triangular intuitionistic fuzzy number was used to fuzzify the coefficients of the objective function and the constraints in the portfolio model. Third, the triangular intuitionistic fuzzy number model was transformed into a linear programming model by using the selected exact ranking function, and the model was solved by MATLAB. Finally, the historical monthly returns of 10 stocks in China’s Stock Exchange from December 2017 to November 2020, lasting 36 months, were selected to demonstrate the model. The results indicate that the portfolio selection model with triangular intuitionistic fuzzy number can better meet the uncertainty of the real securities market, and more reasonable investment decision guidance can be provided for investors. Besides, the limitations of this study are pointed out, and implications and directions for future research are discussed.

Introduction

Portfolio problem is a hot issue in the field of finance. How to allocate investment funds to maximize returns and minimize risks is a problem that scholars have been studying. Markowitz assuming that the return on securities is a random variable, the method of return on securities is used to measure the investment risk, the mean variance model is proposed for portfolio selection in [1]. The model is a double objective decision model with the goal of expected return (mean) and risk (variance) of portfolio. Due to the limitation of mean variance model in practical application, and the complexity of calculation, to overcome the difficulties of Markowitz model, many scholars have improved the model. For example, in [2], Mao established mean semi-variance portfolio model with semi-variance to measure risk, and he reduced the amount of calculation by using absolute deviation to describe risk index. The mean absolute deviation model was constructed by Konno in [3], and the mean semi- absolute deviation model was given by Speranza in [4].

In the securities market, the return and risk of securities are uncertain, and investors have subjective will to the investment risk and return, therefore, the return and risk of securities are fuzzy, all these require investors to make good investment decisions in an uncertain environment.

In 1965, Zadeh in [5] established the fuzzy set theory with membership function to describe the continuous transition of the membership degree of an element to a set, which provides a method for quantitative description and analysis of fuzzy phenomena. Atanassov in [6] defined intuitionistic fuzzy sets (IFS) by adding a new attribute parameter non membership function, which can describe the fuzzy nature of the objective world more finely. Since then, many scholars have studied the portfolio selection by using fuzzy set theory. Chen et al. in [7] considered the portfolio problem with fuzzy expected rate of return, they established a fuzzy linear programming model for portfolio selection by simplifying variance constraint with fuzzy constraint, and they designed a fuzzy algorithm to solve the model.

Chen et al. in [8] Established a fuzzy multi-objective portfolio selection model by fuzzing the three objectives of return, variance and bias in the multi-objective portfolio model, and they took membership function and non- membership function as new objective function, at last,they gave the solution method. By introducing credibility skewness and fuzzy liquidity constraints, Song et al. [9] established the mean-variance-skewness-sine-entropy portfolio optimization model and the mean-variance-skewness-sine-entropy portfolio optimization model with fuzzy liquidity constraints under both stochastic uncertainty and fuzzy uncertainty, and then used Markov method to solve the fuzzy return. On the basis of Zimmermann’s fuzzy linear programming problem, Arpita et al. in [10] and [11] proposed a method to solve the linear programming problem when both the constraint coefficient matrix and the cost coefficient are intuitionistic fuzzy. By defining a class of intuitionistic fuzzy inequalities, the membership function and non- membership function of them are given respectively, a model solving method based on total exact function is proposed under considering the risk preference of decision-makers, and this method is applied to the portfolio by Yu et al. in [12]. A Nagoorgani Ponnalagu in [13] defined the division operation of triangular intuitionistic fuzzy numbers, they used α,β-cut sets and scoring functions to sort triangular intuitionistic fuzzy numbers, and introduced an accurate function to solve triangular intuitionistic fuzzy numbers. Sun in [14] used non- membership degree and hesitation degree to describe the fuzziness of things, and used intuitionistic fuzzy number to express the return rate, value at risk and turnover rate of fuzzy portfolio. In order to reduce the investment risk, the optimal portfolio model with the goal of maximizing the return and minimizing the risk was established by constructing the investment proportion constraint with Yager’s law. Taking interval intuitionistic fuzzy preference relation as the main research content, Wang and Lu in [15] proposed the corresponding group decision-making method and applied it to practical decision-making problems.

Yang et al. first regarded the return rate of assets as a trapezoidal fuzzy number and proposed a fuzzy return rate fitting model to determine the parameters of the fuzzy return rate of assets based on the historical return rate of assets and expert opinions. Secondly, a measure of portfolio diversification is proposed. Finally, after taking the probability mean of portfolio return as its return measure and the lower half variance of portfolio return as its risk measure, they built a Multi- Criteria portfolio adjustment model of fuzzy Mean- Lower -Semi-Variance-Diversification in [16].

Song and Deng in [17] studied the distribution of stock yield meet the trapezoidal fuzzy number model portfolio. By replacing the probability mean and covariance in the portfolio model with the probability mean and covariance respectively, they established a dual objective model using the lower probability variance to describe the risk. Then, they used the linear weighting method to transform the dual objective model into a single objective model and designed a hybrid algorithm to solve it. Li and Yi in [18] proposed a new trapezoidal fuzzy number with adaptive index. They first give the mean, variance and skewness of the probability expectation under the new measure, and then a new trapezoidal fuzzy number was introduced into the fuzzy Mean-Variance model and Mean-Variance -Skewness model for optimal asset allocation. By introducing the loss aversion measure as the objective function and the absolute semi deviation from the expected value of return and below average as the risk measure, Ruiz et al. in [19] proposed a new credibility portfolio selection model.

Since Markowitz’s portfolio theory was put forward in 1965, different researchers have optimized and explored the fuzzy portfolio model from different angles and using different methods, and a lot of results were achieved. New measurement methods were adopted to improve the model based on the shortcomings of the original portfolio return and risk measurement methods. For example, the fuzzy probability mean was used to measure the rate of return, and the semi-variance and absolute deviation were used to replace the variance to measure the risk of portfolio; Or the constraints of traditional models were relaxed; Or the algorithm for solving the model was optimized. Considering the fuzziness of the stock market, the objective function was improved by using the concept of fuzzy satisfaction; or by defining the fuzzy possibility mean variance, the decision ariables of the model was improved; or the portfolio problem with fuzzy was solved directly u using the interval number. All these research results have laid a solid foundation for expanding the field of portfolio research.

Combining fuzzy theory with portfolio theory, this paper studies the portfolio model under fuzzy conditions. The main work of this paper is to establish a triangular intuitionistic fuzzy portfolio selection model by fuzzifying the objective function and constraint coefficient of the model, then the triangular intuitionistic fuzzy number model is transformed into clear number model by using the given exact ranking function, and the solution method is given. The structure of this paper is as follows, in the first section, we introduce some fuzzy portfolio models and their applications, in the second section, we establish a triangular intuitionistic fuzzy portfolio selection model, in the third section, we give the relevant knowledge of intuitionistic fuzzy number set, transform the model established in the second section into a clear number model, and give the solution,in the fourth section, as the application of the model, we gave an empirical study. Finally, we gave some conclusions.

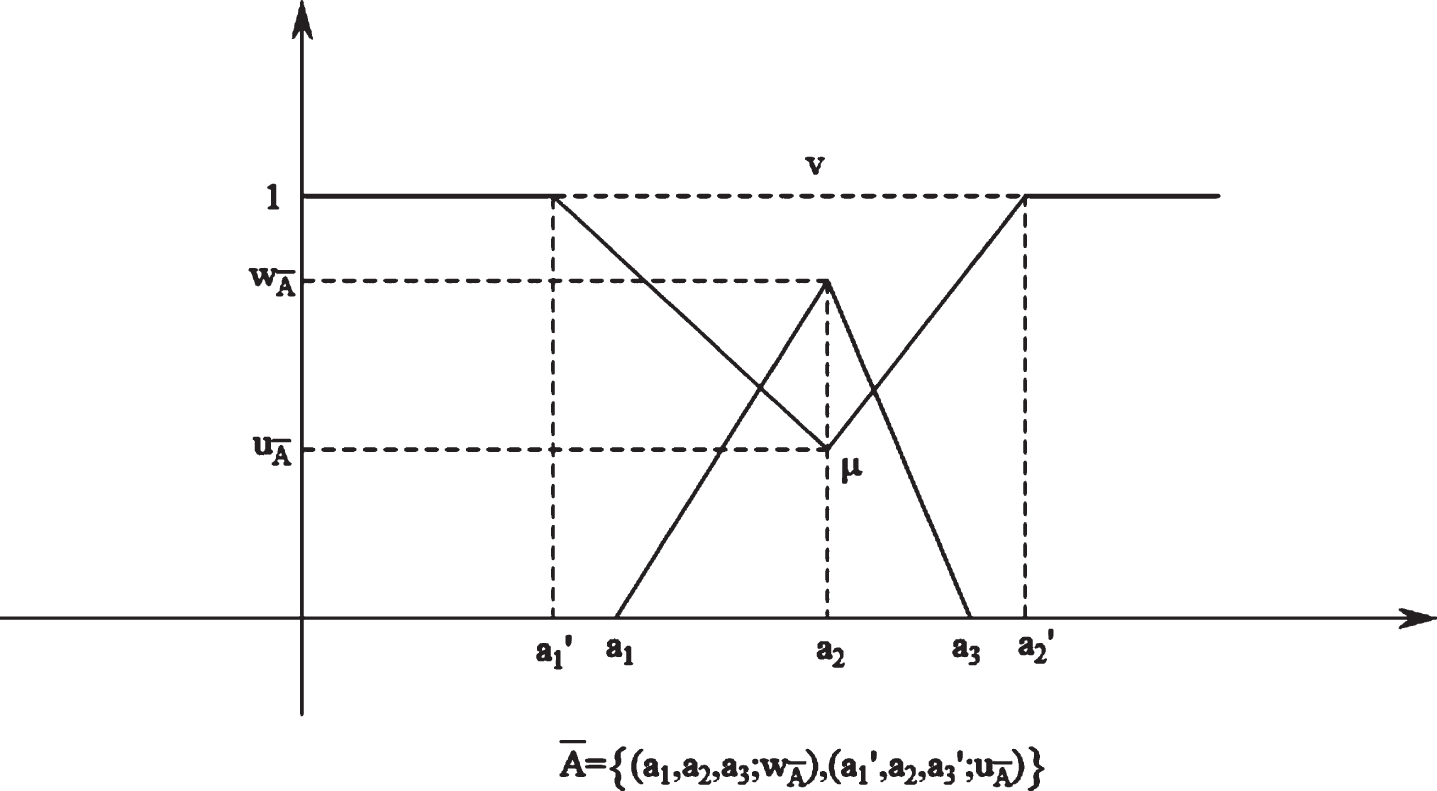

Definition and operation of intuitionistic fuzzy numbers

Here

Triangular intuitionistic fuzzy number

be two triangular intuitionistic fuzzy numbers, then the operation between

Here f (α) is a nonnegative increasing function defined on the interval [0,1], and satisfied:

For convenience, let’s assume f(α)=α, so we have the following Equation (4):

Therefore, the ranking relation of triangular intuitionistic fuzzy numbers

Model formulation

Assuming that in the investment period, short selling is not allowed, transaction costs are not considered, risk assumption is avoided, bank interest rate remains unchanged, and investors want to maximize the expected return and minimize their risk level.

Suppose that investors hold n kinds of enterprise assets S

i

(i = 1,2,...,n), R

i

represents the return rate of the i-th asset, x

i

represents the investment proportion of the i-th asset, x=(x1,x2,...,x

n

) represents the portfolio, r

i

= E(R

i

) represents the expected return rate of the i-th asset, q

i

= E|R

i

- E (R

i

) | represents the absolute deviation, and q represents the upper limit of the risk that the investor can undertake, ɛ

i

(i = 1, 2, . . . , n) is the upper limit of the investment proportion of the i-th asset, and we build the model of portfolio optimization as follows:

The feasible domain of the portfolio optimization problem (5) is:

The expected return of asset x is given by

In practical problems, due to various uncertainties, it is often difficult to determine the coefficients of objective functions and constraints. In this paper, we consider the solution of portfolio selection model with objective function and constraint coefficient given by triangular intuitionistic fuzzy numbers,

Where

By defining 2.3–2.5, the

Data collection

There are three important indexes in China’s stock market: Shanghai Composite Index (SCI), Shenzhen Component Index (SZSI) and Growth Enterprise Index (GEM). Among them, the SCI mainly reflects the average price of all the listed stocks on the Shanghai Stock Exchange, which includes most of China’s large blue chip stocks and is highly representative in China’s stock market. CZSI is a comprehensive reflection of the stock prices of A and B shares listed on Shenzhen Stock Exchange by taking the stocks of 40 market representative listed companies from all the stocks in Shenzhen Stock Exchange as the calculation objects. GEM, a comprehensive reflection of China’s second board stock market average price changes. The index reflects the listed companies with high growth, but they are often established for a short time, small in scale, and not outstanding in performance, but there is a lot of room for growth. SSE 50 Index, SSE 180 Indexand SSE 380 Indexare all scale indexes of SCI series, representing the price changes of 50, 180 and 380 companies with the largest market value respectively. SZSI 100 index, SZSI 200 index, SZSI 500 index, SZSI 700 index and SZSI 1000 index belong to the SZSI scale index series, which represent the average prices of the largest 100, 200, 200 to 700, 700 and 700 to 1700 listed companies in Shenzhen Stock Exchange respectively. The CSI 300 index comprehensively reflects the average prices of the 300 stocks with the largest market value in Shanghai Stock Exchange and Shenzhen Stock Exchange. It represents the prices of major stocks in China’s stock market.

Our datas come from Guo Tai-An database (https://www.gtarsc.com/). Here we give the index codes and names of 10 stocks needed in our numerical example (Table 1).

Index code (IdxCd) and index name (IdxNm)

Index code (IdxCd) and index name (IdxNm)

In order to illustrate the model and method proposed in the previous section, we give an example to verify it. We collected historical earnings data for the 10 stocks in Table 1 from December 29, 2017 to November 30, 2020,and their historical monthly average returns are calculated, as shown in Table 2, the absolute deviation of their historical monthly average returns is also calculated, as shown in Table 3.

Average monthly return of historical return

Average monthly return of historical return

Absolute deviation of historical monthly average return

Triangular intuitionistic fuzzy expected return

Triangular intuitionistic fuzzy absolute deviation of return distribution

Where

The above model is solved by

The core problem of portfolio theory is “how to maximize the return under the risk that one can bear” or “how to minimize the risk that one can bear under the certain return??. Therefore, portfolio selection is to meet the balance of investors’ risk and return by using reasonable methods to allocate various assets. Because there are social, political and human psychological factors in the financial market, the historical data can not accurately reflect the future return of risk assets. Our research motivation is to use fuzzy mathematics knowledge and portfolio theory to explore the construction and application of portfolio model which is closer to the real transaction.

The main innovations of this paper are as follows: Considering the fuzziness of the securities market, the triangular intuitionistic fuzzy number is used to defuzzify the coefficients of the objective function and constraints in the portfolio model, so as to make the model more in line with the uncertainty of the real securities market and provide more reasonable investment decision guidance for investors.

In this paper, a portfolio selection model with triangular intuitionistic fuzzy number and its solution are proposed. The advantages of this method are as follows, 1) The risk preference of decision-makers is considered, which fully reflects the cognitive level of decision-makers; 2) A model solving method based on an accurate function is given. The example results show that the method is effective.

However, there are still some limitations in our work, and the limitation lies in the uncertainty caused by the subjective will of investors, mainly in the following aspects: 1) How to better describe portfolio risk in a fuzzy environment; 2) It is difficult to obtain empirical fuzzy data because it is necessary to integrate historical data with experts’ opinions. So the future research lies in how to better quantify the fuzzy index, improve the model and verify the effectiveness of the model.

Footnotes

Acknowledgments

This research was supported by Research Fund of Mathematics Discipline of Hunan University of Humanities, Science and Technology. Thank them for their support. The authors are grateful to the editors and anonymous reviewers for their valuable comments and suggestions for the successful publication of this work.